startups weekly

Auto Added by WPeMatico

Auto Added by WPeMatico

My big question for 2021, and the one that is on every startup’s mind, is how will a cataclysmic event such as a global pandemic show up in post-pandemic innovation? I think we’re in the early innings of seeing what “aha moments” have materialized into companies. And we won’t know the pandemic’s true impact on our psyches until the dust settles and we have an opportunity to reflect.

We do know it will be fascinating to watch. In 2020, innovators and investors were forced to stand still, and witness cracks, fractures and rubble in society in a way like never before. It was a humbling year that, for much of the tech community, was mostly spent inside, away and alone.

One reaction I’ve noticed so far — that isn’t necessarily new but comes with new weight — is a rush of innovation that focuses on reducing friction. Take trends like the rise of building in public or the unbundling of venture capital. Or remote work’s shift from enabling communication to now needing to enable passive and active collaboration. Apply the same idea to mental health, education and fitness. Heck, we’re even seeing people take the Y Combinator format and apply it to anything that makes sense, from helping operators turn into investors to helping employees try to turn their side gig into a full-time company.

While these movements didn’t begin because of the coronavirus, they all seem to have a huge, pandemic-sized asterisk next to it.

It would be easy to dismiss these movements as small and inconsequential. But, as my colleague and fellow Equity co-host Danny Crichton pointed out this week, “sometimes the most important changes in venture and startups more generally have come from lowering that last bit of friction to action.”

Lowering friction feels like the mantra with which we all need to enter 2021.

I already have hope that innovation will come from a more diverse set of people, whether it’s in a hacker house for undergraduate women or a student-founded service that matches undergraduate students to nonprofits. So, as we enter the new year — and bear with me here — I urge you to be optimistic.

The last year in tech hasn’t left people exhausted and hopeless, it’s left them energized and ready.

Maze, computer artwork. (Image Credits: Pasieka / Getty Images)

When SAP announced that Qualtrics was getting spun out in July, the full-circle moment made the Equity podcast crew jump to our mics with guesses around why. Now, months later, there’s a new S-1 filing, and more to color in. Alex Wilhelm broke down the Utah-based unicorn’s numbers, noting that it’s the second time Qualtrics has filed.

Will the second time be the charm that Qualtrics needs to actually go public this time around? I’ll let you make the call yourself once you sift through Alex’s analysis of the valuation and financials.

Blackboard Business Strategy Concept. (Image Credits: hanibaram / Getty Images)

If those three words in a single subhed elicit a certain reaction from you, Danny Crichton has a bone to pick with you. He wrote a piece this week about tech’s cynicism around anything new, underscoring how Miami’s future as a tech hub, Substack’s future as a replacement for traditional journalism and Clubhouse’s future as a social media disruptor have come under fire as expected:

The cynicism of immediate perfection is one of the strange dynamics of startups in 2020. There is this expectation that a startup, with one or a few founders and a couple of employees, is somehow going to build a perfect product on day one that mitigates any potential problem even before it becomes one. Maybe these startups are just getting popularized too early, and the people who understand early product are getting subsumed by the wider masses who don’t understand the evolution of products?

Danny’s argument is to give these companies a little more grace to execute on a vision they themselves are not even close to scratching the surface of. When it comes to holding specific decision-makers and businesses to a certain standard, I prefer a more fluid conversation. But I do agree that writing off a business because it hasn’t done everything correctly from the start can hurt progress. It’s easy to be grumpy, but why not choose to be an optimist? Tell me your optimistic bets by responding to this newsletter or tweeting me @nmasc_.

Skyline of downtown Miami, Florida looking toward the Brickell neighborhood on Biscayne Bay. Brickell is one of the largest financial districts in the United States and also has many high-rise residential condominium and apartment towers. (Image Credits: John Coletti / Getty Images)

Speaking of humbling moments and optimism, our own Sarah Perez wrote a piece this week about EarlyBird, an app that lets families and friends gift investments to children. While Acorns and Stash have similar offerings, EarlyBird is bringing a fresh UX play to financial literacy, freedom and education. There’s a ton of work left to be done, hurdles to deal with, and giant unicorns to compete with. EarlyBird, however, is only weeks old, so there’s much to watch out for.

VP Caleb Frankel, now EarlyBird COO, explained the early inspiration:

“This all started with a problem I experienced years ago when my beautiful baby niece was born. I found myself head over heels and spending hundreds and hundreds of dollars on just the most ridiculous stuff — pretty much just junk gifts,” he says. “I wanted to have a larger impact in her life and something that she could really use when she grew up.”

Image Credits: oxygen (opens in a new window) / Getty Images

Attending CES 2021? TechCrunch wants to meet your startup

Gift Guide: Last-minute subscriptions to keep the gifts going all year

Seen on Extra Crunch

How artificial intelligence will be used in 2021

On the diversity front, 2020 may prove a tipping point

The 2020 boom in climate tech SPACs

2021 will be a calmer year for semiconductors and chips (except for Intel)

Understanding Europe’s big push to rewrite the digital rulebook

Seen on TechCrunch

China lays out ‘rectification’ plan for Jack Ma’s fintech empire Ant

NSO used real people’s location data to pitch its contact-tracing tech, researchers say

India’s slow 2020 told through dollars and cents

An earnest review of a robotic cat pillow

The Equity pod put together a 2021 predictions episode (with Chris Gates, our producer, making a guest appearance on the mic as well!). We talk about IPO candidates, San Francisco and the future of drugs.

2020 brought several million downloads to the podcast, and we’re super thankful to all of y’ all for tuning in. This year will be even bigger, better and, hey, maybe we’ll even get to make fun of each other in person too.

Till next week,

Natasha Mascarenhas

Powered by WPeMatico

Editor’s note: Get this free weekly recap of TechCrunch news that any startup can use by email every Saturday morning (7 a.m. PT). Subscribe here.

Maybe it is a stock market bubble, or a tech-stock bubble at least. And maybe DoorDash, Airbnb and C3.ai and their bankers should have priced higher regardless to take advantage of all of the enthusiasm. It’s hard to avoid reactions like that, after DoorDash, for example, doubled its final private share price to $102 for its public debut on Wednesday — only to see the price climb to $175 at the end of the week.

Or maybe none of this will matter, because the future is way bigger and the companies are going to get there regardless. That’s what Saar Gur tells Connie Loizos this week about DoorDash, which he had invested in many years ago:

I actually started my career at Lehman Brothers on the investment banking team, and so having seen the IPO process, while I can appreciate [frustration that a] company left some money on the table based on the pricing, the tactical challenge [is that] it’s very hard to predict. You know what the market will bear once it moves to retail investors.

What’s exciting to me is [that] DoorDash is raising money because they are just getting started. I do think this could be a $500 billion-plus company. There’s so much to be excited about. As for the capital-raising event, I think it’s hard for the bankers to know where it will land with the broader market, so I’m not as negative as maybe some others.

Here’s the blow-by-blow coverage of the craziest tech IPO week in the craziest (IPO) year in decades, resuming from where I left off last Friday:

DoorDash amps its IPO range ahead of blockbuster IPO (EC)

The IPO market looks hot as Airbnb and C3.ai raise price targets (EC)

Wish wants to be the Amazon for the rest of us; will retail investors buy it?

DoorDash said to price at $102 per share, doubling its final private price

Airbnb said to price IPO between $67 and $68

While several marketplace unicorns prepare IPOs, a VC digs into the data (EC)

DoorDash, C3.ai skyrocket in public market debuts

How DoorDash and C3.ai can defend their red-hot IPO valuations (EC)

Airbnb’s first-day pop caps off a stellar week for tech IPOs (EC)

In public and private markets, cloud earnings and valuations heat up (EC)

Photo via Natasha Mascarenhas

The year is coming to a close for my time writing this newsletter, too. I’m going to be returning full-time to my regular job editing Extra Crunch and stuff in the back offices here at TechCrunch virtual HQ. My colleague Natasha Mascarenhas will be taking over starting next week.

You’re in good hands. In fact you may have noticed many of her articles and her weekly contributions to Equity showing up here already. Since joining us from Crunchbase News earlier this year, she’s been covering early-stage startups and the San Francisco tech scene in general, with a big focus on edtech. We have a lot more planned across Equity, Extra Crunch and more, and she’ll be able to tie it all together around her daily coverage. Stay tuned for an action-packed 2021 (and follow her on Twitter in the meantime).

Alex Wilhelm hears from one startup founder who has taken a bit of an alternative approach to building a SaaS company. Here’s more:

Now north of $200 million in revenue, [Nextiva] is a quiet giant and, notably, has not taken venture capital funding along its path to scale. Chatting with CEO and co-founder Tomas Gorny, I got to dig a little under the skin of the company’s history. It goes a little something like this: After moving to California in 1996 at the age of 20, Gorny eventually founded a web hosting company in 2001 after working for tech companies during the dot-com boom. The web hosting company wound up selling to another company called Endurance International in 2007, which sold as a combined entity for around a billion dollars in 2011, later going public before being taken private last month for $3 billion — you can read this TechCrunch piece that mentions Endurance from 2010 for a bit of the historical record.

Gorny founded Nextiva in 2008, focused on what it describes today as “UcaaS,” or unified communications as a service. The startup grew to about $40 million in annual recurring revenue (ARR), at which point it ran into issues with a third-party system that would integrate hardware, and support and services software, which sparked a shift in its thinking. The company set out to build a platform.

Nextiva expanded horizontally, adding CRM software, analytics and other functionality to its broader suite as it scaled. And it grew efficiently; starting with money from its founding team, Gorny told TechCrunch that even if he had used someone else’s money, he would have built the company in the same manner.

Here’s Natasha’s take, from a little explainer we did this week following some Twitter conversations:

The reason I love writing about tech and do the sometimes formulaic funding-round story is because I meet people who are crazy enough to bet their entire legacy on a napkin-stage idea. That’s the story, and the surprise and the tension. The dollar sign is just the first way in.

Having raised fundings that got covered in TechCrunch, and having written many many funding round articles over the year, I agree. The funding round is often the only way to prove that you have traction, if you are trying to get more attention.

Image Credits: Bryce Durbin / TechCrunch

Swedish fintech decacorn Klarna pioneered new ways for users to buy online without credit cards over the decade, and is now battling rivals large and small across the world. How did it all happen? Steve O’Hear sits down with founder Sebastian Siemiatkowski for an exclusive in-depth interview that Extra Crunch subscribers have been eating up this week. Here’s his description:

In a wide-ranging interview, Siemiatkowski confronts criticisms head on, including that Klarna makes it too easy to get into debt, and that buy now, pay later needs to be regulated. We also discuss Klarna’s business model and the balancing act required to win over consumers and keep merchants onside.

We also learn how, under his watch and as the company began to scale, Klarna missed the next big opportunity in fintech, instead being usurped by Adyen and Stripe. Siemiatkowski also shares what’s next for the company as it ventures further into the world of retail banking after gaining a bank license in 2017.

Here’s a painfully fascinating excerpt from Siemiatkowski:

One of the drawbacks that we had at the company was that none of the three co-founders had any engineering background; we couldn’t code. We were connected to five engineers that by themselves were amazing engineers, but we had a slight misunderstanding. Their idea was that they were going to come in, build a prototype, ship it, and then leave for 37% of the equity. Our understanding was that they were going to come in, ship it, and if it started scaling they would stay with us and work for a longer period of time. This is the classic mistake that you do as a startup.

Image Credits: TechCrunch

It seems that the US government has finally had enough of Facebook’s aggressive expansion and acquisition practices. After years of light regulation, the Federal Trade Commission and, separately, 49 state attorneys general are suing to break up social networking company. You can find lots of commentary about the details on TechCrunch and elsewhere.

But here’s my take for you to remember, as you watch headlines about this continue into next year: Facebook was always ready. I covered the company closely during its early years, and even back then it was talking about being the operating system for the internet, like Microsoft Windows was for desktop. The implied and whispered goal was to get as big as possible before regulations inevitably hit, like what Microsoft did. Here we are, with Facebook in a leading market position, with a massive army of lawyers who have been preparing for years. Without getting further into the lawsuits or political landscape where it’s all happening… I don’t expect a breakup. But maybe new restrictions on acquisitions or something could limit growth potential? Its big wins this decade have been from acquisitions.

One boring scenario I don’t see discussed much is simply that its products remain the phone book of the era for much of the world. Somewhat regulated this way or that way in various jurisdictions and banned outright in some — and very big and successful still.

TC Sessions: Space 2020 launches next week

Announcing the final agenda for TC Sessions: Space 2020

Don’t miss the university research showcase at TC Sessions: Space 2020

Hear the latest from Kayhan Space and Firehawk Aerospace at TC Sessions: Space

Give the gift of Extra Crunch for 25% off

Extra Crunch Partner Perk: Find peace of mind with ‘Spotify for Mindfulness & Sleep’ app Aura

TechCrunch

Survey: Americans think Big Tech isn’t so bad after all

Despite the pandemic, small business optimism persists

Mixtape podcast: Making technology accessible for everyone

Macron promotes European tech ecosystem in an interview with Zennström

Equity Monday: Airbnb pricing, Sequoia makes money and early-stage rounds

Extra Crunch

What to expect while fundraising in 2021

3 ways the pandemic is transforming tech spending

Why Sapphire’s Jai Das thinks the Salesforce-Slack deal could succeed

China watches and learns from the US in AR/VR competition

Is 2020 bringing more edtech rounds than ever, or does it simply feel that way?

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast (now on Twitter!), where we unpack the numbers behind the headlines.

What a week, yeah? Instead of the news cycle slowing as the year races to a close, things are still as hot as ever. We have funding rounds big and small, IPOs, first-day extravaganza and more.

Luckily we had the whole crew around — Chris and Danny and Natasha and me. Here’s the rundown:

And that’s that! If you aren’t tired, have you even been paying attention?

Equity drops every Monday at 7:00 a.m. PST and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Editor’s note: Get this free weekly recap of TechCrunch news that any startup can use by email every Saturday morning (7 a.m. PT). Subscribe here.

Did you follow all of the unicorn news from the last couple of weeks? No? Here’s a list of headlines to catch you up, because this holiday season is already featuring mega acquisitions, even more IPO filings, and a steady drumbeat of fundraises.

Somehow, after one of the toughest years in recent memory, the tech industry is heading into December with more enthusiasm than ever. (Still remember the WeWork IPO fiasco from last year? No?)

Salesforce buys Slack in a $27.7B megadeal

Everyone has an opinion on the $27.7B Slack acquisition

What to make of Stripe’s possible $100B valuation

How the pandemic drove the IPO wave we see today

A roundup of recent unicorn news

C3.ai’s initial IPO pricing guidance spotlights the public market’s tech appetite (EC)

Working to understand C3.ai’s growth story (EC)

Insurtech’s big year gets bigger as Metromile looks to go public (EC)

Wall Street needs to relax, as startups show remote work is here to stay (EC)

In first IPO price range, Airbnb’s valuation recovers to pre-pandemic levels (EC)

3 new $100M ARR club members and a call for the next generation of growth-stage startups (EC)

Connie Loizos sat down with Jason Green of leading enterprise-focused firm Emergence Capital to get his view of SPACs, and how they are likely to be used next year and beyond. But early-stage startups, don’t miss his affirmation of Zoom meetings as part of the fundraising process going forward.

I would say that over the last five years, we’ve made almost a total transition. Now we’re very much a data-driven, thesis-driven outbound firm, where we’re reaching out to entrepreneurs soon after they’ve started their companies or gotten seed financing. The last three investments that we made were all relationships that [date back] a year to 18 months before we started engaging in the actual financing process with them. I think that’s what’s required to build a relationship and the conviction, because financings are happening so fast.

I think we’re going to actually do more investments this year than we maybe have ever done in the history of the firm, which is amazing to me [considering] COVID. I think we’ve really honed our ability to build this pipeline and have conviction, and then in this market environment, Zoom is actually helping expand the landscape that we’re willing to invest in. We’re probably seeing 50% to 100% more companies and trying to whittle them down over time and really focus on the 20 to 25 that we want to dig deep on as a team.

Thousands of startup founders will resume the trek around Silicon Valley VC offices, once the vaccines arrive. But we’ll remember 2020 as the year that venture truly joined the cloud.

Image Credits: Brighteye Ventures

Every level of education was forced online by the pandemic this year, at least temporarily. While the children might be back in the classroom already, higher education and corporate education are still booming remotely. Natasha Mascarenhas analyzed the latest market changes for Extra Crunch, and put together a panel of industry leaders for a special Thanksgiving edition of Equity. Here’s more about what you’ll find on the show:

For this Equity Dive, we zero onto one part of that conversation: Edtech’s impact on higher education. We brought together Udacity co-founder and Kitty Hawk CEO Sebastian Thrun, Eschaton founder and college dropout Ian Dilick, and Cowboy Ventures investor Jomayra Herrera to answer our biggest questions.

Here’s what we got into:

- How the state of remote school is leading to gap years among students.

- A framework for how to think of higher education’s main three products (including which is most defensible over time).

- What learnings we can take from this COVID-19 experiment on remote schooling to apply to the future.

- Why edtech is flocking to the notion of life-long learning.

- The reality of who self-paced learning serves — and who it leaves out.

SaaS is continuing to be reshaped by consumer internet techniques, with top companies of our era competing through word-of-mouth growth versus incumbent sales forces. The revenue model must be precise for this to scale, though. In a guest post for Extra Crunch, Caryn Marooney and David Cahn of Coatue lay out a strategic framework for how to price your bottoms-up SaaS product the right way for the market. Called “MAP,” for Metrics, Activity and People, it helps you sort your product against the actual ways that people are trying to use and pay for it. Here’s how they describe the A:

Activity: How do your customers really use your product and how do they describe themselves? Are they creators? Are they editors? Do different customers use your product differently? Instead of metrics, a key anchor for pricing may be the different roles users have within an organization and what they want and need in your product. If you choose to anchor on activity, you will need to align feature sets and capabilities with usage patterns (e.g., creators get access to deeper tooling than viewers, or admins get high privileges versus line-level users). For example:

- Figma — Editors versus viewers: Free to view, starts changing after two edits.

- Monday — Creators versus viewers: Free to view, creators are charged $10-$20/month.

- Smartsheet — Creators versus viewers: Free to view, creators are charged $10+/month.

Extra Crunch membership now available to readers in Israel

Find out how we’re working toward living and working in space at TC Sessions: Space 2020

Aerospace’s Steve Isakowitz to speak at TC Sessions: Space 2020

Investors Lockheed Martin Ventures and SpaceFund are coming to TC Sessions: Space 2020

TechCrunch

Calling VCs in Israel: Be featured in The Great TechCrunch Survey of European VC

SEC issues proposed rulemaking to give gig workers equity compensation

The downfall of adtech means the trust economy is here

How Ryan Reynolds and Mint Mobile worked without becoming the joke

What will tomorrow’s tech look like? Ask someone who can’t see

Extra Crunch

Mental health startups are raising spirits and venture capital

Who’s building the grocery store of the future?

Strike first, strike hard, no mercy: How emerging managers can win

This is a good time to start a proptech company

7 things we just learned about Sequoia’s European expansion plans

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast (now on Twitter!), where we unpack the numbers behind the headlines.

We’re back with not an Equity Shot or Dive of Monday, this is just the regular show! So, we got back to our roots by looking at a huge number of early-stage rounds. And a few other things that we were just too excited about to not mention.

So from Chris and Danny and Natasha and I, here’s the rundown:

That was a lot, but how could we leave any of it out? We’re back Monday with more!

Equity drops every Monday at 7:00 a.m. PDT and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Editor’s note: Get this free weekly recap of TechCrunch news that any startup can use by email every Saturday morning (7 a.m. PT). Subscribe here.

The wait was long but this week the time was right: Airbnb finally filed its S-1 and so did Affirm, C3.ai, Roblox, and Wish. We are likely to see these five price on public markets before the end of an already superlative year for tech IPOs. The ongoing pandemic and political turmoil were not scary enough, apparently.

This coming decade, you have to think that we’ll see a more even spread of tech companies going public. Many of the companies above have been bottled up for years behind privately funded growth strategies. Today, however, the industry has a better grasp of SPACs and direct listings, and various funding routes. Companies have more options from their founding for how they might grow and exit one day. Public investors in 2020 also seem to have a deeper appreciation for the current revenue numbers and future growth opportunities for tech companies. Why, I can still remember all the geniuses who bragged about shorting the Facebook IPO not so long ago.

Will we see a more even spread of where IPOs come from? While all of this week’s filers are headquartered in San Francisco or environs, that now feels almost like a coincidental reference to the years when these companies were founded. More states have been minting their own unicorns, with Ohio-based Root Insurance recently going public and Utah-based Qualtrics heading (back) that way. Tech startups are now global, meanwhile, and plenty of countries are working to keep their unicorns closer to home than New York.

On to the headlines from TechCrunch and Extra Crunch:

If you didn’t make $1B this week, you are not doing VC right (EC)

Inside Affirm’s IPO filing: A look at its economics, profits and revenue concentration (EC)

5 questions from Airbnb’s IPO filing (EC)

The VC and founder winners in Airbnb’s IPO (EC)

Wish files to go public with 100M monthly actives, $1.75B in 2020 revenue thus far

Unpacking the C3.ai IPO filing (EC)

With a 2021 IPO in the cards, what do we know about Robinhood’s Q3 performance? (EC)

(Photo by Win McNamee/Getty Images)

What does Joe Biden intend as president around technology policy? On the one hand, tech companies might not be returning to the White House too fast. “All told, we’re seeing some familiar names in the mix, but 2020 isn’t 2008,” Taylor Hatmaker explains about potential presidential appointments from the industry. “Tech companies that emerged as golden children over the last 10 years are radioactive now. Regulation looms on the horizon in every direction. Whatever policy priorities emerge out of the Biden administration, Obama’s technocratic gilded age is over and we’re in for something new.”

However, tech industries and companies focused on shared goals might find support. In a review of Biden’s climate-change policies, Jon Shieber looks at major green infrastructure plans that could be on the way.

Any policies that a Biden administration enacts would have to focus on economic opportunity broadly, and much of the proposed plan from the campaign fulfills that need. One of its key propositions was that it would be “creating good, union, middle-class jobs in communities left behind, righting wrongs in communities that bear the brunt of pollution, and lifting up the best ideas from across our great nation — rural, urban and tribal,” according to the transition website. An early emphasis on grid and utility infrastructure could create significant opportunities for job creation across America — and be a boost for technology companies. “Our electric power infrastructure is old, aging and not secure,” said Abe Yokell, co-founder of the energy and climate-focused venture capital firm Congruent Ventures. “From an infrastructure standpoint, transmission distribution really should be upgraded and has been underinvested over the years. And it is in direct alignment with providing renewable energy deployment across the U.S. and the electrification of everything.”

Image Credits: Steve Proehl (opens in a new window) / Getty Images

A skilled labor shortage is piling on top of the construction industry’s traditional challenges this year. The result is that tech adoption is getting a big push into the real world, Allison Xu of Bain Capital Ventures writes in a guest column for Extra Crunch this week. She maps out six main construction categories where tech startups are emerging, including project conception, design and engineering, pre-construction, construction execution, post construction and construction management. Here’s an excerpt from the article about that last item:

- How it works today: Construction management and operations teams manage the end-to-end project, with functions such as document management, data and insights, accounting, financing, HR/payroll, etc.

- Key challenges: The complexity of the job site translates to highly complex and burdensome paperwork associated with each project. Managing the process requires communication and alignment across many stakeholders.

- How technology can address challenges: The nuances of the multistakeholder construction process merit value in a verticalized approach to managing the project. Construction management tools like Procore, Hyphen Solutions and IngeniousIO have created ways for contractors to coordinate and track the end-to-end process more seamlessly. Other players like Levelset have taken a construction-specific approach to functions like invoice management and payments.

Pandemic-era work solutions like online team meeting spaces are heading towards a less certain, vaccine-based reality. Have we all gone remote-first enough that they will have a real market, still? Natasha Mascarenhas checks in with some of the top companies to see how it’s looking, here’s more:

With the goal of making remote work more spontaneous, there are dozens of new startups working to create virtual HQs for distributed teams. The three that have risen to the top include Branch, built by Gen Z gamers; Gather, created by engineers building a gamified Zoom; and Huddle, which is still in stealth.

The platforms are all racing to prove that the world is ready to be a part of virtual workspaces. By drawing on multiplayer gaming culture, the startups are using spatial technology, animations and productivity tools to create a metaverse dedicated to work.

The biggest challenge ahead? The startups need to convince venture capitalists and users alike that they’re more than Sims for Enterprise or an always-on Zoom call. The potential success could signal how the future of work will blend gaming and socialization for distributed teams.

Head of the US Space Force, Gen. John W. ‘Jay’ Raymond, joins us at TechCrunch Sessions: Space

Amazon’s Project Kuiper chief David Limp is coming to TC Sessions: Space

TechCrunch

Against all odds: The sheer force of immigrant startup founders

S16 Angel Fund launches a community of founders to invest in other founders

Why are telehealth companies treating healthcare like the gig economy?

A court decision in favor of startup UpCodes may help shape open access to the law

Extra Crunch

Will Zoom Apps be the next hot startup platform?

Is the internet advertising economy about to implode?

Surging homegrown talent and VC spark Italy’s tech renaissance

Why some VCs prefer to work with first-time founders

3 growth tactics that helped us surpass Noom and Weight Watchers

A report card for the SEC’s new equity crowdfunding rules

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast (now on Twitter!), where we unpack the numbers behind the headlines.

This week wound up being incredibly busy. What else, with a week that included both the Airbnb and Affirm IPO filings, a host of mega-rounds for new unicorns, some fascinating smaller funding events and some new funds?

So we had a lot to get through, but with Chris and Danny and Natasha and your humble servant, we dove in headfirst:

What a week! Three episodes, some new records, and a very tired us after all the action. More on Monday!

Equity drops every Monday at 7:00 a.m. PDT and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Editor’s note: Get this free weekly recap of TechCrunch news that any startup can use by email every Saturday morning (7 a.m. PT). Subscribe here.

DoorDash has become the go-to delivery choice for millions of people cooped up during the pandemic this year. Now it has filed an S-1, revealing its financials as it nears a long-intended IPO. These innards show an exciting business — and a larger story about how the year is going for tech companies in general.

When the company filed initial public offering paperwork back in February, it was coming off of an expensive year of growth in 2019. The California state legislature was passing laws, meanwhile, that directly targeted its gig-economy labor model. Then the pandemic hit. More from Alex Wilhelm:

DoorDash has grown incredibly rapidly, scaling its revenues from $291 million in 2018 to $885 million in 2019. And more recently, from $587 million in the first nine months of 2019 to $1.92 billion in the same period of 2020. That is 226% growth in 2020 thus far… How high-quality is DoorDash’s revenue? In the first three quarters of 2019, the company had gross margins of 39.9%, and in the same period of 2020 the figure rose to 53.1%, a huge improvement for the consumer consumable delivery confab.

The other jolt of good news for the company arrived last week. A California ballot proposition passed that preserved the contractor model it relies on for deliveries.

World events did not take a breath, though. A COVID-19 vaccine appeared on the horizon this week, and could lead to the pandemic ending as soon as next year. Will this be bad for DoorDash’s business? Alex took another look at the numbers for Extra Crunch, and didn’t come away with a clear answer. On the one hand, the company has been making ongoing investments in its delivery platform technology, which has helped to drive the success this year already. On the other hand, the S-1 is open about post-pandemic reality — profitability is going to decline. Alex:

To buy into the DoorDash IPO, especially at its currently floated $25 billion price, you have to believe that the company’s revenue growth will slow modestly at most. Otherwise the price makes no sense. Bearish investors who might expect the company to post negative growth in Q3 2021 won’t pay any price for DoorDash shares, but in between the two camps is a mess of vaccine timings, shifts in consumer behavior and macroeconomic questions that could determine how many American families can afford delivery. All of which will impact DoorDash’s future growth rates.

For those looking further out, DoorDash stock is about how you think the pandemic is going to change the world for the long term, or not. Are we going to be using DoorDash more often now for deliveries? Are we going to be at home as much in the first place? Or are we going to go back to offices, stores and restaurants like we did before?

Speaking of investors, Danny Crichton illustrates why it pays to bet on the world changing. The company has raised nearly $2.5 billion over the years. Today that includes an 18.2% ownership stake by Sequoia, 22.1% by the SoftBank Vision Fund, and 9.3% by Singapore’s GIC. As he writes for Extra Crunch, the founding executives Tony Xu, Andy Fang and Stanley Tang each own around 5% — smallish wedges of a growing pie. Maybe that is too much dilution? Or maybe, considering all of the other delivery companies that have failed or gone sideways, this is the pinnacle of success in the sector.

(Photo by Dogukan Keskinkilic/Anadolu Agency via Getty Images)

We all knew that at some point solutions would be figured out. But as COVID-19 cases have climbed this season, and as anxiety built around elections, it was hard to believe that the vaccine was right around the corner. The initial success reported Monday by BioNTech and Pfizer may mean that these two companies are close to success. But many other companies are attempting to use the same experimental gene-based vaccines so we may see others winners soon.

The stock market is already repricing tech stocks, in any case. Besides the timely arrival of the DoorDash S-1, here are a few other headlines about the impact of the news:

Positive vaccine news punishes pandemic-boosted companies like Zoom, Peloton, Etsy

What happens to high-flying startups if the pandemic trade flips? (EC)

As public investors reprice edtech bets, what’s ahead for the hot startup sector? (EC)

5 VCs discuss the future of SaaS and software after Pfizer’s vaccine breakthrough (EC)

Image Credits: John Artman

In other news about political turbulence and the tech world, Rita Liao inspects Tencent’s quietly huge fintech empire and concludes that it “will need to tread more carefully on regulatory issues.”

Here’s why, for those trying to understand this global company and its place across markets:

As Ant Group seizes the world’s attention with its record initial public offering, which was abruptly called off by Beijing, investors and analysts are revisiting the fintech interests of Tencent, Ant’s arch rival in China. It’s somewhat complicated to do this, not least because they are sprawled across a number of Tencent properties and, unlike Ant, don’t go by a single brand or operational structure — at least, not one that is obvious to the outside world. However, when you tease out Tencent’s fintech activity across its wider footprint — from direct operations like WeChat Pay through to its sizeable strategic investments and third-party marketplaces — you have something comparable in size to Ant, and in some services even bigger.

Image Credits: the_progressive (opens in a new window) / Flickr (opens in a new window) under a CC BY-SA 2.0 (opens in a new window) license. (Image has been modified)

Serial founder Darshan Somashekar writes that if you want to build a great edtech product, then perhaps it should be a game. Here’s more, from his guest column for Extra Crunch this week:

Earlier this year, we launched Solitaired, a casual gaming platform that ties card games to educational experiences and brain training. We’re still early, but signs are encouraging: Our average time on site is 30 minutes, more than three times that of our earlier business. Even better, users come back often, on average returning more than five times per month. Since we’re now in the gaming space, we should have expected these metrics, but they still blew our expectations away. We’ve also found that the downsides can be mitigated. For example, high engagement has led to strong virality, driving down our CAC and increasing our growth. In-app purchase abuses can be tempting for game developers, but by focusing on user growth KPIs, we don’t have the desire to go down those routes. Lastly, the threat of Big Tech is there, but at present most of their attempts have yet to strike a chord among users. More importantly, that’s why choosing a market so massive that even individual Big Tech players can’t dominate is key: With a market this size, you can shoot for the stars, miss the moon and still do well for yourself.

Pioneers of in-space refueling and manufacturing join TC Sessions: Space 2020

NASA’s head of human spaceflight, Kathryn Lueders, will join us at TC Sessions: Space

Get fast money for your space startup at TC Sessions Space this December

TechCrunch

This startup is betting that you want to binge remote-work content

Calling Dublin VCs: Be featured in The Great TechCrunch Survey of European VC

Human Capital: The gig economy in a post-Prop 22 world

‘Free speech’ social network Parler tops app store rankings following Biden’s election win

Renewable power represents almost 90% of total global power capacity added in 2020

Extra Crunch

Square and PayPal earnings bring good (and bad) news for fintech startups

What I wish I’d known about venture capital when I was a founder

Conflicts in California’s trade secret laws on customer lists create uncertainty

What we’ve learned about working from home 7 months into the pandemic

Dear Sophie: What does Biden’s win mean for tech immigration?

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast (now on Twitter!), where we unpack the numbers behind the headlines.

The full Equity crew was on hand to debate the current venture capital market, curious about how risk-on, or risk-off things really are today. Danny, Natasha and I framed the conversation around a number of news items from the week, including:

It was a busy week, despite the month. Expect more of the same next week.

Finally, don’t forget that our own Chris Gates is cutting Equity videos out of every episode that you can find over on YouTube. He does a great job and it’s great to be on video, as well as audio platforms.

Equity drops every Monday at 7:00 a.m. PDT and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Editor’s note: Get this free weekly recap of TechCrunch news that any startup can use by email every Saturday morning (7 a.m. PT). Subscribe here.

Let’s think beyond Monday, for a minute, to the trends playing out in technology this coming decade. While humanity’s problems have never been greater, our tools have never been better. Here’s more, from Danny Crichton:

The 2010s were all about executing on the dreams of mobile, cloud, and basic data. Those ideas had historical antecedents going back in some cases decades or more (Vannevar Bush’s description of the internet dates to the 1940s, for instance). But for the first time, we had the infrastructure and the users to actually build these products and make them useful. It was quite possibly the most extensive greenfield opportunity in the history of technology.

Yet, that greenfield is increasingly fallow. Business has cycles and seasonality as much as media reporting does. The easy stuff has been done. Building an app to text people has been done by dozens before. There are a multitude of analytics packages, and payroll providers, and credit card issuers, and more. What’s required this decade is to start to encroach on the harder questions, topics like how we build a better society, make people more empowered to do deep and creative work, and how we can build a more resilient and sustainable planet for all.

None of these topics have pure point solutions — but that is what is going to make this coming decade so damn interesting. It’s going to take intense collaboration, multiple inventions and products, as well as legal and cultural changes, to realize these next improvements. If you have grown sick (as I have) of the latest apps and SaaS products du jour, this decade is going to be an amazing one to experience and build.

In a companion article for Extra Crunch, he explores five key areas of the future, that he calls: Wellness, Climate, Data Society, Creativity and Fundamentals. Here’s an excerpt from the Data Society part:

Data may be ubiquitous, but it’s amazing how much work it can still be to calculate an LTV, or the return on an advertising campaign. No-code tools solve some of these problems, but what we need is a whole revolution in our data tools. We need to be able to sketch out lines of inquiry and have our tools augment our thinking from data. What are we missing? What gaps in our thinking should we be filling in? What data am I lacking to make a fully-formed decision? Am I overly biased toward one statistic versus a more holistic depiction of my situation? From personal decisions to business strategy, we need better tools to abstract the complexity of today’s modern society.

We also need better thinking around how to network knowledge. Roam Research and some other tools are starting to get better at helping users think in terms of a knowledge graph, but there is an incredible amount of potential if these ideas can be democratized and packaged into easier-to-use interfaces. How do we handle the increasing depth of most fields of knowledge and allow more people to get to the frontiers as quickly as possible?

Finally, we need to further our understanding of complexity and chaos and build those theories into the fundamental structures of our society. How do we make governance more adaptable and resilience, so that when massive crises like COVID-19 happen, we don’t see a complete breakdown in our society? Can we create more flexible systems around ownership and property that can create more diverse housing, or material ownership, or intellectual property? Empowering technology (“blockchain!” but could be all kinds of things) coupled with legal changes could dramatically evolve these core elements of our society.

Even today, we are still locked into a mental model built around paper, titles, and maybe if you are lucky, an Excel spreadsheet. There is so much work to be done to empower each of us through data this decade.

The building blocks of the Data Society concept are getting remade faster than ever this year, as the pandemic has shuttered traditional commerce and education, and forced open alternative approaches. For example, somebody starting a small business today basically has to use a lot of software. But crossing this initial barrier means they can do things like automatically track the lifetime value of each customer. Previous generations of small businesses simply did not have the resources and skills to do such things with the low-tech options available.

That’s the generational power of no-code, as Danny detailed separately on TechCrunch:

In business today, it’s not enough to just open a spreadsheet and make some casual observations anymore. Today’s new workers know how to dive into systems, pipe different programs together using no-code platforms and answer problems with much more comprehensive — and real-time — answers.

It’s honestly striking to see the difference. Whereas just a few years ago, a store manager might (and strong emphasis on might) put their sales data into Excel and then let it linger there for the occasional perusal, this new generation is prepared to connect multiple online tools to build an online storefront (through no-code tools like Shopify or Squarespace), calculate basic LTV scores using a no-code data platform and prioritize their best customers with marketing outreach through basic email delivery services. And it’s all reproducible, as it is in technology and code and not produced by hand.

There are two important points here. First is to note the degree of fluency these new workers have for these technologies, and just how many members of this generation seem prepared to use them. They just don’t have the fear to try new programs, and they know they can always use search engines to find answers to problems they are having.

Second, the productivity difference between basic computer literacy and a bit more advanced expertise is profound. Even basic but accurate data analysis on a business can raise performance substantially compared to gut instinct and expired spreadsheets.

How do we realize this future? Zooming in from the generational perspective, Natasha Mascarenhas takes a closer look at how school teachers are adapting to the pandemic — and the emerging online education world they are entering. Some, at least, seem to be moving into supplemental part-time teaching. While the educational experience is not the same as in-person, it clearly has its own value. Here’s one company as an example:

Outschool is a platform that sells small-group classes led by teachers on a large expanse of topics, from Taylor Swift Spanish class to engineering lessons through Lego challenges. In the past year, teachers on Outschool have made more than $40 million in aggregate, up from $4 million in total earnings the year prior.

CEO Amir Nathoo estimates that teachers are able to make between $40 to $60 per hour, up from an average of $30 per hour in earnings in traditional public schools. Outschool itself has surged over 2,000% in new bookings, and recently turned its first profit.

Outschool makes more money if teachers join the platform full-time: teachers pocket 70% of the price they set for classes, while Outschool gets the other 30% of income. But, Nathoo views the platform as more of a supplement to traditional education. Instead of scaling revenue by convincing teachers to come on full-time, the CEO is growing by adding more part-time teachers to the platform.

Maybe one day soon, a class about online business will be a graduation requirement for a high school diploma. And we’ll see that sort of education drive more success in the next generation of your local Main Street.

The problems of the coming decade might be harder than ever, but the solutions are there for the making.

Image Credits: Intpro / Getty Images

The combination of consumer tech product skills and enterprise revenue models fueled this decade’s explosion of SaaS success stories. This week, Caryn Marooney and David Cahn of Coatue management distilled the lessons of this model into a popular how-to article for Extra Crunch. Here’s an excerpt, showing how market leaders approach key metrics and pricing:

The MAP customer value framework:

Metrics: What are the key metrics the customers care about? Is there a threshold of value associated with this metric? Metrics can include things like minutes, messages, meetings, data and storage. Examples:

- Zoom — Minutes: Free with a 40-minute time limit on group meetings.

- Slack — Messages: Free until 10,000 total messages.

- Airtable — Records: Free until 1,200 records.

Activity: How do your customers really use your product? Are they creators? Are they editors? Do different customers use your product differently? Examples:

- Figma — Editors versus viewers: Free to view, starts changing after two edits.

- Monday.com — Creators versus viewers: Free to view, creators are charged $30+/month.

- Smartsheet — Creators versus viewers: Free to view, creators are charged $10+/month.

People: How do your customers fit into a broader organization? Are they mostly individuals? Groups? Part of an enterprise? Examples:

Superhuman — Individuals only: No free version, $30/month.

Asana — Small team versus bigger teams: Teams of <15 people can use the product free.

Atlassian — Free versus team versus enterprise: Pricing scales with size of team.

Image Credits: Nigel Sussman (opens in a new window)

The stock market was off this week, but not entirely. Root Insurance was the big IPO this week, ending at $24 per share. That’s a bit below its aggressive $27 opening price per share, but is still in the range of its target pricing from the other week. It is, in other words, a success already for the company — and we’ll see what happens when the entire market stops gyrating around the elections.

“For the Midwest, Ohio-based Root’s IPO is a win,” Alex Wilhelm wrote for Extra Crunch. “The company shows that it is possible to build high-growth technology companies worth billions of dollars far from coastal hubs. For the broader insurtech space, Root’s IPO is a win. The company follows Lemonade to the public markets, setting a strong valuation mark again for the neo-insurance startup market. For similar companies like Clearcover, MetroMile and all startups that related to Root and Lemonade, it’s a good day.”

It’s still looking good for any software company with a growth story, as Alex goes on to say, and it’s looking good for more IPOs this year. Like Airbnb.

But enough about IPOs this year — Alex also built on previous coverage to explore Databricks going public next year, which sounds quite likely at this point.

TechCrunch

Why you have to pay attention to the Indian startup scene

Yale may have just turned institutional investing on its head with a new diversity edict

Cloud infrastructure revenue grows 33% this quarter to almost $33B

We need new business models to burst old media filter bubbles

Former Facebook and Pinterest exec Tim Kendall traces ‘extractive business models’ to VCs

Extra Crunch

Good and bad board members (and what to do about them)

New GV partner Terri Burns has a simple investment thesis: Gen Z

As venture capital rebounds, what’s going on with venture debt?

In the ‘buy now, pay later’ wars, PayPal is primed for dominance

Dear Sophie: Any upgrade options for E-2 visa holders interested in changing jobs?

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast (now on Twitter!), where we unpack the numbers behind the headlines.

A few notes before we get into this. One, we have a bonus episode coming this Saturday focused on this week’s earnings reports. And, second, we did not record video this week. So, if you like watching the show on YouTube, this is not the week for that!

Right, here’s what Natasha, Danny and your humble servant got into this week:

We capped off with the latest from r2c, and then got the hell off the mics. Catch you all Saturday, and then back to regular programming on Monday morning.

Equity drops every Monday at 7:00 a.m. PDT and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Editor’s note: Get this free weekly recap of TechCrunch news that any startup can use by email every Saturday morning (7 a.m. PT). Subscribe here.

Startup failure is easy to hold up as a type of martyrdom for progress, especially if the founders are starting out scrappy in the first place and trying to save the world. But heroic narrative gets complicated when the startup failure involves the biggest names in entertainment, dubious product decisions, and well over $1 billion in losses in an already very competitive consumer tech subcategory.

I was going to skip any mention of Quibi because, like me, you have heard more than enough already. But this week its shutdown announcement turned into a debate on Twitter about the nature of startup failure and whether this was still the right kind. Many in the startup world said it was still good, basically because most any ambitious startup effort leads to progress. Danny Crichton, in turn, argues that the negativity was fully justified in this case.

Let’s be honest: Most startups fail. Most ideas turn out wrong. Most entrepreneurs are never going to make it. That doesn’t mean no one should build a startup, or pursue their passions and dreams. When success happens, we like to talk about it, report on it and try to explain why it happens — because ultimately, more entrepreneurial success is good for all of us and helps to drive progress in our world.

But let’s also be clear that there are bad ideas, and then there are flagrantly bad ideas with billions in funding from smart people who otherwise should know better. Quibi wasn’t the spark of the proverbial college dropout with a passion for entertainment trying to invent a new format for mobile phones with ramen money from friends and family. Quibi was run by two of the most powerful and influential executives in the United States today, who raised more money for their project than other female founders have raised collectively this year.

Ouch. However, I think this still misses the bigger dynamic happening.

Quibi was so easy to criticize that it created an opportunity to plausibly defend for anyone who wants to show that they are here for the startups no matter how crazy. When you defend Quibi, you’re defending your own process, and making it clear to the next generation of startups that you’re personally not scared off from other people with crazy ideas and have the will to try even if the result is a big mess. Which is who founders want to hire in the early days, and who investors want to bet on.

I support both sides of this mass-signaling game. Analysts and journalists have provided a broad range of valuable insights about how Quibi was doing it wrong, that are no doubt being internalized by founders of all types. Meanwhile, Quibi defenders are no doubt sorting through their inbound admirers for great new deals. All in all, Quibi and the debate around it might ultimately make future companies a little better. Which is what we all wanted in the first place, right?

Image Credits: Larry Knupp (opens in a new window) / Shutterstock (opens in a new window)

The IPO market has not shut down (yet) for election turmoil and whatnot. First up, managed service provider Datto went out on Wednesday and has inched up since then — a strong outcome for the company and its private equity owner, even if third parties did not benefit from an additional pop. A few more notes from Alex Wilhelm:

Datto’s CEO Tim Weller told TechCrunch in a call that the company will still be well-capitalized after the public offering, saying that it will have a very strong cash position.

The company should have places to deploy its remaining cash. In its S-1 filings, Datto highlighted a COVID-19 tailwind stemming from companies accelerating their digital transformation efforts. TechCrunch asked the company’s CEO whether there was an international component to that story, and whether digital transformation efforts are accelerating globally and not merely domestically. In a good omen for startups not based in the United States, the executive said that they were.

Next to market, Root Insurance released its stock pricing set this week, raising the goal to a valuation above $6 billion. It’s definitely on track to be Ohio’s biggest tech IPO to date. Here’s Alex again, with a comparison against Lemonade, another recently IPOed insurance tech provider for Extra Crunch:

[I]t appears that Root at around $6 billion is cheap compared to Lemonade’s pricing today. So, if you’d like to anticipate that Root raises its IPO price range to bring it closer to the multiples that Lemonade enjoys, feel free as you are probably not wrong. Are we saying that Root will double its valuation to match Lemonade’s current metrics? No. But closing the gap a bit? Sure.

For insurtech startups, even Root’s current pricing is strong. Recall that Root was worth $3.65 billion just last August. At $6.34 billion, the company has appreciated massively in just the last year and change. A small repricing could boost Root’s valuation differential to a flat 100% rather easily.

So, for MetroMile and ClearCover and the rest of the related players, do enjoy these good times as long as they last….

Image Credits: Dong Wenjie (opens in a new window) / Getty Images

A year ago, the market looked quite young. But now, the pandemic has made the value of augmented and virtual reality clearer to the world. Lucas Matney, who has been covering the topic here for years, just conducted a survey of seven top investors in the space. While they mostly continue to see the vertical as a bit early, they see it getting relevant fast. Here’s one key response, from Brianne Kimmel of Work Life Ventures, on Extra Crunch:

Most investors I chat with seem to be long-term bullish on AR, but are reticent to invest in an explicitly AR-focused startup today. What do you want to see before you make a play here?

I think it all comes down to a unique insight and a competitive advantage when it comes to distribution. And so, I’ll use these new [Zoom] apps as an example, I think that they’re a great example where there are certain aspects of roles and certain highly specialized skills where teaching educating and doing your daily job on Zoom won’t actually cut it. I do foresee AR applications becoming an integral part of certain types of work. I also think that now that as a lot of the larger platforms such as Zoom are more open, people will start building on the platforms and there will be AR-specific use cases that can help industries where, you know, a traditional video conferencing experience doesn’t quite cut it.

In other survey news, Mike Butcher continues his (sadly virtual) tour across European startup hubs for EC, this week checking in with investors in Zurich, Switzerland. Here’s a tidy explanation of the city and country’s deep technical experience, from Michael Blank of investiere:

Which industries in your city and region seem well-positioned to thrive, or not, long term? What are companies you are excited about (your portfolio or not), which founders?

Switzerland has always been at the forefront of technological innovation in areas such as precision engineering or life sciences. We strongly believe that Switzerland will also thrive in the long run in those areas. Thinking for example about additive manufacturing startups such as 9T Labs or Scrona, drone companies such as Verity or Wingtra or health tech startups such as Aktiia or Versantis.

Brussels investors, Mike is headed your way next. You can reach him here.

Announcing the agenda for TC Sessions: Space 2020

Rocket Lab’s Peter Beck is coming to TC Sessions: Space 2020

Extra Crunch Partner Perk: Get 6 months free of Zendesk Support and Sales CRM

TechCrunch

Equity Monday: Three neat venture rounds, and Alibaba’s latest

The smart speaker market is expected to grow 21% next year

Financial institutions can support COVID-19 crowdfunding campaigns

Ready Set Raise, an accelerator for women built by women, announces third class

Extra Crunch

Here’s how fast a few dozen startups grew in Q3 2020

Late-stage deals made Q3 2020 a standout VC quarter for US-based startups

Founders don’t need to be full-time to start raising venture capital

Three views on the future of media startups

Dear Sophie: What visa options exist for a grad co-founding a startup?

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast (now on Twitter!), where we unpack the numbers behind the headlines.

Myself, along with Danny and Natasha had a lot to get through, and more to say than expected. A big thanks to Chris for cutting the show down to size.

Now, what did we get to? Aside from a little of everything, we ran through:

Whew! It was a lot, but also very good fun. Look for clips on YouTube if you’d like, and we’ll chat you all next Monday.

Powered by WPeMatico

Editor’s note: Get this free weekly recap of TechCrunch news that any startup can use by email every Saturday morning (7 a.m. PT). Subscribe here.

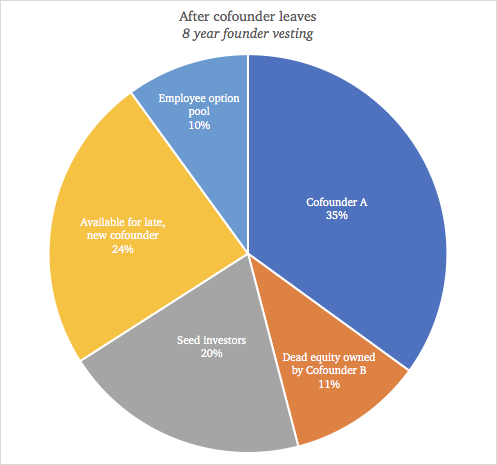

The four-year vesting schedule that the typical startup uses today is a problem waiting to happen. If one founder ends up quitting a year or two before the last cliff, they still own a large share of the cap table through many rounds to come. The departing founder might consider that fair, but the remaining founder(s) are the ones adding on the additional value — and resentment is not the only issue.

“The opportunity cost of dead equity is talent and capital,” Jake Jolis of Matrix Partners explains in a guest post for us this week. “Compensating talent and raising capital are the (only) two things you can use your startup’s equity for, and you need to do both in order for your company to grow large. If you want to build a big business, the road ahead is still long and windy, and you’re going to need every bit of help you can get. If your competitors don’t have dead equity you’re literally competing with a handicap.”

Instead, he argues that founders who are just starting out should consider doubling the vesting schedule to eight years or so. In one example he gives, a founder who leaves after two and a half years on a four-year plan could end up with 22% of the company even after a big new funding round, the creation of an employee stock option pool, and additional shares set aside for a replacement cofounder-level hire. On an eight-year plan, that would be only 11%, and there would be a lot more remaining to entice new cofounders.

The full article is on Extra Crunch, but I’m including more key parts here given the broad value:

Given the risks still ahead of the business, this level of compensation is often much more fair from a value-creation standpoint. With less dead equity on the cap table, the startup is still attractive in the eyes of VCs and well-positioned to attract a strong co-founder replacement to take the company forward. The alternative can cripple the company, and even co-founder B won’t be happy owning a larger percent of zero. While it’s better to do it when you start the company, a co-founder unit can elongate their vesting later on as well. The main requirement is that all the co-founders believe it’s in their best interest and agree to it. Most repeat founders I’ve talked to agree that four years is too short. Personally, if I started another company, I’d pick something like eight. You definitely don’t need to. You might decide four or six is better for your co-founder unit and your company.

One final thought, from my startup cofounder years. The departing cofounder should still want to see the company succeed as big as possible to maximize the value of their own shares. On the steep slope between failure and success in this business, vesting longer is a powerful way to help the company will deliver the most back to them after the hard work of the early days.

Image Credits: FirstMark

SPACs are an exciting development for any type of investor, public or private, Amish Jani of FirstMark Capital tells Connie Loizos. Indeed, his firm has historically focused on writing early-stage checks, so at first it is a bit jarring to see the FirstMark Horizon Acquisition SPAC raise $360 million and head out looking for the right unicorn. But he explains it all quite well an extensive interview this week:

TC: Why SPACs right now? Is it fair to say it’s a shortcut to a hot public market, in a time when no one quite knows when the markets could shift?

AJ: There are a couple of different threads that are coming together. I think the first one is the possibility that [SPACs] work, and really well. [Our portfolio company] DraftKings [reverse-merged into a SPAC] and did a [private investment in a public equity deal]; it was a fairly complicated transaction and they used this to go public, and the stock has done incredibly well.

In parallel, [privately held companies] over the last five or six years could raise large sums of capital, and that was pushing out the timeline [to going public] fairly substantially. [Now there are] tens of billions of dollars in value sitting in the private markets and [at the same time] an opportunity to go public and build trust with public shareholders and leverage the early tailwinds of growth.

He goes on to explain why public markets are likely to stay hot for the right SPACs far into the future.

AJ: I think a bit of a misconception is this idea that most investors in the public markets want to be hot money or fast money. There are a lot of investors that are interested in being part of a company’s journey and who’ve been frustrated because they’ve been frozen out of being able to access these companies as they’ve stayed private longer. So our investors are some of are our [limited partners], but the vast majority are long-only funds, alternative investment managers and people who are really excited about technology as a long-term disrupter and want to be aligned with this next generation of iconic companies.

Check out the whole thing on TechCrunch.

Maybe Segment would have gone public sometime soon, but instead Twilio has scooped it up for $3.2 billion this week. The popular data management tool will now be a part of Twilio’s ever-expanding suite of customer communication products. Perhaps it’s another sign of a consolidation phase taking hold in the sector, after a Pre-Cambrian explosion of SaaS startups over the last decade? Alex Wilhelm dug into the financials of the deal for Extra Crunch and came away thinking that the deal was not too expensive — in fact he thinks Segment may have been able to hold out for a little more, especially considering the multiplication of Twilio’s stock price this year.

Databricks, meanwhile, has evolved from an open-source data analytics platform that struggled to make revenues to a run rate of $350 million. Per an interview that Alex did for EC with chief executive Ali Ghodsi, the factors in this growth included a shift to focus on more proprietary code, big customers and sophisticated features. It’s now aiming for an IPO next year.

And what about that IPO market, which was a bit quieter this week? Alex gives a letter grade to each of the 18 most notable tech companies that have gone public this year, and observes that most them are continuing to stay in positive territory from their initial prices.

Image Credits: Brent Franson for Paystack

Lagos has been building a strong local startup scene for years, and this week that translated into a win that could mark a new era for the city, country and beyond. Stripe has agreed to acquire payments provider Paystack in a deal that Ingrid Lunden hears was worth more than $200 million. With Stripe’s own aims for a massive IPO, Paystack is poised to produce ongoing returns for the company and its investors, as well as providing Nigeria with a new generation of investors, founders and highly skilled employees who are tightly interlinked with Silicon Valley and other innovation centers.

A startup hub just needs one or two of the right deals to change everything. Readers who were paying attention when Google bought YouTube almost exactly 14 years ago today will remember the ensuing surge in fundings, foundings, acquisitions and overall consumer internet industry activity that helped the Silicon Valley internet scene get back on its feet (and helped this site get on the map, too). Stripe has said it is planning more global expansion that could include additional deals like this, so more cities around the world could be getting their moments this way.

Donau City development area – Vienna, Austria

In this week’s European investor survey for Extra Crunch, Mike Butcher checks in on Vienna, Austria, which has been tallying up growth in local startup activity recently. Here’s Eva Ahr of Capital 300, which focuses on Germanic and Central Eastern European investments, regarding about the impact of the pandemic on the local markets:

Telemedicine, online education has been accelerated. We see a shift that otherwise would have taken years, especially in the relatively conservative German-speaking area. As mentioned previously, mental health solutions, hiring and employing remotely are some of the opportunities highlighted by COVID-19. Companies that are heavily exposed are those that have been serving the long tail of companies, small merchants, and local businesses that were closed down or experienced much less traffic in past months and hence are extremely sensitive around their cost base, discontinuing services that are not 110% essential.

Mike is also working on a Lisbon survey and we’d love to hear from any investors focused on the city and Portugal in general.

Discuss the unbundling of early-stage VC with Unusual Ventures’ Sarah Leary & John Vrionis

TechCrunch:

If the ad industry is serious about transparency, let’s open-source our SDKs

Brazil’s Black Silicon Valley could be an epicenter of innovation in Latin America

South Korea pushes for AI semiconductors as global demand grows

The need for true equity in equity compensation

Trump’s latest immigration restrictions are bad news for American workers

Extra Crunch:

How COVID-19 and the resulting recession are impacting female founders

Startup founders set up hacker homes to recreate Silicon Valley synergy

Brighteye Ventures’ Alex Latsis talks European edtech funding in 2020

Dear Sophie: I came on a B-1 visa, then COVID-19 happened. How can I stay?

What the iPhone 12 tells us about the state of the smartphone industry in 2020

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast (now on Twitter!), where we unpack the numbers behind the headlines.

The whole crew was back today, with Natasha and Danny and I gathered to parse over what was really a blast of news. Lots of startups are raising. Lots of VCs are raising. And some unicorns are shooting to go public. It’s a lot to get through, but we’re here to catch you up.

Here’s what we got into:

And with that, we’re off until Monday morning. Chat soon, and stay safe.

Equity drops every Monday at 7:00 a.m. PDT and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Editor’s note: Get this free weekly recap of TechCrunch news that any startup can use by email every Saturday morning (7 a.m. PT). Subscribe here.

Why are there so many tech IPOs right now? Startups are finding that they can get higher valuations from public markets than private ones these days, because so many public investors want to put serious money in tech. Also, the lure of the future, the benevolence of the Fed, the retail investor boom, the sheer number of unicorns that have been waiting for any decent moment to go, the new ways a company can go public… these are some of the reasons Alex Wilhelm found after reviewing the latest listings and quarterly data about tech in public markets.

Various political and economic turmoils threaten to end the run, but the impact to the startup world has arrived. Consider it for a minute before the newsletter dives into stocks, SPACs, emerging industries and other useful startup news.

From this IPO boom, there’ll be another wave of startup employee wealth flooding into adjacent real-world spaces, but spread more broadly outside of the Bay Area than the days of Facebook and Twitter IPOs. Some of those employees will become investors and maybe founders, and the now-public startups will replace those positions with big-company people. The dynamics around tech hiring will be further reshaped in surprising new ways, all combined with the other changes happening like remote work.

Today, if you’re founding a startup now, you can now confidently chart new ways to build your company long-term that previous generations of founders could barely imagine.

This coming decade, we might see a startup go public that raises from pre-seed rolling funds first, pulls in newly legalized crowdfunding, matches with the right VCs from among the thousands that have are operating these days — or perhaps the startup raises debt because it’s doing that well. It could stay private as long as it wants using the various financing and secondary market possibilities that have been figured out over the last decade. Then, when it is ready to go public, it could choose between traditional options, the perfect SPAC and a direct listing, and keep the shareholder pool in favor of the true believers who have been with the company over the course of the journey.

This current group of IPOs also demonstrates something else. Tech is no longer defined as some profitless, highly valued consumer tech startup in San Francisco. It can come from anywhere, it can solve practical problems, it can make real money, and it can keep building and growing — provided you’re okay with some ongoing risk. No wonder public markets like tech these days.

Take a look at Root Insurance, an insurtech unicorn that has already helped define the Columbus, Ohio startup scene. It’s a “startup Rorscach test,” as Alex details this week about its new IPO filing. “You can find things to like (improving adjusted margins! revenue growth!), and you can find things to not like (spiraling losses! negative margins!) very easily.”

Here’s more from the Extra Crunch article:

It appears that the tailwind that many insurance providers have seen during COVID-19 has provided Root with a nice boost (driving fell during the pandemic, leading some insurance providers to return premiums.) Root is taking advantage of the moment by filing when it can show sharply improved economics.

That’s smart. But how do those improved economics bear out in traditional accounting? Let’s find out:

- Root’s revenue has skyrocketed from $43.3 million in 2018 to $290.2 million in 2019. In the first half of 2020, Root managed $245.4 million in revenue, up 135.73% from what it managed in the first half of 2019.

- Root’s losses have also shot higher, from a net loss of $69.1 million in 2018 to $282.4 million in 2019. The startup has managed to consistently lose more money over time. This was also true more recently, when its H1 2020 net loss of $144.5 million dwarfed its H1 2019 loss of $97.0 million.

The other filing this week is for Affirm, which provides a point-of-sale credit for customers (without all the tricks of credit cards). It’s also a symbol of how innovation works across the decades, for those future founders who are studying the IPO experiments of unicorns today.