Southeast Asia

Auto Added by WPeMatico

Auto Added by WPeMatico

Earlier this year, the founders of event analytics platform Hubilo pivoted to become a virtual events platform to survive the impact of COVID-19. Today, the startup announced it has raised a $4.5 million seed round, led by Lightspeed, and says it expects to exceed $10 million bookings run rate and host more than one million attendees over the next few months.

The round also included angel investors Freshworks CEO Girish Mathrubootham; former LinkedIn India CEO Nishant Rao; Slideshare co-founder Jonathan Boutelle; and Helpshift CEO Abinash Tripathy.

Hubilo’s clients have included the United Nations, Roche, Fortune, GITEX, IPI Singapore, Tech In Asia, Infocomm Asia and Clarion Events. The startup is headquartered in San Francisco, but about 12% of its sales are currently from Southeast Asia, and it plans to further scale in the region. It will also focus on markets in the United States, Europe, the Middle East and Africa.

Vaibhav Jain, Hubilo’s founder and CEO, told TechCrunch that many of its customers before the pandemic were enterprises and governments that used its platform to help organize large events. Those were also the first to stop hosting in-person events.

In February, “we knew that most, if not all, physical events were getting postponed or cancelled globally. To counter the drop in demand for offline events, we agreed to extend the contracts by six more months at no cost,” Jain said. “However, this was not enough to retain our clients and most of them either cancelled the contracts or put the contract on hold indefinitely.”

As a result, Hubilo’s revenue dropped to zero in February. With about 30 employees and reserves for only three months, Jain said the company had to choose between shutting down or finding an alternative model. Hubilo’s team created an MVP (minimum viable product) virtual event platform in less than a month and started by convincing a client to use it for free. That first virtual event was hosted in March and “since then, we’ve never looked back,” said Jain.

This means Hubilo is now competing with other virtual event platforms, like Cvent and Hopin (which was used to host TechCrunch Disrupt). Jain said his company differentiates by giving organizers more chances to rebrand their virtual spaces; focusing on sponsorship opportunities that include contests, event feeds and virtual lounges to increase attendee engagement; and providing data analytic features that include integration with Salesforce, Marketo and HubSpot.

With so many events going virtual that “Zoom fatigue” and “webinar fatigue” have now become catchphrases, event organizers have to not only convince people to buy tickets, but also keep them engaged during an event.

Hubilo “gamifies” the experience of attending a virtual event with features like its Leaderboard. This enables organizers to assign points for things like watching a session, visiting a virtual booth or messaging someone. Then they can give prizes to the attendees with the most points. Jain said the Leaderboard is Hubilo’s most used feature.

Powered by WPeMatico

Running a small to medium-sized business means a small staff needs to juggle a plethora of tasks, like bookkeeping, tax records and regulatory filings. Singaporean startup Lanturn streamlines their workload with a combination of corporate services and an internal platform that helps automate administrative work. Lanturn announced today that it has raised a $3 million seed round led by East Ventures and CoCoon Ignite Ventures.

Spun out from Zave, a Singaporean management app (and another startup in East Ventures’ portfolio), two years ago, Lanturn now has almost 400 clients. It focuses on startups and SMEs, acting as a “one-stop online corporate services” solution, and uses its internal tech platform to differentiate from other corporate service providers.

Lanturn’s services include helping companies incorporate in Singapore and handling visa applications for new hires. It is led by chief executive officer Velisarios Kattoulas.

Kattoulas told TechCrunch that Lanturn’s seed funding will be used for hiring and to develop its technology.

In a statement about the investment, East Ventures managing partner and co-founder Batara Eto said, “We are pleased to support solutions that enable agility and adaptability among businesses, especially in the wake of the pandemic, and Lanturn provides that by leveraging technology to streamline corporate services and empower businesses to make more informed data-driven decisions.”

Other participants in the round included individual investors Alex Turnbull; RVP Equity managing partner Saki Georgiadis; Meiyen Tan, the head of Oon & Bazul’s restructuring and insolvency practice; White & Case Asia-Pacific partner Chris Kelly; and Next Billion Ventures venture partner Tiang Foo Lim.

Lanturn’s clients range in size from very early-stage startups with only one person, to small and mid-sized asset managers, SMEs and tech firms that have more than 100 employees spread across several countries.

The COVID-19 pandemic meant there was less demand for Lanturn’s services this year than the company had expected, but on the other hand, “the pandemic has highlighted to clients that because Lanturn has its own cloud-based corporate services platform, we can serve them as well today as we could before the pandemic,” Kattoulas said. “That’s helped us maintain momentum, and it’s one reason we’ll grow more this year than almost any cloud-based or traditional corporate services firm.”

Powered by WPeMatico

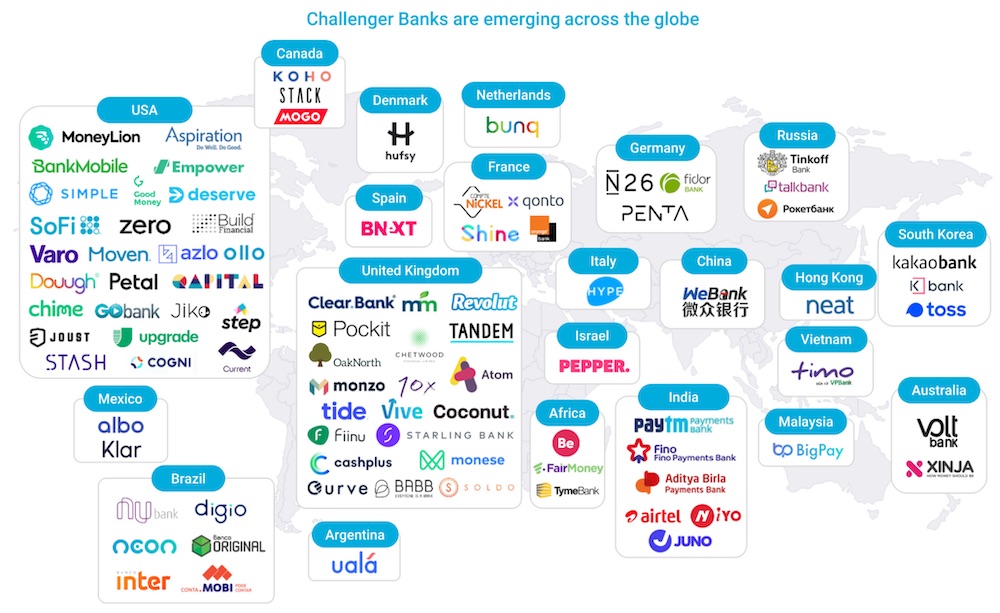

The neobank, or digital bank, phenomenon continues to take the world by storm, with global winners, from Brazil’s Nubank valued at $10 billion and Berlin’s N26 valued at $3.5 billion, to Chime, now valued at $14.5 billion as the most valuable consumer fintech in the United States.

Neobanks have led the charge of the $3.6 billion in venture capital funding for consumer fintech startups this year. And as the coronavirus-fueled acceleration of digital transformation continues, it seems the digital bank is here to stay, with some estimates pointing to neobanks reaching 60 million customers in North America and Europe by the end of 2020, and surpassing 145 million by 2024.

The space is also becoming more crowded, a trend which will only accelerate with fintech eating the world and creating greater infrastructure that enables any company to include a bank account as a product extension.

FT Partners Fintech Industry Research, January 2020

As a result, neobanks are not a monolithic model and not all are created equal. Looking underneath the hood of business models across the globe reveals remarkable operational differences and highlights specific features that are more likely to succeed in the long-term.

Today there are five distinct models that are leading globally:

Interchange-led: Relies on payments revenue, sourced through interchange as the revenue driver. Every time a customer uses the neobank’s card as a payment method they get paid [e.g. Chime / US; Neon (hybrid of 1 & 2) / Brazil].

Credit-led: Leverages a credit-first model, starting off with a credit card or similar offering, and later providing a bank account [e.g. Nubank, Neon (hybrid of 1 & 2) / Brazil].

Powered by WPeMatico

While Southeast Asia’s startup ecosystems are still young compared to those in China or India, it has matured over the last five years. Unicorns like Grab, Gojek and Garena are continuing to grow, and more competitive startups are emerging in sectors like fintech, e-commerce and logistics. That leads to the question: Will consolidation start to pick up?

The consensus by investors interviewed by Extra Crunch is: Yes, but slowly at first. In the meantime, there are still roadblocks to mergers and acquisitions, including few buyers and the size of markets like Indonesia, which means startups there have a lot of room to grow on their own, even alongside competitors. But many Southeast Asian startup ecosystems are rapidly evolving, and consolidations may speed up in the next few years.

During a Disrupt session, East Ventures partner Melisa Irene spoke about consolidation as a strategy, especially when larger companies, like Grab, decide to expand into new services by acquiring smaller players. In an interview with Extra Crunch, Irene elaborated on the idea.

“Companies that want to get more value out of their customers by expanding into other services can do it internally by developing it, or do it externally by buying existing companies that have been operating in the same or adjacent sectors,” she said.

For many years, companies opted not to do that because of the cost, she added, but that mindset started to shift a few years ago.

In 2018, Grab acquired Uber’s Southeast Asia operations, still one of the highest-profile examples of consolidation in the region. The “superapp” also built out its financial services business by acquiring fintech startups Kudo, iKaaz, Bento and OVO.

Grab rival Gojek has been an even busier buyer, acquiring 13 startups so far according to Crunchbase, including Vietnamese payments startup WePay and Indonesian point-of-sale platform Moka earlier this year.

Meanwhile, Traveloka acquired three competing online travel agencies in 2018, while e-commerce platform Tokopedia bought Bridestory, its first publicly known acquisition, last year to expand into the Indonesian bridal industry.

Golden Gate Ventures partner Justin Hall said he has seen attitudes toward consolidation in Southeast Asia gradually shift since the investment firm was founded in 2011.

“I would say over the next two to three years, we’re definitely going to start seeing much more M&A occurring than versus the last eight to 10 years. It’s the confluence of different factors. One, I think corporate VC is starting to pour a little bit more money into the space. You have a lot of international tech companies, e.g., from China, or regional unicorns that are being much more acquisitive in their strategy,” Hall said.

He added that an often overlooked factor is that a lot of regional early-stage and institutional funds launched about a decade ago, building a foundation for Southeast Asia’s startup ecosystems. Many of these funds started out with a 10-year mandate and as a result, general partners may start examining how they can orchestrate sales, for example by talking to corporate acquirers, financiers or other sources of capital for an exit.

“A lot of activity that you’re starting to see right now is under the table. We have funds coming up on that 10-year mark, saying, ‘Let’s see where we can derive value within our portfolio, within specific companies that we can sell.’ That is going to start happening en masse over the next two years once we hit that 10-year mark for a lot of these funds.”

Powered by WPeMatico

A month after completing Y Combinator’s accelerator program, BukuWarung, an financial tech startup that serves small businesses in Indonesia, announced it has raised new funding from a roster of high-profile investors, including partners of DST Global, Soma Capital and 20VC.

The amount of the funding was undisclosed, but a source told TechCrunch that it was between $10 million to $15 million. The new capital will be used to hire for BukuWarung’s technology team. TechCrunch first profiled BukuWarung in July.

Angel investors in the round include several high-profile founders and executives: finance technology platform Plaid’s co-founder William Hockey; Tinder co-founder Justin Mateen; Superhuman founder Rahul Vohra; Adobe chief product officer Scott Belsky; Clearbit chairman and startup advisor Josh Buckley; former Uber chief product officer Manik Gupta; Spotify’s former head of new markets in Asia Sriram Krishnan; 20VC founder Harry Stebbings; Nancy Xiao, an investor with Bond Capital; and Fast co-founder Allison Barr Allen. Angel investors from WhatsApp, Square and Airbnb also participated.

Launched last year by co-founders Chinmay Chauhan and Abhinay Peddisetty, BukuWarung is targeted at the 60 million “micromerchants” in Indonesia, including neighborhood store (or warung) owners. The app was originally created as a replacement for pen and apper ledgers, but plans to introduce financial services including credit, savings and insurance. In August, the company integrated digital payments into its platform, enabling merchants to take customer payments from bank accounts and digital wallets like OVO and DANA. BukuWarung’s goal is to fill the same role for Indonesian merchants that KhataBook and OKCredit do in India.

One of the reasons BukuWarung launched digital payments was in response to customer demand for contactless transactions and instant payouts during the COVID-19 pandemic. Since introducing the feature, the company said it has already processed several million U.S. dollars in total payment volume (TPV) on an annualized basis. The company says it now serves about 1.2 million merchants across 750 locations in Indonesia, focusing on tier 2 and tier 3 cities.

Digital payments is also the first step into building out BukuWarung’s financial services, which will help differentiate it from other bookkeeping. The payments features is currently free and BukuWarung is experimenting with different monetization models, including making a small margin on fees.

“The reason why we launched payments is also very strategic, because there is a lot of pull in the market. We have already seen several millions annualized TPV in less than a month, because the payments we offer are cost-efficient as well and cheaper than to get from a bank,” Chauhan told TechCrunch.

“If you look at the Indian players, like Khatabook, they have also launched digital payments. The reason for that is because it’s a very essential step for building a business and monetization,” he added. “If you don’t have payments, you can’t do anything like that.”

Chauhan added that building a financial services platform is the difference between providing a utility app that replaces bookkeeping ledgers, and becoming an essential service for merchants that will eventually include lending for working capital, savings and insurance products. The bookkeeping features on BukuWarung will feed into the financial services aspect by providing data to score creditworthiness, and help small merchants, who often have difficulty securing working capital from traditional banks, get access to lines of credit.

Powered by WPeMatico

Stripe has led a $12 million Series A round in Manila-based online payment platform PayMongo, the startup announced today.

PayMongo, which offers an online payments API for businesses in the Philippines, was the first Filipino-owned financial tech startup to take part in Y Combinator’s accelerator program. Y Combinator and Global Founders Capital, another previous investor, both returned for the Series A, which also included participation from new backer BedRock Capital.

PayMongo partners with financial institutions, and its products include a payments API that can be integrated into websites and apps, allowing them to accept payments from bank cards and digital wallets like GrabPay and GCash. For social commerce sellers and other people who sell mostly through messaging apps, the startup offers PayMongo Links, which buyers can click on to send money. PayMongo’s platform also includes features like a fraud and risk detection system.

In a statement, Stripe’s APAC business lead Noah Pepper said it invested in PayMongo because “we’ve been impressed with the PayMongo team and the speed at which they’ve made digital payments more accessible to so many businesses across the Philippines.”

The startup launched in June 2019 with $2.7 million in seed funding, which the founders said was one of the largest seed rounds ever raised by a Philippines-based fintech startup. PayMongo has now raised a total of almost $15 million in funding.

Co-founder and chief executive Francis Plaza said PayMongo has processed a total of almost $20 million in payments since launching, and grown at an average of 60% since the start of the year, with a surge after lockdowns began in March.

He added that the company originally planned to start raising its Series A in in the first half of next year, but the growth in demand for its services during COVID-19 prompted it to start the round earlier so it could hire for its product, design and engineering teams and speed up the release of new features. These will include more online payment options; features for invoicing and marketplaces; support for business models like subscriptions; and faster payout cycles.

PayMongo also plans to add more partnerships with financial service providers, improve its fraud and risk detection systems and secure more licenses from the central bank so it can start working on other types of financial products.

The startup is among fintech companies in Southeast Asia that have seen accelerated growth as the COVID-19 pandemic prompted many businesses to digitize more of their operations. Plaza said that overall digital transactions in the Philippines grew 42% between January and April because of the country’s lockdowns.

PayMongo is currently the only payments company in the Philippines with an onboarding process that was developed to be completely online, he added, which makes it attractive to merchants who are accepting online payments for the first time. “We have a more efficient review of compliance requirements for the expeditious approval of applications so that our merchants can use our platform right away and we make sure we have a fast payout to our merchants,” said Plaza.

If the momentum continues even as lockdowns are lifted in different cities, that means the Philippine’s central bank is on track to reach its goal of increasing the volume of e-payment transactions to 20% of total transactions in the country this year. The government began setting policies in 2015 to encourage more online payments, in a bid to bolster economic growth and financial inclusion, since smartphone penetration in the Philippines is high, but many people don’t have a traditional bank account, which often charge high fees.

Though lockdown restrictions in the Philippines have eased, Plaza said PayMongo is still seeing strong traction. “We believe the digital shift by Filipino businesses will continue, largely because both merchants and customers continue to practice safety measures such as staying at home and choosing online shopping despite the more lenient quarantine levels. Online will be the new normal for commerce.”

Powered by WPeMatico

Based in Bangkok, Freshket simplifies the process of getting fresh produce from farms to tables. Launched in 2017, the startup has now raised a $3 million Series A, led by Openspace Ventures.

Other participants included Thai private equity firm ECG-Research; Innospace; and Pamitra Wineka and Ivan Sustiawan, the co-founders of Indonesian agriculture technology startup TaniHub. French-Singaporean food conglomerate Denis Asia Pacific and Thai family office Seedersclub, who made previous investments in Freshket, also returned for the Series A.

Freshket’s technology includes an e-commerce marketplace that connects farmers and food processors to businesses, like restaurants, and consumers in Thailand. The startup was co-founded by chief executive Ponglada Paniangwet and chief marketing officer Tuangploi Chiwalaksanangkoon, who each worked in marketing before launching Freshket three years ago.

Paniangwet told TechCrunch she wanted to enter agritech because her family has worked in the agriculture business for 25 years. “I grew up learning a lot about what worked and didn’t work in the industry,” Paniangwet said. “Overall, the industry is tedious, messy and highly manual.”

Freshket’s goal is to become “an enabler for the entire food supply chain,” she added.

Before Freshket, Paniangwet started a processing center, which sources, cuts and trims fresh produce at wholesale fresh markets before delivering them to restaurants and other customers. She realized technology could be used to simplify the supply chain, increasing farmers’ incomes and the quality of produce received by customers.

There is also ample market opportunity. According to an April 2019 Euromonitor International report, the food service market in Thailand is worth over $7.7 billion in annual purchases, made by more than 200,000 restaurants (link in Thai).

Chiwalaksanangkoon, who was already good friends with Paniangwet, left her position at one of Thailand’s largest banks to co-found Freshket. The company’s platform pull together Thailand’s fragmented produce supply chain by bringing together processing centers and suppliers, and connecting them directly with farmers, who usually rely on middlemen. Freshket also provides its users with data to help them predict supply and demand for their crops.

The expenses of operating a delivery business, especially for perishable goods, can be very high. To stay cost-efficient, Freshket itself doesn’t stock fresh produce. Instead, Freshket tells its network, including farmers, how much product they will need to provide on a daily basis, so they can plan their supply chains.

Paniangwet also said the B2B food delivery business has high average order values, fortifying its unit economics. Freshket’s order, warehouse and logistics management systems are all linked together and “because of that, we are able to control the flow of goods, limit additional and labor costs and keep our overall cost base manageable,” she said.

Freshket’s main rivals in the B2B space are traditional supply chain businesses; in the consumer space, it is up against include grocery delivery startups. It competes with delivery apps by offering lower retail prices, since Freshket is already tapped into a streamlined supply chain. For B2B customers, Freshket’s selling points include more precise delivery, a wider variety of products and produce gradings.

Freshket’s new funding will be used to upgrade its supply management technology. In the future, Paniangwet said the company plans to add more services, like financing, demand forecasting and price matching.

Freshket is among several startups in Southeast Asia markets focused on streamlining the food supply chain in different countries. Others include TaniHub and Eden Farm in Indonesia, Agribuddy in Cambodia and Singapore-based Glife.

This is the third agritech investment Openspace Ventures, which focuses on early-stage companies in Southeast Asia, has made (the other are TaniHub and Singaporean grocery platform RedMart).

In a press statement about the investment, Openspace Ventures founding partner Hian Goh said, “As Openspace Ventures’ second investment in Thailand this year, Freshket reflects our growing conviction in the potential of the Thai market for high quality and innovative startups.”

Powered by WPeMatico

In Indonesia, about half of adults are “underbanked,” meaning they don’t have access to bank accounts, credit cards and other traditional financial services. A growing list of tech companies are working on solutions, from Payfazz, which operates a network of financial agents in small towns, to digital payment services from GoJek and Grab. As a result, financial inclusion is increasing for consumers and small businesses in Southeast Asia’s largest country, but one group remains underserved: schools.

InfraDigital was founded in 2018 by chief executive officer Ian McKenna and chief operating officer Indah Maryani. Both have backgrounds in financial tech, and their platform enables parents to pay school tuition with the same digital services they use for electricity bills or online shopping. The startup currently serves about 400 schools and recently raised a Series A led by AppWorks.

Many Indonesian schools still rely on cash payments, which are often delivered by kids to their teachers.

“My kid had just started school, and one day I spotted my wife giving him an envelope full of cash for tuition. He was only three years old,” McKenna said. “That triggered my curiosity about how these financial systems work.”

To give parents an easier alternative, InfraDigital, which is registered with Indonesia’s central bank, partners with banks, convenience store chains like Indomaret, online wallets and digital payment services like GoPay to allow them to send tuition money online.

“The way you pay your electricity bill, it’s likely that your school is already there, regardless of whether you have a bank account or live in a really remote place” where many people make cash payments for services at convenience stores, McKenna said. The startup is now working on a system for schools in areas that don’t have access to convenience store chains and banks.

Before building InfraDigital’s network, McKenna and Maryani had to understand why many schools still rely on cash payments and paper ledgers to manage tuition.

“Banks have been trying to tap into the education market for a long time, 12 to 15 years probably, but no one has become the biggest bank for schools,” said Maryani. “The reason behind that is because they come in with their own products and they don’t try to resolve the issues schools are facing. Since they are focused on the consumer side, they don’t really see schools or other offline businesses as their customers, and there is a lot of customization that they need to do.”

For example, a school might have 2,000 students and charge each of them about USD $10 a month in school fees. But they also collect separate payments for books, uniforms, and building fees. InfraDigital’s founders say schools typically send out an average of about 2.5 invoices a month.

Digitizing payments also makes it easier for schools to track their finances. InfraDigital provides its clients with a backend application for accounting and enrollment management. It automatically tracks tuition payments as they come in.

“People don’t get paid that much and they are ridiculously busy taking care of thousands of kids. It’s really, really tough,” McKenna said. “When you’re giving them a solution, it’s not about features, it’s not about tools, it’s about the practicalities of their day-to-day life and how we are going to assist them with it. So you remove that burden from them.”

During the COVID-19 pandemic, which resulted in movement restriction orders in different areas of Indonesia, InfraDigital’s founders say the platform was able to forecast trends even before schools officially closed. They started surveying schools in their client base, and sent back data to help them forecast how school closures would affect their income.

“From the school’s perspective, it’s a really damaging situation, with 30% to 60% income drops. Teachers don’t get paid. If the economy goes down, parents at lower-income schools, which are a big part of our client base, won’t be able to pay,” McKenna said. “It’s built into the model, and we’ll continue seeing that however long the economic impact of COVID-19 lasts.”

Powered by WPeMatico

South Africa-based renewable energy startup Sun Exchange has raised $3 million to close its Series A funding round totaling $4 million.

The company operates a peer-to-peer, crypto-enabled business that allows individuals anywhere in the world to invest in solar infrastructure in Africa.

How’s that all work?

“You as an individual are selling electricity to a school in South Africa, via a solar panel you bought through the Sun Exchange,” explained Abe Cambridge, the startup’s founder and CEO.

“Our platform meters the electricity production of your solar panel. Arranges for the purchasing of that electricity with your chosen energy consumer, collects that money and then returns it to your Sun Exchange wallet.”

It costs roughly $5 a solar cell to get in and transactions occur in South African Rand or Bitcoin.

“The reason why we chose Bitcoin is we needed one universal payment system that enables micro transactions down to a millionth of a U.S. cent,” Cambridge told TechCrunch on a call.

He co-founded the Cape Town-headquartered startup in 2015 to advance renewable energy infrastructure in Africa. “I realized the opportunity for solar was enormous, not just for South Africa, but for the whole of the African continent,” said Cambridge.

“What was required was a new mechanism to get Africa solar powered.”

Sub-Saharan Africa has a population of roughly 1 billion people across a massive landmass and only about half of that population has access to electricity, according to the International Energy Agency.

Recently, Sun Exchange’s main market South Africa — which boasts some of the best infrastructure in the region — has suffered from blackouts and power outages.

Image Credits: Sun Exchange

Sun Exchange has members in 162 countries who have invested in solar power projects for schools, businesses and organizations throughout South Africa, according to company data.

The $3 million — which closed Sun Exchange’s $4 million Series A — came from the Africa Renewable Power Fund of London’s ARCH Emerging Markets Partners.

With the capital, the startup plans to enter new markets. “We’re going to expand into other Sub-Saharan African countries. We’ve got some clear opportunities on our roadmap,” Cambridge said, referencing Nigeria as one of the markets Sun Exchange has researched.

There are several well-funded solar energy startups operating in Africa’s top economic and tech hubs, such as Kenya and Nigeria. In East Africa, M-Kopa sells solar hardware kits to households on credit, then allows installment payments via mobile phone using M-Pesa mobile money. The venture is backed by $161 million from investors including Steve Case and Richard Branson.

In Nigeria, Rensource shifted from a residential hardware model to building solar-powered micro utilities for large markets and other commercial structures.

Sun Exchange operates as an asset free model and operates differently than companies that install or manufacture solar panels.

“We’re completely supplier agnostic. We are approached by solar installers who operate on the African continent. And then we partner with the best ones,” said Cambridge — who presented the startup’s model at TechCrunch Startup Battlefield in Berlin in 2017.

“We’re the marketplace that connects together the user of the solar panel to the owner of the solar panel to the installer of the solar panel.”

Abe Cambridge, Image Credits: TechCrunch

Sun Exchange generates revenues by earning margins on sales of solar panels and fees on purchases and kilowatt hours generated, according to Cambridge.

In addition to expanding in Africa, the startup looks to expand in the medium to long-term to Latin America and Southeast Asia.

“Those are also places that would really benefit from from solar energy, from the speed in which it could be deployed and the environmental improvements that going solar leads to,” said Cambridge.

Powered by WPeMatico

Singapore-based fintech startup GoBear has raised $17 million from returning investors Walvis Participaties, a Dutch venture capital firm, and Aegon N.V., a life insurance and asset management provider. The funding brings GoBear’s total funding so far to $97 million, and will be used to expand its consumer financial services platform, which is available in seven Asian markets: Hong Kong, Indonesia, Malaysia, the Philippines, Singapore, Thailand and Vietnam.

Founder and CEO Adrian Chng told TechCrunch that GoBear will focus on what it calls its “three growth pillars”: an online financial supermarket that evolved from the company’s financial products aggregator/comparison service; an online insurance brokerage; and its digital lending business, which it recently expanded by acquiring consumer lending platform AsiaKredit.

The company has also added three new executives over the past few months: chief information technology officer Valeriy Gasratov; chief strategy officer Jinnee Lim as Chief Strategy Officer; and Mike Singh from AsiaKredit as its new chief lending officer.

GoBear originally launched in 2015 as a metasearch engine, before transitioning into financial services. The company now works with over 100 financial partners, including banks and insurance providers, and says its platform has been used by over 55 million people to search for more than 2,000 personal financial products.

The startup serves consumers who don’t have credit cards or other access to traditional credit building tools. Similar to other fintech companies that focus on underbanked populations, GoBear aggregates and analyzes alternative sources of data to judge lending risk, including patterns in consumer behavior. For example, Chng said if a loan application is filled out in less than a minute, it is more likely to be fraudulent, and applications made between 8:30PM and midnight are less risky than ones made between 2AM to 5AM.

Data points from smartphones is also used to assess creditworthiness in markets like the Philippines, where the credit card penetration rate is less than 10%, but more than 40% of the population uses a smartphone.

Despite the COVID-19 pandemic, Chng said GoBear has been gross margin positive since the end of 2019. Interest in travel insurance has declined, but the company has continued to see demand for other insurance products and lending. Its online insurance brokerage has grown its average order by 52% over the last three months, and the company has seen 50% year-over-year growth from its loan products.

There are other fintech companies in Asia that overlap with some of the services that GoBear offers, like comparison platform MoneySmart, CompareAsiaGroup and Grab Financial Group. In terms of competition, Chng told TechCrunch that not only is the market opportunity in Asia huge (he said there are 400 million underbanked people across GoBear’s seven markets), but the company also differentiates with its three core services, which are all interconnected and draw on the same data sources to score credit.

Chng anticipates that the pandemic will spur more financial institutions to begin digitizing their products and looking for partners like GoBear to help them manage risk. In turn, that will make more financial institutions open to using non-traditional data to score credit, enabling underbanked markets to have increased access to financial products.

“The momentum is here. I think now is the time for tech and data to transform financial services,” he said. “As a platform, we are really looking for partners to come with us for the next phase of growth and investment. I feel positive even with COVID-19, because I think that we will have more acceleration, and the opportunity to change people’s lives and benefit them and investors by solving tough problems will only increase.”

Powered by WPeMatico