SPACs

Auto Added by WPeMatico

Auto Added by WPeMatico

ServiceMax, a company that builds software for the field-service industry, announced yesterday that it will go public via a special purpose acquisition company, or SPAC, in a deal valued at $1.4 billion. The transaction comes after ServiceMax was sold to GE for $915 million in 2016, before being spun out in late 2018. The company most recently raised $80 million from Salesforce Ventures, a key partner.

Broadly, ServiceMax’s business has a history of modest growth and cash consumption.

ServiceMax competes in the growing field-service industry primarily with ServiceNow, and interestingly enough given Salesforce Ventures’ recent investment, Salesforce Service Cloud. Other large enterprise vendors like Microsoft, SAP and Oracle also have similar products. The market looks at helping digitize traditional field service, but also touches on in-house service like IT and HR giving it a broader market in which to play.

GE originally bought the company as part of a growing industrial Internet of Things (IoT) strategy at the time, hoping to have a software service that could work hand in glove with the automated machine maintenance it was looking to implement. When that strategy failed to materialize, the company spun out ServiceMax and until now it remained part of Silver Lake Partners thanks to a deal that was finalized in 2019.

TechCrunch was curious why that was the case, so we dug into the company’s investor presentation for more hints about its financial performance. Broadly, ServiceMax’s business has a history of modest growth and cash consumption. It promises a big change to that storyline, though. Here’s how.

The company’s pitch to investors is that with new capital it can accelerate its growth rate and begin to generate free cash flow. To get there, the company will pursue organic (in-house) and inorganic (acquisition-based) growth. The company’s blank-check combination will provide what the company described as “$335 million of gross proceeds,” a hefty sum for the company compared to its most recent funding round.

Powered by WPeMatico

Bright Machines is going public via a SPAC-led combination, it announced this morning. The transaction will see the 3-year-old company merge with SCVX, raising gross cash proceeds of $435 million in the process.

After the transaction is consummated, the startup will sport an anticipated equity valuation of $1.6 billion.

The Bright Machines news indicates that the great SPAC chill was not a deep freeze. And the transaction itself, in conjunction with the previously announced Desktop Metal blank-check deal, implies that there is space in the market for hardware startup liquidity via SPACs. Perhaps that will unlock more late-stage capital for hardware-focused upstarts.

Today we’re first looking at what Bright Machines does, and then the financial details that it shared as part of its news.

Bright Machines is trying to solve a hard problem related to industrial automation by creating microfactories. This involves a complex mix of hardware, software and artificial intelligence. While robotics has been around in one form or another since the 1970s, for the most part, it has lacked real intelligence. Bright Machines wants to change that.

The company emerged in 2018 with a $179 million Series A, a hefty amount of cash for a young startup, but the company has a bold vision and such a vision takes extensive funding. What it’s trying to do is completely transform manufacturing using machine learning.

At the time of that funding, the company brought in former Autodesk co-CEO Amar Hanspal as CEO and former Autodesk founder and CEO Carl Bass to sit on the company board of directors. AutoDesk itself has been trying to transform design and manufacturing in recent years, so it was logical to bring these two experienced leaders into the fold.

The startup’s thesis is that instead of having what are essentially “unintelligent” robots, it wants to add computer vision and a heavy dose of sensors to bring a data-driven automation approach to the factory floor.

Powered by WPeMatico

The number of SPACs in the deep tech sector was skyrocketing, but a combination of increased SEC scrutiny and market forces over the past few weeks has slowed the pace of new SPAC transactions. The correction is an inevitable step on the path to mainstreaming SPACs as an alternative to IPOs, but it won’t cause them to go away. Instead, blank-check vehicles will evolve and will occupy a small and specialized — but important — part of the startup financing landscape.

I believe that SPAC financings can solve a major problem for all capital-intensive technology startups: the need for faster — and potentially cheaper — access to large amounts of capital to fund product development over multiple years.

The tsunami of SPAC financings sparked commentary from all corners of the capital markets community, from equity analysts and securities lawyers to VCs and fund managers — and even central bankers. That’s understandable, as more than $60 billion of SPAC deals have been announced since the beginning of 2020, plus $55 billion in PIPE capital, according to investment bank PJT Partners.

The views debated by finance experts often relate to the reasonableness of SPAC pricing and transaction structures, the alignment of incentives for stakeholders, and post-merger financial and stock price performance. But I’m not going to add another voice to the debate on the risk-reward calculus.

As the co-founder of a quantum computing software startup who worked in financial markets for two decades, I’d like to offer my perspective on two issues that I think my peers care more about: Can SPACs still solve the funding problem for capital-intensive, deep tech startups? And will they become a permanent financing option?

I believe that SPAC financings can solve a major problem for all capital-intensive technology startups: the need for faster — and potentially cheaper — access to large amounts of capital to fund product development over multiple years.

SPACs have created a limitless well of capital that deep tech startups are diving into. That’s because they are proving to be more attractive than other sources of financing, such as taking investments from later-stage VC funds or growth equity funds with finite fund sizes and specific investment themes.

The supply of growth capital from these vehicles has been astounding. In 2020, SPACs alone raised more than $83 billion via 248 IPOs, which is equal to a third of the total $300 billion raised by the entire global VC community. If the present rate of financings had continued, the annual amount of SPAC financings would have been on par with the total R&D expenditure of the U.S. government — roughly $130 billion to $150 billion.

This new supply of capital can let startups keep the lights on, helping them address a practical need while they develop products that may take a decade to field. Before SPACs, any startup that wanted to remain independent had to lurch from one round of VC financing to the next. That, as well as the intense IPO process, is a major time sink for management teams and distracts them from focusing on product development.

Powered by WPeMatico

In light of climate change and escalating global energy demand, more emphasis is being placed on emerging clean technologies — ranging from renewables and energy storage to nuclear power. Although these technologies have tremendous potential, they require lots of innovation, and innovation needs abundant capital.

The issue: early-stage financing for clean tech hasn’t been plentiful, and it’s stifling the growth of new energy companies. Why is this? In general, clean tech companies lack the startup advantages of agility and flexibility.

“Moving fast” works for products such as consumer mobile apps and SaaS solutions. The clean tech sector, on the other hand, tends to involve highly regulated, capital-intensive, mission-critical infrastructure.

That has hurt both returns and well-intentioned impact. According to Cambridge Associates, venture-backed companies have returned, on average, -15% internal rate of return (IRR) since 2000. Contrast that to venture-backed companies in healthcare, which returned 24% in IRR over the same time period.

While noble in its aims to make the world a better, cleaner, safer, healthier place through technology, clean tech venture capital has suffered simply because clean tech does not fit the traditional venture capital model. Central to the venture capital model is the ability to de-risk new ideas and significantly capitalize the most promising ones, allowing for liquidity via M&A or initial public offering (IPO).

Early-stage financing for clean tech hasn’t been plentiful, and it’s stifling the growth of new energy companies.

This construct allows for the return of venture capital dollars, plus appreciation that enables VC firms to raise new funds. These capitalization events also allow the venture-backed company to accelerate growth and maximize market impact.

How this construct works is evident when comparing healthcare and clean tech. In healthcare, new innovations are de-risked by VCs. More mature innovations are acquired or reach IPO every year. As a result, the average annual ratio of dollars raised via an exit to VC-invested dollars since 2012 is 1.8. This ratio is only 0.2 for clean tech, an 800-plus percent difference in the wrong direction. This has resulted in poor returns and limited capitalization of clean tech companies.

Given the state of the world’s environment and lack of abundant energy in emerging economies, we need to collectively fix this issue. Special purpose acquisition companies (SPACs) are significantly improving clean tech’s venture capital construct. According to Investopedia:

SPACs are companies with no commercial operations that are formed strictly to raise capital through an initial public offering (IPO) for the purpose of acquiring an existing company.

Also known as “blank-check companies,” SPACs have been around for decades. In recent years, they’ve become more popular, attracting big-name underwriters and investors and raising a record amount of IPO money in 2019.

In 2020, more than 110 SPACs completed transactions in the U.S., capitalizing these companies with more than $29 billion.

In 2020, SPACs capitalized clean tech companies with almost $4 billion of capital, including Fisker, Lordstown Motors, QuantumScape, Hyliion, XL Fleet and others. This helped push the ratio of funds raised at exit to venture capital invested in 2020 from the previous 0.2 average to a much healthier 0.6, a 200% improvement.

In 2021, we will likely see even further improvement. Why? Because there are 43 active SPACs looking toward or finalizing merger targets with a clean tech focus, potentially providing $12 billion in growth capital. Even if there are no more new SPACs in 2021 and a historically low average of M&As and IPOs, 2021 promises continued improvement for clean tech investment.

One of the most high-profile clean tech SPACs was Nikola Corporation. The battery-electric and hydrogen-powered truck maker has attracted much fanfare since going public last June through a reverse merger with special purpose acquisition company VectoIQ. The company’s market capitalization soared and things seemed to be going well, but things became controversial later in the year when the company was accused of making false statements about its technology and other things.

Although examples such as Nikola have the potential to tarnish the emergence of SPACs as a way to spur clean tech investing, they shouldn’t. There are plenty of examples of emerging companies that scream quality and integrity. For example, Stem*, a leader in the energy storage optimization space, is now going public, pending SEC approval, via the Star Peak SPAC.

Public markets are receiving the SPAC with enthusiasm. Assuming the merger happens, Stem will be capitalized with greater than $450 million of cash to accelerate growth and drive impact. It’s an illustration of SPACs as a positive venture capital construct that is needed to make clean tech work and become a thriving sector.

As a long-time clean tech venture capitalist myself, it is interesting that public investment via the SPAC may be the correcting element for the clean tech VC construct. For years, I assumed that corporates would step up their M&A activity at premium valuations to solve this issue, but I’ve spent a long time waiting.

Judging by activity, corporates seem content to continue playing the still very important investor/nurturer role, versus the “owning” role. Regardless, capitalizing promising clean tech companies can only mean one thing: clean-tech-related impact is coming like never before as these companies require and use capital to scale.

New and more diverse approaches to finding and funding new, great clean tech companies are sorely needed. SPACs are going to be the tool needed to bring clean tech up to par with sectors such as healthcare. It’s a development that will benefit all of us.

*Stem is a Wind Ventures portfolio company.

Powered by WPeMatico

On Monday, Pluralsight, a Utah-based startup that sells software development courses to enterprises, announced that it has been acquired by Vista for $3.5 billion.

The deal, yet to close, is one of the largest enterprise buys of the year: Vista is getting an online training company that helps retrain techies with in-demand skills through online courses in the midst of a booming edtech market. Additionally, the sector is losing one of its few publicly traded companies just two years after it debuted on the stock market.

The Pluralsight acquisition is largely a positive signal that shows the strength of edtech’s capital options as the pandemic continues.

Investors and founders told Techcrunch that the Pluralsight acquisition is largely a positive signal that shows the strength of edtech’s capital options as the pandemic continues.

“What’s happening in edtech is that capital markets are liquidating,” said Deborah Quazzo, managing partner of GSV Advisors.

Quazzo, a seed investor in Pluralsight, said the ability to move fluidly between privately held and publicly held companies is a characteristic of tech sectors with deep capital markets, which is different from edtech’s “old days, where the options to exit were very narrow.”

Powered by WPeMatico

AvePoint, a company that gives enterprises using Microsoft Office 365, SharePoint and Teams a control layer on top of these tools, announced today that it would be going public via a SPAC merger with Apex Technology Acquisition Corporation in a deal that values AvePoint at around $2 billion.

The acquisition brings together some powerful technology executives, with Apex run by former Oracle CFO Jeff Epstein and former Goldman Sachs head of technology investment banking Brad Koenig, who will now be working closely with AvePoint’s CEO Tianyi Jiang. Apex filed for a $305 million SPAC in September 2019.

Under the terms of the transaction, Apex’s balance of $352 million plus a $140 million additional private investment will be handed over to AvePoint. Once transaction fees and other considerations are paid for, AvePoint is expected to have $252 million on its balance sheet. Existing AvePoint shareholders will own approximately 72% of the combined entity, with the balance held by the Apex SPAC and the private investment owners.

Jiang sees this as a way to keep growing the company. “Going public now gives us the ability to meet this demand and scale up faster across product innovation, channel marketing, international markets and customer success initiatives,” he said in a statement.

AvePoint was founded in 2001 as a company to help ease the complexity of SharePoint installations, which at the time were all on-premise. Today, it has adapted to the shift to the cloud as a SaaS tool and primarily acts as a policy layer enabling companies to make sure employees are using these tools in a compliant way.

The company raised $200 million in January this year led by Sixth Street Partners (formerly TPG Sixth Street Partners), with additional participation from prior investor Goldman Sachs, meaning that Koenig was probably familiar with the company based on his previous role.

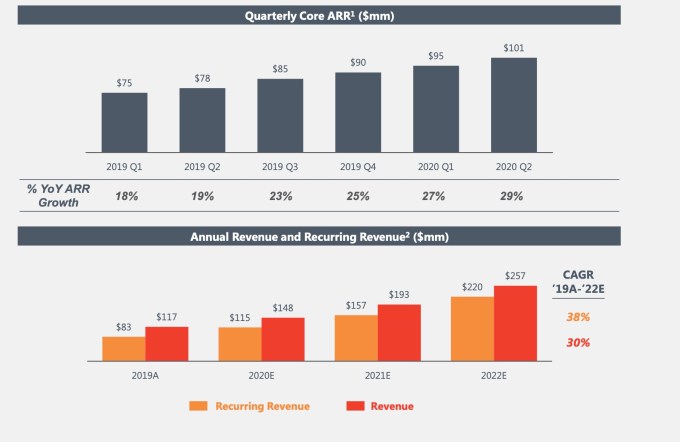

The company has raised a total of $294 million in capital before today’s announcement. It expects to generate almost $150 million in revenue by the end of this year, with ARR growing at over 30%. It’s worth noting that the company’s ARR and revenue has been growing steadily since Q12019. The company is projecting significant growth for the next two years with revenue estimates of $257 million and ARR of $220 million by the end of 2022.

Image Credits: AvePoint

The deal is expected to close in the first quarter of next year. Upon close the company will continue to be known as AvePoint and be publicly traded on Nasdaq under the new ticker symbol AVPT.

Powered by WPeMatico

2020 has been a year of social upheaval. Around the world, society is identifying different problems in our culture and pushing for widespread change. While there are notable steps we can all take, from altering exclusionary company policies to signing action-oriented petitions, the VC and investment world has another, often overlooked option: Investing in change-the-world startups.

Increasingly, angel investors and institutional funds have begun allocating a portion of their funds to startups focused on diversity and social good, whether focused on democratized access to healthcare and education, or larger scale issues like climate change.

Initially, shifting funds to empower social good may seem like a hefty feat, however investors can embrace this mindshift in three simple steps: (1) redistributing stagnant investments; (2) leveraging democratized access to change-making startups; and (3) identifying founders tracking toward success.

Most of the world’s money is tied up in stagnant places. Whether invested in real estate, bonds or other traditional vehicles, this capital typically often shows conservative returns to investors — and has negligible impact on society. The intent isn’t malicious.

Most family offices and private wealth managers strive to minimize losses and these sorts of uniformed portfolios are safe. Even the most seasoned investors should incorporate more variety into their portfolios, determining where they can make profitable investments that yield higher returns while advancing societal good. Investors can take small steps to get more confident in expanding their strategies.

To start, reframe your thinking into seeing the potential opportunity rather than the risk. A good way to do this: Look at how high-risk public equities performed over the last five years and compare it to ventures within tech. Investors will see a significant disparity and the opportunity to make different returns.

The idea is not to put an entire profile in a single venture. Rather, an investor should take a portion of their portfolio in a high-risk investment sector, like public equities or fund structures, and put it in a similar risk profile with a better return. Gradually increasing these increments, starting at 15% and slowly scaling up, can help investors to see outsized returns while making a difference in the process.

For startups of all sizes, democratized access to investors will accelerate the use of capital for social good. Until recently, only the world’s wealthiest people had exposure to premium capital, but crowdfunding and accelerator programs have ushered in new opportunities, forging connections that might not have otherwise been possible.

These avenues have opened new doors for investors and startups. Access to developed networks or innovation hubs like Silicon Valley are no longer make-or-breaks for those looking to raise capital. Extended global opportunity for startups also means investors have more options to find promising ventures that align with their values, regardless of their location.

But while crowdfunding and accelerators have made the world more accessible, they come with sizable challenges. Despite making early-stage investment more obtainable, crowdfunding often does not bring the most valuable investors to the table.

Crowdfunding also inundates platforms with poor-quality deal flow, making it more strenuous for investors to connect with fruitful opportunities. Meanwhile, various accelerators and incubation platforms have emerged, which have advanced global connection, but tend to be quite noisy.

To succeed, entrepreneurs need more than capital. Rather, they need strategic support from experienced investors who can help them make decisions and scale in an impactful way. With a world of ideas at their fingertips, investors should take time to sift through their options and find the ideas that move them the most, prioritizing quality deals and looking toward platforms that curate promising connections.

Now is the right time to invest in startups. People who innovate during the pandemic have triple the hustle of those who build in safer economies. But while the timing is right, it’s equally important that the fit is right. I’m a big believer in investing in potential: Ambition, unwavering tenacity and empathy are desirable qualities that can help bring game-changing ideas to fruition.

If an investor funds a passionate leader with a strong vision and ability to attract talent, then the groundwork is laid to build something meaningful. When considering the change-makers to invest in, ask: Is this the right person to be building this company? Do they have the ability to attract and lead talent? Is the market big enough, and is there a significant enough problem to build a company around?

If the answer isn’t yes to all of these questions, it’s important to gauge if you can see a theoretical exit, or if the company is pre-seed or Series A, if they have the ability to scale to a decent size.

Despite this, investing in startups, no matter how good their intentions, can scare investors. One way to overcome trepidation is to invest in larger-stage startups that seem less risky and then wade into earlier-stage startups at your own pace. Special purpose acquisition companies (SPACs) are also becoming an interesting investment option.

SPACs are corporations formed for the sole purpose of raising investment capital through an IPO. The proceeds are then used to buy one or more existing companies, an option that could decrease anxiety for risk-averse investors looking to expand their comfort zone.

Any strategy an investor chooses to embrace social good is a step in the right direction. Capital is a tangible way to fuel innovation and bring about impactful change.

Democratized access to startups yields more opportunity for investors to find ventures that align with their values while diversifying their profiles can provide tremendous results. And when that return means disrupting the status quo and empowering societal change? Everyone wins.

Powered by WPeMatico

I live in San Francisco, but I work an East Coast schedule to get a jump on the news day. So I’d already been at my desk for a couple of hours on Wednesday morning when I looked up and saw this:

What color is the sky this morning pic.twitter.com/nt5dZp5wWc

— Walter Thompson (@YourProtagonist) September 9, 2020

As unsettling as it was to see the natural environment so transformed, I still got my work done. This is not to boast: I have a desk job and a working air filter. (People who make deliveries in the toxic air or are homeschooling their children while working from home during a global pandemic, however, impress the hell out of me.)

Not coincidentally, two of the Extra Crunch stories that ran since our Tuesday newsletter tie directly into what’s going on outside my window:

As this guest post predicted, a suboptimal attempt I made to track a delayed package using interactive voice response (IVR) indeed poisoned my customer experience, and;

Sheltering in place to avoid the novel coronavirus — and wildfire smoke — is fueling growth in the video-game industry, perhaps one factor in Unity Software Inc.’s plan to go public ahead of competitor Epic Games. In a two-part series, we looked at how the company has expanded beyond games and shared a detailed financial breakdown.

We covered a lot of ground this week, so scroll down or visit the recently redesigned Extra Crunch home page. If you’d like to receive this roundup via email each Tuesday and Friday, please click here.

Thanks very much for reading Extra Crunch; I hope you have a relaxing and safe weekend.

Walter Thompson

Senior Editor

@yourprotagonist

Image Credits: Nigel Sussman (opens in a new window)

In a two-part series that ran on TechCrunch and Extra Crunch, former media columnist Eric Peckham returned to share his analysis of Unity Software Inc.’s S-1 filing.

Part one is a deep dive that explains how the company has grown beyond gaming to develop multiple revenue streams and where it’s headed.

For part two on Extra Crunch, he studied the company’s numbers to offer some context for its approximately $11 billion valuation.

Image Credits: Edwin Remsberg (opens in a new window) / Getty Images

As we’ve covered previously, the COVID-19 pandemic is making the world a lot smaller.

Investors who focus on their own backyards still have an advantage, but the ability to set up a quick coffee meeting with a promising investor is no longer one of them.

Even though some VCs are cutting first checks after Zoom calls, regional investors’ personal networks are still a trump card. Tourists will always rely on guide books, however, which is why we continue to survey investors around the world.

A Dealroom report issued this summer determined that 97 VC funds backed more than 1,600 funding rounds in Poland last year. With over 2,400 early- and late-stage startups and 400,000 engineers in the country, it’s easy to see why foreign investors are taking notice.

Editor-at-large Mike Butcher reached out to several investors who focus on Warsaw and Poland in general to learn more about the startups fueling their interest across fintech, gaming, security and other sectors:

We’ll run the conclusion of his survey next Tuesday.

Image Credits: cnythzl (opens in a new window) / Getty Images

Even for fledgling startups, creating a robust customer service channel — or at least one that doesn’t annoy people — is a reliable way to keep users in the sales funnel.

Using AI and automation is fine, but now that consumers have grown used to asking phones and smart speakers to predict the weather and read recipe instructions, their expectations are higher than ever.

If you’re trying to figure out what people want from hyper-personalized customer experiences and how you can operationalize AI to give them what they’re after, start here.

Image Credits: Nigel Sussman (opens in a new window)

For today’s edition of The Exchange, Natasha Mascarenhas joined Alex Wilhelm to examine how the pandemic-fueled surge of interest in edtech is manifesting on the funding front.

The numbers suggest that funding will far surpass the sector’s high-water mark set in 2018, so the duo studied the numbers through August 31, which included a number of mega-rounds that exceeded $100 million.

“Now the challenge for the sector will be keeping its growth alive in 2021, showing investors that their 2020 bets were not merely wagers made during a single, overheated year,” they conclude.

Image Credits: WhataWin (opens in a new window) / Getty Images

The odds are low that someone’s going to enter my home and steal my belongings. I still lock my door when I leave the house, however, and my valuables are insured. I’m an optimist, not a fool.

Similarly: Is your startup’s cybersecurity strategy based on optimism, or do you have an actual response plan in case of a data breach?

Security reporter Zack Whittaker has seen some shambolic reactions to security lapses, which is why he turned in a post-mortem about a corporation that got it right.

“Once in a while, a company’s response almost makes up for the daily deluge of hypocrisy, obfuscation and downright lies,” says Zack.

Image Credits: Eric Burger/EyeEm (opens in a new window) / Getty Images

There’s a lot of buzz about special purpose acquisition companies these days.

Used-car marketplace Shift announced its SPAC in June 2020, and is on track to complete the process in the next few months, so co-founder/co-CEO George Arison wrote an Extra Crunch guest post to share what he has learned.

Step one: “If you go the SPAC route, you’ll need to become an expert at financial engineering.”

Image Credits: Sophie Alcorn

Dear Sophie:

I am a software engineer and have been looking at job postings in the U.S. I’ve heard from my friends about J-1 Visa Training or J-1 Research.

What is a J-1 status? What are the requirements to qualify? Do I need to find a U.S. employer willing to sponsor me before I apply for one? Can I get a visa? How long could I stay?

— Determined in Delhi

Image Credits: Patrick T. Fallon/Bloomberg (opens in a new window) / Getty Images

While we count down to the September 23 premiere of NYSE: PLTR, Danny Crichton looked at the “robust secondary market” that has allowed some investors to acquire shares early.

“Given the number of people involved and the number of shares bought and sold over the past 18 months, we can get some insight regarding how insiders perceive Palantir’s value,” he writes.

Image Credits: JakeOlimb / Getty Images

Zack Whittaker interviewed Bugcrowd CTO, founder and chairman Casey Ellis about the best practices he recommends for creating a startup culture that takes security seriously.

“It’s an everyone problem,” said Ellis, who encouraged founders to promote the notion of “productive paranoia.”

Now that the threat envelope includes everyone from marketing to engineering, employees need to “internalize the fact that bad stuff can and does happen if you do it wrong,” Ellis said.

Powered by WPeMatico