starling bank

Auto Added by WPeMatico

Auto Added by WPeMatico

Assembling a startup team is harder than assembling 10 IKEA dressers, and the stakes are much, much higher.

Starting with the assumption that 90% of startups will fail and the most successful ones take an average of six years to IPO, founders must make careful decisions about whom they invite to join the core team.

Will that stellar engineer become a great CTO? Should your product person be opinionated or a team player? Are you even the best choice for CEO?

ThoughtSpot CEO Sudheesh Nair shared some of his thoughts about building a sturdy leadership team and drafted a thorough checklist for entrepreneurs who are putting a crew together. His initial advice?

“Investors love founder-CEOs, and founders are often fantastic candidates for this role. But not everyone can do it well, and more importantly, not everyone wants to.”

In a related article, Gregg Adkin, VP and managing director at Dell Technologies Capital, shared the framework he’s developed for helping founders set up their board.

Choosing the right mix of people can impact everything from fundraising to hiring: “Investors often ask founders about their board [because] it says a lot about their character, their judgment and their willingness to be challenged,” he writes.

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

Miranda Halpern spoke to Amsterdam-based coach Ward van Gasteren for our latest growth marketing interview, which is free to read.

In their discussion, van Gasteren addressed misconceptions about growth hacking, the mistakes most startups are likely to make, and the distinctions he draws between growth hacking and growth marketing:

“Growth hacking is great to kickstart growth, test new opportunities and see what tactics work,” he tells us.

“Marketers should be there to continue where the growth hackers left off: Build out those strategies, maintain customer engagement, and keep tactics fresh and relevant.”

Thanks very much for reading Extra Crunch this week; I hope you have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

Image Credits: sureeporn / Getty Images

In his first column since returning to TechCrunch, reporter Ryan Lawler considered the potential ripples Square’s purchase of Afterpay may send across the pond of buy now, pay later startups.

For commentary and perspective, he interviewed:

The investors he spoke to agreed that deferring payments helps drive e-commerce, “but scale matters and long-term margins look slim for BNPL startups,” reports Ryan.

Image Credits: Ivan Bajic (opens in a new window) / Getty Images

Businesses have been deploying AI solutions for 20 years, but few have achieved the outstanding gains in efficiency and profitability promised when the technology first appeared.

But there’s a burgeoning new generation of enterprise AI, Eshwar Belani, an operating partner at Symphony AI, writes in a guest column.

“Companies on the leading edge of AI innovation have advanced to the next generation, which will define the coming decade of big data, analytics and automation — Enterprise AI 2.0.”

Image Credits: Joan Cros Garcia-Corbis (opens in a new window) / Getty Images

Over the next 18 months, one technologist says the increased adoption of embodied artificial intelligence will open a path to superintelligence — incredibly powerful software that dwarfs anything the human mind could produce.

“All the crazy Boston Dynamics videos of robots jumping, dancing, balancing and running are examples of embodied AI,” says Chris Nicholson, founder and CEO of Pathmind, which uses deep reinforcement learning to optimize industrial operations and supply chains.

“The field is moving fast and, in this revolution, you can dance.”

Image Credits: Nigel Sussman (opens in a new window)

The Exchange looks at the valuations of public insurtech companies and considers what that means for startups — but from a slightly different perspective.

“We’d typically riff on the new values of public neoinsurance companies and use that data to work our way into a guess concerning what the price declines might mean for related startups,” Alex Wilhelm writes. “Taking public-market data and using it to better understand private markets is pretty much the national pastime of this column.

“Not today.”

Image Credits: Anastassiia (opens in a new window) / Getty Images

The fact that the globe is awash in venture capital should not be news to readers of this newsletter.

For founders, it means more than just fat checks, Kunal Lunawat, the co-founder and managing partner of Agya Ventures, writes in a guest column.

“Founders would be well served to go back to the basics and focus on the principles of fundraising when determining who sits on their cap table.”

Image Credits: Nigel Sussman (opens in a new window)

Alex Wilhelm checks in on results from Starling Bank and Monzo to see what the neobanks’ most recent financial figures say about the state of neobanks overall.

“Although some neobanks are managing to clean up their ledgers and work toward profits — or reach profitability — not all are in the black,” he notes.

But among those that are?

“At least a portion of the neobanking world is financially stable enough to consider public offerings.”

Image Credits: MicroStockHub (opens in a new window)/ Getty Images

The red-hot venture capital market may give founders lots of investors to choose from, but the most important thing (if you can be choosy) is being able to trust and rely on your investors, Ripple Ventures’ Matt Cohen and True’s Tony Conrad write in a guest column.

“This … new dynamic is forcing founders to be extremely selective about exactly who is sitting around their mentorship table,” they write.

“It’s simply not possible to have numerous deep and meaningful relationships to extract maximum value at the early stage from seasoned investors.”

Image Credits: A-Digit (opens in a new window) / Getty Images

Assembling a board of directors is not merely about finding individuals who can aid your early-stage journey, Gregg Adkin, the vice president and managing director at Dell Technologies Capital, writes in a guest column.

The composition of the board can also impact your fundraising.

“Investors often ask founders about their board [because] it says a lot about their character, their judgment and their willingness to be challenged,” he writes.

Adkins offers a framework he calls “SPIFS” — for strategy, people, image, finance and systems for compliance — to aid founders in setting up a board.

Image Credits: Nigel Sussman (opens in a new window)

In the wake of Deliveroo’s plans to abandon the Spanish market after the country passed legislation requiring companies dependent on gig workers to hire employees, Alex Wilhelm wondered about the battle for smaller markets and whether third place is sufficient.

“One company exiting a market is not a big deal, but we were curious about Deliveroo’s comments regarding the need for market leadership — or something close to it — to warrant continued investment,” he writes for The Exchange.

“Is this the common reality for startups battling for market position, no matter if those markets are cities or countries?”

Powered by WPeMatico

Over the past year, startup banks have proven that they have a shot at disrupting retail banking. These challengers have amassed a war chest of funding, announced some ambitious international expansion plans and attracted millions of customers.

And yet, building a bank has proven to be even harder than building a startup in general. Retail banks aren’t willing to sit back and watch startups eat their lunch. Here’s a look back at the biggest moves of the year from challenger banks, some trends you should keep an eye on and the upcoming challenges for those startups.

Due to the regulatory framework and the size of the market, it is much easier to launch a challenger bank in Europe compared to anywhere else in the world. That’s why challenger banks have been thriving in Europe.

When a company gets a full banking license from the central bank of a EU country, the startup can passport its license across all EU countries and operate across the continent.

N26 raised a ton of money in 2019: last January, the Berlin-based startup announced a $300 million funding round, raising another $170 million in July. The company is now valued at $3.5 billion.

With more than 3.5 million customers in Europe, N26 announced some ambitious expansion plans. N26 is now live in the U.S. and is already planning a launch in Brazil.

Revolut has also been aggressively expanding in order to beat its competitors to new markets. In addition to its home market in the U.K., Revolut is available across Europe. In 2019, the company expanded to Singapore and Australia and currently has at least 8 million users.

While Revolut announced that it should launch in the U.S. and Canada by the end of last year, the clock ran out on that prediction. The startup has been very transparent about its expansion plans, even though it sometimes means that you have to wait months or even years before a full rollout.

For instance, Revolut announced in September 2018 that it would launch in New Zealand, Hong Kong and Japan “in the coming months.” It later became “early 2019,” then “2019.” India, Brazil, South Africa, Mexico and the UAE have also all been mentioned at some point. In other words: launching a banking product in a new country is hard.

The U.S. is a tedious market as you have to get a license in all 50 states to operate across the country

Monzo has been doing well at home in the U.K. It has attracted 3 million customers and raised £113 million (~$144m) in funding last year from Y Combinator’s Continuity fund. It is expanding to the U.S., but the rollout has been slow.

Nubank is another well-funded challenger bank. Backed by Tencent, the startup has raised a $400 million Series F round from TCV. According to the WSJ, the startup has a valuation above $10 billion.

Originally from Brazil, Nubank expanded to Mexico and has plans to expand to Argentina.

Chime is increasingly looking like the bigger player in the U.S., recently raising a $500 million funding round and reached a valuation of $5.8 billion. It only operates in the U.S.

Starling Bank and Atom Bank only operate in the U.K. Bunq is based in Amsterdam with a product tailor-made for the Netherlands, but it accepts customers across Europe.

This isn’t meant to be an exhaustive list as it’s becoming increasingly hard to cover all challenger banks.

There are a few basic features that separate challenger banks from legacy retail banks. Signing up is extremely simple and only requires a mobile app. The mobile app itself is usually much more polished than traditional banking apps.

Users receive a Mastercard or Visa debit card that communicates with the company’s server for each transaction. This way, users can receive instant notifications, block and unblock their cards and turn off some features, such as foreign payments, ATM withdrawals and online transactions.

Challenger banks usually customers promise no markup fees on transactions in foreign currencies, but there are sometimes some limits on this feature.

So how do these companies make money? When you pay with your card, banks generate a tiny, tiny interchange fee of money on each transaction. It’s really small, but it could become serious revenue at scale with tens of millions or hundreds of millions of users.

Challenger banks also offer other financial services like insurance products, foreign exchange or consumer credit. Some challenger banks develop those features in house, but many of those features are actually managed by external fintech partners. Challenger banks generate a commission on those products.

But the most promising product is premium subscriptions. While challenger banks started with free accounts and low, transparent fees, they have been selling premium subscriptions for a fixed monthly fee.

Challenger banks have become a software-as-a-service industry with a freemium component

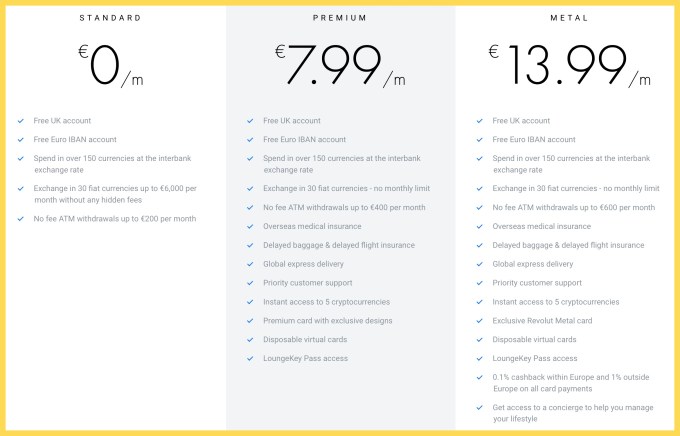

For example, Revolut offers premium accounts for €7.99 per month with higher limits, some insurance benefits that you’d expect from a premium card and access to advanced features, such as cryptocurrencies and disposable virtual cards. There’s a super premium product for €13.99 called Metal with a metal card design, cashback on card payments and access to a concierge feature.

This seems a bit counterintuitive, but premium subscriptions have been performing well, according to discussions with people working in the industry. You pay a lot in subscription fees in order to avoid small transactional fees. (And you also get a cool card.)

Challenger banks have become a software-as-a-service industry with a freemium component. It leads to a premium positioning and high expectations from customers.

Revolut’s fees top out at €13.99/month.

Powered by WPeMatico

Starling Bank, the U.K. challenger bank founded by banking veteran Anne Boden, is set to open a second U.K. office this summer, where it plans to recruit up to 50 software engineers and up to 100 customer service team members. The planned location is Southampton, on the south coast of England, and will be Starling’s first office outside of London.

In a call with Boden late on Friday, she told me the majority of its Southampton office will be new hires who will be helping to build out the challenger back’s business-banking product. In just less than a year, Starling has garnered more than 30,000 SME business-account sign-ups, adding to around 500,000 consumer current accounts.

The company plans to invest heavily in its business-banking division over the next few years, partly off the back of being awarded a £100 million grant from the Capability and Innovation Fund (CIF), which was set up by Royal Bank of Scotland to fulfill European state aid conditions arising from the bank’s £45 billion U.K. government bailout during the financial crisis.

Boden says that Southampton was chosen as Starling’s new office for its entrepreneurial spirit and high level of tech talent. She says the city is gaining a reputation as a “burgeoning tech hub” and has a growing skilled jobs market and good transport links, including to and from London.

More broadly, she wants Starling to “spread the fintech love” beyond its traditional base of London. There’s an increasing sense that U.K. tech is too London-centric and that the country’s fast-growing tech sector and the employment opportunities it represents should be more evenly distributed.

To that end, Southampton was recently identified in research conducted by global service company CBRE as a technology “Super Cluster” based on the level, concentration and growth of tech-sector employment in the city.

The city’s tech scene is also supported by the University of Southampton (where Tim Berners-Lee was previously Chair of Computer Science) and home to the Web Science Institute, where Dame Wendy Hall is based. Nearby is also “innovation hub” Southampton Science Park, spanning 72 acres and housing a mixture of commercial offices, laboratories and meeting and conferencing facilities.

Meanwhile, the news of a second Starling office comes a month after the challenger bank announced it had raised £75 million (~$97 million) in further funding. The new capital consisted of a £60 million Series C round led by Merian Global Investors, including Merian Chrysalis, with £15 million in follow-on funding from Starling’s existing backer and major shareholder Harald McPike. It brings total funding to date for the London-based challenger bank to £133 million, not including the more recent £100 million CIF grant.

Further forward, I’m told Starling is also committed to opening a second regional contact centre to support its growing customer base of SME businesses and individual current account holders. There was previously talk that Wales, the country from where Boden hails, could be chosen, although the bank is also eyeing up the North of England and the Midlands.

Powered by WPeMatico

In another example of Starling Bank jumping on the Open Banking/PSD2 train before legislation in the U.K. and Europe next year will force banks to do so, it is launching its latest API partnership: this time with Yoyo Wallet, the U.K.-based mobile payment and loyalty platform. Read More

In another example of Starling Bank jumping on the Open Banking/PSD2 train before legislation in the U.K. and Europe next year will force banks to do so, it is launching its latest API partnership: this time with Yoyo Wallet, the U.K.-based mobile payment and loyalty platform. Read More

Powered by WPeMatico

Digital-only UK “challenger” bank, Starling Bank, has added support for Apple Pay — meaning its customers can now add their Starling debit card to their Apple Wallet and make contactless payments drawing from funds in their Starling account via their Apple devices.

Digital-only UK “challenger” bank, Starling Bank, has added support for Apple Pay — meaning its customers can now add their Starling debit card to their Apple Wallet and make contactless payments drawing from funds in their Starling account via their Apple devices.