sv angel

Auto Added by WPeMatico

Auto Added by WPeMatico

Forward Kitchens was working quietly on its digital storefront for restaurants and is now announcing a $2.5 million seed round.

Raghav Poddar started the company two years ago and was part of the Y Combinator Summer 2019 cohort. Poddar told TechCrunch he has been a foodie his entire life. Lately, he was relying on food delivery and pickup services, and while visiting with some of the restaurant owners, he realized a few things: first, not many had a good online presence, and second, these restaurants had the ability to cook cuisine representative of their communities.

That led to the idea of Forward Kitchens, which provides a turnkey tool for restaurants to set up an online presence, including food delivery, where they can create multiple digital storefronts easily and without having to contact each delivery platform. The company ran pilot programs in a handful of restaurants, and this is the first year coming out of stealth.

“It’s an expansion of what they have on the menu, but is not immediately available in the neighborhood,” Poddar added. “Kitchens can keep the costs and headcount the same, but be able to service the demand and get more orders because it is fulfilling a need for the neighborhood, which is why we can grow so fast.”

Here’s how it works: Forward Kitchens goes into a restaurant and takes into account its capacity for additional cooking and the demographic area, as well as what food is available near it, and helps the restaurant create the storefront.

Each restaurant is able to build multiple storefronts, for example, an Italian restaurant setting up a storefront just to sell its popular mac n’ cheese or other small plates on demand. A couple hundred digital storefronts were already created, Poddar said.

A group of investors, including Y Combinator, Floodgate, Slow Ventures and SV Angel and angel investors Michael Seibel of YC, Ram Shriram and Thumbtack’s Jonathan Swanson, were involved in the round.

The new funding will be used to expand the company’s footprint and reach, and to hire a team in operations, sales and engineering to help support the product.

“Forward Kitchens is empowering independent kitchens to create digital storefronts and receive more online sales,” Seibel said via email. “With Forward Kitchens, a kitchen can create world-class digital storefronts at the click of a button.”

Powered by WPeMatico

Now that you have that COVID dog, Embark Veterinary wants to help him or her be in your life for a long time by offering DNA testing with the goal of curbing preventable diseases and increasing the lifespan of dogs by three years within the next decade.

The Boston-based dog genetics company raised $75 million in Series B funding in what the company is calling “the biggest Series B for a pet startup to date.” SoftBank Vision Fund 2 was the lead investor and was joined by existing investors F-Prime Capital, SV Angel, Slow Ventures, Freestyle Capital and Third Kind Venture Capital.

The new round boosts Embark’s total funding to $94.3 million since the company was founded in 2015, according to Crunchbase data. It also gives it a post-money valuation of $700 million, Embark founder and CEO Ryan Boyko told TechCrunch.

Boyko has been a dog lover all his life, and also interested in biology and evolution. Dogs, in particular, are fascinating to him because of their variety: they can be bred to be two pounds or 200 pounds, and come in all shapes and sizes. His interest led him to study dogs in order to understand their evolution.

“I began to think about health problems, and honestly, dogs are a better system for using genetics to better their health than humans,” Boyko said. “You can breed them, so genetics has as much power to cause health problems as it can improve quality and life.”

Embark’s dog DNA test retails for $199 and enables dog owners, breeders and veterinarians to personalize care plans based on a dog’s unique genetic profile. It can test for over 350 breeds and 200 genetic health risks, as well as physical traits. Similar to a 23andMe test, test users can learn characteristics about breed, health and ancestry.

For example, the test could show that a healthy dog may have a gene that predisposes them to slipped discs. If the dog has that, then weight management would be an important factor in their care regime, as would not allowing them to jump off the couch. Another common genetic risk is HUU, or Hyperuricosuria, which is elevated levels of uric acid in urine that could lead to bladder stones due to the way dogs process minerals. By changing the dog’s diet, it could reduce the risk for developing the stones, which are painful and expensive to treat, Boyko said.

The test’s technology revolves around proprietary genotyping technology that analyzes more than 200,000 genetic markers, currently two times more information than any other dog DNA test on the market, Boyko said. This gives Embark the world’s largest database of canine health and biological information, enabling the company to provide insights into certain conditions and make new discoveries about health risks, traits and breeds.

Embark aims to become the standard of care for dog owners and vets. It grew 235% between 2019 and 2020 and saw five times the sales over the past two years. To support that growth, the company intends to use the new funding to bring on key hires and expand its database. Boyko anticipates adding more than 100 employees between 2021 and 2022.

Boyko said the opportunity in the pet startup space is huge. Indeed, U.S. spending on pets reached nearly $100 billion in 2020, up from $95.7 billion in 2019, according to the American Pet Products Association.

At the same time, venture capital interest in U.S. pet-focused companies, from nutrition to travel to healthcare, grew 29.5% from 2019 and 2020, according to Crunchbase data. In addition to Embark’s funding, 2021 was good to other pet startups as well, including pet insurance company Wagmo, raising $12.5 million, connected pet collar company Fi received $30 million and Rover, which announced plans to go public via SPAC.

Lydia Jett, partner at SoftBank Investment Advisers, told TechCrunch that this was her first pet-based investment, and what Embark is doing brings advances to a category right now where people care about their pets enough that they want to do something that will expand their value of life.

Jett said the management team being dedicated to DNA-based analytics is the future, and Embark is starting this big curve when it comes to pets and the convergence of real emotional ties to pets and the ability to improve their lives.

“This company is a driver of change to happen,” she added. “We are the largest consumer investor in the world, and Embark is very much aligned with what we are seeing across our portfolio that consumers are revisiting priorities and choices. That is a major trend, but still early in the cycle of personalization for their pets.”

Powered by WPeMatico

Open-source framework startup Serverless Stack announced Friday that it raised $1 million in seed funding from a group of investors that includes Greylock Partners, SV Angel and Y Combinator.

The company was founded in 2017 by Jay V and Frank Wang in San Francisco, and they were part of Y Combinator’s 2021 winter batch.

Serverless Stack’s technology enables engineers to more easily build full-stack serverless apps. CEO V said he and Wang were working in this space for years with the aim of exposing it to a broader group of people.

While tooling around in the space, they determined that the ability to build serverless apps was not getting better, so they joined Y Combinator to hone their idea on how to make the process easier.

Here’s how the technology works: The open-source framework allows developers to test and make changes to their applications by directly connecting their local machines to the cloud. The problem with what V called an “old-school process” is that developers would upload their apps to the cloud, wait for it to run and then make any changes. Instead, Serverless Stack connects directly to the cloud for the ability to debug applications locally, he added.

Since its launch six months ago, Serverless Stack has grown to over 2,000 stars on GitHub and was downloaded more than 60,000 times.

Dalton Caldwell, managing director of YC, met V and Wang at the cohort and said he was “super impressed” because the pair were working in the space for a long time.

“These folks are experts — there are probably just half a dozen people who know as much as they do, as there aren’t that many people working on this technology,” Caldwell told TechCrunch. “The proof is in the pudding, and if they can get people to adopt it, like they did on GitHub so far, and keep that community engagement, that is my strongest signal of staying power.”

V has earmarked the new funding to expand the team, including hiring engineers to support new use cases.

Serverless initially gravitated toward specific use cases — APIs are now allowing its community to chime in and it is using that as a guide, V said. It recently announced more of a full-stack use case for building out APIs with a database and also building out the front end frameworks.

Ultimately, V’s roadmap includes building out more tools with a vision of getting Serverless Stack to the point where a developer can come on with an idea and take it all the way to an IPO using his platform.

“That’s why we want the community to drive the roadmap,” V told TechCrunch. “We are focused on what they are building and when they are in production, how they are managing it. Eventually, we will build out a dashboard to make it easier for them to manage all of their applications.”

Powered by WPeMatico

Startups need money. State and local governments need startups and the employment growth they offer. It should be obvious that the two groups can work together and make each other happy. Unfortunately, nothing could be further from the truth.

Each year, governments spend tens of billions of dollars on economic development incentives designed to attract employers and jobs to their communities. There are a huge number of challenges, however, for startups and individual contributors trying to apply for these programs.

First, economic development leaders typically focus on massive, flagship projects that are splashy and will drive the news cycle and bring good media attention to their elected official bosses. So, for example, you get a massive, $10 billion Foxconn plant in Wisconsin tied to hundreds of millions of incentives, only to see the project sputter into the ground.

Then there is the paperwork. As you’d expect with any government application process, it can be arduous to find the right incentive programs, apply for credits at the right time and max out the opportunities available.

That’s where MainStreet comes in.

Its CEO and founder Doug Ludlow’s third company. He previously founded Hipster, which sold to AOL, and The Happy Home Company, which sold to Google. After that transaction, Ludlow went on to become chief of staff for SMB ads at the tech giant, where he saw firsthand the challenges that startups and all small companies face in growing outside of major urban hubs like San Francisco.

When he and his co-founders Dan Lindquist and Daniel Griffin first started, they were focused on what Ludlow described as “a network of remote work hubs.” As they were experimenting last November they tried paying people to leave the Bay Area, offering them $10,000 if they moved to other cities. The offer caused a sensation, with outlets like CNN covering the news.

While the interest from customers was great, what ignited Ludlow and his co-founders’ passions was that “literally dozens of cities, states and counties reached out, letting us know that they had an incentive program.” As the team explored further, they realized there was a huge untapped opportunity to connect startups to these preexisting programs.

MainStreet was born, and it’s an idea that has also attracted the attention of investors. The company announced today that it raised a $2.3 million round from Gradient Ventures, Weekend Fund and others.

Startups apply for economic incentives through MainStreet’s platform, and then MainStreet takes a 20% cut of any successful application. Notably, that cut is only taken when the incentive is actually disbursed (there’s no upfront cost), and there is also no on-going subscription fee to use the platform. “If you identify the credit that you’re able to use six months from now, we will charge you six months from now, when you’re actually getting that credit. It seems to be a business model that is aligned well with founders,” Ludlow said.

Right now, he says that the average MainStreet client saves $51,000, and that MainStreet has crossed the $1 million ARR run rate threshold.

Right now, the company’s core clientele are startups applying for payroll credits and research and development credits, but Ludlow says that MainStreet is working to expand beyond its tech roots to all small businesses such as restaurants. The company also wants to expand the number of economic development programs that startups can apply for. Given the myriad of governments and programs, there are hundreds if not thousands of more programs to onboard onto the platform.

MainStreet’s team. Image Credits: MainStreet

While MainStreet is helping startups and small businesses, it also wants to help governments improve their operations around economic development. With MainStreet, “we can report back to cities and states showing exactly what their tax dollars or tax credits are being utilized for,” Ludlow said. “So the accountability is orders of magnitude greater than they had before. So already, there’s this better system for tracking the success of incentives.”

The big question for MainStreet this year is navigating the crisis around the COVID-19 pandemic. While more small businesses than ever need help navigating credits, state and local governments have suffered huge shortfalls in revenues as taxes have dried up and Washington continues to debate over what, if any aid, to offer. There’s no money for economic development, yet, economic development has never been more important than right now.

Ultimately, MainStreet is pushing the vanguard of economic development thinking forward away from massive checks designed to underwrite industrial factories to a more flexible and dynamic model of incentivizing knowledge workers to move to areas outside the major global cities. It’s an interesting bet, and one that, at the very least, will help many startups get the economic incentives they rightly have access to.

Outside of Gradient and Weekend Fund, Shrug Capital, SV Angel, Remote First Capital, Basement Fund, Basecamp Ventures, Backend Capital and a host of angels participated in the round.

Powered by WPeMatico

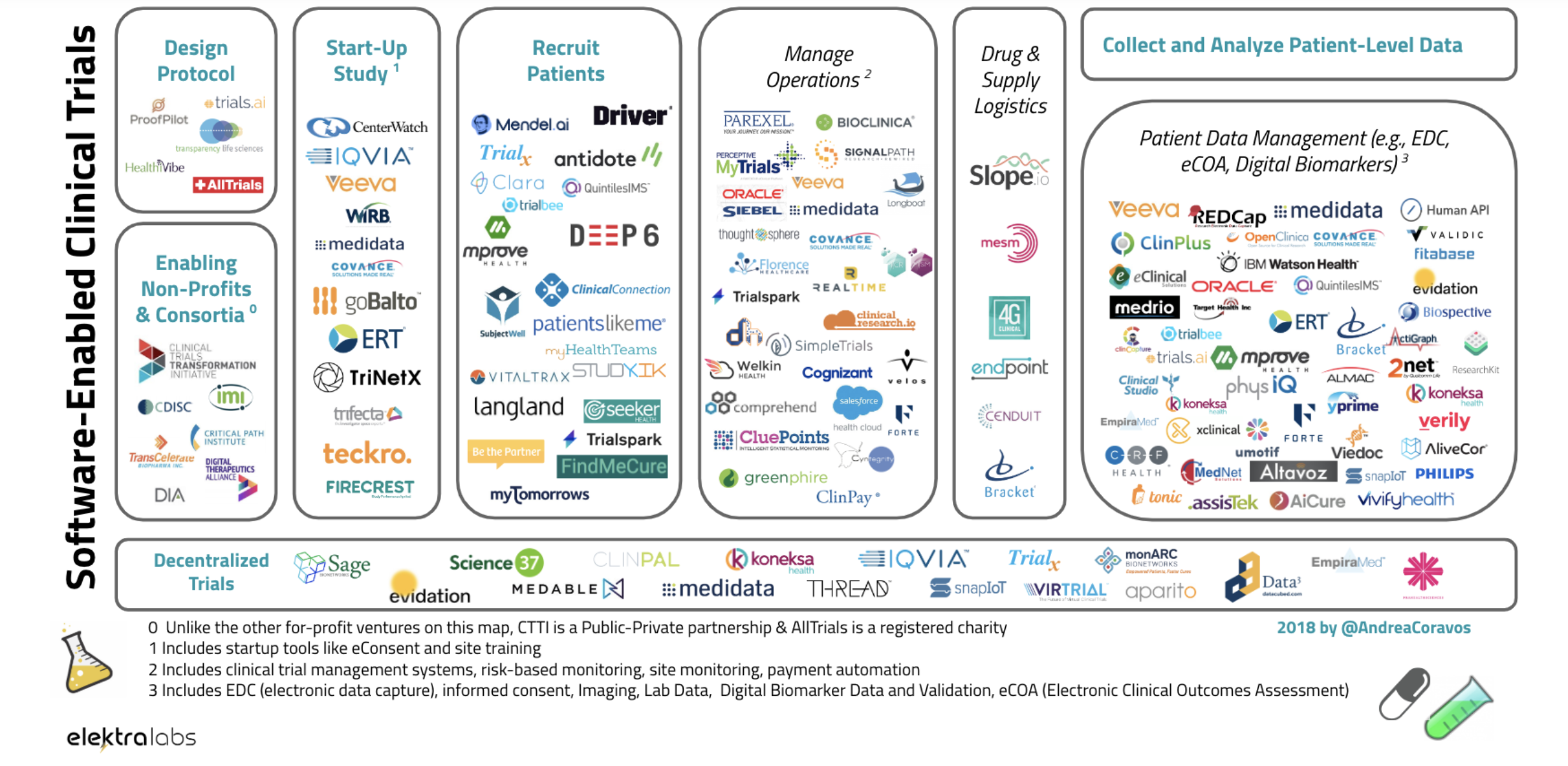

Depending on which study you believe, the wearable and digital health market could be worth anywhere from $30 billion to nearly $90 billion in the next six years.

If the numbers around the size of the market are a moving target, just think about how to gauge the validity and efficacy of the products that are behind all of those billions of dollars in spending.

Andy Coravos, the co-founder of Elektra Labs, certainly has.

Coravos, whose parents were a dentist and a nurse practitioner, has been thinking about healthcare for a long time. After a stint in private equity and consulting, she took a coding bootcamp and returned to the world she was raised in by taking an internship with the digital therapeutics company Akili Interactive.

Coravos always thought she wanted to be in healthcare, but there was one thing holding her back, she says. “I’m really bad with blood.”

That’s why digital therapeutics made sense. The stint at Akili led to a position at the U.S. Food and Drug Administration as an entrepreneur in residence, which led to the creation of Elektra Labs roughly two years ago.

Now the company is launching Atlas, which aims to catalog the biometric monitoring technologies that are flooding the consumer health market.

These monitoring technologies, and the applications layered on top of them, have profound implications for consumer health, but there’s been no single place to gauge how effective they are, or whether the suggestions they’re making about how their tools can be used are even valid. Atlas and Elektra are out to change that.

The FDA has been accelerating its clearances for software-driven products like the atrial fibrillation detection algorithm on the Apple Watch and the ActiGraph activity monitors. And big pharma companies like Roche, Pfizer and Novartis have been investing in these technologies to collect digital biomarker data and improve clinical trials.

Connected technologies could provide better care, but the technologies aren’t without risks. Specifically, the accuracy of data and the potential for bias inherent in algorithms that were created using flawed data sets mean there’s a lot of oversight that still needs to be done, and consumers and pharmaceutical companies need to have a source of easily accessible data about the industry.

”The increase in FDA clearances for digital health products coupled with heavy investment in technology has led to accelerated adoption of connected tools in both clinical trials and routine care. However, this adoption has not come without controversy,” said Coravos in a statement. “During my time as an Entrepreneur in Residence in the FDA’s Digital Health Unit, it became clear to me that like pharmacies which review, prepare, and dispense drug components, our healthcare system needs infrastructure to review, prepare, and dispense connected technologies components.”

The analogy to a pharmacy isn’t an exact fit, because Elektra Labs currently doesn’t prepare or dispense any of the treatments that it reviews. But Atlas is clearly the first pillar that the digital therapeutics industry needs as it looks to supplant pharmaceuticals as treatments for some of the largest and most expensive chronic conditions (like diabetes).

Courtesy of Andrea Coravos/Elektra Labs

Coravos and here team interviewed more than 300 professionals as they built the Atlas toolkit for pharmaceutical companies and other healthcare stakeholders seeking a one-stop shop for all their digital healthcare data needs. Like a drug label, or nutrition label, Atlas publishes labels that highlight issues around the usability, validation, utility, security and data governance of a product.

In an article in Quartz earlier this year, Coravos made her pitch for Elektra Labs and the types of things it would monitor for the nascent digital therapeutics industry. It includes the ability to handle adverse events involving digital therapies by providing a single source where problems could be reported; a basic description for consumers of how the products work; an assessment of who should actually receive digital therapies, based on the assessment of how well certain digital products perform with certain users; a description of a digital therapy’s provenance and how it was developed; a database of the potential risks associated with the product; and a record of the product’s security and privacy features.

As the projections on market size show, the problem isn’t going to get any smaller. As Google’s recent acquisition bid for Fitbit and the company’s reported partnership with Ascension on “Project Nightingale” to collect and digitize more patient data shows, the intersection of technology and healthcare is a huge opportunity for technology companies.

“Google is investing more. Apple is investing more… More and more of these devices are getting FDA cleared and they’re becoming not just wellness tools but healthcare tools,” says Coravos of the explosion of digital devices pitching potential health and wellness benefits.

Elektra Labs is already working with undisclosed pharmaceutical companies to map out the digital therapeutic environment and identify companies that might be appropriate partners for clinical trials or acquisition targets in the digital market.

“The FDA is thinking about these digital technologies, but there were a lot of gaps,” says Coravos. And those gaps are what Elektra Labs is designed to fill.

At its core, the company is developing a catalog of the digital biomarkers that modern sensing technologies can track and how effective different products are at providing those measurements. The company is also on the lookout for peer-reviewed published research or any clinical trial data about how effective various digital products are.

Backing Coravos and her vision for the digital pharmacy of the future are venture capital investors, including Maverick Ventures, Arkitekt Ventures, Boost VC, Founder Collective, Lux Capital, SV Angel and Village Global.

Alongside several angel investors, including the founders and chief executives from companies including: PillPack, Flatiron Health, National Vision, Shippo, Revel and Verge Genomics, the venture investors pitched in for a total of $2.9 million in seed funding for Coravos’ latest venture.

“Timing seems right for what Elektra is building,” wrote Brandon Reeves, an investor at Lux Capital, which was one of the first institutional investors in the company. “We have seen the zeitgeist around privacy data in applications on mobile phones and now starting to have the convo in the public domain about our most sensitive data (health).”

If the validation of efficacy is one key tenet of the Atlas platform, then security is the other big emphasis of the company’s digital therapeutic assessment. Indeed, Coravos believes that the two go hand-in-hand. As privacy issues proliferate across the internet, Coravos believes that the same troubles are exponentially compounded by internet-connected devices that are monitoring the most sensitive information that a person has — their own health records.

In an article for Wired, Koravos wrote:

Our healthcare system has strong protections for patients’ biospecimens, like blood or genomic data, but what about our digital specimens? Due to an increase in biometric surveillance from digital tools—which can recognize our face, gait, speech, and behavioral patterns—data rights and governance become critical. Terms of service that gain user consent one time, upon sign-up, are no longer sufficient. We need better social contracts that have informed consent baked into the products themselves and can be adjusted as user preferences change over time.

We need to ensure that the industry has strong ethical underpinning as it brings these monitoring and surveillance tools into the mainstream. Inspired by the Hippocratic Oath—a symbolic promise to provide care in the best interest of patients—a number of security researchers have drafted a new version for Connected Medical Devices.

With more effective regulations, increased commercial activity, and strong governance, software-driven medical products are poised to change healthcare delivery. At this rate, apps and algorithms have the opportunity to augment doctors and complement—or even replace—drugs sooner than we think.

Powered by WPeMatico

Exchanges like Coinbase have ballooned in size by taking the mechanics of equity markets and fitting them to cryptocurrency markets, but as the space expands in its scope and craftiness, new exchanges trading asset classes native to cryptocurrency are taking off and attracting the attention of top Silicon Valley VCs. Oh, and Coinbase, too.

Blade is a new cryptocurrency derivatives exchange launching in three weeks. Prior to starting the company, CEO Jeff Byun and his co-founder Henry Lee founded OrderAhead, a delivery startup platform that was eventually acquired in-part by Square in 2017. The pair’s newest company shares little in common with their previous venture, but they are bringing aboard some of the same investors to support them.

Blade is announcing that they’ve raised $4.3 million in seed funding from a host of investors, including Coinbase, SV Angel, A.Capital, Slow Ventures, Justin Kan and Adam D’Angelo.

The exchange is tackling perpetual swap contracts.

Perpetuals are a crypto-native trading instrument that Byun says are “arguably the fastest growing segment of cryptocurrency trading.” They allow traders to bet on the future values of cryptocurrencies in relation to another and the instruments have no expiration dates, unlike fixed maturity futures. Traders can bet on how the price of Bitcoin can increase relative to USD, but they can also make bets relative to other altcoins like Monero, DogeCoin, Zcash, Ripple and Binance Coin. Here’s what’s on the Blade menu at the moment.

Blade’s noteworthy spins on perpetuals trading — compared to other exchanges — are that most of the contracts will be set up on simplified vanilla contracts, the perpetuals will also be margined/settled in USD Tether and the company is offering higher leverages (up to 150x on BTC-USD and BTC-KRW) on trades.

")

Blade is raising funds from Silicon Valley’s VCs, but U.S. investors won’t be legally able to participate in the exchange. U.S. government agencies have been a bit more stringent in regulating cryptocurrencies, so there’s more trading activity taking place on exchanges outside the jurisdiction. Blade itself is an offshore entity with a U.S. subsidiary; its primary market is East Asia.

“It’s kind of a bifurcated market,” Byun tells TechCrunch. “Either you have exchanges like Coinbase or Gemini or Bitrex that cater to the U.S. market that are highly regulated or the exchanges that cater to the non-U.S. market that are much less regulated, but that’s where most of the volume is.”

While the company is still three weeks away from launch, the founders have bold ambitions.

“In the long term, we want to be the CME (Chicago Mercantile Exchange) of crypto,” Byun tells me. “Coinbase and Binance are building this foundational structure for crypto, but I think we are too and in a sense that derivatives are at their core about risk transfer, we want to be building the foundational layer for risk transfer in the crypto markets.”

Powered by WPeMatico

When Shomik Dutta and Betsy Hoover first met in 2007, he was coordinating fundraising and get-out-the-vote efforts for Barack Obama’s first presidential campaign and she was a deputy field director for the campaign.

Over the next two election cycles the two would become part of an organizing and fundraising team that transformed the business of politics through its use of technology — supposedly laying the groundwork for years of Democratic dominance in organizing, fundraising, polling and grassroots advocacy.

Then came Donald J. Trump and the 2016 election.

For both Dutta and Hoover, the 2016 outcome was a wake-up call against complacency. What had worked for the Democratic party in 2008 and 2012 wasn’t going to be effective in future election cycles, so they created the investment firm Higher Ground Labs to provide financing and a launching pad for new companies serving Democratic campaigns and progressive organizations.

“As the political world shifts from analog to digital, we need a lot more tools to capture that spend,” says Dutta. “Democrats are spending on average 70 cents of every dollar raised on television ads. We are addicted to old ways of campaigning. If we want to activate and engage an enduring majority of voters we have to go where they are (and that’s increasingly online) and we have to adapt to be able to have these conversations wherever they are.”

While the Obama campaign effectively used the internet as a mobilization tool in its two campaigns, the lessons of social media and mobile technologies that offer a “direct-to-consumer” politics circumventing traditional norms have, in the ensuing years, been harnessed most effectively by conservative organizations, according to some scholars and activists.

“The internet is a tool and in that sense it’s neutral, but just like other communication tools from the past, people with more power, with more resources, with more organization, have been able to take advantage of it,” Jen Schradie, an assistant professor at the Observatoire sociologique du changement at Sciences Po in Paris, told Vox in an interview earlier this month.

Schradie is a scholar whose recent book, “The Revolution That Wasn’t,” contends that the internet’s early application as a progressive organizing tool has been overtaken by more conservative elements. “The idea of neutrality seems more true of the internet because the costs of distributing information are dramatically lower than with something like television or radio or other communication tools,” she said. “However, to make full use of the internet, you still need substantial resources and time and motivation. The people who can afford to do this, who can fund the right digital strategy, create a major imbalance in their favor.”

Schradie contends that a web of privately funded think tanks, media organizations, talk radio and — increasingly — mobile applications have woven a conservative stitch into the fabric of social media. The medium’s own tendency to promote polarizing and fringe viewpoints also served to amplify the views of pundits who were previously believed to be political outliers.

Essentially, these sites have enabled commentators and personalities to create a patchwork of “grassroots” organizations and media operations dedicated to reaching an audience receptive to their particular political message that’s funded by billionaire donors and apolitical corporate ad dollars.

Then there’s the technology companies, like Cambridge Analytica, which improperly used access to Facebook data for targeting purposes — also financed by these same billionaires.

“The last six years have witnessed millions and millions of dollars of private Koch money and Mercer money that have gone to pretty sophisticated data and media efforts to advance the Republican agenda,” says Dutta. “I want to even the scale.”

Dutta is referring to Charles and David Koch and Robert Mercer, the scions and founder (respectively) of two family dynasties worth billions. The Koch brothers support a web of political advocacy groups, while Mercer and his daughter were large backers of Breitbart News and Cambridge Analytica, two organizations that arguably provided much of the policy underpinnings and online political machinery for the Trump presidential campaign.

But there’s also the simple fact that Donald Trump’s digital strategy director, Brad Parscale, was able to effectively and inexpensively leverage the social media tools and data troves amassed by the Republican National Committee that were already available to the candidate who won the Republican primary. In fact, in the wake of Romney’s loss, Republicans spent years building up profiles of 200 million Americans for targeted messaging in the 2016 election.

“Who controls Facebook controls the 2016 election,” Parscale said during a speaking engagement at the Romanian Academy of Sciences, according to a report in Forbes.

Parscale, now the campaign manager for the president’s 2020 reelection campaign recalled, “These guys from Facebook walked into my office and said: ‘we have a beta … it’s a new onboarding tool … you can onboard audiences straight into Facebook and we will match them to their Facebook accounts,’ ” according to Forbes .

During the 2016 campaign, Hillary Clinton’s team made 66,000 visual ads, according to Parscale, while the Trump campaign made 5.9 million ads by leveraging social media networks and the language of memes. And in the run-up to the 2020 election, Parscale intends to go back to the same well. The Trump campaign has already spent more than $5 million on Facebook ads in the current election cycle, according to The New York Times — outspending every single Democratic candidate in the field and roughly all of the Democrats combined.

Dutta and Hoover are working to offset this movement with investments of their own. Back in 2017, the two launched Higher Ground Labs, an early-stage company accelerator and investment firm dedicated to financing technology companies that could support progressive causes.

The firm has $15 million committed from investors, including Reid Hoffman, the co-founder of LinkedIn and a partner at Greylock; Ron Conway, the founder of SV Angel and an early backer of Google, Facebook and Twitter; Chris Sacca, an early investor in Uber; and Elizabeth Cutler, the founder of SoulCycle. Already, Higher Ground has invested in more than 30 companies focused on services like advocacy outreach, polling and campaign organizing — among others.

The latest cohort of companies to receive backing Higher Ground Labs

“It is vitally important that Democrats learn to do their campaigns online,” says Dutta. “The way you recruit volunteers; the way you poll sentiment; the way you target and mobilize voters has to be done with online tools and has to improve in the progressive movement and that’s the job of Higher Ground Labs to fix.”

For-profit companies have a critical role to play in election organizing and mobilization, Dutta says. Thanks to government regulation, only private companies are allowed to trade data across organizations and causes (provided they do it at fair market value). That means advocacy groups, unions and others can tap the information these companies collect — for a fee.

The Democratic Party already has one highly valued private company that it uses for its technology services. Formed from the merger of NGP Software and Voter Activation Network, two companies that got their start in the late 1990s and early 2000s, NGP VAN is the largest software and technology services provider for Democratic campaigns. It’s also a highly valued company, which received roughly $100 million in financing last year from the private equity firm Insight Venture Partners, according to people familiar with the investment. Terms of the deal were not disclosed.

“Our vision has been to build a platform that would break down the painful data silos that exist in the campaigns and nonprofit space, and to offer truly best-in-class digital, fundraising and organizing features that could serve both the largest and the smallest nonprofits and campaigns, all with one unified CRM,” wrote Stu Trevelyan, the chief executive of NGP VAN + EveryAction, in an August blogpost announcing the investment. “We’re so excited that others, like our new partners at Insight, share that vision, and we can’t wait to continue innovating and growing together in the coming years.”

Even as private equity dollars boost the firepower of organizations like NGP VAN, venture capitalists are financing several companies from the Higher Ground Labs portfolio.

Civis Analytics, a startup founded by the former chief analytics officer of Barack Obama’s 2012 reelection campaign, raised $22 million from outside investors, and counts Higher Ground Labs among its backers. Qriously, another Higher Ground Labs portfolio company, was acquired by Brandwatch, as was GroundBase, a messaging platform acquired by the nonprofit progressive advocacy organization ACRONYM.

Other companies in the portfolio are also attracting serious attention from investors. Standouts like Civis Analytics and Hustle, which raised $30 million last May, show that investors are buying into the proposition that these companies can build lasting businesses serving Democratic and progressive political campaigns and corporate businesses that would also like to rally employees or personalize a marketing pitch to customers.

These are companies like Change Research, an earlier-stage company that just launched from Higher Ground Labs accelerator last year. That company, founded by Mike Greenfield, a serial Silicon Valley entrepreneur who was the first data scientist working on the problem of fraud detection at PayPal, and Pat Reilly, a communications professional who worked with state and local Democratic politicians, is slashing the cost of political polling.

“I wanted to do something for American democracy to try and improve the state of things,” Greenfield said in an interview last year.

For Greenfield, that meant increasing access to polling information. He cited the test case of a Kansas special election in a district that Donald Trump had won by 27 points. Using his own proprietary polling data, Greenfield predicted that the Democratic challenger, James Thompson, would pose a significant threat to his Republican opponent, Mike Estes.

Estes went on to a 7% victory at the ballot, but Thompson’s campaign did not have access to polling data that could have helped inform his messaging and — potentially — sway the election, said Greenfield.

“Public opinion is used to ween out who can be most successful based on how much money they’re able to raise for a poll,” says Reilly. It’s another way that electoral politics is skewed in favor of the people with disposable income to spend what is a not-insignificant amount of money on campaigns.

Polls alone can cost between $20,000 to $30,000 — and Change Research has been able to cut that by 80% to 90%, according to the company’s founders.

“It’s safe to say that most of the world was stunned by the outcome [of the presidential election] because most polls predicted the opposite,” says Greenfield. “Being a good American and as a parent of a 10-year-old and a 12-year-old, providing forward-thinking candidates and causes with the kind of insight they needed to win up and down the ballot could not only be a good business, but really help us save our democracy.”

Change Research isn’t just polling for politicians. Last year, the company conducted roughly 500 polls for political candidates and advocacy groups.

“The way that I’ve described Change Research to investors is that we want to simultaneously move the world in a better direction and having a positive impact while building a substantial business,” says Greenfield. “We’re only going to work with candidates and causes that we’re aligned with.”

Being exclusively focused on progressive causes isn’t the liability that many in the broader business community would think, says Dutta. Many Democratic organizations won’t work with companies that sell services to both sides of the aisle.

For Higher Ground Labs, a stipulation for receiving their money is a commitment not to work with any Republican candidate. Corporations are okay, but conservative causes and organizations are forbidden.

“We’re in a moment of existential crisis in America and this Republican party is deeply toxic to the health and future of our country,” says Dutta. “The only path out of this mess is to vote Republicans out of office and to do that we need to make it easier for good candidates to run for office and to engage a broader electorate into voting regularly.”

Powered by WPeMatico

Hello Alfred — the startup that assigns in-home assistants to take care of your recurring chores and tasks — has announced the launch of a new service tier that will provide more properties and residents with access to the company’s underlying technology.

The company, which won the Startup Battlefield competition at our 2014 Disrupt event in San Francisco, looks to unlock valuable time for users by handling the long list of small routine items that add up over the course of a week and still require human oversight.

Hello Alfred partners with building owners to provide residents with dedicated home managers that assist with various errands and on-request services, such as apartment cleaning, grocery delivery, laundry services, prescription refills and more. Users have a direct line of communication with the company’s hospitality team through Hello Alfred’s mobile app, where they can manage tasks and set recurring appointments.

The new platform, “Powered by Alfred,” acts as a fairly similar but more accessible alternative to the company’s current offering. Residents in buildings equipped with “Powered by Alfred” are given access to all of the company’s solutions with the exception of the weekly visits from dedicated home managers currently included in the existing service. By excluding the dedicated in-home service, Hello Alfred is able to offer its new service tier at a lower price point and integrate with more buildings faster.

Property owners using “Powered by Alfred” can customize packages to include the services that best fit the needs of their residents and can upgrade or change service levels at any time. Both residents and building owners using the new platform are also given more control and direct access to Hello Alfred’s proprietary technology, allowing users to control functions that normally fall under the purview of the company’s dedicated home managers.

Additionally, with the launch of the new offering, Hello Alfred will be consolidating its various solutions under one central app, where residents and building managers can handle all inquiries, appointments and payments.

Hello Alfred’s new service tier, “Powered by Alfred,” provides a single, shared access point for resident and property owners to manage inquiries and drive property performance / Hello Alfred Press Kit

The launch of “Powered by Alfred” seems to be a natural evolution for the company, which seeks to make its offering more accessible to all residents of all backgrounds.

Hello Alfred previously employed a consumer-facing business model, in which customers would pay a monthly subscription fee for the array of in-home services and access to the company’s team of hospitality specialists, referred to as Alfreds.

However, around the time of the startup’s Series B round, Hello Alfred adopted the model of partnering directly with property owners to offer its services complimentary to residents. The partnership structure was not only a more conducive model for scaling but also enabled the company to offer the same services to any resident in an Alfred-equipped building, regardless of socioeconomic status.

Hello Alfred quickly built up a sizeable backlog of property owners hoping to integrate the platform into their units, according to the company. However, the task of maintaining dedicated staffing for every unit in every location made it difficult for the Alfred team to satisfy its swelling demand, having to instead focus resources primarily on luxury properties.

With “Powered by Alfred” removing in-home management services, the company has been able to improve accessibility and better satisfy the market’s appetite for its services, now rolling out the offering to non-luxury buildings and properties that previously sat in its pipeline.

Behind the launch of the new platform — which the company has piloted over the course of several months — Hello Alfred has increased its market share by more than 50 percent, with its services now available in more than 150,000 residential properties.

“We want Alfred to be a utility. We want to make “help” a universal utility and make it something anyone can access,” Hello Alfred CEO and co-founder Marcela Sapone told TechCrunch. “We wanted to find a way where we could accelerate growth and get human-focused help into urban buildings to help most urban environments.”

The launch represents the latest step in Hello Alfred’s broader expansion plans, which appear to have ramped up in recent months. Hello Alfred is now active in 16 cities — including Houston, where the company plans to launch next week — with its new offering available across all of its active markets. The startup already boasts an impressive partnership roster that includes more than 20 of the largest property owners in the U.S., and the Alfred team expects its new offering to open up further opportunities for partnerships across different property classes and different stages of a resident’s life cycle.

“As WeWork transformed commercial real estate, Hello Alfred is transforming residential real estate, and redefining what it means to live in a city today,” said Sapone. “This business expansion allows us to not only satisfy increasing demand for our service, but to connect every part of the resident experience — from the moment you sign your lease, until the moment you move to another Hello Alfred building.”

To date, the company has raised just over $63.5 million in venture capital, according to data from PitchBook, from prestigious investment brands that include New Enterprise Associates, Spark Capital, SV Angel, Moderne Ventures, Invesco and others.

Powered by WPeMatico

A YC startup called GBatteries has come out of stealth with a bold claim: they can recharge an electric car as quickly as it takes to fill up a tank of gas.

Created by aerospace engineer Kostya Khomutov, electrical engineers Alex Tkachenko and Nick Sherstyuk, and CCO Tim Sherstyuk, the company is funded by the likes of Airbus Ventures, Initialized Capital, Plug and Play and SV Angel.

The system uses AI to optimize the charging systems in electric cars.

“Most companies are focused on developing new chemistries or materials (ex. Enevate, Storedot) to improve charging speed of batteries. Developing new materials is difficult, and scaling up production to the needs of automotive companies requires billions of $,” said Khomutov. “Our technology is a combination of software algorithms (AI) and electronics, that works with off-the-shelf Li-ion batteries that have already been validated, tested, and produced by battery manufacturers. Nothing else needs to change.”

The team makes some bold claims. The product allows users to charge a 60kWh EV battery pack with 119 miles of range in 15 minutes as compared to 15 miles in 15 minutes today. “The technology works with off-the-shelf lithium ion batteries and existing fast charge infrastructure by integrating via a patented self-contained adapter on a car charge port,” writes the team. They demonstrated their product at CES this year.

Most charging systems depend on fairly primitive systems for topping up batteries. Various factors — including temperature — can slow down or stop a charge. GBatteries manages this by setting a very specific charging model that “slows down” and “speeds up” the charge as necessary. This allows the charge to go much faster under the right conditions.

The company bloomed out of frustration.

“We’ve always tinkered with stuff together since before I was even a teenager, and over time had created a burgeoning hardware lab in our basement,” said Tim Sherstyuk. “While I was studying Chemistry at Carleton University in Ottawa, we’d often debate and discuss why batteries in our phones got so bad so rapidly — you’d buy a phone, and a year later it would almost be unusable because the battery degraded so badly.”

“This sparked us to see if we can solve the problem by somehow extending the cycle life of batteries and achieve better performance, so that we’d have something that lasts. We spent a few weeks in our basement lab wiring together a simple control system along with an algorithm to charge a few battery cells, and after 6 months of testing and iterations we started seeing a noticeable difference between batteries charged conventionally, and ones using our algorithm. A year and a half later of constant iterations and development, we applied and were accepted in 2014 into YC.”

While it’s not clear when this technology will hit commercial vehicles, it could be the breakthrough we all need to start replacing our gas cars with something a little more environmentally friendly.

Powered by WPeMatico

The working class of the United States doesn’t get many breaks these days. It’s not just a function of low pay and long hours, but also the incredible uncertainty of income and expenses that makes surviving week-to-week so challenging. One in five Americans have a negative net wealth, even in an economy where the unemployment rate is the lowest in almost two decades. Banks, meanwhile, are actively dissuading the working class from banking with them, creating a permanent class of unbanked and underbanked citizens.

For Jon Schlossberg, CEO and co-founder of Even.com, improving the plight of ordinary Americans and their finances is a deeply personal and professional mission. And now that mission has a huge new bucket of capital behind it, with Keith Rabois of Khosla Ventures leading a $40 million Series B round into the Oakland-based startup. Rabois is a return investor, having previously backed the company in its late 2014 seed round. With this latest round of capital, Even.com has now raised $50.5 million.

When Even.com first launched its eponymous app, the goal was to offer income smoothing for workers, helping them avoid usurious payday loans to make ends meet. Since that first launch several years ago, Schlossberg and his team learned that the only way to improve the finances for the working class is to help them budget better — ending the need for loans in the first place. “To do anything with your life, unless you are just born to the right family, you need to spend your money wisely, but we never teach you how to do that,” Schlossberg explained to me.

Last year, Even.com announced that it had stopped evening through its Pay Protection product. Instead, Schlossberg said that Even.com has evolved and wanted to “build a new kind of financial institution with products that fit your life.” It still has a feature it brands as Instapay, which allows users to request their earned pay in advance of their payday.

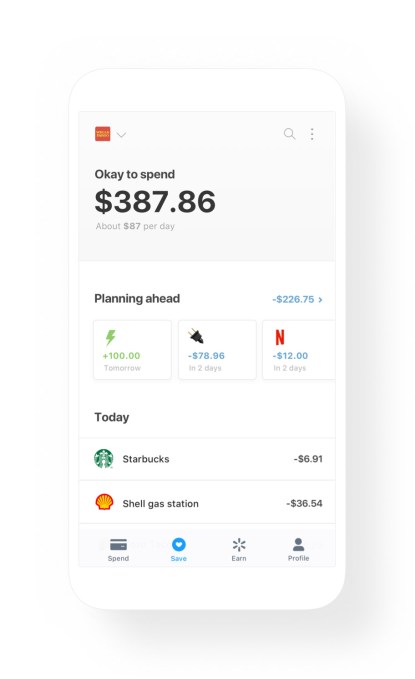

But Even.com is increasingly focused on improving the quality of its intelligent budgeting feature. Using artificial intelligence models honed over the past few years, the company now gives users of its Even app an “Okay to spend” figure that helps them think through their cash flow. By giving a predictive figure rather than a checking account balance, Even can help its users avoid sudden surprise expenses that can trigger the kind of financial death spiral that has become a familiar story in America. The company will also soon launch an automatic savings feature similar to Digit or Acorns that helps people build up regular savings.

Even’s Okay to spend feature gives insight into future cash flows before it is too late

While the company offers an increasingly comprehensive suite of financial tools, it has decided to avoid charging users specific use fees, opting instead for a subscription model. Schlossberg explained that “We are a mission-oriented company, but talk is cheap and where the rubber hits the road, it’s how you make money.” Even is free for users participating through partner employers, or $2.99 a month for individuals without a sponsor.

The company’s highest expense feature is Instapay due to underwriting, and so the company makes higher profits when fewer of its customers need access to payday credit. In other words, the better that its users budget, the fewer loans it will underwrite, and the more money the company makes. We are “directly incentivized to help people with their financial health,” Schlossberg noted.

Even has proven attractive to corporate customers, including Walmart, which partnered with the startup last December to offer its service to all 1.4 million employees at the retailer. Since the launch of that partnership, more than 200,000 Walmart employees regularly use the app, according to Even, and the typical active user checks their Okay to spend balance four times a week. A majority of active users have also taken out an Instapay through Even.

More interestingly, salaried employees at Walmart used the app slightly more than hourly workers, proving that just having a guaranteed income isn’t necessarily a panacea to financial trouble for many American households.

Even.com’s Series B round is all about expansion and growth for the company. Even intends to open an East Coast office this year, and intends to expand its product further into the Fortune 500 with partnerships similar to its Walmart deal. The company currently has 37 employees. In addition to Khosla, the startup raised funding from Valar Ventures, Allen & Company, Harrison Metal, SV Angel, Silicon Valley Bank and others.

Powered by WPeMatico