stanford

Auto Added by WPeMatico

Auto Added by WPeMatico

Jumia may be the first startup you’ve heard of from Africa. But the e-commerce venture that recently listed on the NYSE is definitely not the first or last word in African tech.

The continent has an expansive digital innovation scene, the components of which are intersecting rapidly across Africa’s 54 countries and 1.2 billion people.

When measured by monetary values, Africa’s tech ecosystem is tiny by Shenzen or Silicon Valley standards.

But when you look at volumes and year over year expansion in VC, startup formation, and tech hubs, it’s one of the fastest growing tech markets in the world. In 2017, the continent also saw the largest global increase in internet users—20 percent.

If you’re a VC or founder in London, Bangalore, or San Francisco, you’ll likely interact with some part of Africa’s tech landscape for the first time—or more—in the near future.

That’s why TechCrunch put together this Extra-Crunch deep-dive on Africa’s technology sector.

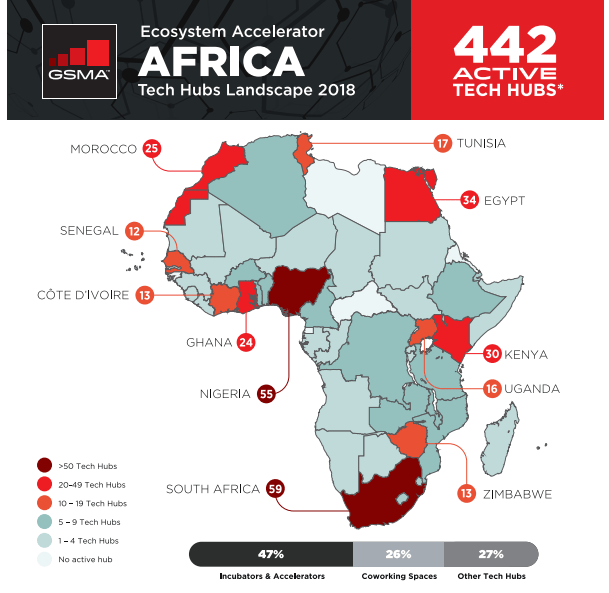

A foundation for African tech is the continent’s 442 active hubs, accelerators, and incubators (as tallied by GSMA). These spaces have become focal points for startup formation, digital skills building, events, and IT activity on the continent.

Prominent tech hubs in Africa include CcHub in Nigeria, Pan-African incubator MEST, and Kenya’s iHub, with over 200 resident members. More of these organizations are receiving funds from DFIs, such as the World Bank, and aid agencies, including France’s $76 million African tech fund.

Prominent tech hubs in Africa include CcHub in Nigeria, Pan-African incubator MEST, and Kenya’s iHub, with over 200 resident members. More of these organizations are receiving funds from DFIs, such as the World Bank, and aid agencies, including France’s $76 million African tech fund.

Blue-chip companies such as Google and Microsoft are also providing money and support. In 2018 Facebook opened its own Hub_NG in Lagos with partner CcHub, to foster startups using AI and machine learning.

Powered by WPeMatico

Brex, the fintech business that’s taken the startup world by storm with its sought after corporate card tailored for entrepreneurs, is raising millions in Series D funding less than a year after it launched, TechCrunch has learned.

Bloomberg reports Brex is raising at a $2 billion valuation, though sources tell TechCrunch the company is still in negotiations with both new and existing investors. Brex didn’t immediately respond to requests for comment.

Kleiner Perkins is leading the round via former general partner Mood Rowghani, who left the storied venture capital fund last year to form Bond alongside Mary Meeker and Noah Knauf. As we’ve previously reported, the Bond crew is still in the process of deploying capital from Kleiner’s billion-dollar Digital Growth Fund III, the pool of capital they were responsible for before leaving the firm.

Bond, which recently closed on $1.25 billion for its debut effort and made its first investment, is not participating in the round for Brex, sources confirm to TechCrunch. Bond declined to comment.

Brex, a graduate of Y Combinator’s winter 2017 cohort, has raised $182 million in VC funding, reaching a valuation of $1.1 billion in October 2018 three months after launching its corporate card for startups and less than a year after completing YC’s accelerator program.

Most recently, Brex attracted a $125 million Series C investment led by Greenoaks Capital, DST Global and IVP. The startup is also backed by PayPal founders Peter Thiel and Max Levchin, and VC firms such as Ribbit Capital, Oneway Ventures and Mindset Ventures, according to PitchBook.

The company’s pace of growth is unheard of, even in Silicon Valley where inflated valuations and outsized rounds are the norm. Why? Brex has tapped into a market dominated by legacy players in dire need of technological innovation and, of course, startup founders always need access to credit. That, coupled with the fact that it’s capitalized on YC’s network of hundreds of startup founders — i.e. Brex customers — has accelerated its path to a multi-billion-dollar price tag.

Brex doesn’t require any kind of personal guarantee or security deposit from its customers, allowing founders near-instant access to credit. More importantly, it gives entrepreneurs a credit limit that’s as much as 10 times higher than what they would receive elsewhere.

Investors may also be enticed by the fact the company doesn’t use third-party legacy technology, boasting a software platform that is built from scratch. On top of that, Brex simplifies a lot of the frustrating parts of the corporate expense process by providing companies with a consolidated look at their spending.

“We have a very similar effect of what Stripe had in the beginning, but much faster because Silicon Valley companies are very good at spending money but making money is harder,” Brex co-founder and chief executive officer Henrique Dubugras told me late last year.

Stripe, for context, was founded in 2010. Not until 2014 did the company raise its unicorn round, landing a valuation of $1.75 billion with an $80 million financing. Today, Stripe has raised a total of roughly $1 billion at a valuation north of $20 billion.

Dubugras and Brex co-founder Pedro Franceschi, 23-year-old entrepreneurs, relocated from Brazil to Stanford in the fall of 2016 to attend the university. They dropped out upon getting accepted into YC, which they applied to with a big dreams for a virtual reality startup called Beyond. Beyond quickly became Brex, a name in which Dubugras recently told TechCrunch was chosen because it was one of few four-letter word domains available.

Brex’s funding history

March 2017: Brex graduates Y Combinator

April 2017: $6.5M Series A | $25M valuation

April 2018: $50M Series B | $220M valuation

October 2018: $125M Series C | $1.1B valuation

May 2019: undisclosed Series D | ~$2B valuation

In April, Brex secured a $100 million debt financing from Barclays Investment Bank. At the time, Dubugras told TechCrunch the business would not seek out venture investment in the near future, though he did comment that the debt capital would allow for a significant premium when Brex did indeed decide to raise capital again.

In 2019, Brex has taken steps several steps toward maturation.Recently, it launched a rewards program for customers and closed its first notable acquisition of a blockchain startup called Elph. Shortly after, Brex released its second product, a credit card made specifically for ecommerce companies.

Its upcoming infusion of capital will likely be used to develop payment services tailored to Fortune 500 business, which Dubugras has said is part of Brex’s long term plan to disrupt the entire financial technology space.

Powered by WPeMatico

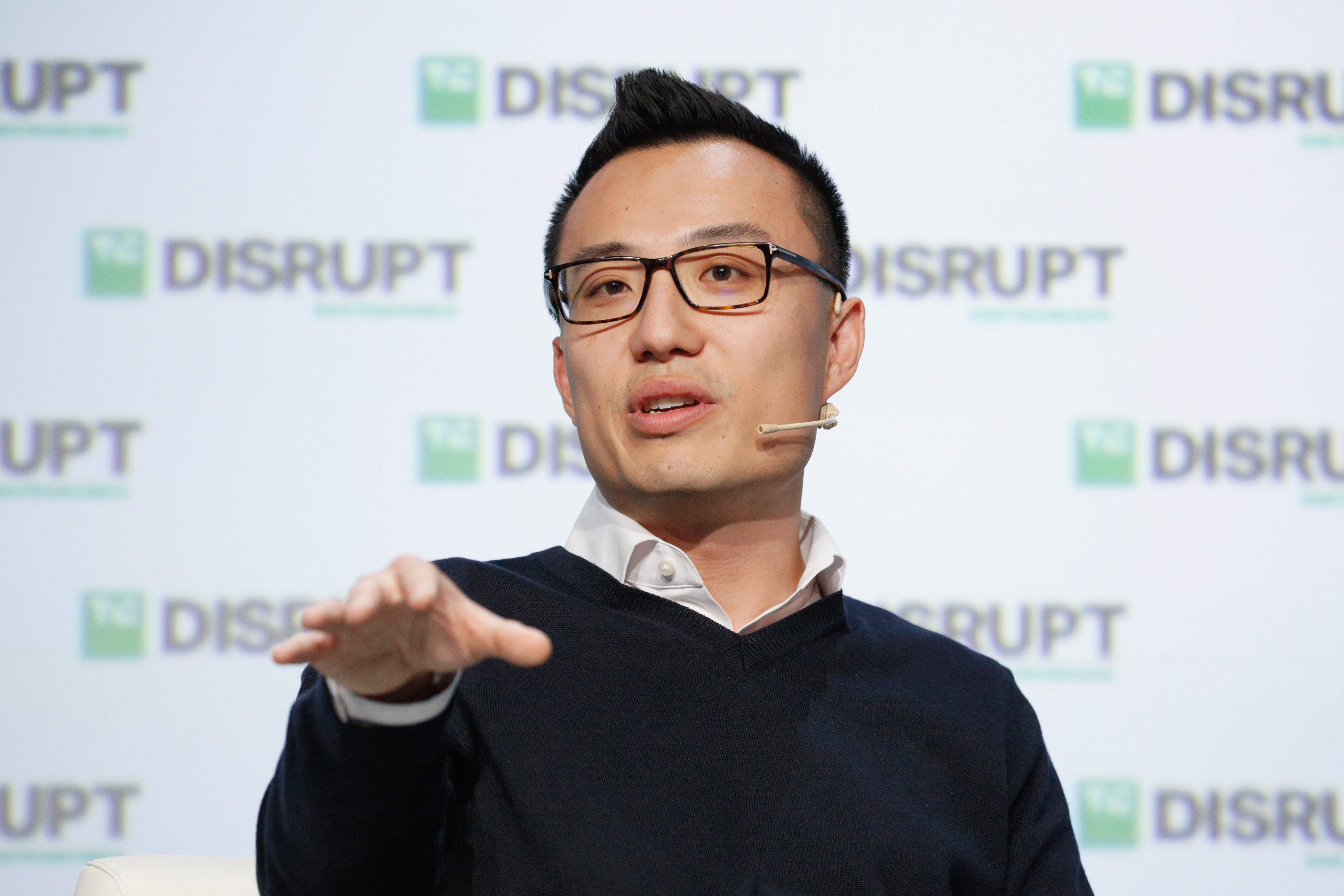

More than five years ago, Sequoia partner Alfred Lin called Tony Xu, the founder of a small on-demand delivery startup called DoorDash, to say he was passing on the company’s seed round.

This was, of course, before venture capital funding in food delivery startups had taken off. DoorDash, launched out of Xu’s Stanford graduate school dorm room, wasn’t worth Sequoia’s capital — yet.

Today, venture capitalists are valuing the San Francisco-based company at a whopping $12.6 billion with a $600 million Series G. New investors Darsana Capital Partners and Sands Capital participated in the deal, which nearly doubles DoorDash’s previous valuation, alongside existing backers Coatue Management, Dragoneer, DST Global, Sequoia Capital, the SoftBank Vision Fund and Temasek Capital Management.

As for Sequoia’s Alfred Lin, he realized his mistake years ago and jumped in on DoorDash’s 2014 Series A, and has participated in every subsequent round since. DoorDash, a graduate of Y Combinator’s Summer 2013 cohort, is also backed by Kleiner Perkins, CRV and Khosla Ventures, among others. In total, the company has raised $2.5 billion in VC funding, making it one of the most well-capitalized private companies in the U.S.

SoftBank, via its prolific dealmaker Jeffrey Housenbold, was responsible for making DoorDash a unicorn in early 2018. The nearly $100 billion Vision Fund led DoorDash’s $535 million Series D, valuing the business at $1.4 billion. Just three months ago, the SoftBank Vision Fund, DST Global, Coatue Management, GIC, Sequoia and Y Combinator put an additional $400 million in the fast-growing business.

SAN FRANCISCO, CA – SEPTEMBER 05: DoorDash CEO Tony Xu speaks onstage during Day 1 of TechCrunch Disrupt SF 2018 at Moscone Center on September 5, 2018 in San Francisco, California. (Photo by Kimberly White/Getty Images for TechCrunch)

Xu told TechCrunch the company’s Series F was “a reflection of superior performance over the past year.” DoorDash was currently seeing 325% growth year-over-year, he said, pointing to recent data from Second Measure showing the service had overtaken Uber Eats in the U.S., coming in second only to GrubHub.

“I think the numbers speak for themselves,” Xu said at the time. “If you just run the math on DoorDash’s course and speed, we’re on track to be number one.”

At a venture capital-focused summit hosted in April, Xu added that DoorDash was the largest delivery platform in America by “pretty wide margins,” explaining that it was, in fact, growing 4x faster than its next closest peer. In this morning’s announcement, the company added that it’s grown 60% since its late February Series F, with its annualized total sales hitting $7.5 billion in March, an increase of 280% year-over-year.

Still, one wonders what kind of growth metrics DoorDash might be sharing to attract that kind of valuation multiple. The company has yet to disclose revenues and is not yet profitable, but has seen its price tag grow astronomically in just two years. Since March 2018, DoorDash’s valuation has skyrocketed from $1.4 billion to $4 billion with a $250 million Series E to $7.1 billion with a $350 million Series F and, finally, to nearly $13 billion with its Series G.

The $12.6 billion valuation makes DoorDash one of the 10 most valuable venture-backed companies in the U.S., surpassing Coinbase, Instacart and even Slack, according to PitchBook.

DoorDash is currently active in more than 4,000 cities in the U.S. and Canada, with hundreds of partners, including both restaurants and supermarkets (Walmart is using DoorDash for grocery deliveries). The company also operates DoorDash Drive, which allows businesses to use the DoorDash network to make their own deliveries.

Powered by WPeMatico

If you took the photos and videos out of pornography, could it appeal to a new audience? Caroline Spiegel’s first startup Quinn aims to bring some imagination to adult entertainment. Her older brother, Snapchat CEO Evan Spiegel, spent years trying to convince people his app wasn’t just for sexy texting. Now Caroline is building a website dedicated to sexy text and audio. The 22-year-old college senior tells TechCrunch that on April 13th she’ll launch Quinn, which she describes as “a much less gross, more fun Pornhub for women.”

TechCrunch checked out Quinn’s private beta site, which is pretty bare bones right now. Caroline tells us she’s already raised less than a million dollars for the project. But given her brother’s success spotting the next generation’s behavior patterns and turning them into beloved products, Caroline might find investors are eager to throw cash at Quinn. That’s especially true given she’s taking a contrarian approach. There will be no imagery on Quinn.

Caroline explains that “There’s no visual content on the site — just audio and written stories. And the whole thing is open source, so people can submit content and fantasies, etc. Everything is vetted by us before it goes on the site.” The computer science major is building Quinn with a three-woman team of her best friends she met while at Stanford, including Greta Meyer, though they plan to relocate to LA after graduation.

The idea for Quinn sprung from a deeply personal need. “I came up with it because I had to leave Stanford my junior year because I was struggling with anorexia and sexual dysfunction that came along with that,” Caroline tells me. “I started to do a lot of research into sexual dysfunction cures. There are about 30 FDA-approved drugs for sexual dysfunction for men but zero for women, and that’s a big bummer.”

She believes there’s still a stigma around women pleasuring themselves, leading to a lack of products offering assistance. Sure, there are plenty of porn sites, but few are explicitly designed for women, and fewer stray outside of visual content. Caroline says photos and videos can create body image pressure, but with text and audio, anyone can imagine themselves in a scene. “Most visual media perpetuates the male gaze … all mainstream porn tells one story … You don’t have to fit one idea of what a woman should look like.”

That concept fits with the startup’s name “Quinn,” which Caroline says one of her best guy friends thought up. “He said this girl he met — his dream girl — was named ‘Quinn.’ ”

Caroline took to Reddit and Tumblr to find Quinn’s first creators. Reddit stuck to text and links for much of its history, fostering the kinky literature and audio communities. And when Tumblr banned porn in December, it left a legion of adult content makers looking for a new home. “Our audio ranges from guided masturbation to overheard sex, and there’s also narrated stories. It’s literally everything. Different strokes for different for folks, know what I mean?” Caroline says with a cheeky laugh.

To establish its brand, Quinn is running social media influencer campaigns where “The basic idea is to make people feel like it’s okay to experience pleasure. It’s hard to make something like masturbation cool, so that’s a little bit of a lofty goal. We’re just trying to make it feel okay, and even more okay than it is for men.”

As for the business model, Caroline’s research found younger women were embarrassed to pay for porn. Instead, Quinn plans to run ads, though there could be commerce opportunities too. And because the site doesn’t bombard users with nude photos or hardcore videos, it might be able to attract sponsors that most porn sites can’t.

Until monetization spins up, Quinn has the sub-$1 million in funding that Caroline won’t reveal the source of, though she confirms it’s not from her brother. “I wouldn’t say that he’s particularly involved other than he’s one of the most important people in my life and I talk to him all the time. He gives me the best advice I can imagine,” the younger sibling says. “He doesn’t have any qualms, he’s very supportive.”

Quinn will need all the morale it can get, as Caroline bluntly admits, “We have a lot of competitors.” There’s the traditional stuff like Pornhub, user-generated content sites like Make Love Not Porn and spontaneous communities like on Reddit. She calls $5 million-funded audio porn startup Dipsea “an exciting competitor,” though she notes that “we sway a little more erotic than they do, but we’re so supportive of their mission.” How friendly.

Quinn’s biggest rival will likely be outdated but institutionalized site Literotica, which SimilarWeb ranks as the 60th most popular adult website, 631st most visited site overall, showing it gets 53 million hits per month. But the fact that Literotica looks like a web 1.0 forum yet has so much traffic signals a massive opportunity for Quinn. With rules prohibiting Quinn from launching native mobile apps, it will have to put all its effort into making its website stand out if it’s going to survive.

But more than competition, Caroline fears that Quinn will have to convince women to give its style of porn a try. “Basically, there’s this idea that for men, masturbation is an innate drive and for women it’s a ‘could do without it, could do with it.’ Quinn is going to have to make a market alongside a product and that terrifies me,” Caroline says, her voice building with enthusiasm. “But that’s what excites me the most about it, because what I’m banking on is if you’ve never had chocolate before, you don’t know. But once you have it, you start craving it. A lot of women haven’t experienced raw, visceral pleasure before, [but once we help them find it] we’ll have momentum.”

Most importantly, Quinn wants all women to feel they have rightful access to whatever they fancy. “It’s not about deserving to feel great. You don’t have to do Pilates to use this. You don’t have to always eat right. There’s no deserving with our product. Our mission is for women to be more in touch with themselves and feel fucking great. It’s all about pleasure and good vibes.”

Powered by WPeMatico

Young founders who want to start companies while still in school have an increasing number of resources to tap into that exist just for them. Students that want to learn how to build companies can apply to an increasing number of fast-track programs that allow them to gain valuable early stage operating experience. The energy around student entrepreneurship today is incredible. I’ve been immersed in this community as an investor and adviser for some time now, and to say the least, I’m continually blown away by what the next generation of innovators are dreaming up (from Analytical Space’s global data relay service for satellites to Brooklinen’s reinvention of the luxury bed).

Bill Gates in 1973

First, let’s look at student founders and why they’re important. Student entrepreneurs have long been an important foundation of the startup ecosystem. Many students wrestle with how best to learn while in school —some students learn best through lectures, while more entrepreneurial students like author Julian Docks find it best to leave the classroom altogether and build a business instead.

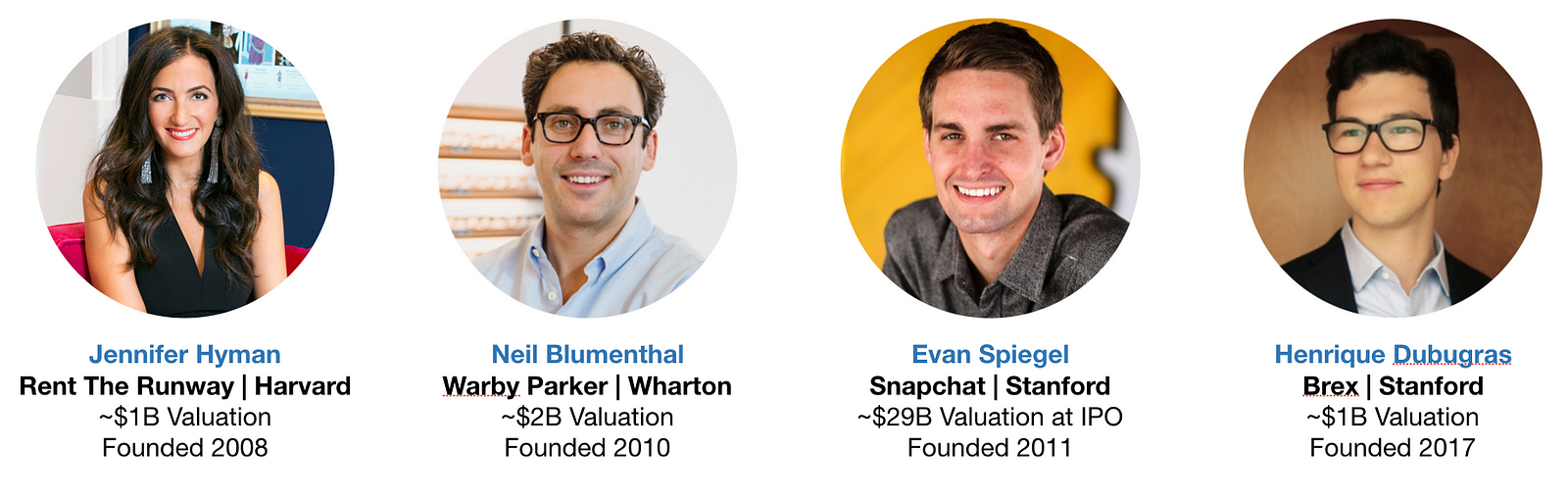

Indeed, some of our most iconic founders are Microsoft’s Bill Gates and Facebook’s Mark Zuckerberg, both student entrepreneurs who launched their startups at Harvard and then dropped out to build their companies into major tech giants. A sample of the current generation of marquee companies founded on college campuses include Snap at Stanford ($29B valuation at IPO), Warby Parker at Wharton (~$2B valuation), Rent The Runway at HBS (~$1B valuation), and Brex at Stanford (~$1B valuation).

Some of today’s most celebrated tech leaders built their first ventures while in school — even if some student startups fail, the critical first-time founder experience is an invaluable education in how to build great companies. Perhaps the best example of this that I could find is Drew Houston at Dropbox (~$9B valuation at IPO), who previously founded an edtech startup at MIT that, in his words, provided a: “great introduction to the wild world of starting companies.”

Student founders are everywhere, but the highest concentration of venture-backed student founders can be found at just 5 universities. Based on venture fund portfolio data from the last six years, Harvard, Stanford, MIT, UPenn, and UC Berkeley have produced the highest number of student-founded companies that went on to raise $1 million or more in seed capital. Some prospective students will even enroll in a university specifically for its reputation of churning out great entrepreneurs. This is not to say that great companies are not being built out of other universities, nor does it mean students can’t find resources outside a select number of schools. As you can see later in this essay, there are a number of new ways students all around the country can tap into the startup ecosystem. For further reading, PitchBook produces an excellent report each year that tracks where all entrepreneurs earned their undergraduate degrees.

Student founders have a number of new media resources to turn to. New email newsletters focused on student entrepreneurship like Justine and Olivia Moore’s Accelerated and Kyle Robertson’s StartU offer new channels for young founders to reach large audiences. Justine and Olivia, the minds behind Accelerated, have a lot of street cred— they launched Stanford’s on-campus incubator Cardinal Ventures before landing as investors at CRV.

StartU goes above and beyond to be a resource to founders they profile by helping to connect them with investors (they’re active at 12 universities), and run a podcast hosted by their Editor-in-Chief Johnny Hammond that is top notch. My bet is that traditional media will point a larger spotlight at student entrepreneurship going forward.

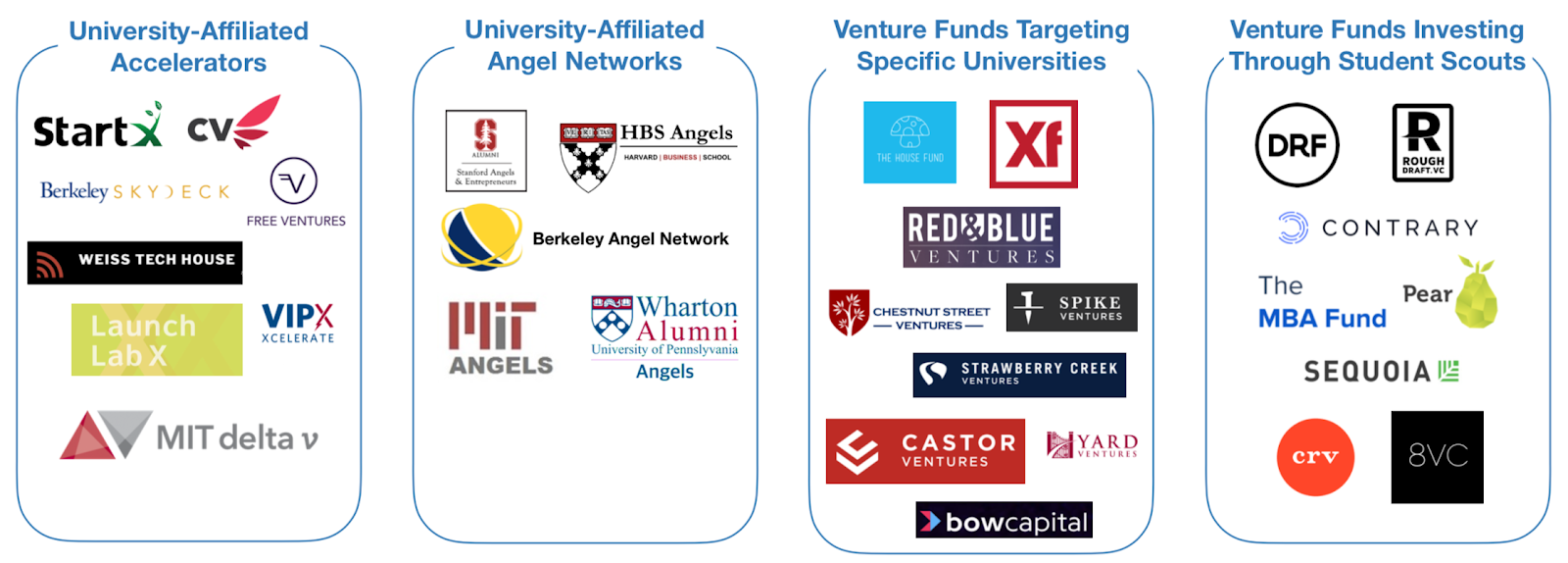

New pools of capital are also available that are specifically for student founders. There are four categories that I call special attention to:

While it is difficult to estimate exactly how much capital has been deployed by each, there is no denying that there has been an explosion in the number of programs that address the pre-seed phase. A sample of the programs available at the Top 5 universities listed above are in the graphic below — listing every resource at every university would be difficult as there are so many.

One alumni-centric fund to highlight is the Alumni Ventures Group, which pools LP capital from alumni at specific universities, then launches individual venture funds that invest in founders connected to those universities (e.g. students, alumni, professors, etc.). Through this model, they’ve deployed more than $200M per year! Another highlight has been student scout programs — which vary in the degree of autonomy and capital invested — but essentially empower students to identify and fund high-potential student-founded companies for their parent venture funds. On campuses with a large concentration of student founders, it is not uncommon to find student scouts from as many as 12 different venture funds actively sourcing deals (as is made clear from David Tao’s analysis at UC Berkeley).

Investment Team at Rough Draft Ventures

In my opinion, the two institutions that have the most expansive line of sight into the student entrepreneurship landscape are First Round’s Dorm Room Fund and General Catalyst’s Rough Draft Ventures. Since 2012, these two funds have operated a nationwide network of student scouts that have invested $20K — $25K checks into companies founded by student entrepreneurs at 40+ universities. “Scout” is a loose term and doesn’t do it justice — the student investors at these two funds are almost entirely autonomous, have built their own platform services to support portfolio companies, and have launched programs to incubate companies built by female founders and founders of color. Another student-run fund worth noting that has reach beyond a single region is Contrary Capital, which raised $2.2M last year. They do a particularly great job of reaching founders at a diverse set of schools — their network of student scouts are active at 45 universities and have spoken with 3,000 founders per year since getting started. Contrary is also testing out what they describe as a “YC for university-based founders”. In their first cohort, 100% of their companies raised a pre-seed round after Contrary’s demo day. Another even more recently launched organization is The MBA Fund, which caters to founders from the business schools at Harvard, Wharton, and Stanford. While super exciting, these two funds only launched very recently and manage portfolios that are not large enough for analysis just yet.

Over the last few months, I’ve collected and cross-referenced publicly available data from both Dorm Room Fund and Rough Draft Ventures to assess the state of student entrepreneurship in the United States. Companies were pulled from each fund’s portfolio page, then checked against Crunchbase for amount raised, accelerator participation, and other metrics. If you’d like to sift through the data yourself, feel free to ping me — my email can be found at the end of this article. To be clear, this does not represent the full scope of investment activity at either fund — many companies in the portfolios of both funds remain confidential and unlisted for good reasons (e.g. startups working in stealth). In fact, the In addition, data for early stage companies is notoriously variable in quality, even with Crunchbase. You should read these insights as directional only, given the debatable confidence interval. Still, the data is still interesting and give good indicators for the health of student entrepreneurship today.

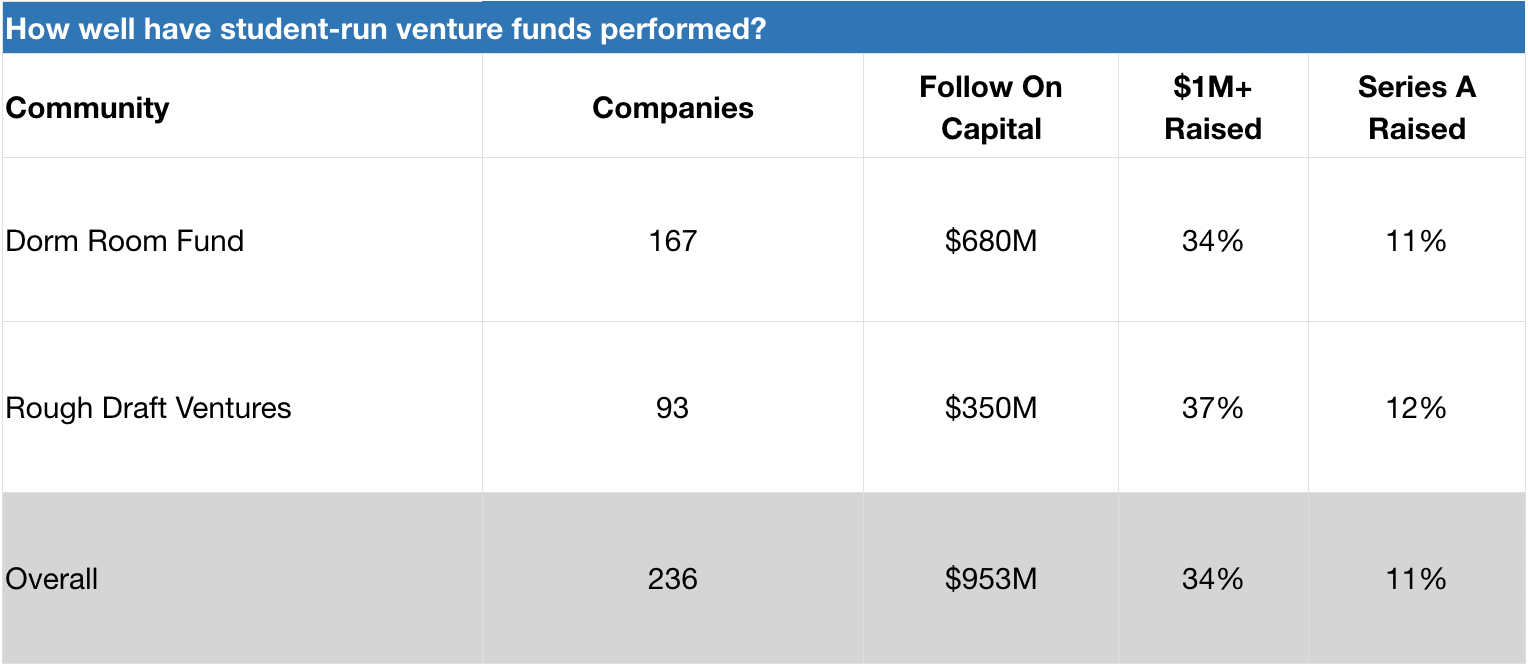

Dorm Room Fund and Rough Draft Ventures have invested in 230+ student-founded companies that have gone on to raise nearly $1 billion in follow on capital. These funds have invested in a diverse range of companies, from govtech (e.g. mark43, raised $77M+ and FiscalNote, raised $50M+) to space tech (e.g. Capella Space, raised ~$34M). Several portfolio companies have had successful exits, such as crypto startup Distributed Systems (acquired by Coinbase) and social networking startup tbh (acquired by Facebook). While it is too early to evaluate the success of these funds on a returns basis (both were launched just 6 years ago), we can get a sense of success by evaluating the rates by which portfolio companies raise additional capital. Taken together, 34% of DRF and RDV companies in our data set have raised $1 million or more in seed capital. For a rough comparison, CB Insights cites that 40% of YC companies and 48% of Techstars companies successfully raise follow on capital (defined as anything above $750K). Certainly within the ballpark!

Dorm Room Fund and Rough Draft Ventures companies in our data set have an 11–12% rate of survivorship to Series A. As a benchmark, a previous partner at Y Combinator shared that 20% of their accelerator companies raise Series A capital (YC declined to share the official figure, but it’s likely a stat that is increasing given their new Series A support programs. For further reading, check out YC’s reflection on what they’ve learned about helping their companies raise Series A funding). In any case, DRF and RDV’s numbers should be taken with a grain of salt, as the average age of their portfolio companies is very low and raising Series A rounds generally takes time. Ultimately, it is clear that DRF and RDV are active in the earlier (and riskier) phases of the startup journey.

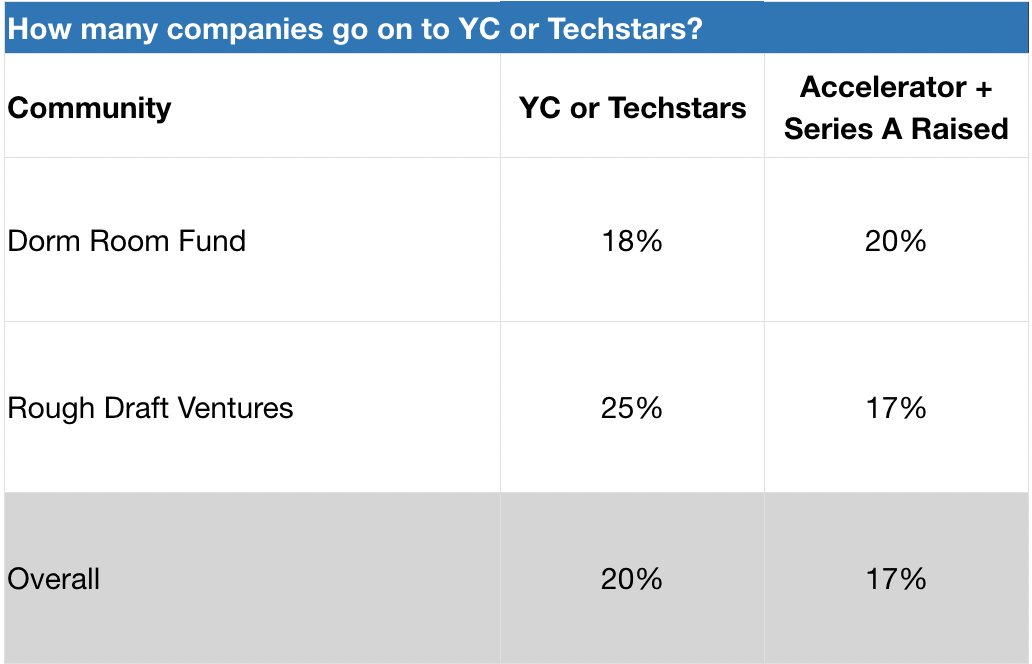

Dorm Room Fund and Rough Draft Ventures send 18–25% of their portfolio companies to Y Combinator or Techstars. Given YC’s 1.5% acceptance rate as reported in Fortune, this is quite significant! Internally, these two funds offer founders an opportunity to participate in mock interviews with YC and Techstars alumni, as well as tap into their communities for peer support (e.g. advice on pitch decks and application content). As a result, Dorm Room Fund and Rough Draft Ventures regularly send cohorts of founders to these prestigious accelerator programs. Based on our data set, 17–20% of DRF and RDV companies that attend one of these accelerators end up raising Series A venture financing.

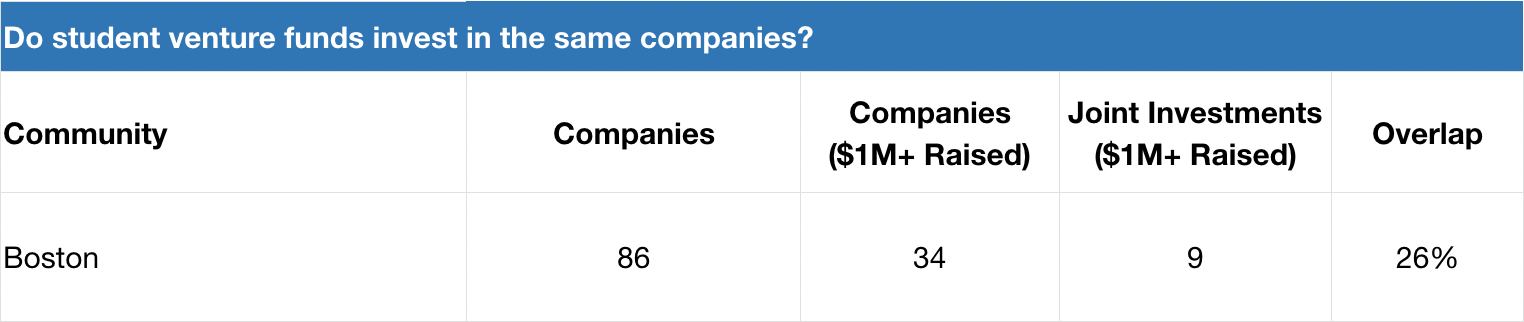

Dorm Room Fund and Rough Draft Ventures don’t invest in the same companies. When we take a deeper look at one specific ecosystem where these two funds have been equally active over the last several years — Boston — we actually see that the degree of investment overlap for companies that have raised $1M+ seed rounds sits at 26%. This suggests that these funds are either a) seeing different dealflow or b) have widely different investment decision-making.

Dorm Room Fund and Rough Draft Ventures should not just be measured by a returns-basis today, as it’s too early. I hypothesize that DRF and RDV are actually encouraging more entrepreneurial activity in the ecosystem (more students decide to start companies while in school) as well as improving long-term founder outcomes amongst students they touch (portfolio founders build bigger and more successful companies later in their careers). As more students start companies, there’s likely a positive feedback loop where there’s increasing peer pressure to start a company or lean on friends for founder support (e.g. feedback, advice, etc).Both of these subjects warrant additional study, but it’s likely too early to conduct these analyses today.

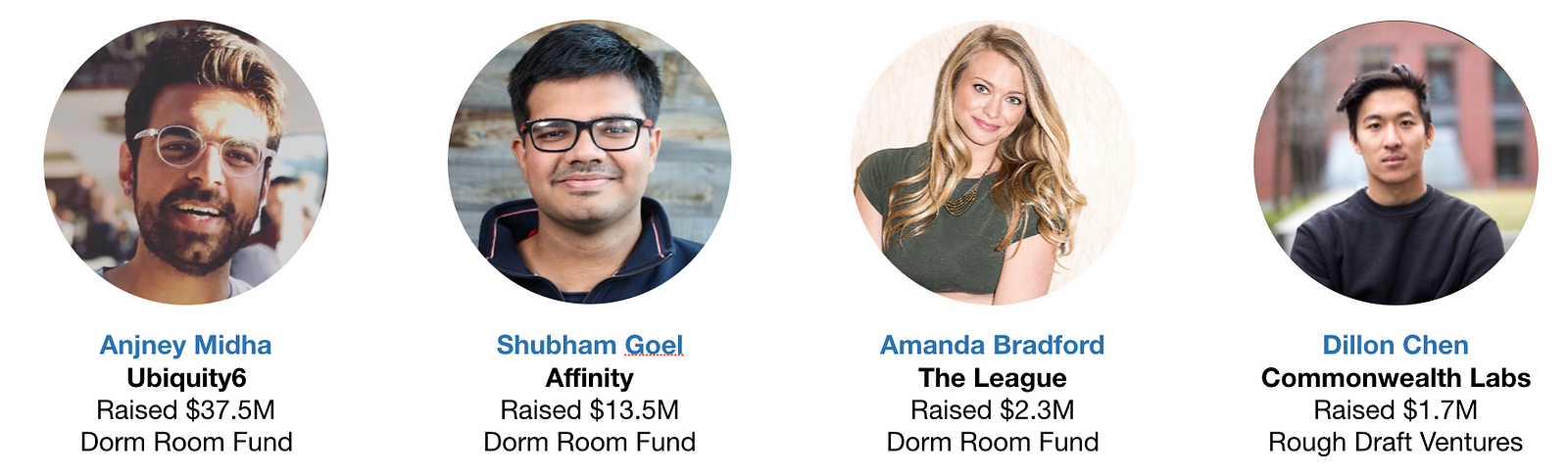

Dorm Room Fund and Rough Draft Ventures have impressive alumni that you will want to track. 1 in 4 alumni partners are founders, and 29% of these founder alumni have raised $1M+ seed rounds for their companies. These include Anjney Midha’s augmented reality startup Ubiquity6 (raised $37M+), Shubham Goel’s investor-focused CRM startup Affinity (raised $13M+), Bruno Faviero’s AI security software startup Synapse (raised $6M+), Amanda Bradford’s dating app The League (raised $2M+), and Dillon Chen’s blockchain startup Commonwealth Labs (raised $1.7M). It makes sense to me that alumni from these communities that decide to start companies have an advantage over their peers — they know what good companies look like and they can tap into powerful networks of young talent / experienced investors.

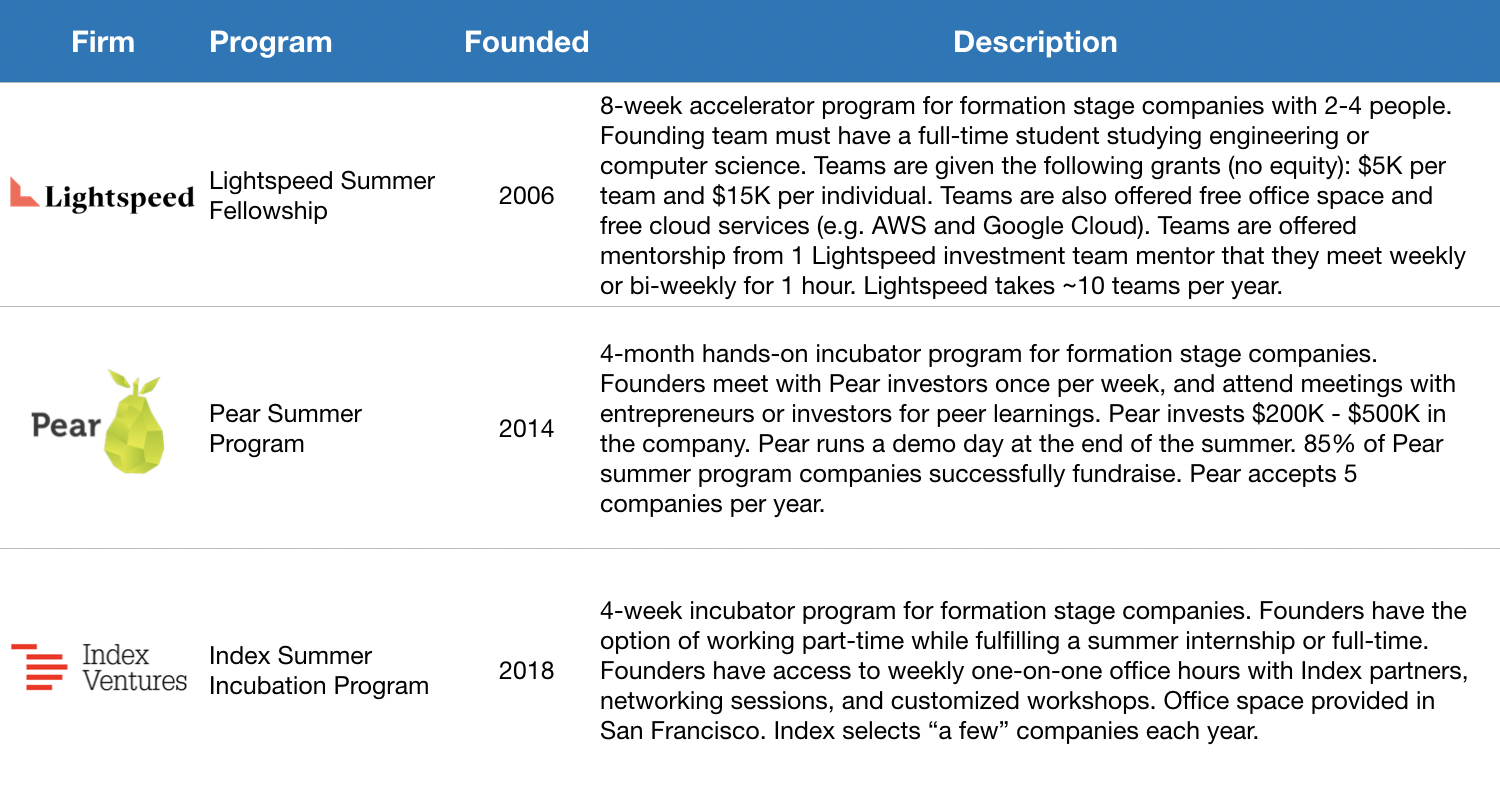

Beyond Dorm Room Fund and Rough Draft Ventures, some venture capital firms focus on incubation for student-founded startups. Credit should first be given to Lightspeed for producing the amazing Summer Fellows bootcamp experience for promising student founders — after all, Pinterest was built there! Jeremy Liew gives a good overview of the program through his sit-down interview with Afterbox’s Zack Banack. Based on a study they conducted last year, 40% of Lightspeed Summer Fellows alumni are currently active founders. Pear Ventures also has an impressive summer incubator program where 85% of its companies successfully complete a fundraise. Index Ventures is the latest to build an incubator program for student founders, and even accepts founders who want to work on an idea part-time while completing a summer internship.

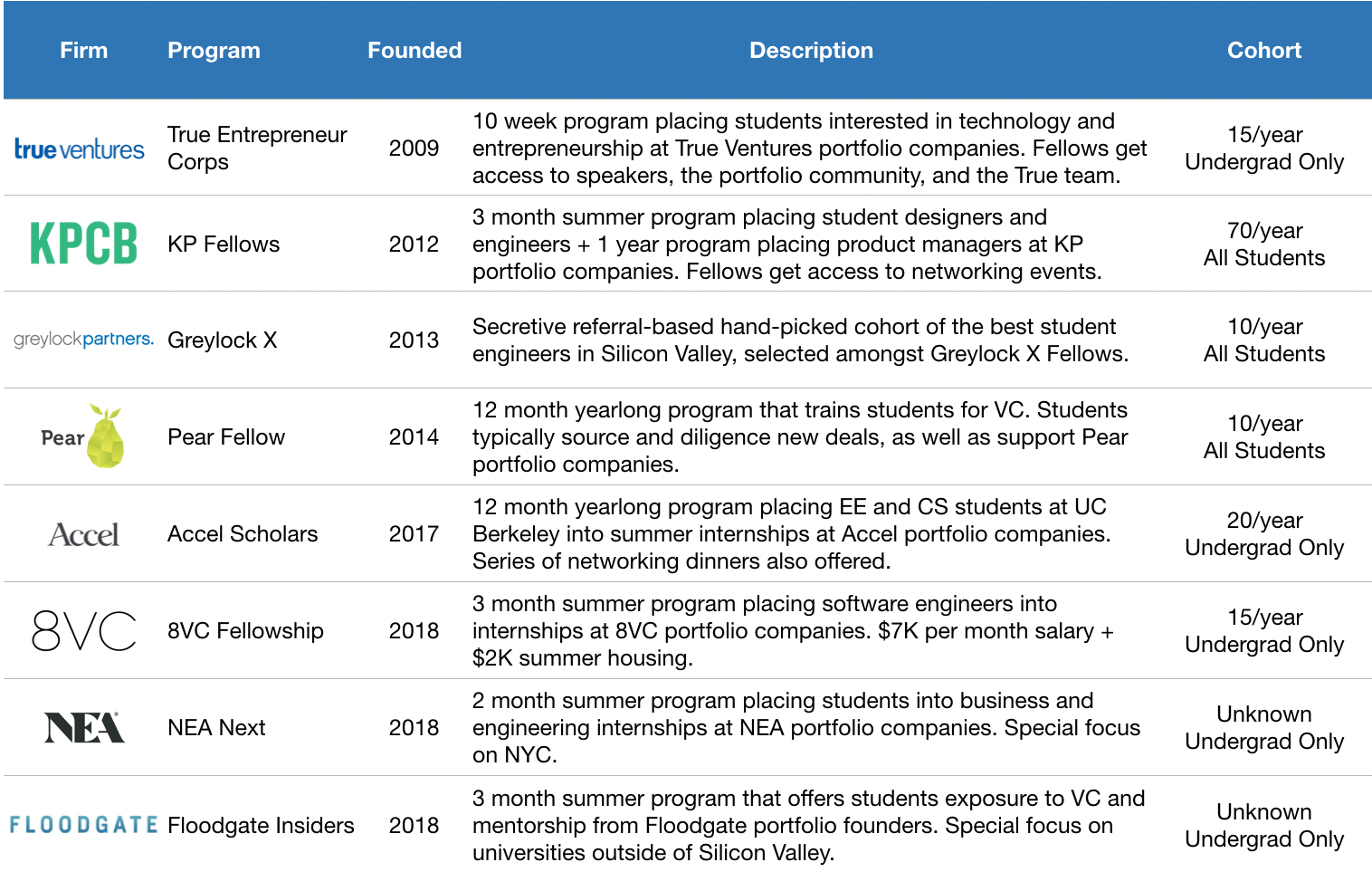

Let’s now look at students who want to join a startup before founding one. Venture funds have historically looked to tap students for talent, and are expanding the engagement lifecycle. The longest running programs include Kleiner Perkins’ class=”m_1196721721246259147gmail-markup–strong m_1196721721246259147gmail-markup–p-strong”> KP Fellows and True Ventures’ TEC Fellows, which focus on placing the next generation’s most promising product managers, engineers, and designers into the portfolio companies of their parent venture funds.

There’s also the secretive Greylock X, a referral-based hand-picked group of the best student engineers in Silicon Valley (among their impressive alumni are founders like Yasyf Mohamedali and Joe Kahn, the folks behind First Round-backed Karuna Health). As these programs have matured, these firms have recognized the long-run value of engaging the alumni of their programs.

More and more alumni are “coming back” to the parent funds as entrepreneurs, like KP Fellow Dylan Field of Figma (and is also hosting a KP Fellow, closing a full circle loop!). Based on their latest data, 10% of KP Fellows alumni are founders — that’s a lot given the fact that their community has grown to 500! This helps explain why Kleiner Perkins has created a structured path to receive $100K in seed funding to companies founded by KP Fellow alumni. It looks like venture funds are beginning to invest in student programs as part of their larger platform strategy, which can have a real impact over the long term (for further reading, see this analysis of platform strategy outcomes by USV’s Bethany Crystal).

KP Fellows in San Francisco

Venture funds are doubling down on student talent engagement — in just the last 18 months, 4 funds have launched student programs. It’s encouraging to see new funds follow in the footsteps of First Round, General Catalyst, Kleiner Perkins, Greylock, and Lightspeed. In 2017, Accel launched their Accel Scholars program to engage top talent at UC Berkeley and Stanford. In 2018, we saw 8VC Fellows, NEA Next, and Floodgate Insiders all launch, targeting elite universities outside of Silicon Valley. Y Combinator implemented Early Decision, which allows student founders to apply one batch early to help with academic scheduling. Most recently, at the start of 2019, First Round launched the Graduate Fund (staffed by Dorm Room Fund alumni) to invest in founders who are recent graduates or young alumni.

Given more time, I’d love to study the rates by which student founders start another company following investments from student scout funds, as well as whether or not they’re more successful in those ventures. In any case, this is an escalation in the number of venture funds that have started to get serious about engaging students — both for talent and dealflow.

Student entrepreneurship 2.0 is here. There are more structured paths to success for students interested in starting or joining a startup. Founders have more opportunities to garner press, seek advice, raise capital, and more. Venture funds are increasingly leveraging students to help improve the three F’s — finding, funding, and fixing. In my personal view, I believe it is becoming more and more important for venture funds to gain mindshare amongst the next generation of founders and operators early, while still in school.

I can’t wait to see what’s next for student entrepreneurship in 2019. If you’re interested in digging in deeper (I’m human — I’m sure I haven’t covered everything related to student entrepreneurship here) or learning more about how you can start or join a startup while still in school, shoot me a note at sxu@dormroomfund.com. A massive thanks to Phin Barnes, Rei Wang, Chauncey Hamilton, Peter Boyce, Natalie Bartlett, Denali Tietjen, Eric Tarczynski, Will Robbins, Jasmine Kriston, Alicia Lau, Johnny Hammond, Bruno Faviero, Athena Kan, Shohini Gupta, Alex Immerman, Albert Dong, Phillip Hua-Bon-Hoa, and Trevor Sookraj for your incredible encouragement, support, and insight during the writing of this essay.

Powered by WPeMatico

Are more Theranos -style scandals looming for investors in healthcare startups?

A team of researchers associated with the Meta-Research Innovation Center at Stanford thinks so. They’ve published a paper warning investors in life sciences startups that a systemic lack of transparency exists in their portfolio companies — creating the possibility for more multi-billion-dollar implosions and scandals like the one that toppled Theranos and its charismatic founder, Elizabeth Holmes.

Indeed, one of the study’s authors, Dr. John Ioannidis, the co-director of the Meta-Research Innovation Center at Stanford and director of the University’s PhD program in Epidemiology and Clinical Research, was among the first people to identify the risks associated with Theranos and its “stealth research.”

Now Dr. Ioannidis and his co-authors, Ioana A. Cristea and Eli M. Cahan, have published a study surveying the publicly available research from the largest privately held companies in the healthcare space, and found them lacking.

Most of the highest-valued startups in healthcare have not published any significant scientific literature, the study found. Nearly half of the publications from companies worth more than $1 billion came from only two startups — 23andMe and Adaptive Biotechnologies, according to the paper.

“Many years ago I was the first person to say that Theranos had a problem,” says Ioannidis. “The problem that I had then was that Theranos did not have any peer-reviewed evidence to show.”

In an interview and in their paper, Ioannidis and Cahan warn that investors have overlooked systemic problems created by the lack of transparency among healthcare startups.

They write:

It would be tempting to dismiss the Theranos case as just one rotten apple. However, we worry that the focus on fraud puts aside a more fundamental concern. Fraud is making waves in the news, but stealth research may have a more detrimental impact.

According to the study’s findings, more than half of the healthcare startups that are worth more than $1 billion have published no highly cited papers at all. For companies that were acquired or are publicly traded that number is around 40 percent.

In all, healthcare startups that are currently valued at more than $1 billion published 425 Pubmed papers. And of those papers only 34 (8 percent, including two reviews) were highly cited. For companies with valuations of more than $1 billion that had been acquired or are publicly traded on stock exchanges, the researchers counted 413 papers, of which 47 (11 percent, including nine reviews) were highly cited.

Digging deeper into some of the companies that had high valuations but little or no published research revealed scores of operational and technological issues for the researchers.

For instance, StemCentrx, which was bought for $10.2 billion in 2016 by AbbVie, had published 16 papers — and only one highly cited paper. Since the acquisition, the Food and Drug Administration had imposed a delay on the readout of the company’s phase II trial for its Rova T targeted antibody drug for cancer treatment. In December, a Phase III trial for Rova T as a second-line treatment for patients with advanced small cell lung cancer was halted because the treatment wasn’t working, according to a report in Targeted Oncology.

Acerta Pharma, another healthcare-focused startup focused on cancer treatments, was bought by AstraZeneca for $7.3 billion. That company published nine articles and had one highly cited paper for a very early study of a potential treatment for relapsed chronic lymphocytic leukemia. Acerta received accelerated approval for a drug called acalabrutinib, which treats a rare form of lymphoma called mantle cell lymphoma. Two years ago, AstraZeneca had to retract data and admit that Acerta falsified preclinical data for its drug.

Then there’s Intarcia, the developer of a device for diabetes treatment that’s worth $5.5 billion. That company had its device rejected by the FDA and was forced to lay off staff and halt a couple of later-stage trials. It had only published six papers — none of them very highly cited.

Ultimately, the researchers concluded that highly valued healthcare startups don’t contribute to published research and that the valuation of these companies by investors is divorced from any externally validated data.

For the researchers (and for investors) this should present a problem.

“Many unicorns may be overvalued [21] and subject to unrealistic scientific expectations,” the study’s authors write. And they reject the argument that simply applying for — and receiving — patents is enough to prove that a technology in the healthcare space has been thoroughly vetted. “[Patents] do not offer the same level of documentation as peer-reviewed articles. For example, Theranos had over 100 patents [1], but these were unable to supplant the vacuum in their evidence,” the researchers wrote.

Even if companies want to protect their technology, there are still ways for them to be more transparent about the results or benefits of their technology. The authors acknowledge that publishing isn’t the primary mission of startups. They can, however publish a few high-value articles, secure their technology through patents and then work with researchers, universities or hospitals to validate the technology and have those organizations publish results of the tests, the authors argue.

As the authors conclude:

Start-ups are key purveyors of innovation and disruption. Consequently, holding them to a minimal standard of evaluation from the scientific community is crucial. Participation in peer review, with all its limitations, is the best way we have to uphold this standard. We are not arguing that start-ups should divert excessive resources to having peer-reviewed papers. However, when their products are destined to affect patient health, they should neither be solely doing marketing. Confidential data sharing with potential investors or regulators cannot replace more open scrutiny by the scientific community.

Powered by WPeMatico

Few issues divide the tech community quite like privacy. Much of Silicon Valley’s wealth has been built on data-driven advertising platforms, and yet, there remain constant concerns about the invasiveness of those platforms.

Such concerns have intensified in just the last few weeks as France’s privacy regulator placed a record fine on Google under Europe’s General Data Protection Regulation (GDPR) rules which the company now plans to appeal. Yet with global platform usage and service sales continuing to tick up, we asked a panel of eight privacy experts: “Has anything fundamentally changed around privacy in tech in 2019? What is the state of privacy and has the outlook changed?”

This week’s participants include:

TechCrunch is experimenting with new content forms. Consider this a recurring venue for debate, where leading experts – with a diverse range of vantage points and opinions – provide us with thoughts on some of the biggest issues currently in tech, startups and venture. If you have any feedback, please reach out: Arman.Tabatabai@techcrunch.com.

Albert Gidari is the Consulting Director of Privacy at the Stanford Center for Internet and Society. He was a partner for over 20 years at Perkins Coie LLP, achieving a top-ranking in privacy law by Chambers, before retiring to consult with CIS on its privacy program. He negotiated the first-ever “privacy by design” consent decree with the Federal Trade Commission. A recognized expert on electronic surveillance law, he brought the first public lawsuit before the Foreign Intelligence Surveillance Court, seeking the right of providers to disclose the volume of national security demands received and the number of affected user accounts, ultimately resulting in greater public disclosure of such requests.

There is no doubt that the privacy environment changed in 2018 with the passage of California’s Consumer Privacy Act (CCPA), implementation of the European Union’s General Data Protection Regulation (GDPR), and new privacy laws enacted around the globe.

“While privacy regulation seeks to make tech companies betters stewards of the data they collect and their practices more transparent, in the end, it is a deception to think that users will have more “privacy.””

For one thing, large tech companies have grown huge privacy compliance organizations to meet their new regulatory obligations. For another, the major platforms now are lobbying for passage of a federal privacy law in the U.S. This is not surprising after a year of privacy miscues, breaches and negative privacy news. But does all of this mean a fundamental change is in store for privacy? I think not.

The fundamental model sustaining the Internet is based upon the exchange of user data for free service. As long as advertising dollars drive the growth of the Internet, regulation simply will tinker around the edges, setting sideboards to dictate the terms of the exchange. The tech companies may be more accountable for how they handle data and to whom they disclose it, but the fact is that data will continue to be collected from all manner of people, places and things.

Indeed, if the past year has shown anything it is that two rules are fundamental: (1) everything that can be connected to the Internet will be connected; and (2) everything that can be collected, will be collected, analyzed, used and monetized. It is inexorable.

While privacy regulation seeks to make tech companies betters stewards of the data they collect and their practices more transparent, in the end, it is a deception to think that users will have more “privacy.” No one even knows what “more privacy” means. If it means that users will have more control over the data they share, that is laudable but not achievable in a world where people have no idea how many times or with whom they have shared their information already. Can you name all the places over your lifetime where you provided your SSN and other identifying information? And given that the largest data collector (and likely least secure) is government, what does control really mean?

All this is not to say that privacy regulation is futile. But it is to recognize that nothing proposed today will result in a fundamental shift in privacy policy or provide a panacea of consumer protection. Better privacy hygiene and more accountability on the part of tech companies is a good thing, but it doesn’t solve the privacy paradox that those same users who want more privacy broadly share their information with others who are less trustworthy on social media (ask Jeff Bezos), or that the government hoovers up data at rate that makes tech companies look like pikers (visit a smart city near you).

Many years ago, I used to practice environmental law. I watched companies strive to comply with new laws intended to control pollution by creating compliance infrastructures and teams aimed at preventing, detecting and deterring violations. Today, I see the same thing at the large tech companies – hundreds of employees have been hired to do “privacy” compliance. The language is the same too: cradle to grave privacy documentation of data flows for a product or service; audits and assessments of privacy practices; data mapping; sustainable privacy practices. In short, privacy has become corporatized and industrialized.

True, we have cleaner air and cleaner water as a result of environmental law, but we also have made it lawful and built businesses around acceptable levels of pollution. Companies still lawfully dump arsenic in the water and belch volatile organic compounds in the air. And we still get environmental catastrophes. So don’t expect today’s “Clean Privacy Law” to eliminate data breaches or profiling or abuses.

The privacy world is complicated and few people truly understand the number and variety of companies involved in data collection and processing, and none of them are in Congress. The power to fundamentally change the privacy equation is in the hands of the people who use the technology (or choose not to) and in the hands of those who design it, and maybe that’s where it should be.

Gabriel Weinberg is the Founder and CEO of privacy-focused search engine DuckDuckGo.

Coming into 2019, interest in privacy solutions is truly mainstream. There are signs of this everywhere (media, politics, books, etc.) and also in DuckDuckGo’s growth, which has never been faster. With solid majorities now seeking out private alternatives and other ways to be tracked less online, we expect governments to continue to step up their regulatory scrutiny and for privacy companies like DuckDuckGo to continue to help more people take back their privacy.

“Consumers don’t necessarily feel they have anything to hide – but they just don’t want corporations to profit off their personal information, or be manipulated, or unfairly treated through misuse of that information.”

We’re also seeing companies take action beyond mere regulatory compliance, reflecting this new majority will of the people and its tangible effect on the market. Just this month we’ve seen Apple’s Tim Cook call for stronger privacy regulation and the New York Times report strong ad revenue in Europe after stopping the use of ad exchanges and behavioral targeting.

At its core, this groundswell is driven by the negative effects that stem from the surveillance business model. The percentage of people who have noticed ads following them around the Internet, or who have had their data exposed in a breach, or who have had a family member or friend experience some kind of credit card fraud or identity theft issue, reached a boiling point in 2018. On top of that, people learned of the extent to which the big platforms like Google and Facebook that collect the most data are used to propagate misinformation, discrimination, and polarization. Consumers don’t necessarily feel they have anything to hide – but they just don’t want corporations to profit off their personal information, or be manipulated, or unfairly treated through misuse of that information. Fortunately, there are alternatives to the surveillance business model and more companies are setting a new standard of trust online by showcasing alternative models.

Melika Carroll is Senior Vice President, Global Government Affairs at Internet Association, which represents over 45 of the world’s leading internet companies, including Google, Facebook, Amazon, Twitter, Uber, Airbnb and others.

We support a modern, national privacy law that provides people meaningful control over the data they provide to companies so they can make the most informed choices about how that data is used, seen, and shared.

“Any national privacy framework should provide the same protections for people’s data across industries, regardless of whether it is gathered offline or online.”

Internet companies believe all Americans should have the ability to access, correct, delete, and download the data they provide to companies.

Americans will benefit most from a federal approach to privacy – as opposed to a patchwork of state laws – that protects their privacy regardless of where they live. If someone in New York is video chatting with their grandmother in Florida, they should both benefit from the same privacy protections.

It’s also important to consider that all companies – both online and offline – use and collect data. Any national privacy framework should provide the same protections for people’s data across industries, regardless of whether it is gathered offline or online.

Two other important pieces of any federal privacy law include user expectations and the context in which data is shared with third parties. Expectations may vary based on a person’s relationship with a company, the service they expect to receive, and the sensitivity of the data they’re sharing. For example, you expect a car rental company to be able to track the location of the rented vehicle that doesn’t get returned. You don’t expect the car rental company to track your real-time location and sell that data to the highest bidder. Additionally, the same piece of data can have different sensitivities depending on the context in which it’s used or shared. For example, your name on a business card may not be as sensitive as your name on the sign in sheet at an addiction support group meeting.

This is a unique time in Washington as there is bipartisan support in both chambers of Congress as well as in the administration for a federal privacy law. Our industry is committed to working with policymakers and other stakeholders to find an American approach to privacy that protects individuals’ privacy and allows companies to innovate and develop products people love.

Dr. Johnny Ryan FRHistS is Chief Policy & Industry Relations Officer at Brave. His previous roles include Head of Ecosystem at PageFair, and Chief Innovation Officer of The Irish Times. He has a PhD from the University of Cambridge, and is a Fellow of the Royal Historical Society.

Tech companies will probably have to adapt to two privacy trends.

“As lawmakers and regulators in Europe and in the United States start to think of “purpose specification” as a tool for anti-trust enforcement, tech giants should beware.”

First, the GDPR is emerging as a de facto international standard.

In the coming years, the application of GDPR-like laws for commercial use of consumers’ personal data in the EU, Britain (post-EU), Japan, India, Brazil, South Korea, Malaysia, Argentina, and China will bring more than half of global GDP under a similar standard.

Whether this emerging standard helps or harms United States firms will be determined by whether the United States enacts and actively enforces robust federal privacy laws. Unless there is a federal GDPR-like law in the United States, there may be a degree of friction and the potential of isolation for United States companies.

However, there is an opportunity in this trend. The United States can assume the global lead by doing two things. First, enact a federal law that borrows from the GDPR, including a comprehensive definition of “personal data”, and robust “purpose specification”. Second, invest in world-leading regulation that pursues test cases, and defines practical standards. Cutting edge enforcement of common principles-based standards is de facto leadership.

Second, privacy and antitrust law are moving closer to each other, and might squeeze big tech companies very tightly indeed.

Big tech companies “cross-use” user data from one part of their business to prop up others. The result is that a company can leverage all the personal information accumulated from its users in one line of business, and for one purpose, to dominate other lines of business too.

This is likely to have anti-competitive effects. Rather than competing on the merits, the company can enjoy the unfair advantage of massive network effects even though it may be starting from scratch in a new line of business. This stifles competition and hurts innovation and consumer choice.

Antitrust authorities in other jurisdictions have addressed this. In 2015, the Belgian National Lottery was fined for re-using personal information acquired through its monopoly for a different, and incompatible, line of business.

As lawmakers and regulators in Europe and in the United States start to think of “purpose specification” as a tool for anti-trust enforcement, tech giants should beware.

John Miller is the VP for Global Policy and Law at the Information Technology Industry Council (ITI), a D.C. based advocate group for the high tech sector. Miller leads ITI’s work on cybersecurity, privacy, surveillance, and other technology and digital policy issues.

Data has long been the lifeblood of innovation. And protecting that data remains a priority for individuals, companies and governments alike. However, as times change and innovation progresses at a rapid rate, it’s clear the laws protecting consumers’ data and privacy must evolve as well.

“Data has long been the lifeblood of innovation. And protecting that data remains a priority for individuals, companies and governments alike.”

As the global regulatory landscape shifts, there is now widespread agreement among business, government, and consumers that we must modernize our privacy laws, and create an approach to protecting consumer privacy that works in today’s data-driven reality, while still delivering the innovations consumers and businesses demand.

More and more, lawmakers and stakeholders acknowledge that an effective privacy regime provides meaningful privacy protections for consumers regardless of where they live. Approaches, like the framework ITI released last fall, must offer an interoperable solution that can serve as a model for governments worldwide, providing an alternative to a patchwork of laws that could create confusion and uncertainty over what protections individuals have.

Companies are also increasingly aware of the critical role they play in protecting privacy. Looking ahead, the tech industry will continue to develop mechanisms to hold us accountable, including recommendations that any privacy law mandate companies identify, monitor, and document uses of known personal data, while ensuring the existence of meaningful enforcement mechanisms.

Nuala O’Connor is president and CEO of the Center for Democracy & Technology, a global nonprofit committed to the advancement of digital human rights and civil liberties, including privacy, freedom of expression, and human agency. O’Connor has served in a number of presidentially appointed positions, including as the first statutorily mandated chief privacy officer in U.S. federal government when she served at the U.S. Department of Homeland Security. O’Connor has held senior corporate leadership positions on privacy, data, and customer trust at Amazon, General Electric, and DoubleClick. She has practiced at several global law firms including Sidley Austin and Venable. She is an advocate for the use of data and internet-enabled technologies to improve equity and amplify marginalized voices.

For too long, Americans’ digital privacy has varied widely, depending on the technologies and services we use, the companies that provide those services, and our capacity to navigate confusing notices and settings.

“Americans deserve comprehensive protections for personal information – protections that can’t be signed, or check-boxed, away.”

We are burdened with trying to make informed choices that align with our personal privacy preferences on hundreds of devices and thousands of apps, and reading and parsing as many different policies and settings. No individual has the time nor capacity to manage their privacy in this way, nor is it a good use of time in our increasingly busy lives. These notices and choices and checkboxes have become privacy theater, but not privacy reality.

In 2019, the legal landscape for data privacy is changing, and so is the public perception of how companies handle data. As more information comes to light about the effects of companies’ data practices and myriad stewardship missteps, Americans are surprised and shocked about what they’re learning. They’re increasingly paying attention, and questioning why they are still overburdened and unprotected. And with intensifying scrutiny by the media, as well as state and local lawmakers, companies are recognizing the need for a clear and nationally consistent set of rules.

Personal privacy is the cornerstone of the digital future people want. Americans deserve comprehensive protections for personal information – protections that can’t be signed, or check-boxed, away. The Center for Democracy & Technology wants to help craft those legal principles to solidify Americans’ digital privacy rights for the first time.

Chris Baker is Senior Vice President and General Manager of EMEA at Box.

Last year saw data privacy hit the headlines as businesses and consumers alike were forced to navigate the implementation of GDPR. But it’s far from over.

“…customers will have trust in a business when they are given more control over how their data is used and processed”

2019 will be the year that the rest of the world catches up to the legislative example set by Europe, as similar data regulations come to the forefront. Organizations must ensure they are compliant with regional data privacy regulations, and more GDPR-like policies will start to have an impact. This can present a headache when it comes to data management, especially if you’re operating internationally. However, customers will have trust in a business when they are given more control over how their data is used and processed, and customers can rest assured knowing that no matter where they are in the world, businesses must meet the highest bar possible when it comes to data security.

Starting with the U.S., 2019 will see larger corporations opt-in to GDPR to support global business practices. At the same time, local data regulators will lift large sections of the EU legislative framework and implement these rules in their own countries. 2018 was the year of GDPR in Europe, and 2019 be the year of GDPR globally.

Christopher Wolf is the Founder and Chair of the Future of Privacy Forum think tank, and is senior counsel at Hogan Lovells focusing on internet law, privacy and data protection policy.

“Regardless of the outcome of the debate over a new federal privacy law, the issue of the privacy and protection of personal data is unlikely to recede.”

with the adoption of a highly-regulatory and broadly-applicable state privacy law in California last Summer (and similar laws adopted or proposed in other states), and with intense focus on the data collection and sharing practices of large tech companies, the time may have come where Congress will adopt a comprehensive federal privacy law. Complicating the adoption of a federal law will be the issue of preemption of state laws and what to do with the highly-developed sectoral laws like HIPPA and Gramm-Leach-Bliley. Also to be determined is the expansion of FTC regulatory powers. Regardless of the outcome of the debate over a new federal privacy law, the issue of the privacy and protection of personal data is unlikely to recede.

Powered by WPeMatico

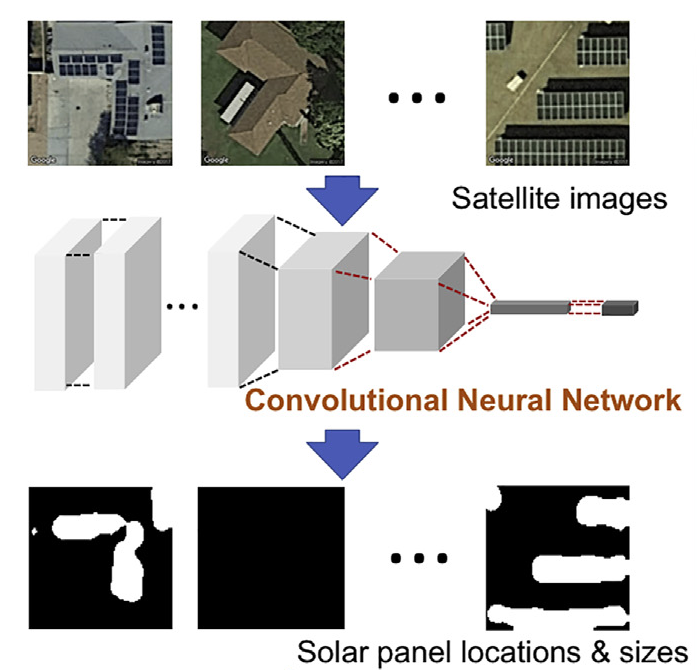

Renewable energy is the future, but at present no one is tracking just who’s got solar panels on their roof, in their back yard, or a shared neighborhood installation. Fortunately, solar panels generally work best when exposed to the light. That makes them easy to spot, and count, from orbit — which is just what the DeepSolar project is doing.

There are a number of initiatives for collecting this information — some regulated, some voluntary, some automated. But none of them is comprehensive enough or accurate enough to base policy or business decisions on at a national or state level.

Stanford engineers (mechanical and civil, respectively) Arun Majumdar and Ram Rajagopal decided to remedy this with what seems like, in retrospect, rather an obvious solution.

Machine learning systems are great at looking at images and finding objects they’ve been “trained” to recognize, whether it’s cats, faces, or cars… so why not solar panels?

Their team, including grad students Jiafan Yu and Zhecheng Wang, put together an image recognition machine learning agent trained on hundreds of thousands of satellite images. The model learns both to identify the presence of solar panels in an image, and to find the shape and area of those panels.

Having evaluated the model on nearly a hundred thousand other randomly sampled satellite images of the U.S., they found they achieved an accuracy of about 90 percent (slightly more or less depending on how it’s measured), which is well ahead of other models, and it estimated cell size with only about a 3 percent error. (Its main weakness is very small installations, Rajagopal told me, but this is partially due to the limits of the imagery.)

The team then put the model to work chewing through over a billion image tiles covering as much of the lower 48 states as they could find suitable imagery for. That excludes quite a bit of area, but consider that much of that is, for example, mountains. Not a lot of solar installations there, and few people are trying to put up cells in national parks.

All in all it’s about 6 percent of the actual country — but Rajagopal pointed out that urban areas comprise only about 3.5 percent, so this covers all of them and more. He estimated that perhaps perhaps 5 percent of installations are in the areas the system has yet to process (but is working on).

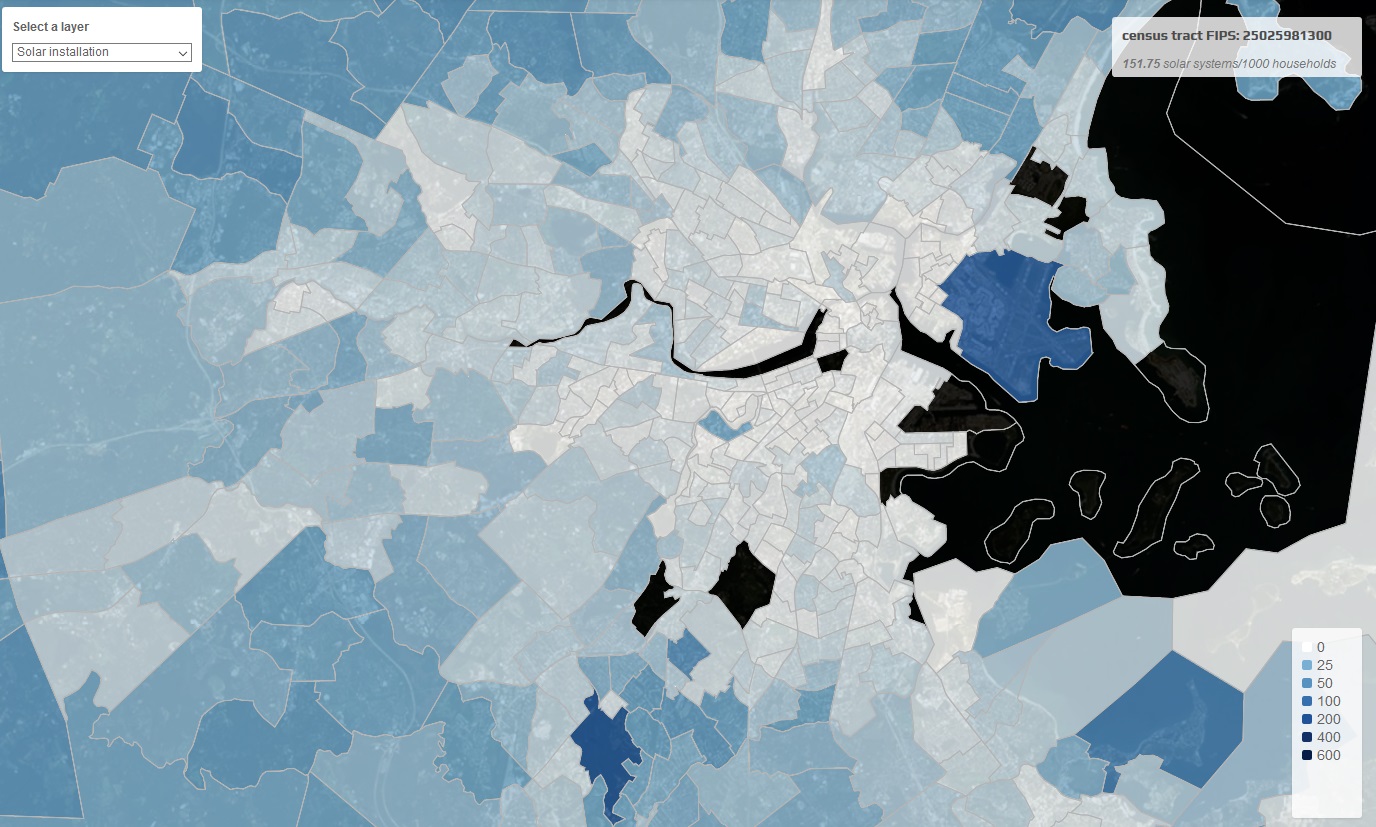

Scanning took a whole month, but at the end the model had found 1.47 million individual solar installations (which could be a few panels on a roof or a whole solar farm). That’s many more than have been counted by other efforts, and the most successful of those didn’t come with the exact location, as DeepSolar’s data does.

Basic plotting of this data produces all kinds of interesting new info. You can compare solar installation density at the state, county, census tract, or even square mile level and compare that to all kinds of other metrics — average sunny days per year, household income, voting preference, and so on.

A couple interesting findings: Only 4 percent of all census tracts (roughly 3,000 out of 75,000) had more than 100 residential-scale solar systems, meaning installations are highly concentrated. Residential solar made up 87 percent of the total installation count, but with a median size of around 25 square meters, only 34 percent of the total solar cell surface area.

Peak deployment density can be found where there are about a thousand people per square mile — think a small town or suburb, not a major city. And there’s a sort of inflection point at which people start installing: when an area receives more than 4.5 kWh per square meter per day of solar radiation. How that corresponds to weather, location, exposure and so on is a more complicated question.

This and other demographics are all good information to know if you want to invest in solar, since they basically tell you where it’s justified or needed.

“We have created and released a website where you can play with the data at the aggregated level (we are keeping it at census tract level) to respect the privacy of consumers,” Rajagopal said. “We are exploring how to make individual detections public while respecting privacy (perhaps by encouraging public participation and crowdsourcing).”

“We decided to share all of the work in open source to encourage others in industry and academia to utilize both the method as well as the data to produce more insights. We feel that changes need to happen fast, and this is one of the ways to aid in that. Perhaps in the future, services can be built around this type of data,” he continued.

Plans are underway to expand the service to the rest of the U.S. and other countries as well. The data is available to peruse here, or here as a map; the team’s paper describing the project was published today in the journal Joule.

Powered by WPeMatico

Every year I teach an MBA course at Stanford about the exciting opportunities for tech investors and entrepreneurs in developing economies. When we designed the syllabus back in 2013, Rocket Internet was still firing on all cylinders on four continents. The unapologetic machine built to copy big American internet companies created billions of dollars for the Samwer brothers and its backers. During Rocket’s golden years, the best startups in the developing economies seemed to inevitably have an original reference in Silicon Valley.

Accordingly, we added a class about the opportunity of replicating business models to seize this information arbitrage. Call it the second-mover advantage.

Despite my conviction about the model, the copycat word — short for replicating startups and attached to these ventures — annoyed me from the start. More than a term to describe a straightforward recipe to launch, I see it as an unconscious way to belittle an entire group of hard-charging founders and investors.

Indeed, while in foreign eyes, we have been building a Mexican Kickstarter, a Middle Eastern Uber, an Indian Amazon or a Colombian Postmates, I argue visionary founders are taking a simple idea that already exists and creating new worlds.

On the internet, there are Einsteins and there are Bob the Builders. I’m Bob the Builder. Oliver Samwer, founder of Rocket Internet

While impact is the final goal, founders can approach the journey in different ways. The most common approach in the startup world is to use the business method, or more pompously, the design thinking methodology. “Fall in love with the problem, not the solution,” mentors keep telling a succession of startup clusters in acceleration programs. The best and “leanest” way to product market fit is by starting small then keep iterating the solution until you nail it.

A second way to start is favored by engineers and scientists: Take a new promising technology or a forgotten molecule, then find a big problem. Keep iterating until you find a problem worth solving, like a hammer looking for a nail.

A third way is starting like painters create, building skills by copying classics, or like a new chef cooks by starting with iconic recipes: replicate a proven idea and iterate until you find traction.

Until a few years ago it was ostensibly the only way to scale in developing economies. The model helped raise local capital from risk-averse investors who needed reassurance. The playbook to scale was unfolding a couple of years ahead and served as a guide to founders without previous startup experience and no local role models. The potential acquirer was identified and sometimes contacted in advance. Founders weren’t crazy and investors weren’t dumb.

Replicating a business model has served in emerging ecosystems as the gateway to entrepreneurship and venture investing.

Photo courtesy of Flickr/A_Marga

According to conventional wisdom, new ecosystems around the world grow through the following three stages, be them in developing economies or more developed countries. First, local and foreign entrepreneurs replicate successful models focused on local markets. Then as the ecosystem evolves, founders start applying existing technologies to solve local problems. Finally, as the tech space matures, new technologies begin to flourish.

In my opinion, those stages never happen sequentially as stated by ecosystem observers. Successful startups that started with a foreign inspiration can outgrow the master. If they are not bought into submission by the first mover, some of the most famous copycats reinvented the original and made it better: Mercado Libre is much more relevant in the e-commerce space than eBay . Flipkart is hardly an Amazon, not to mention WeChat. These companies are in turn some of the most prolific tech innovators on the globe. Truly ecosystems evolve organically in unique ways reflecting their history, geopolitical environment, economic structure and cultural features.

Two ways to defend the status quo: “It’s been done before” and “It’s never been done before.” –Thibault @Kpaxs

Recently, it’s hard to hear American observers use the word copycat to describe any American company. After all, Guilt replicated VentesPrivees and Lime, Chinese dockless bike sharing and many more examples. All American startups are treated as innovators while the rest as mere followers.

Recently, Chinese or Indian startups seem to be given the benefit of the doubt regarding their originality. Is it because these regions have become more innovative? Maybe. But it’s also because these ecosystems have gained the respect of Silicon Valley. Indeed, Chinese consumer tech surpassed decisively the U.S. as the most important country in terms of investments.

So here’s my humble suggestion to our wealthier and more accomplished colleagues: stop using the c-word with founders. It’s offensive. Most probably, these founders are facing more challenges to build their companies and lower odds for success that the first mover. If anything, they have more merit than the originals.

As for founders, when they call you a me-too, remember all teams started somewhere, somehow. In fact, most started like Bob the Builder before turning into Einsteins. The truth is, it doesn’t matter where you start. You can start by applying a new technology or protocol. You can start with a problem you feel passionate about. You can start by replicating a business model. It doesn’t really matter if you take a big swing at the future and trust you will figure out how to make it happen. It doesn’t matter what label they use while you change the world for the better.

Powered by WPeMatico

Alumni Ventures Group’s (AVG) limited partners aren’t endowment or pension funds. Its typical LP is a heart surgeon in Des Moines, Iowa.

The firm has both an unorthodox model of fundraising and dealmaking. Across 25 micro funds, AVG is raising and investing upwards of $200 million per year for and in tech startups.

Tucked away in Boston, far from the limelight of Silicon Valley, few seem to be paying attention to AVG. There are a few reasons why, and those seem to be working to the firm’s advantage.

Today, AVG is announcing a close of roughly $30 million for three additional funds: Green D Ventures, Chestnut Street Ventures and Purple Arch Ventures, which represent capital committed by Dartmouth, the University of Pennsylvania and Northwestern alums, respectively.

AVG walks and talks like a venture fund, but a peek under the hood reveals its unconventional fundraising mechanisms.

Rather than collecting $5 million minimum investments from institutional LPs, AVG takes $50,000 directly from individual alums of prestigious universities. The firm pools the capital and creates university-specific venture funds for graduates of Duke, Stanford, Harvard, MIT and several other colleges.

“People don’t really know what to make of us because we’re so different,” said Michael Collins, AVG’s founder and chief executive officer.

Collins started AVG to make venture capital more accessible to individual people. He’s been a VC since 1986, formerly of TA Associates, and had grown tired of the hubris that runs rampant in the industry. In 2014, he started a $1.5 million fund for alums of his alma mater, Dartmouth. Since then, AVG has grown into 25 funds, each of which fundraise annually and are seeing substantial growth over their previous raises.

“What we observed is VC is a really good asset class but it’s really designed for institutional investors,” Collins (pictured below) said. “It’s really hard for individual people to put together a smart, simple portfolio unless they do it themselves. That’s why we created AVG.”

AVG and its team of 40 investment professionals make 150 to 200 investments per year of roughly $1 million each in U.S. startups across industries. In the second quarter of 2018, PitchBook listed the firm as the second most active global investor, ranked below only Plug and Play Tech Center and above the likes of Kleiner Perkins, NEA and Accel.

Unlike the Kleiners, NEAs and Accels of the world, AVG never leads investments. Collins says they just “tuck themselves into” a deal with a great lead investor. They don’t take board seats; Collins says he doesn’t see any value in more than one VC on a company board. And they don’t try to negotiate deal terms.

Though unusual, all of this works to their advantage. Founders appreciate the easy capital and access to AVG’s network, and other VC firms don’t view AVG as a threat, making it easier for the firm to get in on great deals.

“We are low friction, we are small and we have a hell of a Rolodex,” Collins said.

Despite a deal flow that’s unmatched by many VC firms, AVG manages to fly under the radar — and the firm is totally OK with that.

“A lot of VC is a bit of a star business where people try to build their own individual brand,” Collins said. “They get out there; they like publicity; they blog; they speak at conferences; they want to be known as the person to bring great deals to. We don’t lead. We work in the background. We just don’t feel the need to put the energy into PR.”

“Most VC returns are really achieved through investing in great companies as opposed to changing the trajectory of a company because you’re on the board,” he added. “If you’re a seed investor in Airbnb or Google, you were really great to be an early investor in that company, not because you sat on the board and you’re brilliance created Google’s success.”

AVG has completed 115 investments in the last 12 months. It’s investing out of 10-year funds, so at just four years in, it has some more waiting to do before it’ll see the full outcomes of its investments. Still, Collins says 65 of their portfolio companies have had liquidity events so far, including Jump, which sold to Uber in April, and Whistle, acquired by Mars Petcare a few years back.

“I hope that we can be a catalyst to bring more people into this asset class,” he concluded.

“I am a big believer that it’s really important that America continues to lead in entrepreneurship and I think the more people that own this asset class the better.”

Powered by WPeMatico