taxes

Auto Added by WPeMatico

Auto Added by WPeMatico

Artificial intelligence has become a fundamental cornerstone of how a lot of business software works, providing a useful boost in reading, understanding and using the often-fragmented trove of data that organizations generate these days. In the latest development, an Israeli startup called Blue dot, which uses AI to help companies handle their tax accounting, is announcing $32 million in funding to continue its growth, specifically addressing the demand from companies for more user-friendly tools to help read and correctly itemize expenses for tax purposes.

“The tax sector is very complicated, and we are playing in a very large space, but it’s a huge revolution,” Blue dot’s CEO and co-founder Isaac Saft said in an interview. “Business and enterprise accounting is just not going to look the same in the future as it does today.”

The funding is being led by Ibex Investors in partnership with Lutetia Technology Partners, with past investors La Maison Partners, Viola and Target Global also contributing. Blue dot rebranded only last week from its original name, VATBox (part of the funding will be used to help Blue dot move deeper into the U.S. market, where the concept of VAT is not quite so ubiquitous: there is no national sales tax and states determine the rates themselves).

PitchBook notes that under its previous name, the startup last raised money in 2017, a $20 million Series B led by Viola at a $120 million post-money valuation.

While Blue dot is not disclosing valuation today, it’s likely to be significantly higher than this based on some of its engagements. In addition to customers like Amazon, tobacco giant BAT and Dell, it also has a partnership with one of the bigger names in expense accounting, SAP Concur, which uses Blue dot to power its expense data entry tool to automatically read charges and figure out how to itemize them so that employees or accountants don’t need to go through the pain of that themselves.

As Saft describes it, part of what is propelling his company’s business is the bigger trend of consumerization and the role that it has played in enterprise services: the working world has picked up a lot of technology tools, led by the smartphone, to help them organize their personal lives, and a lot of what they are being “served” through technology is increasingly personalized with lower barriers of entry, whether its on e-commerce sites, entertainment or social media. In the working world, people can often be frustrated as a result with how much work something like expenses can involve — a process that gets ever more complicated the more strict tax regimes become.

Blue dot’s approach is to essentially view the tax accounting process as something that can be improved with AI to make it easier for people to use — whether those people are workers itemizing their expenses, or accountants auditing them and running those through even bigger accounting processes. With a machine learning system that both takes into account a company’s own internal compliance and company policies, and the wider tax and regulatory framework, Blue dot helps “read” an expense and figure out how to notate it, how much tax should be accounted and where, and so on.

This is especially important as the process of entering and managing expenses gets pushed out to the people spending the money, rather than dedicated accountants handling that work on their behalf. An awareness of how modern offices are functioning today and evolving is one reason why investors were interested here.

“We believe Blue dot can change the way organizations worldwide manage accounting and its tax implications for their expenses,” Gal Gitter, a partner at Ibex, said in a statement. “There’s been a major market shift away from centralization of enterprise functions, including procurement. As that accelerates, more companies will be looking for ways to replace costly and complex manual processes with digital, automated solutions that use data and AI to essentially enable transactions to report themselves, which Blue dot delivers.”

Powered by WPeMatico

Founders, entrepreneurs, and tech executives in the know realize they may be able to avoid paying tax on all or part of the gain from the sale of stock in their companies — assuming they qualify.

If you’re a founder who’s interested in exploring this opportunity, put careful consideration put into the formation, operation and selling of your company.

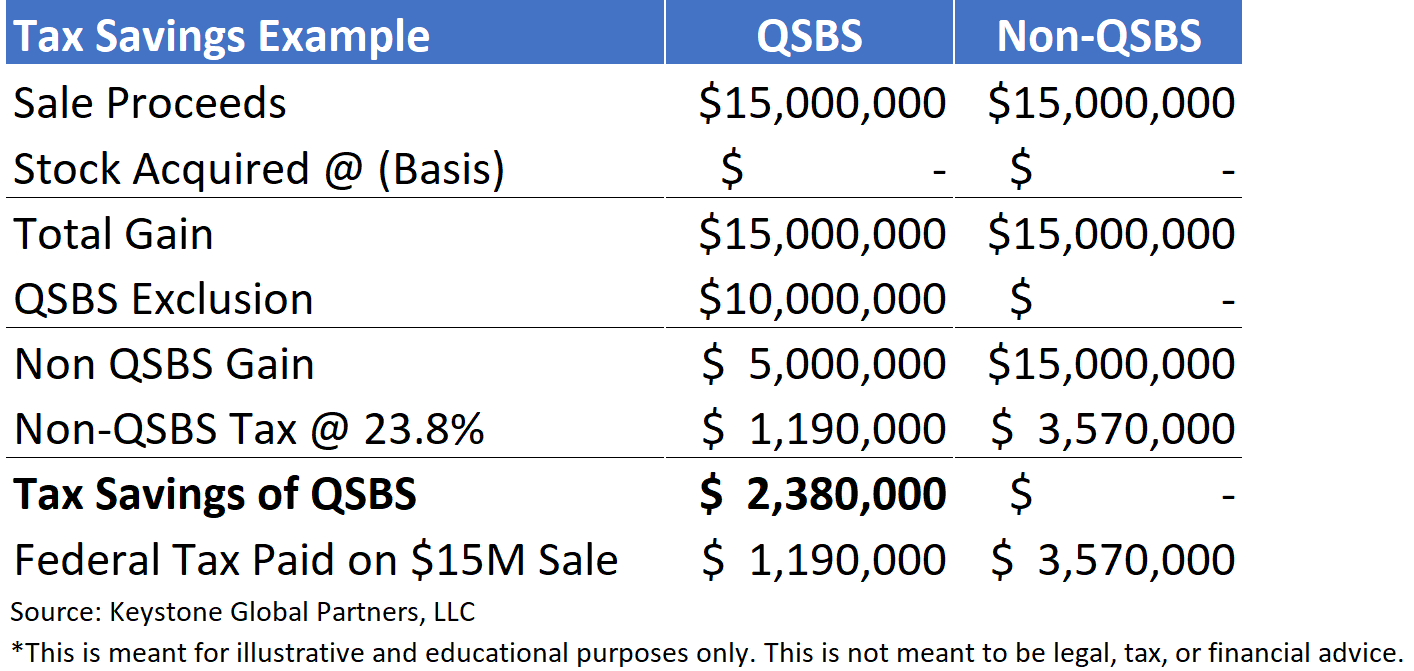

Qualified Small Business Stock (QSBS) presents a significant tax savings opportunity for people who create and invest in small businesses. It allows you to potentially exclude up to $10 million, or 10 times your tax basis, whichever is greater, from taxation. For example, if you invested $2 million in QSBS in 2012, and sell that stock after five years for $20 million (10x basis) you could pay zero federal capital gains tax on that gain.

These tax savings can be so significant, that it’s one of a handful of high-priority items we’ll first discuss, when working with a founder or tech executive client. Surprisingly, most people in general either:

Founders who are scaling their companies usually have a lot on their minds, and tax savings and personal finance usually falls to the bottom of the list. For example, I recently met with someone who will walk away from their upcoming liquidity event with between $30-40 million. He qualifies for QSBS, but until our conversation, he hadn’t even considered leveraging it.

Instead of paying long-term capital gains taxes, how does 0% sound? That’s right — you may be able to exclude up to 100% of your federal capital gains taxes from selling the stake in your company. If your company is a venture-backed tech startup (or was at one point), there’s a good chance you could qualify.

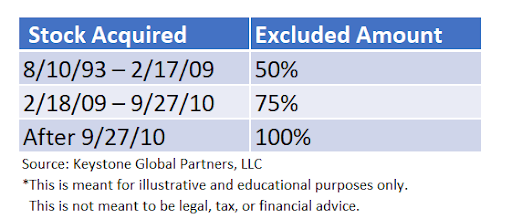

In this guide I speak specifically to QSBS on a federal tax level, however it’s important to note that many states such as New York follow the federal treatment of QSBS, while states such as California and Pennsylvania completely disallow the exclusion. There is a third group of states, including Massachusetts and New Jersey, that have their own modifications to the exclusion. Like everything else I speak about here, this should be reviewed with your legal and tax advisors.

My team and I recently spoke with a founder whose company was being acquired. She wanted to do some financial planning to understand how her personal balance sheet would look post-acquisition, which is a savvy move.

We worked with her corporate counsel and accountant to obtain a QSBS representation from the company and modeled out the founder’s effective tax rate. She owned equity in the form of company shares, which met the criteria for qualifying as Section 1202 stock (QSBS). When she acquired the shares in 2012, her cost basis was basically zero.

A few months after satisfying the five-year holding period, a public company acquired her business. Her company shares, first acquired for basically zero, were now worth $15 million. When she was able to sell her shares, the first $10 million of her capital gains were completely excluded from federal taxation — the remainder of her gain was taxed at long-term capital gains.

This founder saved millions of dollars in capital gains taxes after her liquidity event, and she’s not the exception! Most founders who run a venture-backed C Corporation tech company can qualify for QSBS if they acquire their stock early on. There are some exceptions.

A frequently asked question as we start to discuss QSBS with our clients is: how do I know if I qualify? In general, you need to meet the following requirements:

When in doubt, follow this flowchart to see if you qualify:

Powered by WPeMatico

India today addressed a long-standing challenge that has been affecting the country’s booming startup ecosystem. As part of a raft of measures to boost overall economic growth from a five-year low, Finance Minister Nirmala Sitharaman said New Delhi is exempting startups from Section 56(2) — a provision more popularly known as an “angel tax” in the local income tax laws — that required startups to pay a certain tax if they received an investment at a rate higher than their “fair market valuation.”

Local tax authority in India does not recognize the discounted cash flow method that many investors use to value early-stage startups, and instead value the company for what it is worth currently, which as you can imagine, is very little. Investors assess a startup’s value based on what it could eventually become in the future.

Prior to today’s announcement, the government levied a 30% tax on affected startups. Sitharaman said any startup that is registered with the Department of Industrial Policy & Promotion, a government body, will be exempted from the angel tax. Those not registered will remain subjected to it, she said in a press conference Friday.

More than 24,000 startups are currently registered with the Department of Industrial Policy & Promotion. The law was originally introduced amid concerns that wealthy people could invest in bogus startups as a way to launder money.

“Angel tax was there to stop shell companies from creating capital from nowhere,” Piyush Goyal, a minister for commerce and industry as well as railways, said in a statement Friday.

The angel tax, which was introduced in 2012, became a roadblock for many investors who wanted to fund early-stage startups. The announcement today comes weeks after the Narendra Modi government said it would address this issue.

Many prominent investors, startup founders, analysts and other industry executives have long publicly criticized the angel tax, telling the government that it is severely hurting the health of the local ecosystem.

Anand Mahindra, chairman of Mahindra Group, said last year that the angel tax needs “immediate attention or else all chances of building a rival to Silicon Valley in India will be lost.”

Sreejith Moolayil, a founder of health food startup True Elements, said the existence of an angel tax would leave many entrepreneurs like him with no choice but to shut down their companies.

Late last year, India’s tax department sent a flurry of notices to startups demanding them to pay the angel tax on funds they received from individual investors. The notices sparked an uproar, with many calling it “harassment.”

“Hope this will address the concerns of DPIIT registered startups. The proposed cell should look into concerns of all startups including those who are already under notice,” said Ashish Aggarwal, who oversees Public Policy at industry body Nasscom, of today’s announcement.

The government will also set up a dedicated cell to address other tax problems that startups face, Sitharaman said. “A startup having any income-tax issue can approach the cell for quick resolution,” the ministry said in a statement.

Jayanth Kolla, founder and chief analyst at research firm Convergence Catalyst, told TechCrunch earlier that the angel tax was the primary reason early-stage startups in the nation were struggling to raise money from investors.

Even as Indian tech startups raised a record $10.5 billion in 2018, early-stage startups saw a decline in the number of deals they participated in and the amount of capital they received. Early-stage startups participated in 304 deals in 2018 and raised $916 million in funds last year, down from $988 million they raised from 380 rounds in 2017 and $1.096 billion they raised from 430 deals the year before, research firm Venture Intelligence told TechCrunch.

I’ve said before, a willingness to relook at policies is a display of strength, not https://t.co/8y4tPp8Iva’s press conference by @nsitharaman will, I hope, mark the start of a new, interactive & interdependent relationship between Govt&business. @narendramodi @AmitShah (1/4)

— anand mahindra (@anandmahindra) August 23, 2019

Sitharaman also announced the country was scrapping a recently introduced additional levy on foreign funds. The government would revoke the surcharge, which increased tax on foreign companies investing in India to over 40%, she said. She also promised to pay out all pending tax refunds owed to small and medium enterprises within 30 days. Companies have long complained that the tax authority takes too much time to refund the money owed to them.

Powered by WPeMatico

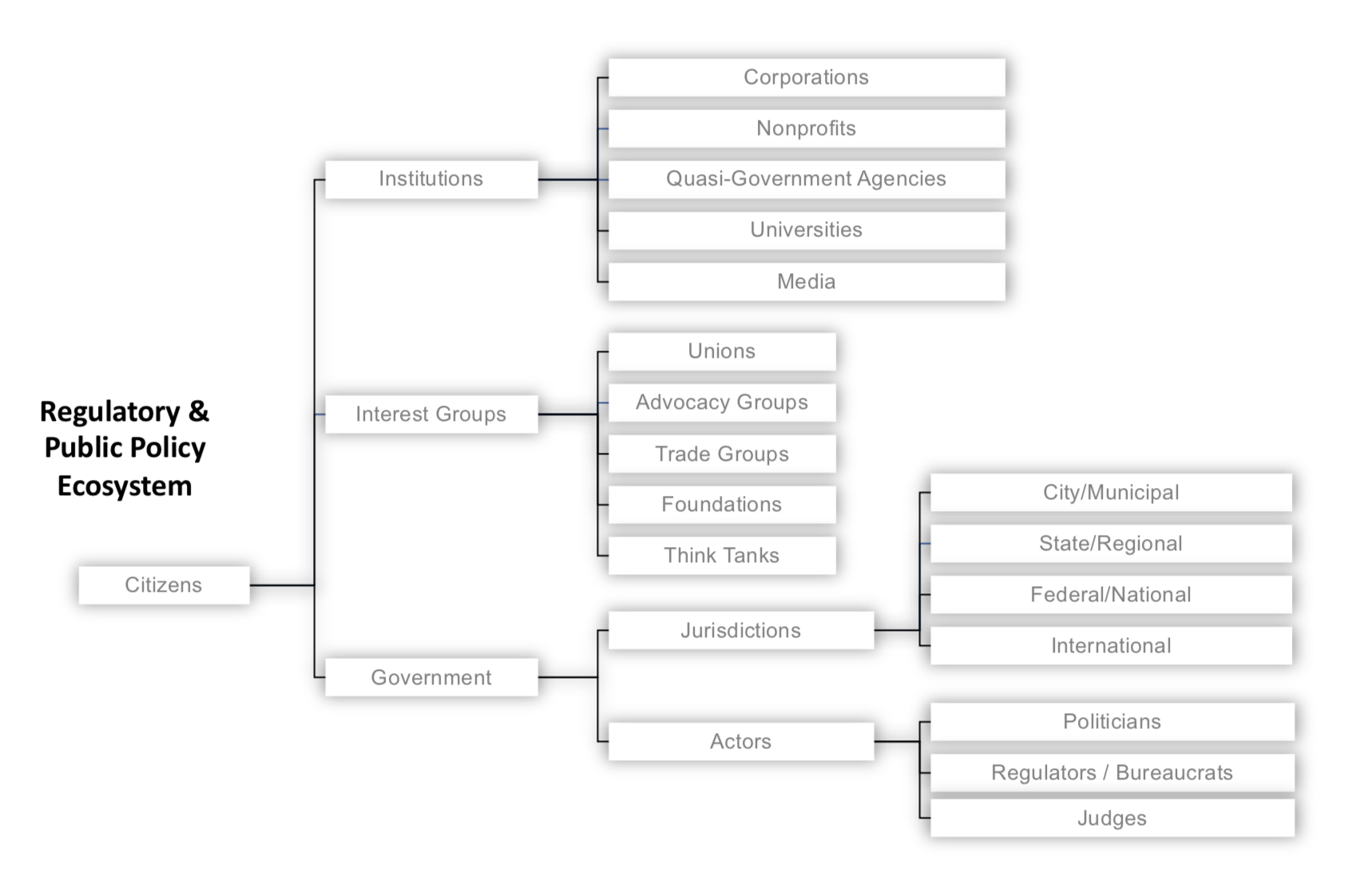

Startups are but one species in a complex regulatory and public policy ecosystem. This ecosystem is larger and more powerfully dynamic than many founders appreciate, with distinct yet overlapping laws at the federal, state and local/city levels, all set against a vast array of public and private interests. Where startup founders see opportunity for disruption in regulated markets, lawyers counsel prudence: regulations exist to promote certain strongly-held public policy objectives which (unlike your startup’s business model) carry the force of law.

Snapshot of the regulatory and public policy ecosystem. Image via Law Office of Daniel McKenzie

Although the canonical “ask forgiveness and not permission” approach taken by Airbnb and Uber circa 2009 might lead founders to conclude it is strategically acceptable to “move fast and break things” (including the law), don’t lose sight of the resulting lawsuits and enforcement actions. If you look closely at Airbnb and Uber today, each have devoted immense resources to building regulatory and policy teams, lobbying, public relations, defending lawsuits, while increasingly looking to work within the law rather than outside it – not to mention, in the case of Uber, a change in leadership as well.

Indeed, more recently, examples of founders and startups running into serious regulatory issues are commonplace: whether in healthcare, where CEO/Co-founder Conrad Parker was forced to resign from Zenefits and later fined approximately $500K; in the securities registration arena, where cryptocurrency startups Airfox and Paragon have each been fined $250K and further could be required to return to investors the millions raised through their respective ICOs; in the social media and privacy realm, where TikTok was recently fined $5.7 million for violating COPPA, or in the antitrust context, where tech giant Google is facing billions in fines from the EU.

Suffice it to say, regulation is not a low-stakes table game. In 2017 alone, according to Duff and Phelps, US financial regulators levied $24.4 billion in penalties against companies and another $621.3 million against individuals. Particularly in today’s highly competitive business landscape, even if your startup can financially absorb the fines for non-compliance, the additional stress and distraction for your team may still inflict serious injury, if not an outright death-blow.

The best way to avoid regulatory setbacks is to first understand relevant regulations and work to develop compliant policies and business practices from the beginning. This article represents a step in that direction, the fifth and final installment in Extra Crunch’s exclusive “Startup Law A to Z” series, following previous articles on corporate matters, intellectual property (IP), customer contracts and employment law.

Given the breadth of activities subject to regulation, however, and the many corresponding regulations across federal, state, and municipal levels, no analysis of any particular regulatory framework would be sufficiently complete here. Instead, the purpose of this article is to provide founders a 30,000-foot view across several dozen applicable laws in key regulatory areas, providing a “lay of the land” such that with some additional navigation and guidance, an optimal course may be charted.

The regulatory areas highlighted here include: (a) Taxes; (b) Securities; (c) Employment; (d) Privacy; (e) Antitrust; (f) Advertising, Commerce and Telecommunications; (g) Intellectual Property; (h) Financial Services and Insurance; and finally (i) Transportation, Health and Safety.

Of course, some regulations may touch on multiple regulatory areas, for example, the “Fair Credit Reporting Act” is a law ultimately about privacy, but it impacts many financial and employment-related services as well. Certain laws may therefore be cross-listed in more than one regulatory area. Also, since we can’t look at every U.S. state and city, this article will focus primarily on the federal and California state laws.

After you focus on the particular regulatory areas that may implicate your business, next reference the short quotations and links to relevant primary and secondary sources below, then work to identify the specific compliance risks you face. This is where other Extra Crunch resources can help. For example, the Verified Experts of Extra Crunch include some of the most experienced and skilled startup lawyers in practice today. Use these profiles to identify attorneys who are focused on serving companies at your particular stage and then seek out any further guidance you need to address the regulatory matters pertinent to your startup.

With that as context, the Startup Law A to Z – Regulatory Compliance checklist is below:

Before diving into further detail, it may be helpful for some readers to note the distinction between a law and a regulation. Simply put, regulations provide more detailed direction on how certain laws should be followed. So regulations are not technically laws, but they carry the force of law (including penalties for violation), since they are adopted by governmental agencies under authority granted by statute. Beyond that, understanding how laws and regulations are actually enacted is helpful to illustrate the extent to which the process is politically driven.

In the U.S., a bill must first pass both legislative branches of government, then, if signed by the executive branch, it will be codified in statute as law (Schoolhouse Rock anyone?). Once codified, the legislative branch will authorize the relevant executive department or agency to determine whether specific regulations are necessary to give the law effect. If so, those executive departments or agencies will determine what further rules are needed, and in turn, work to enforce them.

At the federal level, for example, proposed regulations are developed first through a “Notice of Proposed Rulemaking,” listed in the Federal Register and filed in the corresponding executive agency’s official docket (available at Regulations.gov). This affords the public an opportunity to comment on the regulations. After receiving comments, the filing agency may revise the proposed regulation before final rules are issued, which again will be published in the Federal Register and then filed in the agency’s official docket at Regulations.gov, before they are codified in the Code of Federal Regulations (CFR).

At nearly every step in this process then, institutions, government, and interest groups are working – sometimes at cross purposes – to shape what the law will be and how it will impact your startup.

The Startup Law A to Z – Regulatory Compliance reference guide is below:

Powered by WPeMatico

Late last week, Congress moved one step closer to passing the American Innovation Act of 2018, a bill that would make accounting and tax changes that would likely increase the valuation of startups in an acquisition.

The House Ways and Means committee approved a bill containing text that would improve the treatment of Net Operating Losses (NOLs) for startups. While many startup founders would probably rather watch paint dry (or build their companies) than dive into complex tax code changes, the provisions in the bill could greatly improve the ability of startups to invest in growth activity, and could drive meaningfully positive impacts to valuations, acquisition prices, capital markets participation and venture returns.

First, though, what are NOLs? Each year, if a company loses money, it can claim the losses as a deduction off of its future taxes. Traditionally, the U.S. tax code has allowed companies to cumulatively track and carry forward NOLs to offset taxable income in future years, reducing the amount of cash required to pay taxes. These NOLs are essentially a cash-like asset, and they can be exchanged in the event that a company is acquired.

However, a long-standing IRS provision, Section 382, which was originally implemented to prevent companies with large tax appetites from acquiring those with large operating losses exclusively to reduce taxes, limits the use of NOL carry-forwards in instances of ownership change.

Currently, in cases of an ownership change, specified as a more than 50 percent change in the ownership of shareholders who own at least 5 percent of a company’s stock, the amount of taxable income for the “post-change” company that can be offset by existing NOLs cannot exceed the value of the “pre-change” company, multiplied by the long-term tax exempt rate set by the IRS.

(Yes, this is why you hire a tax attorney.)

The net-net is that this provision has been particularly challenging for startups, which often trigger this limiting condition, given they frequently operate in the red through growth stages and often see frequent, sizable changes in their ownership structure due to fundraising, public offerings and acquisitions.

The House bill would alleviate this complication by protecting these tax offsets and creating an exception to the section 382 provision for startups, allowing the application of NOLs and R&D tax credits realized in the first three years of operations regardless of ownership change limitations.

These changes have a number of benefits for startups. It would provide increased flexibility around early-stage financing activities and remove potential issues that could arise with capital markets activity. Additionally, with startups more easily maintaining tax offsets to reduce their cash taxes, startups would have larger cash balances to invest in growth efforts.

The protection of the NOL from ownership change limitations could also have serious impacts to company valuations and the attractiveness of startups as acquisition candidates. With acquirers better able to utilize existing tax offsets, startups should benefit from higher purchase prices from the inclusion of NOL balances in valuations, helping founder and VC returns.

The bill passed through committee through a voice vote with no objections and is now expected to be voted on by the rest of the House later this month before advancing to the Senate. The bill has 23 co-sponsors, all Republican.

Powered by WPeMatico

Facebook today said it is shifting to a “local selling structure” in countries outside the U.S. That means that rather than directly route its revenue to its international headquarters in Dublin, local policymakers and governments will potentially get an opportunity for greater visibility into the company’s revenue related to local advertising sales. Read More

Facebook today said it is shifting to a “local selling structure” in countries outside the U.S. That means that rather than directly route its revenue to its international headquarters in Dublin, local policymakers and governments will potentially get an opportunity for greater visibility into the company’s revenue related to local advertising sales. Read More

Powered by WPeMatico

In an effort to envision how the pending tax bill might affect U.S. startups and their investors, Crunchbase News reached out to tech industry taxation experts. We touched the M&A climate, tax treatment of interest expenses and whether rising costs of living in high-tax states will prompt an exodus to cheaper locales. Here, then, are some thoughts on the potential impacts. Read More

In an effort to envision how the pending tax bill might affect U.S. startups and their investors, Crunchbase News reached out to tech industry taxation experts. We touched the M&A climate, tax treatment of interest expenses and whether rising costs of living in high-tax states will prompt an exodus to cheaper locales. Here, then, are some thoughts on the potential impacts. Read More

Powered by WPeMatico

The first generation of gig economy contractors is essentially riding shotgun as an entirely new industry defines itself. While they enjoy flexibility and a convenient way to supplement a primary income, they also must act as guinea pigs uncovering the shortcomings of the industry’s support network. One issue in particular has become a clear gap for gig economy workers: taxes. Read More

The first generation of gig economy contractors is essentially riding shotgun as an entirely new industry defines itself. While they enjoy flexibility and a convenient way to supplement a primary income, they also must act as guinea pigs uncovering the shortcomings of the industry’s support network. One issue in particular has become a clear gap for gig economy workers: taxes. Read More

Powered by WPeMatico

A proposed tax that charges people as their startup equity vests instead of when they cash it out and actually have money to pay the taxes could wreck how tech companies recruit talent. And the industry doesn’t have much time to mobilize to get this tax changed.

A proposed tax that charges people as their startup equity vests instead of when they cash it out and actually have money to pay the taxes could wreck how tech companies recruit talent. And the industry doesn’t have much time to mobilize to get this tax changed.