stripe

Auto Added by WPeMatico

Auto Added by WPeMatico

Venture capital investment exploded across a number of geographies in 2019 despite the constant threat of an economic downturn.

San Francisco, of course, remains the startup epicenter of the world, shutting out all other geographies when it comes to capital invested. Still, other regions continue to grow, raking in more capital this year than ever.

In Utah, a new hotbed for startups, companies like Weave, Divvy and MX Technology raised a collective $370 million from private market investors. In the Northeast, New York City experienced record-breaking deal volume with median deal sizes climbing steadily. Boston is closing out the decade with at least 10 deals larger than $100 million announced this year alone. And in the lovely Pacific Northwest, home to tech heavyweights Amazon and Microsoft, Seattle is experiencing an uptick in VC interest in what could be a sign the town is finally reaching its full potential.

Seattle startups raised a total of $3.5 billion in VC funding across roughly 375 deals this year, according to data collected by PitchBook. That’s up from $3 billion in 2018 across 346 deals and a meager $1.7 billion in 2017 across 348 deals. Much of Seattle’s recent growth can be attributed to a few fast-growing businesses.

Convoy, the digital freight network that connects truckers with shippers, closed a $400 million round last month bringing its valuation to $2.75 billion. The deal was remarkable for a number of reasons. Firstly, it was the largest venture round for a Seattle-based company in a decade, PitchBook claims. And it pushed Convoy to the top of the list of the most valuable companies in the city, surpassing OfferUp, which raised a sizable Series D in 2018 at a $1.4 billion valuation.

Convoy has managed to attract a slew of high-profile investors, including Amazon’s Jeff Bezos, Salesforce CEO Marc Benioff and even U2’s Bono and the Edge. Since it was founded in 2015, the business has raised a total of more than $668 million.

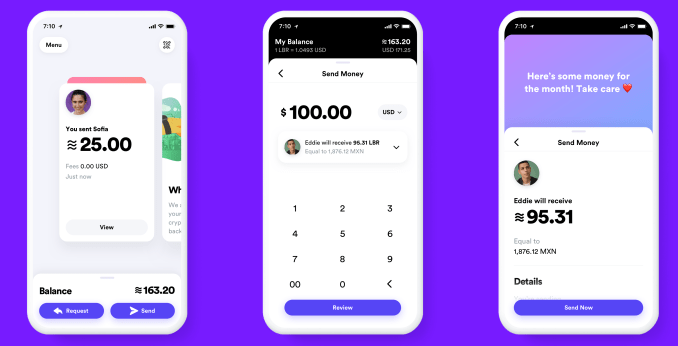

Remitly, another Seattle-headquartered business, has helped bolster Seattle’s startup ecosystem. The fintech company focused on international money transfer raised a $135 million Series E led by Generation Investment Management, and $85 million in debt from Barclays, Bridge Bank, Goldman Sachs and Silicon Valley Bank earlier this year. Owl Rock Capital, Princeville Global, Prudential Financial, Schroder & Co Bank AG and Top Tier Capital Partners, and previous investors DN Capital, Naspers’ PayU and Stripes Group also participated in the equity round, which valued Remitly at nearly $1 billion.

Up-and-coming startups, including co-working space provider The Riveter, real estate business Modus and same-day delivery service Dolly, have recently attracted investment too.

A number of other factors have contributed to Seattle’s long-awaited rise in venture activity. Top-performing companies like Stripe, Airbnb and Dropbox have established engineering offices in Seattle, as has Uber, Twitter, Facebook, Disney and many others. This, of course, has attracted copious engineers, a key ingredient to building a successful tech hub. Plus, the pipeline of engineers provided by the nearby University of Washington (shout-out to my alma mater) means there’s no shortage of brainiacs.

There’s long been plenty of smart people in Seattle, mostly working at Microsoft and Amazon, however. The issue has been a shortage of entrepreneurs, or those willing to exit a well-paying gig in favor of a risky venture. Fortunately for Seattle venture capitalists, new efforts have been made to entice corporate workers to the startup universe. Pioneer Square Labs, which I profiled earlier this year, is a prime example of this movement. On a mission to champion Seattle’s unique entrepreneurial DNA, Pioneer Square Labs cropped up in 2015 to create, launch and fund technology companies headquartered in the Pacific Northwest.

Boundless CEO Xiao Wang at TechCrunch Disrupt 2017

Operating under the startup studio model, PSL’s team of former founders and venture capitalists, including Rover and Mighty AI founder Greg Gottesman, collaborate to craft and incubate startup ideas, then recruit a founding CEO from their network of entrepreneurs to lead the business. Seattle is home to two of the most valuable businesses in the world, but it has not created as many founders as anticipated. PSL hopes that by removing some of the risk, it can encourage prospective founders, like Boundless CEO Xiao Wang, a former senior product manager at Amazon, to build.

“The studio model lends itself really well to people who are 99% there, thinking ‘damn, I want to start a company,’ ” PSL co-founder Ben Gilbert said in March. “These are people that are incredible entrepreneurs but if not for the studio as a catalyst, they may not have [left].”

Boundless is one of several successful PSL spin-outs. The business, which helps families navigate the convoluted green card process, raised a $7.8 million Series A led by Foundry Group earlier this year, with participation from existing investors Trilogy Equity Partners, PSL, Two Sigma Ventures and Founders’ Co-Op.

Years-old institutional funds like Seattle’s Madrona Venture Group have done their part to bolster the Seattle startup community too. Madrona raised a $100 million Acceleration Fund earlier this year, and although it plans to look beyond its backyard for its newest deals, the firm continues to be one of the largest supporters of Pacific Northwest upstarts. Founded in 1995, Madrona’s portfolio includes Amazon, Mighty AI, UiPath, Branch and more.

Voyager Capital, another Seattle-based VC, also raised another $100 million this year to invest in the PNW. Maveron, a venture capital fund co-founded by Starbucks mastermind Howard Schultz, closed on another $180 million to invest in early-stage consumer startups in May. And new efforts like Flying Fish Partners have been busy deploying capital to promising local companies.

There’s a lot more to say about all this. Like the growing role of deep-pocketed angel investors in Seattle have in expanding the startup ecosystem, or the non-local investors, like Silicon Valley’s best, who’ve funneled cash into Seattle’s talent. In short, Seattle deal activity is finally climbing thanks to top talent, new accelerator models and several refueled venture funds. Now we wait to see how the Seattle startup community leverages this growth period and what startups emerge on top.

Powered by WPeMatico

One of the biggest trends in the world of financial technology has been an ongoing push towards consolidation, where larger fish are snapping up smaller fish (including a proliferation of interesting startups) to get improved economies of scale in a business model where every transaction brings incremental returns. But today, a startup that has built the concept of consolidation into its basic DNA has raised another round of funding to continue doubling down on its business.

Rapyd — a London-based startup that has built an API that lets customers tap into a range of financial services spanning payments, checkout, funds collection, fund disbursements, compliance as a service, foreign exchange, card issuing and soon logistics across a wide range of geographies — has picked up an additional $20 million. Rapyd’s valuation with the funding is now at $1.2 billion (up from just under $1 billion in October).

The $20 million comes from new investment firm Durable Capital Partners.

Notably, it was only in October that Rapyd announced a $100 million raise. CEO and co-founder and Arik Shtilman said that Rapyd has now raised $180 million in total, with previous investors in the startup including Oak HC/FT Tiger Global, Coatue, General Catalyst, Target Global, Stripe and Entrée Capital. (Stripe, itself a fast-growing fintech upstart, remains only a financial investor in the company, Shtilman confirmed.)

Durable is the firm founded by Henry Ellenbogen, formerly a star investor at T. Rowe Price, in what Rapyd said was the firm’s first investment. (Note: Durable was also announced earlier as an investor in Convoy’s $400 million round, some clear signs that it’s open for business now.)

With Rapyd only recently raising a round, Shtilman said that the reason for the — err — rapid follow up was because the company is gearing up to make some acquisitions, as it too moves in on the consolidation trend by adding in more tools into its “Swiss Army Knife” of services.

“We’ve started to look at two acquisitions that were bigger than what we originally planned, with prices more in the range of $100 million,” he said. Up to now, Rapyd has largely built its technology from the ground up, but this will be about “getting at new business very quickly,” he added. Both deals are in progress now and are likely to close in February / March. One is of a card issuing platform (a la Marqeta), and the other is of a company based in Asia Pacific that is a significant player in payments in the region.

The focus on Asia Pacific both for testing out new services and acquisitions is in part because this, along with Latin America, have shaped up to be important geographies for the company. In the last three months, Rapyd has signed on 20 additional large-scale companies, Shtilman said, with several of them based out of, or serving, customers out of the two regions.

In fact, Rapyd doesn’t talk much about actual customers, but they include e-commerce merchants, gig-economy platforms — including Uber — financial institutions, and technology providers. The basic pitch is that financial services are complex, and providing one like payments often means having to offer others. Building these from scratch if this is not your core competency can be time-consuming and costly, and so that is where a company like Rapyd steps in with its API.

This is what attracted its newest investor, too. “Durable Capital Partners LP has a vision to identify and invest in promising early stage growth companies and invest in teams that have bold ideas but can also execute at a world-class level and build much larger companies,” said Ellenbogen in a statement. “I believe the Fintech-as-a-Service category has tremendous potential as companies seek to embed financial services as an integral part of the next generation technology stack. I believe Rapyd is very well positioned to drive this trend and I believe Arik’s track record in scaling cloud-based businesses will deliver success in this sector.”

When we last talked with Rapyd in October, we asked Shtilman about whether the company would ever move into logistics as part of its range of tools. After all, when you think about the complexities of procuring, storing and moving goods, it’s clear that logistics is one of the cornerstones you need to get right in an online business.

He said that this was on the company’s roadmap, and now Rapyd is in a pilot in Indonesia — an interesting test bed, considering that the country’s is spread across thousands of islands — where it has integrated a logistics service and given access to a single merchant as stage one of its closed beta. It’s also in discussions with other companies about how it can incorporate their services into the Rapyd platform to provide further “logistics as a service” to customers. He also confirmed the Durable has been a help here, by making an introduction to Convoy as part of that wider strategy.

Powered by WPeMatico

There’s a strategic cost to the defection of Visa, Stripe, eBay, and more from the Facebook -led cryptocurrency Libra Association . They’re not just names dropping off a list. Each potentially made Libra more useful, ubiquitous, or reputable. Now they could become obstacles to the token’s launch or growth.

Fearing regulators’ inquiries not just into their Libra involvement but the rest of their businesses, these companies are pulling out at least for now. None had made precise commitments to integrating Libra into their products, and they’ve said they could still get involved later. But their exit clouds the project’s future and leaves Facebook to absorb more of the blowback.

Here’s what each of the departing Libra Association members brought to the table and how they could spawn new challenges for the cryptocurrency:

With one of most widely-accepted payment methods, Visa could have helped make Libra universally spendable. It’s also one of the most prestigious names in finance, lending deep credibility to the project. Visa’s departure leaves Libra looking more like tech companies barging into payments, conjuring fears of their move fast, break things approach that could cause financial ruin if Libra runs into problems. It also could leave Libra with a much weaker presence in brick-and-mortar shops. No one will want to own a cryptocurrency that doesn’t appreciate in value and can’t be easily spent.

The involvement of MasterCard alongside Visa made Libra look like the incumbents adapting to modern technologies. This made it less threatening, and gave cryptocurrency an air of inevitability. MasterCard would have also brought an even wider network of locations where Libra could one day be used for payment. Now MasterCard and Visa might actively work against Libra to prevent their payment methods being made obsolete by Libra and its elimination of transaction fees through the blockchain. Two of Libras biggest allies could become its biggest foes.

Facebook has repeatedly told regulators that its Calibra app plus integrations into Messenger and WhatsApp would not be the only Libra wallets, pointing to PayPal . Facebook’s head of Libra David Marcus told Congress when asked about the social network’s outsized power to exploit Libra through its own Calibra wallet that “you have companies like PayPal and others that will, of course, collaborate, but [also] compete with us”. Now Facebook won’t have a scaled payment method it doesn’t own to point to as a likely alternative for people who don’t want to trust Facebook’s Calibra, Messenger, or WhatsApp to be their Libra wallet. The Libra Association also loses PayPal’s enormous network of online merchants that accept it, plus the inroad to integration into its peer-to-peer payback app Venmo. PayPal convinced the mainstream public to trust online payments — the exact kind of trust Facebook desperately needs. The fact that Marcus was also the former president of PayPal but couldn’t keep it in the association raises concerns about the group’s coalition-building prowess.

Stripe’s enormous popularity with ecommerce vendors made it a valuable Libra Association member. Together with PayPal, Stripe facilitates a huge portion of online transactions outside of China. Its ease of integration made it a top pick for developers Facebook surely hoped would build atop Libra. Stripe’s exit destroys a critical bridge to the fintech startup ecosystem that could have helped institutionalize Libra. Now the association will have to work on engineering payment widgets from scratch without Stripe’s assistance, which could slow adoption if it ever launches.

There’s a clear reason all these payment processors bailed. Senators Brian Schatz (D-HI) and Sherrod Brown (D-OH) wrote a letter to Visa, MasterCard, and Stripe’s CEOs this week explaining that “If you take this on, you can expect a high level of scrutiny from regulators not only on Libra-related activities, but on all payment activities.”

As one of the longest standing ecommerce companies, eBay bolstered beliefs that Libra could be used to power transactions between untrusted strangers without a costly middleman. It might have also put Libra into practice on one of the top western online marketplaces outside of Amazon. Without destinations like eBay onboard, average netizens will have fewer opportunities to be exposed to Libra’s potential to eliminate transaction fees.

One of the lesser-known Libra Association members, Mercado Pago helps merchants receive payments via email or in installments. The idea of connecting financially underserved populations has been core to Facebook’s pitch for why Libra should exist. The Libra Association has been light on the details of how exactly it serves this demographic, relying on the inclusion of partners like Mercado Pago to help it figure this out later. Mercado Pago’s departure leaves Libra looking more like a financial power grab rather than a tool to assist the disadvantaged.

On Monday, the remaining Libra Association members will meet to finalize the initial member list, elect a board, and create a charter to govern the project. This forced the hands of the companies above, who had their last chance to depart this week before being pulled deeper into Libra.

UNITED STATES – JULY 16: David Marcus, head of Facebook’s Calibra digital wallet service, prepares to testify during the Senate Banking, Housing and Urban Affairs Committee hearing on “Examining Facebook’s Proposed Digital Currency and Data Privacy Considerations” on Tuesday, July 16, 2019. (Photo By Bill Clark/CQ Roll Call)

Who’s left includes venture capital firms, ride sharing companies, non-profits, and cryptocurrency companies. They are less tied up with the status quo of payment processing, and therefore had less to lose. The blockchain-specific companies were likely hoping to piggyback on financial giants like Visa to get Libra approved and create more legitimacy for their industry as a whole.

These partners could help fund an ecosystem of Libra developers, create daily use cases, spread the system in the developing world, and push for alliances between Libra and cryptocurrency players. Facebook will need to fight to keep them aboard if it wants to avoid Libra looking like a unilateral disruption of the economy.

For Libra to actually launch, Facebook needs to make serious concessions and divert from its initial vision. Otherwise if it continues to butt heads with regulators, more members could flee. One option floated by Libra Association member Andreessen Horowitz’s a16z Crypto partner Chris Dixon was for Libra to be denominated in US dollars instead of a basket of international currencies. That might lessen fears that Libra intends to compete directly with the dollar.

It’s become apparent that Facebook will not get its ideal cryptocurrency out the door. This is the brand tax of 100 scandals coming back to bite it. Now the best it can hope for is to get even a watered-down version launched, prove it can actually help the underbanked, and then hope to convince regulators it’s well-intentioned.

Powered by WPeMatico

After a week of launching new services to bring payments giant Stripe into the areas of lending and credit, the company is announcing another big step forward to fuel its growth: it’s raising another $250 million in funding at a pre-money valuation of $35 billion, money to fuel more international expansion, launching more products and targeting larger enterprise-sized businesses.

This is a huge jump in valuation for the company: Stripe was valued at $22.5 billion earlier this year when it raised $100 million.

The startup said that General Catalyst, Andreessen Horowitz and Sequoia are all in the round already. We’ve also heard that SoftBank had been considering an investment. “It was a big miss when SoftBank didn’t invest two years ago,” one source close to the VC said to TechCrunch. But we’ve confirmed also with John Collison — the president of Stripe who co-founded the company with his brother Patrick (who is the CEO) — that SoftBank is not in this round.

Nor will there be any corporate strategics involved in this round. Of note, Collison today confirmed that the bank providing the financial backing for its new cash advance and corporate card services is Celtic Bank, based in Salt Lake City. But the bank is not taking a strategic investment in the company as part of that deal.

Although the round is not yet closed, Collison said the $250 million size is unlikely to change. The round should close in the next several weeks, he added.

Stripe has long been reluctant to talk about when it might consider going public, and this round will put that prospect off even further. “We are still very happy as a private company,” Collison said today. “Our emphasis remans on the long-term opportunities.”

Stripe spent the first several years of its life slowly building up its payments business — which primarily consisted of providing an API to e-commerce businesses so that they could easily integrate a payments option in their apps or websites.

But in more recent years, it’s started to accelerate its growth with a significantly larger range of financial services — notably, now it describes its business as a “Global Payments and Treasury Network.” The latest products — cash advances and credit cards — are coming on the heels of other services that include incorporation services, fraud protection and and more.

All this means not only that the company can diversify its own revenues, but it can differentiate itself from (or, in some cases, offer the same services as) its competitors. Others offering similar services to Stripe’s include PayPal and Adeyn on the payments front, but as it adds more services, it’s also opening new competitive fronts with other rivals, now including Square, Brex and Clearbanc.

While the U.S. remains Stripe’s main market, especially for new launches, it’s getting increasingly global. The company last week expanded its payments out to eight more countries and that is set to expand again to total 40 in the coming months.

The company says it processes “hundreds of billions of dollars a year for millions of businesses worldwide,” although it declines to give specific numbers. Wayfair, Airbnb, Twilio, GitHub and The RealReal are among the kind of “enterprise” customers that it hopes to target more. Indeed, as startups in e-commerce grow into huge businesses, they are turning from being the kinds of small companies that Stripe used to target into the big companies that it now wants to target.

“This comes in the context of the fact that we feel strongly about Stripe’s role in the growing internet economy,” Collison said.

As we have pointed out before, the internet economy, for all its seeming ubiquity, is still a small part of all commerce, which is one reason brick and mortar is likely to be another target for Stripe in the long run, building on the point-of-sale services it already provides — even as the company continues to reap the rewards of its traction in the digital universe.

“Even now, in 2019, less than eight percent of commerce happens online,” said John Collison, president and co-founder of Stripe, in a statement announcing the round. “We’re investing now to build the infrastructure that’ll power internet commerce in 2030 and beyond. If we get it right, we can help the internet fulfill its potential as an engine for global economic progress.”

Updated with comments from John Collison, the co-founder of Stripe

Powered by WPeMatico

Last week, when the popular payments startup Stripe made some waves with its first move into money lending through the launch of Stripe Capital, we reported that the company was also soon going to be launching a credit card. Now, that news is official. Today, the company is doubling down on financing with the launch of corporate cards for business customers.

Announced officially today to coincide with the company’s developer event Stripe Sessions, the Stripe Corporate Card — as the product is officially called — is a Visa that will be open to businesses that are incorporated in the U.S., although they can operate elsewhere.

Notably, users are expected to pay their balance in full each month, so for now there is no interest rate, or fee, to use the card, with Stripe making its money by way of the interchange fee that comes with every transaction using the card.

“We’re not freezing cards based on late or no payments,” Cristina Cordova, the business lead overseeing the launch, said in an interview. “A pretty common reason for non-payment is that a person switched bank accounts and forgot to update the information. But we think we’ll have fewer problems because we have banking information for accepting revenue, by way of our payments business.”

The move is another major step ahead for Stripe as it continues to diversify its business and bring on more financial products to become a one-stop shop for e-commerce and other companies for all the transactions they might need to make in the course of their lives. It is a little ironic that it’s taken years for credit cards to get added into the mix, considering Stripe’s earliest homepages and marketing efforts were built around the design of a credit card (a reference to taking payments online, not issuing credit, of course).

In any case, the list of products now offered by Stripe is long — longer, you might say, than it takes to incorporate a Stripe service into a developer workflow. In addition to its API-based flagship payments product — which is available as a direct service or, via Stripe Connect, for third parties via marketplaces and other platforms — it offers billing and invoicing, in-person payment services (via Terminal), business analytics, fraud prevention on transactions (Radar), company incorporation (Atlas) and a range of content around business strategy.

Some of these Stripe products are free to use, and some come at a price: The main point for offering them together is to build more engagement and loyalty from customers to keep them from migrating to other services. In that regard, credit cards are a cornerstone of how businesses operate, to handle day-to-day expenses in a more accountable way, and this is an area that is already well-served by others, including startups like Brex but also a plethora of challenger and traditional banks. So as much as anything else, this is a clear move to help stave off competition.

At the same time, it underscores how Stripe is leveraging the huge amount of data that it has amassed about its users and payments on the platform: It’s not just about enabling single services, but about using the byproducts of those services — data — to put fuel into new products.

Today, to underscore its global ambitions in that regard, Stripe is adding some expansions to several of its existing products. For example, it will now allow businesses to make payouts in local currencies in 45 countries (an important detail, for example, for marketplaces and network-based companies like ridesharing businesses).

The credit card product will follow a model similar to that of Stripe Capital. As with the lending product, there is a single bank issuing the credit and the card. Amber Feng, head of financial infrastructure for Stripe, confirmed to me that it is actually the same bank that’s providing the cash behind Stripe Capital. Stripe is still declining to name the bank itself, but hints that we may hear more about it soon, which leads me to wonder what news might be coming next.

(Funding perhaps would make sense? The company has raised a whopping $785 million to date and has a valuation of $22.5 billion at the moment. Given that Stripe has made indications that a public listing is not on the cards soon, that might imply, with the launch of these new financing products, that more capital might be raised soon.)

Also similar to Stripe Capital, the underwriting of the card is based on Stripe data. That is to say, business users are verified and approved based on turnover (revenues) as measured by the Stripe payments platform itself; and in cases where applicants are “pre-revenue,” they can be evaluated based on other data sources. For example, if they have used Stripe Atlas to incorporate their businesses, the paperwork supplied for that is used by Stripe to vet the customer’s suitability for a credit card.

Notably, the cards will be delivered in the spirit of instant gratification: If you are applying and get approved, you can within minutes download a virtual card to your Apple Wallet as you await the physical card to arrive in the post.

Stripe is big on data in its own business, and it’s bringing some of that into this product with spending controls that can be set by person and by category; real-time expense reporting by way of texts; rewards of 2% back on spending in the business’s most-used categories; and integration with financial software like QuickBooks and Expensify.

Powered by WPeMatico

While the software revolution started out slowly, over the past few years it’s exploded and the fastest-growing segment to-date has been the shift towards software as a service or SaaS.

SaaS has dramatically lowered the intrinsic total cost of ownership for adopting software, solved scaling challenges and taken away the burden of issues with local hardware. In short, it has allowed a business to focus primarily on just that — its business — while simultaneously reducing the burden of IT operations.

Today, SaaS adoption is increasingly ubiquitous. According to IDG’s 2018 Cloud Computing Survey, 73% of organizations have at least one application or a portion of their computing infrastructure already in the cloud. While this software explosion has created a whole range of downstream impacts, it has also caused software developers to become more and more valuable.

The increasing value of developers has meant that, like traditional SaaS buyers before them, they also better intuit the value of their time and increasingly prefer businesses that can help alleviate the hassles of procurement, integration, management, and operations. Developer needs to address those hassles are specialized.

They are looking to deeply integrate products into their own applications and to do so, they need access to an Application Programming Interface, or API. Best practices for API onboarding include technical documentation, examples, and sandbox environments to test.

APIs tend to also offer metered billing upfront. For these and other reasons, APIs are a distinct subset of SaaS.

For fast-moving developers building on a global-scale, APIs are no longer a stop-gap to the future—they’re a critical part of their strategy. Why would you dedicate precious resources to recreating something in-house that’s done better elsewhere when you can instead focus your efforts on creating a differentiated product?

Thanks to this mindset shift, APIs are on track to create another SaaS-sized impact across all industries and at a much faster pace. By exposing often complex services as simplified code, API-first products are far more extensible, easier for customers to integrate into, and have the ability to foster a greater community around potential use cases.

Graphics courtesy of Accel

Whether you realize it or not, chances are that your favorite consumer and enterprise apps—Uber, Airbnb, PayPal, and countless more—have a number of third-party APIs and developer services running in the background. Just like most modern enterprises have invested in SaaS technologies for all the above reasons, many of today’s multi-billion dollar companies have built their businesses on the backs of these scalable developer services that let them abstract everything from SMS and email to payments, location-based data, search and more.

Simultaneously, the entrepreneurs behind these API-first companies like Twilio, Segment, Scale and many others are building sustainable, independent—and big—businesses.

Valued today at over $22 billion, Stripe is the biggest independent API-first company. Stripe took off because of its initial laser-focus on the developer experience setting up and taking payments. It was even initially known as /dev/payments!

Stripe spent extra time building the right, idiomatic SDKs for each language platform and beautiful documentation. But it wasn’t just those things, they rebuilt an entire business process around being API-first.

Companies using Stripe didn’t need to fill out a PDF and set up a separate merchant account before getting started. Once sign-up was complete, users could immediately test the API with a sandbox and integrate it directly into their application. Even pricing was different.

Stripe chose to simplify pricing dramatically by starting with a single, simple price for all cards and not breaking out cards by type even though the costs for AmEx cards versus Visa can differ. Stripe also did away with a monthly minimum fee that competitors had.

Many competitors used the monthly minimum to offset the high cost of support for new customers who weren’t necessarily processing payments yet. Stripe flipped that on its head. Developers integrate Stripe earlier than they integrated payments before, and while it costs Stripe a lot in setup and support costs, it pays off in brand and loyalty.

Checkr is another excellent example of an API-first company vastly simplifying a massive yet slow-moving industry. Very little had changed over the last few decades in how businesses ran background checks on their employees and contractors, involving manual paperwork and the help of 3rd party services that spent days verifying an individual.

Checkr’s API gives companies immediate access to a variety of disparate verification sources and allows these companies to plug Checkr into their existing on-boarding and HR workflows. It’s used today by more than 10,000 businesses including Uber, Instacart, Zenefits and more.

Like Checkr and Stripe, Plaid provides a similar value prop to applications in need of banking data and connections, abstracting away banking relationships and complexities brought upon by a lack of tech in a category dominated by hundred-year-old banks. Plaid has shown an incredible ramp these past three years, from closing a $12 million Series A in 2015 to reaching a valuation over $2.5 billion this year.

Today the company is fueling an entire generation of financial applications, all on the back of their well-built API.

Graphics courtesy of Accel

Accel’s first API investment was in Braintree, a mobile and web payment systems for e-commerce companies, in 2011. Braintree eventually sold to, and became an integral part of, PayPal as it spun out from eBay and grew to be worth more than $100 billion. Unsurprisingly, it was shortly thereafter that our team decided to it was time to go big on the category. By the end of 2014 we had led the Series As in Segment and Checkr and followed those investments with our first APX conference in 2015.

Plaid, Segment, Auth0, and Checkr had only raised Seed or Series A financings! And we are even more excited and bullish on the space. To convey just how much API-first businesses have grown in such a short period of time, we thought it would be useful perspective to share some metrics over the past five years, which we’ve broken out in the two visuals included above in this article.

While SaaS may have pioneered the idea that the best way to do business isn’t to actually build everything in-house, today we’re seeing APIs amplify this theme. At Accel, we firmly believe that APIs are the next big SaaS wave — having as much if not more impact as its predecessor thanks to developers at today’s fastest-growing startups and their preference for API-first products. We’ve actively continued to invest in the space (in companies like, Scale, mentioned above).

And much like how a robust ecosystem developed around SaaS, we believe that one will continue to develop around APIs. Given the amount of progress that has happened in just a few short years, Accel is hosting our second APX conference to once again bring together this remarkable community and continue to facilitate discussion and innovation.

Graphics courtesy of Accel

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I noted some challenges plaguing mental health tech startups. Before that, I wrote about Zoom and Superhuman’s PR disasters.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you don’t subscribe to Startups Weekly yet, you can do that here.

Anyway, onto the subject on everyone’s mind this week: SoftBank’s second Vision Fund.

Well into the evening on Thursday, SoftBank announced a target of $108 billion for the Vision Fund 2. Yes, you read that correctly, $108 billion. SoftBank indeed plans to raise even more capital for its sophomore vehicle than it did for the record-breaking debut vision fund of $98 billion, which was majority-backed by the government funds of Saudi Arabia and Abu Dhabi, as well as Apple, Foxconn and several other limited partners.

Its upcoming fund, to which SoftBank itself has committed $38 billion, has attracted investment from the National Investment Corporation of National Bank of Kazakhstan, Apple, Foxconn, Goldman Sachs, Microsoft and more. Microsoft, a new LP for SoftBank, reportedly hopped on board with the Japanese telecom giant as part of a grand scheme to convince the massive fund’s portfolio companies to transition to Microsoft Azure, the company’s cloud platform that competes with Amazon Web Services . Here’s more on that and some analysis from TechCrunch editor Jonathan Shieber.

News of the second Vision Fund comes as somewhat of a surprise. We’d heard SoftBank was having some trouble landing commitments for the effort. Why? Well, because SoftBank’s investments have included a wide-range of upstarts, including some uncertain bets. Brandless, a company into which SoftBank injected a lot of money, has struggled in recent months, for example. Wag is said to be going downhill fast. And WeWork, backed with billions from SoftBank, still has a lot to prove.

Here’s everything else we know about The Vision Fund 2:

On to other news…

WeWork is planning a September listing

The company made headlines again this week after word slipped it was accelerating its IPO plans and targeting a September listing. We don’t know much about its IPO plans yet as we are still waiting on the co-working business to unveil its S-1 filing. Whether WeWork can match or exceed its current private market valuation of $47 billion is unlikely. I expect it will pull an Uber and struggle, for quite some time, to earn a market cap larger than what VCs imagined it was worth months earlier.

The consumer financial app made headlines twice this week. The first time because it raised a whopping $323 million at a $7.6 billion valuation. That is a whole lot of money for a business that just raised a similarly sized monster round one year ago. In fact, it left us wondering, why the hell is Robinhood worth $7.6 billion? Then, in a major security faux pas, the company revealed it has been storing user passwords in plaintext. So, go change your Robinhood password and don’t trust any business to value your security. Sigh.

Another day, another huge fintech round

While we’re on the subject on fintech, TechCrunch editor Danny Crichton noted this week the rise of mega-rounds in the fintech space. This week, it was personalized banking app MoneyLion, which raised $100 million at a near unicorn valuation. Last week, it was N26, which raised another $170 million on top of its $300 million round earlier this year. Brex raised another $100 million last month on top of its $125 million Series C from late last year. Meanwhile, companies like payments platform Stripe, savings and investment platform Raisin, traveler lender Uplift, mortgage backers Blend and Better and savings depositor Acorns have also raised massive new rounds this year. Naturally, VC investment in fintech is poised to reach record levels this year, according to PitchBook.

Arianna Huffington, the CEO of Thrive Global, stepped down from Uber’s board of directors this week, a team she had been apart of since 2016. She addressed the news in a tweet, explaining that there were no disagreements between her and the company, rather, she was busy and had other things to focus on. Fair. Benchmark’s Matt Cohler also stepped down from the board this week, which leads us to believe the ride-hailing giant’s advisors are in a period of transition. If you remember, Uber’s first employee and longtime board member Ryan Graves stepped down from the board in May, just after the company’s IPO.

Today I told my fellow @Uber board members that given @Thrive‘s growth, I will no longer be able to give my board duties the attention they deserve, so I will be stepping down. I look forward to watching Uber go from strength to strength! Here is the email I sent to the board: pic.twitter.com/sck0CPLwAV

— Arianna Huffington (@ariannahuff) July 24, 2019

Unity, now valued at $6B, raising up to $525M

Bird is raising a Sequoia-led Series D at $2.5B valuation

SMB payroll startup Gusto raises $200M Series D

Elon Musk’s Boring Company snags $120M

a16z values camping business HipCamp at $127M

An inside look at the startup behind Ashton Kutcher’s weird tweets

Dataplor raises $2M to digitize small businesses in Latin America

While we’re on the subject of amazing TechCrunch #content, it’s probably time for a reminder for all of you to sign up for Extra Crunch. For a low price, you can learn more about the startups and venture capital ecosystem through exclusive deep dives, Q&As, newsletters, resources and recommendations and fundamental startup how-to guides. Here are some of my current favorite EC posts:

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Equity co-host Alex Wilhelm, TechCrunch editor Danny Crichton and I unpack Robinhood’s valuation and argue about scooter startups. Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast and Spotify.

That’s all, folks.

Powered by WPeMatico

Facebook has finally revealed the details of its cryptocurrency, Libra, which will let you buy things or send money to people with nearly zero fees. You’ll pseudonymously buy or cash out your Libra online or at local exchange points like grocery stores, and spend it using interoperable third-party wallet apps or Facebook’s own Calibra wallet that will be built into WhatsApp, Messenger and its own app. Today Facebook released its white paper explaining Libra and its testnet for working out the kinks of its blockchain system before a public launch in the first half of 2020.

Facebook won’t fully control Libra, but instead get just a single vote in its governance like other founding members of the Libra Association, including Visa, Uber and Andreessen Horowitz, which have invested at least $10 million each into the project’s operations. The association will promote the open-sourced Libra Blockchain and developer platform with its own Move programming language, plus sign up businesses to accept Libra for payment and even give customers discounts or rewards.

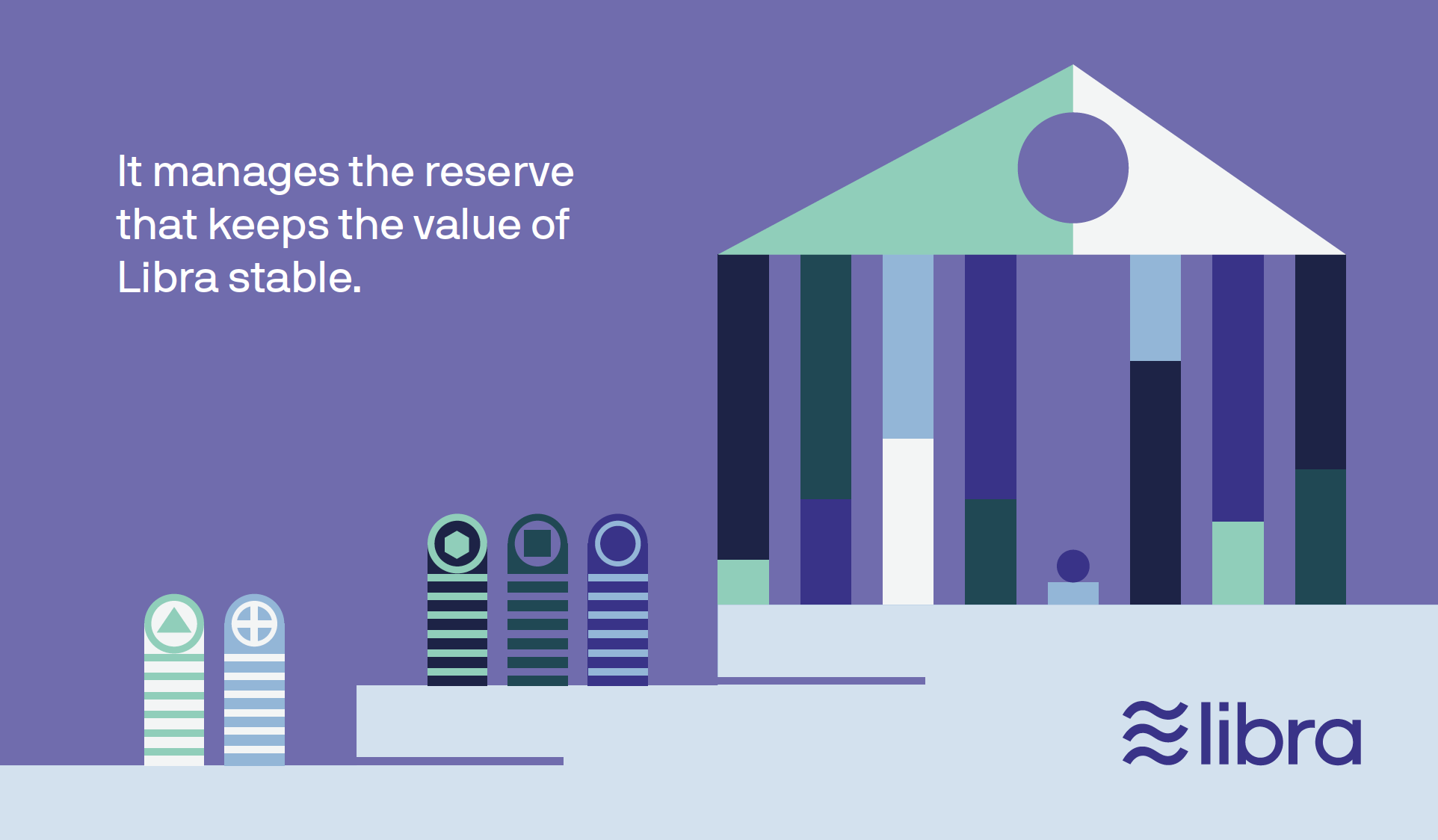

Facebook is launching a subsidiary company also called Calibra that handles its crypto dealings and protects users’ privacy by never mingling your Libra payments with your Facebook data so it can’t be used for ad targeting. Your real identity won’t be tied to your publicly visible transactions. But Facebook/Calibra and other founding members of the Libra Association will earn interest on the money users cash in that is held in reserve to keep the value of Libra stable.

Facebook’s audacious bid to create a global digital currency that promotes financial inclusion for the unbanked actually has more privacy and decentralization built in than many expected. Instead of trying to dominate Libra’s future or squeeze tons of cash out of it immediately, Facebook is instead playing the long-game by pulling payments into its online domain. Facebook’s VP of blockchain, David Marcus, explained the company’s motive and the tie-in with its core revenue source during a briefing at San Francisco’s historic Mint building. “If more commerce happens, then more small businesses will sell more on and off platform, and they’ll want to buy more ads on the platform so it will be good for our ads business.”

In cryptocurrencies, Facebook saw both a threat and an opportunity. They held the promise of disrupting how things are bought and sold by eliminating transaction fees common with credit cards. That comes dangerously close to Facebook’s ad business that influences what is bought and sold. If a competitor like Google or an upstart built a popular coin and could monitor the transactions, they’d learn what people buy and could muscle in on the billions spent on Facebook marketing. Meanwhile, the 1.7 billion people who lack a bank account might choose whoever offers them a financial services alternative as their online identity provider too. That’s another thing Facebook wants to be.

Yet existing cryptocurrencies like Bitcoin and Ethereum weren’t properly engineered to scale to be a medium of exchange. Their unanchored price was susceptible to huge and unpredictable swings, making it tough for merchants to accept as payment. And cryptocurrencies miss out on much of their potential beyond speculation unless there are enough places that will take them instead of dollars, and the experience of buying and spending them is easy enough for a mainstream audience. But with Facebook’s relationship with 7 million advertisers and 90 million small businesses plus its user experience prowess, it was well-poised to tackle this juggernaut of a problem.

Now Facebook wants to make Libra the evolution of PayPal . It’s hoping Libra will become simpler to set up, more ubiquitous as a payment method, more efficient with fewer fees, more accessible to the unbanked, more flexible thanks to developers and more long-lasting through decentralization.

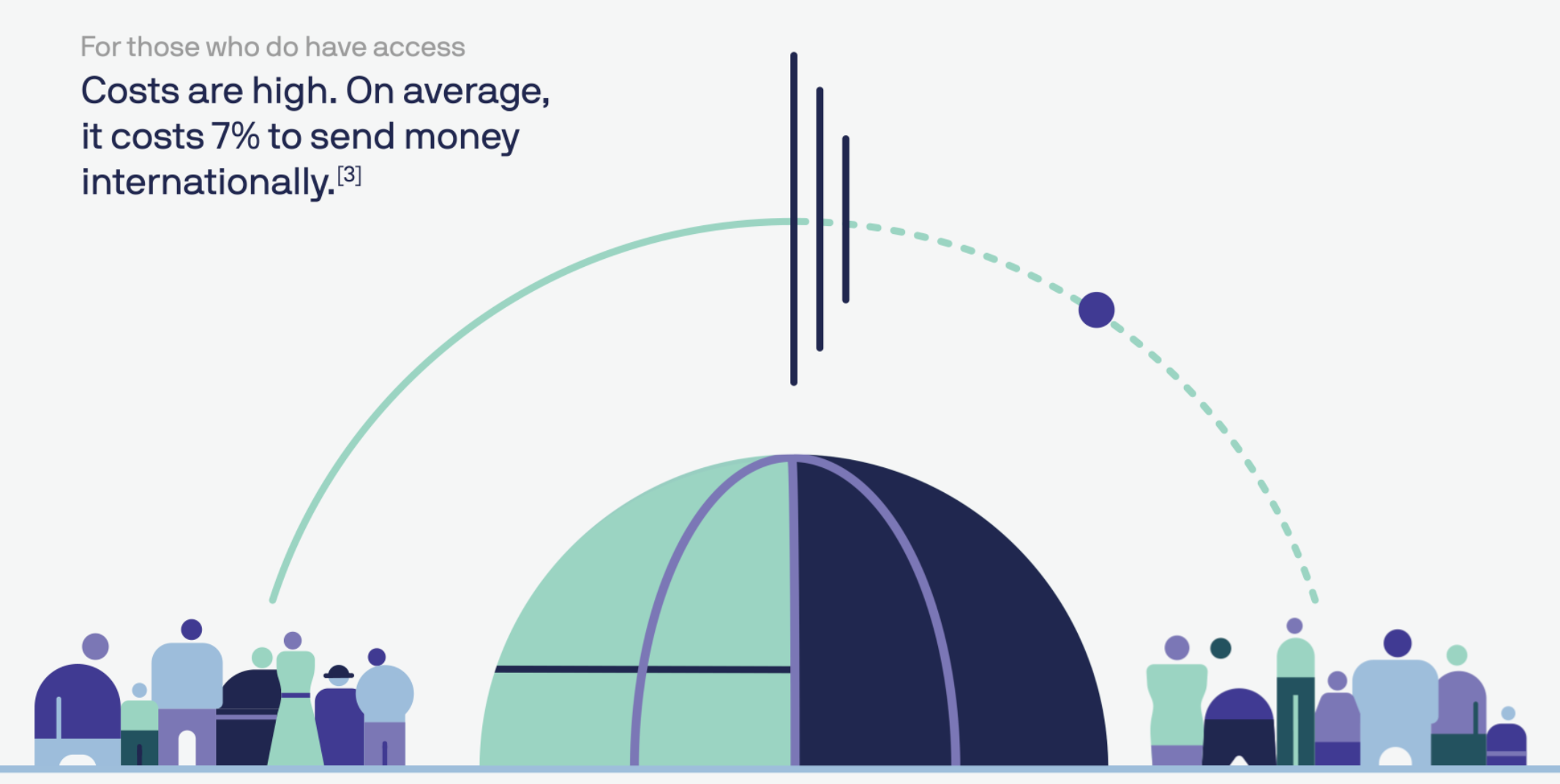

“Success will mean that a person working abroad has a fast and simple way to send money to family back home, and a college student can pay their rent as easily as they can buy a coffee,” Facebook writes in its Libra documentation. That would be a big improvement on today, when you’re stuck paying rent in insecure checks while exploitative remittance services charge an average of 7% to send money abroad, taking $50 billion from users annually. Libra could also power tiny microtransactions worth just a few cents that are infeasible with credit card fees attached, or replace your pre-paid transit pass.

…Or it could be globally ignored by consumers who see it as too much hassle for too little reward, or too unfamiliar and limited in use to pull them into the modern financial landscape. Facebook has built a reputation for over-engineered, underused products. It will need all the help it can get if wants to replace what’s already in our pockets.

By now you know the basics of Libra. Cash in a local currency, get Libra, spend them like dollars without big transaction fees or your real name attached, cash them out whenever you want. Feel free to stop reading and share this article if that’s all you care about. But the underlying technology, the association that governs it, the wallets you’ll use and the way payments work all have a huge amount of fascinating detail to them. Facebook has released more than 100 pages of documentation on Libra and Calibra, and we’ve pulled out the most important facts. Let’s dive in.

Facebook knew people wouldn’t trust it to wholly steer the cryptocurrency they use, and it also wanted help to spur adoption. So the social network recruited the founding members of the Libra Association, a not-for-profit which oversees the development of the token, the reserve of real-world assets that gives it value and the governance rules of the blockchain. “If we were controlling it, very few people would want to jump on and make it theirs,” says Marcus.

Each founding member paid a minimum of $10 million to join and optionally become a validator node operator (more on that later), gain one vote in the Libra Association council and be entitled to a share (proportionate to their investment) of the dividends from interest earned on the Libra reserve into which users pay fiat currency to receive Libra.

The 28 soon-to-be founding members of the association and their industries, previously reported by The Block’s Frank Chaparro, include:

Facebook says it hopes to reach 100 founding members before the official Libra launch and it’s open to anyone that meets the requirements, including direct competitors like Google or Twitter. The Libra Association is based in Geneva, Switzerland and will meet biannually. The country was chosen for its neutral status and strong support for financial innovation including blockchain technology.

To join the association, members must have a half rack of server space, a 100Mbps or above dedicated internet connection, a full-time site reliability engineer and enterprise-grade security. Businesses must hit two of three thresholds of a $1 billion USD market value or $500 million in customer balances, reach 20 million people a year and/or be recognized as a top 100 industry leader by a group like Interbrand Global or the S&P.

Crypto-focused investors must have more than $1 billion in assets under management, while Blockchain businesses must have been in business for a year, have enterprise-grade security and privacy and custody or staking greater than $100 million in assets. And only up to one-third of founding members can by crypto-related businesses or individually invited exceptions. Facebook also accepts research organizations like universities, and nonprofits fulfilling three of four qualities, including working on financial inclusion for more than five years, multi-national reach to lots of users, a top 100 designation by Charity Navigator or something like it and/or $50 million in budget.

The Libra Association will be responsible for recruiting more founding members to act as validator nodes for the blockchain, fundraising to jump-start the ecosystem, designing incentive programs to reward early adopters and doling out social impact grants. A council with a representative from each member will help choose the association’s managing director, who will appoint an executive team and elect a board of five to 19 top representatives.

Each member, including Facebook/Calibra, will only get up to one vote or 1% of the total vote (whichever is larger) in the Libra Association council. This provides a level of decentralization that protects against Facebook or any other player hijacking Libra for its own gain. By avoiding sole ownership and dominion over Libra, Facebook could avoid extra scrutiny from regulators who are already investigating it for a sea of privacy abuses as well as potentially anti-competitive behavior. In an attempt to preempt criticism from lawmakers, the Libra Association writes, “We welcome public inquiry and accountability. We are committed to a dialogue with regulators and policymakers. We share policymakers’ interest in the ongoing stability of national currencies.”

A Libra is a unit of the Libra cryptocurrency that’s represented by a three wavy horizontal line unicode character ≋ like the dollar is represented by $. The value of a Libra is meant to stay largely stable, so it’s a good medium of exchange, as merchants can be confident they won’t be paid a Libra today that’s then worth less tomorrow. The Libra’s value is tied to a basket of bank deposits and short-term government securities for a slew of historically stable international currencies, including the dollar, pound, euro, Swiss franc and yen. The Libra Association maintains this basket of assets and can change the balance of its composition if necessary to offset major price fluctuations in any one foreign currency so that the value of a Libra stays consistent.

A Libra is a unit of the Libra cryptocurrency that’s represented by a three wavy horizontal line unicode character ≋ like the dollar is represented by $. The value of a Libra is meant to stay largely stable, so it’s a good medium of exchange, as merchants can be confident they won’t be paid a Libra today that’s then worth less tomorrow. The Libra’s value is tied to a basket of bank deposits and short-term government securities for a slew of historically stable international currencies, including the dollar, pound, euro, Swiss franc and yen. The Libra Association maintains this basket of assets and can change the balance of its composition if necessary to offset major price fluctuations in any one foreign currency so that the value of a Libra stays consistent.

The name Libra comes from the word for a Roman unit of weight measure. It’s trying to invoke a sense of financial freedom by playing on the French stem “Lib,” meaning free.

The Libra Association is still hammering out the exact start value for the Libra, but it’s meant to be somewhere close to the value of a dollar, euro or pound so it’s easy to conceptualize. That way, a gallon of milk in the U.S. might cost 3 to 4 Libra, similar but not exactly the same as with dollars.

The idea is that you’ll cash in some money and keep a balance of Libra that you can spend at accepting merchants and online services. You’ll be able to trade in your local currency for Libra and vice versa through certain wallet apps, including Facebook’s Calibra, third-party wallet apps and local resellers like convenience or grocery stores where people already go to top-up their mobile data plan.

Each time someone cashes in a dollar or their respective local currency, that money goes into the Libra Reserve and an equivalent value of Libra is minted and doled out to that person. If someone cashes out from the Libra Association, the Libra they give back are destroyed/burned and they receive the equivalent value in their local currency back. That means there’s always 100% of the value of the Libra in circulation, collateralized with real-world assets in the Libra Reserve. It never runs fractional. And unliked “pegged” stable coins that are tied to a single currency like the USD, Libra maintains its own value — though that should cash out to roughly the same amount of a given currency over time.

When Libra Association members join and pay their $10 million minimum, they receive Libra Investment Tokens. Their share of the total tokens translates into the proportion of the dividend they earn off of interest on assets in the reserve. Those dividends are only paid out after Libra Association uses interest to pay for operating expenses, investments in the ecosystem, engineering research and grants to nonprofits and other organizations. This interest is part of what attracted the Libra Association’s members. If Libra becomes popular and many people carry a large balance of the currency, the reserve will grow huge and earn significant interest.

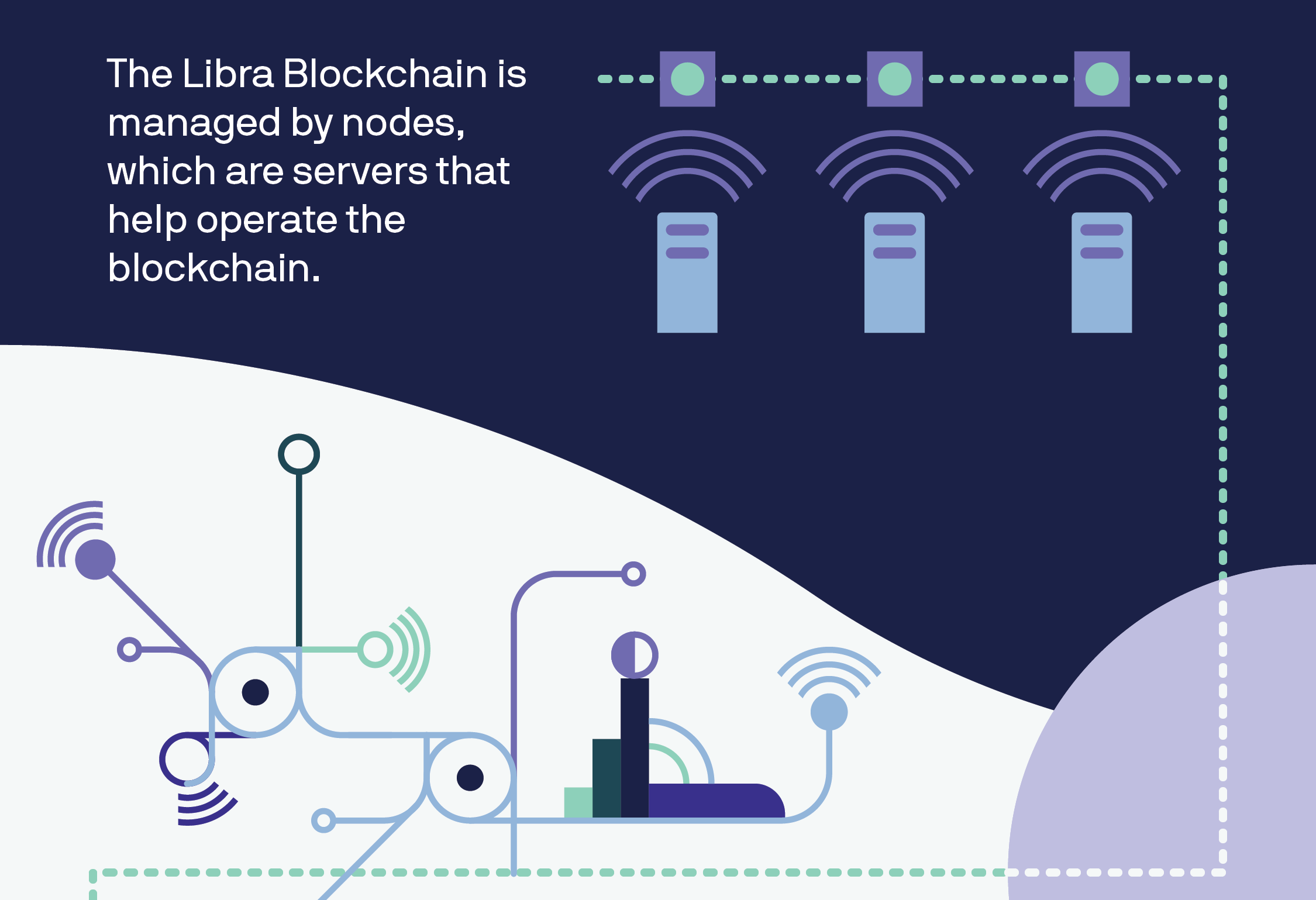

Every Libra payment is permanently written into the Libra Blockchain — a cryptographically authenticated database that acts as a public online ledger designed to handle 1,000 transactions per second. That would be much faster than Bitcoin’s 7 transactions per second or Ethereum’s 15. The blockchain is operated and constantly verified by founding members of the Libra Association, which each invested $10 million or more for a say in the cryptocurrency’s governance and the ability to operate a validator node.

When a transaction is submitted, each of the nodes runs a calculation based on the existing ledger of all transactions. Thanks to a Byzantine Fault Tolerance system, just two-thirds of the nodes must come to consensus that the transaction is legitimate for it to be executed and written to the blockchain. A structure of Merkle Trees in the code makes it simple to recognize changes made to the Libra Blockchain. With 5KB transactions, 1,000 verifications per second on commodity CPUs and up to 4 billion accounts, the Libra Blockchain should be able to operate at 1,000 transactions per second if nodes use at least 40Mbps connections and 16TB SSD hard drives.

Transactions on Libra cannot be reversed. If an attack compromises over one-third of the validator nodes causing a fork in the blockchain, the Libra Association says it will temporarily halt transactions, figure out the extent of the damage and recommend software updates to resolve the fork.

Transactions aren’t entirely free. They incur a tiny fraction of a cent fee to pay for “gas” that covers the cost of processing the transfer of funds similar to with Ethereum. This fee will be negligible to most consumers, but when they add up, the gas charges will deter bad actors from creating millions of transactions to power spam and denial-of-service attacks. “We’ve purposely tried not to innovate massively on the blockchain itself because we want it to be scalable and secure,” says Marcus of piggybacking on the best elements of existing cryptocurrencies.

Currently, the Libra Blockchain is what’s known as “permissioned,” where only entities that fulfill certain requirements are admitted to a special in-group that defines consensus and controls governance of the blockchain. The problem is this structure is more vulnerable to attacks and censorship because it’s not truly decentralized. But during Facebook’s research, it couldn’t find a reliable permissionless structure that could securely scale to the number of transactions Libra will need to handle. Adding more nodes slows things down, and no one has proven a way to avoid that without compromising security.

That’s why the Libra Association’s goal is to move to a permissionless system based on proof-of-stake that will protect against attacks by distributing control, encourage competition and lower the barrier to entry. It wants to have at least 20% of votes in the Libra Association council coming from node operators based on their total Libra holdings instead of their status as a founding member. That plan should help appease blockchain purists who won’t be satisfied until Libra is completely decentralized.

The Libra Blockchain is open source with an Apache 2.0 license, and any developer can build apps that work with it using the Move coding language. The blockchain’s prototype launches its testnet today, so it’s effectively in developer beta mode until it officially launches in the first half of 2020. The Libra Association is working with HackerOne to launch a bug bounty system later this year that will pay security researchers for safely identifying flaws and glitches. In the meantime, the Libra Association is implementing the Libra Core using the Rust programming language because it’s designed to prevent security vulnerabilities, and the Move language isn’t fully ready yet.

Move was created to make it easier to write blockchain code that follows an author’s intent without introducing bugs. It’s called Move because its primary function is to move Libra coins from one account to another, and never let those assets be accidentally duplicated. The core transaction code looks like: LibraAccount.pay_from_sender(recipient_address, amount) procedure.

Eventually, Move developers will be able to create smart contracts for programmatic interactions with the Libra Blockchain. Until Move is ready, developers can create modules and transaction scripts for Libra using Move IR, which is high-level enough to be human-readable but low-level enough to be translatable into real Move bytecode that’s written to the blockchain.

The Libra ecosystem and the Move language will be completely open to use and build, which presents a sizable risk. Crooked developers could prey on crypto novices, claiming their app works just the same as legitimate ones, and that it’s safe because it uses Libra. But if consumers get ripped off by these scammers, the anger will surely bubble up to Facebook. Yet still, Calibra’s head of product tells me, “There are no plans for the Libra Association to take a role in actively vetting [developers],” Calibra’s head of product Kevin Weil tells me.

Even though it’s tried to distance itself sufficiently via its subsidiary Libra and the association, many people will probably always think of Libra as Facebook’s cryptocurrency and blame it for their woes.

Read our full story on the dangers of Libra’s unvetted developer platform

The Libra Association wants to encourage more developers and merchants to work with its cryptocurrency. That’s why it plans to issue incentives, possibly Libra coins, to validator node operators who can get people signed up for and using Libra. Wallets that pull users through the Know Your Customer anti-fraud and money laundering process or that keep users sufficiently active for over a year will be rewarded. For each transaction they process, merchants will also receive a percentage of the transaction back.

Businesses that earn these incentives can keep them, or pass some or all of them along to users in the form of free Libra tokens or discounts on their purchases. This could create competition between wallets to see which can pass on the most rewards to their customers, and thereby attract the most users. You could imagine eBay or Spotify giving you a discount for paying in Libra, while wallet developers might offer you free tokens if you complete 100 transactions within a year.

“One challenge for Spotify and its users around the world has been the lack of easily accessible payment systems – especially for those in financially underserved markets,” Spotify’s Chief Premium Business Officer Alex Norström writes. “In joining the Libra Association, there is an opportunity to better reach Spotify’s total addressable market, eliminate friction and enable payments in mass scale.”

This savvy incentive system should massively help ratchet up Libra’s user count without dictating how businesses balance their margins versus growth. Facebook also has another plan to grow its developer ecosystem. By offering venture capital firms like Andreessen Horowitz and Union Square Ventures a portion of the reserve interest, they’re motivating to fund startups building Libra infrastructure.

So how do you actually own and spend Libra? Through Libra wallets like Facebook’s own Calibra and others that will be built by third-parties, potentially including Libra Association members like PayPal. The idea is to make sending money to a friend or paying for something as easy as sending a Facebook Message. You won’t be able to make or receive any real payments until the official launch next year, though, but you can sign up for early access when it’s ready here.

None of the Libra Association members agreed to provide details on what exactly they’ll build on the blockchain, but we can take Facebook’s Calibra wallet as an example of the basic experience. Calibra will launch alongside the Libra currency on iOS and Android within Facebook Messenger, WhatsApp and a standalone app. When users first sign up, they’ll be taken through a Know Your Customer anti-fraud process where they’ll have to provide a government-issued photo ID and other verification info. They’ll need to conduct due diligence on customers and report suspicious activity to the authorities.

From there you’ll be able to cash in to Libra, pick a friend or merchant, set an amount to send them and add a description and send them Libra. You’ll also be able to request Libra, and Calibra will offer an expedited way of paying merchants by scanning your or their QR code. Eventually it wants to offer in-store payments and integrations with point-of-sale systems like Square.

The Libra Association’s e-commerce members seem particularly excited about how the token could eliminate transaction fees and speed up checkout. “We believe blockchain will benefit the luxury industry by improving IP protection, transparency in the product life cycle and — as in the case of Libra — enable global frictionless e-commerce,” says FarFetch CEO Jose Neves.

Facebook CEO Mark Zuckerberg explained some of the philosophy behind Libra and Calibra in a post today. “It’s decentralized — meaning it’s run by many different organizations instead of just one, making the system fairer overall. It’s available to anyone with an internet connection and has low fees and costs. And it’s secured by cryptography which helps keep your money safe. This is an important part of our vision for a privacy-focused social platform — where you can interact in all the ways you’d want privately, from messaging to secure payments.”

By default, Facebook won’t import your contacts or any of your profile information, but may ask if you wish to do so. It also won’t share any of your transaction data back to Facebook, so it won’t be used to target you with ads, rank your News Feed, or otherwise earn Facebook money directly. Data will only be shared in specific instances in anonymized ways for research or adoption measurement, for hunting down fraudsters or due to a request from law enforcement. And you don’t even need a Facebook or WhatsApp account to sign up for Calibra or to use Libra.

“We realize people don’t want their social data and financial data commingled,” says Marcus, who’s now head of Calibra. “The reality is we’ll have plenty of wallets that will compete with us and many of them will not be in social, and if we want to successfully win people’s trust, we have to make sure the data will be separated.”

In case you are hacked, scammed or lose access to your account, Calibra will refund you for lost coins when possible through 24/7 chat support because it’s a custodial wallet. You also won’t have to remember any long, complex crypto passwords you could forget and get locked out from your money, as Calibra manages all your keys for you. Given Calibra will likely become the default wallet for many Libra users, this extra protection and smoother user experience is essential.

For now, Calibra won’t make money. But Calibra’s head of product Kevin Weil tells me that if it reaches scale, Facebook could launch other financial tools through Calibra that it could monetize, such as investing or lending. “In time, we hope to offer additional services for people and businesses, such as paying bills with the push of a button, buying a cup of coffee with the scan of a code or riding your local public transit without needing to carry cash or a metro pass,” the Calibra team writes. That makes it start to sound a lot like China’s everything app WeChat.

Facebook got one thing right for sure: Today’s money doesn’t work for everyone. Those of us living comfortably in developed nations likely don’t see the hardships that befall migrant workers or the unbanked abroad. Preyed on by greedy payday lenders and high-fee remittance services, targeted by muggers and left out of traditional financial services, the poor get poorer. Libra has the potential to get more money from working parents back to their families and help people retain credit even if they’re robbed of their physical possessions. That would do more to accomplish Facebook’s mission of making the world feel smaller than all the News Feed Likes combined.

If Facebook succeeds and legions of people cash in money for Libra, it and the other founding members of the Libra Association could earn big dividends on the interest. And if suddenly it becomes super quick to buy things through Facebook using Libra, businesses will boost their ad spend there. But if Libra gets hacked or proves unreliable, it could cost lots of people around the world money while souring them on cryptocurrencies. And by offering an open Libra platform, shady developers could build apps that snatch not just people’s personal info like Cambridge Analytica, but their hard-earned digital cash.

Facebook just tried to reinvent money. Next year, we’ll see if the Libra Association can pull it off. It took me 4,000 words to explain Libra, but at least now you can make up your own mind about whether to be scared of Facebook crypto.

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a newsletter published every Saturday that dives into the week’s noteworthy venture capital deals, funds and trends. Before I dive into this week’s topic, let’s catch up a bit. Last week, I wrote about the proliferation of billion-dollar companies. Before that, I noted the uptick in beverage startup rounds. Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets.

Now, time for some quick notes on Peloton’s confirmed initial public offering. The fitness unicorn, which sells a high-tech exercise bike and affiliated subscription to original fitness content, confidentially filed to go public earlier this week. Unfortunately, there’s no S-1 to pore through yet; all I can do for now is speculate a bit about Peloton’s long-term potential.

What I know:

A bullish perspective: Peloton, an early player in the fitness tech space, has garnered a cult following since its founding in 2012. There is something to be said about being an early-player in a burgeoning industry — tech-enabled personal fitness equipment, that is — and Peloton has certainly proven its bike to be genre-defining technology. Plus, Peloton is actually profitable and we all know that’s rare for a Silicon Valley company. (Peloton is actually New York-based but you get the idea.)

A bearish perspective: The market for fitness tech is heating up, largely as a result of Peloton’s own success. That means increased competition. Peloton has not proven itself to be a nimble business in the slightest. As Darrell noted in his piece, in its seven years of operation, “Peloton has put out exactly two pieces of hardware, and seems unlikely to ramp that pace. The cost of their equipment makes frequent upgrade cycles unlikely, and there’s a limited field in terms of other hardware types to even consider making. If hardware innovation is your measure for success, Peloton hasn’t really shown that it’s doing enough in this category to fend of legacy players or new entrants.”

TL;DR: Peloton, unlike any other company before it, sits evenly at the intersection of fitness, software, hardware and media. One wonders how Wall Street will value a company so varied. Will Peloton be yet another example of an over-valued venture-backed unicorn that flounders once public? Or will it mature in time to triumphantly navigate the uncertain public company waters? Let me know what you think. And If you want more Peloton deets, read Darrell’s full story: Weighing Peloton’s opportunity and risks ahead of IPO.

Anyways…

Public company corner

In addition to Peloton’s IPO announcement, CrowdStrike boosted its IPO expectations. Aside from those two updates, IPO land was pretty quiet this week. Let’s check in with some recently public businesses instead.

Uber: The ride-hailing giant has let go of two key managers: its chief operating officer and chief marketing officer. All of this comes just a few weeks after it went public. On the brightside, Uber traded above its IPO price for the first time this week. The bump didn’t last long but now that the investment banks behind its IPO are allowed to share their bullish perspective publicly, things may improve. Or not.

Zoom: The video communications business posted its first earnings report this week. As you might have guessed, things are looking great for Zoom. In short, it beat estimates with revenues of $122 million in the last quarter. That’s growth of 109% year-over-year. Not bad Zoom, not bad at all.

We cover a lot of startup and big tech news here at TechCrunch. Sometimes, the really great features writers put a lot of time and energy into fall between the cracks. With that said, I just want to take a moment this week to highlight a few of the great stories published on our site recently:

A peek inside Sequoia Capital’s low-flying, wide-reaching scout program by Connie Loizos

How to calculate your event ROI by Sarah Shewey

Why four security companies just sold for $1.5B by Ron Miller

In case you missed it, Bird is in negotiations to acquire Scoot, a smaller scooter upstart with licenses to operate in the coveted market of San Francisco. Scoot was last valued at around $71 million, having raised about $47 million in equity funding to date from Scout Ventures, Vision Ridge Partners, angel investor Joanne Wilson and more. Bird, of course, is a whole lot larger, valued at $2.3 billion recently.

On top of this deal, there was no shortage of scooter news this week. Bird, for example, unveiled the Bird Cruiser, an electric vehicle that is essentially a blend between a bicycle and a moped. Here’s more on the booming scooter industry.

Thumbtack is raising up to $120M on a flat valuation

Depop, a shopping app for millennials, bags $62M

Fitness startup Mirror nears $300M valuation with fresh funding

Step raises $22.5M led by Stripe to build no-fee banking services for teens

Possible Finance lands $10.5M to provide kinder short-term loans

Voatz raises $7M for its mobile voting technology

Flexible housing startup raises $2.5M

Legacy, a sperm testing and freezing service, raises $1.5M

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I discuss how a future without the SoftBank Vision Fund would look, Peloton’s IPO and data-driven investing.

Powered by WPeMatico

Brex, the fintech business that’s taken the startup world by storm with its sought after corporate card tailored for entrepreneurs, is raising millions in Series D funding less than a year after it launched, TechCrunch has learned.

Bloomberg reports Brex is raising at a $2 billion valuation, though sources tell TechCrunch the company is still in negotiations with both new and existing investors. Brex didn’t immediately respond to requests for comment.

Kleiner Perkins is leading the round via former general partner Mood Rowghani, who left the storied venture capital fund last year to form Bond alongside Mary Meeker and Noah Knauf. As we’ve previously reported, the Bond crew is still in the process of deploying capital from Kleiner’s billion-dollar Digital Growth Fund III, the pool of capital they were responsible for before leaving the firm.

Bond, which recently closed on $1.25 billion for its debut effort and made its first investment, is not participating in the round for Brex, sources confirm to TechCrunch. Bond declined to comment.

Brex, a graduate of Y Combinator’s winter 2017 cohort, has raised $182 million in VC funding, reaching a valuation of $1.1 billion in October 2018 three months after launching its corporate card for startups and less than a year after completing YC’s accelerator program.

Most recently, Brex attracted a $125 million Series C investment led by Greenoaks Capital, DST Global and IVP. The startup is also backed by PayPal founders Peter Thiel and Max Levchin, and VC firms such as Ribbit Capital, Oneway Ventures and Mindset Ventures, according to PitchBook.

The company’s pace of growth is unheard of, even in Silicon Valley where inflated valuations and outsized rounds are the norm. Why? Brex has tapped into a market dominated by legacy players in dire need of technological innovation and, of course, startup founders always need access to credit. That, coupled with the fact that it’s capitalized on YC’s network of hundreds of startup founders — i.e. Brex customers — has accelerated its path to a multi-billion-dollar price tag.

Brex doesn’t require any kind of personal guarantee or security deposit from its customers, allowing founders near-instant access to credit. More importantly, it gives entrepreneurs a credit limit that’s as much as 10 times higher than what they would receive elsewhere.

Investors may also be enticed by the fact the company doesn’t use third-party legacy technology, boasting a software platform that is built from scratch. On top of that, Brex simplifies a lot of the frustrating parts of the corporate expense process by providing companies with a consolidated look at their spending.

“We have a very similar effect of what Stripe had in the beginning, but much faster because Silicon Valley companies are very good at spending money but making money is harder,” Brex co-founder and chief executive officer Henrique Dubugras told me late last year.

Stripe, for context, was founded in 2010. Not until 2014 did the company raise its unicorn round, landing a valuation of $1.75 billion with an $80 million financing. Today, Stripe has raised a total of roughly $1 billion at a valuation north of $20 billion.

Dubugras and Brex co-founder Pedro Franceschi, 23-year-old entrepreneurs, relocated from Brazil to Stanford in the fall of 2016 to attend the university. They dropped out upon getting accepted into YC, which they applied to with a big dreams for a virtual reality startup called Beyond. Beyond quickly became Brex, a name in which Dubugras recently told TechCrunch was chosen because it was one of few four-letter word domains available.

Brex’s funding history

March 2017: Brex graduates Y Combinator

April 2017: $6.5M Series A | $25M valuation

April 2018: $50M Series B | $220M valuation

October 2018: $125M Series C | $1.1B valuation

May 2019: undisclosed Series D | ~$2B valuation

In April, Brex secured a $100 million debt financing from Barclays Investment Bank. At the time, Dubugras told TechCrunch the business would not seek out venture investment in the near future, though he did comment that the debt capital would allow for a significant premium when Brex did indeed decide to raise capital again.

In 2019, Brex has taken steps several steps toward maturation.Recently, it launched a rewards program for customers and closed its first notable acquisition of a blockchain startup called Elph. Shortly after, Brex released its second product, a credit card made specifically for ecommerce companies.

Its upcoming infusion of capital will likely be used to develop payment services tailored to Fortune 500 business, which Dubugras has said is part of Brex’s long term plan to disrupt the entire financial technology space.

Powered by WPeMatico