stablecoin

Auto Added by WPeMatico

Auto Added by WPeMatico

In the wake of Coinbase’s direct listing earlier this year, other crypto companies may be looking to go public sooner than later. That appears to be the case with Circle, a Boston-based technology company that provides API-delivered financial services and a stablecoin.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Circle will not direct list or pursue a traditional IPO. Instead, the company is combining with Concord Acquisition Corp., a SPAC, or blank-check company. The transaction values the crypto shop at an enterprise value of $4.5 billion and an equity value of around $5.4 billion.

The offering marks an interesting moment for the crypto market. Unlike Coinbase, which operates a trading platform and generates fees in a manner that is widely understood by public-market investors, Circle’s offerings are a bit more exotic.

The offering marks an interesting moment for the crypto market. Unlike Coinbase, which operates a trading platform and generates fees in a manner that is widely understood by public-market investors, Circle’s offerings are a bit more exotic.

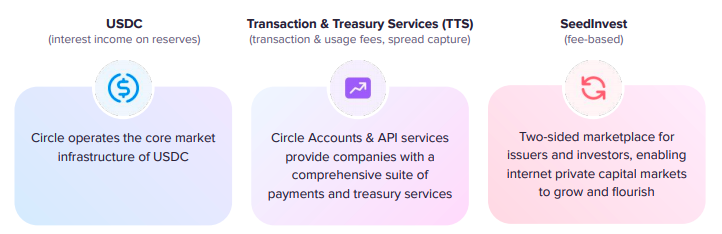

Circle’s SPAC presentation details a company whose core business deals with a stablecoin — a crypto asset pegged to an external currency, in this case, the U.S. dollar — and a set of APIs that provide crypto-powered financial services to other companies. It also owns SeedInvest, an equity crowdfunding platform, though Circle appears to generate the bulk of its anticipated revenues from its other businesses.

For more on the deal itself, TechCrunch’s Romain Dillet has a piece focused on the transaction. Here, we’ll dig into the company’s investor presentation, talk about its business model, and riff on its historical and anticipated results and valuation multiples.

In short, we get to have a little fun. Let’s begin.

As noted above, Circle has three main business operations. Here’s how it describes them in its deck:

Image Credits: Circle investor presentation

Let’s consider each one, starting with USDC.

Stablecoins have become popular in recent quarters. Because they are pegged to an external currency, they operate as an interesting form of cash inside the crypto world. If you want to have on-chain buying power, but don’t want to have all your value stored in more volatile, and tax-inducing, cryptos that you might have to sell to buy anything else, stablecoins can operate as a more stable sort of liquid currency. They can combine the stability of the U.S. dollar, say, and the crypto world’s interesting financial web.

Powered by WPeMatico

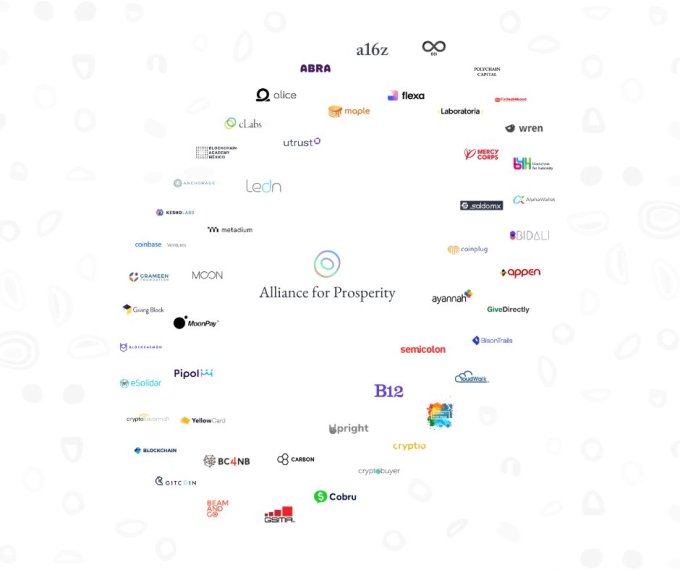

Some Libra Association members like Andreessen Horowitz and Coinbase Ventures are double-dipping, backing a competing cryptocurrency developer platform. Launching today with over 50 partners, non-profit The Celo Foundation’s ‘Alliance For Prosperity’ offers a way for developers to build decentralized mobile apps that are based on Celo’s blockchain platform and USD stablecoin.

The open-source Celo platform is still in testing with plans to officially launch its mainnet in April. The non-profit founded in 2017 has raised $36.4 million, including its Series A where Andreessen Horowitz’s a16z Crypto bought $15 million worth of Celo Gold tokens.

The biggest differentiator of Celo’s network versus other blockchains is that payments in the Celo Dollar stablecoin can be sent to people’s phone numbers rather than complicated addresses. The goal is to make delivering utility via blockchain easier by building a flexible network of applications that doesn’t scare regulators like Libra has.

The Alliance For Prosperity includes Andreessen Horowitz (which funded Celo), Coinbase (Ventures), Bison Trails, Anchorage, and Mercy Corps — all of which are also Libra Association members. That could potentially create a conflict of interest regarding which cryptocurrency and developer platform they promote to their portfolio companies, integrate into their products, or focus on for delivering financial services to the needy.

Other high-profile Alliance partners include Carbon, GiveDirectly, Grameen Foundation, Maple, and Polychain. Partners have made a somewhat vague commitment to “backing development efforts of the project, building infrastructure, implementing desired use cases on the platform, integrating Celo assets in their projects, or collaborating on education campaigns in their communities to further advance the use of blockchain technology” according to Chuck Kimble, Celo’s cLabs head of business development and head of the Alliance. Anyone can apply to join the open network, and there’s no minimum financial investment like Libra’s $10 million prerequisite.

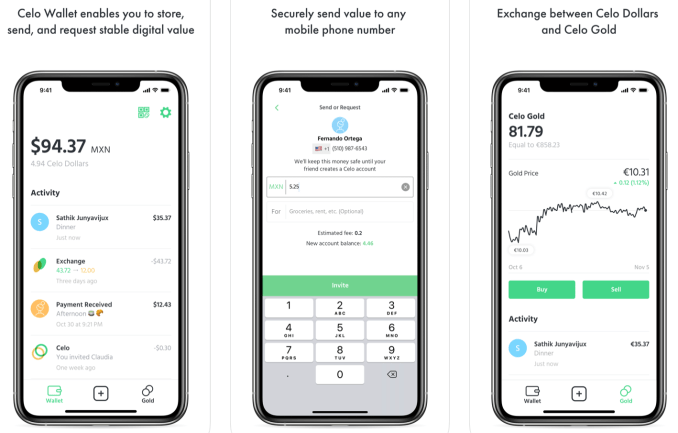

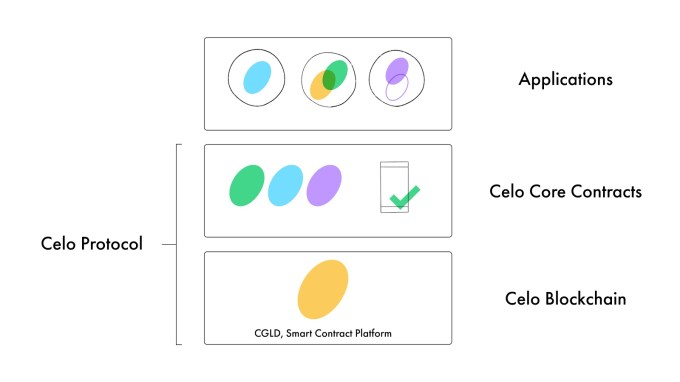

Celo isn’t trying to replace the dollar with its own synthetic currency, and its reserve is backed with other cryptocurrencies rather than fiat cash. That might make it more acceptable to regulators who were worried that Libra’s token and fiat currency bundle-backed reserve could impact the global financial system. The first of the decentralized apps on the platform, the Celo Wallet, is already available for iOS and Android.

Like many blockchain projects, there are some lofty intentions for social impact with Celo. Use cases include “powering mobile and online work, enabling faster and affordable remittances, reducing the operational complexities of delivering humanitarian aid, facilitating payments, and enabling microlending” says Kimble. The real driver of this potential is Celo’s promise of much lower transaction fees than traditional middlemen charge.

When asked what the biggest threats to Celo’s success are, he told me “Banking infrastructure improving faster than we expect” and “Mobile adoption or LTE data not expanding on their current trajectory.” He did not mention the developer fatigue, regulatory scrutiny, technical complexity, or slow adoption of blockchain utilities that have plagued other crypto for good projects.

Here’s the full list of members working towards these goals:

Abra, Alice, AlphaWallet, Anchorage, Appen, Ayannah, Andreessen Horowitz, B12, BC4NB (Blockchain for the Next Billion), BeamAndGo, Bidali, Bison Trails, Blockchain Academy Mexico, Blockchain.com, Blockchain for Humanity (b4h), Blockchain for Social Impact (BSIC), Blockdaemon, Carbon, cLabs, CloudWalk Inc, Cobru, Coinbase, Coinplug, Cryptio, Cryptobuyer, CryptoSavannah, eSolidar, Fintech4Good, Flexa, Gitcoin, GiveDirectly, Grameen Foundation, GSMA, KeshoLabs, Laboratoria, Ledn, Maple, Mercy Corps, Metadium, Moon, MoonPay, Pipol, Pngme, Polychain, Project Wren, SaldoMX, Semicolon Africa, The Giving Block, Utrust, Upright, Yellow Card, and 88i. [Update: Ledger joined this morning.]

“Many of these organizations have on-the-ground operations that will begin to get Celo into the hands of those who have been underserved by the current global financial system” Andreessen Horowitz general partner Katie Haun told me. “Our hope is that this partnership will start unlocking the potential of internet money”. To spur adoption, the Alliance will distribute ‘Prosperity Gifts’ in the form of financial grants to developers proposing Celo products that would benefit society.

There are also some peculiar characteristics of Celo’s system. People exchange other cryptocurrencies for Celo Gold, then exchange that for Celo Dollars they can spend. The reserve is backed with other cryptocurrencies like bitcoin and ethereum rather that fiat, and isn’t fully collateralized. That could make it vulnerable to a Celo bank run or crash in price of those currencies. Celo also lets arbitrageurs pocket the difference if Celo Gold and Celo Dollars get out of sync.

While it might not be a danger to the world financial system like Libra, it could be a danger to itself. At least on the anti-money laundering front, cLabs — the team that’s kicking off development of the Celo platform — has hired former Capital One head of enterprise risk management Jai Ramaswamy. Plus, the Celo founders come well pedigreed, including Marek Olszewski and Rene Reinsberg who spun out machine learning startup Locu from MIT and sold it to GoDaddy, as well as EigenTrust inventor and former MIT Media Lab professor Sep Kamvar.

While it might not be a danger to the world financial system like Libra, it could be a danger to itself. At least on the anti-money laundering front, cLabs — the team that’s kicking off development of the Celo platform — has hired former Capital One head of enterprise risk management Jai Ramaswamy. Plus, the Celo founders come well pedigreed, including Marek Olszewski and Rene Reinsberg who spun out machine learning startup Locu from MIT and sold it to GoDaddy, as well as EigenTrust inventor and former MIT Media Lab professor Sep Kamvar.

So far, 130 teams have expressed interest in building on the Celo platform. For reference, Libra said 1,500 organizations had said they wanted to work on that project four months after its reveal. Celo Camp and Blockchain for Social Impact Incubator will also be fostering projects for the blockchain.

Celo could make banking cheaper and more accessible while power new fintech innovation. But for any of that to happen, it will need to get enough developers building truly useful products, make the blockchain and currency exchange simple enough for mainstream audiences in developing nations, and grow adoption to meaningful levels few cryptocurrency projects have yet achieved. The Alliance For Prosperity will have to throw their weight into this project, not just their names, if it’s going to succeed.

Powered by WPeMatico

After eBay, Visa, Stripe and other high-profile partners ditched the Facebook -backed cryptocurrency collective, Libra scored a win today with the addition of Shopify. The e-commerce platform will become a member of Libra Association, contributing at least $10 million and operating a node that processes transactions for the Facebook-originated stable coin.

If Libra manages to assuage international regulators’ concerns, which are currently blocking its roll out, Shopify could gain a way to process transactions without paying credit card fees. Libra is designed to move between wallets with zero or nearly-zero fees. That could save money for Shopify and the 1 million merchants running online shops on its platform.

Shopify stressed that helping merchants reduce fees and bringing commerce opportunities to developing nations as reasons it’s joining the Libra Association . “Much of the world’s financial infrastructure was not built to handle the scale and needs of internet commerce,” Shopify writes. Here are the most critical parts of its announcement:

Our mission is to make commerce better for everyone and to do that, we spend a lot of our time thinking about how to make commerce better in parts of the world where money and banking could be far better . . . As a member of the Libra Association, we will work collectively to build a payment network that makes money easier to access and supports merchants and consumers everywhere . . . Our mission has always been to support the entrepreneurial journey of the more than one million merchants on our platform. That means advocating for transparent fees and easy access to capital, and ensuring the security and privacy of our merchants’ customer data. We want to create an infrastructure that empowers more entrepreneurs around the world.

As part of the Libra Association, Shopify will become a validator node operator, gain one vote on the Libra Association council and can earn dividends from interest earned on the Libra reserve in proportion to its investment, which is $10 million at a minimum.

The Libra Association had lost much of its e-commerce expertise when a string of members abandoned the project in October amidst regulatory scrutiny. That included traditional payment processors like Visa and Mastercard, online processors like Stripe and PayPal and marketplaces like eBay. That threw into question whether Libra would have the right partners to make the cryptocurrency accepted in enough places to be useful to people.

As it works to convince regulators Libra is safe, Facebook has been working on its other payment plays, including Facebook Pay and WhatsApp Pay, that rely on traditional bank transfers or credit cards.

Shopify’s CEO Tobi Lutke tweeted that “Shopify spends a lot of time thinking about how to make commerce better in parts of the world where money and banking could be far better. That’s why we decided to become a member of the Libra Association.”

“We are proud to welcome Shopify, Inc. (SHOP) to the Libra Association. As a multinational commerce platform with over one million businesses in approximately 175 countries, Shopify, Inc. brings a wealth of knowledge and expertise to the Libra project,” writes Dante Disparte, the Libra Association’s head of Policy and Communications. “Shopify joins an active group of Libra Association members committed to achieving a safe, transparent, and consumer-friendly implementation of a global payment system that breaks down financial barriers for billions of people.”

A recent hire further tied the two companies together. Facebook’s former lead product manager for its payment platform and billing teams, Kaz Nejatian, in September became Shopify’s VP and GM of money.

Operating an e-commerce store can be difficult or impossible without a traditional bank account that can be tough to attain in some developing countries. Libra could allow these merchants to establish a Libra Wallet where payments are sent instantly, without steep credit card fees, and in theory could be cashed out at local brick-and-mortar establishments or ATMs for local fiat currency.

Shopify’s credit card readers

But for any of that to happen, the Libra Association will have to convince the U.S. government, the EU and more that it won’t help terrorists launder money, hurt people’s privacy or weaken nations’ power in the global financial system. “The French Finance Minister Bruno Le Maire said, “the monetary sovereignty of countries is at stake from a possible privatisation of money . . . we cannot authorise the development of Libra on European soil.”

Libra was initially slated to launch in 2020. We’ll see.

—

Here’s the full list of Libra Association members:

Current

Facebook’s Calibra, Shopify, PayU, Farfetch, Lyft, Spotify, Uber, Illiad SA, Anchorage, Bison Trails, Coinbase, Xapo, Andreessen Horowitz, Union Square Ventures, Breakthrough Initiatives, Ribbit Capital, Thrive Capital, Creative Destruction Lab, Kiva, Mercy Corps, Women’s World Banking.

Former members

Vodafone, Visa, Mastercard, Stripe, PayPal, Mercado Pago, Bookings Holdings, eBay.

Powered by WPeMatico

Facebook has finally revealed the details of its cryptocurrency, Libra, which will let you buy things or send money to people with nearly zero fees. You’ll pseudonymously buy or cash out your Libra online or at local exchange points like grocery stores, and spend it using interoperable third-party wallet apps or Facebook’s own Calibra wallet that will be built into WhatsApp, Messenger and its own app. Today Facebook released its white paper explaining Libra and its testnet for working out the kinks of its blockchain system before a public launch in the first half of 2020.

Facebook won’t fully control Libra, but instead get just a single vote in its governance like other founding members of the Libra Association, including Visa, Uber and Andreessen Horowitz, which have invested at least $10 million each into the project’s operations. The association will promote the open-sourced Libra Blockchain and developer platform with its own Move programming language, plus sign up businesses to accept Libra for payment and even give customers discounts or rewards.

Facebook is launching a subsidiary company also called Calibra that handles its crypto dealings and protects users’ privacy by never mingling your Libra payments with your Facebook data so it can’t be used for ad targeting. Your real identity won’t be tied to your publicly visible transactions. But Facebook/Calibra and other founding members of the Libra Association will earn interest on the money users cash in that is held in reserve to keep the value of Libra stable.

Facebook’s audacious bid to create a global digital currency that promotes financial inclusion for the unbanked actually has more privacy and decentralization built in than many expected. Instead of trying to dominate Libra’s future or squeeze tons of cash out of it immediately, Facebook is instead playing the long-game by pulling payments into its online domain. Facebook’s VP of blockchain, David Marcus, explained the company’s motive and the tie-in with its core revenue source during a briefing at San Francisco’s historic Mint building. “If more commerce happens, then more small businesses will sell more on and off platform, and they’ll want to buy more ads on the platform so it will be good for our ads business.”

In cryptocurrencies, Facebook saw both a threat and an opportunity. They held the promise of disrupting how things are bought and sold by eliminating transaction fees common with credit cards. That comes dangerously close to Facebook’s ad business that influences what is bought and sold. If a competitor like Google or an upstart built a popular coin and could monitor the transactions, they’d learn what people buy and could muscle in on the billions spent on Facebook marketing. Meanwhile, the 1.7 billion people who lack a bank account might choose whoever offers them a financial services alternative as their online identity provider too. That’s another thing Facebook wants to be.

Yet existing cryptocurrencies like Bitcoin and Ethereum weren’t properly engineered to scale to be a medium of exchange. Their unanchored price was susceptible to huge and unpredictable swings, making it tough for merchants to accept as payment. And cryptocurrencies miss out on much of their potential beyond speculation unless there are enough places that will take them instead of dollars, and the experience of buying and spending them is easy enough for a mainstream audience. But with Facebook’s relationship with 7 million advertisers and 90 million small businesses plus its user experience prowess, it was well-poised to tackle this juggernaut of a problem.

Now Facebook wants to make Libra the evolution of PayPal . It’s hoping Libra will become simpler to set up, more ubiquitous as a payment method, more efficient with fewer fees, more accessible to the unbanked, more flexible thanks to developers and more long-lasting through decentralization.

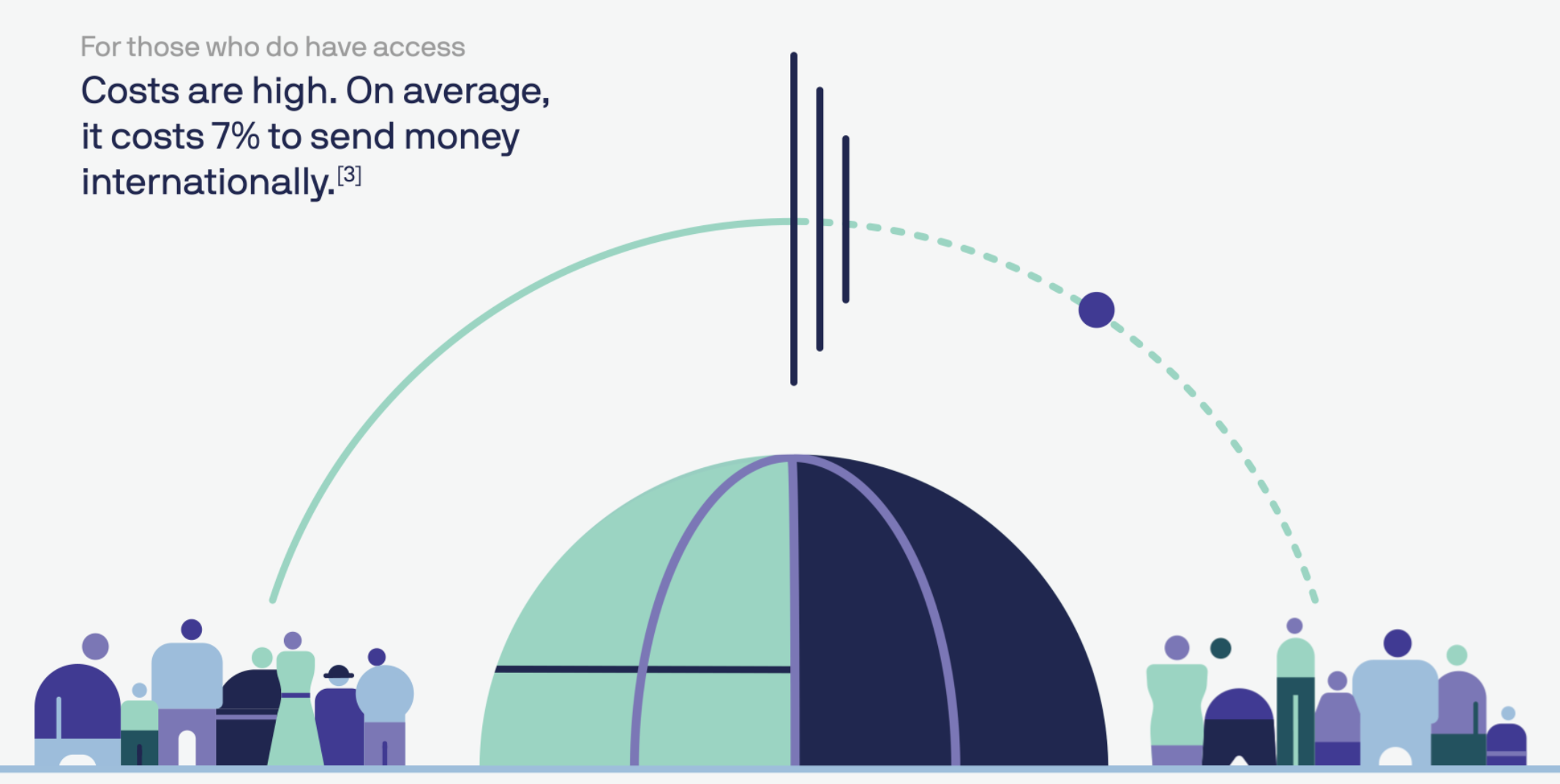

“Success will mean that a person working abroad has a fast and simple way to send money to family back home, and a college student can pay their rent as easily as they can buy a coffee,” Facebook writes in its Libra documentation. That would be a big improvement on today, when you’re stuck paying rent in insecure checks while exploitative remittance services charge an average of 7% to send money abroad, taking $50 billion from users annually. Libra could also power tiny microtransactions worth just a few cents that are infeasible with credit card fees attached, or replace your pre-paid transit pass.

…Or it could be globally ignored by consumers who see it as too much hassle for too little reward, or too unfamiliar and limited in use to pull them into the modern financial landscape. Facebook has built a reputation for over-engineered, underused products. It will need all the help it can get if wants to replace what’s already in our pockets.

By now you know the basics of Libra. Cash in a local currency, get Libra, spend them like dollars without big transaction fees or your real name attached, cash them out whenever you want. Feel free to stop reading and share this article if that’s all you care about. But the underlying technology, the association that governs it, the wallets you’ll use and the way payments work all have a huge amount of fascinating detail to them. Facebook has released more than 100 pages of documentation on Libra and Calibra, and we’ve pulled out the most important facts. Let’s dive in.

Facebook knew people wouldn’t trust it to wholly steer the cryptocurrency they use, and it also wanted help to spur adoption. So the social network recruited the founding members of the Libra Association, a not-for-profit which oversees the development of the token, the reserve of real-world assets that gives it value and the governance rules of the blockchain. “If we were controlling it, very few people would want to jump on and make it theirs,” says Marcus.

Each founding member paid a minimum of $10 million to join and optionally become a validator node operator (more on that later), gain one vote in the Libra Association council and be entitled to a share (proportionate to their investment) of the dividends from interest earned on the Libra reserve into which users pay fiat currency to receive Libra.

The 28 soon-to-be founding members of the association and their industries, previously reported by The Block’s Frank Chaparro, include:

Facebook says it hopes to reach 100 founding members before the official Libra launch and it’s open to anyone that meets the requirements, including direct competitors like Google or Twitter. The Libra Association is based in Geneva, Switzerland and will meet biannually. The country was chosen for its neutral status and strong support for financial innovation including blockchain technology.

To join the association, members must have a half rack of server space, a 100Mbps or above dedicated internet connection, a full-time site reliability engineer and enterprise-grade security. Businesses must hit two of three thresholds of a $1 billion USD market value or $500 million in customer balances, reach 20 million people a year and/or be recognized as a top 100 industry leader by a group like Interbrand Global or the S&P.

Crypto-focused investors must have more than $1 billion in assets under management, while Blockchain businesses must have been in business for a year, have enterprise-grade security and privacy and custody or staking greater than $100 million in assets. And only up to one-third of founding members can by crypto-related businesses or individually invited exceptions. Facebook also accepts research organizations like universities, and nonprofits fulfilling three of four qualities, including working on financial inclusion for more than five years, multi-national reach to lots of users, a top 100 designation by Charity Navigator or something like it and/or $50 million in budget.

The Libra Association will be responsible for recruiting more founding members to act as validator nodes for the blockchain, fundraising to jump-start the ecosystem, designing incentive programs to reward early adopters and doling out social impact grants. A council with a representative from each member will help choose the association’s managing director, who will appoint an executive team and elect a board of five to 19 top representatives.

Each member, including Facebook/Calibra, will only get up to one vote or 1% of the total vote (whichever is larger) in the Libra Association council. This provides a level of decentralization that protects against Facebook or any other player hijacking Libra for its own gain. By avoiding sole ownership and dominion over Libra, Facebook could avoid extra scrutiny from regulators who are already investigating it for a sea of privacy abuses as well as potentially anti-competitive behavior. In an attempt to preempt criticism from lawmakers, the Libra Association writes, “We welcome public inquiry and accountability. We are committed to a dialogue with regulators and policymakers. We share policymakers’ interest in the ongoing stability of national currencies.”

A Libra is a unit of the Libra cryptocurrency that’s represented by a three wavy horizontal line unicode character ≋ like the dollar is represented by $. The value of a Libra is meant to stay largely stable, so it’s a good medium of exchange, as merchants can be confident they won’t be paid a Libra today that’s then worth less tomorrow. The Libra’s value is tied to a basket of bank deposits and short-term government securities for a slew of historically stable international currencies, including the dollar, pound, euro, Swiss franc and yen. The Libra Association maintains this basket of assets and can change the balance of its composition if necessary to offset major price fluctuations in any one foreign currency so that the value of a Libra stays consistent.

A Libra is a unit of the Libra cryptocurrency that’s represented by a three wavy horizontal line unicode character ≋ like the dollar is represented by $. The value of a Libra is meant to stay largely stable, so it’s a good medium of exchange, as merchants can be confident they won’t be paid a Libra today that’s then worth less tomorrow. The Libra’s value is tied to a basket of bank deposits and short-term government securities for a slew of historically stable international currencies, including the dollar, pound, euro, Swiss franc and yen. The Libra Association maintains this basket of assets and can change the balance of its composition if necessary to offset major price fluctuations in any one foreign currency so that the value of a Libra stays consistent.

The name Libra comes from the word for a Roman unit of weight measure. It’s trying to invoke a sense of financial freedom by playing on the French stem “Lib,” meaning free.

The Libra Association is still hammering out the exact start value for the Libra, but it’s meant to be somewhere close to the value of a dollar, euro or pound so it’s easy to conceptualize. That way, a gallon of milk in the U.S. might cost 3 to 4 Libra, similar but not exactly the same as with dollars.

The idea is that you’ll cash in some money and keep a balance of Libra that you can spend at accepting merchants and online services. You’ll be able to trade in your local currency for Libra and vice versa through certain wallet apps, including Facebook’s Calibra, third-party wallet apps and local resellers like convenience or grocery stores where people already go to top-up their mobile data plan.

Each time someone cashes in a dollar or their respective local currency, that money goes into the Libra Reserve and an equivalent value of Libra is minted and doled out to that person. If someone cashes out from the Libra Association, the Libra they give back are destroyed/burned and they receive the equivalent value in their local currency back. That means there’s always 100% of the value of the Libra in circulation, collateralized with real-world assets in the Libra Reserve. It never runs fractional. And unliked “pegged” stable coins that are tied to a single currency like the USD, Libra maintains its own value — though that should cash out to roughly the same amount of a given currency over time.

When Libra Association members join and pay their $10 million minimum, they receive Libra Investment Tokens. Their share of the total tokens translates into the proportion of the dividend they earn off of interest on assets in the reserve. Those dividends are only paid out after Libra Association uses interest to pay for operating expenses, investments in the ecosystem, engineering research and grants to nonprofits and other organizations. This interest is part of what attracted the Libra Association’s members. If Libra becomes popular and many people carry a large balance of the currency, the reserve will grow huge and earn significant interest.

Every Libra payment is permanently written into the Libra Blockchain — a cryptographically authenticated database that acts as a public online ledger designed to handle 1,000 transactions per second. That would be much faster than Bitcoin’s 7 transactions per second or Ethereum’s 15. The blockchain is operated and constantly verified by founding members of the Libra Association, which each invested $10 million or more for a say in the cryptocurrency’s governance and the ability to operate a validator node.

When a transaction is submitted, each of the nodes runs a calculation based on the existing ledger of all transactions. Thanks to a Byzantine Fault Tolerance system, just two-thirds of the nodes must come to consensus that the transaction is legitimate for it to be executed and written to the blockchain. A structure of Merkle Trees in the code makes it simple to recognize changes made to the Libra Blockchain. With 5KB transactions, 1,000 verifications per second on commodity CPUs and up to 4 billion accounts, the Libra Blockchain should be able to operate at 1,000 transactions per second if nodes use at least 40Mbps connections and 16TB SSD hard drives.

Transactions on Libra cannot be reversed. If an attack compromises over one-third of the validator nodes causing a fork in the blockchain, the Libra Association says it will temporarily halt transactions, figure out the extent of the damage and recommend software updates to resolve the fork.

Transactions aren’t entirely free. They incur a tiny fraction of a cent fee to pay for “gas” that covers the cost of processing the transfer of funds similar to with Ethereum. This fee will be negligible to most consumers, but when they add up, the gas charges will deter bad actors from creating millions of transactions to power spam and denial-of-service attacks. “We’ve purposely tried not to innovate massively on the blockchain itself because we want it to be scalable and secure,” says Marcus of piggybacking on the best elements of existing cryptocurrencies.

Currently, the Libra Blockchain is what’s known as “permissioned,” where only entities that fulfill certain requirements are admitted to a special in-group that defines consensus and controls governance of the blockchain. The problem is this structure is more vulnerable to attacks and censorship because it’s not truly decentralized. But during Facebook’s research, it couldn’t find a reliable permissionless structure that could securely scale to the number of transactions Libra will need to handle. Adding more nodes slows things down, and no one has proven a way to avoid that without compromising security.

That’s why the Libra Association’s goal is to move to a permissionless system based on proof-of-stake that will protect against attacks by distributing control, encourage competition and lower the barrier to entry. It wants to have at least 20% of votes in the Libra Association council coming from node operators based on their total Libra holdings instead of their status as a founding member. That plan should help appease blockchain purists who won’t be satisfied until Libra is completely decentralized.

The Libra Blockchain is open source with an Apache 2.0 license, and any developer can build apps that work with it using the Move coding language. The blockchain’s prototype launches its testnet today, so it’s effectively in developer beta mode until it officially launches in the first half of 2020. The Libra Association is working with HackerOne to launch a bug bounty system later this year that will pay security researchers for safely identifying flaws and glitches. In the meantime, the Libra Association is implementing the Libra Core using the Rust programming language because it’s designed to prevent security vulnerabilities, and the Move language isn’t fully ready yet.

Move was created to make it easier to write blockchain code that follows an author’s intent without introducing bugs. It’s called Move because its primary function is to move Libra coins from one account to another, and never let those assets be accidentally duplicated. The core transaction code looks like: LibraAccount.pay_from_sender(recipient_address, amount) procedure.

Eventually, Move developers will be able to create smart contracts for programmatic interactions with the Libra Blockchain. Until Move is ready, developers can create modules and transaction scripts for Libra using Move IR, which is high-level enough to be human-readable but low-level enough to be translatable into real Move bytecode that’s written to the blockchain.

The Libra ecosystem and the Move language will be completely open to use and build, which presents a sizable risk. Crooked developers could prey on crypto novices, claiming their app works just the same as legitimate ones, and that it’s safe because it uses Libra. But if consumers get ripped off by these scammers, the anger will surely bubble up to Facebook. Yet still, Calibra’s head of product tells me, “There are no plans for the Libra Association to take a role in actively vetting [developers],” Calibra’s head of product Kevin Weil tells me.

Even though it’s tried to distance itself sufficiently via its subsidiary Libra and the association, many people will probably always think of Libra as Facebook’s cryptocurrency and blame it for their woes.

Read our full story on the dangers of Libra’s unvetted developer platform

The Libra Association wants to encourage more developers and merchants to work with its cryptocurrency. That’s why it plans to issue incentives, possibly Libra coins, to validator node operators who can get people signed up for and using Libra. Wallets that pull users through the Know Your Customer anti-fraud and money laundering process or that keep users sufficiently active for over a year will be rewarded. For each transaction they process, merchants will also receive a percentage of the transaction back.

Businesses that earn these incentives can keep them, or pass some or all of them along to users in the form of free Libra tokens or discounts on their purchases. This could create competition between wallets to see which can pass on the most rewards to their customers, and thereby attract the most users. You could imagine eBay or Spotify giving you a discount for paying in Libra, while wallet developers might offer you free tokens if you complete 100 transactions within a year.

“One challenge for Spotify and its users around the world has been the lack of easily accessible payment systems – especially for those in financially underserved markets,” Spotify’s Chief Premium Business Officer Alex Norström writes. “In joining the Libra Association, there is an opportunity to better reach Spotify’s total addressable market, eliminate friction and enable payments in mass scale.”

This savvy incentive system should massively help ratchet up Libra’s user count without dictating how businesses balance their margins versus growth. Facebook also has another plan to grow its developer ecosystem. By offering venture capital firms like Andreessen Horowitz and Union Square Ventures a portion of the reserve interest, they’re motivating to fund startups building Libra infrastructure.

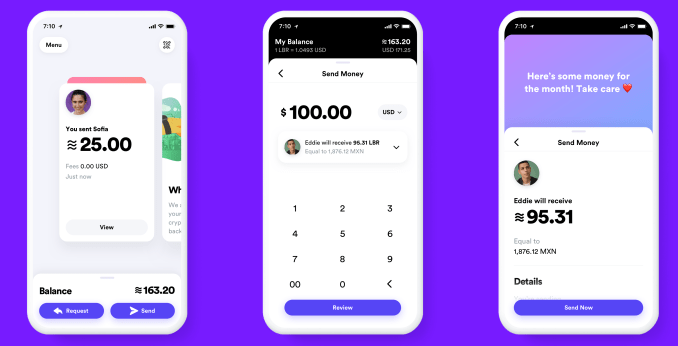

So how do you actually own and spend Libra? Through Libra wallets like Facebook’s own Calibra and others that will be built by third-parties, potentially including Libra Association members like PayPal. The idea is to make sending money to a friend or paying for something as easy as sending a Facebook Message. You won’t be able to make or receive any real payments until the official launch next year, though, but you can sign up for early access when it’s ready here.

None of the Libra Association members agreed to provide details on what exactly they’ll build on the blockchain, but we can take Facebook’s Calibra wallet as an example of the basic experience. Calibra will launch alongside the Libra currency on iOS and Android within Facebook Messenger, WhatsApp and a standalone app. When users first sign up, they’ll be taken through a Know Your Customer anti-fraud process where they’ll have to provide a government-issued photo ID and other verification info. They’ll need to conduct due diligence on customers and report suspicious activity to the authorities.

From there you’ll be able to cash in to Libra, pick a friend or merchant, set an amount to send them and add a description and send them Libra. You’ll also be able to request Libra, and Calibra will offer an expedited way of paying merchants by scanning your or their QR code. Eventually it wants to offer in-store payments and integrations with point-of-sale systems like Square.

The Libra Association’s e-commerce members seem particularly excited about how the token could eliminate transaction fees and speed up checkout. “We believe blockchain will benefit the luxury industry by improving IP protection, transparency in the product life cycle and — as in the case of Libra — enable global frictionless e-commerce,” says FarFetch CEO Jose Neves.

Facebook CEO Mark Zuckerberg explained some of the philosophy behind Libra and Calibra in a post today. “It’s decentralized — meaning it’s run by many different organizations instead of just one, making the system fairer overall. It’s available to anyone with an internet connection and has low fees and costs. And it’s secured by cryptography which helps keep your money safe. This is an important part of our vision for a privacy-focused social platform — where you can interact in all the ways you’d want privately, from messaging to secure payments.”

By default, Facebook won’t import your contacts or any of your profile information, but may ask if you wish to do so. It also won’t share any of your transaction data back to Facebook, so it won’t be used to target you with ads, rank your News Feed, or otherwise earn Facebook money directly. Data will only be shared in specific instances in anonymized ways for research or adoption measurement, for hunting down fraudsters or due to a request from law enforcement. And you don’t even need a Facebook or WhatsApp account to sign up for Calibra or to use Libra.

“We realize people don’t want their social data and financial data commingled,” says Marcus, who’s now head of Calibra. “The reality is we’ll have plenty of wallets that will compete with us and many of them will not be in social, and if we want to successfully win people’s trust, we have to make sure the data will be separated.”

In case you are hacked, scammed or lose access to your account, Calibra will refund you for lost coins when possible through 24/7 chat support because it’s a custodial wallet. You also won’t have to remember any long, complex crypto passwords you could forget and get locked out from your money, as Calibra manages all your keys for you. Given Calibra will likely become the default wallet for many Libra users, this extra protection and smoother user experience is essential.

For now, Calibra won’t make money. But Calibra’s head of product Kevin Weil tells me that if it reaches scale, Facebook could launch other financial tools through Calibra that it could monetize, such as investing or lending. “In time, we hope to offer additional services for people and businesses, such as paying bills with the push of a button, buying a cup of coffee with the scan of a code or riding your local public transit without needing to carry cash or a metro pass,” the Calibra team writes. That makes it start to sound a lot like China’s everything app WeChat.

Facebook got one thing right for sure: Today’s money doesn’t work for everyone. Those of us living comfortably in developed nations likely don’t see the hardships that befall migrant workers or the unbanked abroad. Preyed on by greedy payday lenders and high-fee remittance services, targeted by muggers and left out of traditional financial services, the poor get poorer. Libra has the potential to get more money from working parents back to their families and help people retain credit even if they’re robbed of their physical possessions. That would do more to accomplish Facebook’s mission of making the world feel smaller than all the News Feed Likes combined.

If Facebook succeeds and legions of people cash in money for Libra, it and the other founding members of the Libra Association could earn big dividends on the interest. And if suddenly it becomes super quick to buy things through Facebook using Libra, businesses will boost their ad spend there. But if Libra gets hacked or proves unreliable, it could cost lots of people around the world money while souring them on cryptocurrencies. And by offering an open Libra platform, shady developers could build apps that snatch not just people’s personal info like Cambridge Analytica, but their hard-earned digital cash.

Facebook just tried to reinvent money. Next year, we’ll see if the Libra Association can pull it off. It took me 4,000 words to explain Libra, but at least now you can make up your own mind about whether to be scared of Facebook crypto.

Powered by WPeMatico

Facebook is finally ready to reveal details about its cryptocurrency codenamed Libra. It’s currently scheduled for a June 18th release of a white paper explaining its cryptocurrency’s basics, according to a source who says multiple investors briefed on the project by Facebook were told that date.

Meanwhile, the company’s Head of Financial Services & Payment Partnerships for Northern Europe Laura McCracken told German magazine WirtschaftsWoche‘s Sebastian Kirsch that the white paper would debut June 18th, and that the cryptocurrency would indeed be pegged to a basket of currencies rather than a single one like the US dollar to prevent price fluctuations. Kirsch tells me “I met Laura at Money2020 Europe in Amsterdam on Tuesday” after she watched fellow Facebook payments exec Paulette Rowe’s talk. “She told me that she wasn’t involved in what David Marcus’ [Facebook Blockchain] team was doing. But that I’d have to wait until June 18th when a whitepaper was supposed to be published to get more details.” She told him she thought the date was already a publicly known fact, which it wasn’t.

Then, yesterday TechCrunch received a request for a June 18th news embargo from one of the communications managers for Facebook’s blockchain team. The Information’s Alex Heath and Jon Victor also reported yesterday that Facebook’s cryptocurrency project would launch later this month.

Facebook declined to comment on any news regarding its cryptocurrency project. There is always a chance that the announcement date could fluctuate if snafus with partners or governments arise. One source says Facebook is targeting a 2020 formal launch of the cryptocurrency

The debut of Libra or whatever Facebook decides to call it could unlock a new era of commerce and payments for the social network. It could be used to offer low or no-fee payments between friends or remittance of earnings to familys from migrant workers abroad who are often gouged by money transfer services.

Sidestepping credit card transaction fees could also allow Facebook’s cryptocurrency to offer a cheaper way to pay merchants for traditional ecommerce, or facilitate microtransactions for a la carte news articles or tipping of content creators. And a better understanding of who buys what or which brands or popular could aid Facebook in ad measurement, ranking, and targeting to amplify its core business.

Here’s what we know about Facebook’s blockchain project:

Name: Facebook will likely use the Libra codename as the public facing name for its cryptocurrency, which The Information reports won’t be called GlobalCoin as the BBC had claimed. Facebook has registed a company called Libra Networks in Switzerland for financial services, Reuters reported. Libra could be a play on the word LIBOR, an abbreviation for the London Inter-bank Offered Rate that’s used as a benchmark interest rate for borrowing between banks. LIBOR is for banks, while Libra is meant to be for the people.

Token: The cryptocurrency will be a stablecoin — a token designed to have a stable price to prevent discrepancies and complications due to price fluctuations during a payment or negotiation process. Facebook has spoken with financial institutions regarding contributing capital to form a $1 billion basket of multiple international fiat currencies and low-risk securities that will serve as collateral to stabilize the price of the coin, The Information reports. Facebook is working with various countries to pre-approve the rollout of the stablecoin.

The head of Facebook’s Blockchain team David Marcus (left) speaks at TechCrunch Disrupt 2016

Usage: Facebook’s cryptocurrency will be transferrable with zero fees via Facebook products including Messenger and WhatsApp. Facebook is working with merchants to accept the token as payment, and may offer sign-up bonuses. The Information also reports Facebook also wants to roll out physical devices for ATMs so users can exchange traditional assets for the cryptocurrency.

Team: Facebook’s blockchain project is overseen by former PayPal President and VP of Facebook Messenger David Marcus. His team includes former Instagram VP of product Kevin Weil, Facebook’s former corporate head of treasury operations Sunita Parasuraman who The Information reports will oversee the token’s treasury, and many elite engineers cherrypicked from Facebook’s ranks. They’ve been working in a dedicated part of Facebook’s headquarters off-limits to other employees to boost secrecy, though the nature of the partnerships needed for launch have led to many leaks.

Governance: Facebook is in talks to create an independent foundation to oversee its cryptocurrency, The Information reports. It’s asking companies to pay $10 million to operate a node that can validate transactions made with its cryptocurrency in exchange for a say in governance of the token. It’s possible that node operators could benefit financially too. By introducing a level of decentralization to the governance of the project, Facebook may be able to avoid regulation related to it holding too much power over a global currency.

Powered by WPeMatico