Startup company

Auto Added by WPeMatico

Auto Added by WPeMatico

Let’s start this week’s newsletter with some data. Nationally, startups pulled in $30.8 billion in the first quarter of 2019, up 22 percent year-on-year, according to Crunchbase’s latest deal round-up.

A closer look at the numbers shows a big drop in angel funding and a slight decrease in mega-rounds, or financings larger than $100 million. The number of mega-rounds fell to 57 deals in Q1 and deal value was down too. With that said, mega-rounds still accounted for $16.4 billion, making Q1 2019 the second-best quarter on record for mega-rounds.

The bottom line is these monstrous deals represented a big chunk (29 percent) of all the dollars invested in U.S. startups in Q1. As investors move downstream and startups opt to stay private longer and longer, we’ll continue to see a greater pick up in mega rounds.

Want more TechCrunch newsletters? Sign up here.

OK, on to other news…

Once trading after the pink confetti was swept up off the floor, analysts and investors had a different story to tell about one of the first unicorns to make its public debut. Lyft began the week struggling to hit its IPO price, closing several days under that $72, despite opening with a 20 percent pop at $86. What’s going on? People are shorting the Lyft stock, looking to profit off the company’s sinking value. Things are looking up though; on Friday as I typed this newsletter, Lyft was trading at about $74 per share.

.@Uber sent @Lyft a whole bunch of cakes on IPO day, how nice. pic.twitter.com/hbZC5HOxbL

— Kate Clark (@KateClarkTweets) April 5, 2019

In other IPO, or shall I say, direct listing news, Slack has reportedly chosen the NYSE for its upcoming exit. A quick reminder why Slack has opted to go public via direct listing: The company doesn’t need any IPO cash thanks to the hundreds of millions of dollars on its balance sheet, but its longtime employees and investors need the liquidity. A direct listing allows it to go public without listing any new shares, with no lockup period and no intermediary bankers. The process saves it some money and expedites the process. OK, that wasn’t as brief as I intended, moving on…

Saying goodbye to venture capital

In a story that sent the entirety of Silicon Valley into a frenzy, Forbes reported that Andreessen Horowitz was denouncing its status as a venture capital firm and would register all its employees as financial advisors. For those inclined, Crunchbase News’ Alex Wilhelm and I unpacked what this means in the latest episode of Equity; for those less inclined, here’s the TLDR: For a16z to have the freedom to make riskier bets, like buying public company stock or heaps of cryptocurrency, the title of financial advisor gives them that ability.

Femtech, defined as any software, diagnostics, products and services that leverage technology to improve women’s health, has attracted some $250 million in VC funding so far this year, according to PitchBook. That puts the sector on pace to secure nearly $1 billion in investment by year-end, greatly surpassing last year’s record of $650 million. For more historical context, startups in the space brought in only $62 million in 2012, $225 million in 2014 and $231 million in 2016.

Alternative financier Clearbanc says it will invest $1 billion in 2,000 e-commerce startups in 2019. Here’s the catch: Until the companies have paid back 106 percent of Clearbanc’s investment, Clearbanc takes a percentage of their revenues every month. Clearbanc’s goal is to help companies preserve equity, favoring a revenue share model rather than the traditional VC model, which eats equity in startups in exchange for capital. I spoke to Clearbanc co-founder Michele Romanow to learn more about Clearbanc’s attempt to disrupt venture capital.

TechCrunch’s Megan Rose Dickey authored the be-all-end-all story on the shared-electric-scooter business. Here’s a quick passage: “The startup ecosystem had become accustomed to the ethos of begging for forgiveness, rather than asking for permission. But that’s not the case with electric scooters. These companies have found their entire businesses to be contingent on the continued approval from individual cities all over the world. That inherently creates a number of potential conflicts.” Extra Crunch subscribers can read the full story here.

Plus, we dropped the Niantic EC-1, in which Greg Kumparak dives deep into the history of the maker Pokemon Go, contributor Sherwood Morrison looked at remote workers and nomads, who represent the next tech hub.

TechCrunch has confirmed that Airbnb has invested between $150 million to $200 million in Indian hotel startup Oyo. Airbnb confirmed the existence of the deal but not the exact amount. The home-sharing giant is continuing to widen its focus beyond “unconventional” hotels as it prepares to begin selling pubic market investors on its long-term vision. Remember, this deal comes right after its big acquisition of HotelTonight.

WeWork acquired Managed by Q this week, a VC-backed startup that helps office managers and other decision-makers handle supply stocking, cleaning, IT support and other non-work related tasks in the office by simply using the Managed by Q dashboard. The company was most recently valued at $250 million, having raised a total of $128.25 million from investors such as GV, RRE and Kapor Capital.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about the future of a16z, Jumia’s IPO, the Midas list and more of this week’s headlines.

Powered by WPeMatico

Microsoft today announced a major expansion of its Azure IP Advantage program, which provides its Azure users with protection against patent trolls. This program now also provides customers who are building IoT solutions that connect to Azure with access to 10,000 patents to defend themselves against intellectual property lawsuits.

What’s maybe most interesting here, though, is that Microsoft is also donating 500 patents to startups in the LOT Network. This organization, which counts companies like Amazon, Facebook, Google, Microsoft, Netflix, SAP, Epic Games, Ford, GM, Lyft and Uber among its close to 400 members, is designed to protect companies against patent trolls by giving them access to a wide library of patents from its member companies and other sources.

“The LOT Network is really committed to helping address the proliferation of intellectual property lawsuits, especially ones that are brought by non-practicing entities, or so-called trolls,” Microsoft CVP and Deputy General Counsel Erich Andersen told me.

This new program goes well beyond basic protection from patent trolls, though. Qualified startups who join the LOT Network can acquire Microsoft patents as part of their free membership and as Andersen stressed, the startups will own them outright. The LOT network will be able to provide its startup members with up to three patents from this collection.

There’s one additional requirement here, though: To qualify for getting the patents, these startups also have to meet a $1,000 per month Azure spend. As Andersen told me, though, they don’t have to make any kind of forward pledge. The company will simply look at a startup’s last three monthly Azure bills.

“We want to help the LOT Network grow its network of startups,” Andersen said. “To provide an incentive, we are going to provide these patents to them.” He noted that startups are obviously interested in getting access to patents as a foundation of their companies, but also to raise capital and to defend themselves against trolls.

The patents we’re talking about here cover a wide range of technologies as well as geographies. Andersen noted that we’re talking about U.S. patents as well as European and Chinese patents, for example.

“The idea is that these startups come from a diverse set of industry sectors,” he said. “The hope we have is that when they approach LOT, they’ll find patents among those 500 that are going to be interesting to basically almost any company that might want a foundational set of patents for their business.”

As for the extended Azure IP Advantage program, it’s worth noting that every Azure customer who spends more than $1,000 per month over the past three months and hasn’t filed a patent infringement lawsuit against another Azure customer in the last two years can automatically pick one of the patents in the program’s portfolio to protect itself against frivolous patent lawsuits from trolls (and that’s a different library of patents from the one Microsoft is donating to the LOT Network as part of the startup program).

As Andersen noted, the team looked at how it could enhance the IP program by focusing on a number of specific areas. Microsoft is obviously investing a lot into IoT, so extending the program to this area makes sense. “What we’re basically saying is that if the customer is using IoT technology — regardless of whether it’s Microsoft technology or not — and it’s connected to Azure, then we’re going to provide this patent pick right to help customers defend themselves against patent suits,” Andersen said.

In addition, for those who do choose to use Microsoft IoT technology across the board, Microsoft will provide indemnification, too.

Patent trolls have lately started acquiring IoT patents, so chances are they are getting ready to make use of them and that we’ll see quite a bit of patent litigation in this space in the future. “The early signs we’re seeing indicate that this is something that customers are going to care about in the future,” said Andersen.

Powered by WPeMatico

As I’m sure everyone reading this knows, female-founded businesses receive just over 2 percent of venture capital on an annual basis. Most of those checks are written to early-stage startups. It’s extremely difficult for female founders to garner late-stage support, let alone cash $100 million checks.

Maybe that’s finally changing. This week, not one but two female-founded and led companies, Glossier and Rent The Runway, raised nine-figure rounds and cemented their status as unicorn companies. According to PitchBook data from 2018, there are only about 15 unicorn startups with female founders. Though I’m sure that number has increased in the last year, you get the point: There are hundreds of privately held billion-dollar companies and shockingly few of those have women founders (even fewer have female CEOs)…

Moving on…

I spent a good part of the week at San Francisco’s Pier 48 in a room full of vest-wearing investors. We listened to some 200 YC companies make their 120-second pitch and though it was a bit of a whirlwind, there were definitely some standouts. ICYMI: We wrote about each and every company that pitched on day 1 and day 2. If you’re looking for the inside scoop on the companies that forwent demo day and raised rounds, or were acquired, before hitting the stage, we’ve got that too.

Lyft: This week, Lyft set the terms for its highly-anticipated initial public offering, expected to be completed next week. The company will charge between $62 and $68 per share, raising more than $2 billion at a valuation of ~$23 billion. We previously reported its initial market cap would be around $18.5 billion, but that was before we knew that Lyft’s IPO was already oversubscribed. Here’s a little more background on the Lyft IPO for those interested.

Uber: The global ride-hailing business flew a little more under the radar this week than last week, but still managed to grab a few headlines. The company has decided to sell its stock on the New York Stock Exchange, which is the least surprising IPO development of 2019, considering its key U.S. competitor, Lyft, has been working with the Nasdaq on its IPO. Uber is expected to unveil its S-1 in April.

Ben Silbermann, co-founder and CEO of Pinterest, at TechCrunch Disrupt SF 2017.

Pinterest: Pinterest, the nearly decade-old visual search engine, unveiled its S-1 on Friday, one of the final steps ahead of its NYSE IPO, expected in April. The $12.3 billion company, which will trade under the ticker symbol “PINS,” posted revenue of $755.9 million in the year ending December 31, 2018, up from $472.8 million in 2017. It has roughly doubled its monthly active user count since early 2016, hitting 265 million last year. The company’s net loss, meanwhile, shrank to $62.9 million in 2018 from $130 million in 2017.

Zoom: Not necessarily the buzziest of companies, but its S-1 filing, published Friday, stands out for one important reason: Zoom is profitable! I know, what insanity! Anyway, the startup is going public on the Nasdaq as soon as next month after raising about $150 million in venture capital funding. The full deets are here.

General Catalyst, a well-known venture capital firm, is diving more seriously into the business of funding seed-stage business. The firm, which has investments in Warby Parker, Oscar and Stripe, announced earlier this week its plan to invest at least $25 million each year in nascent teams.

Earlier this week, Opendoor, the SoftBank -backed real estate startup, filed paperwork to raise even more money. According to TechCrunch’s Ingrid Lunden, the business is planning to raise up to $200 million at a valuation of roughly $3.7 billion. It’s possible this is a Series E extension; after all, the company raised its $400 million Series E only six months ago. Backers of OpenDoor include the usual suspects: Andreessen Horowitz, Coatue, General Atlantic, GV, Initialized Capital, Khosla Ventures, NEA and Norwest Venture Partners.

Startup capital

Backstage Capital founder and managing partner Arlan Hamilton, center.

Axios’ Dan Primack and Kia Kokalitcheva published a report this week revealing Backstage Capital hadn’t raised its debut fund in total. Backstage founder Arlan Hamilton was quick to point out that she had been honest about the challenges of fundraising during various speaking engagements, and even on the Gimlet “Startup” podcast, which featured her in its latest season. A Twitter debate ensued and later, Hamilton announced she was stepping down as CEO of Backstage Studio, the operations arm of the venture fund, to focus on raising capital and amplifying founders. TechCrunch’s Megan Rose Dickey has the full story.

This week, TechCrunch’s Connie Loizos revisited a long-held debate: Pro rata rights, or the right of an earlier investor in a company to maintain the percentage that he or she (or their venture firm) owns as that company matures and takes on more funding. Here’s why pro rata rights matter (at least, to VCs).

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about Glossier, Rent The Runway and YC Demo Days. Then, in a special Equity Shot, we unpack the numbers behind the Pinterest and Zoom IPO filings.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico

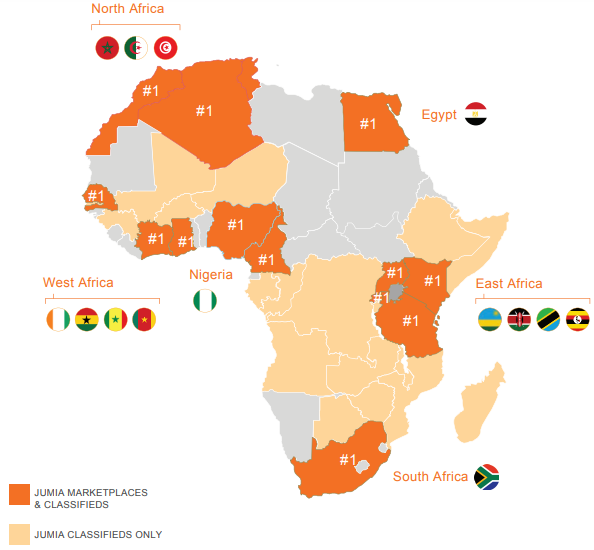

Pan-African e-commerce company Jumia filed for an IPO on the New York Stock Exchange today, per SEC documents and confirmation from CEO Sacha Poignonnec to TechCrunch.

The valuation, share price and timeline for public stock sales will be determined over the coming weeks for the Nigeria-headquartered company.

With a smooth filing process, Jumia will become the first African tech startup to list on a major global exchange.

Poignonnec would not pinpoint a date for the actual IPO, but noted the minimum SEC timeline for beginning sales activities (such as road shows) is 15 days after submitting first documents. Lead adviser on the listing is Morgan Stanley .

There have been numerous press reports on an anticipated Jumia IPO, but none of them confirmed by Jumia execs or an actual SEC, S-1 filing until today.

Jumia’s move to go public comes as several notable consumer digital sales startups have faltered in Nigeria — Africa’s most populous nation, largest economy and unofficial bellwether for e-commerce startup development on the continent. Konga.com, an early Jumia competitor in the race to wire African online retail, was sold in a distressed acquisition in 2018.

With the imminent IPO capital, Jumia will double down on its current strategy and regional focus.

“You’ll see in the prospectus that last year Jumia had 4 million consumers in countries that cover the vast majority of Africa. We’re really focused on growing our existing business, leadership position, number of sellers and consumer adoption in those markets,” Poignonnec said.

The pending IPO creates another milestone for Jumia. The venture became the first African startup unicorn in 2016, achieving a $1 billion valuation after a $326 funding round that included Goldman Sachs, AXA and MTN.

Founded in Lagos in 2012 with Rocket Internet backing, Jumia now operates multiple online verticals in 14 African countries, spanning Ghana, Kenya, Ivory Coast, Morocco and Egypt. Goods and services lines include Jumia Food (an online takeout service), Jumia Flights (for travel bookings) and Jumia Deals (for classifieds). Jumia processed more than 13 million packages in 2018, according to company data.

Starting in Nigeria, the company created many of the components for its digital sales operations. This includes its JumiaPay payment platform and a delivery service of trucks and motorbikes that have become ubiquitous with the Lagos landscape.

Starting in Nigeria, the company created many of the components for its digital sales operations. This includes its JumiaPay payment platform and a delivery service of trucks and motorbikes that have become ubiquitous with the Lagos landscape.

Jumia has also opened itself up to traders and SMEs by allowing local merchants to harness Jumia to sell online. “There are over 81,000 active sellers on our platform. There’s a dedicated sellers page where they can sign-up and have access to our payment and delivery network, data, and analytic services,” Jumia Nigeria CEO Juliet Anammah told TechCrunch.

The most popular goods on Jumia’s shopping mall site include smartphones (priced in the $80 to $100 range), washing machines, fashion items, women’s hair care products and 32-inch TVs, according to Anammah.

E-commerce ventures, particularly in Nigeria, have captured the attention of VC investors looking to tap into Africa’s growing consumer markets. McKinsey & Company projects consumer spending on the continent to reach $2.1 trillion by 2025, with African e-commerce accounting for up to 10 percent of retail sales.

Jumia has not yet turned a profit, but a snapshot of the company’s performance from shareholder Rocket Internet’s latest annual report shows an improving revenue profile. The company generated €93.8 million in revenues in 2017, up 11 percent from 2016, though its losses widened (with a negative EBITDA of €120 million). Rocket Internet is set to release full 2018 results (with updated Jumia figures) April 4, 2019.

Jumia’s move to list on the NYSE comes during an up and down period for B2C digital commerce in Nigeria. The distressed acquisition of Konga.com, backed by roughly $100 million in VC, created losses for investors, such as South African media, internet and investment company Naspers .

In late 2018, Nigerian online sales platform DealDey shut down. And TechCrunch reported this week that consumer-focused venture Gloo.ng has dropped B2C e-commerce altogether to pivot to e-procurement. The CEO cited better unit economics from B2B sales.

In late 2018, Nigerian online sales platform DealDey shut down. And TechCrunch reported this week that consumer-focused venture Gloo.ng has dropped B2C e-commerce altogether to pivot to e-procurement. The CEO cited better unit economics from B2B sales.

As demonstrated in other global startup markets, consumer-focused online retail can be a game of capital attrition to outpace competitors and reach critical mass before turning a profit. With its unicorn status and pending windfall from an NYSE listing, Jumia could be better positioned than any venture to win on e-commerce at scale in Africa.

Powered by WPeMatico

Venture investors are pouring billions of dollars into feeding their hunger for food and agriculture startups. Whether that trend line is due to enthusiasm for the sector or just broader heavy investing in the VC space is much less clear.

According to a recent report published by AgFunder – a VC and investing marketplace focused on the agriculture and food sectors – the “AgriFood” space is booming. Using data from Crunchbase and several other data partners, the organization published its “2018 AgriFood Tech Investing Report” this morning, finding that investment in AgriFood companies increased 43% year-over-year, reaching $16.9 billion in 2018.

AgFunder classifies AgriFood tech as “the small but growing segment of the startup and venture capital universe that’s aiming to improve or disrupt the global food and agriculture industry.” Their definition is intentionally broad, encompassing everything from crop and livestock biotech, property management systems, and payments, to biomaterials and meat alternatives, all the way up to tech platforms for restaurants, grocers, deliveries and at-home cooks.

While some of the AgriFood tech categories – such as delivery or restaurant software – have long been popular destinations for venture capital, we’re now seeing a more diverse array of startups innovating across the entire food supply chain. According to the report, expansion in AgriFood is fairly consistent across upstream (agricultural and farming) subsectors to downstream (more consumer-facing) subsectors, with each group growing roughly 44% and 42% year-over-year respectively.

The data also shows growth occurring across almost all deal stages. AgriFood saw huge increases in the average deal size and total investment for late-stage companies in particular, as venture-backed startups have grown to global scale. And penetrating and attracting capital from international markets seems more feasible than ever. AgriFood investing, which traditionally has been largely US-centric, is rapidly becoming a global phenomenon, with more than half of total funding – and some of the largest rounds – now coming from companies and investors outside the US.

Powered by WPeMatico

Three miles from Seattle’s South Lake Union neighborhood — better known as Amazonia to locals — sits Pioneer Square. The original heart of the city, the area has managed to hold on to its decades-old charm as other parts of town are besieged by Amazon-contracted architects.

On a mission to champion Seattle’s unique entrepreneurial DNA, startup studio Pioneer Square Labs has not only adopted the neighborhood’s moniker but established its fast-growing HQ at its center.

Pioneer Square Labs, or PSL, cropped up in 2015 to create, launch and fund technology companies headquartered in the Pacific Northwest. Operating under the startup studio model, PSL’s team of former founders and venture capitalists, including Rover and Mighty AI founder Greg Gottesman, collaborate to craft and incubate startup ideas, then recruit a founding CEO from their network of entrepreneurs to lead the business. The team uses an innovative method of rapidly ideating, testing and, if necessary, scrapping ideas, dubbed its “validation engine.”

The model differs from an accelerator or incubator. Y Combinator, for example, admits existing business into its months-long program, deploying its expertise and capital to bolster early-stage startups. PSL, on the other hand, creates startups and provides would-be founders with a derisked platform for company building.

“It’s a dream job,” PSL co-founder Greg Gottesman told TechCrunch. “If someone would say to you ‘hey, you can come into work every day, think about all the problems that are interesting to solve, all the tech that’s available and you have the resources to build companies,’ that’s just a dream come true … It’s just been a very fun ride.”

Xiao Wang, the CEO of Pioneer Square Labs spin-out Boundless, pitching at TechCrunch Disrupt SF 2017

The startup studio model is working for PSL. To date, it has raised $27.5 million in equity funding to build out its platform, in addition to an $80 million fundraise for its debut venture fund, which invests in PSL companies and other Pacific Northwest businesses. Of the 13 companies to emerge from PSL in the last three years, all have raised follow-on rounds from venture capital firms at an aggregate valuation of $200 million. According to PitchBook, PSL companies comprised 14.3 percent of all early-stage VC deals in Washington state in 2018.

Among PSL’s portfolio companies are cloud security compliance platform Shujinko, which closed a $2.8 million seed round from Unusual Ventures, Defy Ventures, Vulcan Capital and more last year. Plus, Boundless, a platform that facilitates the process of applying for immigrant status in the U.S., and Tally, a sports-prediction app spearheaded by football star Russell Wilson. Other recent spin-outs include Remarkably, a marketing and analytics software provider, and Attunely, a debt-collection-tech platform.

Pioneer Square Labs’ growing team of former operators, VCs, data scientists, engineers and more

Greg Gottesman, a former managing director at Seattle VC fund Madrona Venture Group, and the founder of its startup studio Madrona Venture Labs, leads PSL alongside a team of seasoned Pacific Northwest investors and entrepreneurs.

Rounding out PSL’s team of managing directors is Julie Sandler, a former investor at Madrona; Geoff Entress, a former venture partner with Voyager Capital and Madrona; Mike Galgon, the founder of the Microsoft-acquired digital agency aQuantive; and T.A. McCann, a serial entrepreneur behind Google-acquired Senosis and BlackBerry-acquired Gist. Ben Gilbert, who runs product at PSL, is another Madrona alum.

After nearly two decades investing in early-stage startups at Madrona, Gottesman made a peaceful exit with ambitions to launch a scalable startup studio independent of any existing VC firm. Madrona, alongside an additional 13 venture firms and Seattle angel investors, like Jeff Bezos and Zillow -founder Rich Barton, bolstered PSL with seed capital right off the bat.

Pioneer Square Labs’ network of entrepreneurs

To differentiate itself from competing company builders and maintain a high level of efficiency, PSL uses a proprietary strategy of rapidly testing and validating business ideas dubbed its “validation engine.” Its special sauce, PSL leverages digital marketing to validate customer demand before they begin real work on any of their ideas.

Long-time marketer Peter Denton leads the effort. Denton, who joined PSL in early 2017, manages day-to-day market validation, growth strategies and market research for the firm’s portfolio companies.

“We joke in some ways [Denton] is the grim reaper,” PSL’s Ben Gilbert told TechCrunch. “He’s responsible for much more kills than anyone else.”

Among the validation engine’s strategies is to build a website for a “company” to test demand for a potential product. Denton and his team market the website to target customer segments through a variety of digital channels, then measure customer resonance with the messaging. They ask potential customers if they are interested in learning more about a new concept or product when it “becomes available” to help understand how much interest a potential business might have before PSL allocates additional time and resources to a project.

To date, PSL has killed more than 100 ideas.

“A lot of studios ultimately won’t be successful because they don’t kill things fast enough,” Gottesman explained. “We kill nine out of 10 of the companies we start. Most of our ideas don’t make it to the promised land.”

In a sense, they are catfishing potential customers, luring them in with a new idea that more than likely will never come to fruition. But the strategy saves PSL the heartache that comes with investing a lot of time into a business idea that never finds its market.

A glimpse of Seattle’s Pioneer Square neighborhood where Pioneer Square Labs is headquartered

In three years, PSL has spun-out 13 companies, ideas for six of which came from the PSL team and seven originated from founders in the PSL network. All of those companies have secured venture funding — $71 million in total for an aggregate valuation of $200 million.

“The most important lesson we learned is it’s all about the people and the talent,” Gottesman said. “If we have an A-plus idea and partner with a B team, the company isn’t going to be successful. On the other hand, if we partner with the best talent, we are likely to be successful even if we fail on other dimensions.”

PSL’s goal is to invigorate the Seattle tech ecosystem and given the aforementioned stats (PSL companies comprised 14.3 percent of all early-stage VC deals in Washington state in 2018) they are well on their way. In 2019, PSL hopes to spin out between six and nine additional businesses.

“We believe we are building the center for early-stage tech innovation in the Pacific Northwest,” PSL’s Julie Sandler told TechCrunch.

Seattle, home to two of the most valuable businesses in the world, has not created as many founders as anticipated. Amazon’s entrepreneurial culture has succeeded in keeping top talent from pursuing their own businesses. PSL’s derisked platform, the firm hopes, will entice those founders, like Boundless CEO Xiao Wang, a former senior product manager at Amazon.

“The studio model lends itself really well to people who are 99 percent there, thinking ‘damn, I want to start a company,’” Gilbert said. “These are people that are incredible entrepreneurs but if not for the studio as a catalyst, they may not have [left].”

Venture capital investment in Washington state is increasing year-over-year, reaching a high of nearly $3 billion in 2018 across roughly 400 deals, per PitchBook. The Seattle tech scene, given its proximity to tech heavyweights and a growing number of satellite engineering offices, only has room to grow.

“We do think Seattle is the most exciting market in the country because of the amount of technical talent you have,” Gottesman said. “You have to believe that if engineering is at the heart of these startups then Seattle will ultimately be a key city in the world in terms of creating great technology startups.”

“We think part of the issue is a lack of capital and a lack of help,” Gottesman added. “If we can provide a little bit of both of those things, we can really put Seattle where it deserves to be, should be and will be.”

Powered by WPeMatico

Unlike 2000 and 2008, everyone in the startup world is expecting a crash to come at any moment. But few are taking concrete steps to prepare for it.

If you’re running a venture-backed startup, you should probably get on that. First, go read RIP Good Times from Sequoia to get a sense for how bad it can get, quickly. Then take a look at the checklist below. You don’t need to build a bomb shelter, yet, but adopting a bit of the prepper mentality now will pay dividends down the road.

The first step in preparing for a coming downturn is making a plan for how you’d get to a point of sustainability. Many startups have been lulled into a false sense of confidence that profit is something they can figure out “later.” Keep in mind, it has to be done eventually and it’s easier to do when the broader economy isn’t crashing around you. There are two complicating factors to keep in mind.

In a downturn, business customers skip investing in capital equipment and new software. Likewise, consumer discretionary spending goes way down. The result is you’ll likely have less revenue than you do now. War-game a variety of scenarios — what you’d do if you lost 20 percent, 50 percent or 80 percent of your revenue, and what decisions would have to be taken to survive.

When a downturn comes, capital markets don’t soften, they seize. Depending on how bad a hypothetical financial crisis got, there’s a good chance that investors would close up their checkbooks and triage. If you aren’t one of your investor’s favorite portfolio companies, there’s a decent chance you may be left in the cold. Don’t even assume you’ll be able to close a down round. Fortunately, showing a plan with a clear path to profitability will allay investors concerns that you’ll need their capital indefinitely and make it more likely you’ll be able to raise.

Planning around these three realities — the need for profits, while experiencing dropping revenue, in a world where capital can’t be had at any valuation — is going to lead to unpleasant conclusions. A dramatically diminished business, major layoffs, and a decisive drop in morale are likely outcomes. Thankfully, you can take steps now to help soften the landing, or if you’re really successful, avoid it entirely.

Getting acquisition costs under control will help you in two ways. First, it’ll lower your burn rate. Chasing growth for growth’s sake is always a short-sighted decision, but especially during the late part of the business cycle. Avoid this even if you’re VC is encouraging it. Second, by carefully analyzing the inputs to your acquisition cost, it will force you to examine the dynamics of your business. It gives you an opportunity to decide if a poorly performing channel or lackluster sales reps are actually smart investments. Even cutting your payback period from 12 months to nine will provide an increased measure of visibility and control.

Instagram took over the web with a team of a dozen. Craigslist is a pillar of the internet with a staff of 40 employees. WhatsApp supported hundreds of millions of daily users with fewer than 50 people. Chances are you need fewer people than you think.

In his new book, Scott Belsky shares an algorithm he used building Behance into a $100M company — automate, automate, then hire. His point was that founders should encourage teams to push hard on improving processes and other labor-saving tools before adding more FTEs.

Don’t institute a hiring freeze or take other actions that might spook the staff, but do send the message that new hires should be the last resort, not the first response to a challenge.

Founders often try to change spending habits, and in turn culture, when it’s too late. Is there a fair bit of business class flying among the executive team? Do your employees stretch your free dinner policy by staying just past the dinner hour to take advantage of free food? At most tech ventures, everyone is truly an owner. Try to help the entire team to internalize that they are spending their own money.

The week the market drops 50 percent is not the week to start a M&A conversation. You should be getting to know the five most likely buyers of your company, now. Find out who the decision makers at each of the companies are and build relationships. Make it a point to catch up with these people at conferences and even consider sending them regular updates about your company’s progress (but not too much data). You’re not running a formal sales process, but helping build up the internal desire to buy your company if the opportunity presents itself. It may not be the exit of your dreams, but it’s nice to have options if you need them.

If you’re coming to a T-juncture regarding office space, you may want to prioritize price and lease flexibility over quality and location. I remember one of our offices at my start-up was a twelve month lease with 6 months free. The landlords were desperate, and so were we!

If you’re in the kind of business that will support annual contracts, figure out a way to offer them. Pre-sell credits to consumers at a discount. More fundamentally, think about how you might be able to adjust your business model so you can get paid before you deliver services. Plenty of viable businesses are asphyxiated by delays in accounts receivable, don’t allow your ambitions to be thwarted by accounting.

One lesson learned in the 2000 bubble was that startups that serve other startups tend to be hit hardest. It’s important to think about how a downturn will impact your customer base. If more than 30 percent of your revenue comes from one industry (perhaps start-ups!), or heaven help you, a single customer, start thinking about managing risk by diversifying your customer base.

Topping up your balance sheet at this point isn’t a bad idea, provided you have the discipline to treat it as a rainy day fund. Communicate this rationale to your investors. It’s also important to use this moment to reflect on valuation. An eye-popping valuation will feel good when you sign the term sheet, but it’s going to feel like a millstone if the economy turns, and the market for blue-chip tech stocks drops precipitously.

Many VCs discourage venture debt. They’ll say “if you need more money, we’ll backstop you.” The problem is when things ugly, they may not be there. Debt providers are a good way to extend the runway. The thing is that it’s best to raise debt capital when you don’t need it. Venture debt can add ⅓ to ½ of additional capital to some funding rounds with minimal dilution and relatively modest interest rates. Do note that when things get bad, some debt funds can get aggressive so do your homework before taking the notes.

It’s tough to predict the top of the market. CNN, Time, The Atlantic, The Wall Street Journal, and many others argued Facebook paying $1 billion for Instagram was a sure sign of a bubble — in 2012. Reputable commentators have claimed that we’re in a bubble every year since, see 2013, 2014, 2015, 2016, 2017, and 2018. Going into survival mode in any of those years would have been a serious mistake for most startups.

Still, we’re only two quarters away from marking the longest economic expansion in US history. The good times have got to end at some point. Venture capital is a hell of a drug and withdrawal can be painful. Keep in mind that there’s no correlation between how much a company raised and how well they did on the public markets. If you’re struggling to make your startup’s economics work, read up on dozens of “invisible unicorns” who show that you can get big without relying on outsized amounts of venture capital.

If your house is in order when the downturn hits, you may actually be able to grow through it. As unprepared competitors go out of business, you’ll find that talent is more plentiful and customer acquisition costs plummet. Some of the best companies have been founded and thrived in the worst of times — if you’re prepared.

Powered by WPeMatico

Young founders who want to start companies while still in school have an increasing number of resources to tap into that exist just for them. Students that want to learn how to build companies can apply to an increasing number of fast-track programs that allow them to gain valuable early stage operating experience. The energy around student entrepreneurship today is incredible. I’ve been immersed in this community as an investor and adviser for some time now, and to say the least, I’m continually blown away by what the next generation of innovators are dreaming up (from Analytical Space’s global data relay service for satellites to Brooklinen’s reinvention of the luxury bed).

Bill Gates in 1973

First, let’s look at student founders and why they’re important. Student entrepreneurs have long been an important foundation of the startup ecosystem. Many students wrestle with how best to learn while in school —some students learn best through lectures, while more entrepreneurial students like author Julian Docks find it best to leave the classroom altogether and build a business instead.

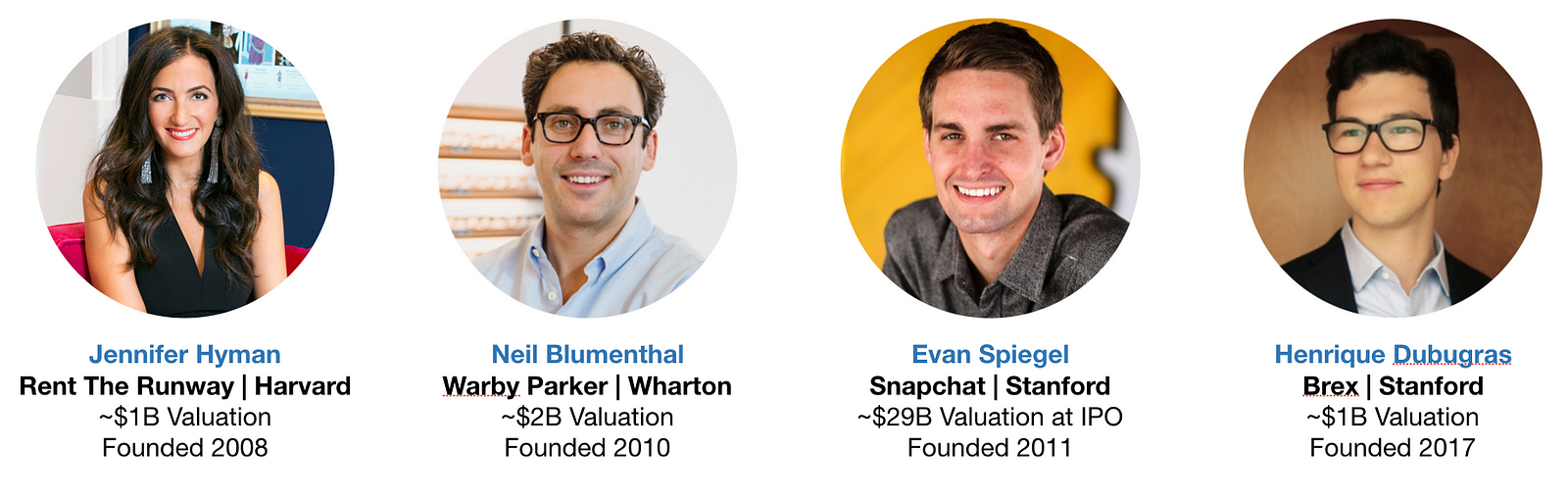

Indeed, some of our most iconic founders are Microsoft’s Bill Gates and Facebook’s Mark Zuckerberg, both student entrepreneurs who launched their startups at Harvard and then dropped out to build their companies into major tech giants. A sample of the current generation of marquee companies founded on college campuses include Snap at Stanford ($29B valuation at IPO), Warby Parker at Wharton (~$2B valuation), Rent The Runway at HBS (~$1B valuation), and Brex at Stanford (~$1B valuation).

Some of today’s most celebrated tech leaders built their first ventures while in school — even if some student startups fail, the critical first-time founder experience is an invaluable education in how to build great companies. Perhaps the best example of this that I could find is Drew Houston at Dropbox (~$9B valuation at IPO), who previously founded an edtech startup at MIT that, in his words, provided a: “great introduction to the wild world of starting companies.”

Student founders are everywhere, but the highest concentration of venture-backed student founders can be found at just 5 universities. Based on venture fund portfolio data from the last six years, Harvard, Stanford, MIT, UPenn, and UC Berkeley have produced the highest number of student-founded companies that went on to raise $1 million or more in seed capital. Some prospective students will even enroll in a university specifically for its reputation of churning out great entrepreneurs. This is not to say that great companies are not being built out of other universities, nor does it mean students can’t find resources outside a select number of schools. As you can see later in this essay, there are a number of new ways students all around the country can tap into the startup ecosystem. For further reading, PitchBook produces an excellent report each year that tracks where all entrepreneurs earned their undergraduate degrees.

Student founders have a number of new media resources to turn to. New email newsletters focused on student entrepreneurship like Justine and Olivia Moore’s Accelerated and Kyle Robertson’s StartU offer new channels for young founders to reach large audiences. Justine and Olivia, the minds behind Accelerated, have a lot of street cred— they launched Stanford’s on-campus incubator Cardinal Ventures before landing as investors at CRV.

StartU goes above and beyond to be a resource to founders they profile by helping to connect them with investors (they’re active at 12 universities), and run a podcast hosted by their Editor-in-Chief Johnny Hammond that is top notch. My bet is that traditional media will point a larger spotlight at student entrepreneurship going forward.

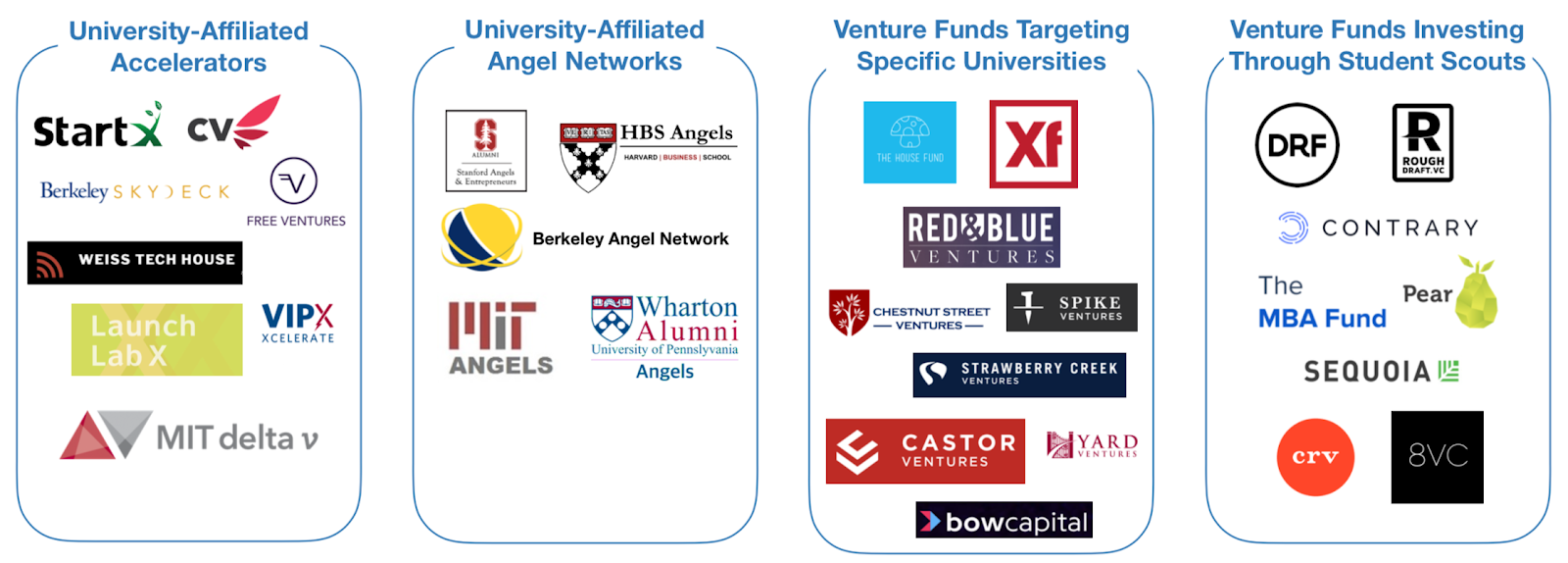

New pools of capital are also available that are specifically for student founders. There are four categories that I call special attention to:

While it is difficult to estimate exactly how much capital has been deployed by each, there is no denying that there has been an explosion in the number of programs that address the pre-seed phase. A sample of the programs available at the Top 5 universities listed above are in the graphic below — listing every resource at every university would be difficult as there are so many.

One alumni-centric fund to highlight is the Alumni Ventures Group, which pools LP capital from alumni at specific universities, then launches individual venture funds that invest in founders connected to those universities (e.g. students, alumni, professors, etc.). Through this model, they’ve deployed more than $200M per year! Another highlight has been student scout programs — which vary in the degree of autonomy and capital invested — but essentially empower students to identify and fund high-potential student-founded companies for their parent venture funds. On campuses with a large concentration of student founders, it is not uncommon to find student scouts from as many as 12 different venture funds actively sourcing deals (as is made clear from David Tao’s analysis at UC Berkeley).

Investment Team at Rough Draft Ventures

In my opinion, the two institutions that have the most expansive line of sight into the student entrepreneurship landscape are First Round’s Dorm Room Fund and General Catalyst’s Rough Draft Ventures. Since 2012, these two funds have operated a nationwide network of student scouts that have invested $20K — $25K checks into companies founded by student entrepreneurs at 40+ universities. “Scout” is a loose term and doesn’t do it justice — the student investors at these two funds are almost entirely autonomous, have built their own platform services to support portfolio companies, and have launched programs to incubate companies built by female founders and founders of color. Another student-run fund worth noting that has reach beyond a single region is Contrary Capital, which raised $2.2M last year. They do a particularly great job of reaching founders at a diverse set of schools — their network of student scouts are active at 45 universities and have spoken with 3,000 founders per year since getting started. Contrary is also testing out what they describe as a “YC for university-based founders”. In their first cohort, 100% of their companies raised a pre-seed round after Contrary’s demo day. Another even more recently launched organization is The MBA Fund, which caters to founders from the business schools at Harvard, Wharton, and Stanford. While super exciting, these two funds only launched very recently and manage portfolios that are not large enough for analysis just yet.

Over the last few months, I’ve collected and cross-referenced publicly available data from both Dorm Room Fund and Rough Draft Ventures to assess the state of student entrepreneurship in the United States. Companies were pulled from each fund’s portfolio page, then checked against Crunchbase for amount raised, accelerator participation, and other metrics. If you’d like to sift through the data yourself, feel free to ping me — my email can be found at the end of this article. To be clear, this does not represent the full scope of investment activity at either fund — many companies in the portfolios of both funds remain confidential and unlisted for good reasons (e.g. startups working in stealth). In fact, the In addition, data for early stage companies is notoriously variable in quality, even with Crunchbase. You should read these insights as directional only, given the debatable confidence interval. Still, the data is still interesting and give good indicators for the health of student entrepreneurship today.

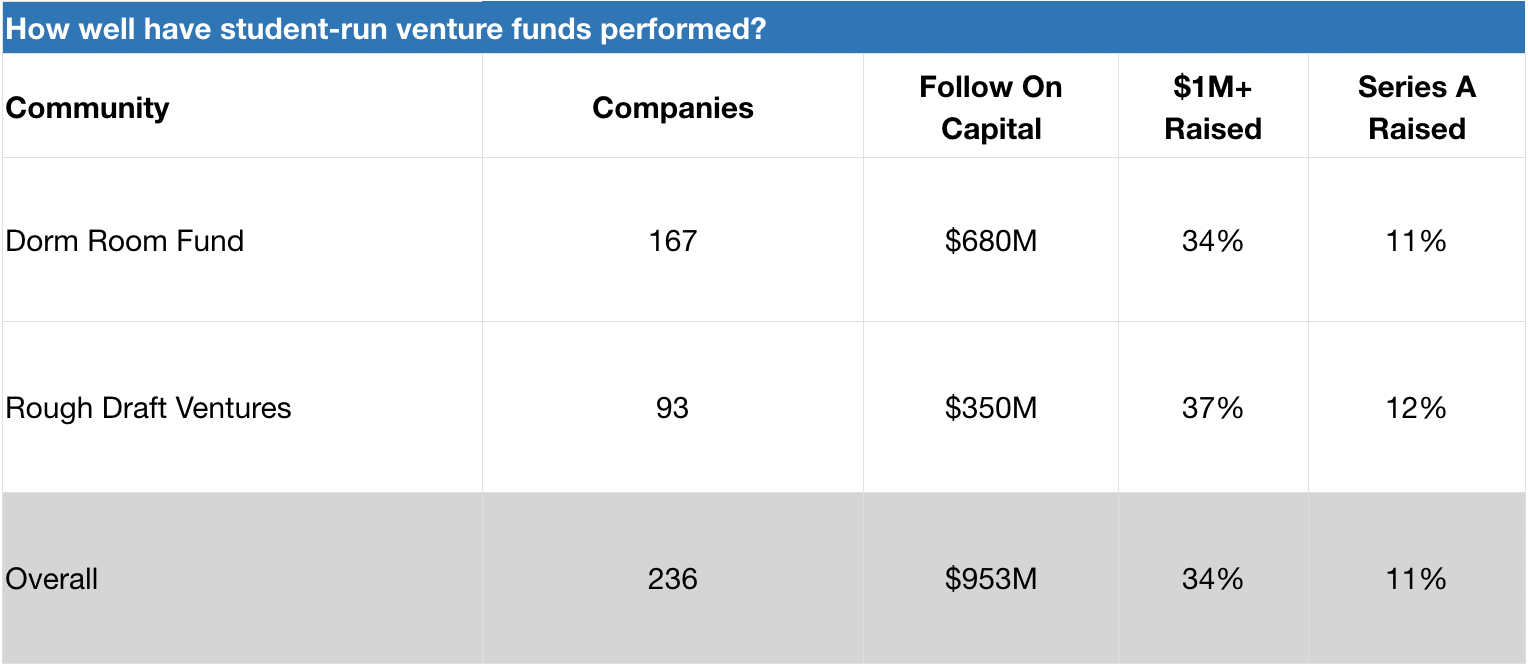

Dorm Room Fund and Rough Draft Ventures have invested in 230+ student-founded companies that have gone on to raise nearly $1 billion in follow on capital. These funds have invested in a diverse range of companies, from govtech (e.g. mark43, raised $77M+ and FiscalNote, raised $50M+) to space tech (e.g. Capella Space, raised ~$34M). Several portfolio companies have had successful exits, such as crypto startup Distributed Systems (acquired by Coinbase) and social networking startup tbh (acquired by Facebook). While it is too early to evaluate the success of these funds on a returns basis (both were launched just 6 years ago), we can get a sense of success by evaluating the rates by which portfolio companies raise additional capital. Taken together, 34% of DRF and RDV companies in our data set have raised $1 million or more in seed capital. For a rough comparison, CB Insights cites that 40% of YC companies and 48% of Techstars companies successfully raise follow on capital (defined as anything above $750K). Certainly within the ballpark!

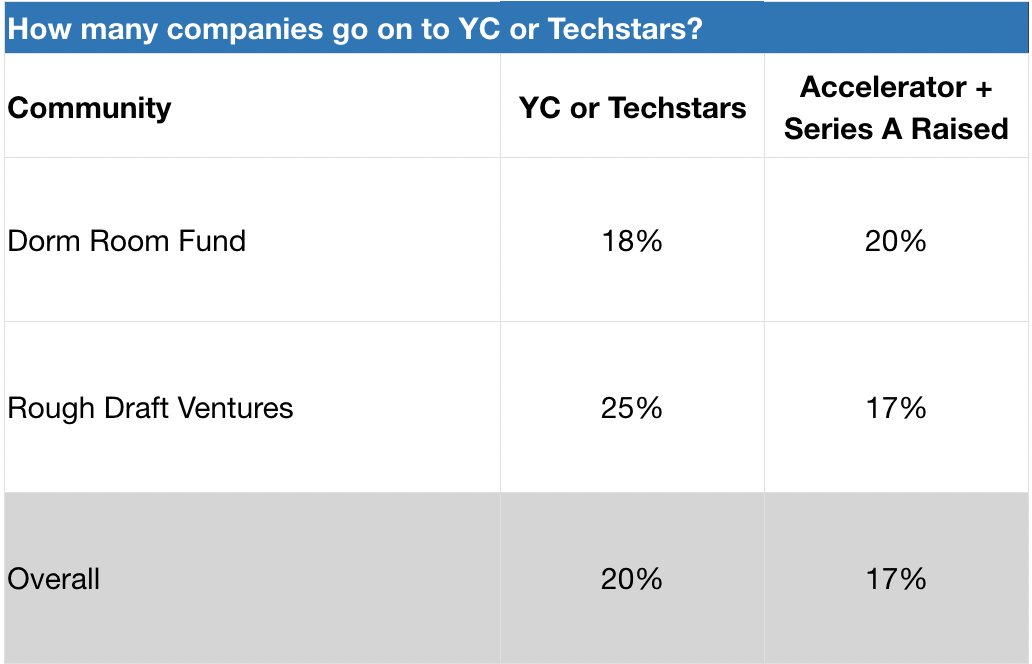

Dorm Room Fund and Rough Draft Ventures companies in our data set have an 11–12% rate of survivorship to Series A. As a benchmark, a previous partner at Y Combinator shared that 20% of their accelerator companies raise Series A capital (YC declined to share the official figure, but it’s likely a stat that is increasing given their new Series A support programs. For further reading, check out YC’s reflection on what they’ve learned about helping their companies raise Series A funding). In any case, DRF and RDV’s numbers should be taken with a grain of salt, as the average age of their portfolio companies is very low and raising Series A rounds generally takes time. Ultimately, it is clear that DRF and RDV are active in the earlier (and riskier) phases of the startup journey.

Dorm Room Fund and Rough Draft Ventures send 18–25% of their portfolio companies to Y Combinator or Techstars. Given YC’s 1.5% acceptance rate as reported in Fortune, this is quite significant! Internally, these two funds offer founders an opportunity to participate in mock interviews with YC and Techstars alumni, as well as tap into their communities for peer support (e.g. advice on pitch decks and application content). As a result, Dorm Room Fund and Rough Draft Ventures regularly send cohorts of founders to these prestigious accelerator programs. Based on our data set, 17–20% of DRF and RDV companies that attend one of these accelerators end up raising Series A venture financing.

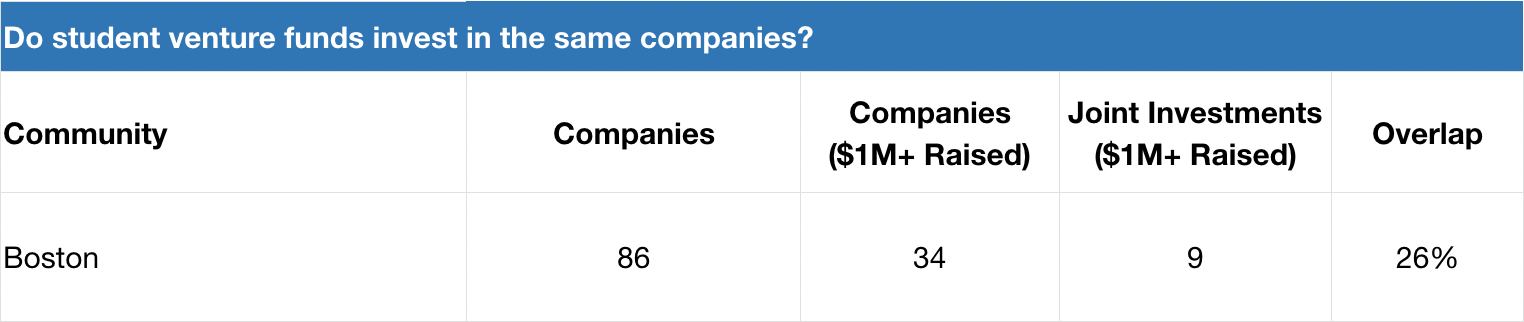

Dorm Room Fund and Rough Draft Ventures don’t invest in the same companies. When we take a deeper look at one specific ecosystem where these two funds have been equally active over the last several years — Boston — we actually see that the degree of investment overlap for companies that have raised $1M+ seed rounds sits at 26%. This suggests that these funds are either a) seeing different dealflow or b) have widely different investment decision-making.

Dorm Room Fund and Rough Draft Ventures should not just be measured by a returns-basis today, as it’s too early. I hypothesize that DRF and RDV are actually encouraging more entrepreneurial activity in the ecosystem (more students decide to start companies while in school) as well as improving long-term founder outcomes amongst students they touch (portfolio founders build bigger and more successful companies later in their careers). As more students start companies, there’s likely a positive feedback loop where there’s increasing peer pressure to start a company or lean on friends for founder support (e.g. feedback, advice, etc).Both of these subjects warrant additional study, but it’s likely too early to conduct these analyses today.

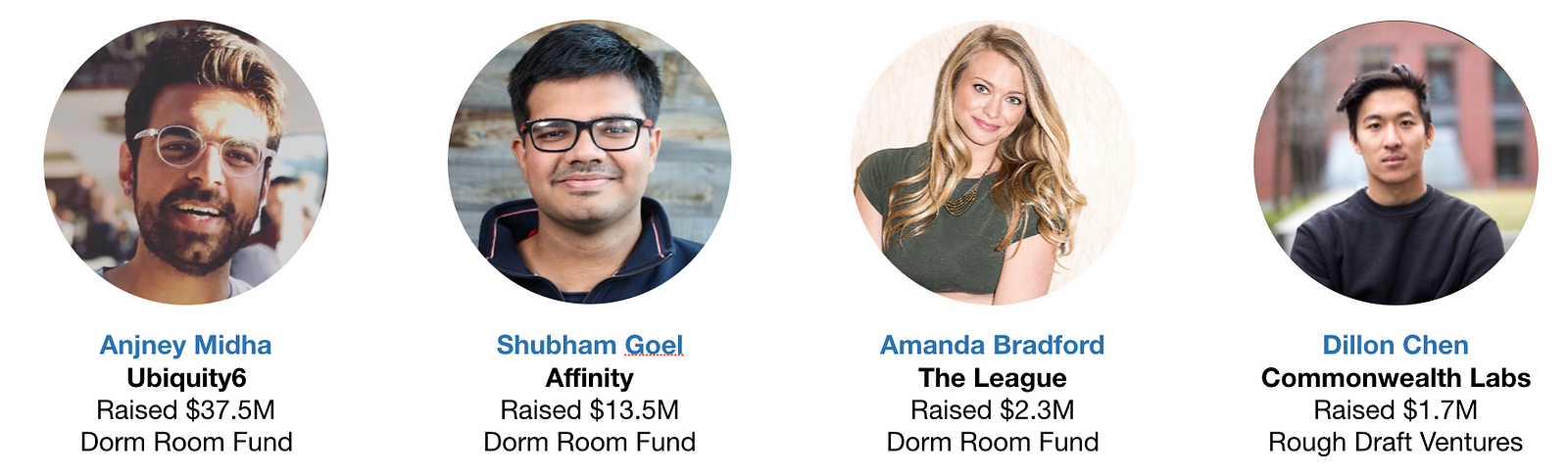

Dorm Room Fund and Rough Draft Ventures have impressive alumni that you will want to track. 1 in 4 alumni partners are founders, and 29% of these founder alumni have raised $1M+ seed rounds for their companies. These include Anjney Midha’s augmented reality startup Ubiquity6 (raised $37M+), Shubham Goel’s investor-focused CRM startup Affinity (raised $13M+), Bruno Faviero’s AI security software startup Synapse (raised $6M+), Amanda Bradford’s dating app The League (raised $2M+), and Dillon Chen’s blockchain startup Commonwealth Labs (raised $1.7M). It makes sense to me that alumni from these communities that decide to start companies have an advantage over their peers — they know what good companies look like and they can tap into powerful networks of young talent / experienced investors.

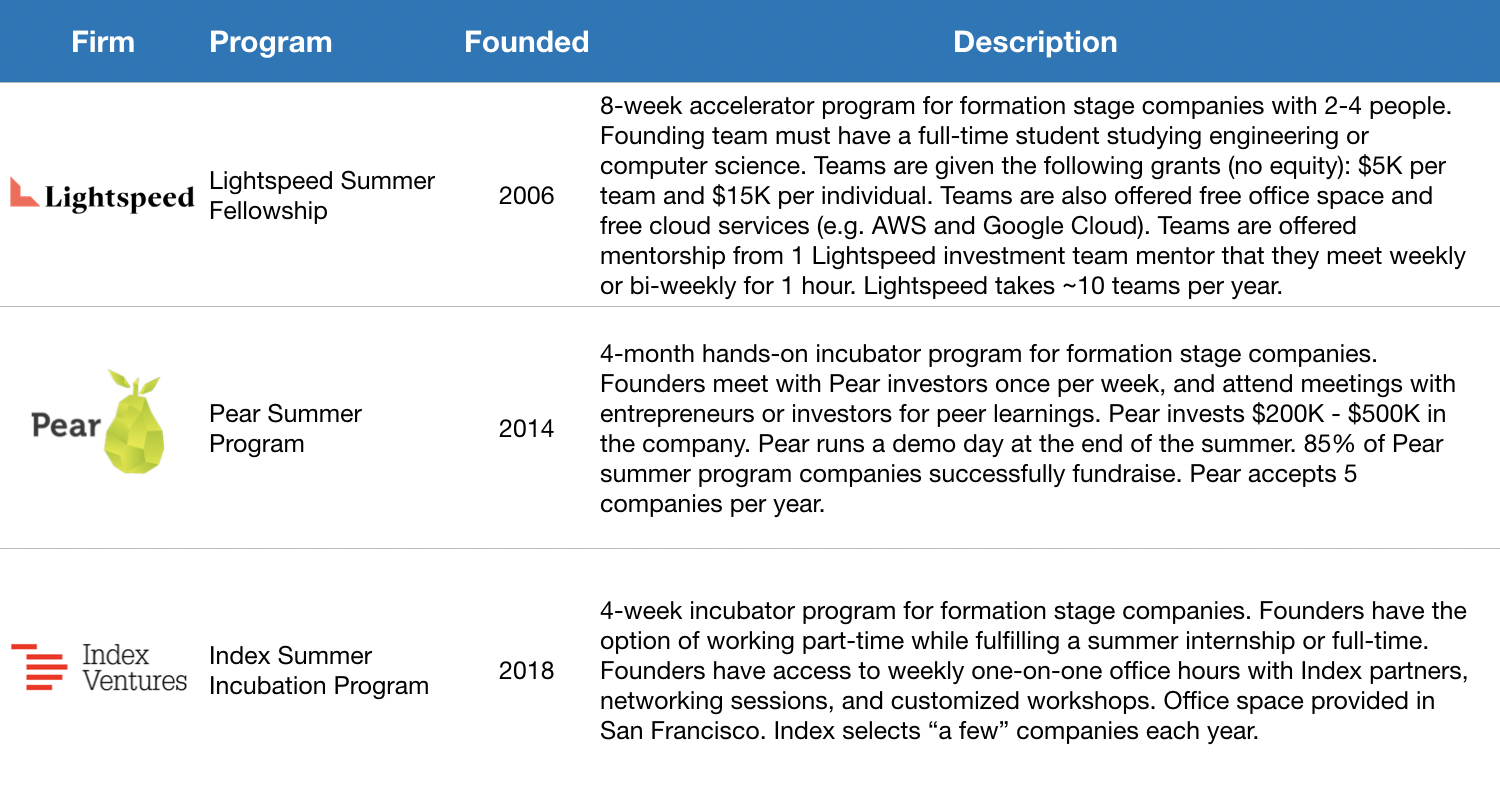

Beyond Dorm Room Fund and Rough Draft Ventures, some venture capital firms focus on incubation for student-founded startups. Credit should first be given to Lightspeed for producing the amazing Summer Fellows bootcamp experience for promising student founders — after all, Pinterest was built there! Jeremy Liew gives a good overview of the program through his sit-down interview with Afterbox’s Zack Banack. Based on a study they conducted last year, 40% of Lightspeed Summer Fellows alumni are currently active founders. Pear Ventures also has an impressive summer incubator program where 85% of its companies successfully complete a fundraise. Index Ventures is the latest to build an incubator program for student founders, and even accepts founders who want to work on an idea part-time while completing a summer internship.

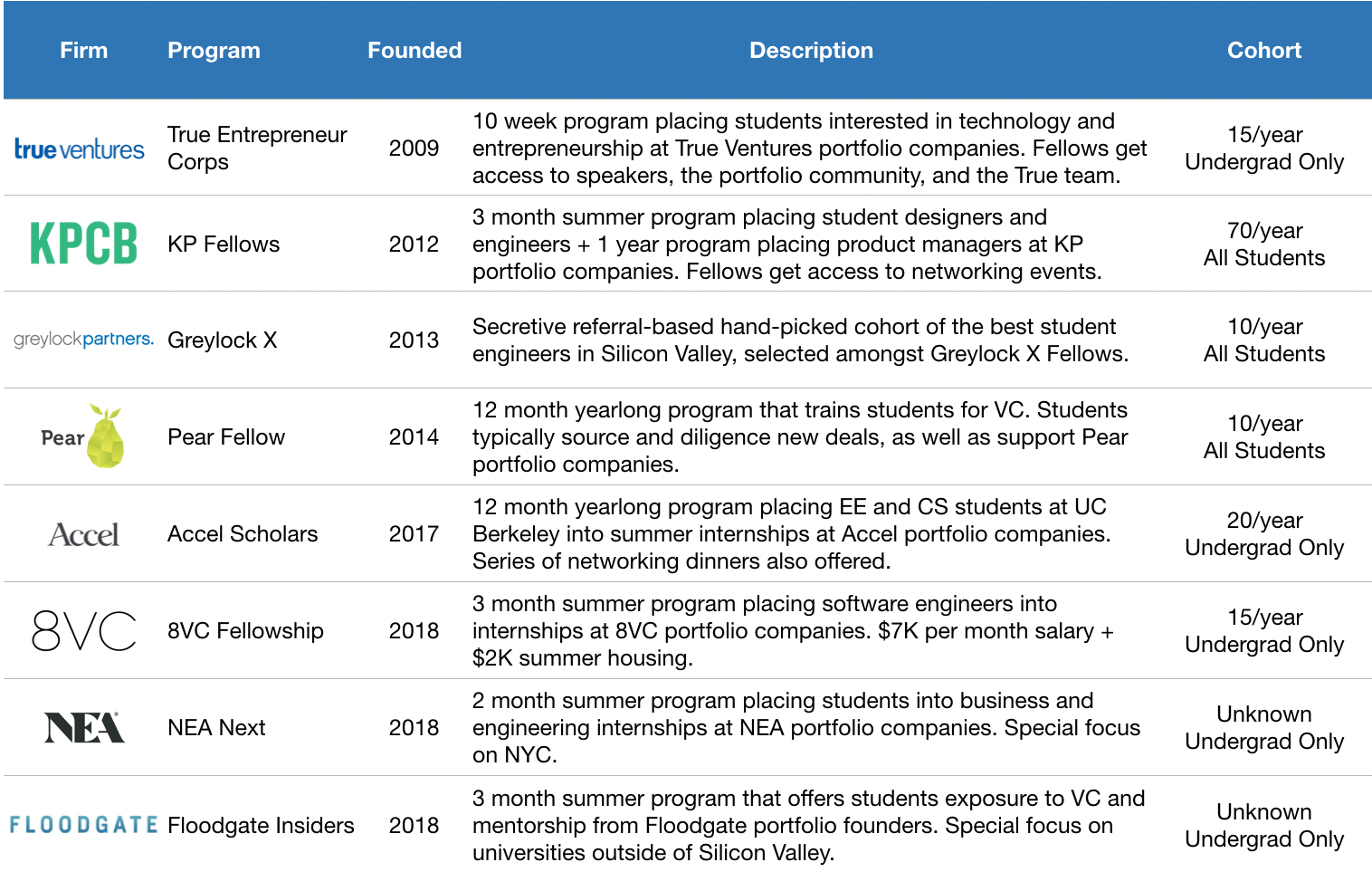

Let’s now look at students who want to join a startup before founding one. Venture funds have historically looked to tap students for talent, and are expanding the engagement lifecycle. The longest running programs include Kleiner Perkins’ class=”m_1196721721246259147gmail-markup–strong m_1196721721246259147gmail-markup–p-strong”> KP Fellows and True Ventures’ TEC Fellows, which focus on placing the next generation’s most promising product managers, engineers, and designers into the portfolio companies of their parent venture funds.

There’s also the secretive Greylock X, a referral-based hand-picked group of the best student engineers in Silicon Valley (among their impressive alumni are founders like Yasyf Mohamedali and Joe Kahn, the folks behind First Round-backed Karuna Health). As these programs have matured, these firms have recognized the long-run value of engaging the alumni of their programs.

More and more alumni are “coming back” to the parent funds as entrepreneurs, like KP Fellow Dylan Field of Figma (and is also hosting a KP Fellow, closing a full circle loop!). Based on their latest data, 10% of KP Fellows alumni are founders — that’s a lot given the fact that their community has grown to 500! This helps explain why Kleiner Perkins has created a structured path to receive $100K in seed funding to companies founded by KP Fellow alumni. It looks like venture funds are beginning to invest in student programs as part of their larger platform strategy, which can have a real impact over the long term (for further reading, see this analysis of platform strategy outcomes by USV’s Bethany Crystal).

KP Fellows in San Francisco

Venture funds are doubling down on student talent engagement — in just the last 18 months, 4 funds have launched student programs. It’s encouraging to see new funds follow in the footsteps of First Round, General Catalyst, Kleiner Perkins, Greylock, and Lightspeed. In 2017, Accel launched their Accel Scholars program to engage top talent at UC Berkeley and Stanford. In 2018, we saw 8VC Fellows, NEA Next, and Floodgate Insiders all launch, targeting elite universities outside of Silicon Valley. Y Combinator implemented Early Decision, which allows student founders to apply one batch early to help with academic scheduling. Most recently, at the start of 2019, First Round launched the Graduate Fund (staffed by Dorm Room Fund alumni) to invest in founders who are recent graduates or young alumni.

Given more time, I’d love to study the rates by which student founders start another company following investments from student scout funds, as well as whether or not they’re more successful in those ventures. In any case, this is an escalation in the number of venture funds that have started to get serious about engaging students — both for talent and dealflow.

Student entrepreneurship 2.0 is here. There are more structured paths to success for students interested in starting or joining a startup. Founders have more opportunities to garner press, seek advice, raise capital, and more. Venture funds are increasingly leveraging students to help improve the three F’s — finding, funding, and fixing. In my personal view, I believe it is becoming more and more important for venture funds to gain mindshare amongst the next generation of founders and operators early, while still in school.

I can’t wait to see what’s next for student entrepreneurship in 2019. If you’re interested in digging in deeper (I’m human — I’m sure I haven’t covered everything related to student entrepreneurship here) or learning more about how you can start or join a startup while still in school, shoot me a note at sxu@dormroomfund.com. A massive thanks to Phin Barnes, Rei Wang, Chauncey Hamilton, Peter Boyce, Natalie Bartlett, Denali Tietjen, Eric Tarczynski, Will Robbins, Jasmine Kriston, Alicia Lau, Johnny Hammond, Bruno Faviero, Athena Kan, Shohini Gupta, Alex Immerman, Albert Dong, Phillip Hua-Bon-Hoa, and Trevor Sookraj for your incredible encouragement, support, and insight during the writing of this essay.

Powered by WPeMatico

Are more Theranos -style scandals looming for investors in healthcare startups?

A team of researchers associated with the Meta-Research Innovation Center at Stanford thinks so. They’ve published a paper warning investors in life sciences startups that a systemic lack of transparency exists in their portfolio companies — creating the possibility for more multi-billion-dollar implosions and scandals like the one that toppled Theranos and its charismatic founder, Elizabeth Holmes.

Indeed, one of the study’s authors, Dr. John Ioannidis, the co-director of the Meta-Research Innovation Center at Stanford and director of the University’s PhD program in Epidemiology and Clinical Research, was among the first people to identify the risks associated with Theranos and its “stealth research.”

Now Dr. Ioannidis and his co-authors, Ioana A. Cristea and Eli M. Cahan, have published a study surveying the publicly available research from the largest privately held companies in the healthcare space, and found them lacking.

Most of the highest-valued startups in healthcare have not published any significant scientific literature, the study found. Nearly half of the publications from companies worth more than $1 billion came from only two startups — 23andMe and Adaptive Biotechnologies, according to the paper.

“Many years ago I was the first person to say that Theranos had a problem,” says Ioannidis. “The problem that I had then was that Theranos did not have any peer-reviewed evidence to show.”

In an interview and in their paper, Ioannidis and Cahan warn that investors have overlooked systemic problems created by the lack of transparency among healthcare startups.

They write:

It would be tempting to dismiss the Theranos case as just one rotten apple. However, we worry that the focus on fraud puts aside a more fundamental concern. Fraud is making waves in the news, but stealth research may have a more detrimental impact.

According to the study’s findings, more than half of the healthcare startups that are worth more than $1 billion have published no highly cited papers at all. For companies that were acquired or are publicly traded that number is around 40 percent.

In all, healthcare startups that are currently valued at more than $1 billion published 425 Pubmed papers. And of those papers only 34 (8 percent, including two reviews) were highly cited. For companies with valuations of more than $1 billion that had been acquired or are publicly traded on stock exchanges, the researchers counted 413 papers, of which 47 (11 percent, including nine reviews) were highly cited.

Digging deeper into some of the companies that had high valuations but little or no published research revealed scores of operational and technological issues for the researchers.

For instance, StemCentrx, which was bought for $10.2 billion in 2016 by AbbVie, had published 16 papers — and only one highly cited paper. Since the acquisition, the Food and Drug Administration had imposed a delay on the readout of the company’s phase II trial for its Rova T targeted antibody drug for cancer treatment. In December, a Phase III trial for Rova T as a second-line treatment for patients with advanced small cell lung cancer was halted because the treatment wasn’t working, according to a report in Targeted Oncology.

Acerta Pharma, another healthcare-focused startup focused on cancer treatments, was bought by AstraZeneca for $7.3 billion. That company published nine articles and had one highly cited paper for a very early study of a potential treatment for relapsed chronic lymphocytic leukemia. Acerta received accelerated approval for a drug called acalabrutinib, which treats a rare form of lymphoma called mantle cell lymphoma. Two years ago, AstraZeneca had to retract data and admit that Acerta falsified preclinical data for its drug.

Then there’s Intarcia, the developer of a device for diabetes treatment that’s worth $5.5 billion. That company had its device rejected by the FDA and was forced to lay off staff and halt a couple of later-stage trials. It had only published six papers — none of them very highly cited.

Ultimately, the researchers concluded that highly valued healthcare startups don’t contribute to published research and that the valuation of these companies by investors is divorced from any externally validated data.

For the researchers (and for investors) this should present a problem.

“Many unicorns may be overvalued [21] and subject to unrealistic scientific expectations,” the study’s authors write. And they reject the argument that simply applying for — and receiving — patents is enough to prove that a technology in the healthcare space has been thoroughly vetted. “[Patents] do not offer the same level of documentation as peer-reviewed articles. For example, Theranos had over 100 patents [1], but these were unable to supplant the vacuum in their evidence,” the researchers wrote.

Even if companies want to protect their technology, there are still ways for them to be more transparent about the results or benefits of their technology. The authors acknowledge that publishing isn’t the primary mission of startups. They can, however publish a few high-value articles, secure their technology through patents and then work with researchers, universities or hospitals to validate the technology and have those organizations publish results of the tests, the authors argue.

As the authors conclude:

Start-ups are key purveyors of innovation and disruption. Consequently, holding them to a minimal standard of evaluation from the scientific community is crucial. Participation in peer review, with all its limitations, is the best way we have to uphold this standard. We are not arguing that start-ups should divert excessive resources to having peer-reviewed papers. However, when their products are destined to affect patient health, they should neither be solely doing marketing. Confidential data sharing with potential investors or regulators cannot replace more open scrutiny by the scientific community.

Powered by WPeMatico

We’re three weeks into January. We’ve recovered from our CES hangover and, hopefully, from the CES flu. We’ve started writing the correct year, 2019, not 2018.

Venture capitalists have gone full steam ahead with fundraising efforts, several startups have closed multi-hundred million dollar rounds, a virtual influencer raised equity funding and yet, all anyone wants to talk about is Slack’s new logo… As part of its public listing prep, Slack announced some changes to its branding this week, including a vaguely different looking logo. Considering the flack the $7 billion startup received instantaneously and accusations that the negative space in the logo resembled a swastika — Slack would’ve been better off leaving its original logo alone; alas…

On to more important matters.

Rubrik more than doubled its valuation

The data management startup raised a $261 million Series E funding at a $3.3 billion valuation, an increase from the $1.3 billion valuation it garnered with a previous round. In true unicorn form, Rubrik’s CEO told TechCrunch’s Ingrid Lunden it’s intentionally unprofitable: “Our goal is to build a long-term, iconic company, and so we want to become profitable but not at the cost of growth,” he said. “We are leading this market transformation while it continues to grow.”

Deal of the week: Knock gets $400M to take on Opendoor

Will 2019 be a banner year for real estate tech investment? As $4.65 billion was funneled into the space in 2018 across more than 350 deals and with high-flying startups attracting investors (Compass, Opendoor, Knock), the excitement is poised to continue. This week, Knock brought in $400 million at an undisclosed valuation to accelerate its national expansion. “We are trying to make it as easy to trade in your house as it is to trade in your car,” Knock CEO Sean Black told me.

While we’re on the subject of VCs’ favorite industries, TechCrunch cybersecurity reporter Zack Whittaker highlights some new data on venture investment in the industry. Strategic Cyber Ventures says more than $5.3 billion was funneled into companies focused on protecting networks, systems and data across the world, despite fewer deals done during the year. We can thank Tanium, CrowdStrike and Anchorfree’s massive deals for a good chunk of that activity.

Send me tips, suggestions and more to kate.clark@techcrunch.com or @KateClarkTweets.

I would be remiss not to highlight a slew of venture firms that made public their intent to raise new funds this week. Peter Thiel’s Valar Ventures filed to raise $350 million across two new funds and Redpoint Ventures set a $400 million target for two new China-focused funds. Meanwhile, Resolute Ventures closed on $75 million for its fourth early-stage fund, BlueRun Ventures nabbed $130 million for its sixth effort, Maverick Ventures announced a $382 million evergreen fund, First Round Capital introduced a new pre-seed fund that will target recent graduates, Techstars decided to double down on its corporate connections with the launch of a new venture studio and, last but not least, Lance Armstrong wrote his very first check as a VC out of his new fund, Next Ventures.

More money goes toward scooters

In case you were concerned there wasn’t enough VC investment in electric scooter startups, worry no more! Flash, a Berlin-based micro-mobility company, emerged from stealth this week with a whopping €55 million in Series A funding. Flash is already operating in Switzerland and Portugal, with plans to launch into France, Italy and Spain in 2019. Bird and Lime are in the process of raising $700 million between them, too, indicating the scooter funding extravaganza of 2018 will extend into 2019 — oh boy!

TechCrunch’s Josh Constine introduced readers to Squad this week, a screensharing app for social phone addicts.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase editor-in-chief Alex Wilhelm and I marveled at the dollars going into scooter startups, discussed Slack’s upcoming direct listing and debated how the government shutdown might impact the IPO market.

Powered by WPeMatico