Startup company

Auto Added by WPeMatico

Auto Added by WPeMatico

Starting today, TechCrunch readers can send an Extra Crunch annual membership as a gift to a friend, family member or co-worker. For a limited time we’re offering the gift at a discounted rate of $99/year (plus tax).

The gifting feature can be found here.

Extra Crunch membership is designed for startup teams, entrepreneurs, investors and business school students, and it includes more than 100 exclusive articles per month:

Extra Crunch membership can save you time time with an exclusive newsletter, no banner ads, Rapid Read mode and our List Builder tool. Annual and two-year members can also save money with discounts on events and access to Partner Perks. Our Partner Perks provide discounted access to services from companies like AWS, Brex, DocSend, Crunchbase, Typeform and more.

Gifting is currently supported in the U.S., Canada, U.K. and select countries in Europe. Purchases can be made through Visa, Mastercard and PayPal in all supported countries, but Amex support is limited to the U.S. and Canada.

If there are other features you’d like to see us add to Extra Crunch, please let us know by leaving a comment on this post or emailing me directly at travis@techcrunch.com.

TechCrunch readers can find the Extra Crunch gifting feature here.

Powered by WPeMatico

SoftBank Investment Advisers and WeWork Labs say they’ve officially kicked off the first session of Emerge, an accelerator program designed for underrepresented founders.

In their press release, the companies describe Emerge as “launched by SoftBank with support from WeWork Labs” (that’s the co-working company’s global accelerator program), with a goal of bringing more equality to tech and venture capital.

It’s an equity-free, eight-week program that includes workshops, access to mentors from SoftBank and the WeWork community and sessions with SoftBank executives. It all culminates in a showcase event for investors and SoftBank partners.

The Emerge website describes the program as based in San Mateo, Calif. — but given COVID-19, the sessions and programming are all virtual.

“Supporting underrepresented founders is a top priority for us, ensuring we see more diverse startups across the tech ecosystem,” said Catherine Lenson, managing partner and chief human resources officer at SoftBank Investment Advisers, in a statement. “There is a lack of diversity in the sector as a whole, and we need to do more to address it. That is why we’re excited to launch this program and to see the positive impact that these inspiring founders will have.”

This is also a reminder that while the larger corporate entities are currently embroiled in a legal and financial dispute, WeWork and its largest investor remain closely intertwined.

Here are the 14 startups in the initial program:

Powered by WPeMatico

Peacetime CEO/Wartime CEO by Ben Horowitz is one of the most commonly cited management think pieces of the last decade.

And for good reason; Horowitz surfaced a fundamental distinction in operating philosophy that is necessary for companies to survive, reinvent and ultimately win when macroeconomic environments shift. The framework is especially useful given how counterintuitive the advice is — behaviors of a peacetime CEO and wartime CEO are often on diametrically opposite sides of the spectrum; it is rare to find a CEO who can successfully emulate both personas.

While in concept it is easy to understand these principles, as with most things in life, nothing can replace the visceral comprehension that comes via learned experience. We are at the onset of enduring the most challenging startup environment of (at least) the last 15 years. COVID-19 is an indiscriminate event that is systematically wiping out businesses, whether “atoms” or “bits.”

For most startup operators, this is the first taste of true systematic adversity. The undercurrents of frothy valuations, the social milieu of early-stage investing and stores of excess capital are coming to a grinding halt as the bull market of the last 12 years is dramatically disrupted. We have an entire generation of founders/CEOs who may conceptually understand the peacetime CEO/wartime CEO ethos, but now, they’re going to actually live it. At the same time as every other founder/CEO. Brutal.

Since the onset of COVID-19, we have spoken to more than 100 founders and CEOs. Naturally, we are hearing frequent allusions to peacetime CEO/wartime CEO as a framework to help navigate the landscape. We’ve even used it over the last few months. While we believe it is a helpful framework, it is also incomplete. Further, we believe its application can lead to deeply problematic outcomes.

At a micro level, the misplaced application of peacetime CEO/wartime CEO can fundamentally change a company for the worse. A wartime CEO, as Horowitz notes, is “completely intolerant, rarely speaks in a normal tone, sometimes uses profanity purposefully, heightens contradictions, and neither indulges consensus building nor tolerates disagreements.” In the strictest application, we are seeing this align with a common false trope that has plagued the tech industry: “To change the world like Steve Jobs, I need to emulate all aspects of Steve Jobs’ personality.” A classic logical fallacy many founders/CEOs have learned the hard way — if you emulate all aspects of Steve Jobs’ personality, it doesn’t mean you will change the world like he did.

Each company is driven by its own unique culture and values — in a crisis situation, while it is important to be adept and agile, it’s equally, if not more important, to triple down on the strongest elements of your culture established pre-crisis. Many of the strongest founders/CEOs we have had the pleasure of coaching and investing in are uniquely world-class in their patience and tolerance, their ability to make the abnormal normal and their commitment to inspire with clarity. It is the adherence to these principles that will help carry their companies through this time.

At a macro level, peacetime CEO/wartime CEO conjures outdated themes that are at best inaccurate, and at worst, counterproductive. War implies “destruction, ruthlessness, blood, death;” there is an innate sense of machismo and bravado in this language reinforcing a homogeneous tech community. This type of vernacular and attitude increases barriers to a more inclusive community excluding women and underrepresented minority participation.

Now is the time for us to propagate community, resourcefulness and generosity.

One of the most common takeaways we have heard in reference to the framework is, “now is the time when real founders are made.” If Rent the Runway, ClassPass, Away, the Wing and the countless other women-led/minority-led startups that have been adversely affected by COVID-19 are not able to bounce back, we highly doubt it is because “they weren’t able to cut it as real founders,” a ridiculous assertion to make under any circumstance.

The peacetime CEO/wartime CEO framework is clearly valuable — it forces us to dissect the behavioral shifts necessary to survive in a crisis. That being said, it needs to evolve. Being firm, decisive and staring down an existential crisis is not mutually exclusive with applying empathy, gratitude and generosity. You can be an intense, laser-focused and paranoid CEO without losing yourself or fundamentally changing the culture of your company.

We know dozens of leaders who are leading their companies through these challenging times without leaving a wake of carnage or damage to the foundation they have spent years building. They are leading with their heart and values and will be remembered for how they carried themselves, treated their employees and guided the company through the crisis. COVID-19 presents us with a unique opportunity as an industry. Now is the right time to retire the false dilemma of peacetime CEO or wartime CEO and empower the rise of the human-centric CEO:

There’s no way to mince words. COVID-19 is having a devastating impact on the startup community. The inevitable is unfortunately occurring every day — many startups will never come back from this. As eternal optimists, however, we see opportunity in this crisis for the broader industry: the rise of the human-centric CEO. Now is the time for us to propagate community, resourcefulness and generosity. It’s the time to be ever thoughtful about employees, colleagues, stakeholders and fellow founder/CEOs in need. Individual startups may not survive this crisis, but it is our hope that an everlasting mentality does.

By no means is this list exhaustive, but it captures the behaviors and attributes from the top leaders we are working with. We believe CEOs should strive to become human-centric. Not only because it’s the right thing to do, but also because we believe it will lead to healthier organizations and better results over time.

Powered by WPeMatico

The economic effects of COVID-19 could delay Africa’s next big IPO — that of Nigerian fintech unicorn Interswitch.

If so, it wouldn’t be the first time the Lagos-based payments company’s plans for going public were postponed; the tech world has been anticipating Interswitch’s stock market debut since 2016.

For the continent’s innovation ecosystem, there’s a lot riding on the digital finance company’s IPO. After e-commerce venture Jumia, it would become only the second listing of a VC-backed African tech company on a major exchange. And Interswitch’s stock market debut — when it occurs — could bring more investor attention and less controversy to the region’s startup scene.

TechCrunch reached out to Interswitch on the window for listing, but the company declined to comment. The tech firm’s path from startup to IPO aspirant traces back to the vision of founder Mitchell Elegbe, a Nigerian electrical engineering graduate whose entire career has pretty much been Interswitch.

Africa’s tech scene is still fairly young, but it does have a timeline with several definitive points. An early one would be the success of mobile money in East Africa, with the launch of Safaricom’s M-Pesa in 2007. Another is the notable wave of VC-backed startups and founders that launched around 2010.

Interswitch CEO Mitchell Elegbe (Photo Credits: Interswitch)

With Interswtich, Elegbe pre-dated both by a number of years, founding his fintech company back in 2002 to connect Nigeria’s largely disconnected banking system. The firm became a pioneer of the infrastructure to digitize Nigeria’s economy.

Interswitch created the first electronic switch whereby Nigerian financial institutions could communicate and thereby operate ATMs and point of sales operations. The company now provides much of the rails for Nigeria’s online banking system.

Powered by WPeMatico

Despite all evidence to the contrary, there’s more to building a startup than raising venture capital.

Founders are finding success without overly relying on VC dollars; some are even sharing profits with their respective employees and customers without the help of traditional funding and Silicon Valley power dynamics.

As some investors slow down their funding pace, it has become clear that profitability trumps funding and venture capital can only take a startup so far when the economy tanks and outside cash streams dry up.

In the Indie.vc portfolio, profitability is its driving force. In fact, its main criterion for funding is that a startup must be on a clear path to profitability with durable fundamentals like high gross margins or the ability to start charging for a product right away, as opposed to companies that need a significant amount of upfront investment for research and development.

Profitability, Indie.vc founder Bryce Roberts tells TechCrunch, needs to be a habit, and founders need to recognize that it’s not a switch they can just turn on. Startups looking to prioritize profitability need to start out as revenue-driven businesses that replace funding milestones with profitability goals.

“Genuinely, it’s not rocket science,” he says. “Profitability isn’t this crazy, elusive thing. It’s literally more achievable than a Series A round. It’s way more achievable than a Series B round. If you look at the kind of fall-off between those rounds, most entrepreneurs would be better off finding their path to profitability and scale.”

Indie.vc, which recently announced its latest batch of investments, advises founders to make sure they have what they need to be stable and then to create and measure value, Roberts says. That value, which differs depending on the company, must be quantifiable as some metric or revenue.

To do that, Roberts says founders should adopt a mindset where they’re focused on creating revenue opportunities, rather than cost savings. Indie.vc’s model also does not prioritize hiring ahead of growth, a strategy that seems to be working for its portfolio during the pandemic.

Powered by WPeMatico

For the vast majority of startup founders who were planning their capital raise in Q1 2020, the COVID-19 blow was so dramatic and sweeping, we cannot see all its effects at once.

One big question on the minds of most founders: How should we plan our next raise in terms of timing, valuation and amounts?

Sarah Guo, partner at Greylock Partners, says the fundraising environment has slowed down significantly, but founders who have built ties with VCs via informal coffee updates and check-ins are at a clear advantage. “Early-stage bets require relationship-building,” says Guo, who has been investing in seed through Series B rounds.

Ram Shanmugam, founder and CEO of AutonomIQ*, a seed-stage code and process automation company, has been strengthening his relationships. For a company that has low operating expenses and a community of 600,000 developers, he says he is not fazed. “Our automation code brings efficiencies and in fact, we have nine inbound leads in Q2. Having said that, we are being realistic at the pace at which we can close these contracts.”

Similarly, Fred Blumer, who exited Hughes Telematics at an enviable $750 million, says he is taking a more pragmatic approach to the Series A raise for his new company, Mile Auto. “We expect to have a 5x growth in our business in 2020, even after adjusting for COVID,” he said. “Our pay-per-mile insurance is a great fit for people who are driving less.” Because so many drivers are sheltering in place, legacy insurance companies are refunding hundreds of millions of dollars to customers, which offers an advantage (and an opportunity) to a startup like his.

“But we need to be patient and mindful. While our families, health and safety are top priority, we are staying focused on our customers,” Blumer said. “Insurtech is a resilient arena, and in my past company we raised $100 million, so working with investors has never been a challenge. Keeping up with growth and perfecting the customer experience are what keep us up at night.” He said he plans to get out in the market after investor confidence returns.

Which may be a good idea, considering Jason Lemkin’s Twitter survey, where only 32% of respondents said they plan to deploy the same amount of capital as in the past. But another 30% are on the opposite end of the spectrum, deploying 40% to 60% less capital.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re taking a look at a bit of data on the European venture capital scene in Q1. As with our looks at other locales like Silicon Valley and other bits of the United States, we’re taking stock of what happened in the first quarter. Q1 2020 includes pre-COVID-19 results, though as some European countries began to lock-down before the United States, there may be more pandemic-impact in the following results than we’ve seen domestically thus far.

Today’s grip of data is via the folks over at PitchBook, who compiled a venture-focused dig through the continent’s first three months of the year. Let’s parse the top numbers, make a comparison or two and then look to what’s next.

Despite COVID-19, China’s broad shuttering and an aged bull market deep, Europe’s venture capital activity in Q1 2020 was mostly fine. It wasn’t great, and there were some less-than-winsome results that could be chalked up to the pandemic, but the first quarter provided an alright start to the year.

Powered by WPeMatico

Earlier today a grip of new data presented a sharply negative picture of the American economy. And this afternoon, news broke that a trio of well-known, heavily-backed unicorns were cutting staff.

With stocks down as well, we’ve received negative signals from the private market, the public market and the economy as a whole in the same day. Let’s take a minute to set the macro stage, and then go over the latest cuts from Carta (first reported by Bloomberg), Zume (Business Insider broke that particular story) and Opendoor (via The Information).

The backdrop for today’s cuts is a faltering American economy. A glance at recent news is sufficient. In the last few hours, home builder confidence recorded the “biggest drop in history,” while retail sales fell 8.7% in March, what CNBC noted was “the most ever in government data,” and CNN Business reported that American factories’ output fell 5.4% in March, “their steepest one-month slowdown since 1946.”

It’s perhaps no surprise, then, that we’ve seen unicorn layoffs all year. In January the news was Vision Fund-backed companies cutting burn to skate closer to profitability. Then, the first round of COVID-19-forced staff cuts landed at big companies; firms like Bird and TripActions slashed staff as their companies were rent by a slowdown in their core operations by the pandemic and its related economic and social changes.

Slimmer cuts at smaller companies have happened on a nearly chronic basis, something that TechCrunch has covered, as well.

Today, however, saw three cuts from three unicorns (private companies worth $1 billion or more) that have long been objects of TechCrunch’s attention. So, let’s talk about them briefly:

It’s getting hard to keep track of all the cuts. Heck, I helped break Modsy layoffs recently with TechCrunch’s Natasha Mascarenhas, and we were first to the BounceX cuts as well. It’s a rough, bad economy, and it’s harming growth-oriented companies that like startup unicorns.

More when we have it, probably sooner than we’d like to report.

Powered by WPeMatico

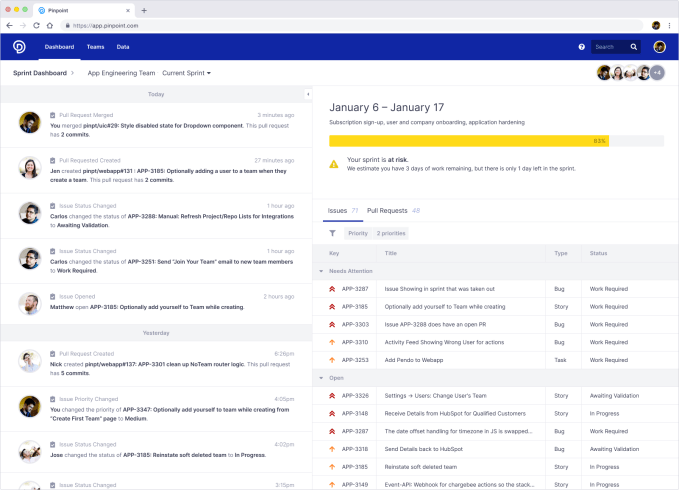

As companies look for better ways to understand how different departments work at a granular level, engineering has traditionally been a black box of siloed data. Pinpoint, an Austin-based startup, has been working on a platform to bring this information into a single view, and today it released a dashboard to help companies understand what’s happening across software engineering from an operational perspective.

Jeff Haynie, co-founder and CEO at Pinpoint says the company’s mission for the last two years has been giving greater visibility into the engineering department, something he says is even more important in the current context with workers spread out at home.

“Companies give engineering a bunch of money, and they build a bunch of amazing things, but in the end, it is just a black box, and we really don’t know what happens,” Haynie said. He says his company has been working to take all of the data to try and contextualize it, bring it together and correlate that information.

Today, they are introducing a dashboard that takes what they’ve been building and pulls it together into a single view, which is 100% self-serve. Prior to this, you needed a bunch of hand-holding from Pinpoint personnel to get it up and running, but today you can download the product and sign into your various services such as your git repository, your CI/CD software, your IDE and so forth.

It also provides a way for engineering personnel to communicate with one another without leaving the tool.

Pinpoint software engineering dashboard. Image Credit: Pinpoint

“Obviously, we will handhold and help people as they need it, and we have an enterprise version of the product with a higher level of SLA, and we have a customer success team to do that, but we’ve really focused this new release on purely self service,” Haynie said.

What’s more, while there is a free version already for teams under 10 people that’s free forever, with the release of today’s product, the company is offering unlimited access to the dashboard for free for three months.

Haynie says they’re like any startup right now, but having experience with several other startups and having lived through 9/11, the dot-com crash, 2008 and so forth, he knows how to hunker down and preserve cash. At the same time, he says they are seeing a lot of in-bound interest in the product, and they wanted to come up with a creative way to help customers through this crisis, while putting the product out there for people to use.

“We’re like any other startup or any other business frankly at this point: we’re nervous and scared. How do you survive this [and how long will it last]? The other side of it is that we’re rushing to take advantage of this inbound interest that we’re getting and trying to sort of seize the opportunity and try to be creative about how we help them.”

The startup hopes that, if companies find the product useful, after three months they won’t mind paying for the full version. For now, it’s just putting it out there for free and seeing what happens with it — just another startup trying to find a way through this crisis.

Powered by WPeMatico

Good morning friends, and welcome back to TechCrunch’s Equity Monday, a short-form audio hit to kickstart your week.

Before we jump into today’s show, don’t forget that the long-form Equity that started in the unicorn era and continue in today’s changed world still drops on Friday. We had a blast last week, so make sure to catch up.

That said, there was a lot to go over this morning, so let’s get into what we had to discuss:

And that’s the show for today. Stay safe, and we’ll be back Friday morning to cap off whatever this week winds up becoming.

Equity drops every Monday at 7:00 AM PT and Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico