startup

Auto Added by WPeMatico

Auto Added by WPeMatico

Andrea Campos has struggled with depression since she was eight years old. Over the years, she’s tried all sorts of therapies — from behavioral to pharmacotherapy.

In 2017, when Campos was in her early 20s, she learned to program and created a system to help manage her mental health. It started as a personal project, but as she talked to more people, Campos realized that many others might benefit from the system as well.

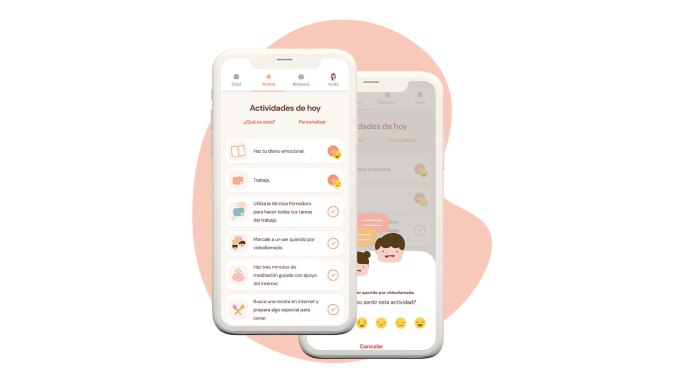

So she built an application to provide access to mental health tools for Spanish-speaking people and began testing it with a small group. At first, Campos herself was her own chatbot, texting with users who were tired of dealing with depression.

“During the month, I was pretending I was an app, and would send these people a list of activities they had to complete during the day, such as writing in a gratitude journal, and then asking them how those activities made them feel,” Campos recalls.

Her thinking was that sometimes with depression and anxiety comes “a lot of avoidance,” where people resist potential treatment out of fear.

The results from her small experiment were encouraging. So, Campos set out to conduct a bigger sample of experiments, and raised about $10,000 via a crowdfunding campaign. With that money, she hired a developer to build a chatbot for her app, which was mostly being used via Facebook Messenger.

Then an earthquake hit Mexico City and that developer lost everything — including his home and computer — and had to relocate.

“I was left with nothing,” Campos says. But that developer introduced her to another, who disappeared with his payment, and again, left Campos, “with nothing.”

“I realized at the beginning of 2019, I was going to have to do this by myself,” Campos said. So she used a site that she described as a “Wix for chatbots,” and created one herself.

After experimenting with the app with a sample of 700 people, Campos was even more encouraged and raised an angel round of funding for Yana, the startup behind her app. (Yana is an acronym for “You Are Not Alone.”) By early 2020, with just three months of runway left, she pivoted to create an app with chatbot integration that wasn’t just limited to use via Facebook Messenger.

Campos ended up launching the app more broadly during the same week that her city in Mexico went into quarantine.

Image Credits: Yana

At first, she said, she saw “normal, steady growth.” But then on October 10, 2020, Apple’s App Store highlighted Yana for International Mental Health Day, and the response was overwhelming.

“It was also my birthday so I was at a spa in a nearby town, relaxing, when I started hearing my cell phone go crazy,” Campos recalls. “Everything went nuts. I had to go back to Mexico City because our servers were exploding since they were not used to having that kind of volume.”

As a result of that exposure, Yana went from having around 80,000 users to reaching 1 million users two weeks later. Soon after that, Google highlighted the app as one of best for personal growth in 2020, and that too led to another spike in users. Today, Yana is about to hit the 5 million-user mark and is also announcing it has raised $1.5 million in funding led by Mexico’s ALLVP, which has also invested in the likes of Cornershop, Flink and Nuvocargo.

When the pandemic hit last year, six of Yana’s nine-person team decided to quarantine together in a “startup house” in Cancun to focus on building the company. Earlier this year, the company had raised $315,000 from investors such as 500 Startups, Magma and Hustle Fund. The company had pitched ALLVP, which was intrigued but wanted to wait until it could write a bigger check.

That time is now, and Yana is now among the top three downloaded apps in Mexico and 12 countries, including Spain, Chile, Ecuador and Venezuela.

With its new capital, Yana is planning to “move away from the depression/anxiety narrative,” according to Campos.

“We want to compete in the wellness space,” she told TechCrunch. “A lot of people were looking for us to deal with crises such as a breakup or a loss but then they didn’t always see a necessity to keep using Yana for longer than the crisis lasted.”

Some of those people would download the app again months later when hit with another crisis.

“We don’t want to be that app anymore,” Campos said. “We want to focus on whole wellness and mental health and transmit something that needs to be built every single day, just like we do with exercise.”

Moving forward, Yana aims to help people with their mental health not just during a crisis but with activities they can do on a daily basis, including a gratitude journal, a mood tracker and meditation — “things that prevent depression and anxiety,” Campos said.

“We want to be a vitamin for our soul, and keeping people mentally healthy on an ongoing basis,” she said. “We also want to include a community inside our application.”

ALLVP’s Federico Antoni is enthusiastic about the startup’s potential. He first met Campos when she was participating in an accelerator program in 2017, and then again recently.

The firm led Yana’s latest round because it “wanted to be on her team.”

“She [Campos] has turned into an amazing leader, and we realized her potential and strength,” he said. “Plus, Yana is an amazing product. When you download it, it’s almost like you can see a soul in there.”

Powered by WPeMatico

Here in the U.S. the concept of using a driver’s data to decide the cost of auto insurance premiums is not a new one.

But in markets like Brazil, the idea is still considered relatively novel. A new startup called Justos claims it will be the first Brazilian insurer to use drivers’ data to reward those who drive safely by offering “fairer” prices.

And now Justos has raised about $2.8 million in a seed round led by Kaszek, one of the largest and most active VC firms in Latin America. Big Bets also participated in the round, along with the CEOs of seven unicorns, including Assaf Wand, CEO and co-founder of Hippo Insurance; David Vélez, founder and CEO of Nubank; Carlos Garcia, founder and CEO of Kavak; Sergio Furio, founder and CEO of Creditas; Patrick Sigrist, founder of iFood and Fritz Lanman, CEO of ClassPass. (There’s a seventh CEO who wishes to remain anonymous). Senior executives from Robinhood, Stripe, Wise, Carta and Capital One also put money in the round.

Serial entrepreneurs Dhaval Chadha, Jorge Soto Moreno and Antonio Molins co-founded Justos, having most recently worked at various Silicon Valley-based companies including ClassPass, Netflix and Airbnb.

“While we have been friends for a while, it was a coincidence that all three of us were thinking about building something new in Latin America,” Chadha said. “We spent two months studying possible paths, talking to people and investors in the United States, Brazil and Mexico, until we came up with the idea of creating an insurance company that can modernize the sector, starting with auto insurance.”

Ultimately, the trio decided that the auto insurance market would be an ideal sector considering that in Brazil, an estimated more than 70% of cars are not insured.

The process to get insurance in the country, by any accounts, is a slow one. It takes up to 72 hours to receive initial coverage and two weeks to receive the final insurance policy. Insurers also take their time in resolving claims related to car damages and loss due to accidents, the entrepreneurs say. They also charge that pricing is often not fair or transparent.

Justos aims to improve the whole auto insurance process in Brazil by measuring the way people drive to help price their insurance policies. Similar to Root here in the U.S., Justos intends to collect users’ data through their mobile phones so that it can “more accurately and assertively price different types of risk.” This way, the startup claims it can offer plans that are up to 30% cheaper than traditional plans, and grant discounts each month, according to the driving patterns of the previous month of each customer.

“We measure how safely people drive using the sensors on their cell phones,” Chadha said. “This allows us to offer cheaper insurance to users who drive well, thereby reducing biases that are inherent in the pricing models used by traditional insurance companies.”

Justos also plans to use artificial intelligence and computerized vision to analyze and process claims more quickly and machine learning for image analysis and to create bots that help accelerate claims processing.

“We are building a design-driven, mobile first and customer experience that aims to revolutionize insurance in Brazil, similar to what Nubank did with banking,” Chadha told TechCrunch. “We will be eliminating any hidden fees, a lot of the small text and insurance-specific jargon that is very confusing for customers.”

Justos will offer its product directly to its customers as well as through distribution channels like banks and brokers.

“By going direct to consumer, we are able to acquire users cheaper than our competitors and give back the savings to our users in the form of cheaper prices,” Chadha said.

Customers will be able to buy insurance through Justos’ app, website or even WhatsApp. For now, the company is only adding potential customers to a waitlist but plans to begin selling policies later this year..

During the pandemic, the auto insurance sector in Brazil declined by 1%, according to Chadha, who believes that indicates “there is latent demand raring to go once things open up again.”

Justos has a social good component as well. Justos intends to cap its profits and give any leftover revenue back to nonprofit organizations.

The company also has an ambitious goal: to help make insurance become universally accessible around the world and the roads safer in general.

“People will face everyday risks with a greater sense of safety and adventure. Road accidents will reduce drastically as a result of incentives for safer driving, and the streets will be safer,” Chadha said. “People, rather than profits, will become the focus of the insurance industry.”

Justos plans to use its new capital to set up operations, such as forming partnerships with reinsurers and an insurance company for fronting, since it is starting as an MGA (managing general agent).

It’s also working on building out its products such as apps, its back end and internal operations tools, as well as designing all its processes for underwriting, claims and finance. Justos’ data science team is also building out its own pricing model.

The startup will be focused on Brazil, with plans to eventually expand within Latin America, then Iberia and Asia.

Kaszek’s Andy Young said his firm was impressed by the team’s previous experience and passion for what they’re building.

“It’s a huge space, ripe for innovation and this is the type of team that can take it to the next level,” Young told TechCrunch. “The team has taken an approach to building an insurance platform that blends being consumer-centric and data-driven to produce something that is not only cheaper and rewards safety but as the brand implies in Portuguese, is fairer.”

Powered by WPeMatico

It’s hard enough to talk about your feelings to a person; Jo Aggarwal, the founder and CEO of Wysa, is hoping you’ll find it easier to confide in a robot. Or, put more specifically, “emotionally intelligent” artificial intelligence.

Wysa is an AI-powered mental health app designed by Touchkin eServices, Aggarwal’s company that currently maintains headquarters in Bangalore, Boston and London. Wysa is something like a chatbot that can respond with words of affirmation, or guide a user through one of 150 different therapeutic techniques.

Wysa is Aggarwal’s second venture. The first was an elder care company that failed to find market fit, she says. Aggarwal found herself falling into a deep depression, from which, she says, the idea of Wysa was born in 2016.

In March, Wysa became one of 17 apps in the Google Assistant Investment Program, and in May, closed a Series A funding round of $5.5 million led by Boston’s W Health Ventures, the Google Assistant Investment Program, pi Ventures and Kae Capital.

Wysa has raised a total of $9 million in funding, says Aggarwal, and the company has 60 full-time employees and about three million users.

The ultimate goal, she says, is not to diagnose mental health conditions. Wysa is largely aimed at people who just want to vent. Most Wysa users are there to improve their sleep, anxiety or relationships, she says.

“Out of the 3 million people that use Wysa, we find that only about 10% actually need a medical diagnosis,” says Aggarwal. If a user’s conversations with Wysa equate with high scores on traditional depression questionnaires like the PHQ-9 or the anxiety disorder questionnaire GAD-7, Wysa will suggest talking to a human therapist.

Naturally, you don’t need to have a clinical mental health diagnosis to benefit from therapy.

Wysa isn’t intended to be a replacement, says Aggarwal (whether users view it as a replacement remains to be seen), but an additional tool that a user can interact with on a daily basis.

“Sixty percent of the people who come and talk to Wysa need to feel heard and validated, but if they’re given techniques of self help, they can actually work on it themselves and feel better,” Aggarwal continues.

Wysa’s approach has been refined through conversations with users and through input from therapists, says Aggarwal.

For instance, while having a conversation with a user, Wysa will first categorize their statements and then assign a type of therapy, like cognitive behavioral therapy or acceptance and commitment therapy, based on those responses. It would then select a line of questioning or therapeutic technique written ahead of time by a therapist and begin to converse with the user.

Wysa, says Aggarwal, has been gleaning its own insights from more than 100 million conversations that have unfolded this way.

“Take for instance a situation where you’re angry at somebody else. Originally our therapists would come up with a technique called the empty chair technique where you’re trying to look at it from the other person’s perspective. We found that when a person felt powerless or there were trust issues, like teens and parents, the techniques the therapists were giving weren’t actually working,” she says.

“There are 10,000 people facing trust issues who are actually refusing to do the empty chair exercise. So we have to find another way of helping them. These insights have built Wysa.”

Although Wysa has been refined in the field, research institutions have played a role in Wysa’s ongoing development. Pediatricians at the University of Cincinnati helped develop a module specifically targeted toward COVID-19 anxiety. There are also ongoing studies of Wysa’s ability to help people cope with mental health consequences from chronic pain, arthritis and diabetes at The Washington University in St. Louis and The University of New Brunswick.

Still, Wysa has had several tests in the real world. In 2020, the government of Singapore licensed Wysa, and provided the service for free to help cope with the emotional fallout of the coronavirus pandemic. Wysa is also offered through the health insurance company Aetna as a supplement to Aetna’s Employee Assistance Program.

The biggest concern about mental health apps, naturally, is that they might accidentally trigger an incident, or mistake signs of self harm. To address this, the U.K.’s National Health Service (NHS) offers specific compliance standards. Wysa is compliant with the NHS’ DCB0129 standard for clinical safety, the first AI-based mental health app to earn the distinction.

To meet those guidelines, Wysa appointed a clinical safety officer, and was required to create “escalation paths” for people who show signs of self harm.

Wysa, says Aggarwal, is also designed to flag responses to self-harm, abuse, suicidal thoughts or trauma. If a user’s responses fall into those categories Wysa will prompt the user to call a crisis line.

In the U.S., the Wysa app that anyone can download, says Aggarwal, fits the FDA’s definition of a general wellness app or a “low risk device.” That’s relevant because, during the pandemic, the FDA has created guidance to accelerate distribution of these apps.

Still, Wysa may not perfectly categorize each person’s response. A 2018 BBC investigation, for instance, noted that the app didn’t appear to appreciate the severity of a proposed underage sexual encounter. Wysa responded by updating the app to handle more instances of coercive sex.

Aggarwal also notes that Wysa contains a manual list of sentences, often containing slang, that they know the AI won’t catch or accurately categorize as harmful on its own. Those are manually updated to ensure that Wysa responds appropriately. “Our rule is that [the response] can be 80%, appropriate, but 0% triggering,” she says.

In the immediate future, Aggarwal says the goal is to become a full-stack service. Rather than having to refer patients who do receive a diagnosis to Employee Assistant Programs (as the Aetna partnership might) or outside therapists, Wysa aims to build out its own network of mental health suppliers.

On the tech side they’re planning expansion into Spanish, and will start investigating a voice-based system based on guidance from the Google Assistant Investment Fund.

Powered by WPeMatico

Amount, a company that provides technology to banks and financial institutions, has raised $99 million in a Series D funding round at a valuation of just over $1 billion.

WestCap, a growth equity firm founded by ex-Airbnb and Blackstone CFO Laurence Tosi, led the round. Hanaco Ventures, Goldman Sachs, Invus Opportunities and Barclays Principal Investments also participated.

Notably, the investment comes just over five months after Amount raised $86 million in a Series C round led by Goldman Sachs Growth at a valuation of $686 million. (The original raise was $81 million, but Barclays Principal Investments invested $5 million as part of a second close of the Series C round). And that round came just three months after the Chicago-based startup quietly raised $58 million in a Series B round in March. The latest funding brings Amount’s total capital raised to $243 million since it spun off from Avant — an online lender that has raised over $600 million in equity — in January of 2020.

So, what kind of technology does Amount provide?

In simple terms, Amount’s mission is to help financial institutions “go digital in months — not years” and thus, better compete with fintech rivals. The company formed just before the pandemic hit. But as we have all seen, demand for the type of technology Amount has developed has only increased exponentially this year and last.

CEO Adam Hughes says Amount was spun out of Avant to provide enterprise software built specifically for the banking industry. It partners with banks and financial institutions to “rapidly digitize their financial infrastructure and compete in the retail lending and buy now, pay later sectors,” Hughes told TechCrunch.

Specifically, the 400-person company has built what it describes as “battle-tested” retail banking and point-of-sale technology that it claims accelerates digital transformation for financial institutions. The goal is to give those institutions a way to offer “a secure and seamless digital customer and merchant experience” that leverages Amount’s verification and analytics capabilities.

Image Credits: Amount

HSBC, TD Bank, Regions, Banco Popular and Avant (of course) are among the 10 banks that use Amount’s technology in an effort to simplify their transition to digital financial services. Recently, Barclays US Consumer Bank became one of the first major banks to offer installment point-of-sale options, giving merchants the ability to “white label” POS payments under their own brand (using Amount’s technology).

“The pandemic dramatically accelerated banks’ interest in further digitizing the retail lending experience and offering additional buy now, pay later financing options with the rise of e-commerce,” Hughes, former president and COO at Avant, told TechCrunch. “Banks are facing significant disruption risk from fintech competitors, so an Amount partnership can deliver a world-class digital experience with significant go-to-market advantages.”

Also, he points out, consumers’ digital expectations have changed as a result of the forced digital adoption during the pandemic, with bank branches and stores closing and more banking done and more goods and services being purchased online.

Amount delivers retail banking experiences via a variety of channels and a point-of-sale financing product suite, as well as features such as fraud prevention, verification, decisioning engines and account management.

Overall, Amount clients include financial institutions collectively managing nearly $2 trillion in U.S. assets and servicing more than 50 million U.S. customers, according to the company.

Hughes declined to provide any details regarding the company’s financials, saying only that Amount “performed well” as a standalone company in 2020 and that the company is expecting “significant” year-over-year revenue growth in 2021.

Amount plans to use its new capital to further accelerate R&D by investing in its technology and products. It also will be eyeing some acquisitions.

“We see a lot of interesting technology we could layer onto our platform to unlock new asset classes, and acquisition opportunities that would allow us to bring additional features to our platform,” Hughes told TechCrunch.

Avant itself made its first acquisition earlier this year when it picked up Zero Financial, news that TechCrunch covered here.

Kevin Marcus, partner at WestCap, said his firm invested in Amount based on the belief that banks and other financial institutions have “a point-in-time opportunity to democratize access to traditional financial products by accelerating modernization efforts.”

“Amount is the market leader in powering that change,” he said. “Through its best-in-class products, Amount enables financial institutions to enhance and elevate the banking experience for their end customers and maintain a key competitive advantage in the marketplace.”

Powered by WPeMatico

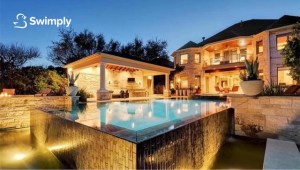

As the oldest of 12 children, Bunim Laskin spent much of his teen years looking for ways to help keep his siblings entertained. Noticing that a neighbor’s pool was often empty, Laskin reached out to ask if his family could use her pool. To make it worth her while, he suggested that they could help cover her expenses for maintaining the pool.

Soon after, five other families had made the same arrangement with her and the pool owner had six families covering 25% of her expenses. This meant that the neighbor was actually making money off her pool. The arrangement sparked a business idea in Laskin’s mind. At the age of 20, he founded Swimply, a marketplace for homeowners to rent out their underutilized pools to local swimmers, with Asher Weinberger.

The Cedarhurst, New York-based company launched a beta in 2018, starting with four pools in the New Jersey area.

“We used Google Earth to find houses, and then knocked on 80 doors with a pool,” CEO Laskin recalls. “We got to 100 pools organically. Word of mouth really helped us grow.” The site was pretty bare bones, he admits, with potential customers only able to view photos of the pools and connect with the pool owner by phone.

That year, Swimply did around 400 reservations and raised $1.2 million from friends and family.

In 2019, Swimply launched what he describes as a “proper” website and app with an automated platform. It grew “four to five times” that year, again mostly organically. In an episode that aired in March 2020, the company appeared on Shark Tank but went home without a deal.

Then the COVID-19 pandemic hit. Swimply, Laskin said, pivoted right into the pandemic.

“We were the perfect solution for people when the world was falling on its head,” he said. The company restructured its offering to ensure that pool owners did not have to interact with guests. “It was the perfect, contact-free, self-serve experience to hang out and be with people you quarantined with.”

The CDC then came out to say that it was safe to swim because chlorine could help kill the virus, and that proved to be a big boon to its business.

“On one end, it was a way for people to have a normal day and on the other, it helped give owners a way to earn an income, at a time when many people were being affected financially,” Laskin told TechCrunch.

Business took off in 2020 with revenue growing 4,000% and now Swimply is announcing a $10 million Series A round. Norwest Venture Partners led the financing, which also included participation from Trust Ventures and a number of angel investors such as Poshmark founder and CEO Manish Chandra; Rob Chesnut, former general counsel and chief ethics officer at Airbnb; Ancestry.com CEO Deborah Liu and Michael Curtis.

Swimply is now operating in a total of 125 U.S. markets, two markets in Canada and five markets in Australia. It plans to use its new capital in part to expand into new markets and toward product development.

Image Credits: Swimply

The way it works is pretty straightforward. Swimply simply connects homeowners that have underutilized backyard spaces and pools with those seeking a way to gather, cool off or exercise, for example. People or families can rent pools by the hour, ranging in price from $15 to $60 per hour (at an average of $45/hour) depending on the amenities. New markets that Swimply has recently expanded to include Portland, Oregon; Raleigh, North Carolina and the California cities of Oakland, San Luis Obispo and Los Gatos.

“The shifting mindset from younger generations about ownership is a huge contributor to increased growth of the Swimply marketplace,” said co-founder Weinberger, who serves as Swimply’s COO. “Swimming is the third most popular activity for adults and number one for children, and yet no other company has tackled the aquatic space to make swimming more affordable and accessible…until now.”

While the company declined to provide hard revenue figures, Laskin said Swimply was seeing “seven digits a month in revenue” and 15,000 to 20,000 reservations a month. Families represent the most popular reservation.

“People can book and pay through our platform, and only 20% of hosts ever meet their guests,” Laskin said. “We’re enabling a new kind of consumer behavior with what we’re doing.”

The company is planning to use its new capital to also rebuild much of its tech infrastructure and boost its customer support team to be more “readily available.”

It is also now offering a complimentary up to $1 million worth of insurance per booking for liability as well as $10,000 for property damage.

Swimply has a little over 20 employees, up 10 times from two people in December of 2020. It plans to double that number over the next few months.

The company’s model has proven quite lucrative for some owners, according to Laskin.

“Last year, there were some owners who earned $10,000 a month. One owner in Denver earned $50,000 last year and he had signed up toward the end of the summer. He should make over $100,000 this year,” Lasken projects.

Its only criteria is that owners offer a clean pool. Eighty-five percent of hosts offer restrooms as well. If they don’t, they are limited to one-hour reservations with a max of five guests. Swimply has also partnered with local pool companies, and if they pay one of its owners a visit and certify that pool, that owner gets a badge on the site “so guests get an additional level of security,” Laskin said.

Ed Yip of Norwest Venture Partners admits that when he first heard of the concept of Swimply, he “didn’t know what to make of it.”

But the more he heard about it, the more excited he got.

“This is the Holy Grail for a consumer investor. We’re not changing consumer behavior, but rather [we] productize the experience and make it safer and easier on both sides,” Yip told TechCrunch.

What also gets the investor excited is the potential for Swimply beyond just swimming pools in the future.

“We’re seeing a ton of demand from hosts wanting to list hot tubs and tennis courts, for example,” Yip said. “So this can turn into a marketplace for shared outdoor resources and that’s a huge market opportunity that adds value on both sides.”

Indeed, the concept of monetizing underutilized space is a growing concept. Earlier this year, we reported on Neighbor, which operates a self-storage marketplace, raising $53 million in a Series B round of funding. Neighbor’s unique model aims to repurpose under-utilized or vacant space — whether it be a person’s basement or the empty floor of an office building — and turn it into storage.

Powered by WPeMatico

The identity verification space has been heating up for a while and the COVID-19 pandemic has only accelerated demand with more people transacting online.

Persona, a startup focused on creating a personalized identity verification experience “for any use case,” aims to differentiate itself in an increasingly crowded space. And investors are banking on the San Francisco-based company’s ability to help businesses customize the identity verification process — and beyond — via its no-code platform in the form of a $50 million Series B funding round.

Index Ventures led the financing, which also included participation from existing backer Coatue Management. In late January 2020, Persona raised $17.5 million in a Series A round. The company declined to reveal at which valuation this latest round was raised.

Businesses and organizations can access Persona’s platform by way of an API, which lets them use a variety of documents, from government-issued IDs through to biometrics, to verify that customers are who they say they are. The company wants to make it easier for organizations to implement more watertight methods based on third-party documentation, real-time evaluation such as live selfie checks and AI to verify users.

Persona’s platform also collects passive signals such as a user’s device, location, and behavioral signals to provide a more holistic view of a user’s risk profile. It offers a low code and no code option depending on the needs of the customer.

The company’s momentum is reflected in its growth numbers. The startup’s revenue has surged by “more than 10 times” while its customer base has climbed by five times over the past year, according to co-founder and CEO Rick Song, who did not provide hard revenue numbers. Meanwhile, Persona’s headcount has more than tripled to just over 50 people.

“When we look back at the space five to 10 years ago, AI was the next differentiation and every identity verification company is doing AI and machine learning,” Song told TechCrunch. “We believe the next big differentiator is more about tailoring and personalizing the experience for individuals.”

As such, Song believes that growth can be directly tied to Persona’s ability to help companies with “unique” use cases with a SaaS platform that requires little to no code and not as much heavy lifting from their engineering teams. Its end goal, ultimately, is to help businesses deter fraud, stay compliant and build trust and safety while making it easier for them to customize the verification process to their needs. Customers span a variety of industries, and include Square, Robinhood, Sonder, Brex, Udemy, Gusto, BlockFi and AngelList, among others.

“The strategy your business needs for identity verification and management is going to be completely different if you’re a travel company verifying guests versus a delivery service onboarding new couriers versus a crypto company granting access to user funds,” Song added. “Even businesses within the same industry should tailor the identity verification experience to each customer if they want to stand out.”

Image Credits: Persona

For Song, another thing that helps Persona stand out is its ability to help customers beyond the sign-on and verification process.

“We’ve built an identity infrastructure because we don’t just help businesses at a single point in time, but rather throughout the entire lifecycle of a relationship,” he told TechCrunch.

In fact, much of the company’s growth last year came in the form of existing customers finding new use cases within the platform in addition to new customers signing on, Song said.

“We’ve been watching existing customers discover more ways to use Persona. For example, we were working with some of our customer base on a single use case and now we might be working with them on 10 different problems — anywhere from account opening to a bad actor investigation to account recovery and anything in between,” he added. “So that has probably been the biggest driver of our growth.”

Index Ventures Partner Mark Goldberg, who is taking a seat on Persona’s board as part of the financing, said he was impressed by the number of companies in Index’s own portfolio that raved about Persona.

“We’ve had our antennas up for a long time in this space,” he told TechCrunch. “We started to see really rapid adoption of Persona within the Index portfolio and there was the sense of a very powerful and very user friendly tool, which hadn’t really existed in the category before.”

Its personalization capabilities and building block-based approach too, Goldberg said, makes it appealing to a broader pool of users.

“The reality is there’s so many ways to verify a user is who they say they are or not on the internet, and if you give people the flexibility to design the right path to get to a yes or no, you can just get to a much better outcome,” he said. “That was one of the things we heard — that the use cases were not like off the rack, and I think that has really resonated in a time where people want and expect the ability to customize.”

Persona plans to use its new capital to grow its team another twofold by year’s end to support its growth and continue scaling the business.

In recent months, other companies in the space that have raised big rounds include Socure and Sift.

Powered by WPeMatico

Remote work is no longer a new topic, as much of the world has now been doing it for a year or more because of the COVID-19 pandemic.

Companies — big and small — have had to react in myriad ways. Many of the initial challenges have focused on workflow, productivity and the like. But one aspect of the whole remote work shift that is not getting as much attention is the culture angle.

A 100% remote startup that was tackling the issue way before COVID-19 was even around is now seeing a big surge in demand for its offering that aims to help companies address the “people” challenge of remote work. It started its life with the name Icebreaker to reflect the aim of “breaking the ice” with people with whom you work.

“We designed the initial version of our product as a way to connect people who’d never met, kind of virtual speed dating,” says co-founder and CEO Perry Rosenstein. “But we realized that people were using it for far more than that.”

So over time, its offering has evolved to include a bigger goal of helping people get together beyond an initial encounter –– hence its new name: Gatheround.

“For remote companies, a big challenge or problem that is now bordering on a crisis is how to build connection, trust and empathy between people that aren’t sharing a physical space,” says co-founder and COO Lisa Conn. “There’s no five-minute conversations after meetings, no shared meals, no cafeterias — this is where connection organically builds.”

Organizations should be concerned, Gatheround maintains, that as we move more remote, that work will become more transactional and people will become more isolated. They can’t ignore that humans are largely social creatures, Conn said.

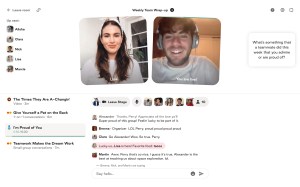

The startup aims to bring people together online through real-time events such as a range of chats, videos and one-on-one and group conversations. The startup also provides templates to facilitate cultural rituals and learning & development (L&D) activities, such as all-hands meetings and workshops on diversity, equity and inclusion.

Gatheround’s video conversations aim to be a refreshing complement to Slack conversations, which despite serving the function of communication, still don’t bring users face-to-face.

Image Credits: Gatheround

Since its inception, Gatheround has quietly built up an impressive customer base, including 28 Fortune 500s, 11 of the 15 biggest U.S. tech companies, 26 of the top 30 universities and more than 700 educational institutions. Specifically, those users include Asana, Coinbase, Fiverr, Westfield and DigitalOcean. Universities, academic centers and nonprofits, including Georgetown’s Institute of Politics and Public Service and Chan Zuckerberg Initiative, are also customers. To date, Gatheround has had about 260,000 users hold 570,000 conversations on its SaaS-based, video platform.

All its growth so far has been organic, mostly referrals and word of mouth. Now, armed with $3.5 million in seed funding that builds upon a previous $500,000 raised, Gatheround is ready to aggressively go to market and build upon the momentum it’s seeing.

Venture firms Homebrew and Bloomberg Beta co-led the company’s latest raise, which included participation from angel investors such as Stripe COO Claire Hughes Johnson, Meetup co-founder Scott Heiferman, Li Jin and Lenny Rachitsky.

Co-founders Rosenstein, Conn and Alexander McCormmach describe themselves as “experienced community builders,” having previously worked on President Obama’s campaigns as well as at companies like Facebook, Change.org and Hustle.

The trio emphasize that Gatheround is also very different from Zoom and video conferencing apps in that its platform gives people prompts and organized ways to get to know and learn about each other as well as the flexibility to customize events.

“We’re fundamentally a connection platform, here to help organizations connect their people via real-time events that are not just really fun, but meaningful,” Conn said.

Homebrew Partner Hunter Walk says his firm was attracted to the company’s founder-market fit.

“They’re a really interesting combination of founders with all this experience community building on the political activism side, combined with really great product, design and operational skills,” he told TechCrunch. “It was kind of unique that they didn’t come out of an enterprise product background or pure social background.”

He was also drawn to the personalized nature of Gatheround’s platform, considering that it has become clear over the past year that the software powering the future of work “needs emotional intelligence.”

“Many companies in 2020 have focused on making remote work more productive. But what people desire more than ever is a way to deeply and meaningfully connect with their colleagues,” Walk said. “Gatheround does that better than any platform out there. I’ve never seen people come together virtually like they do on Gatheround, asking questions, sharing stories and learning as a group.”

James Cham, partner at Bloomberg Beta, agrees with Walk that the founding team’s knowledge of behavioral psychology, group dynamics and community building gives them an edge.

“More than anything, though, they care about helping the world unite and feel connected, and have spent their entire careers building organizations to make that happen,” he said in a written statement. “So it was a no-brainer to back Gatheround, and I can’t wait to see the impact they have on society.”

The 14-person team will likely expand with the new capital, which will also go toward helping adding more functionality and details to the Gatheround product.

“Even before the pandemic, remote work was accelerating faster than other forms of work,” Conn said. “Now that’s intensified even more.”

Gatheround is not the only company attempting to tackle this space. Ireland-based Workvivo last year raised $16 million and earlier this year, Microsoft launched Viva, its new “employee experience platform.”

Powered by WPeMatico

With the increase of digital transacting over the past year, cybercriminals have been having a field day.

In 2020, complaints of suspected internet crime surged by 61%, to 791,790, according to the FBI’s 2020 Internet Crime Report. Those crimes — ranging from personal and corporate data breaches to credit card fraud, phishing and identity theft — cost victims more than $4.2 billion.

For companies like Sift — which aims to predict and prevent fraud online even more quickly than cybercriminals adopt new tactics — that increase in crime also led to an increase in business.

Last year, the San Francisco-based company assessed risk on more than $250 billion in transactions, double from what it did in 2019. The company has over several hundred customers, including Twitter, Airbnb, Twilio, DoorDash, Wayfair and McDonald’s, as well a global data network of 70 billion events per month.

To meet the surge in demand, Sift said today it has raised $50 million in a funding round that values the company at over $1 billion. Insight Partners led the financing, which included participation from Union Square Ventures and Stripes.

While the company would not reveal hard revenue figures, President and CEO Marc Olesen said that business has tripled since he joined the company in June 2018. Sift was founded out of Y Combinator in 2011, and has raised a total of $157 million over its lifetime.

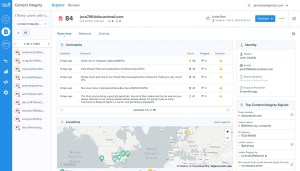

The company’s “Digital Trust & Safety” platform aims to help merchants not only fight all types of internet fraud and abuse, but to also “reduce friction” for legitimate customers. There’s a fine line apparently between looking out for a merchant and upsetting a customer who is legitimately trying to conduct a transaction.

Sift uses machine learning and artificial intelligence to automatically surmise whether an attempted transaction or interaction with a business online is authentic or potentially problematic.

Image Credits: Sift

One of the things the company has discovered is that fraudsters are often not working alone.

“Fraud vectors are no longer siloed. They are highly innovative and often working in concert,” Olesen said. “We’ve uncovered a number of fraud rings.”

Olesen shared a couple of examples of how the company thwarted fraud incidents last year. One recently involved money laundering through donation sites where fraudsters tested stolen debit and credit cards through fake donation sites at guest checkout.

“By making small donations to themselves, they laundered that money and at the same tested the validity of the stolen cards so they could use it on another site with significantly higher purchases,” he said.

In another case, the company uncovered fraudsters using Telegram, a social media site, to make services available, such as food delivery, with stolen credentials.

The data that Sift has accumulated since its inception helps the company “act as the central nervous system for fraud teams.” Sift says that its models become more intelligent with every customer that it integrates.

Insight Partners Managing Director Jeff Lieberman, who is a Sift board member, said his firm initially invested in Sift in 2016 because even at that time, it was clear that online fraud was “rapidly growing.” It was growing not just in dollar amounts, he said, but in the number of methods cybercriminals used to steal from consumers and businesses.

“Sift has a novel approach to fighting fraud that combines massive data sets with machine learning, and it has a track record of proving its value for hundreds of online businesses,” he wrote via email.

When Olesen and the Sift team started the recent process of fundraising, Insight actually approached them before they started talking to outside investors “because both the product and business fundamentals are so strong, and the growth opportunity is massive,” Lieberman added.

“With more businesses heavily investing in online channels, nearly every one of them needs a solution that can intelligently weed out fraud while ensuring a seamless experience for the 99% of transactions or actions that are legitimate,” he wrote.

The company plans to use its new capital primarily to expand its product portfolio and to scale its product, engineering and sales teams.

Sift also recently tapped Eu-Gene Sung — who has worked in financial leadership roles at Integral Ad Science, BSE Global and McCann — to serve as its CFO.

As to whether or not that meant an IPO is in Sift’s future, Olesen said that Sung’s experience of taking companies through a growth phase such as what Sift is experiencing would be valuable. The company is also for the first time looking to potentially do some M&A.

“When we think about expanding our portfolio, it’s really a buy/build partner approach,” Olesen said.

Powered by WPeMatico

Nearly exactly one month ago, digital real estate platform Loft announced it had closed on $425 million in Series D funding led by New York-based D1 Capital Partners. The round included participation from a mix of new and existing investors such as DST, Tiger Global, Andreessen Horowitz, Fifth Wall and QED, among many others.

At the time, Loft was valued at $2.2 billion, a huge jump from its being just near unicorn territory in January 2020. The round marked one of the largest ever for a Brazilian startup.

Now, today, São Paulo-based Loft has announced an extension to that round with the closing of $100 million in additional funding that values the company at $2.9 billion. This means that the 3-year-old startup has increased its valuation by $700 million in a matter of weeks.

Baillie Gifford led the Series D-2 round, which also included participation from Tarsadia, Flight Deck, Caffeinated and others. Individuals also put money in the extension, including the founders of Better (Zach Frenkel), GoPuff, Instacart, Kavak and Sweetgreen.

Loft has seen great success in its efforts to serve as a “one-stop shop” for Brazilians to help them manage the home buying and selling process.

Image Credits: Loft

In 2020, Loft saw the number of listings on its site increase “10 to 15 times,” according to co-founder and co-CEO Mate Pencz. Today, the company actively maintains more than 13,000 property listings in approximately 130 regions across São Paulo and Rio de Janeiro, partnering with more than 30,000 brokers. Not only are more people open to transacting digitally, more people are looking to buy versus rent in the country.

“We did more than 6x YoY growth with many thousands of transactions over the course of 2020,” Pencz told TechCrunch at the time of the company’s last raise. “We’re now growing into the many tens of thousands, and soon hundreds of thousands, of active listings.”

The decision to raise more capital so soon was due to a variety of factors. For one, Loft has received “overwhelming investor interest” even after “a very, very oversubscribed main round,” Pencz said.

“We have seen a continued acceleration in our market share growth, especially in São Paulo and Rio de Janeiro, the two markets we currently operate in,” he added. “We saw an opportunity to grow even faster with additional capital.”

Pencz also pointed out that Baillie Gifford has relatively large minimum check size requirements, which led to the extension being conducted at a higher price and increased the total round size “by quite a bit to be able to accommodate them.”

While the company was less forthcoming about its financials as of late, it told me last year that it had notched “over $150 million in annualized revenues in its first full year of operation” via more than 1,000 transactions.

The company’s revenues and GMV (gross merchandise value) “increased significantly” in 2020, according to Pencz, who declined to provide more specifics. He did say those figures are “multiples higher from where they were,” and that Loft has “a very clear horizon to profitability.”

Pencz and Florian Hagenbuch founded Loft in early 2018 and today serve as its co-CEOs. The aim of the platform, in the company’s words, is “bringing Latin American real estate into the e-commerce age by developing online alternatives to analogue legacy processes and leveraging data to create transparency in highly opaque markets.” The U.S. real estate tech company with the closest model to Loft’s is probably Zillow, according to Pencz.

In the United States, prospective buyers and sellers have the benefit of MLSs, which in the words of the National Association of Realtors, are private databases that are created, maintained and paid for by real estate professionals to help their clients buy and sell property. Loft itself spent years and many dollars in creating its own such databases for the Brazilian market. Besides helping people buy and sell homes, it offers services around insurance, renovations and rentals.

In 2020, Loft also entered the mortgage business by acquiring one of the largest mortgage brokerage businesses in Brazil. The startup now ranks among the top-three mortgage originators in the country, according to Pencz. When it comes to helping people apply for mortgages, he likened Loft to U.S.-based Better.com.

This latest financing brings Loft’s total funding raised to an impressive $800 million. Other backers include Brazil’s Canary and a group of high-profile angel investors such as Max Levchin of Affirm and PayPal, Palantir co-founder Joe Lonsdale, Instagram co-founder Mike Krieger and David Vélez, CEO and founder of Brazilian fintech Nubank. In addition, Loft has also raised more than $100 million in debt financing through a series of publicly listed real estate funds.

Loft plans to use its new capital in part to expand across Brazil and eventually in Latin America and beyond. The company is also planning to explore more M&A opportunities.

This article was updated post-publication to reflect accurate investor information.

Powered by WPeMatico

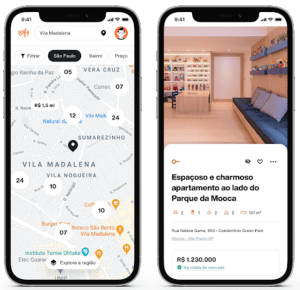

Casa Blanca, which aims to develop a “Bumble-like app” for finding a home, has raised $2.6 million in seed funding.

Co-founder and CEO Hannah Bomze got her real estate license at the age of 18 and worked at Compass and Douglas Elliman Real Estate before launching Casa Blanca last year.

She launched the app last October with the goal of matching home buyers and renters with homes using an in-app matchmaking algorithm combined with “expert agents.” Buyers get up to 1% of home purchases back at closing. Similar to dating apps, Casa Blanca’s app is powered by a simple swipe left or right.

Samuel Ben-Avraham, a partner and early investor of Kith and an early investor in WeWork, led the round for Casa Blanca, bringing its total raise to date to $4.1 million.

The New York-based startup recently launched in the Colorado market and has seen some impressive traction in a short amount of time.

Since launching the app in October, Casa Blanca has “made more than $100M in sales” and is projected to reach $280 million this year between New York and its Denver launch.

Bomze said the app experience will be customized for each city with the goal of creating a personalized experience for each user. Casa Blanca claims to streamline and sort listings based on user preferences and lifestyle priorities.

Image Credits: Casa Blanca

“People love that there is one place to book, manage feedback, schedule and communicate with a branded agent for one cohesive experience,” Bomze said. “We have a breadth of users from first time buyers to people using our platform for $15 million listings.”

Unlike competitors, Casa Blanca applies a direct-to-consumer model, she pointed out.

“While our agents are an integral part of the company, they are not responsible for bringing in business and have more organizational support, which allows them to focus on the individual more and creates a better end-to-end experience for the consumer,” Bomze said.

Casa Blanca currently has over 38 agents in NYC and Colorado, compared to about 15 at this time last year.

“We are in a growth phase and finding a unique opportunity in this climate, in particular, because there are many women exploring new, more flexible job opportunities,” Bomze noted.

The company plans to use its new capital to continue expanding into new markets, nationally and globally; as well as enhancing its technology and scaling.

“As we continue to grow in new markets, the app experience will be curated to each city — for example, in Colorado you can edit your preferences based on access to ski areas — to make sure we’re offering a personalized experience for each user,” Bomze said.

Powered by WPeMatico