Softbank

Auto Added by WPeMatico

Auto Added by WPeMatico

More than half of the U.S. population has stayed away from considering life insurance because they believe it’s probably too expensive, and the most common way to buy it today is in person. A startup that’s built a platform that aims to break down those conventions and democratize the process by making life insurance (and the benefits of it) more accessible is today announcing significant funding to fuel its rapidly growing business.

Ethos, which uses more than 300,000 data points online to determine a person’s eligibility for life insurance policies, which are offered as either term or whole life packages starting at $8/month, has picked up $100 million from a single investor, SoftBank Vision Fund 2. Peter Colis, Ethos’s CEO and co-founder, said that the funding brings the startup’s valuation to over $2.7 billion.

This is a quick jump for the company: It was only two months ago that Ethos picked up a $200 million equity round at a valuation of just over $2 billion.

It has now raised $400 million to date and has amassed a very illustrious group of backers. In addition to SoftBank they include General Catalyst, Sequoia Capital, Accel, GV, Jay-Z’s Roc Nation, Glade Brook Capital Partners, Will Smith and Robert Downey Jr.

This latest injection of funding — which will be used to hire more people and continue to expand its product set into adjacent areas of insurance like critical illness coverage — was unsolicited, Colis said, but comes on the heels of very rapid growth.

Ethos — which is sold currently only in the U.S. across 49 states — has seen both revenues and user numbers grow by over 500% compared to a year ago, and it’s on track to issue some $20 billion in life insurance coverage this year. And it is approaching $100 million in annualized growth profit. Ethos itself is not yet profitable, Colis said.

There are a couple of trends going on that speak to a wide opportunity for Ethos at the moment.

The first of these is the current market climate: Globally we are still battling the COVID-19 global health pandemic, and one impact of that — in particular given how COVID-19 has not spared any age group or demographic — has been more awareness of our mortality. That inevitably leads at least some part of the population to considering something like life insurance coverage that might not have thought about it previously.

However, Colis is a little skeptical on the lasting impact of that particular trend. “We saw an initial surge of demand in the COVID period, but then it regressed back to normal,” he said in an interview. Those who were more inclined to think about life insurance around COVID-19 might have come around to considering it regardless: It was being driven, he said, by those with pre-existing health conditions going into the pandemic.

That, interestingly, brings up the second trend, which goes beyond our present circumstances, and Colis believes will have the more lasting impact.

While there have been a number of startups, and even incumbent providers, looking to rethink other areas of insurance such as car, health and property coverage, life insurance has been relatively untouched, especially in some markets like the U.S. Traditionally, someone taking out life insurance goes through a long vetting process, which is not all carried out online and can involve medical examinations and more, and yes, it can be expensive: The stereotype you might best know is that only wealthier people take out life insurance policies.

Much like companies in fintech that have rethought how loan applications (and payback terms) can be rethought and evaluated afresh using big data — pulling in a new range of information to form a picture of the applicant and the likelihood of default or not — Ethos is among the companies that is applying that same concept to a different problem. The end result is a much faster turnaround for applications, a considerably cheaper and more flexible offer (term life insurance lasts only as long as a person pays for it), and generally a lot more accessibility for everyone potentially interested. That pool of data is growing all the time.

“Every month, we get more intelligent,” said Colis.

There is also the matter of what Ethos is actually selling. The company itself is not an insurance provider but an “insuretech” — similar to how neobanks use APIs to integrate banking services that have been built by others, which they then wrap with their own customer service, personalization and more — Ethos integrates with third-party insurance underwriters, providing customer service, more efficient onboarding (no in-person medical exams for example) and personalization (both in packages and pricing) around them. Given how staid and hard it is to get more traditional policies, it’s essentially meant completely open water for Ethos in terms of finding and securing new customers.

Ethos’s rise comes at a time when we are seeing other startups approaching and rethinking life insurance also in the U.S. and further afield. Last week, YuLife in the U.K. raised a big round to further build out its own take on life insurance, which is to sell policies that are linked to an individual’s own health and wellness practices — the idea being that this will make you happier and give more reason to pay for a policy that otherwise feels like some dormant investment; but also that it could help you live longer (Sproutt is another also looking at how to emphasize the “life” aspect of life insurance). Others like DeadHappy and BIMA are, like Ethos, rethinking accessibility of life insurance for a wider set of demographics.

There are some signs that Ethos is catching on with its mission to expand that pool, not just grow business among the kind of users who might have already been considering and would have taken out life insurance policies. The startup said that more than 40% of its new policy holders in the first half of 2021 had incomes of $60,000 or less, and nearly 40% of new policy holders were under the age of 40. The professions of those customers also speak to that democratization: The top five occupations, it said, were homemaker, insurance agent, business owner, teacher and registered nurse.

That traction is likely one reason why SoftBank came knocking.

“Ethos is leveraging data and its vertically integrated tech stack to fundamentally transform life insurance in the U.S.,” said Munish Varma, managing partner at SoftBank Investment Advisers, in a statement. “Through a fast and user-friendly online application process, the company can accurately underwrite and insure a broad segment of customers quickly. We are excited to partner with Peter Colis and the exceptional team at Ethos.”

Powered by WPeMatico

News broke this morning that Revolut, a U.K.-based consumer fintech player, raised a Series E round of funding worth $800 million at a valuation of $33 billion. Those figures are breathtaking not only due to their sheer scale, but also thanks to their radical divergence from Revolut’s preceding funding event.

At times, The Exchange, TechCrunch’s markets-and-startups column, runs into two topics worth exploring in a single day. Today is such a day. You can check out our earlier notes on the buy now, pay later startup market and Apple’s entrance into the BNPL space here. Now, let’s talk about neobanks.

As TechCrunch’s Ingrid Lunden wrote earlier today concerning the news:

This latest Series E is being co-led by Softbank Vision Fund 2 and Tiger Global, who appear to be the only backers in this round. It comes on the heels of rumors earlier this month Revolut was raising big. Revolut last raised about a year ago, when it closed out a Series D at $580 million, but what is stunning is how much its valuation has changed since then, growing 6x (it was $5.5 billion last year).

Stunning indeed.

Lunden also went on to report on the company’s changing financial picture based on Revolut’s recently released 2020 results. In this entry, we’re digging more deeply into those financial results and usage metrics detailed by the fintech megacorn.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The picture that emerges is one of a company with a rapidly improving financial image, albeit with some blank spaces regarding recent customer growth.

Powered by WPeMatico

Vianai Systems, an AI startup founded by Vishal Sikka, former chief executive of Indian IT services giant Infosys, said on Wednesday it has raised $140 million in a round led by SoftBank Vision Fund 2.

The two-year-old startup said a number of industry luminaries also participated in the new round, which brings its total to-date raise to at least $190 million. The startup raised $50 million in its seed financing round, but there’s no word on the size of its Series A round.

Details about what exactly the Palo Alto-headquartered startup does is unclear. In a press statement, Dr. Vishal Sikka said the startup is building a “better AI platform, one that puts human judgment at the center of systems that bring vast AI capabilities to amplify human potential.” Sikka, 54, resigned from the top role at Infosys in 2017 after months of acrimony between the board and a cohort of founders.

“Vianai helps its customers amplify the transformation potential within their organizations using a variety of advanced AI and ML tools with a distinct approach in how it thoughtfully brings together humans with technology. This human-centered approach differentiates Vianai from other platform and product companies and enables its customers to fulfill AI’s true promise,” the startup said.

The startup claims it has already amassed as its customers many of the world’s largest and most respected businesses, including insurance giant Munich Re.

Its investors include Jim Davidson (co-founder of Silver Lake), Henry Kravis and George Roberts (co-founders of KKR), and Jerry Yang (founding partner of AME and co-founder of Yahoo). Dr. Fei-Fei Li (co-director of the Stanford Institute for Human-Centered AI) has joined Vianai Systems’ advisory board.

“With the AI revolution underway, we believe Vianai’s human-centered AI platform and products provide global enterprises with operational and customer intelligence to make better business decisions,” said Deep Nishar, senior managing partner at SoftBank Investment Advisers, in a statement. “We are pleased to partner with Dr. Sikka and the Vianai team to support their ambition to fulfill AI’s promise to drive fundamental digital transformations.”

Powered by WPeMatico

Paytm, India’s most valuable startup, confirmed to its shareholders and employees on Monday that it plans to file for an IPO.

In a letter to shareholders and employees, Paytm said that it plans to raise money by issuing fresh equity in the IPO, and also sell existing shareholders’ shares at the event. The startup has offered its employees the option to sell their stakes in the firm.

This is the first time the Noida-headquartered firm, which is valued at $16 billion and has raised over $3 billion to date, has commented on its plans about the IPO. The startup said in the letter that it has received an in-principle approval from the board of directors to pursue the public market.

Paytm, which is backed by Alibaba and SoftBank, hasn’t shared when it plans to file for the IPO, but has sought shareholders’ response to their intention to sell stakes by the end of the month.

Two sources familiar with the matter told TechCrunch that Paytm plans to raise about $3 billion and is targeting a valuation of up to $30 billion in the IPO. Paytm declined to comment.

Paytm’s letter — obtained by TechCrunch — to shareholders on Monday.

This isn’t the first time Paytm has planned to explore the public route. Exactly 10 years ago, long before Paytm established itself as the largest mobile wallet firm and expanded to several financial and commerce services, the startup had filed with the regulator with intentions to become public. The startup at the time cancelled the IPO plan and instead raised money from VCs to explore new avenues for growth.

A lot is riding on a successful IPO of Paytm — which reported a consolidated loss of $233.6 million for the financial year that ended in March this year, down from $404 million a year ago. (The startup’s revenue fell 10% during this period to $437.6 million.) India’s stock markets are yet to be fully tested for tech startups’ stocks in the country — though retail investors have shown good signs in recent years.

The startup, which competes with Google Pay and Flipkart-backed PhonePe, has realigned its payments strategy in recent years to assume a leadership position in the merchant payments market.

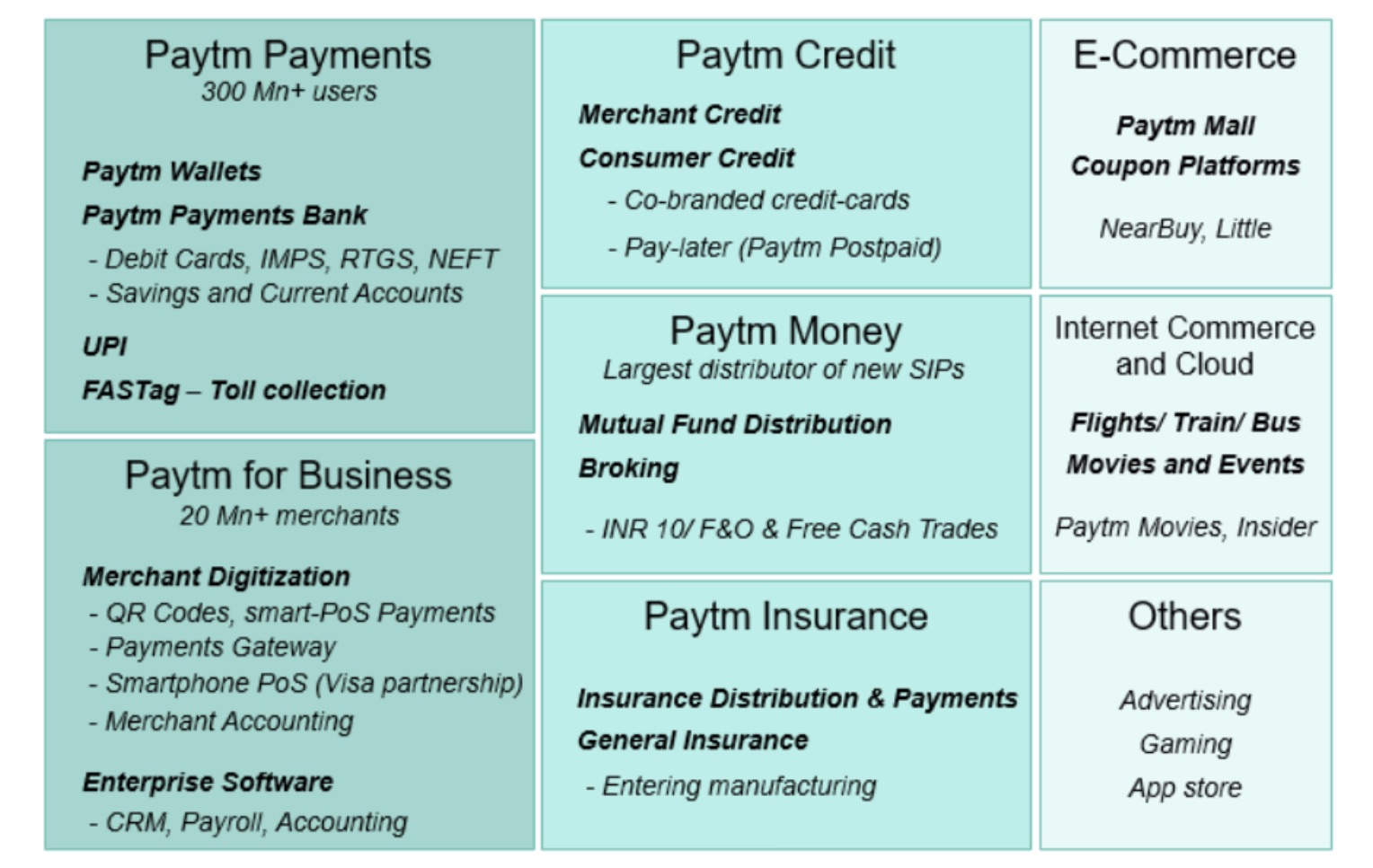

In a report to its clients late last month, analysts at Bernstein said the startup’s credit tech vertical is likely to lead the next wave of its revenue growth.

An overview of Paytm’s financial services ecosystem (Bernstein)

“With the advent of UPI, there has been a rising narrative that questioned Paytm’s market leadership,” the analysts wrote, referring to the exponential growth of payments stack developed by retail banks in India that has been adopted by several firms, including Google and PhonePe (as well as Paytm), and which has somewhat lowered the appeal of mobile wallets in India.

“However, under the hood, Paytm leads on merchant payments and has built an ecosystem of synergistic fintech verticals around its ‘super-app.’ The ecosystem spans payments (wallet/UPI), full-suite merchant acquiring, credit tech, digital bank, wealth, and insurance tech. We believe the super-app battle in India is not a ‘winner takes all’ but a game of execution, business building, and creating a superior customer experience with ecosystem integration,” Bernstein analysts added.

Paytm is the latest Indian giant startup that has expressed an interest in becoming public in recent months. Earlier this year, food delivery startup Zomato said it plans to raise $1.1 billion through an initial public offering. TechCrunch reported last month that Flipkart was in talks to raise over $1 billion in what is expected to be its financial fundraise ahead of an IPO.

Powered by WPeMatico

Just about every week there’s a blockbuster round coming out of South America, but in certain countries such as Ecuador, things have been more hush-hush. However, Kushki, a Quito-based fintech, is bringing attention to the region with today’s announcement of an $86 million Series B and a $600 million valuation.

“We never thought that we would return home [from the U.S.] and build a company that was more valuable in Ecuador than we had built in the U.S.,” said Aron Schwarzkopf, CEO and co-founder of Kushki.

Schwarzkopf and his business partner, Sebastián Castro, previously built and sold a fintech called Leaf in the U.S. in 2014. The two are originally from Ecuador but moved to Boston for college, where they met watching soccer.

Unlike many other fintechs in LatAm that are out to help the unbanked, Kushki works behind the scenes building the tech infrastructure that companies like Nubank use to transfer money. Some of the functionalities they build enable both local and cross-border payment players in credit and debit cards, bank transfers, digital cash, mobile wallets and other alternative payment methods.

“We realized there was a gigantic opportunity to democratize and create infrastructure to move money,” Schwarzkopf told TechCrunch.

The company, which was founded in 2017, already has operations in Mexico, Colombia, Ecuador, Peru and Chile. The Series B will be used to accelerate growth and expand to Brazil and nine other markets in Central America.

Generally, expanding to Brazil is an expensive proposition, and therefore not a path that all companies can take, even though it can be an extremely profitable move if done right. Some of the challenges include the need to translate everything into Portuguese followed by the varying financial regulations.

That’s why Kushki’s approach has to be somewhat custom in each country.

“We focus on going into the markets and we basically rebuild an entire infrastructure, so we put everything into one API,” said Schwarzkopf.

Products similar to Kushki have been successful in other regions around the world, such as in India with Pine Labs, Africa with Flutterwave and Checkout.com, which now has 15 international offices.

To build all this infrastructure, Kushki, which means “cash” in a native Andes dialect, has raised a total of $100 million from SoftBank and an undisclosed global growth equity firm, as well as previous investors including DILA Capital, Kaszek Ventures, Clocktower Ventures and Magma Partners.

“From now until 2060, people will need servers and ways to move money, and we knew that the existing payment infrastructure couldn’t support that,” said Schwarzkopf.

Powered by WPeMatico

Fintech and proptech are two sectors that are seeing exploding growth in Latin America, as financial services and real estate are two categories in particular dire need of innovation in a region.

Brazil’s QuintoAndar, which has developed a real estate marketplace focused on rentals and sales, has seen impressive growth in recent years. Today, the São Paulo-based proptech has announced it has closed on $300 million in a Series E round of funding that values it at an impressive $4 billion.

The round is notable for a few reasons. For one, the valuation — high by any standards but especially for a LatAm company — represents an increase of four times from when QuintoAndar raised a $250 million Series D in September 2019.

It’s also noteworthy who is backing the company. Silicon Valley-based Ribbit Capital led its Series E financing, which also included participation from SoftBank’s LatAm-focused Innovation Fund, LTS, Maverik, Alta Park, an undisclosed U.S.-based asset manager fund with over $2 trillion in AUM, Kaszek Ventures, Dragoneer and Accel partner Kevin Efrusy.

Having backed the likes of Coinbase, Robinhood and CreditKarma, Ribbit Capital has historically focused on early-stage investments in the fintech space. Its bet on QuintoAndar represents clear faith in what the company is building, as well as its confidence in the startup’s plans to branch out from its current model into a one-stop real estate shop that also offers mortgage, title, insurance and escrow services.

The latest round brings QuintoAndar’s total raised since its 2013 inception to $635 million.

Ribbit Capital Partner Nick Huber said QuintoAndar has over the years built “a unique and trusted brand in Brazil” for those looking for a place to call home.

“Whether you are looking to buy or to rent, QuintoAndar can support customers through the entire transaction process: from browsing verified inventory to signing the final contracts,” Huber told TechCrunch. “The ability to serve customers’ needs through each phase of life and to do so from start to finish is a unique capability, both in Brazil and around the world.”

QuintoAndar describes itself as an “end-to-end solution for long-term rentals” that, among other things, connects potential tenants to landlords and vice versa. Last year, it expanded also into connecting a home buyers to sellers.

Image Credits: QuintoAndar

TechCrunch spoke with co-founder and CEO Gabriel Braga and he shared details around the growth that has attracted such a bevy of high-profile investors.

Like most other businesses around the world, QuintoAndar braced itself for the worst when the COVID-19 pandemic hit last year — especially considering one core piece of its business is to guarantee rents to the landlords on its platform.

“In the beginning, we were afraid of the implications of the crisis but we were able to honor our commitments,” Braga said. “In retrospect, the pandemic was a big test for our business model and it has validated the strength and defensibility of our business on the credit side and reinforced our value proposition to tenants and landlords. So after the initial scary moments, we actually felt even more confident in the business that we are building.”

QuintoAndar describes itself as “a distant market leader” with more than 100,000 rentals under management and about 10,000 new rentals per month. Its rental platform is live in 40 cities across Brazil, while its home-buying marketplace is live in four. Part of its plans with the new capital is to expand into new markets within Brazil, as well as in Latin America as a whole.

The startup claims that, in less than a year, QuintoAndar managed to aggregate the largest inventory among digital transactional platforms. It now offers more than 60,000 properties for sale across Sao Paulo, Rio de Janeiro, Belho Horizonte and Porto Alegre. To give greater context around the company’s growth of that side of its platform: In its first year of operation, QuintoAndar closed more than 1,000 transactions. It has now surpassed the mark of 8,000 transactions in annualized terms, growing between 50% and 100% quarter over quarter.

As for the rentals side of its business, Braga said QuintoAndar has more than 100,000 rentals under management and is closing about 10,000 new rentals per month. The company is not profitable as it’s focused on growth, although it’s unit economics are particularly favorable in certain markets such as Sao Paulo, which is financing some of its growth in other cities, according to Braga.

Now, the 2,000-person company is looking to begin its global expansion with plans to enter the Mexican market later this year. With that, Braga said QuintoAndar is looking to hire “top-tier” talent from all over.

“We want to invest a lot in our product and tech core,” he said. “So we’re trying to bring in more senior people from abroad, on a global basis.”

CEO Braga and CTO André Penha came up with the idea for QuintoAndar after receiving their MBAs at Stanford University. As many startups do, the company was founded out of Braga’s personal “nightmare” of an experience — in this case, of trying to rent an apartment in Sao Paulo.

The search process, he recalls, was difficult as there was not enough information available online and renters were forced to provide a guarantor, or co-signer, from the same city or pay rent insurance, which Braga described as “very expensive.”

“Overall, I felt it was a very inefficient and fragmented process with no transparency or tech,” Braga told me at the time of the company’s last raise. “There was all this friction and high cost involved, just real tangible problems to solve.”

The concept for QuintoAndar (which can be translated literally to “Fifth Floor” in Portuguese) was born.

“Little by little, we created a platform that consolidated supply and inventory in a uniform way,” Braga said.

The company took the search phase online for the first time, according to Braga. It also eliminated the need for tenants to provide a guarantor, thereby saving them money. On the other side, QuintoAndar also works to help protect the landlord with the guarantee that they will get their rent “on time every month,” Braga said.

It’s been interesting watching the company evolve and grow over time, just as it’s been fascinating seeing the region’s startup scene mature and shine in recent years.

Powered by WPeMatico

Sinch — a Twilio competitor based out of Sweden that provides a suite of services to companies to build communications and specifically “customer engagement” into their services by way of APIs — has been on a steady funding and acquisitions march in the last several months to scale its business, and today comes the latest development on that front.

The company has announced that it has raised another $1.1 billion in a direct share issue, with significant chunks of that funding coming from Temasek and SoftBank, in order to continue building its business.

Specifically, the company — which is traded on the Swedish stock exchange Nasdaq Stockhom and currently has a market cap of around $11 billion — said that it was making a new share issue of 7,232,077 shares at SEK 1,300 per share, raising approximately SEK 9.4 billion (equivalent to around $1.1 billion at current rates).

Sinch said that investors buying the shares included “selected Swedish and international investors of institutional character,” highlighting that Temasek and SB Management (a direct subsidiary of SoftBank Group Corp.) would respectively take SEK 2,085 million and 0.7 million shares. This works out to a $252 million investment for Temasek, and $110 million for SoftBank.

SoftBank last December took a $690 million stake in Sinch (when it was valued at $8.2 billion). That was just ahead of the company scooping up Inteliquent in the U.S. in January for $1.14 billion to move a little closer to Twilio’s home turf.

Sinch is not saying much more beyond the announcement of the share issue for now, except that the raise was made to shore up its financial position ahead of more M&A activity.

“Sinch has an active M&A-agenda and a track record of successful acquisitions, making [it] well placed to drive continued consolidation of the messaging and [communications platform as a service, CPaaS] market,” it said in a short statement. “Furthermore, the increased financial flexibility that the directed new share issue entails further strengthens the Company’s position as a relevant and competitive buyer.”

The company is profitable and active in more than 40 markets, and CEO Oscar Werner said in Sinch’s most recent earnings report that in the last quarter alone that its communications APIs — which work across channels like SMS, WhatsApp, Facebook Messenger, chatbots, voice and video — handled 40 billion mobile messages.

Notably, its strategy has a strong foothold in the U.S. because of the Inteliquent acquisition. It will be interesting to see how and if it continues to consolidate to build up market share in that part of the world, or whether it focuses elsewhere, given the heft of two very strong Asian investors now in its stable.

“Becoming a leader in the U.S. voice market is key to establish Sinch as the leading global cloud communications platform,” said Werner in January.

While Sinch has focused much of its business, as has Twilio, around an API-based model focused on communications services, its acquisition of Inteliquent also gave it access to a large, legacy Infrastructure-as-a-Service (IaaS) product set, aimed at telcos to provide off-net call termination (when a call is handed off from one carrier to another) and toll-free numbers.

Tellingly, when Sinch acquired Inteliquent, the two divisions each accounted for roughly half of its total business, but the CPaaS business is growing at twice the rate of IaaS, which points to how Sinch views the future for itself, too.

Powered by WPeMatico

Sweden’s Exeger, which for over a decade has been developing flexible solar cell technology (called Powerfoyle) that it touts as efficient enough to power gadgets solely with light, has taken in another tranche of funding to expand its manufacturing capabilities by opening a second factory in the country.

The $38 million raise is comprised of $20M in debt financing from Swedbank and Swedish Export Credit Corporation (SEK), with a loan amounting to $12M from Swedbank (partly underwritten by the Swedish Export Credit Agency (EKN) under the guarantee of investment credits for companies with innovations) and SEK issuing a loan amounting to $8M (partly underwritten by the pan-EU European Investment Fund (EIF)); along with $18M through a directed share issue to Ilija Batljan Invest AB.

The share issue of 937,500 shares has a transaction share price of $19.2 — which corresponds to a pre-money valuation of $860M for the solar cell maker.

Back in 2019 SoftBank also put $20M into Exeger, in two investments of $10M — entering a strategic partnership to accelerate the global rollout of its tech and further extending its various investments in solar energy.

The Swedish company has also previously received a loan from the Swedish Energy Agency, in 2014, to develop its solar cell tech. But this latest debt financing round is its first on commercial terms (albeit partly underwritten by EKN and EIF).

Exeger says its solar cell tech is the only one that can be printed in free-form and different colors, meaning it can “seamlessly enhance any product with endless power”, as its PR puts it.

So far two devices have integrated the Powerfoyle tech: A bike helmet with an integrated safety taillight (by POC), and a pair of wireless headphones (by Urbanista). Although neither has yet been commercially launched — but both are slated to go on sale next month.

Exeger says its planned second factory in Stockholm will allow it to increase its manufacturing capacity tenfold by 2023, helping it target a broader array of markets sooner and accelerating its goal of mass adoption of its tech.

Its main target markets for the novel solar cell technology currently include consumer electronics, smart home, smart workplace, and IoT.

More device partnerships are slated as coming this year.

Exeger’s Powerfoyle solar cell tell integrated into a pair of Urbanista headphones (Image Credits: Exeger/Urbanista)

“We don’t label our rounds but take a more pragmatic view on fundraising,” said Giovanni Fili, founder and CEO. “Developing a new technology, a new energy source, as well as laying the foundation for a new industry takes time. Thus, a company like ours requires long-term strategic investors that all buy into the vision as well as the overall strategy. We have spent a lot of time and energy on this, and it has paid off. It has given the company the resources required, both time and money, to bring an invention to a commercial launch, which is where we are today.”

Fili added that it’s chosen to raise debt financing now “because we can”.

“The same answer as when asked why we build a new factory in Stockholm, Sweden, rather than abroad. We have always said that once commercial, we will start leveraging the balance sheet when securing funds for the next factory. Thanks to our long-standing relationship with Swedbank and SEK, as well as the great support of the Swedish government through EKN underwriting part of the loans, we were able to move this forward,” he said.

Discussing the forthcoming two debut gizmos, the POC Omne Eternal helmet and the Urbanista Los Angeles headphones — which will both go sale in June — Fili says interest in the self-powered products has “surpassed all our expectations”.

“Any product which integrates Powerfoyle is able to charge under all forms of light, whether from indoor lamps or natural outdoor light. The stronger the light, the faster it charges. The POC helmet, for example, doesn’t have a USB port to power the safety light because the ambient light will keep it charging, cycling or not,” he tells TechCrunch.

“The Urbanista Los Angeles wireless headphones have already garnered tremendous interest online. Users can spend one hour outdoors with the headphones and gain three hours of battery time. This means most users will never need to worry about charging. As long as you have our product in light, any light, it will constantly charge. That’s one of the key aspects of our technology, we have designed and engineered the solar cell to work wherever people need it to work.”

“This is the year of our commercial breakthrough,” he added in a statement. “The phenomenal response from the product releases with POC and Urbanista are clear indicators this is the perfect time to introduce self-powered products to

the world. We need mass scale production to realize our vision which is to touch the lives of a billion people by 2030, and that’s why the factory is being built now.”

Powered by WPeMatico

Restoring and preserving the world’s forests has long been considered one of the easiest, lowest-cost and simplest ways to reduce the amount of greenhouse gases in the atmosphere.

It’s by far the most popular method for corporations looking to take an easy first step on the long road to decarbonizing or offsetting their industrial operations. But in recent months the efficacy, validity and reliability of a number of forest offsets have been called into question thanks to some blockbuster reporting from Bloomberg.

It’s against this uncertain backdrop that investors are coming in to shore up financing for Pachama, a company building a marketplace for forest carbon credits that it says is more transparent and verifiable thanks to its use of satellite imagery and machine learning technologies.

That pitch has brought in $15 million in new financing for the company, which co-founder and chief executive Diego Saez Gil said would be used for product development and the continued expansion of the company’s marketplace.

Launched only one year ago, Pachama has managed to land some impressive customers and backers. No less an authority on things environmental than Jeff Bezos (given how much of a negative impact Amazon operations have on the planet), gave the company a shoutout in his last letter to shareholders as Amazon’s outgoing chief executive. And the largest e-commerce company in Latin America, Mercado Libre, tapped the company to manage an $8 million offset project that’s part of a broader commitment to sustainability by the retailing giant.

Amazon’s Climate Pledge Fund is an investor in the latest round, which was led by Bill Gates’ investment firm Breakthrough Energy Ventures. Other investors included Lowercarbon Capital (the climate-focused fund from über-successful angel investor, Chris Sacca), former Uber executive Ryan Graves’ Saltwater, the MCJ Collective, and new backers like Tim O’Reilly’s OATV, Ram Fhiram, Joe Gebbia, Marcos Galperin, NBA All-star Manu Ginobili, James Beshara, Fabrice Grinda, Sahil Lavignia and Tomi Pierucci.

That’s not even the full list of the company’s backers. What’s made Pachama so successful, and given the company the ability to attract top talent from companies like Google, Facebook, SpaceX, Tesla, OpenAI, Microsoft, Impossible Foods and Orbital Insights, is the combination of its climate mission applied to the well-understood forest offset market, said Saez Gil.

“Restoring nature is one of the most important solutions to climate change. Forests, oceans and other ecosystems not only sequester enormous amounts of CO2 from the atmosphere, but they also provide critical habitat for biodiversity and are sources of livelihood for communities worldwide. We are building the technology stack required to be able to drive funding to the restoration and conservation of these ecosystems with integrity, transparency and efficiency” said Saez Gil. “We feel honored and excited to have the support of such an incredible group of investors who believe in our mission and are demonstrating their willingness to support our growth for the long term.”

Customers outside of Latin America are also clamoring for access to Pachama’s offset marketplace. Microsoft, Shopify and SoftBank are also among the company’s paying buyers.

It’s another reason that investors like Y Combinator, Social Capital, Tobi Lutke, Serena Williams, Aglaé Ventures (LVMH’s tech investment arm), Paul Graham, AirAngels, Global Founders, ThirdKind Ventures, Sweet Capital, Xplorer Capital, Scott Belsky, Tim Schumacher, Gustaf Alstromer, Facundo Garreton and Terrence Rohan were able to commit to backing the company’s nearly $24 million haul since its 2020 launch.

“Pachama is working on unlocking the full potential of nature to remove CO2 from the atmosphere,” said Carmichael Roberts from BEV, in a statement. “Their technology-based approach will have an enormous multiplier effect by using machine learning models for forest analysis to validate, monitor and measure impactful carbon neutrality initiatives. We are impressed by the progress that the team has made in a short period of time and look forward to working with them to scale their unique solution globally.”

Powered by WPeMatico

Banking tech startup Zeta is inching closer to the much sought-after unicorn status as it engages with investors to finalize a new round, two sources familiar with the matter told TechCrunch.

SoftBank Vision Fund 2 is in advanced stages of talks to lead a ~$250 million Series D round in the five-year-old startup, the sources said. The investment proposal values the Indian startup, co-founded by high-profile entrepreneur Bhavin Turakhia, at over $1 billion, up from $300 million in its maiden external funding (Series C) in 2019.

The round has yet to close, a third person said.

A SoftBank spokesperson declined to comment.

Five-year-old Zeta helps banks launch modern retail and fintech products. The thesis is that banks — largely operating on antiquated technologies — today don’t have the time and expertise to offer the best experience to hundreds of millions of customers and fintech firms they serve.

Zeta is attempting to help banks either use the startup’s cloud-native, API-first banking stack as its core framework or build services atop it to offer better a experience to all customers — think of improved mobile app and debit and credit features. It also offers API, SDKs and payment gateways to banks to work more efficiently with fintech firms.

The startup has amassed clients in several Asian and Latin American markets.

Turakhia, with his brother Divyank, started his first venture in 1998. Along the way, they sold four web companies to Endurance for $160 million. Zeta is the third startup Bhavin has co-founded since then — the other being business messaging platform Flock and Radix.

When the deal is finalized, Zeta would join a growing list of Indian startups that have turned a unicorn in recent months. Last week, social commerce Meesho — also backed by SoftBank Vision Fund 2 — fintech firm CRED, e-pharmacy firm PharmEasy, millennials-focused Groww, business messaging platform Gupshup and social network ShareChat attained the unicorn status.

The story was updated with additional details and to note that the round hasn’t closed.

Powered by WPeMatico