Starling

Auto Added by WPeMatico

Auto Added by WPeMatico

The global venture capital bet on neobanks is massive. London-based Starling Bank has raised more than $900 million, per Crunchbase. The same data source indicates that Chime has raised $1.5 billion. Monzo has raised nearly $650 million. And the list goes on: E-commerce-focused neobank Juni raised $21.5 million last month. Novo, an SMB-focused neobank, raised $41 million in June. Nubank has raised $2.3 billion. And FairMoney has locked down more than $50 million.

On and on and on.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

But despite our general inclination to lump banking-focused fintech providers that serve consumers, business customers or both into a single bucket, there’s wide divergence in how the various neobank players are performing in the market.

Back in August 2020, The Exchange noted that many neobanks were racking up steep losses. Our read at the time was that the capital being poured into the fintech category was being invested aggressively in the name of growth. Based on recent results, that view is holding up.

But not all neobanks are the unprofitable enterprises that they once were. Chime indicated in September 2020 that it generates positive, unadjusted EBITDA. That’s a stricter profit metric than the one that Lyft used recently to claim its ascendance into the realm of profitable companies; Lyft posted positive adjusted EBITDA in its most recent quarter, but burned cash to fund its operations and posted a wide net loss in the period.

But not all neobanks are the unprofitable enterprises that they once were. Chime indicated in September 2020 that it generates positive, unadjusted EBITDA. That’s a stricter profit metric than the one that Lyft used recently to claim its ascendance into the realm of profitable companies; Lyft posted positive adjusted EBITDA in its most recent quarter, but burned cash to fund its operations and posted a wide net loss in the period.

And Starling Bank reached what it describes as profitable territory in October 2020. Things have changed since our first look into neobank results.

The trend of positive neobank news continued this June, when Revolut reported its recent financial performance. The company did post rather negative aggregate results for the 2020 period. But when we drilled down into its quarterly results, we saw the picture of a fintech company scaling its gross margins and revenues while nearly reaching adjusted net income neutrality by Q4 2020. We were impressed.

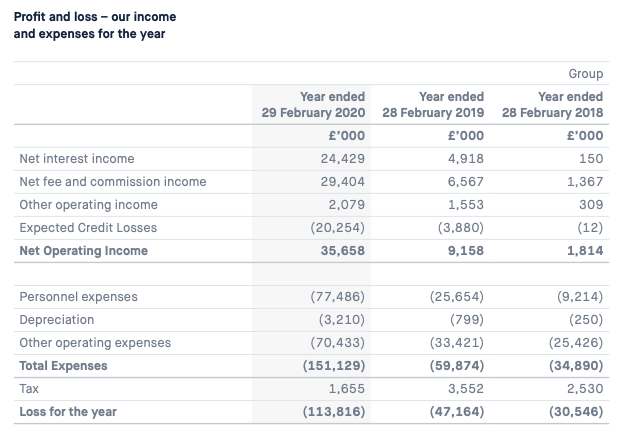

This morning, let’s add to our running dig into neobank results by parsing recently released data from Starling Bank and Monzo. As we’ll see, although some neobanks are managing to clean up their ledgers and work toward profits — or reach profitability — not all are in the black.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest private market news, talks about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here and myself here — and make sure to check out our Friday show that featured the Square-Tidal deal, some recent IPOs and some super-neat rounds.

Much like today’s show, if I am being honest. Here’s the rundown:

A packed kickoff to what promises to be a packed week!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 AM PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

Venture capitalists and other investors have poured capital into fintech startups around the world in recent years, including a record number of rounds worth $100 million or more in the second quarter of 2020. In Q2 2020 venture-backed fintech startups raised 28 nine-figure rounds, underscoring the scale of the bet investors are making on fintech’s long-term success.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Inside that fintech wave are various hubs of activity, including payments tech, investing and banking. That last category has helped give rise to so-called neobanks, startup banking entities that offer mobile-first, consumer-friendly banking tools and services. Given the old-fashioned nature of banking in many countries (and how far out of reach banking remains for many) neobanks have seen strong uptake by users in recent years.

And the startup cohort has raised oceans of capital to help fuel its growth. In America, Chime was most recently valued at $5.8 billion after raising hundreds of millions in late 2019. More recently, neobank Revolut added $80 million to its Q1 2020 round worth $500 million. Revolut is also worth north of $5 billion. Monzo is well-funded (albeit at a recent valuation reduction), Latin America-focused NuBank is worth $10 billion, according to Crunchbase, Starling recently raised another £40 million, while Germany’s N26 is worth over $3 billion after its most recent nine-figure round.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

Of course, startups don’t raise money for fun; they raise it to invest it in their operations and drive scale. So, we knew that these megafundraisers were losing money on purpose. All the same, let’s peek at the economics of several neobanks, as their now dated and thus not at all current results can provide useful context on two points: Why investors are excited to put their capital to work in neobanks, and why neobanks always seem to have another check to announce.

To prevent my receiving unhappy emails from irked fans of these companies, please bear in mind that we’re looking several quarters back when observing the following results.

It would be lovely to have more recent data, but with European neobanks reporting their — roughly — 2019 results in recent weeks, this is what we have. We are going to parse the numbers, but we will not conflate past performance with current results. We do not know much about 2020 neobank financial performance.

Anyhoo, to the numbers. You can read the full documents from Monzo here, Starling here (or here, if that link is struggling) and Revolut here.

Let’s start with Monzo, which has a clear set of figures for us to peek at:

Image Credits: Monzo

Powered by WPeMatico

The European fintech wave can’t stop and won’t stop. That’s why I’m excited to announce that the founder and CEO of Starling Bank Anne Boden is joining us at Disrupt Berlin.

While it feels like everybody is talking about challenger banks, Boden started thinking about building a new bank back in 2014. She ditched a carrer in traditional banks to start her own thing.

Starling provides a current account specifically designed for your phone. You can open an account in just a few minutes using the company’s mobile app.

Whenever you use your card or send money, you can instantly see the transaction in the app — there’s no delay. You can also receive push notifications instantly. When it comes to your card, you can lock it when you can’t find it, and there’s no exchange fee when you use your card abroad. Starling supports Apple Pay, Google Pay, Samsung Pay, Fitbit Pay and, yes, even Garmin Pay.

Starling is even better with multiple people. For instance, if your roommate or significant other also has a Starling account, you can create a joint account for shared bills. You can also send money instantly to other Starling accounts.

The startup has been building a marketplace to become the only banking app you need. There are already a handful of fintech companies leveraging the Starling API. You’ll find savings, investment and mortgage products. You can centralize your paper receipts and more from the Starling app.

The startup already has its own banking license and has been raising a funding round of more than $100 million.

Starling operates in a very competitive market, with well-funded startups such as Monzo, Revolut and N26 all iterating quite quickly. That’s why it’s going to be interesting to hear Boden’s take on challenger banks, the fintech industry and her experience with Starling.

TechCrunch is coming back to Berlin to talk with the best and brightest people in tech from Europe and the rest of the world. In addition to fireside chats and panels, new startups will participate in the Startup Battlefield Europe to win the coveted cup.

Tickets to the show, which runs November 29-30, are available here.

Powered by WPeMatico

London-based Tail is a new fintech startup that offers a glimpse into the promise of Open Banking. This is seeing upcoming legislation in the EU and U.K. force banks to offer third-party developer access to your bank account data — with your permission, of course.

London-based Tail is a new fintech startup that offers a glimpse into the promise of Open Banking. This is seeing upcoming legislation in the EU and U.K. force banks to offer third-party developer access to your bank account data — with your permission, of course.  We already knew that GoCardless co-founder Tom Blomfield was working on a new U.K. banking startup, but now, thanks in part to a noisy series of Tweets from investors, developers and the company’s own Twitter account, more details have emerged.

We already knew that GoCardless co-founder Tom Blomfield was working on a new U.K. banking startup, but now, thanks in part to a noisy series of Tweets from investors, developers and the company’s own Twitter account, more details have emerged.