stock options

Auto Added by WPeMatico

Auto Added by WPeMatico

Every startup founder faces the same issue — how do you manage your cap table and equity plans in a transparent and lightweight manner? If you’re based in the U.S., chances are you’re using an equity management solution like Carta. But if you’re not based in the U.S., you don’t have a ton of options.

Ledgy wants to become the ownership management tool for the rest of the world. Based in Switzerland, several well-known European startups are already using Ledgy, such as Wefox, Kry, Bitpanda, Gorillas and Trade Republic.

The company recently closed a $10 million Series A funding round led by Sequoia Capital. Other investors in the round include Xavier Niel, Harry Stebbings, Visionaries Club, UiPath’s Daniel Dines and Front’s Mathilde Collin. Some of Ledgy’s existing investors also invested once again, such as Myke Näf, Paul Sevinç, btov Partners, Creathor Ventures and VI Partners.

A few years ago, when Ledgy co-founder and CEO Yoko Spirig talked with an entrepreneur, the founder showed her how he managed ownership. He opened an Excel spreadsheet and scrolled, scrolled, scrolled… “Each line represented a share. You can imagine how error-prone it is,” she told me.

While the implementation was odd, most companies in Europe are still using Excel spreadsheets to manage ownership. And Ledgy wants to convince those companies that switching to a software solution that has been specifically designed to solve this issue could be beneficial.

“The key has really been to focus on the software infrastructure. What we do is that we have implemented automation workflows that are adaptable depending on countries,” Spirig said. “We’re not focusing on one regulation and we’re really offering the infrastructure layer,” she added.

That’s why Ledgy already supports 32 countries. It has tweaked its product even more specifically for Germany, Austria and Switzerland. There will be more country-specific releases in the near future for startups based in the U.K. and France. 1,500 companies are using Ledgy right now.

When you switch to Ledgy, there are three main advantages. First, like other software-as-a-service products, Ledgy acts as a single source of truth for all stakeholders — the HR team, the finance team, investors, lawyers and employees.

The second selling point is that you can automate some of the most tedious tasks. For instance, Ledgy can automatically generate documents based on templates and different variables. Signed documents are stored on Ledgy. You can export data every quarter or every year for compliance reasons.

Third, it fosters transparency across the company. Employees can check the value of their options. They can see how much their options could be worth if the leadership team is in the process of raising a new round of funding.

With today’s funding round, Ledgy plans to expand into new markets. The company also plans to roll out support for public companies so that some of its existing customers can go public and keep using Ledgy.

Image Credits: Ledgy

Powered by WPeMatico

There’s an old startup adage that goes: Cash is king. I’m not sure that is true anymore.

In today’s cash rich environment, options are more valuable than cash. Founders have many guides on how to raise money, but not enough has been written about how to protect your startup’s option pool. As a founder, recruiting talent is the most important factor for success. In turn, managing your option pool may be the most effective action you can take to ensure you can recruit and retain talent.

That said, managing your option pool is no easy task. However, with some foresight and planning, it’s possible to take advantage of certain tools at your disposal and avoid common pitfalls.

In this piece, I’ll cover:

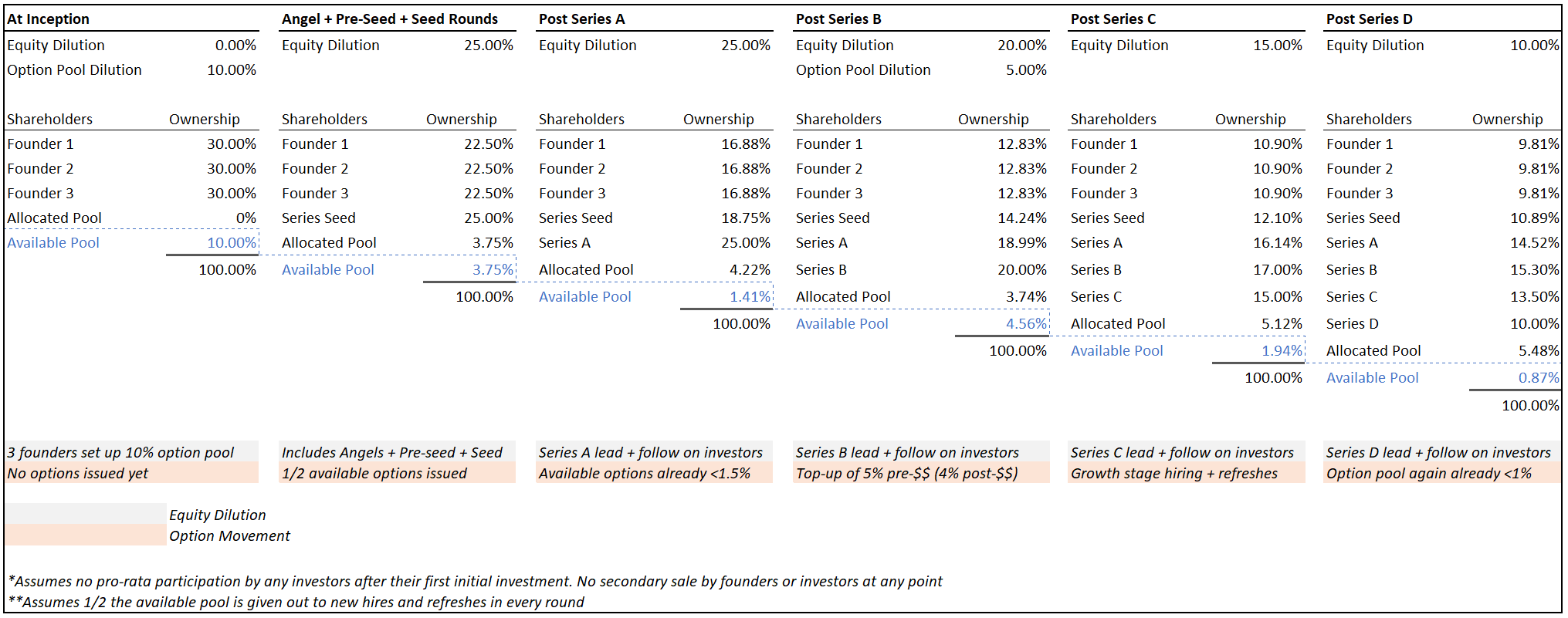

Let’s run through a quick case study that sets the stage before we dive deeper. In this example, there are three equal co-founders who decide to quit their jobs to become startup founders.

Since they know they need to hire talent, the trio gets going with a 10% option pool at inception. They then cobble together enough money across angel, pre-seed and seed rounds (with 25% cumulative dilution across those rounds) to achieve product-market fit (PMF). With PMF in the bag, they raise a Series A, which results in a further 25% dilution.

The easiest way to ensure you don’t run out of options too quickly is simply to start with a bigger pool.

After hiring a few C-suite executives, they are now running low on options. So at the Series B, the company does a 5% option pool top-up pre-money — in addition to giving up 20% in equity related to the new cash injection. When the Series C and D rounds come by with dilutions of 15% and 10%, the company has hit its stride and has an imminent IPO in the works. Success!

For simplicity, I will assume a few things that don’t normally happen but will make illustrating the math here a bit easier:

Obviously, every situation is unique and your mileage may vary. But this is a close enough proxy to what happens to a lot of startups in practice. Here is what the available option pool will look like over time across rounds:

Image Credits: Allen Miller

Note how quickly the pool thins out — especially early on. In the beginning, 10% sounds like a lot, but it’s hard to make the first few hires when you have nothing to show the world and no cash to pay salaries. In addition, early rounds don’t just dilute your equity as a founder, they dilute everyone’s — including your option pool (both allocated and unallocated). By the time the company raises its Series B, the available pool is already less than 1.5%.

Powered by WPeMatico

There’s a reason startup compensation packages usually include equity, or stock options. For one, it’s a way for startups to remain competitive in the job market and attract top talent. But it’s also a way to reward those employees who join early and give them a tangible reason to stay incentivized to grow the company.

The problem is that while many employees do understand that their equity compensation could mean a big payday in the future — and, in 2021, that’s more likely than ever — they don’t often understand the inevitable complexities of their stock options. That puts employees at risk of not getting the most value after an IPO or, worse, losing them.

If you’ve ever been confused about your equity, or haven’t thought much about it, you’re not alone. That’s why I’m going to share three things all employees joining a startup should do with their equity:

While many startups are getting better at proactively communicating the value of your equity package upfront, some are still figuring out the best way to do it. That’s because, unlike the more straightforward number of a salary, stock options are more nuanced — they’re a living, breathing type of compensation.

The most important pieces of information to pay attention to are your 409A valuation, your strike price, the type of options you were granted and the preferred share price.

The 409A valuation is based on your company’s valuation. This is also referred to as the fair market value (FMV). The 409A valuation can, and does, often change — they have to be updated at least once a year by a third-party valuator in order to meet tax rules. The 409A also changes during a fundraising event. Investors involved in the funding round determine how they value the company and are given options, at that valuation, in exchange for cash.

The most important pieces of information to pay attention to are your 409A valuation, your strike price, the type of options you were granted and the preferred share price.

Since the company has now been valued higher, the 409A changes for everyone. It’s also possible for the 409A to go down if, for any reason, the company is now valued at a lower amount. This is known as a “down round.” Airbnb had a notable down round during the pandemic, though it eventually recovered and went public.

Your strike price is the price at which you can buy your stock options (also known as exercising). Yes, buy. You are given the option to buy them, which is why they are called stock options. But know that your strike price will likely never change. However, if you’re ever given more stock options (perhaps as a future bonus), this would be a separate grant and the strike price could be different. Companies are legally required to issue stock options at the most recent 409A price (or higher).

Powered by WPeMatico

Thirty European tech CEOs of big startups signed a letter about stock options in Europe. Other tech CEOs can join the group and sign the letter before it is sent to policymakers on January 7.

As you can read in the letter below, these CEOs think Silicon Valley isn’t the only region suffering from talent crunch. It could be a “serious bottleneck to growth.”

“Over the next twelve months, Europe’s startups will need to hire more than 100,000 employees,” the letter says. “Without delay, we call on legislators to fix the patchy, inconsistent and often punitive rules that govern employee ownership—the practice of giving staff options to acquire a slice of the company they’re working for.”

Here’s the current list of signatories: Johannes Reck (GetYourGuide), Alice Zagury (The Family), Christian Reber (Pitch), Johannes Schildt (KRY / LIVI), Peter Mühlmann (Trustpilot), Ilkka Paanenen (Supercell), Taavet Hinrikus (TransferWise), Lucas Carne (Privalia), Jean-Charles Samuelian (Alan), Alex Saint (Secret Escapes), Dr. Tamaz Georgadze (Raisin), Patrick Collison (Stripe), Nikolay Storonsky (Revolut), Samir Desai (Funding Circle), Markus Villig (Taxify), Jean-Baptise Rudelle (Criteo), Nicolas Brusson (BlaBlaCar), Jacob de Geer (iZettle), David Okuniev (Typeform), José Neves (Farfetch), Felix Van de Maele (Collibra), Joris Van Der Gucht (Silverfin), Daniel Dines (UiPath), Rohan Silva (Second Home), Niklas Östberg (Delivery Hero), Dominik Richter (Hello Fresh), Dr. Raoul Scherwitzl (NaturalCycles), Alex Depledge (RESI), Juan de Antonio (Cabify).

Here’s the letter:

OPEN LETTER TO EUROPE’S POLICYMAKERS

Not Optional: Europe must attract more talent to startups

This following letter will be sent to Europe’s policymakers on 7 January 2019.

Policymakers, entrepreneurs and investors must work together to bring more talent to Europe’s startups. Here’s why.

The European tech sector has never been stronger. From London to Lisbon, Paris to Prague, Europe is now nurturing some of the world’s most dynamic and creative companies. And not all are fledgling young startups: many are already substantial, high-growth enterprises set to succeed in the global market.

The days of living in Silicon Valley’s shadow are over. We no longer lack ambition and capital. Now, Europe is a shining powerhouse of bold, new business models that drive economic growth, generate jobs and improve people’s lives.

We’d all like to see this fair weather continue, but storm clouds are gathering on the horizon.

Europe could be the world’s most entrepreneurial continent but the limited availability of talent to nurture and fuel its blossoming start-up ecosystem is a serious bottleneck to growth. That’s why we, the founders and executives of Europe’s leading tech businesses, now urge policymakers to put talent at the top of their agenda.

Over the next twelve months, Europe’s startups will need to hire more than 100,000 employees. Add to that the number of employees that start-ups yet to be born will need to get their ideas off the ground. Reaching that goal will be hard, but hard things are what we do and we’re ready to rise to the challenge.

Without delay, we call on legislators to fix the patchy, inconsistent and often punitive rules that govern employee ownership—the practice of giving staff options to acquire a slice of the company they’re working for.

This isn’t just a perk on top of a salary: universally, stock options reward employees for taking the risk of joining a young, unproven business, and give them a real stake in their company’s future success. Stock options are one of the main levers that startups use to recruit the talent they need; these companies simply can’t afford to pay the higher wages of more established businesses.

But policies that currently govern employee ownership across Europe are often archaic and highly ineffective. Some are so punishing that they put our startups at a major disadvantage to their peers in Silicon Valley and elsewhere, with whom we’re competing for the best designers, developers, product managers, and more.

If we fail to take action, we could see a brain drain of Europe’s best and brightest, leading to fewer jobs created and slower growth. That’s why we need to create startup-friendly employee share ownership schemes, to help Europe’s tech sector—its greatest engine of growth, innovation and employment—to succeed and thrive in the global labour market.

If we don’t eliminate the talent bottleneck, we risk squandering the incredible momentum that European tech has built up in recent years. The next Google, Amazon or Netflix could well come from Europe, but for that to happen, reforming the rules of employee ownership is definitely not optional.

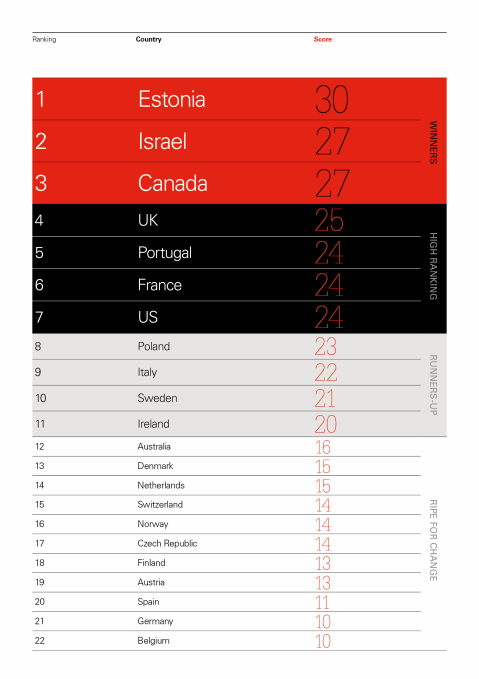

According to Index Ventures, the company that is coordinating this effort, some countries already have startup-friendly policies, while others lag behind:

The VC firm recommends overhauling policies in some countries and harmonizing policies across Europe. New rules should follow those six principles:

- Create a stock option scheme that is open to as many startups and employees as possible, offering favourable treatment in terms of regulation and taxation. Design a scheme based on existing models in the UK, Estonia or France to avoid further fragmentation and complexity.

- Allow startups to issue stock options with non-voting rights, to avoid the burden of having to consult large numbers of minority shareholders.

- Defer employee taxation to the point of sale of shares, when employees receive cash benefit for the first time.

- Allow startups to issue stock options based on an accepted ‘fair market valuation’, which removes tax uncertainty.

- Apply capital gains (or better) tax rates to employee share sales.

- Reduce or remove corporate taxes associated with the use of stock options.

Powered by WPeMatico

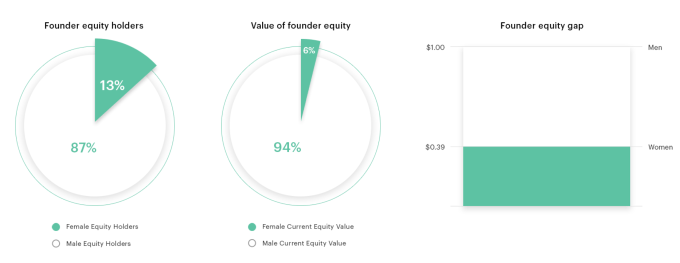

Even bigger than the salary gap that sees women earn $.82 on the dollar is the equity gap. A new study from Carta and the ex-Twitter female investor group #Angels reveals that women make up 35 percent of startup equity-holding employees, yet own just 20 percent of the equity. That means they own just $0.47 for every $1 that men own. Even worse, women account for 13 percent of startup founders but just 6 percent of founder equity — or merely $0.39 on the dollar.

Combined, that means only 9 percent of founder and employee startup equity is owned by women.

“This is not just about wealth” says #Angels’ Chloe Sladden. “Wealth from successful exits goes on to shape the entire industry. It’s about who has power and who gets to decide what gets funded.” #Angels’ Jessica Verrilli notes that “Having this data is going to be a watershed moment and catalyze more urgency to address this underrepresentation.”

#Angels’ Chloe Sladden

The study by cap table management tool Carta (formerly eShares) looked at a subset of its privately held company customers including roughly 180,000 employees, 15,000 founders, and 6,000 companies encompassing $45 billion in equity value.

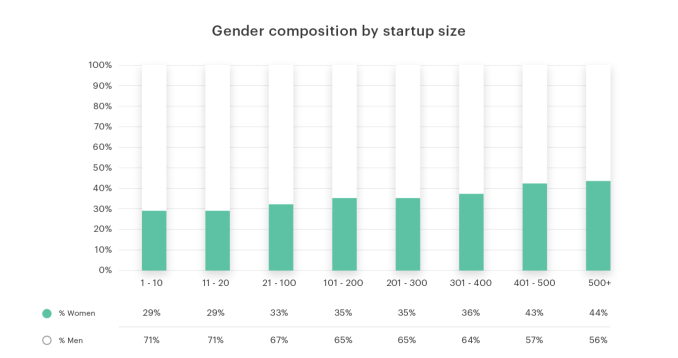

Amongst the hypothesized causes of the gap are that female-led startups get valued lower and diluted more, there’s less total capital allocated to women due to investor and industry bias, the underrepresentation of women as investors, challenges facing women during negotiations, and that they often team-up with more co-founders that have to split the equity pool.

#Angels’ Jana Messerschmidt explains that the gap table spotlights how women aren’t being hired for early engineering and leadership positions. These roles often get the lion’s share of equity, and when women are hired for sales, marketing, and HR jobs, “those folks are getting less equity because they are joining later and we have a hypothesis of how those roles are valued differently.” Sladden reminds founders to focus on diversity from day one. “Don’t push this off as something you’ll fix down the road as you’re facing all the other challenges.”

Once a successful startup gets acquired or IPOs and paper money turns into cash, tech workers often reinvest their winnings into more startups as angels, fund LPs, or by starting their own venture firm. If only men are getting enough equity to make those downstream investments, their biases could further unbalance the gender breakdown of the tech industry. The #Angels say they’ve found this translates into fewer fundraising term sheets and bargaining power for female founders when they come to the Sand Hill Road boy’s club for venture capital.

Beyond more diverse hiring, the #Angels believe it’s critical that the industry demystify equity so more women know how to exercise stock options and score tax advantages for maximum gain. “You shouldn’t need to have an MBA to know the importance of equity and how to negotiate for it” says Sladden. Better financing avenues for those women who need up-front capital to exercise their stock options could also ensure it’s not just those who already have money who can make money through equity.

Sladden concludes, “We hope this is going to start a movement. We hope that CEOs will start to measure it and talk about it.”

Powered by WPeMatico

As valuations continue to rise, early stage VCs are getting more “creative” with their deal structuring. In particular, I’ve seen a rise in requests for ESOP shares to be allocated to lead investors for their “value added services.” It’s common to give ESOP to advisors for their value add, so why not investors? Read More

As valuations continue to rise, early stage VCs are getting more “creative” with their deal structuring. In particular, I’ve seen a rise in requests for ESOP shares to be allocated to lead investors for their “value added services.” It’s common to give ESOP to advisors for their value add, so why not investors? Read More

Powered by WPeMatico

A proposed tax that charges people as their startup equity vests instead of when they cash it out and actually have money to pay the taxes could wreck how tech companies recruit talent. And the industry doesn’t have much time to mobilize to get this tax changed.

A proposed tax that charges people as their startup equity vests instead of when they cash it out and actually have money to pay the taxes could wreck how tech companies recruit talent. And the industry doesn’t have much time to mobilize to get this tax changed.