talent

Auto Added by WPeMatico

Auto Added by WPeMatico

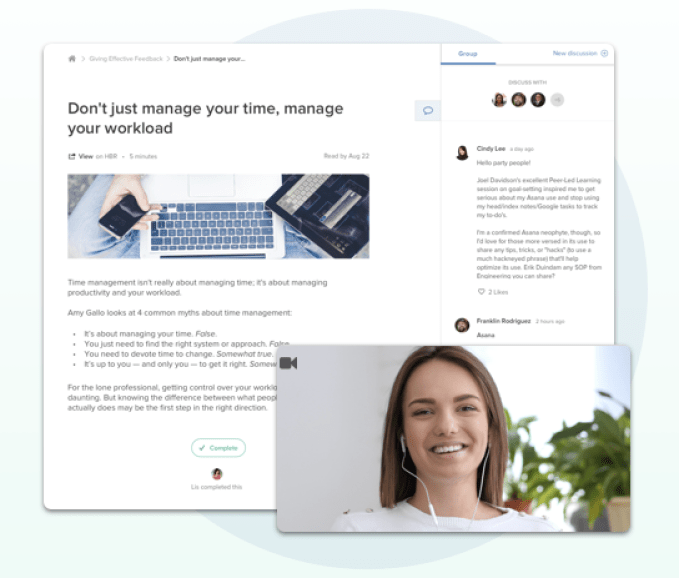

While companies might pay for a CEO coach, lower level employees often get stuck with lame skill-building worksheets or no mentorship at all. Not only does that limit their potential productivity, but it also makes them feel stagnated and undervalued, leading them to jump ship.

Therapy… err… executive coaching is finally becoming destigmatized as entrepreneurs and their teams realize that everyone can’t be crushing it all the time. Building a business is hard. It’s okay to cry sometimes. But the best thing you can do is be vulnerable and seek help.

Torch emerged from stealth last year with $18 million in funding to teach empathy to founders and C-suite execs. Since 2013, Everwise has raised $26 million from Sequoia and others for its peer-to-peer mentorship marketplace that makes workplace guidance accessible to rank-and-file staffers. Tomorrow they’ll official announce their merger under the Torch name to become a full-stack career coach for every level of employee.

“As human beings, we face huge existential challenges in the form of pandemics, climate change, the threats coming down the pipe from automation and AI” says Torch co-founder and CEO Cameron Yarbrough. “We need to create leaders at every single level of an organization and ignite these people with tools and human support in order to level up in the world.”

Startup acquisitions and mergers can often be train wrecks because companies with different values but overlapping products are jammed together. But apparently it’s gone quite smoothly since the products are so complementary, with all 70 employees across the two companies keeping their jobs. “Everwise is much more bottom up whereas Torch is about the upper levels, and it just sort of made sense” says Garry Tan, partner and co-founder of Initialized Capital that funded Torch’s Series A and is also a client of its coaching.

How does each work? Torch goes deep, conducting extensive 360-interviews with an executive as well as their reports, employees, and peers to assess their empathy, communication, vision, conflict resolution, and collaboration. Clients’ executives do extensive 360-interviews. It establishes quantifiable goals that executives work towards through video call sessions with Torch’s coaches. They learn about setting healthy workplace boundaries, staying calm amidst arguments, motivating staff without seeming preachy, and managing their own ego.

This coaching can be exceedingly valuable for the leaders setting a company’s strategy and tone. But the one-on-one sessions are typically too expensive to buy for all levels of employees. That’s where Everwise comes in.

Everwise goes wide, offering a marketplace with 6,000 mentors across different job levels and roles that can provide more affordable personal guidance or group sessions with 10 employees all learning from each other. It also provides a mentorship platform where bigger companies can let their more senior staffers teach junior employees exactly what it takes to succeed. That’s all stitched together with a curated and personalized curriculum of online learning materials. Meanwhile, a company’s HR team can track everyone’s progress and performance through its Academy Builder dashboard.

“We know Gen Z has grown up with mentors by their side from SAT prep” says Torch CMO Cari Jacobs. Everwise lets them stay mentored, even at early stages of their professional life. “As they advance through their career, they might notch up to more executive private coaching.” Post-merger, Torch can keep them sane and ambitious throughout the journey.

“It really allows us to move up market without sacrificing all the traction we’ve built working with startups and mid-market companies,” Yarbrough tells me. Clients have included Reddit and ZenDesk, but also giants like Best Buy, Genentech, and T-Mobile.

The question is whether Everwise’s materials are engaging enough to not become just another employee handbook buried on an HR site that no one ever reads. Otherwise, it could just feel like bloat tacked onto Torch. Meanwhile, scaling up to bigger clients pits Torch against long-standing pillars of the executive coaching industry like Aon and Korn Ferry that have been around for decades and have billions in revenue. Meanwhile, new mental health and coaching platforms are emerging like BetterUp and Sounding Board.

But the market is massive since so few people get great coaching right now. “No one goes to work and is like, ‘Man, I wish my boss was less mindful,’” Tan jokes. When Yarbrough was his coach, the Torch CEO taught the investor that while many startup employees might think they thrive on flexibility, “people really want high love and high structure.” In essence, that’s what Torch is trying to deliver — a sense of emotional camaraderie mixed with a prod in the direction of fulfilling their destiny.

Powered by WPeMatico

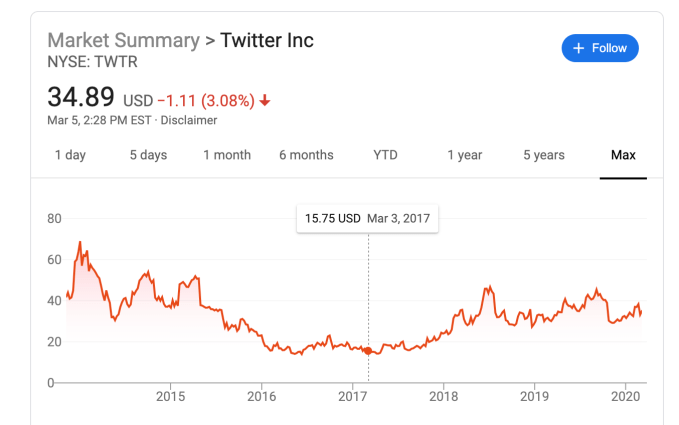

Twitter CEO Jack Dorsey might not spend six months a year in Africa, claims the real product development is under the hood and gives an excuse for deleting Vine before it could become TikTok. Today he tweeted, via Twitter’s investor relations account, a multi-pronged defense of his leadership and the company’s progress.

The proclamations come as notorious activist investor Elliott Management prepares to pressure Twitter into a slew of reforms, potentially including replacing Dorsey with a new CEO, Bloomberg reported last week. Sources confirmed to TechCrunch that Elliott has taken a 4% to 5% stake in Twitter. Elliott has previously bullied eBay, AT&T and other major corporations into making changes and triggered CEO departures.

…Focusing on one job and increasing accountability has made a huge difference for us. One of our core jobs is to keep people informed. We want to be a service that people turn to… to see what’s happening, to be a credible source that people learn from.

— Twitter Investor Relations (@TwitterIR) March 5, 2020

Specifically, Elliott is seeking change because of Twitter’s weak market performance, which as of last month had fallen 6.2% since July 2015, while Facebook had grown 121%. The corporate raider reportedly takes issue with Dorsey also running fintech giant Square, and having planned to spend up to six months a year in Africa. Dorsey tweeted that “Africa will define the future (especially the bitcoin one!),” despite cryptocurrency having little to do with Twitter.

Rapid executive turnover is another sore spot. Finally, Twitter is seen as moving glacially slow on product development, with little about its core service changing in the past five years beyond a move from 140 to 280 characters per tweet. Competing social apps like Facebook and Snapchat have made landmark acquisitions and launched significant new products like Marketplace, Stories and Discover.

Dorsey spoke today at the Morgan Stanley investor conference, though apparently didn’t field questions about Elliott’s incursion. The CEO did take to his platform to lay out an argument for why Twitter is doing better than it looks, though without mentioning the activist investor directly. That type of response, without mentioning to whom it’s directed, is popularly known as a subtweet. Here’s what he outlined:

On democracy: Twitter has prioritized healthy conversation and now “the #1 initiative is the integrity of the conversation around the elections” around the world, which it’s learning from. It’s now using humans and machine learning to weed out misinformation, yet Twitter still hasn’t rolled out labels on false news despite Facebook launching them in late 2016.

On revenue: Twitter expects to complete a rebuild of its core ad server in the first half of 2020, and it’s improving the experience of mobile app install ads so it can court more performance ad dollars. This comes seven years late to Facebook’s big push around app install ads.

On shutting down products: Dorsey claims that “5 years ago we had to do a really hard reset and that takes time to build from… we had been a company that was trying to do too many things…” But was it? Other than Moments, which largely flopped, and the move to the algorithmic feed ranking, Twitter sure didn’t seem to be doing too much and was already being criticized for slow product evolution as it tried to avoid disturbing its most hardcore users.

On stagnation: “Some people talk about the slow pace of development at Twitter. The expectation is to see surface level changes, but the most impactful changes are happening below the surface,” Dorsey claims, citing using machine learning to improve feed and notification relevance.

Yet it seems telling that Twitter suddenly announced yesterday that it was testing Instagram Stories-esque feature Fleets in Brazil. No launch event. No U.S. beta. No indication of when it might roll out elsewhere. It seems like hasty and suspiciously convenient timing for a reveal that might convince investors it is actually building new things.

On talent: Twitter is apparently hiring top engineers “that maybe we couldn’t get 3 years ago.” 2017 was also Twitter’s share price low point of $14 compared to $34 today, so it’s not much of an accomplishment that hiring is easier now. Dorsey claims that “Engineering is my main focus. Everything else follows from that.” Yet it’s been years since fail whales were prevalent, and the core concern now is that there’s not enough to do on Twitter, rather than what it does offer doesn’t function well.

On Jack himself: Dorsey says he should have added more context “about my intention to spend a few months in Africa this year,” including its growing population that’s still getting online. Yet the “Huge opportunity especially for young people to join Twitter” seemed far from his mind as he focused on how crypto trading was driving adoption of Square’s Cash App.

“I need to reevaluate” the plan to work from Africa “in light of COVID-19 and everything else going on.” That makes coronavirus a nice scapegoat for the decision while the phrase “everything else” is doing some very heavy lifting in the face of Elliott’s activist investing.

Photographer: Cole Burston/Bloomberg via Getty Images

On fighting harassment: Nothing. The fact that Twitter’s most severe ongoing problem doesn’t even get a mention should clue you in to how many troubles have stacked up in front of Dorsey.

Running Twitter is a big job. So big it’s seen a slew of leaders ranging from founders like Ev Williams to hired guns like Dick Costolo peel off after mediocre performance. If Dorsey wants to stay CEO, that should be his full-time, work-from-headquarters gig.

This isn’t just another business. Twitter is a crucial communications utility for the world. Its absence of innovation, failure to defend vulnerable users and an inability to deliver financially has massive repercussions for society. It means Twitter hasn’t had the products or kept the users to earn the profits to be able to invest in solving its problems. Making Twitter live up to its potential is no side hustle.

Powered by WPeMatico

Justin Kan’s hybrid legal software and law firm startup Atrium is shutting down today after failing to figure out how to deliver better efficiency than a traditional law firm, the CEO tells TechCrunch exclusively. The startup has now laid off all its employees, which totaled just over 100. It will return some of its $75.5 million in funding to investors, including Series B lead Andreessen Horowitz. The separate Atrium law firm will continue to operate.

“I’m really grateful to the customers and the team members who came along with me and our investors. It’s unfortunate that this wasn’t the outcome that we wanted but we’re thankful to everyone that came with us on the journey” said Kan. He’d previously founded Justin.tv which pivoted to become Twitch and later sold to Amazon for $970 million. “We decided to call it and wind down the startup operations. There will be some capital returned to investors post wind-down” Kan told me.

Atrium had attempted a pivot back in January, laying off its in-house lawyers to become a more pure software startup with better margins. Some of its lawyers formed a separate standalone legal firm and took on former Atrium clients. But Kan tells me that it was tough to regain momentum coming out of that change, which some Atrium customers tell me felt chaotic and left them unsure of their legal representation.

More layoffs quietly ensued as divisions connected to those lawyers were eliminated. But trying to build software for third-party lawyers, many of which have entrenched processes and older leadership, proved difficult. The streamlined workflows may not have seemed worth the thrash of adopting new technology.

“If you look at our original business model with the veritcalized law firm, a lot of these companies that have this kind of full stack model are not going to survive” Kan explained. “A lot of these companies, Atrium included, did not figure out how to make a dent in operational efficiency.”

Founded in 2017, Atrium built software for startups to navigate fundraising, hiring, acquisition deals, and collaboration with their legal team. Atrium also offered in-house lawyers that could provide counsel and best practices in these matters. The idea was that the collaboration software would make its lawyers more efficient than a traditional law firm so they could get work done faster, translating to savings for clients and Atrium.

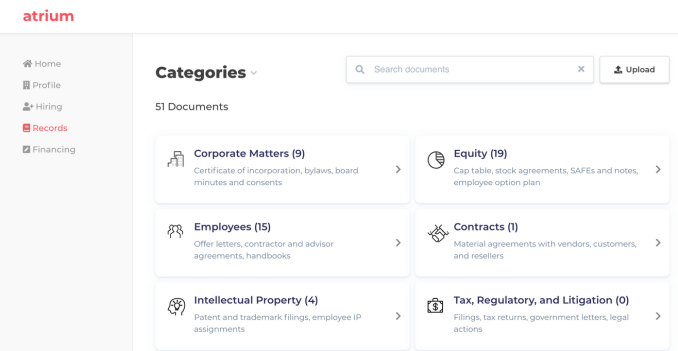

Atrium’s software included Records, a Dropbox-esque system for keeping track of legal documents, and Hiring, which instantly generated employment offer letters based on details punched into a form while keeping track of signatures. The startup hoped it could prevent clients and lawyers from wasting time digging through email chains or missing a sign-off that could put them in legal jeopardy.

The company tried to generate client leads by hosting fundraising workshops for startups, starring Kan and his stories from growing Twitch. A charismatic leader with a near-billion dollar exit under his belt, investors and founders alike were quick to buy into Kan’s vision and advice. Startups saw Atrium as an ally with industry expertise that could help them avoid dirty term sheets or botched hires.

But keeping a large squad of lawyers on staff proved costly. Atrium priced packages of its software and legal assistance under subscriptions, with momentous deals like acquisitions incurring add-on fees. The model relied less on milking clients with steep hourly rates measured down to six-minute increments like most law firms.

Yet eliminating the busy work for lawyers through its software didn’t materialize into bountiful profits. The pivot saught to create a professional services network where Atrium could route clients to attorneys. The layoffs had shaken faith in the startup as clients demanded stability lest they be caught without counsel at a tough time

Rather than trudge on, Kan decided to fold the company. The standalone Atrium law firm will continue to operate under partners Michel Narganes and Matthew Melville, but the startup developing legal software is done.

Atrium’s implosion could send ripples through the legaltech scene, and push other entrepreneurs to start with a more focused software-only approach.

Powered by WPeMatico

Fearing weak fundraising options in the wake of the WeWork implosion, late stage startups are tightening their belts. The latest is another Softbank-funded company, joining Zume Pizza (80% of staff laid off), Wag (80%+), Fair (40%), Getaround (25%), Rappi (6%), and Oyo (5%) that have all cut staff to slow their burn rate and reduce their funding needs. Freight forwarding startup Flexport that is laying off 3% of its global staff.

“We’re restructuring some parts of our organization to move faster and with greater clarity and purpose. With that came the difficult decision to part ways with around 50 employees” a Flexport spokesperson tells TechCrunch after we asked today if it had seen layoffs like its peers.

Flexport CEO Ryan Petersen

Flexport had raised a $1 billion Series D led by SoftBank at a $3.2 billion valuation a year ago, bringing it to $1.3 billion in funding. The company helps move shipping containers full of goods between manufacturers and retailers using digital tools unlike its old-school competitors.

“We underinvested in areas that help us serve clients efficiently, and we over-invested in scaling our existing process, when we actually needed to be agile and adaptable to best serve our clients, especially in a year of unprecedented volatility in global trade” the spokesperson explained.

Flexport still had a record year, working with 10,000 clients to finance and transport goods. The shipping industry is so huge that it’s still only the seventh largest freight forwarder on its top Trans-Pacific Eastbound leg. The massive headroom for growth plus its use of software to coordinate supply chains and optimize routing is what attracted SoftBank.

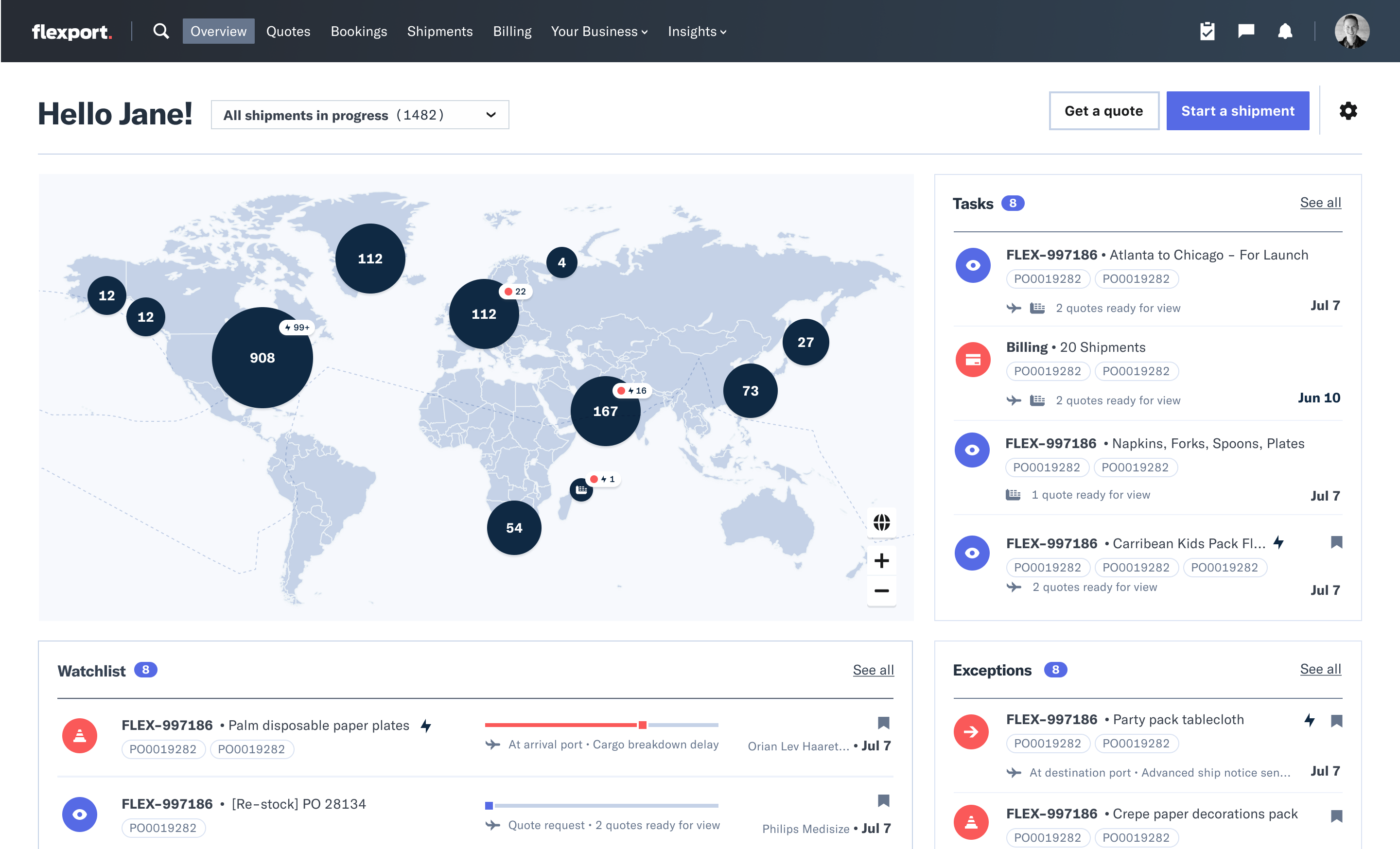

The Flexboard Platform dashboard offers maps, notifications, task lists, and chat for Flexport clients and their factory suppliers.

But many late-stage startups are worried about where they’ll get their next round after taking huge sums of cash from SoftBank at tall valuations. As of November, SoftBank had only managed to raise about $2 billion for its Vision Fund 2 despite plans for a total of $108 billion, Bloomberg reported. LPs were partially spooked by SoftBank’s reckless investment in WeWork. Further layoffs at its portfolio companies could further stoke concerns about entrusting it with more cash.

Unless growth stage startups can cobble together enough institutional investors to build big rounds, or other huge capital sources like sovereign wealth funds materialize for them, they might not be able to raise enough to keep rapidly burning. Those that can’t reach profitability or find an exit may face down-rounds that can come with onerous terms, trigger talent exodus death spirals, or just not provide enough money.

Flexport has managed to escape with just 3% layoffs for now. Being proactive about cuts to reach sustainability may be smarter than gambling that one’s business or the funding climate with suddenly improve. But while other SoftBank startups had to spend tons to edge out direct competitors or make up for weak on-demand service margins, Flexport at least has a tried and true business where incumbents have been asleep at the wheel.

Powered by WPeMatico

“We’re trying to shift cryptocurrency from this speculative asset class to driving real-world utility,” Coinbase CEO Brian Armstrong tells me. How? Through commerce and micropayments. But now Coinbase has the who to build it. Today the startup announced it has hired away former head of Product for Indian e-commerce giant Flipkart and Google Shopping VP of Product Surojit Chatterjee to become Coinbase’s chief product officer.

“I’ve always enjoyed being associated with technology that is on the brink of changing how we live” writes Chatterjee. “Google ads has helped democratize commerce, Flipkart and ecommerce has revolutionized life in India, and I believe Coinbase is going to turn conventional finance on its head.”

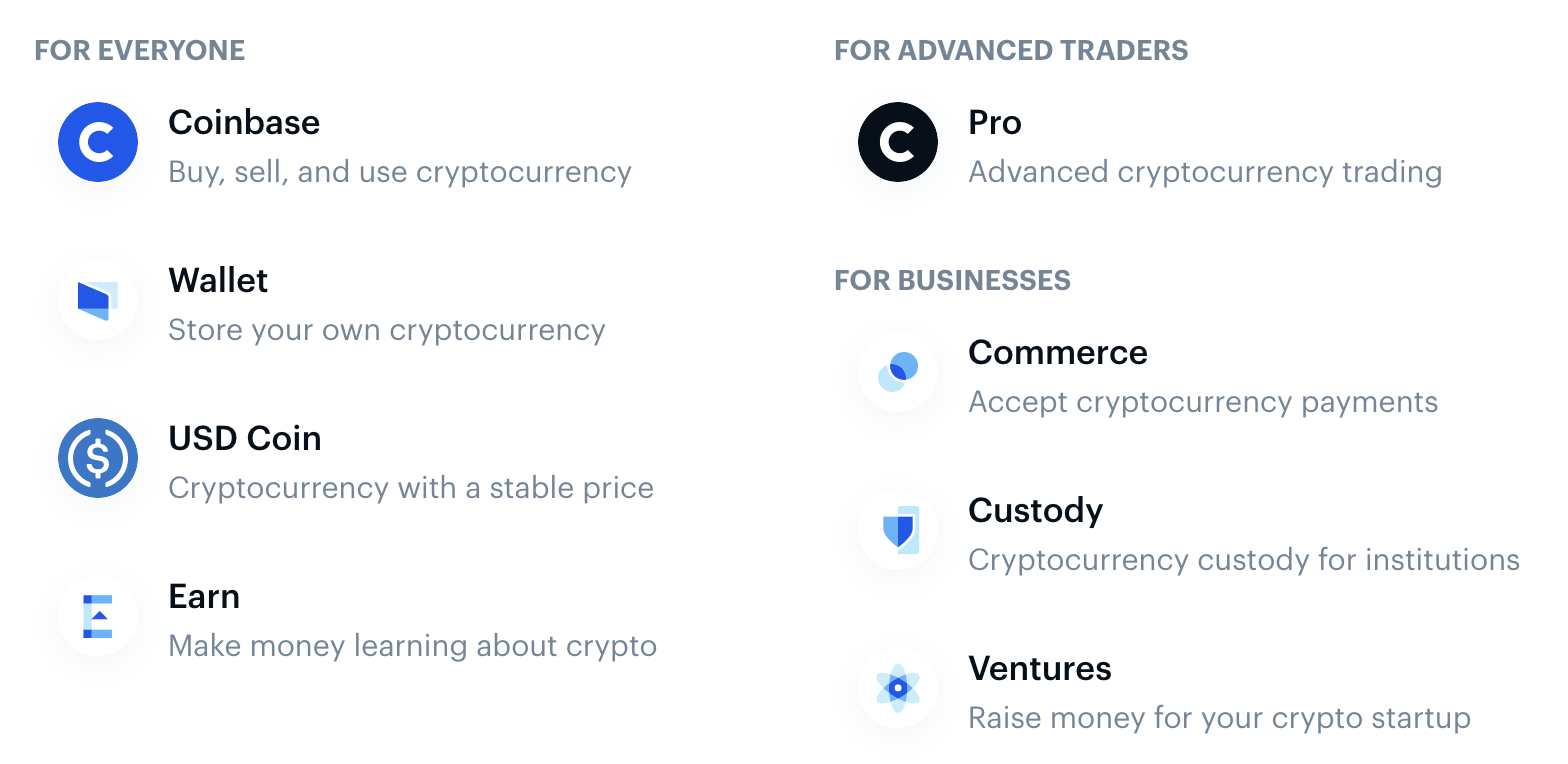

Chatterjee spent more than 11 years at Google over two stints, the first as a founding member of Google’s mobile search Ads product that’s grown to tens of billions in revenue per year. When he starts at Coinbase next week, Armstrong tells me he’ll help Coinbase organize its complex array of products, including its cryptocurrency exchange, wallet, stablecoin, incentivized crypto education platform Earn and Coinbase Commerce that lets businesses take payments in Bitcoin, Ethereum and more. Chatterjee replaces Jeremy Henrickson, the former Coinbase CPO who departed in December 2018.

“Surojit is a huge asset here because we’re a product-led company,” Armstrong says. “We have different leaders and they increasingly have responsibilities around P&L. Having one really experienced chief product officer that can mentor them and teach them to own revenues and budgets — really in the model of Google — that will professionalize Coinbase.”

One opportunity Armstrong hopes Chatterjee can help Coinbase seize on is building products for emerging markets where financial infrastructure is weak. “E-commerce is not equally distributed around the world. Micropayments don’t work that well … Him spending time living in India, a developing market, he deeply understands mobile money.” Given the explosion of phone-based payments, the demonetization and the prevalence of cash on delivery methods in India that Flipkart dealt with, “his background is kind of ideal from that worldly perspective,” Armstrong explains.

Chatterjee cites his upbringing as inspiration to deliver “economic freedom for everyone,” as Armstrong says is Coinbase’s mission. “Growing up in India in a poor middle-class household, I saw very closely what a lack of liquid cash does to a family’s lifestyle,” Chatterjee recalls.

“As a kid I would go with my mom to a local bank to withdraw money. And believe me when I tell you that the process was epic!” It included withdrawal slips, tokens and anxiously trying to match current signatures to versions decades old. When India demonetized and made everyone exchange their cash, “My dad, who was almost 80 at that time, stood in a queue for five hours to get 2000 Rs, which was the per-day limit for the first week. That’s less than $30!” Digital money could ensure people always have access to everything they own.

Surojit Chatterjee (far right) rides along for a Flipkart delivery to understand the consumer commerce experience

In developed countries, Armstrong sees a chance for Chatterjee to enable digital content creators to turn their passion into their profession. “There’s lots of people who lurk on Reddit or Stack Overflow and answer questions … If there was real money on these things, these could be their full time jobs — contributing content on user-generated social sites,” Armstrong predicts. “I think you’d see a lot more contributions, as well.”

Now might be the perfect time to hire Chatterjee since we’re in a lull period for cryptocurrency in the wake of the rush at the end of 2018. “Crypto is always challenging to navigate. In these periods when it’s relatively quiet, we tend to do really well,” Armstrong says. The company grew market share, volume and app installs versus competitors between 50% and 100%, according to the CEO. Referencing ancient war strategy, Armstrong concludes that, “There’s years where you just want to train the soldiers and stockpile resources and you’re basically just preparing. We’re building the company, not just responding to crazy hype.”

Powered by WPeMatico

After appointing a new CEO and CFO last summer, cloud infrastructure provider DigitalOcean is embarking on a wider reorganisation: the startup has announced a round of layoffs, with potentially between 30 and 50 people affected.

DigitalOcean has confirmed the news with the following statement:

“DigitalOcean recently announced a restructuring to better align its teams to its go-forward growth strategy. As part of this restructuring, some roles were, unfortunately, eliminated. DigitalOcean continues to be a high-growth business with $275M in [annual recurring revenues] and more than 500,000 customers globally. Under this new organizational structure, we are positioned to accelerate profitable growth by continuing to serve developers and entrepreneurs around the world.”

Before the confirmation was sent to us this morning, a number of footprints began to emerge last night, when the layoffs first hit, with people on Twitter talking about it, some announcing that they are looking for new opportunities and some offering help to those impacted. Inbound tips that we received estimate the cuts at between 30 and 50 people. With around 500 employees (an estimate on PitchBook), that would work out to up to 10% of staff affected.

It’s not clear what is going on here — we’ll update as and when we hear more — but when Yancey Spruill and Bill Sorenson were respectively appointed CEO and CFO in July 2019 (Spruill replacing someone who was only in the role for a year), the incoming CEO put out a short statement that, in hindsight, hinted at a refocus of the business in the near future:

“My aspiration is for us to continue to provide everything you love about DO now, but to also enhance our offerings in a way that is meaningful, strategic and most helpful for you over time.”

The company provides a range of cloud infrastructure services to developers, including scalable compute services (“Droplets” in DigitalOcean terminology), managed Kubernetes clusters, object storage, managed database services, Cloud Firewalls, Load Balancers and more, with 12 data centers globally. It says it works with more than 1 million developers across 195 countries. It has also been expanding the services that it offers to developers, including more enhancements in its managed database services, and a free hosting option for continuous code testing in partnership with GitLab.

All the same, as my colleague Frederic pointed out when DigitalOcean appointed its latest CEO, while developers have generally been happy with the company, it isn’t as hyped as it once was, and is a smallish player nowadays.

And in an area of business where economies of scale are essential for making good margins on a business, it competes against some of the biggest leviathans in tech: Google (and its Google Cloud Platform), Amazon (which as AWS) and Microsoft (with Azure). That could mean that DigitalOcean is either trimming down as it talks to investors for a new round; or to better conserve cash as it sizes up how best to compete against these bigger, deep-pocketed players; or perhaps to start thinking about another kind of exit.

In that context, it’s notable that the company not only appointed a new CFO last summer, but also a CEO with prior CFO experience. It’s been a while since DigitalOcean has raised capital. According to PitchBook data, DigitalOcean last raised money in 2017, an undisclosed amount from Mighty Capital, Glean Capital, Viaduct Ventures, Black River Ventures, Hanaco Venture Capital, Torch Capital and EG Capital Advisors. Before that, it took out $130 million in debt, in 2016. Altogether it has raised $198 million, and its last valuation was from a round in 2015, $683 million.

It’s been an active week for layoffs among tech startups. Mozilla laid off 70 employees this week; and the weed delivery platform Eaze is also gearing up for more cuts amid an emergency push for funding.

We’ll update this post as we learn more. Best wishes to those affected by the news.

Powered by WPeMatico

Seventy-five-million-dollar-funded legal services startup Atrium doesn’t want to be the next company to implode as the tech industry tightens its belt and businesses chase margins instead of growth via unsustainable economics. That’s why Atrium is laying off most of its in-house lawyers.

Now, Atrium will focus on its software for startups navigating fundraising, hiring and collaborating with lawyers. Atrium plans to ramp up its startup advising services. And it’s also doubling down on its year-old network of professional service providers that help clients navigate day-to-day legal work. Atrium’s laid-off attorneys will be offered spots as preferred providers in that network if they start their own firm or join another.

“It’s a natural evolution for us to create a sustainable model,” Atrium co-founder and CEO Justin Kan tells TechCrunch. “We’ve made the tough decision to restructure the company to accommodate growth into new business services through our existing professional services network,” Kan wrote on Atrium’s blog. He wouldn’t give exact figures, but confirmed that more than 10 but less than 50 staffers are impacted by the change, with Atrium having a headcount of 150 as of June.

The change could make Atrium more efficient by keeping fewer expensive lawyers on staff. However, it could weaken its $500 per month Atrium membership that included some services from its in-house lawyers that might be more complicated for clients to get through its professional network. Atrium will also now have to prove the its client-lawyer collaboration software can survive in the market with firms paying for it rather than it being bundled with its in-house lawyers’ services.

“We’re making these changes to move Atrium to a sustainable model that provides high-quality services to our clients. We’re doing it proactively because we see the writing on the wall that it’s important to have a sustainable business,” Kan says. “That’s what we’re doing now. We don’t anticipate any disruption of services to clients. We’re still here.”

Justin Kan (Atrium) at TechCrunch Disrupt SF 2017

Founded in 2017, Atrium promised to merge software with human lawyers to provide quicker and cheaper legal services. Its technology can help automatically generate fundraising contracts, hiring offers and cap tables for startups while using machine learning to recommend procedures and clauses based on anonymized data from its clients. It also serves like a Dropbox for legal, organizing all of a startup’s documents to ensure everything’s properly signed and teams are working off the latest versions without digging through email.

The $500 per month Atrium membership offered this technology plus limited access to an in-house startup lawyer for consultation, plus access to guide books and events. Clients could pay extra if they needed special help such as with finalizing an acquisition deal, or access to its Fundraising Concierge service for aid with developing a pitch and lining up investor meetings.

Kan tells me Atrium still has some in-house lawyers on staff, which will help it honor all its existing membership contracts and power its new emphasis on advising services. He wouldn’t say if Atrium is paid any equity for advising, or just cash. The membership plan may change for future clients, so lawyer services are provided through its professional network instead.

“What we noticed was that Atrium has done a really good job of building a brand with startups. Often what they wanted from attorneys was…advice on ‘how to set my company up,’ ‘how to set my sales and marketing team up,’ ‘how to get great terms in my fundraising process,’ ” so Atrium is pursuing advising, Kan tells me. “As we sat down to look at what’s working and what’s not working, our focus has been to help founders with their super-hero story, connect them with the right providers and advisors, and then helping quarterback everything you need with our in-house specialists.”

LawSites first reported Saturday that Atrium was laying off in-house lawyers. A source says that Atrium’s lawyers only found out a week ago about the changes, and they’ve been trying to pitch Atrium clients on working with them when they leave. One Atrium client said they weren’t surprised by the changes because they got so much legal advice for just $500 per month, which they suspected meant Atrium was losing money on the lawyers’ time as it was so much less expensive than competitors. They also said these cheap legal services rather than the software platform were the main draw of Atrium, and they’re unsure if the tech on its own is valuable enough.

One concern is Atrium might not learn as quickly about which services to translate into software if it doesn’t have as many lawyers in-house. But Kan believes third-party lawyers might be more clear and direct about what they need from legal technology. “I feel like having a true market for the software you’re building is better than having an internal market,” he says. “We get feedback from the outside firms we work with. I think in some ways that’s the most valuable feedback. I think there’s a lot of false signals that can happen when you’re the both the employer and the supplier.”

It was critical for Atrium to correct course before getting any bigger, given the fundraising problems hitting late-stage startups with poor economics in the wake of the WeWork debacle and SoftBank’s troubles. Atrium had raised a $10.5 million Series A in 2017 led by General Catalyst alongside Kleiner, Founders Fund, Initialized and Kindred Ventures. Then in September 2018, it scored a huge $65 million Series B led by Andreessen Horowitz.

Raising even bigger rounds might have been impossible if Atrium was offering consultations with lawyers at far below market rate. Now it might be in a better position to attract funding. But the question is whether clients will stick with Atrium if they get less access to a lawyer for the same price, and whether the collaboration platform is useful enough for outside law firms to pay for.

Kan had gone through tough pivots in the past. He had strapped a camera to his head to create content for his live-streaming startup Justin.tv, but wisely recentered on the 3% of users letting people watch them play video games. Justin.tv became Twitch and eventually sold to Amazon for $970 million. His on-demand personal assistant startup Exec had to switch to just cleaning in 2013 before shutting down due to rotten economics.

Rather than deny the inevitable and wait until the last minute, with Atrium Kan tried to make the hard decision early.

Powered by WPeMatico

“Despite a lot of publicity and social media, number of sign-ups were modest,” reads one of the last monthly reports I sent to my VCs before my startup ceased to exist. “After the initial wave, sign-ups have slowed right down to near pre-launch levels. User acquisition is our number-one priority and my biggest headache.”

Like, I suspect, many other early-stage founders, I hated the monthly chore of writing a short report for investors. We used the PPP format (progress, problems and plans) for these regular missives, but progress was almost always slow and most of the time, problems far outstripped plans.

On good months, I was far more motivated to file our monthly report — it is a very human thing to want to deliver good news — and on bad months I had a million other more important things I thought a CEO should be spending their time on.

However, according to a research conducted by Jan Luca Ernst, a masters student at The University of St. Gallen, I may have been misguided. In his thesis, supported by Prof. Dr. Elgar Fleisch (Professor of Technology Management at University of St. Gallen) and Florian Schweitzer (a partner at VC firm btov), he writes “startups that submit regular, high-quality reports are shown by the statistics to be better investments than other startups.”

The research was based on analysis of hundreds of monthly startup reports submitted to btov Partners by portfolio companies out of its first two funds, which ran between 2006 to 2014. Specifically, researchers looked at 64 startups, covering the performance of startups during the first two years after initial investment from the first fund, and the performance during a single year, 2015, for the second fund.

“Hypotheses on the positive effects of monthly startup reports were tested, using several multivariate regressions,” write the paper’s authors. “As a result, several initial assumptions were discarded.”

For example, the punctuality of startup reports did not appear to indicate whether a startup would be more successful. In contrast, the frequency of reporting (at a confidence level of 95%), as well as the quality of the reporting (at a confidence level of 99%), were identified as contributors to success.

“Overall, the findings emphasize the importance of the post-investment phase and the value added by venture capitalists beyond financial support,” say Ernst, Fleisch and Schweitzer. “One main implication of the findings has an impact on subsequent investment rounds. Startups that submit regular, high-quality reports are shown by the statistics to be better investments than other startups. This may be an indicator that justifies further investment, that, in turn, leads to better performance.”

The authors also suggest that, in the future, investors may ask for “full, unfiltered access” to all past reporting of a startup, including evidence on the quality of reports and regularity of submission. “This would increase transparency and therefore eventually lead to better investment decision making,” they write.

With that said, during a call with btov’s Florian Schweitzer, he conceded that correlation doesn’t necessarily mean cause, but argued that there are many softer, and sometimes hidden, positive outcomes from monthly reports — especially when a founder does them honestly and whole heartedly.

Extra Crunch: What should a monthly report contain?

Florian Schweitzer: We always define what we would like or what we think would be sensible, because for each startup, of course, it is different. In general, the idea is that the founders can do the report in half an hour. Usually, it contains something like eight KPIs, and then some bullet points reflecting on what went well, and what are the challenges right now. And those challenges are a superb opportunity to understand where the founder is struggling, and where we can support them. So it can be a very, very productive agenda for a discussion, which we usually have regularity.

I think it is very good that founders sit back and think for half an hour: what happened during the last 30 days? What did I want to achieve? What did I not achieve? And to be honest about the progress and challenges.

Powered by WPeMatico

Every once in a while on VC Twitter, a comment or statement seems so outlandish, so completely outrageous, that it must be — certainly has to be — false. Such as it was for Primary Ventures investor Jason Shuman, who commented on the recent prices for pitch deck advice in the Valley today:

Founder friend just told me that SF deck designers have quoted him between $20K to $40K + the right to invest up to $250K…my mind is officially blown

— Jason Shuman

(@BoatShuman) December 20, 2019

You can almost hear that plaintive scream, “My mind is officially blown” (Shuman doesn’t scream, mind you). And indeed, in a world where more and more founders are worried about a bubble; assets are more, let’s say, Notionally expensive than ever before; and everything just seems a little bit crazy these days, it seems downright, fucking insane to think that a PowerPoint file and some “thoughts” are worth tens of thousands of dollars, and a goddamn term sheet to boot.

But they are.

Or at the very least, they can be. And I say that as the guy who wrote an article last week entitled, “How to avoid the startup trap of the parasitic consultant.”

For sure, not every pitch deck consultant is worth top dollar, any more than not every croissant in New York’s West Village is worth $10. But some are, and certainly an elect chosen set of consultants are worth every penny they demand.

The best consultants are not luxuries to plaster on your WeWork’s walls, but critical tools to invest in your startup. Framing a startup’s thesis, product, team, and market exactly right is a qualitative skill that can’t be learned from reading a book or scanning through a founder friend’s deck or two. Get a single slide wrong, or hell, a single bullet point wrong and the whole thing can blow up in a pitch meeting in thirty seconds or less.

Trust me. As a former VC investor, I have gotten hung up on single sentences before. A founder has put their life’s work into a company, synoptically condensed it to a handful of slides, and I am stuck on eight words. But those eight words make no sense, and once something doesn’t make sense, the whole edifice of excitement and confidence comes crashing down. Eight words — one badly chosen verb and adjective.

A good pitch deck consultant may barely move the needle on a fundraise, while a superstar may not just get you a better term sheet, they may fundamentally transform the entire course of your startup’s trajectory. Those are the stakes.

And of course, it’s not just pitch deck consultants who can do this. The right PR consultants can potentially get you traction that no one else can. The right sales consultants may lock in those critical early design customers that represent the difference between an orderly liquidation and a massive Series A. The right product marketing specialists or pricing experts may be what drives conversions and eliminates churn.

What’s so hard today for founders is that the Valley has indeed matured, and all these consultants and more are available. There are the hucksters and the tricksters, the bon vivants thriving on naive capital, the idiot clowns cloaked in their own compelling pitch decks.

But as the market has expanded for these services, at least some superstars are emerging from the marketplace, people who can offer more value for you in a week or two than the mediocrities can in a year.

Your job as founder is to constantly probe and find those diamonds, and get them working on your idea at any cost — even costs that might at times seem insane.

The thing with tech startups today is that they are built upon strata of superstardom. Superstar talents lead to superstar products, superstar VC capital, and ultimately, superstar exits. Superstar momentum is real. Yes, yes, yes, not every time, and every stage in the pipeline is multiplied by a stochastic chance of failure, for sure. But idiocy has rarely been a path to success.

And so as with all parts of innovation, it’s all about making the right investments in the right people and the right ideas. $50K or even $500K for a consultant won’t do anything if they are the wrong person working on the wrong idea — parasites are parasites after all. But leverage that early seed capital into the right people working on the right problems, and that’s where the magic happens.

And so I can understand some of the outrage over these figures, as well as the lingering presumption behind them that VCs care more about a startup’s deck than the underlying startup itself. Those frustrations are palpable and not insane, but let’s not avoid the tough question: everything has some value attached to it. It shouldn’t surprise anyone that top experts in their fields, who understand their own leverage, would take advantage of their expertise and drive their own prices higher.

Paying tens of thousands of dollars for a pitch deck consultant isn’t a prerequisite for securing a venture capital round. There are founders whose entire skill is securing capital for their companies who have never paid a penny for this skill.

Yet ultimately, all early-stage startups face the same challenge: too many activities, too little time. Something, somewhere is going to have to get outsourced today and the quality of that external work is largely going to be determined by how much you are willing to pay for it. What you choose to spend whatever capital you have will determine the trajectory of your startup. So whether it is pitch decks or another activity, never blink from those top dollars. It may very well be what gets you the top dollar in the end.

Powered by WPeMatico

I’ve been following Estonia-headquartered Jobbatical and its founder, Karoli Hindriks, for years. Part of the vanguard of startups working on infrastructure for digital nomads, the startup has been building the base platform to help global job seekers hire and fire their governments.

As Jobbatical has worked with more and more companies and governments though, it has learned that the friction here is not just finding employment globally for talented individuals, but rather the actual process of applying for immigration and work permits, ranging from forms that must be filed in person to the hours of labor it can take to fill out an application.

“What started to happen was that the relocation part… became something that the clients came back to us and said, ‘Can you do relocation for everyone and not just those coming through Jobbatical?’” Hindriks explained.

Last year, Jobbatical began to refocus its platform on powering relocation for workers at companies, and now its new strategy is coming into focus with the launch of the company’s new offices in Spain and Germany, announced on stage earlier today at TechCrunch Disrupt Berlin.

In the process, the company hopes to not just make the immigration process easier — but also much faster.

“How much time are government officials doing dummy work?” Hindriks asked. “30-40% of the consulate’s time is spent on answering the question of ‘what is the status of my visa?’”

The problem is that feedback in the immigration system is not available to all the players involved. Immigration process agents at companies who handle their workers’ visas have to constantly search around to make sure they are moving each of their cases forward. Managers have no idea when their workers may move, while employees are kept in the dark about their current status, inducing anxiety.

Hindriks’ vision is to help each of these three sides use a “TurboTax for immigration” to streamline the process. Jobbatical now can handle immigration applications in Estonia, Germany, and Spain and hopes to add Finland early next year.

But the more ambitious vision is ultimately to help governments drive their processes faster. Similar to how, say, the U.S. tax agency the Internal Revenue Service offers eFiling, Hindriks sees a future where Jobbatical can help facilitate immigration filings and massively speed up the efficiency of governments around these processes by allowing workers to directly submit applications to the government. She is working with two countries today to create exactly these sorts of digital submission systems.

It’s a space that has heated up in recent years as immigration continues to flow across the world. Boundless, for instance, helps individuals apply for U.S. green cards. Jobbatical is focused on the B2B market, focused on companies with global workforces.

Despite the deep debate in many countries over immigration, the reality is that every country has skills deficits that can be helped with smart and efficient immigration. Jobbatical is one company that may make the system more fair and relaxing for stressed workers looking to build their international careers.

Powered by WPeMatico