stock

Auto Added by WPeMatico

Auto Added by WPeMatico

One of the big reasons you’re giving 110% of your talent and effort to your private company is because you’re hoping to eventually cash in on all those vested incentive stock options (ISOs) that have been sitting in some account, waiting for the day your company goes public.

There’s nothing wrong with that. Who doesn’t dream of reaping an options windfall and using it to retire early, buy a house, pay off their college loans, travel around the world or become a full-time philanthropist?

Unfortunately, when it comes to figuring out how to cash in their stock awards, most employees are on their own.

Their employers can’t always provide the answers they need — especially when the questions relate to personal finances. Most companies admit they need to be better at explaining how ISOs work in general, but they can’t legally work one-on-one with employees to help them exercise and sell shares the right way.

Most companies admit they need to be better at explaining how ISOs work in general, but they can’t legally work one-on-one with employees to help them exercise and sell shares the right way.

That’s why, when the time is right, many employees actively look for help from a qualified fiduciary financial adviser who can walk these could-be “options millionaires” through various cash-in scenarios.

Here’s a real-life example (using a pseudonym).

Kurt is a 50-year-old VP of product management at a healthcare startup that just went public. Over his three years with the company, Kurt had amassed 350,000 ISOs worth approximately $6 million. Unlike many options millionaires, he didn’t intend to cash in everything and retire early. He planned to stay with the firm but wanted to liquidate enough ISOs to pay for a vacation home and add greater diversification to his investment portfolio. This presented significant tax risks that Kurt wasn’t aware of.

If Kurt exercised his ISOs and sold the shares before a year had passed, his profits would be characterized as short-term capital gains, which are taxed as ordinary income.

To illustrate the potential tax implications of this action, we created a hypothetical scenario that showed if Kurt exercised all of his ISOs and sold the shares immediately, he would incur approximately $6 million in ordinary income, which would push him into the top tax bracket and put him on the hook for almost $3 million in combined federal and state taxes.

Powered by WPeMatico

Uber and Lyft lost a lot of money in 2020. That’s not a surprise, as COVID-19 caused many ride-hailing markets to freeze, limiting demand for folks moving around. To combat the declines in their traditional businesses, Uber continued its push into consumer delivery, while Lyft announced a push into business-to-business logistics.

But the decline in demand harmed both companies. We can see that in their full-year numbers. Uber’s revenue fell from $13 billion in 2019 to $11.1 billion in 2020. Lyft’s fell from $3.6 billion in 2019 to a far-smaller $2.4 billion in 2020.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But Uber and Lyft are excited that they will reach adjusted profitability, measured as earnings before interest, taxes, depreciation, amortization and even more stuff stripped out, by the fourth quarter of this year.

Ride-hailing profits have long felt similar to self-driving revenues: just a bit over the horizon. But after the year from hell, Uber and Lyft are pretty damn certain that their highly adjusted profit dreams are going to come through.

Ride-hailing profits have long felt similar to self-driving revenues: just a bit over the horizon. But after the year from hell, Uber and Lyft are pretty damn certain that their highly adjusted profit dreams are going to come through.

This morning, let’s unpack their latest numbers to see if what the two companies are dangling in front of investors is worth desiring. Along the way we’ll talk BS metrics and how firing a lot of people can cut your cost base.

Using normal accounting rules, Uber lost $6.77 billion in 2020, an improvement from its 2019 loss of $8.51 billion. However, if you lean on Uber’s definition of adjusted EBITDA, its 2019 and 2020 losses fall to $2.73 billion and $2.53 billion, respectively.

So what is this magic wand Uber is waving to make billions of dollars worth of red ink go away? Let’s hear from the company itself:

We define Adjusted EBITDA as net income (loss), excluding (i) income (loss) from discontinued operations, net of income taxes, (ii) net income (loss) attributable to non-controlling interests, net of tax, (iii) provision for (benefit from) income taxes, (iv) income (loss) from equity method investments, (v) interest expense, (vi) other income (expense), net, (vii) depreciation and amortization, (viii) stock-based compensation expense, (ix) certain legal, tax, and regulatory reserve changes and settlements, (x) goodwill and asset impairments/loss on sale of assets, (xi) acquisition and financing related expenses, (xii) restructuring and related charges and (xiii) other items not indicative of our ongoing operating performance, including COVID-19 response initiative related payments for financial assistance to Drivers personally impacted by COVID-19, the cost of personal protective equipment distributed to Drivers, Driver reimbursement for their cost of purchasing personal protective equipment, the costs related to free rides and food deliveries to healthcare workers, seniors, and others in need as well as charitable donations.

Er, hot damn. I can’t recall ever seeing an adjusted EBITDA definition with 12 different categories of exclusion. But, it’s what Uber is focused on as reaching positive adjusted EBITDA is key to its current pitch to investors.

Indeed, here’s the company’s CFO in its most recent earnings call, discussing its recent performance:

We remain on track to turn the EBITDA profitable in 2021, and we are confident that Uber can deliver sustained strong top-line growth as we move past the pandemic.

So, if investors get what Uber promises, they will get an unprofitable company at the end of 2021, albeit one that, if you strip out a dozen categories of expense, is no longer running in the red. This, from a company worth north of $112 billion, feels like a very small promise.

And yet Uber shares have quadrupled from their pandemic lows, during which they fell under the $15 mark. Today Uber is worth more than $60 per share, despite shrinking last year and projecting years of losses (real), and possibly some (fake) profits later in the year.

Powered by WPeMatico

If you’ve been lucky enough to keep your job or business, you almost certainly know someone who wasn’t so fortunate.

Thousands have lost their jobs as companies significantly reduce workforces to adjust to uncertainties and economic challenges created by COVID-19. Many of these people in tech are now faced with a number of questions, from how they’ll pay next month’s rent to whether they’re eligible for unemployment. One area that is particularly confusing is what to do if your compensation package was tied to equity.

Here are some ways I suggest approaching the issue.

Layoffs have become part and parcel of the current economic crisis with unemployment figures skyrocketing to record highs as a result of COVID-19. From multinational conglomerates to mom-and-pop stores, everyone is feeling the impact, and the startup sector is no different.

Despite difficult circumstances, the silver lining for employees is that we have seen many management teams go the extra mile to help their teams, especially when it comes to equity. Compared to traditional layoff situations, companies in the COVID-19 era are offering generous extensions and accelerated vesting on their options, which is undeniably good news for employees with equity.

Typically, equity plans come with a 90-day exercise window after employment termination. That means that if you leave the company, you will have to exercise your options within 90 days or they go back to the company. However, lots of management teams have decided to extend these deadlines many years out given the circumstances.

While layoffs are not easy, it’s been great to see management teams doing the right thing when it comes to equity for their employees who have been laid off. Offering extensions is a benefit that employers should be offering their employees who have helped build the company.

If your company is not offering this, consider negotiating and asking for an extension. This is the right thing to do for employees who are now out of work and a paycheck for the foreseeable future. Both options do not require the company to pay cash at the moment, so there are few reasons a company should deny this request in this environment.

Even if you are granted an extension to exercise your options, employees that hold incentive stock options (ISOs) should look into exercising their options now to maximize their equity’s value.

Many companies are offering extensions for option exercises. While this is great in that it gives employees more time to figure out their exercise situation, waiting past the 90-day window may have much bigger tax consequences that employees need to consider.

ISOs are much more tax advantageous compared to non-qualified stock options (NSOs). They are not taxed under standard income tax and if you sell the stock two years after grant date and one year after exercise date, you sell them as part of a qualifying disposition. In short, this allows you to effectively convert everything north of your strike price to preferential long-term capital gain rates.

As part of offering these tax advantages, the tax code has limitations on ISOs. Most relevant to us at this point is that the fact that you cannot have ISOs past 90 days after you are no longer an employee. This means that even if your company allows an extension on your stock options past the typical 90-day expiration window, your ISOs will convert to NSOs and lose their tax benefit.

This creates a potential planning opportunity that employees who have been laid off need to consider. If you feel good about the upside of the company, then you should consider exercising your ISOs today to capture the potential tax benefits rather than letting them convert to NSOs. Employees who wait risk putting themselves in the same difficult situation once the extension ends at typically less favorable conditions due to an increased 409A valuation.

In light of the economic slowdown many companies have begun to cut costs. Reduced pay or furloughing employees has become the new norm as businesses of all sizes struggle to navigate these changing times.

It can obviously be concerning if you find yourself in this situation. But for startup employees, the COVID-19 crisis could provide an opportunity to negotiate your compensation package to make up for this decrease, and even set yourself up to prosper in the future.

Startups typically offer equity as a means of deferred compensation and as a way to incentivize employees to own a piece of the company they are building. The compensation is deferred as most startups are cash-strapped and cannot afford to pay you what a larger company may be able to.

If your company is now asking you to take a pay cut, or even take no pay during this time, you should consider asking for additional equity to make up for the lost compensation. While not all companies may be amenable to offering more equity, there is no cash outlay from the company’s standpoint, so it’s an efficient way for your company to compensate you for your sacrifice while preserving their cash.

In addition, offering more equity shows a commitment from management to their employees during this difficult time. It may be the win-win scenario for your company and yourself in the long-run so it’s worth having the conversation with management to discuss if this is available for you.

If your company does offer you more equity, make sure you ask whether the 409A (or fair market value) of the company is being updated. With revised forecasts given the COVID-19 situation, it may be possible for your company to issue your stock at a lower strike price if the company revalues its 409A.

I can sympathize with startup employees right now because I faced a similar situation when I left a startup that I had joined as employee number four and was forced to wave goodbye to the equity I had banked on.

If you want to take action on equity but don’t know where to start, now might be a good time to brush up on how your stock options work. As the economy begins to reopen, there’s a good chance we’ll see a rush for candidates in tech as companies compete to bring in some of the extremely talented folks who lost their jobs this week.

Those who have a good understanding of equity may be positioned for a big payday down the line.

Powered by WPeMatico

Founders, entrepreneurs, and tech executives in the know realize they may be able to avoid paying tax on all or part of the gain from the sale of stock in their companies — assuming they qualify.

If you’re a founder who’s interested in exploring this opportunity, put careful consideration put into the formation, operation and selling of your company.

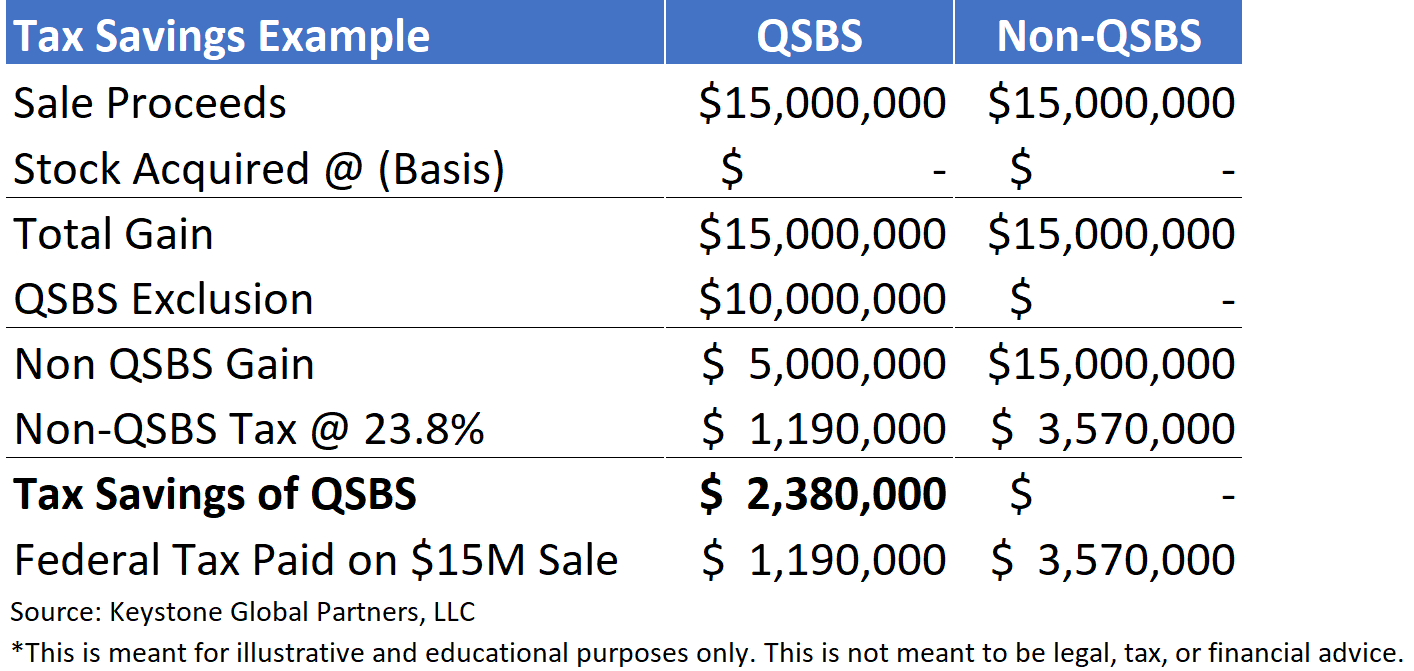

Qualified Small Business Stock (QSBS) presents a significant tax savings opportunity for people who create and invest in small businesses. It allows you to potentially exclude up to $10 million, or 10 times your tax basis, whichever is greater, from taxation. For example, if you invested $2 million in QSBS in 2012, and sell that stock after five years for $20 million (10x basis) you could pay zero federal capital gains tax on that gain.

These tax savings can be so significant, that it’s one of a handful of high-priority items we’ll first discuss, when working with a founder or tech executive client. Surprisingly, most people in general either:

Founders who are scaling their companies usually have a lot on their minds, and tax savings and personal finance usually falls to the bottom of the list. For example, I recently met with someone who will walk away from their upcoming liquidity event with between $30-40 million. He qualifies for QSBS, but until our conversation, he hadn’t even considered leveraging it.

Instead of paying long-term capital gains taxes, how does 0% sound? That’s right — you may be able to exclude up to 100% of your federal capital gains taxes from selling the stake in your company. If your company is a venture-backed tech startup (or was at one point), there’s a good chance you could qualify.

In this guide I speak specifically to QSBS on a federal tax level, however it’s important to note that many states such as New York follow the federal treatment of QSBS, while states such as California and Pennsylvania completely disallow the exclusion. There is a third group of states, including Massachusetts and New Jersey, that have their own modifications to the exclusion. Like everything else I speak about here, this should be reviewed with your legal and tax advisors.

My team and I recently spoke with a founder whose company was being acquired. She wanted to do some financial planning to understand how her personal balance sheet would look post-acquisition, which is a savvy move.

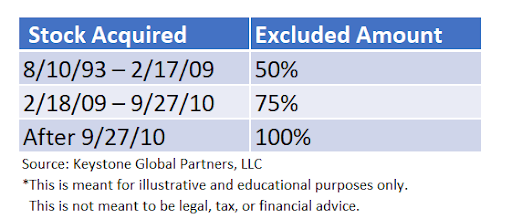

We worked with her corporate counsel and accountant to obtain a QSBS representation from the company and modeled out the founder’s effective tax rate. She owned equity in the form of company shares, which met the criteria for qualifying as Section 1202 stock (QSBS). When she acquired the shares in 2012, her cost basis was basically zero.

A few months after satisfying the five-year holding period, a public company acquired her business. Her company shares, first acquired for basically zero, were now worth $15 million. When she was able to sell her shares, the first $10 million of her capital gains were completely excluded from federal taxation — the remainder of her gain was taxed at long-term capital gains.

This founder saved millions of dollars in capital gains taxes after her liquidity event, and she’s not the exception! Most founders who run a venture-backed C Corporation tech company can qualify for QSBS if they acquire their stock early on. There are some exceptions.

A frequently asked question as we start to discuss QSBS with our clients is: how do I know if I qualify? In general, you need to meet the following requirements:

When in doubt, follow this flowchart to see if you qualify:

Powered by WPeMatico

The increase in activity in the pre-IPO secondary market means that founders, early employees, and investors are receiving liquidity much sooner in a company’s lifecycle than ever before. For most startups and privately-held companies, liquidity is often an issue for stockholders, as no market exists for selling shares and/or transfer restrictions can prevent their sale. Secondary stock transactions, however, are a way to work around this problem.

Here’s a quick look at how they work and what to keep in mind, especially if you’re going through the process for the first time. (If you’re not familiar, secondaries are transactions in which an existing stockholder sells their stock for cash to third parties or back to the company itself before the company undergoes an exit; traditionally, an exit refers to an M&A or an IPO.)

Offering secondary transactions to founders is a tool VCs have been using to win deals. For example, if a VC promises that the founders will receive $1,000,000 in cash through a secondary sale from a $15,000,000 venture financing round, the founders will likely prefer that VC’s term sheet to a term sheet from a VC that does not offer that deal.

Powered by WPeMatico

Stripe Atlas was launched by payments company Stripe last year to help small businesses set themselves up as a legal, incorporated business entity in the U.S. Now with “thousands” of entrepreneurs from 125+ countries using Atlas, Stripe is expanding it with a new feature as it hones its focus on being a platform for startup services. Companies that are signed up to Atlas (which… Read More

Stripe Atlas was launched by payments company Stripe last year to help small businesses set themselves up as a legal, incorporated business entity in the U.S. Now with “thousands” of entrepreneurs from 125+ countries using Atlas, Stripe is expanding it with a new feature as it hones its focus on being a platform for startup services. Companies that are signed up to Atlas (which… Read More

Powered by WPeMatico

Traders who have an idea for a money-making algorithm have two choices: learn to code themselves, or hire a great engineer. But neither of these two options are realistic, especially for part-time traders who don’t have a large bankroll behind them. Meet Algoriz, a startup participating in Y Combinator’s Winter 2017 batch. Read More

Traders who have an idea for a money-making algorithm have two choices: learn to code themselves, or hire a great engineer. But neither of these two options are realistic, especially for part-time traders who don’t have a large bankroll behind them. Meet Algoriz, a startup participating in Y Combinator’s Winter 2017 batch. Read More

Powered by WPeMatico

A startup from Columbus called BYLINED is aiming to make it a bit easier for brands and people to come together in a win/win situation resulting in more unique photography. Through their free app and photo ecosystem, BYLINED enables brands, agencies or publishers to issue a request for a certain type of photo—an assignment or commission so to speak—that people with smartphones… Read More

A startup from Columbus called BYLINED is aiming to make it a bit easier for brands and people to come together in a win/win situation resulting in more unique photography. Through their free app and photo ecosystem, BYLINED enables brands, agencies or publishers to issue a request for a certain type of photo—an assignment or commission so to speak—that people with smartphones… Read More

Powered by WPeMatico

It seems most founders believe investors asking for “extras” on the side are simply greedy and short-sighted. While it’s easy to criticize investors, I believe this behavior is driven in large part as a response to conditions founders have created in early stage investing. I believe two trends, when taken together, have eroded the “one round, one price” standard. Read More

It seems most founders believe investors asking for “extras” on the side are simply greedy and short-sighted. While it’s easy to criticize investors, I believe this behavior is driven in large part as a response to conditions founders have created in early stage investing. I believe two trends, when taken together, have eroded the “one round, one price” standard. Read More

Powered by WPeMatico

Following trading today, Etsy reported its Q3 financial performance, including revenue of $66 million, and earnings loss per share of $0.06. The Street expected Etsy to lose $0.06 per share, off revenue of around $66.17 million. So that’s a “met expectations.” The company reported 1.5 million active sellers and 22.6 million active buyers. The company was up 3.18 percent… Read More

Following trading today, Etsy reported its Q3 financial performance, including revenue of $66 million, and earnings loss per share of $0.06. The Street expected Etsy to lose $0.06 per share, off revenue of around $66.17 million. So that’s a “met expectations.” The company reported 1.5 million active sellers and 22.6 million active buyers. The company was up 3.18 percent… Read More

Powered by WPeMatico