tax

Auto Added by WPeMatico

Auto Added by WPeMatico

As an entrepreneur, you started your business to create value, both in what you deliver to your customers and what you build for yourself. You have a lot going on, but if building personal wealth matters to you, the assets you’re creating deserve your attention.

You can implement numerous advanced planning strategies to minimize capital gains tax, reduce future estate tax and increase asset protection from creditors and lawsuits. Capital gains tax can reduce your gains by up to 35%, and estate taxes can cost up to 50% on assets you leave to your heirs. Careful planning can minimize your exposure and actually save you millions.

Smart founders and early employees should closely examine their equity ownership, even in the early stages of their company’s life cycle. Different strategies should be used at different times and for different reasons. The following are a few key considerations when determining what, if any, advanced strategies you might consider:

Some additional items to consider include issues related to qualified small business stock (QSBS), gift and estate taxes, state and local income taxes, liquidity, asset protection, and whether you and your family will retain control and manage the assets over time.

Smart founders and early employees should closely examine their equity ownership, even in the early stages of their company’s life cycle.

Here are some advanced equity planning strategies that you can implement at different stages of your company life cycle to reduce tax and optimize wealth for you and your family.

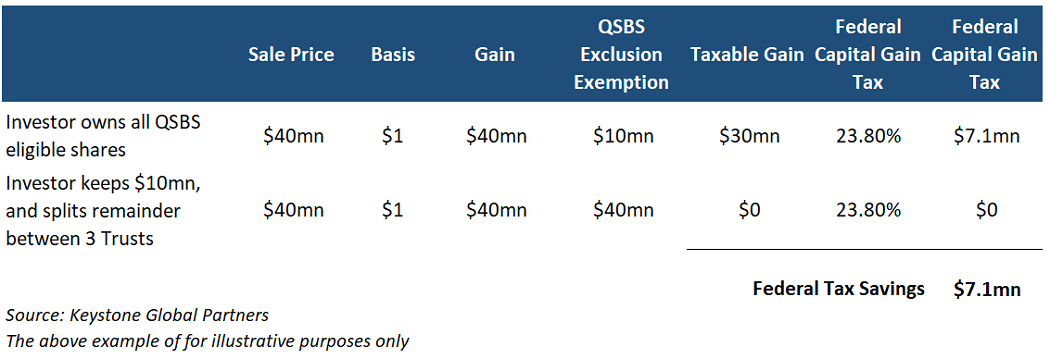

QSBS allows you to exclude tax on $10 million of capital gains (tax of up to 35%) upon an exit/sale. This is a benefit every individual and some trusts have. There is significant opportunity to multiply the QSBS tax exclusion well beyond $10 million.

The founder can gift QSBS eligible stock to an irrevocable nongrantor trust, let’s say for the benefit of a child, so that the trust will qualify for its own $10 million exclusion. The founder owning the shares would be the grantor in this case. Typically, these trusts are set up for children or unborn children. It is important to note that the founder/grantor will have to gift the shares to accomplish this, because gifted shares will retain the QSBS eligibility. If the shares are sold into the trust, the shares lose QSBS status.

Image Credits: Peyton Carr

In addition to the savings on federal taxes, founders may also save on state taxes. State tax can be avoided if the trust is structured properly and set up in a tax-exempt state like Delaware or Nevada. Otherwise, even if the trust is subject to state tax, some states, like New York, conform and follow the federal tax treatment of the QSBS rules, while others, like California, do not. For example, if you are a New York state resident, you will also avoid the 8.82% state tax, which amounts to another $2.6 million in tax savings if applied to the example above.

This brings the total tax savings to almost $10 million, which is material in the context of a $40 million gain. Notably, California does not conform, but California residents can still capture the state tax savings if their trust is structured properly and in a state like Delaware or Nevada.

Currently, each person has a limited lifetime gift tax exemption, and any gifted amount beyond this will generate up to a 40% gift tax that has to be paid. Because of this, there is a trade-off between gifting the shares early while the company valuation is low and using less of your gift tax exemption versus gifting the shares later and using more of the lifetime gift exemption.

The reason to wait is that it takes time, energy and money to set up these trusts, so ideally, you are using your lifetime gift exemption and trust creation costs to capture a benefit that will be realized. However, not every company has a successful exit, so it is sometimes better to wait until there is a certain degree of confidence that the benefit will be realized.

One way for the founder to plan for future generations while minimizing estate taxes and high state taxes is through a parent-seeded trust. This trust is created by the founder’s parents, with the founder as the beneficiary. Then the founder can sell the shares to this trust — it doesn’t involve the use of any lifetime gift exemption and eliminates any gift tax, but it also disqualifies the ability to claim QSBS.

The benefit is that all the future appreciation of the asset is transferred out of the founder’s and the parent’s estate and is not subject to potential estate taxes in the future. The trust can be located in a tax-exempt state such as Delaware or Nevada to also eliminate home state-level taxes. This can translate up to 10% in state-level tax savings. The trustee, an individual selected by the founder, can make distributions to the founder as a beneficiary if desired.

Further, this trust can be used for the benefit of multiple generations. Distributions can be made at the discretion of the trustee, and this skips the estate tax liability as assets are passed from generation to generation.

This strategy enables the founder to minimize their estate tax exposure by transferring wealth outside of their estate, specifically without using any lifetime gift exemption or being subject to gift tax. It’s particularly helpful when an individual has used up all their lifetime gift tax exemption. This is a powerful strategy for very large “unicorn” positions to reduce a founder’s future gift/estate tax exposure.

For the GRAT, the founder (grantor) transfers assets into the GRAT and gets back a stream of annuity payments. The IRS 7520 rate, currently very low, is a factor in calculating these annuity payments. If the assets transferred into the trust grow faster than the IRS 7520 rate, there will be an excess remainder amount in GRAT after all the annuity payments are paid back to the founder (grantor).

This remainder amount will be excluded from the founder’s estate and can transfer to beneficiaries or remain in the trust estate tax-free. Over time, this remainder amount can be multiples of the initial contributed value. If you have company stock that you expect will pop in value, it can be very beneficial to transfer those shares into a GRAT and have the pop occur inside the trust.

This way, you can transfer all the upside gift and estate tax-free out of your estate and to your beneficiaries. Additionally, because this trust is structured as a grantor trust, the founder can pay the taxes incurred by the trust, making the strategy even more powerful.

One thing to note is that the grantor must survive the GRAT’s term for the strategy to work. If the grantor dies before the end of the term, the strategy unravels and some or all the assets remain in his estate as if the strategy never existed.

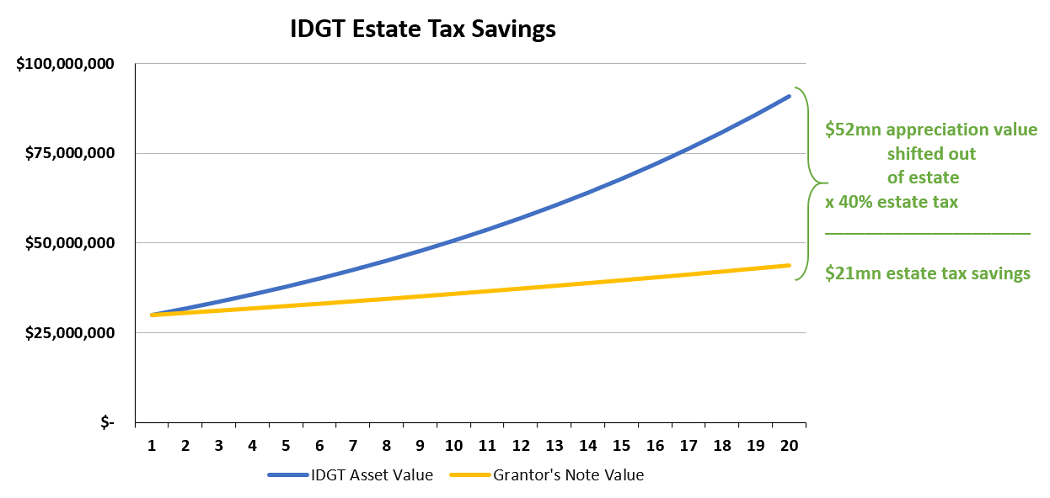

This is similar to the GRAT in that it also enables the founder to minimize their estate tax exposure by transferring wealth outside of their estate, but has some key differences. The grantor must “seed” the trust by gifting 10% of the asset value intended to be transferred, so this approach requires the use of some lifetime gift exemption or gift tax.

The remaining 90% of the value to be transferred is sold to the trust in exchange for a promissory note. This sale is not taxable for income tax or QSBS purposes. The main benefits are that instead of receiving annuity payments back, which requires larger payments, the grantor transfers assets into the trust and can receive an interest-only note. The payments received are far lower because it is interest-only (rather than an annuity).

Image Credits: Peyton Carr

Another key distinction is that the IDGT strategy has more flexibility than the GRAT and can be generation-skipping.

If the goal is to avoid generation-skipping transfer tax (GSTT), the IDGT is superior to the GRAT, because assets are measured for GSTT purposes when they are contributed to the trust prior to appreciation rather than being measured at the end of the term for a GRAT after the assets have appreciated.

Depending on a founder’s situation and goals, we may use some combination of the above strategies or others altogether. Many of these strategies are most effective when planning in advance; waiting until after the fact will limit the benefits you can extract.

When considering strategies for protecting wealth and minimizing taxes as it relates to your company stock, there’s a lot to take into account — the above is only a summary. We recommend you seek proper counsel and choose wealth transfer and tax savings strategies based on your unique situation and individual appetite for complexity.

Powered by WPeMatico

Artificial intelligence has become a fundamental cornerstone of how a lot of business software works, providing a useful boost in reading, understanding and using the often-fragmented trove of data that organizations generate these days. In the latest development, an Israeli startup called Blue dot, which uses AI to help companies handle their tax accounting, is announcing $32 million in funding to continue its growth, specifically addressing the demand from companies for more user-friendly tools to help read and correctly itemize expenses for tax purposes.

“The tax sector is very complicated, and we are playing in a very large space, but it’s a huge revolution,” Blue dot’s CEO and co-founder Isaac Saft said in an interview. “Business and enterprise accounting is just not going to look the same in the future as it does today.”

The funding is being led by Ibex Investors in partnership with Lutetia Technology Partners, with past investors La Maison Partners, Viola and Target Global also contributing. Blue dot rebranded only last week from its original name, VATBox (part of the funding will be used to help Blue dot move deeper into the U.S. market, where the concept of VAT is not quite so ubiquitous: there is no national sales tax and states determine the rates themselves).

PitchBook notes that under its previous name, the startup last raised money in 2017, a $20 million Series B led by Viola at a $120 million post-money valuation.

While Blue dot is not disclosing valuation today, it’s likely to be significantly higher than this based on some of its engagements. In addition to customers like Amazon, tobacco giant BAT and Dell, it also has a partnership with one of the bigger names in expense accounting, SAP Concur, which uses Blue dot to power its expense data entry tool to automatically read charges and figure out how to itemize them so that employees or accountants don’t need to go through the pain of that themselves.

As Saft describes it, part of what is propelling his company’s business is the bigger trend of consumerization and the role that it has played in enterprise services: the working world has picked up a lot of technology tools, led by the smartphone, to help them organize their personal lives, and a lot of what they are being “served” through technology is increasingly personalized with lower barriers of entry, whether its on e-commerce sites, entertainment or social media. In the working world, people can often be frustrated as a result with how much work something like expenses can involve — a process that gets ever more complicated the more strict tax regimes become.

Blue dot’s approach is to essentially view the tax accounting process as something that can be improved with AI to make it easier for people to use — whether those people are workers itemizing their expenses, or accountants auditing them and running those through even bigger accounting processes. With a machine learning system that both takes into account a company’s own internal compliance and company policies, and the wider tax and regulatory framework, Blue dot helps “read” an expense and figure out how to notate it, how much tax should be accounted and where, and so on.

This is especially important as the process of entering and managing expenses gets pushed out to the people spending the money, rather than dedicated accountants handling that work on their behalf. An awareness of how modern offices are functioning today and evolving is one reason why investors were interested here.

“We believe Blue dot can change the way organizations worldwide manage accounting and its tax implications for their expenses,” Gal Gitter, a partner at Ibex, said in a statement. “There’s been a major market shift away from centralization of enterprise functions, including procurement. As that accelerates, more companies will be looking for ways to replace costly and complex manual processes with digital, automated solutions that use data and AI to essentially enable transactions to report themselves, which Blue dot delivers.”

Powered by WPeMatico

Nobody likes dealing with taxes — until the system works in your favor. In many countries, startups can receive tax credits for their R&D work and related employee cost, but as with all things bureaucracy, that’s often a slow and onerous task. Boast.ai aims to make this process far easier, by using a mix of AI and tax experts. The company, which currently has about 1,000 customers, today announced that it has raised a $23 million Series A round led by Radian Capital.

Launched in 2012 by co-founders Alex Popa (CEO) and Lloyed Lobo (president), Boast focuses on helping companies — and especially startups — in the U.S. and Canada claim their R&D tax credits.

“Globally, over $200 billion has been given in R&D incentives to fund businesses, not only in the U.S. and Canada, but the U.K., Australia, France, New Zealand, Ireland give out these incentives,” Lobo explained. “But there’s huge red tape. It’s a cumbersome process. You got to dive in and figure out work that qualifies and what doesn’t. Then you’ve got to file it with your taxes. Then if the government audits you, it’s like a long, laborious process.”

Image Credits: Boast.ai

After working on a few other startup ideas, the co-founders decided to go all-in on Boast. And in the process of working on other ideas, they also realized that AI wasn’t going to be able to do it all, but that it was getting good enough to augment humans to make a complex process like dealing with R&D tax credits scalable.

“The way I think to bootstrap a company is three things,” Lobo explained. “One, customers are looking for an outcome. Get them that outcome in the fastest, cheapest way possible. Two, when you’re doing that, you may have to do a lot of manual work. Figure out what those manual touch points are and then build the workflow to automate that. And once you have those two things, then you’ll have enough data to start working on artificial intelligence and machine learning. Those are the key learnings that we learned the hard way.”

So after doing some of that manual work, Boast can now automatically pull in data using tech tools like JIRA and GitHub and a company’s financial tools like QuickBooks, Gusto and (soon) ADP. It then uses its algorithms to cluster this data, figure out how much time employees spend on projects that would qualify for a tax credit and automate the tax filing process. Throughout the process — and to interact with the government if necessary — the company keeps humans in the loop.

“So all our [customer success] team is engineers,” Lobo noted. “Because if you don’t have engineers they can’t inform the decision-making process. They help figure out if there are any loose ends and then they deal with the audits, communicating with the government and whatnot. That’s how we’re able to effectively get SaaS-like margins or more.”

Ideally, a tool like Boast pays for itself and the company says it has secured more than $150 million in R&D tax credits since launch. Currently, it’s also doubling growth year over year, and that’s what made the founders decide to raise outside money for the first time. That funding will go toward increasing the sales team (which is currently only four people strong) and improving the platform, but Lobo was clear that he doesn’t want to be too aggressive. The goal, he said, is not to have to raise again until Boast can hit the $30 to $50 million revenue mark.

Once fully implemented, Boast also effectively becomes a system of record for all R&D and engineering data. And indeed, that’s the company’s overall vision, with the tax credits being somewhat of a Trojan horse to get to this point. By the middle of next year, the team plans to offer a new product around R&D-based financing, Lobo tells me.

Over the years, the Boast team also focused on not just growing its customer base but also the overall startup ecosystem in the markets in which it operates, with a special focus on Canada. The Boast team, for example, is also the team behind the popular annual Traction conference in Vancouver, Canada (Disclosure: I’ve moderated sessions at the event since its inception). A thriving startup ecosystem creates a larger client base for Boast, too, after all — and coincidently, the team met its investors at the event, too.

Powered by WPeMatico

Every year around this time, Uber drivers, Wag dog walkers, Bird scooter chargers, social media influencers and other gig economy workers face the unsightly challenge of paying their taxes.

Companies like Uber and Lyft classify their drivers as independent contractors, which means you aren’t given any benefits and the company doesn’t withhold any of your taxes. This puts gig workers in a tough position come tax day, especially if they aren’t prepared to shell out big sums to the IRS.

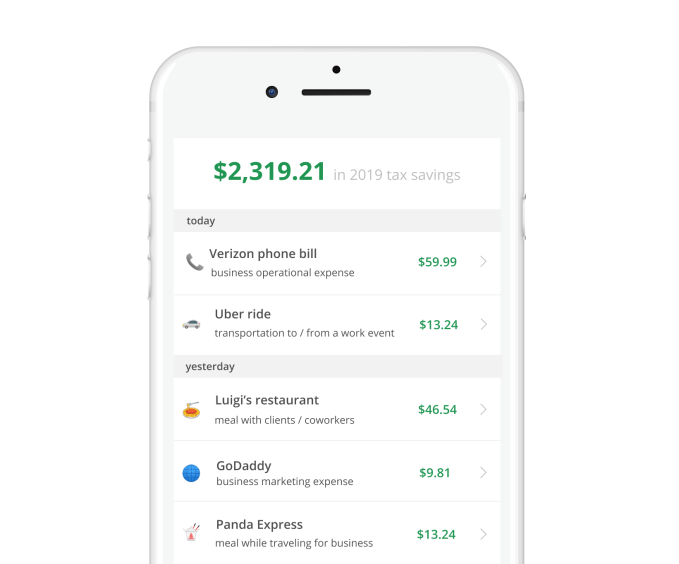

Keeper, a startup that’s just graduated from the Y Combinator startup accelerator, is here to make taxes a lot easier for that demographic and to save them as much money as possible.

Founded by childhood buddies and former debate partners Paul Koullick and David Kang, the San Francisco-based company has raised $1.65 million on a $10 million valuation in a round led by Jake Jolis of Matrix Partners.

Keeper co-founders Paul Koullick (left) and David Kang

The pair entered YC this winter with a big idea and little to show for it. Come March, they had developed a full-fledged product and accumulated 200 paying customers. With their first round of funding, they plan to add to their small but growing team and acquire 10,000 customers in the next 18 months.

“There are some companies that are trying to go very broad and trying to cover the whole spectrum of benefits; we’re just trying to go really deep on taxes,” Kang told TechCrunch. “This is a pain point. This is where people are definitely leaving the most money on the table.”

Keeper guesses the average gig worker in the U.S. is overpaying their taxes by more than 20 percent, or about $1,550 for those making more than $25,000 per year. Why? Because these independent contractors aren’t claiming the tax write-offs available to them, like phone bills, car maintenance fees and even a Spotify subscription for drivers.

“If you’re a dog walker, there are so many things you need to be writing off, like your poop bags, your extra leashes, your parking,” Koullick told TechCrunch. “This population needs the guidance of an accountant, but they can’t afford one and we’re trying to create this third option.”

Like a personal accountant, Keeper monitors gig workers’ expenses all year in search of possible tax deductions, saving each user $173 per month on average, it estimates. The startup uses Plaid to follow its customers’ transaction history, and once per day sends a text message asking if there are any tax write-offs to note. Over time, it gets smarter and smarter, keeping the SMS questions to a minimum.

Keeper doesn’t fully file taxes for 1099 workers yet, but will begin offering a quarterly tax filing service in June. Next year, it plans to offer a full-year tax-filing service.

Koullick, Keeper’s chief executive officer, worked in product at Square before joining another startup, called Stride, where he built and scaled Stride Tax, a mileage and expense-tracking app. Kang, for his part, has spent most of his post-graduate career at a trading firm in Chicago, focused on quantitative modeling. The two toyed with a few startup ideas before landing on Keeper’s tax business.

“We wanted to build something that actually mattered to real people,” Koullick explained. “And we wanted to do it in the financial space where we were happy to wade through ugly details and systems on their behalf.”

Keeper isn’t the only recent YC alum focused on the growing gig economy. Another, Catch, sells health insurance, retirement savings plans and tax-withholding services directly to freelancers, contractors or anyone uncovered. Given the rapid rise of Uber and other gig platforms, it’s no wonder YC startups are tapping into the various business opportunities available there.

“We’re willing to tackle some of these topics that are kind of boring and mundane and really intensive,” Kang added. “Like the average person doesn’t want to think about taxes or filling out forms. We saw that as an opportunity for us to step in and be like, hey, we’ll take it.”

Powered by WPeMatico

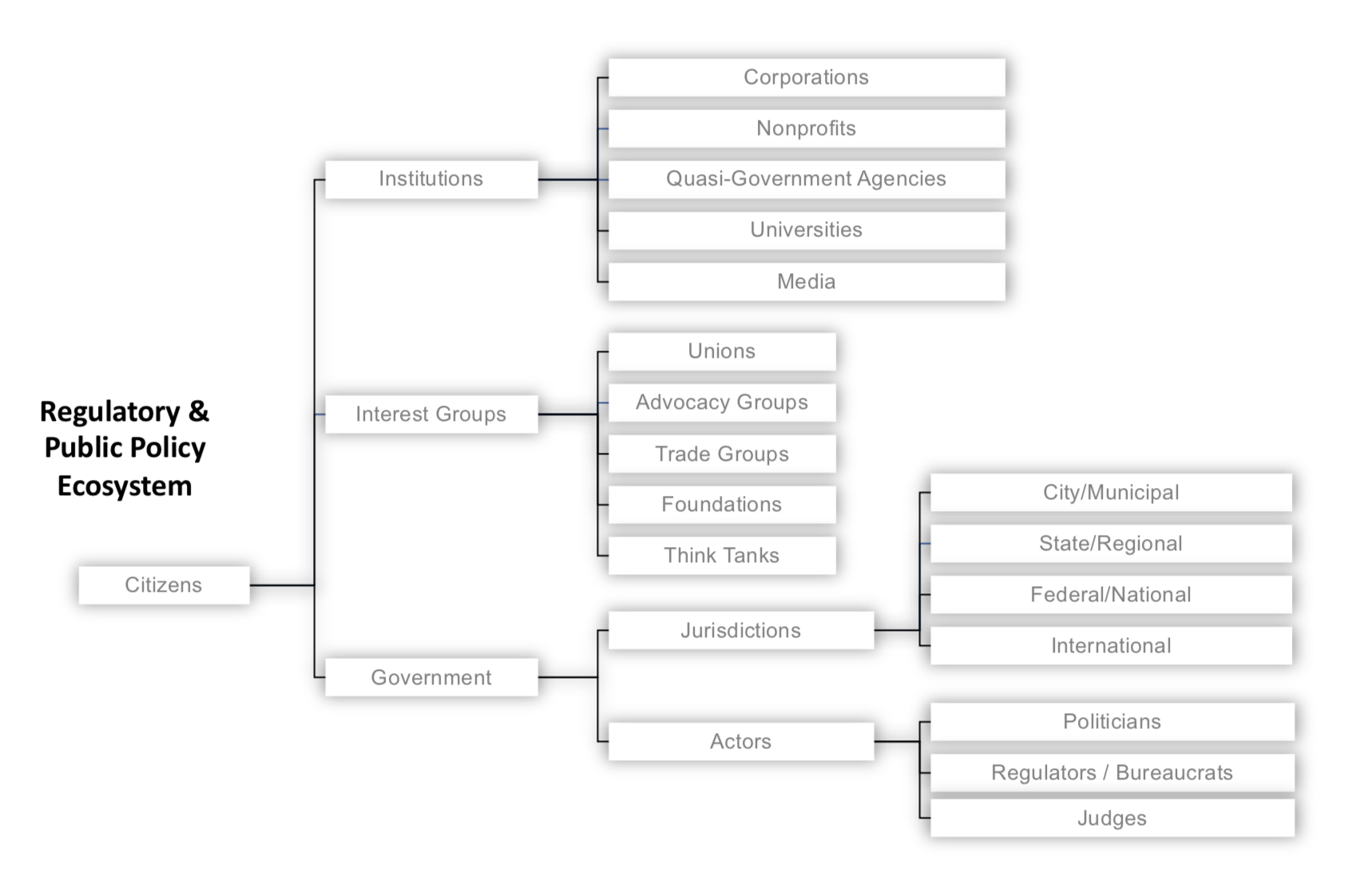

Startups are but one species in a complex regulatory and public policy ecosystem. This ecosystem is larger and more powerfully dynamic than many founders appreciate, with distinct yet overlapping laws at the federal, state and local/city levels, all set against a vast array of public and private interests. Where startup founders see opportunity for disruption in regulated markets, lawyers counsel prudence: regulations exist to promote certain strongly-held public policy objectives which (unlike your startup’s business model) carry the force of law.

Snapshot of the regulatory and public policy ecosystem. Image via Law Office of Daniel McKenzie

Although the canonical “ask forgiveness and not permission” approach taken by Airbnb and Uber circa 2009 might lead founders to conclude it is strategically acceptable to “move fast and break things” (including the law), don’t lose sight of the resulting lawsuits and enforcement actions. If you look closely at Airbnb and Uber today, each have devoted immense resources to building regulatory and policy teams, lobbying, public relations, defending lawsuits, while increasingly looking to work within the law rather than outside it – not to mention, in the case of Uber, a change in leadership as well.

Indeed, more recently, examples of founders and startups running into serious regulatory issues are commonplace: whether in healthcare, where CEO/Co-founder Conrad Parker was forced to resign from Zenefits and later fined approximately $500K; in the securities registration arena, where cryptocurrency startups Airfox and Paragon have each been fined $250K and further could be required to return to investors the millions raised through their respective ICOs; in the social media and privacy realm, where TikTok was recently fined $5.7 million for violating COPPA, or in the antitrust context, where tech giant Google is facing billions in fines from the EU.

Suffice it to say, regulation is not a low-stakes table game. In 2017 alone, according to Duff and Phelps, US financial regulators levied $24.4 billion in penalties against companies and another $621.3 million against individuals. Particularly in today’s highly competitive business landscape, even if your startup can financially absorb the fines for non-compliance, the additional stress and distraction for your team may still inflict serious injury, if not an outright death-blow.

The best way to avoid regulatory setbacks is to first understand relevant regulations and work to develop compliant policies and business practices from the beginning. This article represents a step in that direction, the fifth and final installment in Extra Crunch’s exclusive “Startup Law A to Z” series, following previous articles on corporate matters, intellectual property (IP), customer contracts and employment law.

Given the breadth of activities subject to regulation, however, and the many corresponding regulations across federal, state, and municipal levels, no analysis of any particular regulatory framework would be sufficiently complete here. Instead, the purpose of this article is to provide founders a 30,000-foot view across several dozen applicable laws in key regulatory areas, providing a “lay of the land” such that with some additional navigation and guidance, an optimal course may be charted.

The regulatory areas highlighted here include: (a) Taxes; (b) Securities; (c) Employment; (d) Privacy; (e) Antitrust; (f) Advertising, Commerce and Telecommunications; (g) Intellectual Property; (h) Financial Services and Insurance; and finally (i) Transportation, Health and Safety.

Of course, some regulations may touch on multiple regulatory areas, for example, the “Fair Credit Reporting Act” is a law ultimately about privacy, but it impacts many financial and employment-related services as well. Certain laws may therefore be cross-listed in more than one regulatory area. Also, since we can’t look at every U.S. state and city, this article will focus primarily on the federal and California state laws.

After you focus on the particular regulatory areas that may implicate your business, next reference the short quotations and links to relevant primary and secondary sources below, then work to identify the specific compliance risks you face. This is where other Extra Crunch resources can help. For example, the Verified Experts of Extra Crunch include some of the most experienced and skilled startup lawyers in practice today. Use these profiles to identify attorneys who are focused on serving companies at your particular stage and then seek out any further guidance you need to address the regulatory matters pertinent to your startup.

With that as context, the Startup Law A to Z – Regulatory Compliance checklist is below:

Before diving into further detail, it may be helpful for some readers to note the distinction between a law and a regulation. Simply put, regulations provide more detailed direction on how certain laws should be followed. So regulations are not technically laws, but they carry the force of law (including penalties for violation), since they are adopted by governmental agencies under authority granted by statute. Beyond that, understanding how laws and regulations are actually enacted is helpful to illustrate the extent to which the process is politically driven.

In the U.S., a bill must first pass both legislative branches of government, then, if signed by the executive branch, it will be codified in statute as law (Schoolhouse Rock anyone?). Once codified, the legislative branch will authorize the relevant executive department or agency to determine whether specific regulations are necessary to give the law effect. If so, those executive departments or agencies will determine what further rules are needed, and in turn, work to enforce them.

At the federal level, for example, proposed regulations are developed first through a “Notice of Proposed Rulemaking,” listed in the Federal Register and filed in the corresponding executive agency’s official docket (available at Regulations.gov). This affords the public an opportunity to comment on the regulations. After receiving comments, the filing agency may revise the proposed regulation before final rules are issued, which again will be published in the Federal Register and then filed in the agency’s official docket at Regulations.gov, before they are codified in the Code of Federal Regulations (CFR).

At nearly every step in this process then, institutions, government, and interest groups are working – sometimes at cross purposes – to shape what the law will be and how it will impact your startup.

The Startup Law A to Z – Regulatory Compliance reference guide is below:

Powered by WPeMatico

The only sure things in this life, according to Ben Franklin, are death and taxes. And a new startup called Visor has just raised $9 million in financing to make one of them as painless as possible.

Unlike Nectome, Visor won’t kill anyone, but it may ring the death knell for the high-end tax advisors that most Americans can’t even access to get help filing and paying their taxes. It’s like having a personalized accountant for the cost of a high-end do-it-yourself tax-prep service.

The $9 million Visor raised came from the venture capital firm Defy, with participation from Unusual Ventures, SVB Capital and existing investors like Obvious Ventures, Fika Ventures and Boxgroup, which had put a previous $6.5 million into the company.

The idea for the company had been percolating for co-founder and chief executive Gernot Zacke since he settled in the U.S.

Growing up in Sweden, Zacke was exposed to a much different process for paying taxes. “The experience of filing taxes in Sweden is that you receive a message from the government that stated how much you made and how much you were withholding. That’s it,” said Zacke. “Taxes should be as easy as ordering a cab.”

That’s the service that Visor aims to provide.

“If you think about the market there are two ways to get your taxes done. There’s the DIY space and then there are other online services but it requires the tax payer to fill out the forms and it leaves the tax payer with a little bit of anxiety,” said Zacke. “We’re delivering the CPA experience through the convenience of a web app and a mobile app.”

On average, Americans spend about 13 hours each year dealing with taxes, and the average American doesn’t have the benefits of a professional advisor who can help optimize the process. That’s what Visor wants to provide.

“You provide the same amount of information you provide to a CPA or TurboTax… we make sure that that information is filed securely on AWS and shared between the docs and the backend,” said Zacke.

The target customers for Zacke’s services are folks who have had a change to their tax situation — whether moving, buying a home or any other life event; or folks who have had a CPA and don’t want to pay the higher fees, he said.

Visor currently has an operations team of around 34 people split between San Francisco and Atlanta.

For Zacke, the pain point he’s solving with the Visor service is very real. A former employee of the European investment firm Atomico, Zacke bounced between the U.S. and Europe — eventually running U.S. investments for the firm before leaving to launch Visor.

Other co-founders and senior executives hail from the tax advisory world, and from employee benefits outsourcing services company Zenefits, along with former Venmo and Square developers.

“Taxpayers spend $20 billion a year to get their taxes prepared and are stuck between spending hours filling out DIY tax software and hiring an expensive CPA,” said Zacke, in a statement. “

Powered by WPeMatico

In other news bears shit in the woods. In today’s second-day President Trump news: ‘The Donald’ has seized, belatedly, on the European Commission’s announcement yesterday that Google is guilty of three types of illegal antitrust behavior — with its Android OS, since 2011 — and that it is fining the company $5 billion; a record-breaking penalty which the Commission’s antitrust chief, Margrethe Vestager, said reflects the length and gravity of the company’s competition infringements.

Trump is not! at all! convinced! though!

“I told you so!” he has tweeted triumphantly just now. “The European Union just slapped a Five Billion Dollar fine on one of our great companies, Google . They truly have taken advantage of the U.S., but not for long!”

I told you so! The European Union just slapped a Five Billion Dollar fine on one of our great companies, Google. They truly have taken advantage of the U.S., but not for long!

— Donald J. Trump (@realDonaldTrump) July 19, 2018

Also not so very long ago, Trump was the one grumbling about U.S. tech giants. Though Amazon is his most frequent target in tech, while Google has been spared the usual tweet lashings. Albeit, on the average day he may not necessarily be able to tell one tech giant from another.

Vestager can though, and she cited Amazon as one of the companies that had suffered as a direct result of contractual conditions Google imposed on device makers using its Android OS — squeezing the ecommerce giant’s potential to build a competing Android ecosystem, with its Fire OS.

Presumably, for Trump, Amazon is not ‘one of our great companies’ though.

At least it’s only Google that gets his full Twitter attention — and a special Trumpian MAGA badge of honor call-out as “one of our great companies” — in the tweet.

Presumably, he hasn’t had this pointed out to him yet though. So, uh, awkward.

Safe to say, Trump is seizing on Google’s antitrust penalty as a stick to beat the EU, set against a backdrop of Trump already having slapped a series of tariffs on EU goods, and Trump recently threatening the EU with tariffs on cars — in what is fast looking like a full blown trade war.

Even so, Trump’s tweet probably wasn’t the kind of support Google was hoping to solicit via its own Twitter missive yesterday…

.@Android has created more choice for everyone, not less. #AndroidWorks pic.twitter.com/FAWpvnpj2G

— Google Europe (@googleeurope) July 18, 2018

#AndroidWorksButTradeWarsDon’t doesn’t make for the most elegant hashtag.

But here’s the thing: Vestager has already responded to Trump’s attack on the Android decision — even though it’s taking place a day late. Because the EU’s “tax lady”, as Trump has been known to vaguely refer to her, is both lit and onit.

During yesterday’s press conference she was specifically asked to anticipate Trump’s tantrum response on hearing the EU antitrust decision against Google, and whether she wasn’t afraid it might affect next week’s meeting between the US president and the European Commission’s president, Jean-Claude Juncker.

“As I know my US colleagues want fair competition just as well as we do,” she responded. “There is a respect that we do our job. We have this very simple mission to make sure that companies play by the rulebook for the market to serve consumers. And this is also my impression that this is what they want in the US.”

Pressed again on political context, given the worsening trade relationship between the US and the EU, Vestager was asked how she would explain that her finding against Google is not part of an overarching anti-US narrative — and how would she answer Trump’s contention that the EU’s “tax lady… really hates the US”.

“Well I’ve done my own fact checking on the first part of that sentence. I do work with tax and I am a woman. So this is 100% correct,” she replied. “It is not correct for the latter part of the sentence though. Because I very much like the US. And I think that would also be what you think because I am from Denmark and that tends to be what we do. We like the U.S. The culture, the people, our friends, traveling. But the fact is that this [finding against Google] has nothing to do with how I feel. Nothing whatsoever. Just as well as enforcing competition law — well, we do it in the world but we don’t do it in a political context. Because then there would never, ever be a right timing.

“The mission is very simple. We have to protect consumers and competition to make sure that consumers get the best of fair competition — choice, innovation, best possible prices. This is what we do. It has been done before, we will continue to do it — no matter the political context.”

Maybe Trump will be able to learn the name of the EU’s “tax lady” if Vestager ends up EU president next year.

Or, well, maybe not. We can only hope so.

Powered by WPeMatico

One of my favorite things to do is riff on Bay Area real estate and tech — of all kinds, residential, commercial, retail … and Justin Bedecarre has been working with San Francisco founders for almost a decade in the commercial real estate market. He’s now a founder of HelloOffice, a technology-powered commercial real estate brokerage. We talk about what 2017 holds for… Read More

One of my favorite things to do is riff on Bay Area real estate and tech — of all kinds, residential, commercial, retail … and Justin Bedecarre has been working with San Francisco founders for almost a decade in the commercial real estate market. He’s now a founder of HelloOffice, a technology-powered commercial real estate brokerage. We talk about what 2017 holds for… Read More

Powered by WPeMatico