Steve Jang

Auto Added by WPeMatico

Auto Added by WPeMatico

Venture capitalists often mutter, “I haven’t seen anything I like lately.” Founders frequently complain that “investors are back-seat drivers who won’t get their hands dirty.” A $55 million fund with a fresh approach is aiming to address both those issues.

Steve Jang and Kanyi Maqubela are two exceedingly smart and sweet guys who couldn’t help but come up with ideas for startups. Jang co-founded music apps Imeem and Soundtracking, meanwhile serving as an early Uber advisor and angel investor in Coinbase. Maqubela worked in operations at career network Doostang (acquired by Universum Global) and solar startup One Block Off the Grid (acquired by NRG) before rising to general partner at Collaborative Fund.

Today the pair officially launch Kindred Ventures to form startups as well as fund them.

“We don’t want to wait for people to come around and solve the problems we think matter,” says Jang. “We’d rather proactively assemble an amazing team to go tackle that problem,” Maqubela follows up. But Kindred Ventures will also step up and lead seed rounds, then help startups orchestrate their follow-on fundraises.

Kindred Ventures partner and co-founder Steve Jang

“The ethos is empathy — to take a very adaptive coaching and mentorship model,” Jang tells me. That means partnering with startups, not merely offering arm’s-length investing. By keeping the portfolio size low, Jang and Maqubela plan to turn concentrated conviction and outsized, hands-on effort into big stakes in tomorrow’s top companies.

“I originally wanted to call the fund Kindred Spirits, but it sounds a little too woo-woo,” Jang says with a laugh. From multiple interviews with the team and its portfolio, though, that’s really the vibe Kindred Ventures is going for — to be the first people founders call when they’re in crisis… whether they need answers or just some cheering up.

Beyond the warm smiles, Kindred already has a strong track record from its prototype phase under Jang’s solo operation since 2014. He’d made a reputation for himself as a fixer through his advising work during Uber’s scrappy early years starting in 2009. It began with Jang writing Garrett Camp a check for his side-project. As the company blossomed without full-time employees, Jang pitched in wherever he could.

After Imeem’s sale to Myspace and later Soundtracking’s acquisition by Rhapsody, Jang made about 50 angel investments of around $25,000 to $250,000 in companies like Coinbase, Blue Bottle Coffee, Postmates and Zymergen under the name Kindred Ventures. Instead of just throwing money around, “I’d help a co-founder — sit down and work with them on product, their presentation for seed funding, hiring their first employees, finding a co-founder — it was quite different from how VCs operate.” Still, he wanted to lead more investments like his favorite seed funds First Round and True Ventures while remaining a thick-or-thin squire to his startups.

But to pour that kind of sweat into the portfolio, Jang needed the help of someone who could dig deep and become an ally to founders in any vertical. He needed someone like Kanyi.

After his stints in operations, Maqubela went on to work at Collaborative Fund for seven years, rising to partner at the firm looking for the intersection of positive impact and profit. He tells me developed a thesis about “what does it mean to be a techno-optimist?: to believe that technology is amoral but can be oriented towards good.”

Maqubela’s super-power is learning. I knew him from Stanford, and now the same reputation precedes him through his portfolio of angel investments like Earnest and Buffer. He’ll immerse himself in any topic or industry, read and call people until he truly gets it and then wedge his entrepreneurial skill set into the cracks to firm up an idea. Still relatively new to venture, Maqubela was seeking someone with a well-worn process for investing and a big heart for what founders go through. He was looking for Steve.

Kindred Ventures partner and co-founder Kanyi Maqubela

The coincidental co-investors became friends, then deliberately funded startups side by side, and now are taking the leap as Kindred Ventures. Together they want to redefine “What does it mean to invest at t=0?. What do they really need?,” Maqubela says.

The plan is to fund about 25 companies through pre-seed and seed per fund, which they’ll raise every two to three years. Kindred is vertical agnostic, but it has a soft spot for the future of cities, work and living. It’s also keen on marketplaces, material science, food innovation, deep tech, enterprise SAAS and developer tools.

Jang and Maqubela are learning from each other day by day, at home and in the office. They’ve each got their own toddler son to juggle alongside Kindred. Added responsibility seems to have made both of them conscious of how each minute counts, no matter who they’re with. The result is you’ll often hear the word “nicest” whenever people describe the pair.

So far Kindred Ventures has funded nine startups from its $55 million initial fund. It’s helped form two companies and hopes to do four to eight per fund. But Kindred won’t be taking founder-level equity in those. Instead it just wants the opportunity to lead the seed round and own 10% to 20% by the time of the Series A.

That makes Kindred Ventures distinct from most startup studios like Atomic that aim for bigger ~30% stakes. “The Studios are creating whole platform teams, services teams, only work on their own ideas, and own a considerable amount of equity,” Jang notes. By leaving more shares for the real CEO, “We’d be able to work with a stronger profile of founders” while avoiding spending so much time per company that the model becomes unscalable. “We’re there at the formation of the company, but it’s not our company.”

Kindred’s two formations come from the disparate medicine and blockchain worlds. Maqubela became an expert in cardiology to help start Heartbeat, which does in-person and remote heart-health diagnostics. “I have a clear bullshit meter for when non-healthtech people try to get into it,” but Maqubela really figured it out, Heartbeat CEO Jeff Wessler, MD, tells me.

On his experience with Kindred, “It’s ‘we’re there for you when you need us’ rather than ‘we’re there for you when we fund you and then we move on,’ ” Wessler says. “Very quickly this evolved into Steve and Kanyi being my absolute numbers 1 and 2.” The investors gave Wessler Entrepreneurship 101 coaching, provided Heartbeat’s first funding and helped it build a team. With their help, the first-time founder has sidestepped common pitfalls and is already turning patients into customers with its $2.5 million in funding.

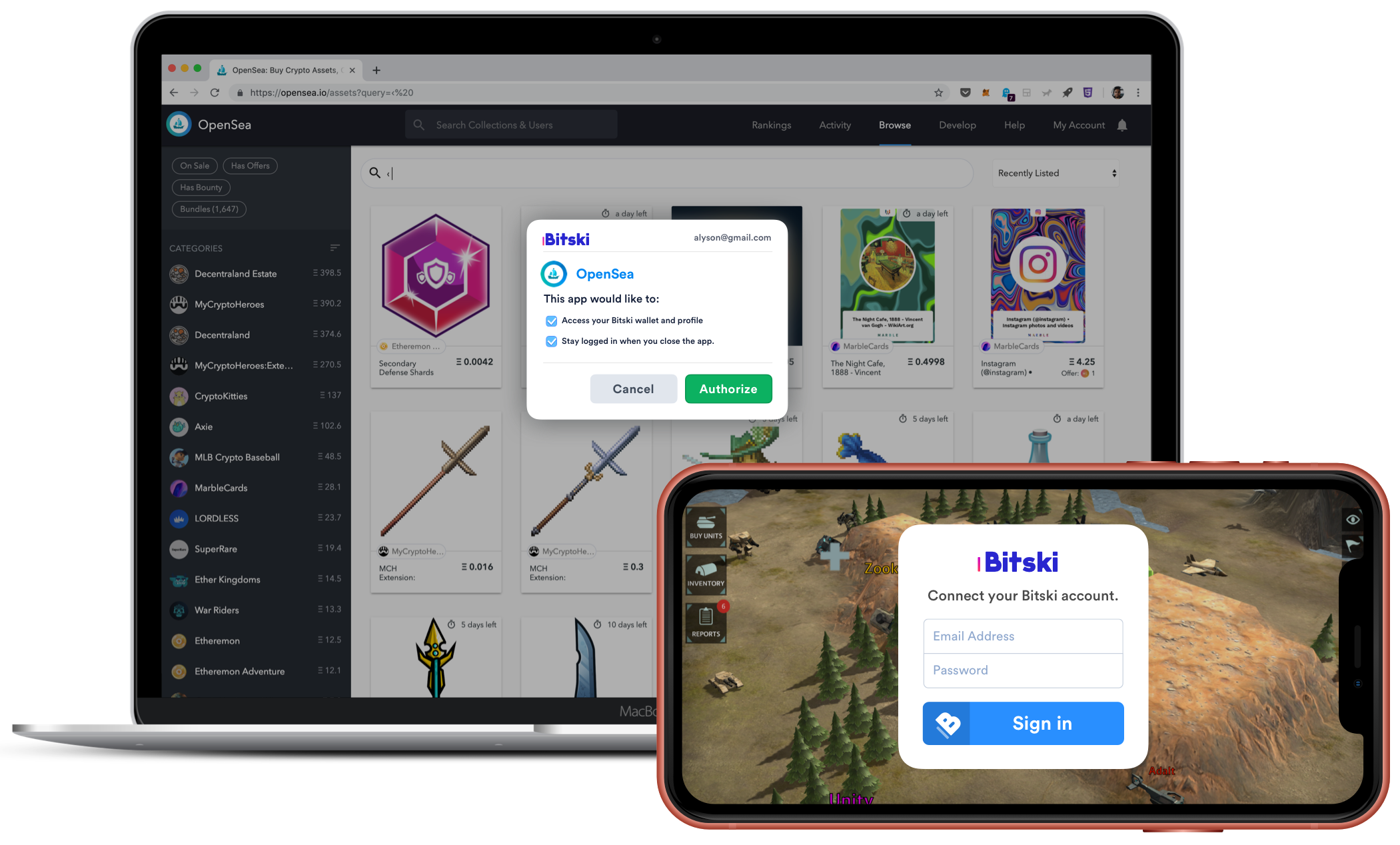

Bitski, a blockchain app login platform, has quickly leveraged Kindred’s support with formation into big funding from top investors. Bitski CEO Donnie Dinch tells me, “In the early days, Steve would be in the office with us, late night jamming on ideas around the evolution of the blockchain space, fundamental products that needed to exist, early use cases etc. There’s a lot of money available for seed-stage projects, but it can be difficult to find an investor willing to grind with the team through the days of pre product-market fit.”

Bitski actually started as collaborative video production app Riff. But Jang and Maqubela’s advice helped it solidy pivot into developer tools for decentralized apps. It’s since gone on to raise $3.5 million from SV Angel, Coinbase, Galaxy Digital and the Winklevoss twins. “The collaborative tone of the relationship really stands out,” says Dinch of Kindred. “Obviously, operating with a high-touch model can take more of the partners’ time, but we haven’t noticed any drop in availability or support.”

Plenty of funds talk a lot about getting their hands dirty. Often that means hiring big teams they can assign to help founders, though, while the partners focus elsewhere. With just two support staff, Jang and Maqubela don’t have that luxury. They’re in constant contact with their investments by WhatsApp, phone and email to work through snags directly.

“They’re always super responsive,” says Michael Karnjarnaprakorn, co-founder of collectibles investing startup Otis that was backed by Kindred’s prototype fund. He cites three big value-adds. Strategy: “Anytime I’m thinking through a big decision, I call them to help me think through it,” including fundraising and product launches. Network: “They have an extremely strong network and are usually one to two degrees away from anyone.” And “everything else,” from mentorship on founder psychology to company building.

Undertaking such intense involvement in their whole portfolio would likely surface concerns about a green VC. But “Steve has essentially been doing this for a decade or so not formalized, so I don’t see any reason it can’t work,” says one of Kindred’s stealth startup founders Brian Norgard. “As companies begin to scale, my sense is they will be less effective because that’s a different game that’s more on the operations side. Still, I see a lot of value that can be created in the early innings.”

Kindred had a sort of grit and passion for early-stage founders and teams that we thought would give us an edge as we started to grow quickly,” says health insurance company Catch‘s co-founder Kristen Tyrrell.” They have been genuinely interested in our mental health. Having Steve fly in to take us to dinner and tell us we’re doing OK is surprisingly meaningful when you’re fighting on every side.”

NEW YORK, NY – MAY 10: Kanyi Maqubela of Collaborative Fund speaks onstage during TechCrunch Disrupt NY 2016 at Brooklyn Cruise Terminal on May 10, 2016 in New York City. (Photo by Noam Galai/Getty Images for TechCrunch)

But being high-touch and concerned with entrepreneurs’ well-being doesn’t mean becoming a push-over yes-man. “Founder empathy is not always founder-friendly,” says Maqubela. “It’s being able to disagree with founders, even very passionately, and still constructively working together. To be able to tell them they’re wrong but come out the other side.”

That means Kindred Ventures isn’t for every founder. Those who want their investors firmly belted in the backseat or locked in the trunk may want to look elsewhere for cash. Smart founders will take all the help they can get, and Kindred strives to give the most per dollar. Jang concludes that, “The idea may come from them or come from us, but we want to back amazing founders on a mission. It’s scratching both itches for us.”

Powered by WPeMatico

Hundreds gathered this week at San Francisco’s Pier 48 to see the more than 200 companies in Y Combinator’s Winter 2019 cohort present their two-minute pitches. The audience of venture capitalists, who collectively manage hundreds of billions of dollars, noted their favorites. The very best investors, however, had already had their pick of the litter.

What many don’t realize about the Demo Day tradition is that pitching isn’t a requirement; in fact, some YC graduates skip out on their stage opportunity altogether. Why? Because they’ve already raised capital or are in the final stages of closing a deal.

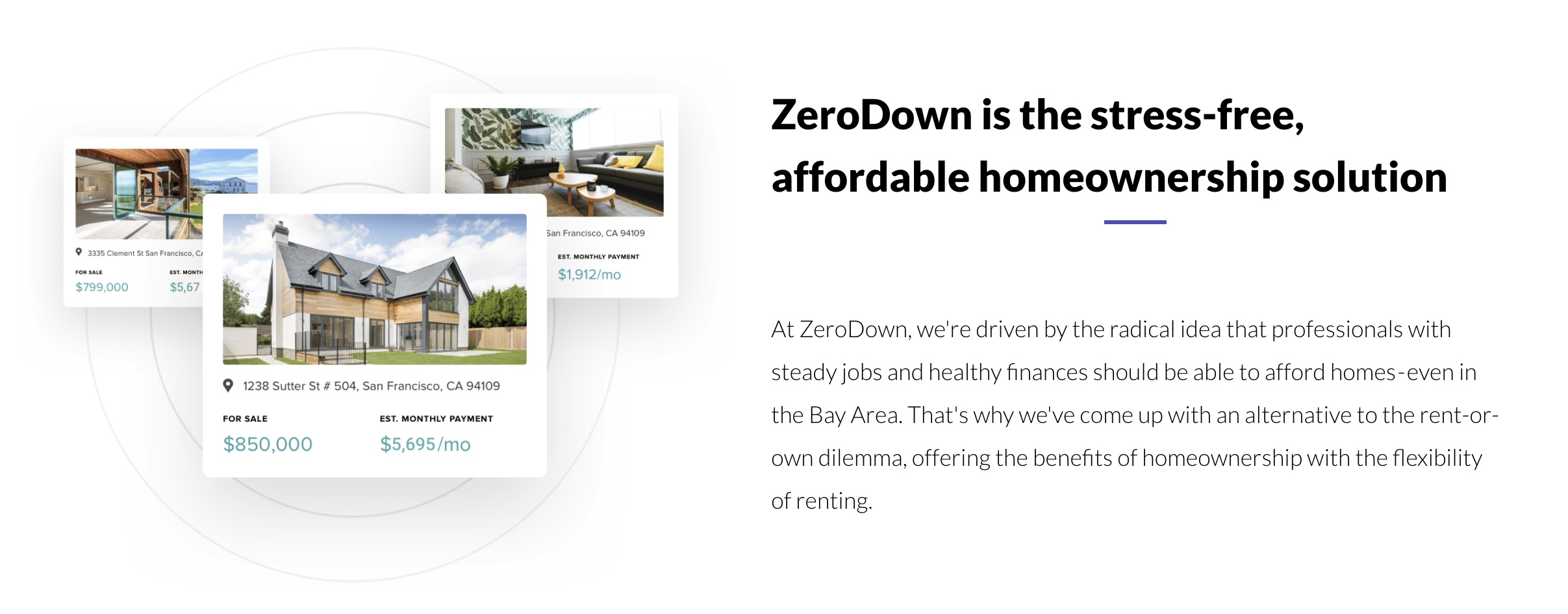

ZeroDown, Overview.AI and Catch are among the startups in YC’s W19 batch that forwent Demo Day this week, having already pocketed venture capital. ZeroDown, a financing solution for real estate purchases in the Bay Area, raised a round upwards of $10 million at a $75 million valuation, sources tell TechCrunch. ZeroDown hasn’t responded to requests for comment, nor has its rumored lead investor: Goodwater Capital.

Without requiring a down payment, ZeroDown purchases homes outright for customers and helps them work toward ownership with monthly payments determined by their income. The business was founded by Zenefits co-founder and former chief technology officer Laks Srini, former Zenefits chief operating officer Abhijeet Dwivedi and Hari Viswanathan, a former Zenefits staff engineer.

The founders’ experience building Zenefits, despite its shortcomings, helped ZeroDown garner significant buzz ahead of Demo Day. Sources tell TechCrunch the startup had actually raised a small seed round ahead of YC from former YC president Sam Altman, who recently stepped down from the role to focus on OpenAI, an AI research organization. Altman is said to have encouraged ZeroDown to complete the respected Silicon Valley accelerator program, which, if nothing else, grants its companies a priceless network with which no other incubator or accelerator can compete.

Overview .AI’s founders’ resumes are impressive, too. Russell Nibbelink and Christopher Van Dyke were previously engineers at Salesforce and Tesla, respectively. An industrial automation startup, Overview is developing a smart camera capable of learning a machine’s routine to detect deviations, crashes or anomalies. TechCrunch hasn’t been able to get in touch with Overview’s team or pinpoint the size of its seed round, though sources confirm it skipped Demo Day because of a deal.

Catch, for its part, closed a $5.1 million seed round co-led by Khosla Ventures, NYCA Partners and Steve Jang prior to Demo Day. Instead of pitching their health insurance platform at the big event, Catch published a blog post announcing its first feature, The Catch Health Explorer.

“This is only the first glimpse of what we’re building this year,” Catch wrote in the blog post. “In a few months, we’ll be bringing end-to-end health insurance enrollment for individual plans into Catch to provide the best health insurance enrollment experience in the country.”

TechCrunch has more details on the healthtech startup’s funding, which included participation from Kleiner Perkins, the Urban Innovation Fund and the Graduate Fund.

Four more startups, Truora, Middesk, Glide and FlockJay had deals in the final stages when they walked onto the Demo Day stage, deciding to make their pitches rather than skip the big finale. Sources tell TechCrunch that renowned venture capital firm Accel invested in both Truora and Middesk, among other YC W19 graduates. Truora offers fast, reliable and affordable background checks for the Latin America market, while Middesk does due diligence for businesses to help them conduct risk and compliance assessments on customers.

Finally, Glide, which allows users to quickly and easily create well-designed mobile apps from Google Sheets pages, landed support from First Round Capital, and FlockJay, the operator an online sales academy that teaches job seekers from underrepresented backgrounds the skills and training they need to pursue a career in tech sales, secured investment from Lightspeed Venture Partners, according to sources familiar with the deal.

Raising ahead of Demo Day isn’t a new phenomenon. Companies, thanks to the invaluable YC network, increase their chances at raising, as well as their valuation, the moment they enroll in the accelerator. They can begin chatting with VCs when they see fit, and they’re encouraged to mingle with YC alumni, a process that can result in pre-Demo Day acquisitions.

This year, Elph, a blockchain infrastructure startup, was bought by Brex, a buzzworthy fintech unicorn that itself graduated from YC only two years ago. The deal closed just one week before Demo Day. Brex’s head of engineering, Cosmin Nicolaescu, tells TechCrunch the Elph five-person team — including co-founders Ritik Malhotra and Tanooj Luthra, who previously founded the Box-acquired startup Steem — were being eyed by several larger companies as Brex negotiated the deal.

“For me, it was important to get them before batch day because that opens the floodgates,” Nicolaescu told TechCrunch. “The reason why I really liked them is they are very entrepreneurial, which aligns with what we want to do. Each of our products is really like its own business.”

Of course, Brex offers a credit card for startups and has no plans to dabble with blockchain or cryptocurrency. The Elph team, rather, will bring their infrastructure security know-how to Brex, helping the $1.1 billion company build its next product, a credit card for large enterprises. Brex declined to disclose the terms of its acquisition.

Y Combinator partners Michael Seibel and Dalton Caldwell, and moderator Josh Constine, speak onstage during TechCrunch Disrupt SF 2018. (Photo by Kimberly White/Getty Images)

Ultimately, it’s up to startups to determine the cost at which they’ll give up equity. YC companies raise capital under the SAFE model, or a simple agreement for future equity, a form of fundraising invented by YC. Basically, an investor makes a cash investment in a YC startup, then receives company stock at a later date, typically upon a Series A or post-seed deal. YC made the switch from investing in startups on a pre-money safe basis to a post-money safe in 2018 to make cap table math easier for founders.

Michael Seibel, the chief executive officer of YC, says the accelerator works with each startup to develop a personalized fundraising plan. The businesses that raise at valuations north of $10 million, he explained, do so because of high demand.

“Each company decides on the amount of money they want to raise, the valuation they want to raise at, and when they want to start fundraising,” Seibel told TechCrunch via email. “YC is only an advisor and does not dictate how our companies operate. The vast majority of companies complete fundraising in the 1 to 2 months after Demo Day. According to our data, there is little correlation between the companies who are most in demand on Demo Day and ones who go on to become extremely successful. Our advice to founders is not to over optimize the fundraising process.”

Though Seibel says the majority raise in the months following Demo Day, it seems the very best investors know to be proactive about reviewing and investing in the batch before the big event.

Khosla Ventures, like other top VC firms, meets with YC companies as early as possible, partner Kristina Simmons tells TechCrunch, even scheduling interviews with companies in the period between when a startup is accepted to YC to before they actually begin the program. Another Khosla partner, Evan Moore, echoed Seibel’s statement, claiming there isn’t a correlation between the future unicorns and those that raise capital ahead of Demo Day. Moore is a co-founder of DoorDash, a YC graduate now worth $7.1 billion. DoorDash closed its first round of capital in the weeks following Demo Day.

“I think a lot of the activity before demo day is driven by investor FOMO,” Moore wrote in an email to TechCrunch. “I’ve had investors ask me how to get into a company without even knowing what the company does! I mostly see this as a side effect of a good thing: YC has helped tip the scale toward founders by creating an environment where investors compete. This dynamic isn’t what many investors are used to, so every batch some complain about valuations and how easy the founders have it, but making it easier for ambitious entrepreneurs to get funding and pursue their vision is a good thing for the economy.”

This year, given the number of recent changes at YC — namely the size of its latest batch — there was added pressure on the accelerator to showcase its best group yet. And while some did tell TechCrunch they were especially impressed with the lineup, others indeed expressed frustration with valuations.

Many YC startups are fundraising at valuations at or higher than $10 million. For context, that’s actually perfectly in line with the median seed-stage valuation in 2018. According to PitchBook, U.S. startups raised seed rounds at a median post-valuation of $10 million last year; so far this year, companies are raising seed rounds at a slightly higher post-valuation of $11 million. With that said, many of the startups in YC’s cohorts are not as mature as the average seed-stage company. Per PitchBook, a company can be several years of age before it secures its seed round.

I did not talk to a single company in this batch raising under $10M post (admittedly I only was able to speak with a fraction of the 205).

— Peter Rojas (@peterrojas) March 20, 2019

Nonetheless, pricey deals can come as a disappointment to the seed investors who find themselves at YC every year but because their reputations aren’t as lofty as say, Accel, aren’t able to book pre-Demo Day meetings with YC’s top of class.

The question is who is Y Combinator serving? And the answer is founders, not investors. YC is under no obligation to serve up deals of a certain valuation nor is it responsible for which investors gain access to its best companies at what time. After all, startups are raking in larger and larger rounds, earlier in their lifespans; shouldn’t YC, a microcosm for the Silicon Valley startup ecosystem, advise their startups to charge the best investors the going rate?

Powered by WPeMatico