Startup company

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome, the HR software that helps organizations make and close offers to new candidates, announced the close of a $6 million seed round today, led by FirstMark Capital. Participating investors include Ludlow Ventures, Nat Turner and Zach Weinberg, and Keenan Rice and Ben Porterfield (which were existing investors), as well as a wide array of angels.

TechCrunch last covered Welcome in August, when it announced a $1.4 million funding round. That the startup was able to raise more as quickly as it has is testament to how hot the early-stage venture capital market is today, and likely an endorsement of Welcome’s economic profile and recent growth.

Past the new capital, Welcome is also launching a new product today called Total Rewards, which helps not just new candidates but also existing employees get a complete, easy-to-understand picture of their compensation, across salary, benefits, equity, etc.

But let’s back up.

Welcome was founded in 2019 by Nick Gavronsky and Rick Pereira, with a mission to help organizations close offers on candidates by providing a much clearer picture of compensation, particularly around equity. Co-founder and CEO Nick Gavronsky explained that many candidates don’t truly understand the value of the equity they’re offered, or how it works.

“A lot of recruiting teams aren’t well-equipped to use it as a selling tool and explain it effectively and showcase the value to candidates to help them think about their ownership at the company,” he added.

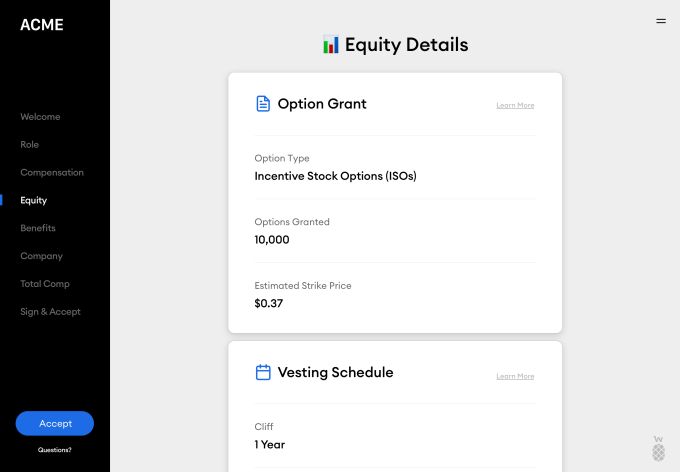

Image Credits: Welcome

Welcome allows companies to organize their compensation offers based on level and position, and deliver that information digitally to candidates in a way that makes sense.

The startup integrates with a variety of other software providers, including Slack, Lever, Greenhouse, ADP and Justworks to name a few, simplifying onboarding for Welcome clients and bringing a broad array of information into one place.

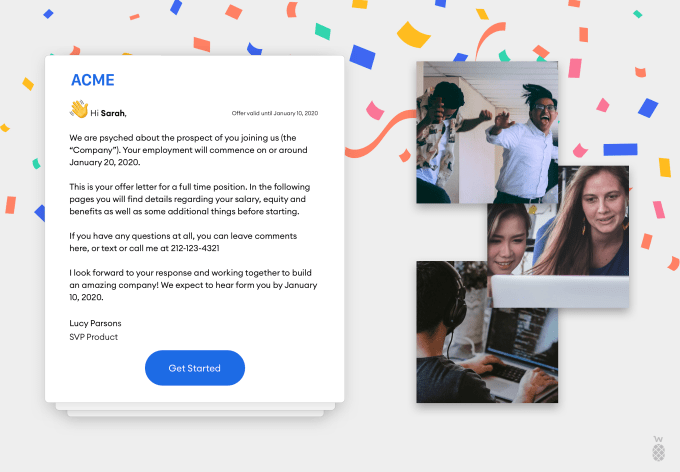

Offers sent through Welcome show a description of the role, equity details, total compensation and even include a welcome note and video. This is in stark contrast to the black and white legal PDF often sent to candidates.

Image Credits: Welcome

The next phase for the company comes in the form of the launch of Total Rewards, which is meant to help retain existing employees, helping them understand their compensation value and their potential at the company.

“Painting a better picture becomes a pre-retention tool,” said Gavronsky. “An employee will sometimes leave thousands of dollars on the table because they don’t understand what they’re walking away from. A lot of times companies will wait until that person is going to resign. Let me now bring up all the things that are great about our company and talk through your stock options. But the decision’s already made. So we wanted something that we can kind of put in with performance reviews.”

Welcome also has plans to offer a third product pillar in the form of real-time accurate industry-wide compensation data, helping companies understand where they fit into the larger ecosystem with regards to compensation.

Thus far, Welcome has 40 companies on the platform, including Uncork and Betterment, with hundreds on the waitlist, according to the co-founders. The company plans to use the funding to build out the team and the product.

Powered by WPeMatico

If I were to pick one thing that unites the global tech scene in terms of culture I would point to the respect and reverence accorded to startup founders.

After all, creating your own company is an ambition many of us harbor. It can bring with it unparalleled freedom, a lasting legacy, prestige, wealth and the ability to do good. Across social and traditional media the feats of founders big and small are lauded for their genius on a daily basis. Many entrepreneurs go to great lengths to showcase their backbreaking hard work and eye-popping success. An outsider would be forgiven for believing that every founder is living the dream as a result of their talent and toil.

Of course, as with nearly every image projected online, the reality is quite different. There is a seldom talked about price of being a founder — the impact on one’s mental health.

A recent study by the National Institute of Mental Health found that 72% of entrepreneurs are directly or indirectly impacted by mental health issues. This compares to 48% of the general population. The damage can also affect loved ones — 23% of entrepreneurs report that they have family members with problems, which is 7% higher than the relations of nonentrepreneurs.

I am in no way a mental health expert. But what I do know from both my own experience and speaking to scores of business owners I work with is that being a founder is an inherently lonely job. Pressure is high and uncertainty pervades every decision. Fear of failure is ever present. Unaddressed, these issues can take a serious toll.

The unpalatable truth is that the situation appears to be getting worse. A similar study conducted in 2015 by Dr. Michael A. Freeman found the rate of mental health issues among founders to be lower — at 50%. While comparing different research pieces is inexact, we only need to look at how the global recession has damaged many companies and how working from home has contributed to feelings of isolation, to know that the environment for startups has got harder this year. Added to this mix is how social media continues to promote an unhealthy fetishization of hustle culture and founding myths.

A number of founders have told me that they have constant feelings of inadequacy and guilt when they compare themselves to the startup gurus who celebrate working 24/7, are constantly selling, raising money or making their millions. They feel they should be working harder or be doing better — just like all the people they read about.

So how do we address this? The first step is talking about it. This means having an environment where we can be honest that not everything is always fine. Speaking to a fellow founder, not about commercial concerns, but about personal worries can be revelatory. I’ve seen it happen in our community. It’s like an “Emperor’s New Clothes” moment.

The myth of the bulletproof, genius, hustling founder can disappear in a puff of smoke as people suddenly realize they are not alone. They find that the concerns, anxieties and uncertainties they feel are almost universal.

Experienced founders can provide invaluable support to people new to the startup scene. They can share their experiences, both failures and success, and reveal some of their coping mechanisms. I would strongly advise founders who are experiencing some of the worries I’ve outlined to actively seek out advice from both their peers and potential mentors — much in the way they may seek out commercial guidance.

Next, we need to address how we tackle the culture and myths around being a founder. Business owners need to know that many of the extraordinary “success stories” they see celebrated online are exactly that — extraordinary.

Similarly, those that promote the principle that working all hours is the only way to be successful are at best talking about what works for them, and are at worst, engaging in a performance to achieve attention. We need to think carefully about how we respond to these posts. There is a fine line between being supportive and enabling unhealthy or damaging behavior and philosophy.

After all, success in the startup scene is all relative. For some owning a small business that makes them a decent income with a good work-life balance is the goal. For others, it is simply being able to do what they love in the way that they want. Very few will get the exit that makes them a millionaire, and an infinitesimally small minority will build the next Facebook . I cannot stress enough how important it is for founders to keep their aims and ambitions in perspective and ignore the noise they hear online.

More broadly, the industry, including the media, does need to get wiser about how it views and represents founders. For example, a pervasive myth is that some of the biggest tech companies in the world started in garages with no money, then through the genius and sheer bloodymindedness of their founder they were grown into a massive corporation.

The reality is that the vast majority of these tech companies benefited from substantial seed capital from family or connections almost from day one. These founders were also quickly surrounded by highly talented people who did a lot of the heavy lifting and, whisper it, a truckload of good luck. In short, the idea of the superhuman founder perpetuated in the industry is, in nearly all cases, nonsense.

In a similar vein, there are also issues around how we frame success and failure.

Success, as I’ve mentioned earlier, is nearly always couched in the most basic numerical terms. The “unicorn” label is bandied about so often that many people fail to realize that it’s simply a valuation that a few investors have given a company. It does not reflect whether the business is actually successful in the traditional sense, i.e., making money. Generally, the startup scene celebrates and idolizes founders who make big exits or achieve “unicorn status” — less is spoken about the thousands of SMEs that employ people, develop and patent new tech, make a tidy profit and pay taxes.

With failure, there is an altogether different problem. The startup scene downplays failure as par for the course. It is, on the face of it, one of the industry’s great virtues. It enables people to try without fear of embarrassment. However, in practice, it can actually minimize real-world fears nearly all founders have. Failure cannot just be brushed off if you’ve devoted years of your life, spent a lot of money and have staff who rely on you. By simply thinking of failure as part of the process we cannot address and talk about this real source of concern in an open way. “Fail fast” only works for those who can afford it.

Individually, these issues may seem like nothing but white noise and the cure for suffering founders may simply be to get off social media. Unfortunately, it isn’t that simple. Social and traditional media is amplifying startup culture, not creating it. The same tropes are on display at every tech conference and meetup. To fit in, the founder is expected to be a fearless, genius visionary. Deviation from this norm, such as by displaying vulnerability around mental health, is by inference, failure.

Despite its shortcomings in relation to diversity, the startup scene is generally one of the most progressive, collaborative and open industries in the world. These virtues are ideally suited to tackling the reluctance to discuss mental health and creating the network of support that ensures people don’t suffer alone.

To make this happen, we need to dispense with the myths and hagiography around being a founder and be more honest about what the reality of running a business actually entails.

Powered by WPeMatico

BuildBuddy, whose software helps developers compile and test code quickly using a blend of open-source technology and proprietary tools, announced a funding round today worth $3.15 million.

The company was part of the Winter 2020 Y Combinator batch, which saw its traditional demo day in March turned into an all-virtual affair. The startups from the cohort then had to raise capital as the public markets crashed around them and fear overtook the startup investing world.

BuildBuddy’s funding round makes it clear that choppy market conditions and a move away from in-person demos did not fully dampen investor interest in YC’s March batch of startups, though it’s far too soon to tell if the group will perform as well as others, given how long it takes for startup winners to mature into exits.

BuildBuddy has foundations in how Google builds software. To get under the skin of what it does, I got ahold of co-founder Siggi Simonarson, who worked at the Mountain View-based search giant for a little over a half decade.

During that time he became accustomed to building software in the Google style, namely using its internal tool called Blaze to compile his code. It’s core to how developers at Google work, Simonarson told TechCrunch. “You write some code,” he added, “you run Blaze build; you write some code, you run Blaze test.”

What sets Blaze apart from other developer tools is that “opposed to your traditional language-specific build tools,” Simonarson said, it’s code agnostic, so you can use it to “build across [any] programming language.”

Google open-sourced the core of Blaze, which was named Bazel, an anagram of the original name.

So what does BuildBuddy do? In product terms, it’s building the pieces of Blaze that Google engineers have access to inside the company, for other developers using Bazel in their own work. In business terms, BuildBuddy wants to offer its service to individual developers for free, and charge companies that use its product.

Simonarson and his co-founder Tyler Williams started small, building a “results UI” tool that they shared with a Bazel user group. The members of that group picked up the tool, rapidly bringing it inside a number of sizable companies.

This origin story underlines something that BuildBuddy has that early-stage startups often lack, namely demonstrable enterprise market appetite. Lots of big companies use Bazel to help create software, and BuildBuddy found its way into a few of them early in its life.

Simply building a useful tool for a popular open-source project is no guarantee of success, however. Happily for BuildBuddy, early users helped it set direction for its product development, meaning that over the summer the startup added the features that its current users most wanted.

Simonarson explained that after BuildBuddy was initially used by external developers, they demanded additional tools, like authentication. In the words of the co-founder, the response from the startup was “great!” The same went for a request for dashboarding, and other features.

Even better for the YC graduate, some of the features requested were the sort that it intends to charge for. That brings us back to money and the round itself.

BuildBuddy closed its round in May. But like with most venture capital tales, it’s not a simple story.

According to Simonarson, his startup started raising the round during one of those awful early-COVID days when the stock market dropped by double-digit percentage points in a single trading session.

BuildBuddy’s goal was to raise $1.5 million. Simonarson was worried at the time, telling TechCrunch that it was his first time fundraising, and that he wasn’t sure if his startup was going to “raise anything at all” in that climate.

But the nascent company secured its first $100,000 check. And then a $300,000 check, over time managing to fill out its round.

So what happened that got the company from $1.5 million to just over $3 million? The investor that put in $300,000 wanted to put in another $2 million. The company talked them down to $1.5 million at a higher cap (BuildBuddy raised its round using a SAFE), and the deal was done at those terms.

The startup initially didn’t want to raise the extra cash, but Simonarson told TechCrunch that at the time it was not clear where the fundraising environment was heading; BuildBuddy raised back when startup layoffs were a leading story, and a return to high-cadence VC rounds was months away.

So BuildBuddy wound up securing $3.15 million to support a current headcount of four. It intends to hire, naturally, lower its comically long runway and keep building out its Bazel-focused service.

Picking a few names from the investor spreadsheet that BuildBuddy sent over — points for completeness to the startup — Y Combinator, Addition, Scribble and Village Global, among others put capital into the round.

Dev tools are hot at the moment. Given that, as soon as BuildBuddy’s ARR starts to get moving, I expect we’ll hear from them again.

Powered by WPeMatico

Startups need to live in the future. They create roadmaps, build products and continually upgrade them with an eye on next year — or even a few years out.

Big companies, often the target customers for startups, live in a much more near-term world. They buy technologies that can solve problems they know about today, rather than those they may face a couple bends down the road. In other words, they’re driving a Dodge, and most tech entrepreneurs are driving a DeLorean equipped with a flux-capacitor.

That situation can lead to a huge waste of time for startups that want to sell to enterprise customers: a business development black hole. Startups are talking about technology shifts and customer demands that the executives inside the large company — even if they have “innovation,” “IT,” or “emerging technology” in their titles — just don’t see as an urgent priority yet, or can’t sell to their colleagues.

How do you avoid the aforementioned black hole? Some recent research that my company, Innovation Leader, conducted in collaboration with KPMG LLP, suggests a constructive approach.

Rather than asking large companies about which technologies they were experimenting with, we created four buckets, based on what you might call “commitment level.” (Our survey had 211 respondents, 62% of them in North America and 59% at companies with greater than $1 billion in annual revenue.) We asked survey respondents to assess a list of 16 technologies, from advanced analytics to quantum computing, and put each one into one of these four buckets. We conducted the survey at the tail end of Q3 2020.

Respondents in the first group were “not exploring or investing” — in other words, “we don’t care about this right now.” The top technology there was quantum computing.

Bucket #2 was the second-lowest commitment level: “learning and exploring.” At this stage, a startup gets to educate its prospective corporate customer about an emerging technology — but nabbing a purchase commitment is still quite a few exits down the highway. It can be constructive to begin building relationships when a company is at this stage, but your sales staff shouldn’t start calculating their commissions just yet.

Here are the top five things that fell into the “learning and exploring” cohort, in ranked order:

Technologies in the third group, “investing or piloting,” may represent the sweet spot for startups. At this stage, the corporate customer has already discovered some internal problem or use case that the technology might address. They may have shaken loose some early funding. They may have departments internally, or test sites externally, where they know they can conduct pilots. Often, they’re assessing what established tech vendors like Microsoft, Oracle and Cisco can provide — and they may find their solutions wanting.

Here’s what our survey respondents put into the “investing or piloting” bucket, in ranked order:

By the time a technology is placed into the fourth category, which we dubbed “in-market or accelerating investment,” it may be too late for a startup to find a foothold. There’s already a clear understanding of at least some of the use cases or problems that need solving, and return-on-investment metrics have been established. But some providers have already been chosen, based on successful pilots and you may need to dislodge someone that the enterprise is already working with. It can happen, but the headwinds are strong.

Here’s what the survey respondents placed into the “in-market or accelerating investment” bucket, in ranked order:

Powered by WPeMatico

Listen up, space fans and aficionados. You have just 48 hours left to secure an early-bird ticket to TC Sessions: Space 2020, a two-day virtual conference dedicated to early-stage space startups and the community that supports them. Join the brilliant minds, leading founders, shrewd investors and boundary-pushing engineers determined to shape the future of space exploration and everything that entails.

Early-bird pricing remains in orbit for another 48 hours. Buy your ticket ($125) before the orbit decays on November 13 at precisely 11:59 p.m. (PT) and save $100.

You’ll have an outstanding selection of presentations, interviews, panel discussions, breakout sessions and interactive Q&As available at the click of your mouse. Expert speakers — spanning the public, private and defense sectors — will share a veritable galaxy of wisdom, experience and insight.

What level of expertise are we talking here? Well, and this is just for starters, we have NASA Associate Administrator of Human Exploration & Operations Mission Directorate Kathryn Lueders, Rocket Lab CEO Peter Beck, U.S. Space Force Chief of Space Operations General Jay Raymond, Lockheed Martin VP and Head of Civil Space Programs Lisa Callahan.

Topics cover a broad swath of technologies, including 3D-printed rockets, earth observation data, orbital operations, ground station networks, launch services, broadband communications, defense operations and manufacturing in space. Explore the event agenda here.

You’ll find up-and-coming early-stage startups and sponsors showcasing their technology in our expo area. See the latest innovations and connect with potential customers, collaborators or investors. And be sure to take advantage of CrunchMatch. Our free AI-based platform takes the pain out of networking and helps you find and connect with the people who align with your goals. It’s the perfect tool to bridge a virtual conference and connect with attendees around the globe.

If you want to showcase your startup in the expo, buy a Startup Exhibitor Package. The price includes three passes, online exhibit space and lead-generation capability. Here’s a hot opportunity — each exhibiting startup gets five minutes to pitch live to Session attendees. Talk about focused exposure.

Pro Pitch Tip: Have a team member hit record right before you step up to the virtual stage, and you’ll have a video of your TC Session pitch — study it for ways to improve or hey, it could be a straight-up marketing tool right out of the gate.

Don’t miss your opportunity to learn from, engage and connect with other brilliant members of your elite community at TC Sessions: Space 2020 on December 16-17. Don’t space out on early-bird savings — only 48 hours left! Purchase your ticket before November 13 at 11:59 p.m. (PT).

Is your company interested in sponsoring TC Sessions: Space 2020? Click here to talk with us about available opportunities.

Powered by WPeMatico

When you’re running your own venture — especially if it’s your first — it’s unlikely you will find the time to deep dive into how venture capital firms work. Fundraising is distracting for founders and can even hurt their company in the early days. But if you only start learning about VCs when you’re already down the fundraising path, you’ll already be too late.

Founders tend to make a series of classic mistakes when raising funding. Error number one (and two) is to raise the wrong amount of money and to do it at the wrong time. This double whammy results in founders being very diluted too early or not raising enough money to reach the next funding stage.

They can also put all their eggs in one basket too early. I made that mistake. I had signed a term-sheet (a nonbinding agreement) for a €2.5 million Series A round, passed the due diligence process, and the investment committee had approved the deal. But at the very last minute, a claim from one of the angels on my cap table made the prospect investor change his mind. In a Point Nine Capital survey, founders said that the two most stressful elements of raising venture capital are not knowing where in the fundraising process they are and not understanding why VCs have rejected their proposal.

On the other hand, if you know what VCs all about, you’ll be geared up for the ride, know the kind of investor personality you’re aiming for, and crucially — you’ll optimize the value of your equity in the long run. Founders who manage to raise more VC funds end up having a greater value stake in their company when the time comes to IPO, according to statistical research. The learning curve is steep; you’re not just studying VC as an industry, but the individual investors themselves. So, I’ve decided to share the main lessons about VC that I wish I’d known when I was a startup founder chasing venture capital.

Startups are all about reaching two milestones: (a) product/market fit and (b) a profitable, repeatable and scalable growth model. Once those two corners are turned, the risk of a startup decreases enormously, which is normally reflected in the valuation. As an early-stage founder, if you want to protect your ownership, make sure you’re raising small amounts of money while your valuations are low.

Save your cash until you de-risk your early-stage startup. Then, raise aggressively when you finally have hard evidence that you have a strong product/market fit and a clear growth model. Be sure you understand when your company reaches that stage and becomes a scaleup. You don’t want to be a founder that has successfully raised a Series A round but has very little ownership and a very long road ahead.

Sometimes, the timing is out of your hands. The price of equity in startups is governed by the supply and demand of capital. Investors themselves have to raise money from another type of investor called Limited Partners (LPs), who may hold stakes in a variety of assets. If LPs have a strong interest in VC assets, there is more supply of capital and the price of startup equity will rise. But the opposite is also true. If you take a look at the last two recessions in the United States (2000 and 2008), you will see that the stock market crash coincided with corrections to valuations in the VC market.

So, be strategic and raise when “the market” has a strong appetite for your equity; otherwise, stretch your runway and wait for the right time. Right now, it’s common to see startups postponing their next raise to 2021, looking for stronger winds.

I see two conditions for startups to raise a large round: (a) a large market that can justify a sizable exit, and (b) a large VC fund (small funds don’t need super sizable exits to be successful).

Assuming the first condition is met, where can we find those large VC funds? Typically, they’ll be in locations close to large markets, with a track record of sizable exits.

Powered by WPeMatico

Year-in, year-out, the gender gap in venture capital investment continues to be a problem women founders face. While the gender gap in other areas (such as the number of women entering tech in general) may be on the right path, this disparity in funding seems to be stagnant. There has been little movement in the amount of VC dollars going to women-founded companies since 2012.

In fintech, the problem is especially prominent: Women-founded fintechs have raised a meager 1% of total fintech investment in the last 10 years. This should come as no surprise, given that fintech combines two sectors traditionally dominated by men: finance and technology. Though by no means does this mean that women aren’t doing incredible work in the field and it’s only right that women founders receive their fair share of VC investment.

In the short term, women founders can take action to boost their chances at VC success in the current investment climate, including leveraging their community and support network and building the necessary self-belief to thrive. In the long term, there needs to be foundational change to level the playing field for women entrepreneurs. VC funds must look at ways they can bring in more women decision-makers, all the way up to the top.

Let’s dive into the state of gender bias in VC investing as it stands, and what founders, stakeholders and funds themselves can do to close the gap.

In 2019, less than 3% of all VC investment went to women-led companies, and only one-fifth of U.S. VC went to startups with at least one woman on the founder team. The average deal size for female-founded or female co-founded companies is less than half that of only male-founded startups. This is especially concerning when you consider that women make up a much bigger portion of the founder community than proportionately receive investment (around 28% of founders are women). Add in the intersection of race and ethnicity, and the figures become bleaker: Black women founders received 0.6% of the funding raised since 2009, while Latinx female founders saw only 0.4% of total investment dollars.

The statistics paint a stark picture, but it’s a disparity that I’ve faced on a personal level too. I have been faced with VC investors who ask my co-founder — in front of me — why I was doing the talking instead of him. On another occasion, a potential investor asked my co-founder who he was getting into business with, because “he needed to know who he’d be going to the bar with when the day was up.”

This demonstrates a clear expectation on the part of VC investors to have a male counterpart within the founding team of their portfolio companies, and that they often — whether subconsciously or consciously — value men’s input over that of the women on the leadership team.

So, if you’re a female founder faced with the prospect of pitching to VCs — what steps can you take to set yourself up for success?

Women founders looking to receive VC investment can take a number of steps to increase their chances in this seemingly hostile environment. My first piece of advice is to leverage your own community and support network, especially any mentors and role models you may have, to introduce you to potential investors. Contacts that know and trust your business may be willing to help — any potential VC is much more likely to pay you attention if you come as a personal recommendation.

If you feel like you’re lacking in a strong support network, you can seek out female-founder and startup groups and start to build your community. For example, The Next Women is a global network of women leaders from progress-driven companies, while Women Tech Founders is a grassroots organization on a mission to connect and support women in technology.

Confidence is key when it comes to fundraising. It’s essential to make sure your sales, pitch and negotiation skills are on point. If you feel like you need some extra training in this area, seek out workshops or mentorship opportunities to make sure you have these skills down before you pitch for funding.

When talking with top male VCs and executives, there may be moments where you feel like they’re responding to you differently because of your gender. In these moments, channeling your self-belief and inner strength is vital: The only way that they’re going to see you as a promising, credible founder is if you believe you are one too.

At the end of the day, women founders must also realize that we are the first generation of our gender playing the VC game — and there’s something exciting about that, no matter how challenging it may be. Even when faced with unconscious bias, it’s vital to remember that the process is a learning curve, and those that come after us won’t succeed if we simply hand the task over to our male co-founder(s).

While there are actions that women can take on an individual level, barriers cannot be overcome without change within the VC firms themselves. One of the biggest reasons why women receive less VC investment than men is that so few of them make up decision-makers in VC funds.

A study by Harvard Business Review concluded that investors often make investment decisions based on gender and ask women founders different questions than their male counterparts. There are countless stories of women not being taken seriously by male investors, and subsequently not being seen as a worthwhile investment opportunity. As a result of this disparity in VC leadership teams, women-focused funds are emerging as a way to bridge the funding gender gap. It’s also worth noting that women VCs are not only more likely to invest in women-founded companies, but also those founded by Black entrepreneurs. In addition to embracing women and minority-focused investors, the VC community as a whole should ensure they’re bringing in more women leaders into top positions.

From day one, the Prometeo team has made concerted efforts to have both men and women in decision-maker roles. Having women in the founding team and in leadership positions has been crucial in not only helping to fight the unconscious bias that might take place, but also in creating a more dynamic work environment, where diversity of thought powers better business decisions.

Striving for gender equality, both within the walls of VC funds and in the founder community, is also better for businesses’ bottom line. In fact, a study by Boston Consulting Group found that women-founded startups generate 78% for every dollar invested, compared to 31% from men-founded companies.

Here in Latin America, women founders receive a higher proportion of VC investment than anywhere else in the world, so it’s no surprise that women are leading the region’s fintech revolution. Having more women in leadership positions is ultimately a better bet for business.

Closing the gender gap in VC funding is no simple task, but it’s one that must be undertaken. With the help of internal VC reform and external initiatives like community building, training opportunities and women-focused support networks, we can work toward finally making the VC game more equitable for all.

Powered by WPeMatico

So much can change in a day.

This morning, news that a trial COVID-19 vaccine candidate had an effective rate of more than 90% shook the financial world. The Pfizer vaccine is reportedly so effective, the company “will have manufactured enough doses to immunize 15 to 20 million people” by the end of the year, according to the New York Times, appears to have given investors the green light to pile back into companies harmed by the pandemic.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

The shift of money from shares that proved popular during the summer is massive and abrupt. Zoom and Peloton are down sharply this morning, while Uber and Lyft are soaring. Indeed, the Dow Jones Industrial Average and S&P 500 indices are up around 4.8% and 3.3% respectively, while SaaS and cloud share are off 3.5%.

Investors are taking money out of companies that were expected to do well thanks to the pandemic and moving that capital into firms that were weakened by the pandemic.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Short-term market movements do not always predict the future accurately, so we should not treat today’s trading as gospel.

That said, it’s not hard to draw some basic conclusions from the trading activity. Here’s what I think we can deduce from today’s stock market activity:

Powered by WPeMatico

The flow of venture capital in 2020 has been surprisingly strong given the year’s general uncertainty, but while investors have showered plenty of dough on growth-stage companies, seed-stage startups are down 32% last quarter compared to the year before.

There have been plenty of recent conversations about alternative funding routes for founders, and one of those oft-overlooked paths has been equity crowdfunding. While crowdfunding platforms like Kickstarter push consumers to back unrealized projects in exchange for products or other services, equity crowdfunding allows consumers to actually invest cash and receive a piece of the company. It’s not a conventional path, but it can be a viable option for companies that have a close relationship with an engaged customer base.

The Security and Exchange Commission’s Regulation Crowdfunding guidelines were adopted under Title III of the JOBS Act back in 2016, but because many entrepreneurs were unfamiliar with how to participate, many of the startups that have taken advantage of it haven’t been the highest quality. The tide could be turning: This week, the SEC updated some of its guidance on crowdfunding, eliminating some ambiguities and increasing the amount of capital companies can raise from both accredited and nonaccredited investors. Additionally, companies can now raise $5 million per year using equity crowdfunding, compared to the previous limit of $1.07 million.

But life has gotten easier in other ways as well for founders pursuing this fundraising type and the platforms that seek to simplify it.

Wefunder is one of a handful of equity crowdfunding platforms that have popped up in the last few years. Before a company can raise on its platform, Wefunder vets them before allowing them to tap into their network of amateur investors who can invest as little as $100 with the median investment sitting at $250. Last month, 40 companies launched on Wefunder and collectively raised $12 million, according to Wefunder CEO Nicholas Tommarello.

Powered by WPeMatico

Whether space is the final frontier remains to be seen, but it’s certainly the next one as far as we’re concerned. On December 16-17, we’re hosting TC Sessions: Space 2020, a two-day online conference and our first event focused squarely on space technology and the early-stage startups and investors that make it possible.

The future of this industry is wide open, and it’s going to require cultivating a deep bench of visionaries to sustain it. And it starts with affordable access for students eager to turn science fiction into fact. Grab your $50 student pass here and get ready to shift your career into warp speed.

Pro Tip: We offer a range of ticket options for nonstudents (including discounts for government, military and nonprofits). Buy yours before early-bird pricing ends on November 13 at 11:59 p.m. PST. Also, current Extra Crunch subscribers receive an additional 20% discount on passes.

This is your chance to hear from the best and brightest people leading this universal expedition. You’ll meet and engage with engineers, founders, investors, executives, military and government officials.

We’re talking officials like NASA administrator Jim Bridenstine and Space Command’s General John W. Raymond. We’re talking founders like Relativity Space’s Tim Ellis and Rocket Lab’s Peter Beck. We’re talking investors like Bessemer Venture Partners’ Tess Hatch and SpaceFund’s Meagan Crawford. And that’s just the tip of the rocket, so to speak.

We’re packing the two-day event with top-notch programming. Set coordinates for the main stage for fireside chats and moderated panel discussions. TechCrunch editors ask the tough questions and dig deep on topics like launch services, orbital operations, ground station networks, broadband communications, earth observation data, manufacturing and military operations in space.

Don’t miss the breakout sessions and Q&As. Breakouts let you explore specific topics. Main stage events always generate lots of questions, and the Q&A sessions give the audience a chance to pose questions to speakers who appeared on the main stage.

Searching for a stellar internship or a job that’s out of this world? Ouch. Explore the expo area where you’ll find early-stage space startups and sponsors showcasing their tech and talent.

That brings us to networking. Remember, this virtual conference reaches thousands of people around the world. It’s prime territory for expanding your network — an essential part of startup success. You’ll have free use of CrunchMatch, our AI-powered networking platform.

It makes quick, efficient work out of finding, scheduling and meeting people. Not just any people — people who align with your startup interests. People who can help you build a business or a career. Answer a few quick questions when you register and CrunchMatch goes to work for you.

We’ll have plenty more to announce over the next two months, so stay tuned. TC Sessions: Space 2020 blasts off on December 16-17. Don’t wait, buy your $50 student pass today and boldly go!

Is your company interested in sponsoring TC Sessions: Space 2020? Click here to talk with us about available opportunities.

Powered by WPeMatico

{kind=link}