sosv

Auto Added by WPeMatico

Auto Added by WPeMatico

Startups developing so-called deep tech often find it challenging to raise capital for various reasons. At TechCrunch Early Stage: Marketing and Fundraising, two experienced investors spoke on the subject and advised startups facing a challenging fundraising path.

Pae Wu and Garrett Winther are both partners at SOSV and run the fund’s programs around biotech and hardware. SOSV doesn’t shy away from startups building complex technology, and because of this, Wu and Winther are well placed to advise on fundraising. They presented three key points targeting startups fundraising for deep tech applications, but the points are applicable to startups of any variety.

Before giving advice, the two acknowledged the nuances across the deep tech ecosystem and each industry. Their presentation is focused on general guidance applicable to nearly every startup.

The first point on Wu and Winther’s presentation sounds a bit self-serving but is based on solid advice. When building a deep tech startup, find the right investor, they said. This is general advice for startups, but according to these two, it’s even more important when building a company that might take longer for the investor to see a return.

In deep tech, it’s essential to think about founder-investor fit. And what we mean by this is understanding why an investor is even in VC in the first place. And what it is that’s driving you, the founder, to do what you do.

And so we look at this fit as a Venn diagram between founders who have a near maniacal devotion to wanting to solve a core systemic problem and investors that thrive on the unique risk profile that comes in deep tech. Because with deep tech, we’re talking about both technical risk, where maybe that insight that is core to the company merely proves that we’re no longer having to break any laws of physics to do whatever it is you’re trying to do. So there’s a big technical risk. (Timestamp: 6:09)

We, as investors, love to see methodical founders who can see the first step that will converge at the right moment of technical and business milestones.

Breakthrough technology hardly came from sudden breakthroughs. As explained in this presentation, it’s critical to set obtainable goals that lead to the desired outcome.

Powered by WPeMatico

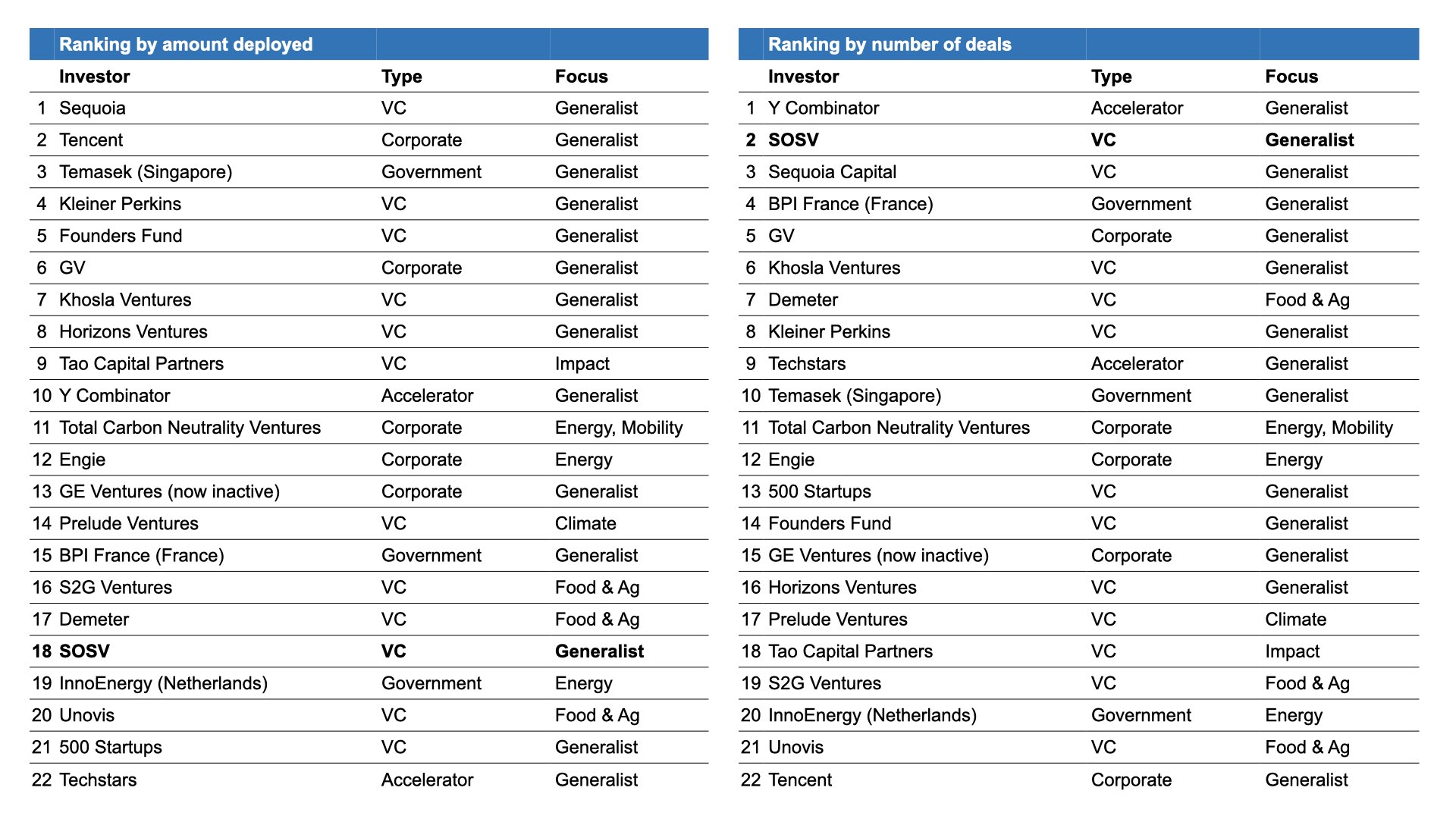

On Earth Day, April 22, SOSV published the SOSV Climate Tech 100, a list of the best startups that we’ve supported from their earliest stages to address climate change. There are always valuable insights embedded in a list like the 100. A TechCrunch story captured the investment perspective, and an SOSV post went deeper into the companies’ category breakdown and founder profiles.

But what can founders learn from the list about climate tech investors? In other words, who invested in the Climate Tech 100? We dug into the “who’s who” of the list, which had more than 500 investors, and here’s what we found.

If you think 500 investors in 100 companies is a lot of investors, you’re right. There are clearly a lot of investors interested in climate tech, and most are generalists just testing the waters. For the Climate Tech 100, about 10% of investors put their money in more than one startup and only seven (less than 2%) wrote a check to four or more. These included Blue Horizon, CPT Capital, EF, Fifty Years, Hemisphere Ventures and Horizons Ventures.

That pattern tracks well with data from PwC, which found that 2,700 unique investors had backed 1,200 startups in its State of Climate Tech 2020 report covering the 2013-2019 period. The report found that only 10 firms out of 2,700 made four or more climate tech deals per year, on average, over the 2013-2019 period. The most active firms are listed in the table below.

Image Credits: PwC, 2020; additional research by SOSV

Capital deployed in climate tech grew at five times the venture capital overall growth rate over the 2013-2019 period.

There is reason to believe that the fragmentation will diminish with the launch of more funds focused on climate tech. Four funds worth more than a billion dollars each have launched since 2020 that fit the description (see chart below).

It’s also encouraging to see that capital deployed in climate tech grew at five times the venture capital overall growth rate over the 2013-2019 period.

Even so, climate tech still only represented 6% of total venture capital deployed in 2019, so there is plenty of room to grow.

Powered by WPeMatico

The world of healthcare has notoriously been described as “broken” — plagued with high-friction workflows, sky-high costs and convoluted business models.

Over the past several years, a long list of innovative startups and salivating venture investors have pinned their focus on repairing the healthcare industry, but its digital transformation still appears to be in the very early innings. After a record-setting 2018, however, digital health investing continued to reach meteoric heights in 2019.

Mammoth pools of capital have flooded into various sub-verticals and business models, backing collections of new B2B and B2C companies focused on optimizing healthcare workflows, improving healthcare access and offering lower-cost distribution models. Over the past two years, digital health startups have raised well over $10 billion in funding across nearly 1,000 deals, according to data from Pitchbook and Crunchbase.

As we close out another strong year for innovation and venture investing in the sector, we asked nine leading VCs who work at firms spanning early to growth stages to share what’s exciting them most and where they see opportunity in the sector:

Participants discuss trends in digital therapeutics, telehealth, mental health and the latest in biotech and medical devices, while also diving into startups improving medical practitioner efficiency, evaluating the evolving regulatory environment and debating valuations and offering a ‘temp check’ on the market for digital health startups leveraging ML.

Although Kleiner Perkins has a long history of investing in iconic health companies, we believe it is still the early innings of digital health as a category today.

When I evaluate new opportunities in the space, I often start by thinking through how the company will move the needle on cost, quality, and access to care — the “iron triangle” of health care systems. Conventional wisdom has been that it’s impossible to improve all three dimensions simultaneously, but we are seeing companies leverage technology to shift this paradigm in meaningful ways.

It’s no longer just a promise. For example, Viz.ai is using artificial intelligence to detect and alert stroke teams to suspected large vessel occlusion strokes, enabling patients to get treatment faster. Their workflows improve access to life-saving care, deliver higher quality through reduced time to treatment (every minute counts as ‘time is brain’ in stroke care), and dramatically reduce the costs associated with long-term disability.

We are also seeing companies provide this type of tech-enabled care outside of the hospital setting. Modern Health is a mental health benefits platform that employers are making available to their employees. The platform triages individual employees to the right level of care, providing clinical care to those with diagnosable depression or anxiety, and making self-guided or preventative care available to everyone else. Their solution improves quality and access by offering mental health services to every employee and reduces the cost associated with untreated mental illness, lost productivity, or employee churn.

Heading into 2020, we’re eager to back digital health companies in new areas that leverage technology to impact cost, quality, and access. A few spaces that I’m excited about are behavioral health (mental health, substance abuse, addiction, etc), care navigation, digital therapeutics, and new models integrating telehealth, remote care and AI to better leverage medical professionals’ time.

Below are some thoughts and coming predictions on health tech broadly:

- Digital therapeutics continue to pick up steam — on the back of Pear and Akili, more companies push to FDA and enter the market. In addition, broader consumer platforms like Calm and Headspace look to broaden their offerings by investigating clinical approvals.

- At least one major pharma looks to expand its consumer surface area by acquiring one of the new digital, consumer-facing generics platform (ex Hims, Ro, NuRx).

- Venture funding for biotech continues to boom with at least three Series A’s of $100M or more in size.

- Drug discovery for neurodegeneration sees a renaissance. High-profile failings of Biogen and the beta-amyloid hypothesis sees a shift of innovation to early-stage biotech and venture creation.

- Big pharma has its DeepMind moment acquiring at least one machine-learning (AI) enabled drug discovery company.

- Clinical trial tech investments heat up; new companies and technologies emerge to make trials patients first and systems get smarter at finding the right patients at their point of care; large incumbents like IQVIA, LabCorp and PPD get acquisitive.

- At least three traditional Sand Hill Road tech venture firms open life science practices or raise dedicated funds.

- Machine learning targets chemistry driven by large advancements in transformer (NLP) models; has the time for computational chemistry finally come?

- HCIT sees a renaissance driven by increased CIO responsibility towards data interoperability. Companies either working on federated ML to allow systems to speak to each other or lightweight edge applications enabling rapid clinical deployment will see quick uptake and traction, until now impossible in HC.

Kristin Baker Spohn, CRV

In the last 10 years, digital health has exploded. Over $16B has been invested in the sector by VCs and we’ve seen IPOs from Livongo, Progyny and Health Catalyst, just in the last year alone. That said, there’s still a lot that mystifies people about the sector — there are spots that are overheated and models that will struggle to deliver venture scale outcomes. I’ve seen digital health evolve first hand as both an operator and investor, and I’m more excited than ever about the future of the space.

A few areas and trends that I’ve been following recently include:

Powered by WPeMatico

The Valley’s affinity for robotics shows no signs of cooling. Technical enhancements through innovations like AI/ML, compute power and big data utilization continue to drive new performance milestones, efficiencies and use cases.

Despite the old saying, “hardware is hard,” investment in the robotics space continues to expand. Money is pouring in across robotics’ billion-dollar sub verticals, including industrial and labor automation, drone delivery, machine vision and a wide range of others.

According to data from Pitchbook and Crunchbase, 2018 saw new highs for the number of venture deals and total invested capital in the space, with roughly $5 billion in investment coming from nearly 400 deals. With robotics well on its way to again set new investment peaks in 2019, we asked 13 leading VCs who work at firms spanning early to growth stages to share what’s exciting them most and where they see opportunity in the sector:

Participants discuss the compelling business models for robotics startups (such as “Robots as a Service”), current valuations, growth tactics and key robotics KPIs, while also diving into key trends in industrial automation, human replacement, transportation, climate change, and the evolving regulatory environment.

Which trends are you most excited in robotics from an investing perspective?

The opportunity to unlock human superpowers:

- Increase productivity to enhance creativity leading to new products and businesses.

- Automating dangerous tasks and eliminating undesirable, dangerous jobs in mining, manufacturing, and shipping/logistics.

- Making the most deadly mode of transport: driving, 100% safe.

How much time are you spending on robotics right now? Is the market under-heated, overheated, or just right?

- Three-quarters of the new opportunities I look at involve some sort of automation.

- The market for robot startups attempting direct human labor replacement, floor-sweeping, and dumb-waiter robots, and robotic lawnmowers and vacuums is OVER heated (too many startups).

- The market for robot startups that assist human workers, increase human productivity, and automate undesirable human tasks is UNDER heated (not enough startups).

Are there startups that you wish you would see in the industry but don’t? Plus any other thoughts you want to share with TechCrunch readers.

I want to see more founders that are building robotics startups that:

- Solve LATENT pain points in specific, well-understood industries (vs. building a cool robot that can do cool things).

- Focus on increasing HUMAN productivity (vs. trying to replace humans).

- Are solving for building interesting BUSINESSES (vs. emphasizing cool robots).

Three years ago, the most compelling companies to us in the industrial space were in software. We now spend significantly more time in verticalized AI and hardware. Robotic companies we find most exciting today are addressing key driver areas of (1) high labor turnover and shortage and (2) new research around generalization on the software side. For many years, we have seen some pretty impressive science projects out of labs, but once you take these into the real world, they fail. In these changing environmental conditions, it’s crucial that robots work effectively in-the-wild at speeds and economics that make sense. This is an extremely difficult combination of problems, and we’re now finally seeing it happen. A few verticals we believe will experience a significant overhaul in the next 5 years include logistics, waste, micro-fulfillment, and construction.

With this shift in robotic capability, we’re also seeing a shift in customer sentiment. Companies who are used to buying outright machines are now more willing to explore RaaS (Robot as a Service) models for compelling robotic solutions – and that repeat revenue model has opened the door for some formerly enterprise software-only investors. On the other hand, companies exploring robotics in place of tasks with high labor shortages, such as trucking or agriculture, are more willing to explore per hour or per unit pick models.

Adoption won’t be overnight, but in the medium term, we are very enthusiastic about the ways robotics will transform industries. We do believe investing in this space requires the right technical know-how and network to evaluate and support companies, so momentum investors looking to dip their hand into a hot space may be disappointed.

We’re entering the early stages of the golden age of robotics. Robotics is already a huge, multibillion-dollar market – but today that market is dominated by industrial robotics, such as welding and assembly robots found on automotive assembly lines around the world. These robots repeat basic tasks, over and over, and are usually separated by caged walls from humans for safety. However, this is rapidly changing. Advances in perception, driven by deep learning, machine vision and inexpensive, high-performance cameras allow robots to safely navigate the real world, escape the manufacturing cages, and closely interact with humans.

I think the biggest opportunities in robotics are those which attack enormous markets where it’s difficult to hire and retain labor. One great example is long-haul trucking. Highway driving represents one of the easiest problems for autonomous vehicles, since the lanes tend to be well-marked, the roads have gentle curves, and all traffic runs in the same direction. In the United States alone, long haul trucking is a multi-hundred billion dollar market every year. The customer set is remarkably scalable with standard trailer sizes and requirements for shipping freight. Yet at the same time, trucking companies have trouble hiring and retaining drivers. It’s the perfect recipe for robotic opportunity.

I’m intrigued by agricultural robots. I’ve seen dozens of companies attacking every part of the farming equation – from field clearing and preparation, to seeding, to weeding, applying fertilizer, and eventually harvesting. I think there’s a lot of value to be “harvested” here by robots, especially since seasonal field labor is becoming harder to find and increasingly expensive. One enormous challenge in this market, however, is that growing seasons mean that the robotic machinery has a lot of downtime and the cost of equipment isn’t as easily amortized in other markets with higher utilization. The other big challenge is that fields are very, very tough on hardware and electronics due to environmental conditions like rain, dust and mud.

There are a ton of important problems to be solved in robotics. The biggest open challenges in my mind are locomotion and grasping. Specifically, I think that for in-building applications, robots need to be able to do all the thing which humans can do – specifically opening and closing doors, climbing stairs, and picking items off of shelves and putting them down gently. Plenty of startups have tackled subsets of these problems, but to date no one has built a generalized solution. To be fair, to get to parity with humans on generalized locomotion and grasping, it’s probably going to take another several decades.

Overall, I feel like the funding environment for robotics is about right, with a handful of overfunded areas (like autonomous passenger vehicles). I think that the most overlooked near-term opportunity in robotics is teleoperation. Specifically, pairing fully automated robotic operations with occasional human remote operation of individual robots. Starship Technologies is a perfect example of this. Starship is actively deploying local delivery robots around the world today. Their first major deployment is at George Mason University in Virginia. They have nearly 50 active robots delivering food around the campus. They’re autonomous most of the time, but when they encounter a problem or obstacle they can’t solve, a human operator in a teleoperation center manually controls the robot remotely. At the same time. Starship tracks and prioritizes these problems for engineers to solve, and slowly incrementally reduces the number of problems the robots can’t solve on their own. I think people view robotics as a “zero or one” solution when in fact there’s a world where humans and robots work together for a long time.

Powered by WPeMatico

Shiru, a new company that’s launching from the latest batch of Y Combinator-backed startups, is joining the ranks of the businesses angling for a spot at the vanguard of the new food technology revolution.

The company was founded by Jasmin Hume, the former director of food chemistry at Just (the company formerly known as Hampton Creek) and takes its name from a homophone of the Chinese shi rou (which Hume has roughly translated to an examination of meat). At Just, Hume was working with a team that was fractionating plants to look at their physical properties to identify what products could be made from the various proteins and chemicals researchers found in the plants.

Shiru, by contrast, is using computational biology to find the ideal proteins for specific applications in the food industry.

The company’s looking at what proteins are best for creating certain kinds of qualities that are used in food additives — things like viscosity building, solubility, foam stability, emulsification and binding, according to Hume.

In some ways, Hume’s approach looks similar to the early product roadmap for Geltor, a company backed by SOSV and IndieBio that was also looking to make functional proteins. The company, which has raised over $18 million to date, shifted its attention to proteins for the beauty industry and cosmetics instead of food — potentially leaving an opening for Shiru to exploit.

Still in its early days, Shiru doesn’t have a product nailed down yet, but the science the company is exploring is increasingly well understood, and Hume says it’s looking at several different genetically engineered feedstocks — from yeasts to undisclosed strains of bacteria and fungi to make its proteins.

“We use the power of molecular design and machine learning to identify protein structures that are more functional than existing alternatives,” says Hume. “The proteins that we are screening for are inspired by nature.”

Hume’s path to founding Shiru involves quite the pedigree. Before Just, she received her doctorate in materials chemistry from New York University, and she’d spent a stretch as a summer associate at the New York-based frontier technology-focused investment firm Lux Capital.

Hume expects to begin pilot production of initial proteins later this year and be producing small but repeatable quantities by the end of 2020.

The company hasn’t raised any outside capital before Y Combinator and is currently in the process of raising a round, Hume said.

Powered by WPeMatico

A week is obviously not enough time to truly understand a market as massive and fascinating as China. Hell, it’s not really even enough time to adjust to the 12-hour time difference from New York. That said, each of the three visits I’ve taken to the country in the past two years has yielded some useful insights into my role as hardware editor here at TechCrunch.

Late last week, I got back from an eight-day trip to Shenzhen in the Guangdong Province of South China and nearby Hong Kong. In some respects, the cities are worlds apart, though a newly opened high-speed rail system has reduced the trip to 30 minutes. Customs issues aside, it’s the height of convenience. Though for political and cultural reasons I’ll not get into here, some have bemoaned the access it’s provided.

This particular visit was sort of a scouting trip. In November, TechCrunch will be hosting its first Hardware Battlefield event in a couple of years. Previous events had been held at CES for reasons of easy access to young startups. This time out, however, we’ve opted to go straight to the source.

Powered by WPeMatico

TechCrunch’s Connie Loizos published some interesting stats on seed and Series A financings this week, courtesy of data collected by Wing Venture Capital. In short, seed is the new Series A and Series A is the new Series B. Sure, we’ve been saying that for a while, but Wing has some clean data to back up those claims.

Years ago, a Series A round was roughly $5 million and a startup at that stage wasn’t expected to be generating revenue just yet, something typically expected upon raising a Series B. Now, those rounds have swelled to $15 million, according to deal data from the top 21 VC firms. And VCs are expecting the startups to be making money off their customers.

“Again, for the old gangsters of the industry, that’s a big shift from 2010, when just 15 percent of seed-stage companies that raised Series A rounds were already making some money,” Connie writes.

As for seed, in 2018, the average startup raised a total of $5.6 million prior to raising a Series A, up from $1.3 million in 2010.

Now on to IPO updates, then a closer look at all the companies raising big rounds. Want more TechCrunch newsletters? Sign up here. Contact me at kate.clark@techcrunch.com or @KateClarkTweets.

![]()

Slack: The workplace communication software provider dropped its S-1 on Friday ahead of a direct listing. That’s when companies sell existing shares directly to the market, allowing them to skip the roadshow and minimize the astronomical fees typically associated with an initial public offering. Here’s the TLDR on financials: Slack reported revenues of $400.6 million in the fiscal year ending January 31, 2019, on losses of $138.9 million. That’s compared to a loss of $140.1 million on revenue of $220.5 million for the year before. Slack’s losses are shrinking (slowly), while its revenues expand (quickly). It’s not profitable yet, but is that surprising?

Zoom was the Slack we thought Slack was all along.

— alex (PVD) (@alex) April 26, 2019

Uber: The ride-hail giant is fast approaching its IPO, expected as soon as next week. On Friday, the company established an IPO price range of $44 to $50 per share to raise between $7.9 billion and $9 billion at a valuation of approximately $84 billion, significantly lower than the $100 billion previously reported estimations. The most likely outcome is Uber will price above range and all the latest estimates will be way off course. Best to sit back and see how Uber plays it. Oh, and PayPal said it would make a $500 million investment in the company in a private placement, as part of an extension of the partnership between the two.

There are a lot of fascinating companies raising colossal rounds, so I thought I’d dive a bit deeper than I normally do. Bear with me.

Carbon: The poster child for 3D printing has authorized the sale of $300 million in Series E shares, according to a Delaware stock filing uncovered by PitchBook. If Carbon raises the full amount, it could reach a valuation of $2.5 billion. Using its proprietary Digital Light Synthesis technology, the business has brought 3D-printing technology to manufacturing, building high-tech sports equipment, a line of custom sneakers for Adidas and more. It was valued at $1.7 billion by venture capitalists with a $200 million Series D in 2018.

Canoo: The electric vehicle startup formerly known as Evelozcity is on the hunt for $200 million in new capital. Backed by a clutch of private individuals and family offices from China, Germany and Taiwan, the company is hoping to line up the new capital from some more recognizable names as it finalizes supply deals with vendors, according to reporting from TechCrunch’s Jonathan Shieber. The company intends to make its vehicles available through a subscription-based model and currently has 400 employees. Canoo was founded in 2017 after Stefan Krause, a former executive at BMW and Deutsche Bank, and another former BMW executive, Ulrich Kranz, exited Faraday Future amid that company’s struggles.

Starry: The Boston-based wireless broadband internet startup has authorized the sale of Series D shares worth up to $125 million, according to a Delaware stock filing. If Starry closes the full authorized raise it will hold a post-money valuation of $870 million. A spokesperson for the company confirmed it had already raised new capital, but disputed the numbers. The company has already raised more than $160 million from investors, including FirstMark Capital and IAC. The company most recently closed a $100 million Series C this past July.

Selina & Sonder: The Airbnb competitor Sonder is in the process of closing a financing worth roughly $200 million at a $1 billion valuation, reports The Wall Street Journal. Investors including Greylock Partners, Spark Capital and Structure Capital are likely to participate. Sonder is four years old but didn’t emerge from stealth until 2018. The startup, which turns homes into hotels, quickly attracted more than $100 million in venture funding. Meanwhile, another hospitality business called Selina has raised $100 million at an $850 million valuation. The company, backed by Access Industries, Grupo Wiese and Colony Latam Partners, builds living/co-working/activity spaces across the world for digital nomads.

Fresh funds: Mary Meeker has made history with the close of her new fund, Bond Capital, the largest VC fund founded and led by a female investor to date. Bond has $1.25 billion in committed capital. If you remember, Meeker ditched Kleiner Perkins last fall and brought the firm’s entire growth team with her. Kleiner said it was a peaceful split that would allow the firm to focus more on its early-stage efforts, leaving the growth investing to Bond. Fortune, however, reported this week that a power struggle of sorts between Meeker and Mamoon Hamid, who joined recently to reenergize the early-stage side of things, was a larger cause of her exit.

Plus, SOSV, a multi-stage venture firm that was founded as the personal investment vehicle of entrepreneur Sean O’Sullivan after his company went public in 1994, has raised $218 million for its third fund. The vehicle has a $250 million target that SOSV expects to meet. Already, the fund is substantially larger than the firm’s previous vehicle, which closed with $150 million.

A grocery delivery startup crumbles: Honestbee, the online grocery delivery service in Asia, is nearly out of money and trying to offload its business. Despite looking impressive from the outside, the company is currently in crisis mode due to a cash crunch — there’s a lot happening right now. TechCrunch’s Jon Russell dives in deep here.

Extra Crunch: “When it comes to working with journalists, so many people are, frankly, idiots. I have seen reporters yank stories because founders are assholes, play unfairly, or have PR firms that use ridiculous pressure tactics when they have already committed to a story.” Sign up for Extra Crunch for a full list of PR don’ts. Here are some other EC pieces to hit the wire this week:

Equity: If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about Kleiner Perkins, Chinese IPOs and Slack & Uber’s upcoming exits.

Powered by WPeMatico

SOSV, a 20-year-old fund with $500 million in assets under management, has been running accelerators for years. Their oldest one, HAX, is the premier hardware accelerator in San Francisco and Shenzhen, and they’ve recently launched a food accelerator in New York and a pair of biology accelerators. Now, however, they’ve just announced DLab, a crypto accelerator that is paired with Cardano to build out distributed apps and solutions.

It is led by Nick Plante, a programmer integral in drafting the JOBS Act and who co-founded Wefunder, a successful crowdfunding platform.

“We can only make this sort of commitment to ecosystems we feel are incredibly compelling; it takes a substantial amount of dedication, education, staffing, and of course the long-term financial commitment to support the space and the companies,” said Plante. “We invest in ecosystems that we identify as ‘macro trends’ like disruptive food, life sciences and synthetic biology, Chinese market entry, IoT and robotics… things that will fundamentally alter the way that we live in the next 100 years.”

“Decentralization is clearly a macro trend, in the macro sense. What’s happening with blockchain and digital ledger technologies has the potential to upend some of the most basic economic incentives that lie beneath the things we do every day; to affect the ways that humans collaborate, identify, trust, govern, and bring new ideas to life… it underlies all of it,” he said.

DLab supplies up to $200,000 in pre-seed funding as well as perks from the SOSV global network of accelerators. They are also offering fellowships in partnership with Cardano to work with projects that would further blockchain research.

“Through last year and the start of this year we kept watching the blockchain ecosystem do some amazing things — along with some criminal things. The surveys and reports about the fraud rates of ICOs and other unpleasantness kept underlining our concerns report after report. The potential for the big economic shifts I mentioned earlier were clearly here but there were so, so many problems; there was a real need for education, for curation, and for proper governance and incentive structures to be put in place,” said Plante.

The group is accepting applications now for a January cohort. The group invests in 150 startups per year, a heady number in these cash-poor times.

Powered by WPeMatico

The dream of a startup founder can often be summarized by the following well-intentioned, and mostly delusional, quote: “We’ll raise a few rounds and in a few years we’ll IPO on Nasdaq.”

But a more likely scenario looks something like this:

You invest a few years of hard work to build something of value. One day you receive an acquisition offer out of the blue. You’re elated. And you’re not prepared. You drop everything to focus on this opportunity. Exclusive due diligence starts. Your company is a mess (IP, contracts, burn). Days become weeks; weeks become months. You’ve neglected business and fundraising. You’re running out of money. M&A is now your one and only option. The buyer says they found a bunch of cockroaches in the walls and drops the price. Now what?

Sound unlikely?

This is still a favorable situation: You had an offer! Think about how much time you invested in your various funding rounds. The hundreds of names and Google spreadsheet or Streak-powered quasi-CRM process.

Have you spent even a fraction of that on understanding exit paths? If you’d rather not live the situation described above, read along.

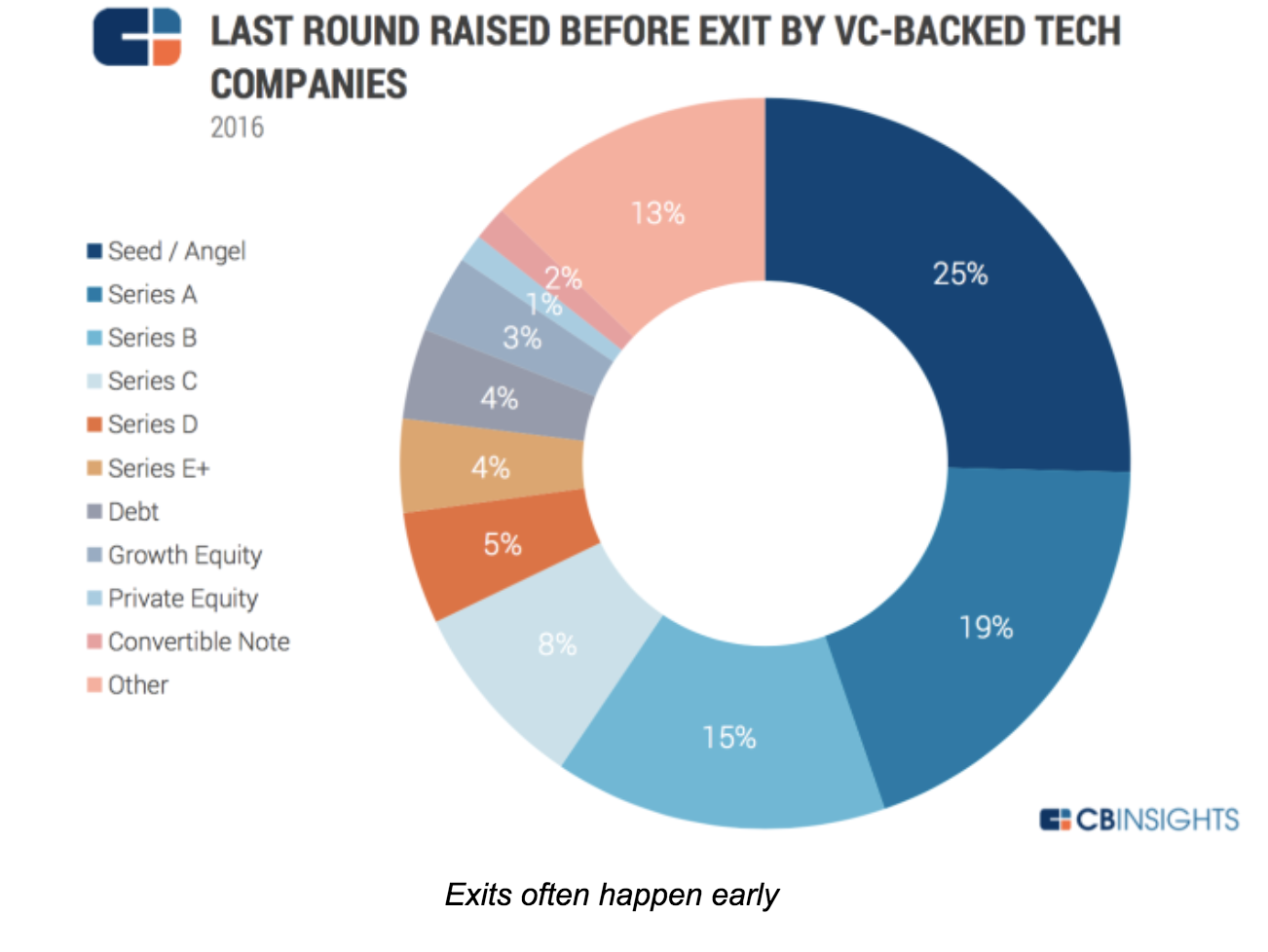

Investors live by exits, but many founders keep dreaming of unicornization and avoid the “E-word” until it’s too late. Yet, in 2016, 97 percent of exits were M&As. And most happened before Series B.

Exits matter because that’s when you, your team and your investors get paid. Oddly enough, and to use a chess metaphor, we hear a lot about the “opening game” (lean startup) and the “mid-game” (growth), but very little about this “end game.”

As a result, founders miss opportunities or leave money on the table. This is a shame. Our fund has more than 700 companies in portfolio. We want the best possible exit for each of them. And fortune favors the prepared! Now, how to get 700 exits (and counting)?

To explore the topic, we organized a series of Master Classes tapping corporate buyers, bankers, investors, lawyers and startup CEOs with M&A or IPO experience in San Francisco. It was a group that included the founders of Guitar Hero — bought by Activision; JUMP Bikes — a SOSV portfolio company bought by Uber, Ubiquisys — bought by Cisco and Withings — bought by Nokia. Each one for hundreds of millions.

Their observations can be summarized below.

“Founders must be aware of what contributes to an exit. This means understanding partnerships and how they are formed in the business space the entrepreneur is working in,” said one Master Class participant.

As founders, you build your product, your company and… optionality. You need to understand the options open to your company, and take steps to enable them.

The most likely one is an acquisition, but there are others like IPO (including small cap), RTO, SBO, LBO, Equity Crowdfunding and even ICO.

“Exit is not a goal per se, but as a CEO it is something you should think about as early in your cycle as possible, while being business-focused,” said the London-based investor Frederic Rombaut, of Seraphim Capital.

Indeed, most participants said that exits should always be on the chief executive’s agenda, no matter how early in the process. “Exits should be on the CEO agenda. Not front and center, but on the agenda. M&A is a by-product of a great business and targeted BD. IPOs are always an option once you’ve built significant cashflow forecasting.”

It’s important to ask questions like: How many “strategic engagements” with potential buyers have you had this month? Is your message and value clear in their eyes? Have you considered an acquisition track in parallel to a fundraise?

It doesn’t stop there:

One thing is sure: The time to exit is not when you’re running out of money.

Unicorn or not, the most likely exit is an acquisition.

As George Patterson, managing director at HSBC in New York said, “Good tech companies are bought, not sold. The question is thus: how to get bought?”

Patterson says it’s important to understand how mergers and acquisitions actually work; how to prepare a startup for an exit; and how to develop a “feel” for the market you’re exiting through and into.

Hearing from corp dev veterans from Cisco, Logitech, Dassault and IBM, a few key ideas emerged:

Motivations vary

It could be from least to most expensive, or as a mix, as listed by Mark Suster, managing partner at Upfront Ventures:

How corporates find you

Corporates find deals via the development of partnerships, investment (CVC), their business units, corp dev research, media and investor connections.

Asked about the best approach, Todd Neville, manager of Corporate Business Development and Strategy at IBM (who gave the most detailed description of the corp dev process), said, “Do something cool to one of the IBM customers. If they rave about even a POC, we’re interested.”

In other words, business development is corporate development.

Get the house in order

Buyers typically want to know three things:

For IP, they will check your contracts (staff and contractors), and run some automated code analysis for proprietary code and open source use. They will evaluate potential IP infringement. No point buying you if you end up costing more in lawsuits!

For your team skills: Sitting down with your engineers will tell them plenty enough without understanding the details of this or that algorithm. The last thing a corporate wants is to be accused of stealing!

Lawyers engaged early can help. The later the clean-up, the more costly and painful.

Develop a feel for your “market”

Develop relationships and create champions within corporates. It will help promote your deal when the time comes, and will let you keep your finger on the pulse of corporate strategy to time your moves.

Do you read the earning calls of Cisco or IBM (or others relevant to you)? This is where strategies are presented. Are your keywords coming up there or in their press releases?

Chris Gilbert, former CEO of Ubiquisys (sold to Cisco for more than $300 million) was very deliberate in planning his exit.

“Selling starts on day one and is a leadership-only function — work out who will be your buyer. Only the CEO can do this. Constantly articulate why a company should buy you,” Gilbert said. Bring clear messages into the acquiring company so it can be presented upwards: give them the presentation you would like them to show their boss! When the time is right, force decisions through competition. If you know they have to buy you, your starting position is strong.”

The dark art of price discovery

There are dozens of formulas (from DCF to comparables) to evaluate a deal — which also means none is “correct.” What matters is: How much would you sell for, and how much is the buyer ready to pay?

Gilbert, at Ubiquisys, described how close interactions with his banker helped drive the price up among the bidders assembled.

Just like buyers, we meet bankers and lawyers too rarely at startup events, but there is much to learn with them. They make deals happen, avoid value erosion and optimize price. They often also make introductions before you engage them, to build goodwill and earn your business.

And if you worry about fees, the right banker handsomely pays for itself by finding more bidders and playing “bad cop” for you, avoiding direct confrontation with your future employer. Do you want a slice of the watermelon or the whole grape?

When asked about what happens after an M&A or IPO, buyers said they generally hoped the founders would stay with them for many years. Often using re-vesting, earn-outs or shares of the acquiring company to incentivize them. Neville, from IBM, mentioned a security company they acquired whose founder is now the head of one of the largest IBM divisions.

In the case of IPOs, supposedly the ultimate “exit,” any block of shares sold by founders would face extreme scrutiny and might cause a price drop.

So who’s exiting during those deals? Investors (and not always).

Eventually, if the average age of a startup at exit is 8-10 years, the active duty period of founders (if not replaced in the meantime) extends even more. Better love the problem you’re solving, and your customers!

Thanks to speakers, participants and supporters of this Master Class series:

London: Frederic Rombaut (Seraphim Capital), Joe Tabberer (FirstBank), Chris Gilbert (Ubiquisys), Jonathan Keeling (Crowdcube), Fred Destin, Tony Fish (AMF Ventures, James Clark (London Stock Exchange), Denise Law (SGCIB).

Paris: Frederic Rombaut (Seraphim Capital), Manuel Gruson (Dassault Systemes), Pierre-Henri Chappaz (Rothschild Global Advisory), Christine Lambert-Goue (All Invest), Olivier Younes (EXPEN), Eric Carreel (Withings), Fabien Bardinet (Balyo), Xavier Lazarus (Elaia Partners), Pierre-Eric Leibovici(Daphni). Jean de La Rochebrochard (Kima Ventures), Jeremy Sartre (SmartAngels), Gwen Regina Tan (Entrepreneur First).

San Francisco: Natasha Ligai (Logitech), Matt Cutler (Cisco),Will Hawthorne, (CODE Advisors), Ryan Rzepecki (JUMP Bikes), Charles Huang (Guitar Hero), Jeff Thomas (Nasdaq), Shahin Farshchi (Lux Capital), Ammar Hanafi (Moment Ventures), Adam J. Epstein (Third Creek Advisors), Nathan Harding (EKSO Bionics), Kate Whitcomb, Anthony Marino and Ethan Haigh (SOSV).

New York: Todd Neville (IBM), George Patterson (HSBC), Ryan Rzepecki (JUMP Bikes), Aaron Kellner (SeedInvest), Jeremy Levine (Bessemer Venture Partners), Taylor Greene (Collaborative Fund), Adam Rothenberg (BoxGroup), Eli Curi (Fenwick & West), Ian Engstrand and Salil Gandhi (Goodwin), Warren Spar(Sparring Partners Capital), Duncan Turner, Vivian Law and Sheng Ge (SOSV).

Powered by WPeMatico

An accelerator for hardware and robotics startups called HAX is holding its 9th Demo Day in San Francisco today. Startups pitching investors there span industries from education to agriculture and medicine. Examples include: FLASH Robotics’ “social robot” EMYS that teaches kids how to speak a new language; Amber Agriculture’s bean-shaped sensors that monitor corn… Read More

An accelerator for hardware and robotics startups called HAX is holding its 9th Demo Day in San Francisco today. Startups pitching investors there span industries from education to agriculture and medicine. Examples include: FLASH Robotics’ “social robot” EMYS that teaches kids how to speak a new language; Amber Agriculture’s bean-shaped sensors that monitor corn… Read More

Powered by WPeMatico