stock market

Auto Added by WPeMatico

Auto Added by WPeMatico

The TechCrunch crew is hard at work writing up the latest from Apple’s iPhone, iPad and Apple Watch event. They have good notes on the megacorp’s hardware updates. But what are the markets saying about the same array of products?

For those of us more concerned with effective S&P dividend yields than screen nit levels, events like Apple’s confab are more interesting for what they might mean for the value of the hosting company than how many GPUs a particular smartphone model has. And, for once, Apple’s stock may have done something a little interesting during the event!

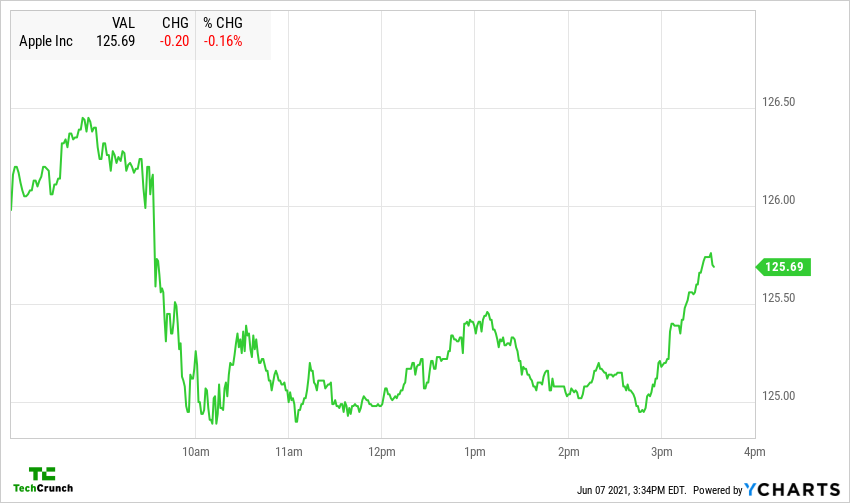

Observe the following chart:

Image Credits: TechCrunch/Y Charts

This is a one-day chart, mind, so we’re looking at intraday changes. We’re zoomed in. And Apple kinda took a bit of a dive during its event that kicked off at 1 p.m. in the above chart.

Normally nothing of import happens to Apple’s shares during its presentations. Which feels weird, frankly, as Apple events detail the product mix that will generate hundreds of billions in revenue. You’d think that they would have more impact than their usual zero.

But today, we had real share price movement when the event wrapped around 2 p.m. ET. Perhaps investors were hoping for more pricey devices? Or were hoping Apple had more up its sleeve? How you rate that holiday Apple product lineup is a matter of personal preference, but investors appear to have weighed in slightly to the negative.

Worth around $2.5 trillion, each 1% that Apple’s stock moves is worth $10 billion. Apple’s loss of 1.5% today — more or less; trading continues as I write this — is worth more than Mailchimp. It’s a lot of money.

You can read the rest of our coverage from the Apple event here. Enjoy!

Powered by WPeMatico

Update: Trading of Robinhood shares has been halted due to volatility. The company’s stock paused at $65.60 on Robinhood itself. Yahoo Finance has a higher $77.03 price on the company’s equity, up a stunning 64.59% today. Things are fluid, but Robinhood may have been halted and then rose again when it resumed trading. Stonks indeed.

Shares of Robinhood, an investing-focused consumer fintech company, soared this morning in premarket trading. The stonk phenomenon, which helped propel minor companies like GameStop and AMC earlier this year, appears to be impacting Robinhood’s own stock; that much GameStop and AMC trading took place on Robinhood’s platform during stonk-fever is irony not lost on this publication.

Here’s what things look like this morning, per Yahoo Finance:

Recall that Robinhood went public at $38 per share, the low end of its range, and sank in its early trading sessions to below its IPO price. Now, it’s worth $54 per share.

Cool.

Normally we’d crack a joke and close this small news item here, but with Robinhood’s IPO featuring a unique twist on the traditional public offering, we have to do a bit more work. When it went public, Robinhood reserved a chunk of its equity for purchase by its own users. The impact of this was that more retail investors likely owned Robinhood equity at the start of its trading life than would be normal with a traditional IPO.

One hypothesis regarding Robinhood’s somewhat slack early trading performance was that early retail demand for its shares was sated by its effort to allow its users to buy stock in its shares, leading to a less-skewed supply/demand curve when it debuted.

Things have changed. What’s going on? Last week, an analyst put a $65 per share price target on the stock. And there are a handful of other ratings to chew on. But the wild swing in the price of Robinhood today appears from our vantage point to be another stonk moment. The stock is being traded like a short-squeeze, even if some market participants are skeptical of the idea due to what they view as a limited short interest in the company.

Checking the Robinhood IR page, there’s no news. Robinhood did not recently report earnings. And the company’s recent 606 filings that deal with PFOF incomes seemed to match up with expectations in revenue terms regarding what the company detailed in its Q2 2021 flash numbers. Perhaps there was more crypto in there than expected, but nothing truly wild.

It appears that Robinhood is simply going up because it is. This happens in 2021; we just have to get used to it.

But what matters most for our purposes is that Robinhood’s decision to sell some IPO stock to its users did not manage to create so much float for the now-public unicorn to diminish weird trading. You can go public in an unusual manner and still catch a stonk wave. Now we know.

Powered by WPeMatico

Robinhood priced at $38 per share this week, opened flat and closed its first day’s trading yesterday worth $34.82 per share, or a bit more than 8% underwater. The company posted a mixed picture today, falling early before recovering to breakeven in late-morning trading.

It wasn’t the debut that some expected Robinhood to have.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

To close out the week, we’re not going to noodle on banned Chinese IPOs or do a full-week mega-round discussion. Instead, let’s parse some notes from a chat The Exchange had with Robinhood’s CFO about his company’s IPO and go over a few reasonable guesses as to why we’re not wondering how much money Robinhood left on the table by pricing its public offering lower than it closed on its first day.

Let’s not be dicks about it. The time for Twitter jokes was yesterday. We’ll put our thinking caps on this morning.

Let’s not be dicks about it. The time for Twitter jokes was yesterday. We’ll put our thinking caps on this morning.

Chatting with Robinhood CFO Jason Warnick earlier this week, we wanted to know why this was the right time for Robinhood to go public.

Now, no public company CEO or CFO will come out and directly say that they are going public because they think that they can defend — or extend — their most recent private valuation thanks to current market conditions.

Instead, execs on IPO day tend to deflect the question, pivoting to a well-oiled bon mot about how their public offering is a mere milestone on their company’s long-term trajectory. For some reason in our capitalist society, during an arch-capitalist event, by a for-profit company, leaders find it critical to downplay their IPO’s importance.1

With that in mind, Warnick did not say Robinhood went public because the IPO market has recently rewarded big-brand consumer tech companies like Airbnb and DoorDash with strong debuts. And he didn’t say that with tech shares near all-time highs and a taste for high-growth concerns, the company was likely set to enter a market that would be willing to price it at a valuation that it found attractive.

Powered by WPeMatico

Today’s WWDC keynote from Apple covered a huge range of updates. From a new macOS to a refreshed watchOS to a new iOS, better privacy controls, FaceTime updates, and even iCloud+, there was something for everyone in the laundry list of new code.

Apple’s keynote was essentially what happens when the big tech companies get huge; they have so many projects that they can’t just detail a few items. They have to run down their entire parade of platforms, dropping packets of news concerning each.

But despite the obvious indication that Apple has been hard at work on the critical software side of its business, especially its services-side (more here), Wall Street gave a firm, emphatic shrug.

This is standard but always slightly confusing.

Investors care about future cash flows, at least in theory. Those future cash flows come from anticipated revenues, which are born from product updates, driving growth in sales of services, software, and hardware. Which, apart from the hardware portion of the equation, is precisely what Apple detailed today.

And lo, Wall Street looked upon the drivers of its future earnings estimates, and did sayeth “lol, who really cares.”

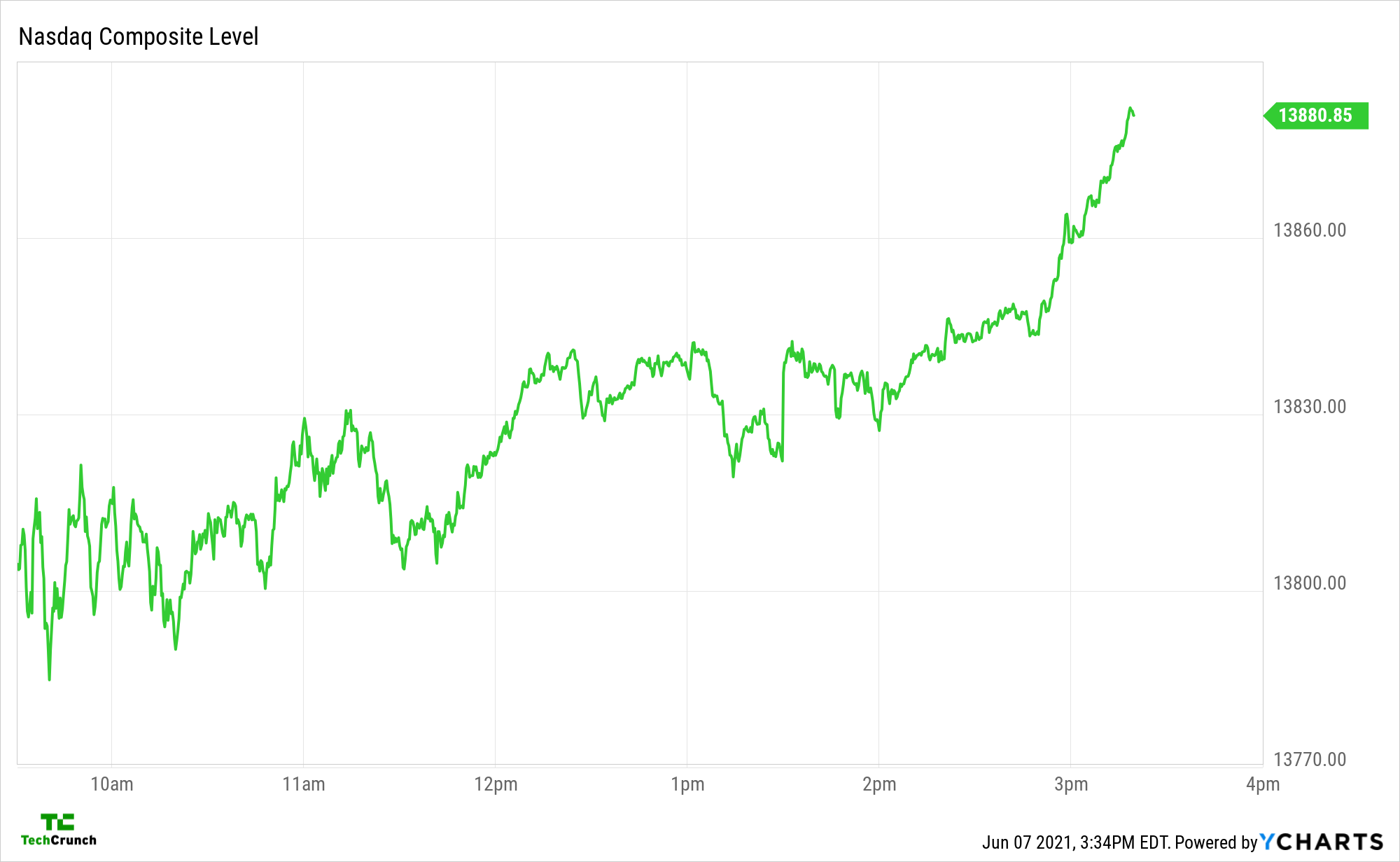

Shares of Apple were down a fraction for most of the day, picking up as time passed not thanks to the company’s news dump, but because the Nasdaq largely rose as trading raced to a close.

Here’s the Apple chart, via YCharts:

And here’s the Nasdaq:

Presuming that you are not a ChartMaster , those might not mean much to you. Don’t worry. The charts say very little all-around so you are missing little. Apple was down a bit, and the Nasdaq up a bit. Then the Nasdaq went up more, and Apple’s stock generally followed. Which is good to be clear, but somewhat immaterial.

, those might not mean much to you. Don’t worry. The charts say very little all-around so you are missing little. Apple was down a bit, and the Nasdaq up a bit. Then the Nasdaq went up more, and Apple’s stock generally followed. Which is good to be clear, but somewhat immaterial.

So after yet another major Apple event that will help determine the health and popularity of every Apple platform — key drivers of lucrative hardware sales! — the markets are betting that all their prior work estimating the True and Correct value of Apple was dead-on and that there is no need for any sort of up-or-down change.

That, or Apple is so big now that investors are simply betting it will grow in keeping with GDP. Which would be a funny diss. Regardless, more from the Apple event here in case you are behind.

Powered by WPeMatico

After years in the backwaters of venture capital, edtech had a booming 2020. Not only did its products become must-haves after schools around the globe went remote, but investors also poured capital into leading projects. There was even some exit activity, with well-known edtech players like Coursera going public earlier this year.

But despite a rush of private capital — which has continued into this year, as we’ll demonstrate — edtech stocks have taken a hammering in recent weeks. So while venture capitalists and other startup investors are pumping more capital into the space in hopes of future outsize returns, the stock market is signaling that things might be heading in the other direction.

Who’s right? One investor that The Exchange spoke to noted that market turbulence is just that, and that he’s tuning into activity but not yet changing his investment strategy. At the same time, the recent volatility is worth tracking in case it’s a preview of edtech’s slowdown.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Let’s look at the changing value of edtech stocks in recent months, parse some preliminary data via PitchBook that provides a good feel for the directional momentum of edtech venture capital, and try to see if there’s irrational exuberance among private investors.

You could argue that it’s public investors who are suffering from irrational pessimism and that private-market investors have the right of it. But since public markets price private markets, we tend to listen to them. Let’s go!

We’re sure that you want to get into the private-market data, so we’ll be brief in describing the public-market carnage. What follows is a digest of edtech stocks and their declines from recent highs:

Powered by WPeMatico

This morning the tech-heavy Nasdaq Composite index is off 2.34% after falling yesterday. Shares of Tesla are off more than 6% today, now mired in a bear-market correction after reaching new all-time highs earlier this year. Apple stock is worth $122.02 per share, down from its recent highs of more than $145.

After a long period of time when it felt like tech stocks only went up, the recent correction is starting to feel material.

There are other ways to measure the selloff. Bessemer’s cloud index is off 4.5% today, after falling over 5% yesterday. And the now-infamous $ARKK, or ARK Innovation ETF that many investors have used as a proxy for growthy tech stocks, is off 6.6% today after falling 5.9% yesterday.

Hell, even bitcoin has taken a pounding in the last few days, after its recent, relentless rise.

What’s driving the rapid turnaround in the value of tech companies, tech-focused indices and tech-adjacents, like cryptocurrencies? Not merely one thing, of course, in an environment as complex as the world’s capital markets. But there is a rising narrative that you should consider.

Namely that the money-is-cheap-and-bond-yield-is-garbage-so-everyone-is-putting-money-into-stocks trade is losing steam. As some yields rise, bonds are become more attractive bets. And as COVID-19 vaccines roll out, some investors are pushing their stock-market bets into categories other than tech.

The result is that the landscape of value is shifting; the winds that were at the back of every tech company are receding, at least for now. If the changed weather persists until the very investment climate that tech stocks exist in reaches a new equilibrium, we could see the appetite for tech IPOs lessen, late-stage private valuations for startup shares dip, and more.

Here’s CNBC from earlier today on what’s changing:

Stocks dropped again on Tuesday as tech shares continued to tumble in the face of higher interest rates and a rotation into stocks more linked to the economic comeback.

Here’s The Wall Street Journal on the same theme, from yesterday:

The lift in yields largely reflects investor expectations of a strong economic recovery. However, the collateral damage could include higher borrowing costs for businesses, more options for investors who had seen few alternatives to stocks and less favorable valuation models for some hot technology shares, investors and analysts said.

And here’s Barrons from this morning, noting that what we’re seeing at home is not merely a U.S. issue:

While members of the NYSE FANG+ index including Tesla, Facebook and Apple have dropped sharply as the yield on the 10-year Treasury has climbed, the sector also is on the retreat overseas.

Powered by WPeMatico

During yesterday’s tense voting and this morning, shares of American-listed technology companies are shooting higher.

The tech-heavy Nasdaq composite is up around 3.35% this morning, more than double what the broad S&P 500 index is currently managing. SaaS and cloud stocks kicked off the day up a staggering 4.98%, a sharp rally in the value of smaller, more growth-oriented technology companies.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

For technology companies on the wings of the IPO market, it’s great news.

In 2020 it can be easy to forget, but tech stocks do not have to rise. They merely have in recent months, perhaps warming the waters for more technology debuts as the fourth quarter races toward its midpoint. The Exchange has heard whispers from several folks that the late-November/early-December period could be active for new filings, bringing rising stocks and pent-up demand together for a possible IPO run.

We’ll see. Today’s rally — and ballot measure results in California — could be the push companies like Airbnb and DoorDash needed to stop faffing around with private filings.

We’ll see. Today’s rally — and ballot measure results in California — could be the push companies like Airbnb and DoorDash needed to stop faffing around with private filings.

In pedestrian terms, the getting is good right now for public tech companies, so if you are going to go public, go get got while the getting stays good.

Today, let’s examine recent market gains for tech stocks and remind ourselves who is expected to go public next. Then, of course, chat about all the unicorns on the unofficial IPO list who could find a greased path ahead of them toward a flotation.

Big tech stocks are gaining, small stocks are up and software companies are hot. The NASDAQ is now less than 5% away from its all-time highs, and the Bessemer Cloud Index is now just 9% down from its own, a rebound from its prior status in correction territory. (A correction occurs when an index falls 10% or more from highs.)

So, who does the rally help? Let’s rock through a list:

Powered by WPeMatico

Now that I’ve offered an overview to help you think through where concentrated stock sits in your overall plan, let’s take a closer look at why selling can be challenging for some.

In the following section, I reveal the facts of the concentrated stock “get rich” myths that reside in the minds of many first-time concentrated stock owners, and I show why it is prudent to consider greater diversification.

Keep reading to learn more about the benefits of diversification, discover how much company stock is likely too much to hold, and the options you have when it comes to diversifying strategically.

There are several hard facts to keep in mind in contemplating maintaining a concentrated position:

The odds of any new IPO being among the top 4% is just slightly better than hitting your lucky number on the roulette wheel. But is your investment portfolio success and the odds of achieving your long-term financial goals something you want to spin the wheel on?

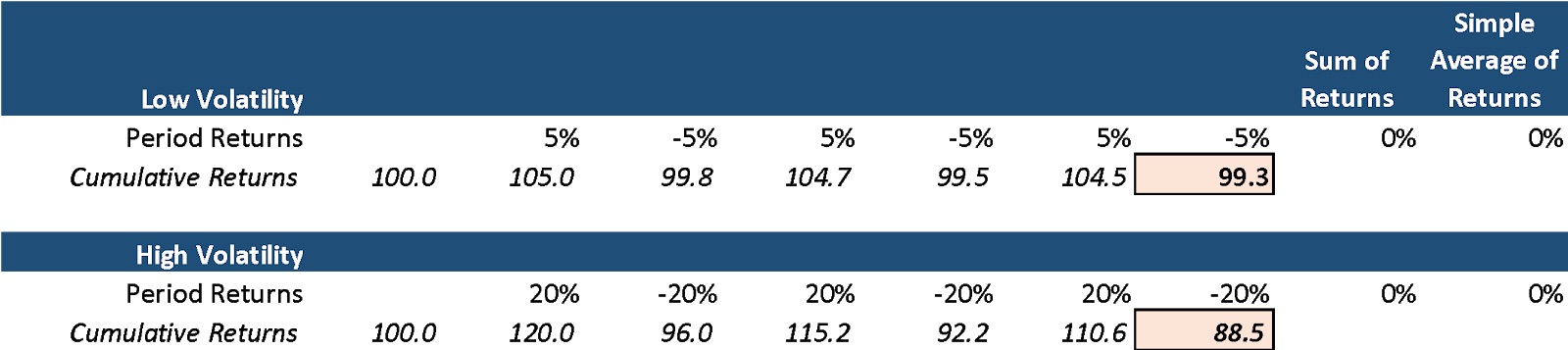

Excess volatility can harm returns. Note the example below that shows the comparison between a low-volatility diversified portfolio versus a high-volatility concentrated portfolio. Despite the same simple average return, the low-volatility portfolio below materially outperforms the high-volatility portfolio.

Image Credits: Peyton Carr

Beyond the math, unexpected spikes in volatility can cause significant price declines. Volatility increases the chances that an investor reacts emotionally and makes a poor investment decision. I’ll cover the behavioral finance aspect of this later. Lowering your portfolio volatility can be as simple as increasing your portfolio diversification.

The Russell 3000, an index representing the 3,000 largest U.S.-based publicly traded companies, has lower volatility when compared against 95%+ of all single stocks. So, how much return do you give up for having lower volatility?

According to Northern Trust Research, the 5.96% annualized average return of the Russell 3000 is 0.73% more than the 5.23% return of the median stock. Additionally, owning the Russell 3000, rather than a single stock, eliminates the likelihood of catastrophic loss scenarios — more than 20% of shares averaged a loss of more than 10% per year over a 20-year time frame.

If this establishes that the avoidance of overly concentrated portfolios is important, how much stock is too much? And at what price should you sell?

We consider any stock position or exposure greater than 10% of a portfolio to be a concentrated position. There is no hard number, but the appropriate level of concentration is dependent on several factors, such as your liquidity needs, overall portfolio value, the appetite for risk and the longer-term financial plan. However, above 10% and the returns and volatility of that single position can begin to dominate the portfolio, exposing you to high degrees of portfolio volatility.

The company “stock” in your portfolio often is only a fraction of your overall financial exposure to your company. Think about your other sources of possible exposure such as restricted stock, RSUs, options, employee stock purchase programs, 401k, other equity compensation plans, as well as your current and future salary stream tied to the company’s success. In most cases, the prudent path to achieving your financial goals involves a well-diversified portfolio.

Facts aside, maintaining a concentrated position in your company stock is far more tempting than taking a more measured approach. Token examples like Zuckerberg and Bezos tend to outshine the dull rationale of reality, and it’s hard to argue against the possibility of becoming fabulously wealthy by betting on yourself. In other words, your emotions can get the best of you.

But your goals — not your emotions — should be driving your investment strategy and decisions regarding your stock. Your investment portfolio and the company stock(s) within it should be used as tools to achieve those goals.

So first, we’ll take a deep dive into the behavioral psychology that influences our decision-making.

Despite all the evidence, sometimes that little voice remains.

“I want to hold the stock.”

Why is it so hard to shake? This is a natural human tendency. I get it. We have a strong impetus to rationalize our biases and not believe we are vulnerable to being influenced by them.

Becoming attached to your company is common, since after all, that stock has made you, or has the potential of making you wealthy. More often than not, selling and diversifying is the tough, but more rational decision.

Numerous studies have furnished insights into the correlation between investing and psychology. Many unrecognized psychological barriers and behavioral biases can influence you to hold concentrated stock even when the data shows that you should not.

Understanding these biases can be helpful when deciding what to do with your stock. These behavioral biases are hard to spot and even harder to overcome. However, awareness is the first step. Here are a few more common behavioral biases, see if any apply to you:

Familiarity bias: Familiarity is likely why so many founders are willing to hold concentrated positions in their own company’s stock. It is easy to confuse the familiarity with your own company with the safety in the stock. In the stock market, familiarity and safety are not always related. A great (safe) company sometimes can have a dangerously overvalued stock price, and terrible companies sometimes have terrifically undervalued stock prices. It’s not just about the quality of the company but the relationship between the quality of a company and its stock price that dictates whether a stock is likely to perform well in the future.

Another way this manifests is when a founder has less experience with stock market investing and has only owned their company stock. They may think the market has more risk than their company when in actuality, it is usually safer than holding just their individual position.

Overconfidence: Every investor is exhibiting overconfidence when they hold an overly concentrated position in an individual stock. Founders are likely to believe in their company; after all, it already achieved enough success to IPO. This confidence can be misplaced in the stock. Founders often are reluctant to sell their stock if it has been going up since they believe it will continue to go up. If the stock has sold off, the opposite is true, and they are convinced it will recover. Often, it is challenging for founders to be objective when they are so close to the company. They commonly believe that they have unique information and know the “true” value of the stock.

Anchoring: Some investors will anchor their beliefs to something they experienced in the past. If the price of the concentrated stock is down, investors may anchor their belief that the stock is worth its recent previous higher value and be unwilling to sell. This previous value of the stock is not an indicator of its real value. The real value is the current price where buyers and sellers exchange the stock while incorporating all presently available information.

Endowment effect: Many investors tend to place a higher value on an asset they currently own than if they did not own it at all. It makes it harder to sell. An excellent way to check for the endowment effect is to ask yourself: “If I did not own these shares, would I purchase them today at this price?” If you are not willing to purchase the shares at this price today, it likely means you are only holding onto the shares because of the endowment effect.

A fun spin on this is to look into the IKEA effect study, which demonstrates that people assign more value to something that they made than it is potentially worth.

When framed this way, investors can make more intentional decisions on whether to continue holding concentrated stock or selling. At times, these biases are hard to spot, which is why having a second person, a co-pilot, or an advisor, is helpful.

Congratulations to those of you with a concentrated stock position in your company; it is hard-earned and likely represents a material wealth. Understand, there is no “right” answer when it comes to managing concentrated stock. Each situation is unique, so it is essential to speak with a professional about options specific to your situation.

It starts with having a financial plan, complete with specific investment goals that you want to achieve. Once you have a clear picture of what you want to accomplish, you can look at the facts in a new light and gain a deeper appreciation for the dangers of holding a concentrated position in company stock versus the benefits of diversification, considering all of the implications and opportunities involved in rational decision-making and investment behavior.

Most individuals understand they can simply and directly sell their equity, but there are a variety of other strategies. Some of these opportunities may be far better at minimizing taxes or better at achieving the desired risk or return profile. Some might wonder what the best timing is to sell. I will cover these topics in the final article of the series.

Powered by WPeMatico

The novel coronavirus has been devastating for many people, families and communities — and the consequences are still being calculated. The tech world has seen wave after wave of layoffs, sometimes multiple waves at one company only weeks apart. Some startups have lost nearly all their revenue, and depending on their cash reserves, have little hope of recovering.

For VCs, the last two months have been an exercise in triage.

Partners have gone through their entire investment portfolios to identify the winners, what’s salvageable and what (at least in their minds) has no hope of resuscitation. If you are in the first two groups, it’s back to whatever normal looks like in the midst of a global pandemic and a deep economic recession.

But what if you suddenly get a call informing you that your investor — perhaps your biggest champion to date — is going to cut the rope and write you off entirely?

That’s what we are going to talk about today.

Before we go anywhere, be thankful if you even know how your investors are judging your startup. Most, unfortunately, will couch the terms they use (“we will be engaging less” or perhaps “we are unlikely to do our pro rata going forward”) rather than just saying directly, “we are writing you off; don’t call us — we’ll call you.” That’s polite and face-saving for all parties, but the lack of transparency can make decisions down the road much harder. It’s better to know where you stand, even if the news is hard.

The first step to approaching this situation is to get your bearings. Much like during a fundraise process, it’s not uncommon for different investors on your cap table to reach different conclusions about your startup’s potential. One investor may write you off, while another has you marked at a more neutral valuation or even positively. This can absolutely be frustrating, and given the emotion of this situation, it can be hard to rationally accept that an investor who once believed in you no longer does so.

Powered by WPeMatico

If you’ve been lucky enough to keep your job or business, you almost certainly know someone who wasn’t so fortunate.

Thousands have lost their jobs as companies significantly reduce workforces to adjust to uncertainties and economic challenges created by COVID-19. Many of these people in tech are now faced with a number of questions, from how they’ll pay next month’s rent to whether they’re eligible for unemployment. One area that is particularly confusing is what to do if your compensation package was tied to equity.

Here are some ways I suggest approaching the issue.

Layoffs have become part and parcel of the current economic crisis with unemployment figures skyrocketing to record highs as a result of COVID-19. From multinational conglomerates to mom-and-pop stores, everyone is feeling the impact, and the startup sector is no different.

Despite difficult circumstances, the silver lining for employees is that we have seen many management teams go the extra mile to help their teams, especially when it comes to equity. Compared to traditional layoff situations, companies in the COVID-19 era are offering generous extensions and accelerated vesting on their options, which is undeniably good news for employees with equity.

Typically, equity plans come with a 90-day exercise window after employment termination. That means that if you leave the company, you will have to exercise your options within 90 days or they go back to the company. However, lots of management teams have decided to extend these deadlines many years out given the circumstances.

While layoffs are not easy, it’s been great to see management teams doing the right thing when it comes to equity for their employees who have been laid off. Offering extensions is a benefit that employers should be offering their employees who have helped build the company.

If your company is not offering this, consider negotiating and asking for an extension. This is the right thing to do for employees who are now out of work and a paycheck for the foreseeable future. Both options do not require the company to pay cash at the moment, so there are few reasons a company should deny this request in this environment.

Even if you are granted an extension to exercise your options, employees that hold incentive stock options (ISOs) should look into exercising their options now to maximize their equity’s value.

Many companies are offering extensions for option exercises. While this is great in that it gives employees more time to figure out their exercise situation, waiting past the 90-day window may have much bigger tax consequences that employees need to consider.

ISOs are much more tax advantageous compared to non-qualified stock options (NSOs). They are not taxed under standard income tax and if you sell the stock two years after grant date and one year after exercise date, you sell them as part of a qualifying disposition. In short, this allows you to effectively convert everything north of your strike price to preferential long-term capital gain rates.

As part of offering these tax advantages, the tax code has limitations on ISOs. Most relevant to us at this point is that the fact that you cannot have ISOs past 90 days after you are no longer an employee. This means that even if your company allows an extension on your stock options past the typical 90-day expiration window, your ISOs will convert to NSOs and lose their tax benefit.

This creates a potential planning opportunity that employees who have been laid off need to consider. If you feel good about the upside of the company, then you should consider exercising your ISOs today to capture the potential tax benefits rather than letting them convert to NSOs. Employees who wait risk putting themselves in the same difficult situation once the extension ends at typically less favorable conditions due to an increased 409A valuation.

In light of the economic slowdown many companies have begun to cut costs. Reduced pay or furloughing employees has become the new norm as businesses of all sizes struggle to navigate these changing times.

It can obviously be concerning if you find yourself in this situation. But for startup employees, the COVID-19 crisis could provide an opportunity to negotiate your compensation package to make up for this decrease, and even set yourself up to prosper in the future.

Startups typically offer equity as a means of deferred compensation and as a way to incentivize employees to own a piece of the company they are building. The compensation is deferred as most startups are cash-strapped and cannot afford to pay you what a larger company may be able to.

If your company is now asking you to take a pay cut, or even take no pay during this time, you should consider asking for additional equity to make up for the lost compensation. While not all companies may be amenable to offering more equity, there is no cash outlay from the company’s standpoint, so it’s an efficient way for your company to compensate you for your sacrifice while preserving their cash.

In addition, offering more equity shows a commitment from management to their employees during this difficult time. It may be the win-win scenario for your company and yourself in the long-run so it’s worth having the conversation with management to discuss if this is available for you.

If your company does offer you more equity, make sure you ask whether the 409A (or fair market value) of the company is being updated. With revised forecasts given the COVID-19 situation, it may be possible for your company to issue your stock at a lower strike price if the company revalues its 409A.

I can sympathize with startup employees right now because I faced a similar situation when I left a startup that I had joined as employee number four and was forced to wave goodbye to the equity I had banked on.

If you want to take action on equity but don’t know where to start, now might be a good time to brush up on how your stock options work. As the economy begins to reopen, there’s a good chance we’ll see a rush for candidates in tech as companies compete to bring in some of the extremely talented folks who lost their jobs this week.

Those who have a good understanding of equity may be positioned for a big payday down the line.

Powered by WPeMatico