Softbank

Auto Added by WPeMatico

Auto Added by WPeMatico

Several weeks after it was reported by the WSJ that two of the biggest investors in SoftBank’s massive Vision Fund vehicle were cool on its planned $16 billion investment in the coworking company WeWork, those plans have changed radically, says the Financial Times.

According to its sources — and confirmed by our own — SoftBank is now in “detailed negotiations” to invest a comparatively modest $2 billion more into WeWork, plans that could be firmed up as soon as the end of this week.

A WeWork spokesperson at the company’s New York headquarters declined to comment.

The development is both surprising and unsurprising. The government-backed funds of Saudi Arabia and Abu Dhabi, which committed $45 billion and $15 billion, respectively, to the Vision Fund, haven’t been been known before to push back against the person pulling its levers, SoftBank CEO Masayoshi Son .

Indeed, given the vast sums of money that the Vision Fund has put to work since being announced in late 2016, it seemed there were few if any checks on Son or the 80-plus people who work for the Vision Fund.

Just some of its many bold bets include, most recently, a $500 million investment in Cambridge Mobile Telematics, an eight-year-old, Boston-area company that previously raised just one round of funding of less than $20 million to build out its technology. The Vision Fund also recently led a $400 million round into Emeryville, Ca.-based Zymergen, which manufacturers molecules for a wide array of industries and already counted SoftBank as an investor.

Still, according to that Journal piece, the two anchor investors were less enthusiastic about a giant new investment in nearly nine-year-old WeWork for numerous reasons, including that they see WeWork as a real estate play and both already have plenty of real estate in their portfolios; that WeWork CEO Adam Neumann would still control the company even while SoftBank was looking to acquire a majority stake; and because SoftBank has already committed $8 billion into WeWork in recent years, including through an agreement last year to invest a fresh $4 billion into the company via a convertible note and a $3 billion warrant that gave it the right to buy additional equity in WeWork.

As it stands, including the $2 billion that WeWork looks to receive from SoftBank imminently, SoftBank will have sunk $10 billion into the company. Perhaps it’s no wonder that the newest $2 billion is not coming from the Vision Fund but from SoftBank directly. (Son sometimes invests off SoftBank’s balance sheet directly, for expediency’s sake and, presumably, in a case such as this one, when there may be pushback from Vision Fund investors.)

Either way, $2 billion more from SoftBank is “hardly a stinging rebuke” of WeWork or its business model, says one person familiar with SoftBank’s thinking. This same source also notes that the $16 billion figure bandied about late last year was “never a lock. There were always numerous options on the table.”

Whether SoftBank regrets what remains a huge bet can only be known in time. A shifting public market certainly seems like reason for worry, given that unprofitable WeWork relies increasingly on freely spending corporate customers for its revenue, including both companies that install their employees at WeWork’s coworking spaces, and those that license the company’s technology and aesthetic to WeWork-ify their own offices.

Unsurprisingly, Neumann, when asked how WeWork would fare in a downturn, told us at a Disrupt event in 2017 that it was positioned perfectly. “Business is a flexible thing,” he’d said at the time. “Space is fixed. Being able to give people that flexibility if a recession comes or when a recession comes is actually going to be a very needed product.”

According to the FT, SoftBank’s earlier plans for WeWork included SoftBank and the Vision Fund paying $10 billion to buy out all outside investors in WeWork. A further $6 billion would have been injected directly into the company, including a $2 billion commitment this year, and a commitment to invest a further $4 billion based on agreed-up performance targets for WeWork in 2020 and 2021.

Our sources say that, as of this writing, the $2 billion being discussed will be split evenly to purchase both primary and secondary shares from earlier investors. We’re also told that the company’s post-money valuation, assuming this newest deal is completed, will be $47 billion, a total that includes $1 billion that Softbank invested in WeWork last year via that convertible note and the $3 billion more than the SoftBank committed last year to invest in the company this year.

WeWork’s losses in the first nine months of 2018 nearly quadrupled from a year earlier to $1.2 billion, says the FT, which says it viewed an investor presentation. The company’s sales meanwhile hit $1.5 billion during the same period.

Powered by WPeMatico

Uber is expected to raise $10 billion later this year in one of the largest U.S. initial public offerings in history. The float will value the ride-hailing giant somewhere between $76 billion — the valuation it garnered with its last private financing — and $120 billion — a sky-high figure assigned by Wall Street bankers that’s had even early Uber investors scratching their heads.

A new report from The Information pegs Uber’s initial market cap at $90 billion. To develop the estimate, the site analyzed undisclosed documents Uber provided creditors in 2017 “in which the company projected it would double net revenue to $14.2 billion by 2019,” ran revenue multiples and compared Uber to GrubHub, which investors say is the business’s closest comparison.

Uber declined to comment on The Information’s analysis.

Uber confidentially filed for its long-awaited IPO last month, marking the beginning of a race to the stock markets between it and U.S. competitor Lyft, which filed just hours before, according to a source with knowledge of the situation. Founded in 2009 by Travis Kalanick, Uber has brought in about $20 billion in a combination of debt and equity funding. It counts SoftBank as its largest shareholder in a cap table that also lists Toyota, T. Rowe Price, Fidelity, TPG Growth and many more. As for the skepticism surrounding Uber’s lofty $120 billion valuation, the eye-popping figure seems unachievable considering the company isn’t profitable and has and continues to burn through cash.

An IPO that large would certainly make its investors happy. First Round Capital, for example, seeded Uber with $1.6 million in the company’s first two funding rounds in 2010 and 2011, according to The Wall Street Journal. At a $120 billion valuation, First Round’s shares would be worth some $5 billion. The venture capital firm, however, sold some of its shares to SoftBank alongside Benchmark, which itself would otherwise own shares worth about $14 billion.

Bradley Tusk, an early Uber investor who signed on to help the company surmount political and regulatory barriers in 2011, own shares said to be worth $100 million, though he too gave up 42 percent of his equity in a secondary sale to SoftBank, he recently told TechCrunch.

“I’m quite happy with the 120 number,” Tusk said. “But … I am a little surprised by [it], it does seem to be a really aggressive number.”

“Any investment in Uber is obviously a long-term bet on the future, like someone who invested in Amazon in the early days,” Tusk added. “One thing [Uber chief executive officer Dara Khosrowshahi] is doing well is really expanding Uber into a mobility company as opposed to just a ride-hailing company.”

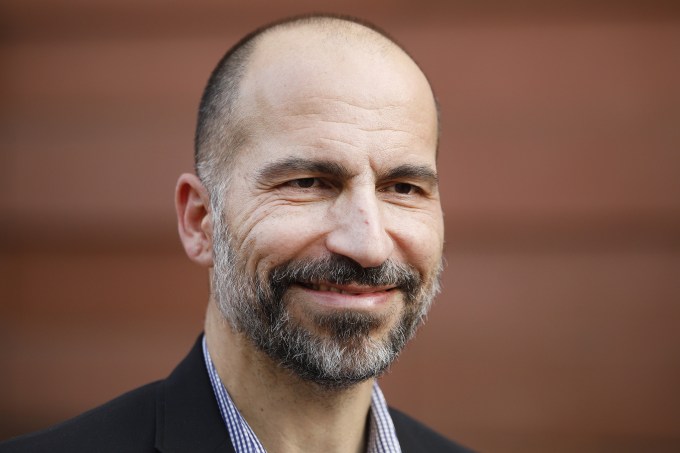

Dara Kowsrowshahi, chief executive officer of Uber, looks on following an event in New Delhi, India, on Thursday, Feb. 22, 2018. Photographer: Anindito Mukherjee/Bloomberg via Getty Images

Uber has opted to go public in a year poised to see the most high-flying unicorn IPOs in history. As we’ve reported in great detail on this site, both Lyft and Uber are planning to float, as are Slack and Pinterest . Many of these companies, however, made the call to make their public markets debut before the stock market took a quick turn south. Poor performing stocks may discourage unicorns from emerging from their cozy VC-protected stalls.

Uber will garner increased scrutiny from Wall Street investors as they begin to parse out its true value. Fortunately the company, which like Amazon has long prioritized growth over profit, has “’clear levers’ it could pull in order to turn on the cash spigots if it wanted to, by reducing its marketing spending both in the U.S. and developing markets and by finding partners to help finance its self-driving car development,” according to The Information. “Pulling those levers would slow revenue growth by a third—from a 33% growth in net revenue to 22 percent growth in net revenue in 2019 [but] it would save Uber $2 billion annually.”

In its third quarter 2018 financial results, Uber posted a net loss of $939 million on a pro forma basis and an adjusted EBITDA loss of $527 million, up about 21 percent quarter-over-quarter. Revenue for Q3 was up five percent QoQ at $2.95 billion and up 38 percent year-over-year.

“We had another strong quarter for a business of our size and global scope,” Uber chief financial officer Nelson Chai said in a statement. “As we look ahead to an IPO and beyond, we are investing in future growth across our platform, including in food, freight, electric bikes and scooters, and high-potential markets in India and the Middle East where we continue to solidify our leadership position.”

We can speculate on Uber’s valuation for days but ultimately Wall Street will determine just how high Uber will go. For now, all we can do is sit and wait for the company to relinquish its S-1 to the masses.

Powered by WPeMatico

Many founders believe in the myth that the first steps of starting a business are the hardest: Attracting the first investment, the first hires, proving the technology, launching the first product and landing the first customer. Although those critical first steps are difficult, they are certainly not the most difficult on the arduous path of building an iconic company. As early and late-stage funding becomes more abundant, founders and their early VC backers need to get smarter about how to position their companies for a looming valley of death in-between. As we’ll learn below, it’s only going to get much, much harder before it gets easier.

Money will have the look, and heft, of dumbbells as the economic cycle turns. Expect an abundance of small, seed checks at one end, an abundance of massive checks for clear, breakout companies at the other, and a dearth of capital for expanding companies with early proof points and market traction. Read more on how to best prepare for this inevitable future. (Image courtesy Flickr/CircaSassy)

There will be an abundance of capital at the two ends of the startup spectrum. At one end, hundreds of seed and micro VCs, each armed with dozens of $250,000-$1 million checks to write every year, are on the prowl for visionary founders with pedigrees and resumes. At the other end, behemoths like SoftBank, sovereigns, as well “early-stage” firms raising larger funds are seeking breakout companies ready for checks that are in the mid-tens to hundreds of millions. There will be a dearth of capital to grow companies from a kernel of a business, to becoming the clear market-defining leader. In fact, we’re already seeing deal volume decreasing significantly as dollars increase, likely evidence of larger checks going into fewer companies.

Even as the overall number of deals decrease below 2012 levels, the overall dollars invested into startups continue to soar. The 200+ “seed-stage” funds formed since 2012 will continue to chase nascent companies. Meanwhile, the increasing number of mega-funds will seek breakout companies into which to make $100 million+ investments. Companies with early traction seeking ~$20 million to grow will be abundant and have difficulty accessing capital.

Founders should no longer assume that their all-star seed and Series A syndicates will guarantee a successful follow-on financing. Progress on recruiting and product development, though necessary, are no longer sufficient for B-rounds and beyond. Founders should be mindful that investors that specialize in leading $20-50 million rounds will have a plethora of well-funded, well-mentored, well-staffed startups with slick presentations, big visions and some early market traction from which to choose.

Today, there is far more capital chasing fewer quality companies. Fewer breakout companies and fear of missing out is making it easy to raise growth rounds with revenue growth, which may not be scalable or even reflective of an attractive business. This is creating false realities and prompting founders to raise big rounds at high prices — which is fine when there is an over-abundance of capital, but can cripple them when capital later becomes scarce. For example, not long ago, cleantech companies, armed with very preliminary sales, raised massive financings from VCs eager to back winners toward scaling into what they characterized as infinite demand. The reality is that the capital required to meet target economics was far greater and demand far smaller. As the private markets turned, access to cash became difficult and most faltered or were acquired for pennies on the dollar.

There is a likely future where capital grows scarce, and investors take a harder look at the underpinnings of revenue, growth and (dis)economies of scale.

What should startup leadership teams emphasize in an inevitable future where the $30 million rounds will be orders of magnitude harder than their $5 million rounds?

Leadership teams put lots of emphasis on revenue. Unfortunately, revenue that’s not representative of the big vision is probably worse than no revenue at all. Companies are initially seeded with the expectation that the founding team can build and sell something. What needs to be proven is the hypothesis that the company can a) build a special product that b) is inexpensive to convince customers to pay for, and c) that those customers represent a massive market. It should be proven that it is unattractive for customers to switch to the inevitable copycats. It should be clear that over time, customers will pay more for additional features, and the cost of acquiring new customers will go down. Simply selling a product to customers that don’t represent that model is worse than not selling anything at all.

Early founding teams are cognitively diverse individuals that can convince early investors that they can overcome the incredible odds of building a company that until now, shouldn’t have existed. They build a unique product, leveraging unique tools satisfying an unmet need. The early teams need to demonstrate the big vision, and that they can recruit the people that can make that vision a reality. Unfortunately, more founders struggle when it comes to recruiting people that have real experience reducing a technology to practice, executing on a product that customers want and charting the path to expand their market with improving unit economics. There are always exceptions of people that do the above for the first time at startups; however, most of today’s iconic startups knew what kind of talent they needed to execute and succeeded in bringing them on board. Who’s on your team?

The attractive SaaS valuation multiples behoove all founders to apply its metrics to their businesses even if they aren’t really SaaS businesses. Sophisticated later-stage investors see right past that and dismiss numbers associated with metrics that are not representative. Semiconductors are about winning dedicated sockets in growing markets. Design tools are about winning and upselling seats in an industry that’s going to be hooked on those tools. Develop a clear understanding of how your business will be measured. Don’t inundate your investor with numbers; present a concise hypothesis for your unfair advantage in a growing market with your current traction being evidence to back it.

“Pouring fuel on the fire” is a misleading metaphor that leads some into believing that capital can grow any business. That’s just as true as watering a plant with a fire hose or putting TNT in your Corolla’s gas tank: most business models and markets simply are not native to the much-sought-after venture growth profile. In fact, most later-stage startups that fail after raising large amounts of capital fail for this reason. Most markets are conducive to businesses with DIS-economies of scale, implying dwindling margins with scale, which is why many businesses are small, serving local, fragmented markets that technology alone cannot consolidate. How do your unit economics improve over time? What are the efficiencies generated by economies of scale? Is there a real network effect that drives these economies?

Image courtesy Getty Images

I expect today’s resourceful founders to seek partners, whether it’s employees, advisors or investors, to help them answer these questions. Together, these cognitively diverse teams will work together to accelerate past any metaphoric valley and build the iconic companies taking humanity to its fantastic future.

Powered by WPeMatico

It appears that most mobile carriers, including O2 and SoftBank, have recovered from yesterday’s cell phone network outage that was triggered by a shutdown of Ericsson equipment running on their networks. That shutdown appears to have been triggered by expired software certificates on the equipment itself.

While Ericsson acknowledged in their press release yesterday that expired certificates were at the root of the problem, you may be wondering why this would cause a shutdown. It turns out that it’s likely due to a fail-safe system in place, says Tim Callan, senior fellow at Sectigo (formerly Comodo CA), a U.S. certificate-issuing authority. Callan has 15 years of experience in the industry.

He indicated that while he didn’t have specific information on this outage, it would be consistent with industry best practices to shut down the system when encountering expired certificates “We don’t have specific visibility into the Ericsson systems in question, but a typical application would require valid certificates to be in place in order to keep operating. That is to protect against breach by some kind of agent that is maliciously inserted into the network,” Callan told TechCrunch.

In fact, Callan said that in 2009 a breach at Heartland Payments was directly related to such a problem. “2009’s massive data breach of Heartland Payment Systems occurred because the network in question did NOT have such a requirement. Today it’s common practice to use certificates to avoid that same vulnerability,” he explained.

Ericsson would not get into specifics about what caused the problem.”Ericsson takes full responsibility for this technical failure. The problem has been identified and resolved. After a complete analysis Ericsson will take measures to prevent such a failure from happening again.”

Among those affected yesterday were millions of O2 customers in Great Britain and SoftBank customers in Japan. SoftBank issued an apology in the form of a press release on the company website. “We deeply apologize to our customers for all inconveniences it caused. We will strive to take all measures to prevent the same network outage.”

As for O2, they also apologized this morning after restoring service, tweeting:

Our 4G network was restored earlier this morning. Our technical teams will continue to monitor service performance closely and we’re starting the full review to understand what happened. We are really sorry for the issues yesterday.

— O2 in the UK (@O2) December 7, 2018

Powered by WPeMatico

A problem with the software in Ericsson equipment is causing outages across the world, including O2 users in Great Britain and SoftBank users in Japan, according to a report in the Financial Times earlier today.

Ericsson took blame for the outage in a press release. It apparently involves faulty software on certain Ericsson equipment used on the affected company’s mobile networks. While Ericsson indicated it involved multiple countries, it appeared to try to minimize the impact by stating it involved “network disturbances for a limited number of customers.” The FT report indicated that it was actually affecting millions of mobile customers worldwide.

Regardless, the company said that an initial analysis attributed the problem to an expired software certificate on the affected equipment. Börje Ekholm, Ericsson president and CEO, said they were working to restore the service as soon as possible, which probably isn’t soon enough for people who don’t have a working cell phone at the moment.

“The faulty software that has caused these issues is being decommissioned and we apologize not only to our customers but also to their customers. We work hard to ensure that our customers can limit the impact and restore their services as soon as possible,” Ekholm said in a statement.

While the press release went on to say they are working to restore the service throughout the day, as of publishing this article, the O2 outage maps still showed problems in the London area and throughout Great Britain.

The AT&T and Verizon outage pages are also currently showing outages in the U.S, but Ericsson reports that these are unrelated to today’s issues with their equipment, which are only affecting customers outside of the US.

(Note that Verizon owns this publication.)

Powered by WPeMatico

First some notes on SoftBank’s rumored expansion into China and its weird fund math, then Foxconn and then quick notes on tech depression, Huawei and more.

TechCrunch is experimenting with new content forms. This is a rough draft of something new — provide your feedback directly to the author (Danny at danny@techcrunch.com) if you like or hate something here.

Kane Wu at Reuters reported overnight that SoftBank is looking to open an office and hire an investment team in China, which Wu says will be based in Shanghai. That’s following the fund’s recent global expansion with new targeted offices in Saudi Arabia and India.

When I saw this, I sort of did a double-take: SoftBank doesn’t have a presence in China? The fund has reportedly been seeking investments in some of China’s leading unicorn stars, including controversial face recognition startup SenseTime, and leading edtech startup Zuoyebang (作业帮, which literally translates as “school assignment help”). (Hat-tips to Selina Wang at Bloomberg, who seems to just be sitting in Vision Fund partner meetings). And of course, it dumped a pretty penny into WeWork China, where it was part of a $500 million syndicate, and is a huge investor in Didi.

It’s sort of obvious that SoftBank would expand to China. What will be interesting though is to see how the fund structures itself long-term. As far as I know, the Vision Fund is a singular “fund” that invests worldwide (send me an email if I am wrong on this count). China has a thicket of regulations on funds and companies, which is one of several reasons we see specifically China-focused vehicles (such as Lightspeed and Lightspeed China or Sequoia and Sequoia China). If the Vision Fund continues to be a unified fund, that would be a notable strategy shift that might be cloned by other trans-Pacific funds.

Rajeev Misra, board director of SoftBank Group and CEO of SoftBank Investment Advisors. Photo by Drew Angerer/Getty Images.

When it first closed the Vision Fund, SoftBank explained they had raised just over $93 billion in committed capital or, more precisely, around $93.15-$93.2 billion, according to the initial investor presentations and its annual Form D filings. In those docs, SoftBank said that the fund was financed with $28 billion from SoftBank and $65 billion from third-party investors.

On top of the $93 billion raised for the Vision Fund, SoftBank detailed that it had committed $4.5 billion of its own capital to a separate “Delta Fund,” which was used to alleviate conflicts around SoftBank’s Didi investment. Thus, SoftBank’s total VC funding aggregates to around $97.7 billion.

To add a complication, SoftBank later shifted $1.6 billion of the Vision Fund’s previously disclosed $65 billion in third-party capital over to the Delta Fund. In current disclosures, SoftBank shows $91.7 billion of committed capital for the Vision Fund ($28.1 billion from SoftBank and $63.6 billion from third-party investors). For the Delta Fund, SoftBank shows $6 billion in committed capital ($4.5 billion SoftBank contribution and $1.6 billion from third-party investors).

Here is where it gets even more complicated. In its latest filings, SoftBank also notes that it completed the interim closing of an additional $5 billion for the Vision Fund in mid-October, “intended for the installment of an incentive scheme for operations of SoftBank Vision Fund.” That additional cash would bring Vision Fund’s total committed capital to $96.7 billion, and $102.7 billion together with the Delta Fund.

While it wouldn’t be included in the committed equity capital total, SoftBank is also rumored to be raising a $4 billion credit facility to help finance additional acquisitions.

So, it’s probably best to say that the Vision Fund — as constituted right now — is $97 billion or $96.7 billion with precision, assuming this $5 billion reaches a final close.

We have, of course, covered SoftBank quite obsessively, particularly its debt situation (Part 1, Part 2, Part 3, Part 4 and Part 5). What we haven’t covered more recently are the latest developments in SoftBank’s IPO, which is slated for December 19th and expected to bring in a haul of $21 billion. More to come on that front in the coming days.

U.S. President Donald Trump and Foxconn Chairman Terry Gou. BRENDAN SMIALOWSKI/AFP/Getty Images

The South China Morning Post reported yesterday that Foxconn is investigating expanding its factories to Vietnam in order to avoid tariffs. Makes sense, and I have some calls this week and next trying to suss out how much hardware supply chains have really changed in response to the trade conflict.

That decision though isn’t just about the trade conflict, but also about the quickly increasing wages of Chinese laborers, as well as political interference from Beijing. The Trump administration’s trade policies are just the excuse Foxconn needs to (at least partially) extricate itself from China, while saving face in the process.

What’s interesting is that Foxconn is also dealing with a massive brush fire in Wisconsin, where it received one of the largest economic development incentives ever offered by an American government, a whopping $3 billion package that was expected to drive manufacturing employment in the state.

Overnight, Republicans in the state legislature passed a bill that would place large restrictions on incoming Democratic governor Tony Evers. Jessie Opoien for the (Madison) Cap Times:

Under the bill, legislators would have increased influence over the Wisconsin Economic Development Corporation, and the WEDC board, not the governor, would appoint the job creation agency’s CEO. However, the governor’s power to appoint a CEO would be restored in September 2019.

That is the agency that provided the Foxconn funding, which has become a political football in Wisconsin politics. Republicans are trying to protect one of the major economic legacies of outgoing governor Scott Walker, as well as what they believe is the future direction of manufacturing work in the state. Democrats smell a boondoggle in the making.

If that wasn’t all, rumored skimpy sales for iPhones is putting enormous pressure on Foxconn’s bottom line. Debby Wu at Bloomberg reported two weeks ago that:

The contract manufacturer aims to cut 20 billion yuan ($2.9 billion) from expenses in 2019 as it faces “a very difficult and competitive year,” according to an internal document obtained by Bloomberg. The company’s spending in the past 12 months is about NT$206 billion ($6.7 billion).

Foxconn is a very dynamic organization that has weathered repeated crises over the years. It is pretty much unique in what it does today: very few other companies can scale up and down hundreds of thousands of workers to meet iPhone and other device demands with such alacrity.

But, the fundamentals of the mobile device market have apparently changed dramatically this year, and Foxconn is likely to be the company most harmed as the assembler of those devices. That could destroy not just the Chinese dream of leading in manufacturing, but also the Vietnam and Wisconsin dreams as well.

Also: If you haven’t read it, this poetry by a Foxconn worker who committed suicide really resonated with me. Foxconn’s suicide problem is well-documented, but we often don’t hear from the individuals themselves.

Blind, the anonymous enterprise chatting app that has taken the tech world by storm, published survey results asking tech employees “I believe I am depressed.” Roughly 40 percent of employees responded yes. Interestingly, there wasn’t too much variation between companies. Amazon had the highest rate at 43 percent and Apple had the lowest rate at 30 percent. It’s an informal survey, probably without high scientific validation, but it is a reminder for all of us in the community that mental health and burnout is very real in the startup and tech ecosystems and we should be vigilant in helping each other when times are rough.

This is one of those stories that we are just going to keep hearing about. After bans in Australia and New Zealand, British Telecom has announced they will not just ban Huawei’s 5G equipment, but also its 3G and 4G equipment. Britain, like Aus/NZ, Canada and the U.S., is part of the Five Eyes intelligence network, and national security officials have been leading the crusade against Huawei infrastructure. What’s interesting is not just the rapidity of the bans, but also that the bans haven’t (from what I have seen) migrated outside the Five Eyes community yet.

Raleigh skyline. Photo by James Willamor used under Creative Commons via Flickr.

Pendo is a digital product management platform that has had quite a bit of success with customers and has raised more than $100 million in VC funding, most recently a Series D from Sapphire. The company announced that they have received a grant from home state North Carolina’s economic development department to grow in the Raleigh region. Pendo is committing $34.5 million to its headquarters (with the potential of creating 590 jobs), while the state will offer around $8.8 million in potential reimbursements over the next 12 years.

Given what I wrote yesterday about Wes McKinney leaving NYC and heading to Nashville and the work Chattanooga is doing to aid startups, it’s great to see other hotspots like Raleigh, NC invest to build out their ecosystems in a compelling way.

Todd Olson, CEO of Pendo, explained to me by email that, “Office rents in our downtown are a fraction of the cost of operating in other cities, and the cost of living is appealing to our employees. They can afford to buy a house here. In some markets around the country, that is becoming more difficult. It’s also just a nice place to live and work.”

Creative work is increasingly going to have to find a lower-cost home.

I am still obsessing about next-gen semiconductors. If you have thoughts there, give me a ring: danny@techcrunch.com.

The LP Anti-Portfolio – Great short read. Lindel Eakman, former managing director at UTIMCO, the University of Texas/Texas A&M endowment, gives a list of funds that he passed on that he now regrets. Unfortunately, this is pretty rare coming from an LP, albeit a former one. It would be great to get more public discussion on which funds were missed and why by LP investors.

Hopefully more reading time tomorrow.

What I’m reading (or at least, trying to read)

Powered by WPeMatico

A flurry of digital-first insurers are betting they can surpass industry incumbents with a little help from technology and a lot of help from venture capitalists.

The latest to land a massive check is Bright Health, a Minneapolis-headquartered provider of affordable individual, family and Medicare Advantage healthcare plans in Alabama, Arizona, Colorado, New York City, Ohio and Tennessee. The company, founded by the former chief executive officer of UnitedHealthcare Bob Sheehy; Kyle Rolfing, the former CEO of UnitedHealth-acquired Definity Health; and Tom Valdivia, another former Definity Health executive, has brought in a $200 million Series C.

The funding values Bright Health at $950 million, according to PitchBook — more than double the $400 million valuation it garnered with its $160 million Series B in June 2017. Sheehy, Bright Health’s CEO, declined to comment on the valuation. New investors Declaration Partners and Meritech Capital participated in the round, with backing from Bessemer Venture Partners, Greycroft, NEA, Redpoint Ventures and others. Bright Health has raised a total of $440 million since early 2016.

VCs have deployed significantly more capital to the insurance technology (insurtech) space in recent years. Startups in the industry, long-known for a serious dearth of innovation, have raked in nearly $3 billion in private capital this year. U.S.-based insurtech startups have raised $2 billion in 2018, a record year for the sector and more than double last year’s total.

Deal count, meanwhile, is swelling. In 2016, there were 72 deals conducted in the space, followed by 86 in 2017 and 94 so far this year, again, according to PitchBook’s data.

Oscar Health, the health insurance provider led by Josh Kushner, is responsible for about 25 percent of the capital invested in U.S. insurtech startups this year. The company has raised a total of $540 million across two notable deals in 2018. The first saw Oscar pulling in $165 million at a $3 billion valuation and the second, announced in August, had Alphabet investing a whopping $375 million. Devoted Health, a Waltham, Mass.-based Medicare Advantage startup, followed up with a massive round of its own. The company nabbed $300 million and announced that it would begin enrolling members to its Medicare Advantage plan in eight Florida counties. Devoted is led by Todd Park, the co-founder of Athenahealth and Castlight Health.

Bright Health co-founders Bob Sheehy, CEO; Tom Valdivia, chief medical officer; and Kyle Rolfing, president

VC’s interest in insurtech isn’t limited to healthcare.

Hippo, which sells home insurance plans at lower premiums, officially launched in 2017 and has brought in $109 million to date. Earlier this month the company announced a $70 million Series C funding round led by Felicis Ventures and Lennar Corporation. Lemonade, which is similarly an insurer focused on homeowners, raised $120 million in a SoftBank-led round late last year. And Root Insurance, an app-based car insurance company founded in 2015, itself raised a $100 million Series D led by Tiger Global Management in August. The financing valued the company at $1 billion.

Together, these companies have raised well over $1 billion this year alone. Why? Because building a health insurance platform is incredibly cash-intensive and particularly difficult given the breadth of incumbents like Aetna or UnitedHealth. Sheehy, considering his 20-year tenure at UnitedHealthcare, may be especially well-positioned to disrupt the industry.

The opportunity here for investors and startups alike is huge; the health insurance market alone is forecasted to be worth more than $1 trillion by 2023. Companies that can leverage technology to create consumer-friendly, efficient and, most importantly, reasonably priced insurance options stand to win big.

As for Bright Health, the company plans to use its $200 million infusion to rapidly expand into new markets, planning to triple its geographic footprint in 2019.

“Bright Health has continued to execute at a fast pace towards our goal of disrupting the old health care model that places insurers at odds with providers,” Sheehy said in a statement. “[Its] current high re-enrollment rate shows that consumers are ready for this improved healthcare experience – especially when it is priced competitively.”

Powered by WPeMatico

WeWork has picked up another $3 billion in financing from SoftBank Corp, not to be confused with SoftBank Vision Fund. The deal comes in the form of a warrant, allowing SoftBank to pay $3 billion for the opportunity to buy shares before September 2019 at a price of $110 or higher, ultimately valuing WeWork at $42 billion minimum.

In August, SoftBank Corp invested $1 billion in WeWork in the form of a convertible note.

According to the Financial Times, SoftBank will pay WeWork $1.5 billion on January 15, 2019 and another $1.5 billion on April 15.

SoftBank is far and away WeWork’s biggest investor, with SoftBank Vision Fund having poured $4.4 billion into the company just last year.

The real estate play out of WeWork is just one facet of the company’s strategy.

More than physical land, WeWork wants to be the central connective tissue for work in general. The company often strikes deals with major service providers at “whole sale” prices by negotiating on behalf of its 300,000 members. Plus, WeWork has developed enterprise products for large corporations, such as Microsoft, who tend to sign longer, more lucrative leases. In fact, these types of deals make up 29 percent of WeWork’s revenue.

The biggest issue is whether or not WeWork can sustain its outrageous growth, which seems to have been the key to its soaring valuation. After all, WeWork hasn’t yet achieved profitability.

Can the vision become a reality? SoftBank seems willing to bet on it.

Powered by WPeMatico

Some more comments from readers on the changing culture around startups filing their Form Ds with the SEC, and then a short update on SoftBank and a bunch more article reviews.

We are experimenting with new content forms at TechCrunch. This is a rough draft of something new – provide your feedback directly to the authors: Danny at danny@techcrunch.com or Arman at Arman.Tabatabai@techcrunch.com if you like or hate something here.

If you haven’t been following our obsession with Form Ds, be sure to read our original piece and follow up. The gist is that startups are increasingly foregoing filing a Form D with the SEC that provides details of their venture rounds like investment size and main investors in order to stay stealth longer. That has implications for journalists and the public, since we rely on these filings in many cases to know who is funding what in the Valley.

Morrison Foerster put together a good presentation two years ago that provides an overview of the different routes that startups can take in disclosing their rounds properly.

Traditionally, the vast majority of startups used Rule 506 for their securities, which mandates that a Form D be filed within 15 days of the first money of the round closing. These days though, more and more startups are opting to use Section 4(a)(2), which doesn’t require a Form D, but also doesn’t provide a “blue sky” exception to start securities laws, which means that startups have to file in relevant state jurisdictions and no longer have preemption from the SEC.

David Willbrand, who chairs the Early Stage & Emerging Company Practice at Thompson Hine LLP, read our original articles on Form Ds and explained by email that the practices around securities disclosures have indeed been changing at his firm and others:

We started pushing 4(a)(2) very hard when our clients kept getting “outed” thru the Form D and upset about it. In my experience, for 99% is the desire to remain in stealth mode, period.

[…]

When I started in 1996, Form Ds were paper, there was no internet, and no one looked. Now they are electronic and the media and blogs scrape daily and publish the information. It actually really is true disclosure! And it’s kind of ironic, right, which goes to your point – now that it’s working, these issuers don’t want it.

[…]

What I find is that the proverbial Series A is the brass ring, and issuers wants to call everything seed rounds (saving the title) until something chunky shows up, and stay below the radar too. So they pop out of the cake publicly for the first time with a big “Series A” that they build press around – and their first Form D.

Another piece of feedback we received was from Augie Rakow, the co-founder and managing partner of Atrium, which bills itself as a “better law firm for startups” that TechCrunch has covered a few times before. He wrote to us that in addition to the media concerns, startups also have to be aware of the broad cross-section of interested parties to Form Ds that hasn’t existed in the past:

Today, there is a bigger audience in terms of who cares about venture backed companies. Whether this spun off from the launch of the Facebook movie or the fact that over two billion people across the global have the internet at their fingertips via smartphones, people are connected and curious. The audience is not only larger but also encompasses more national and international interests. This means there are simply more eyes on trends, announcements, and intel on privately held companies whether they are media, investors, or your competitors. Companies that have a good reason to stay stealth may want to avoid attracting this attention by not making a public Form D filing.

For startups, the obvious advice is to just consult your attorney and consider the tradeoffs of having a very clean safe harbor versus more work around regulatory filings to stay stealthy.

But the real message here is for journalists. Form Ds are no longer common among seed-stage startups, and indeed, startup founders and venture investors have a lot of latitude in choosing how and when they file. You can no longer just watch the SEC’s EDGAR search platform and break stories anymore. Building up a human sourcing capability is the only way to get into those early investment rounds today.

Finally — and this is something that is hard to prove one way or the other — the lack of disclosure may also mean that the fears around seed financing dropping off a cliff may be at least a little bit unfounded. Eliot Brown at the Wall Street Journal reported just yesterday that the number of seed financings is down 40 percent, according to PitchBook data. How much of that drop is because of changing macroeconomic conditions, versus changes in filing disclosures?

Tokyo Stock Exchange. Photo by electravk via Getty Images

Last week, I also got obsessed with SoftBank. The company confirmed today that it intends to move forward with the IPO of its Japanese mobile telecom unit, according to WSJ and many other sources. The company is targeting more than $20 billion in proceeds, and its overallotment could drive that above $25 billion, or roughly the level of Alibaba’s record IPO haul.

One interesting note from Taiga Uranaka at Reuters on the public issue is that everyday investors will likely play an outsized role in the IPO process:

Yet SoftBank’s brand name is still likely to draw retail investors long accustomed to using SoftBank’s phone and internet services. Many still see CEO Son as a tech visionary who challenged entrenched rivals NTT DoCoMo Inc ( 9437.T ) and KDDI, and brought Apple Inc’s ( AAPL.O ) iPhone to Japan.

Japanese households are commonly seen as an attractive target in IPOs with their 1,829 trillion yen in financial assets, even if they are traditionally risk-averse with over 50 percent of assets in cash and deposits.

More than 80 percent of the shares will be offered to domestic retail investors, a person with knowledge of the matter told Reuters.

Pavel Alpeyev at Bloomberg noted that “SoftBank is looking to tempt investors with a dividend payout ratio of about 85 percent of net income, according to the filing. Based on net income in the last fiscal year, that would work out to an almost 5 percent yield at the indicated IPO price.” A higher dividend ratio is particularly attractive to retired individual investors.

Despite SoftBank’s horrifying levels of debt, Japanese consumers may well save the company from itself and allow it to effectively jump start its balance sheet yet again. Complemented with a potential Vision Fund II, Masayoshi Son’s vision for a completely transformed SoftBank seems waiting for him in the cards.

Tech C.E.O.s Are in Love With Their Principal Doomsayer – Nellie Bowles writes a feature on Yuval Noah Harari, the noted philosopher and popular author of Sapiens. Bowles investigates the paradoxical popularity of Harari, who sees technology as creating a permanent “useless class” and criticizes Silicon Valley with his now enduring popularity in the region. Interesting personal details on the somewhat reclusive Israeli, but ultimately the question of the paradox remains sadly mostly unanswered. (2,800 words)

Why Doctors Hate Their Computers – Atul Gawande discusses learning and using Epic, the dominant electronic medical records software platform, and discovers the challenges of building static software for the complex adaptive system that is health care. His observations of the challenges of software engineering will be well-known to anyone who has read Fred Brooks, but the piece does an excellent job of exploring the balancing act between the needs of technocratic systems and the human design needed to make messy and complicated professions work. Worth a read. (8,900 words)

Picking flowers, making honey: The Chinese military’s collaboration with foreign universities – An excellent study by Alex Joske at the Australia Strategic Policy Institute on the hundreds of military scientists from China who use foreign academic exchanges as a means of information acquisition for critical scientific and engineering knowledge, including in the United States. China’s government under Xi Jinping has made indigenous technology development a chief domestic priority, and the U.S. innovation economy is encouraged to increasingly guard its intellectual property. (6,500 words)

The Digital Deciders – New America report by Robert Morgus who investigates the fracturing of the internet, which I have written about at some length. Morgus finds that a small group of countries (the “digital deciders”) will determine whether the internet continues to be open or whether nationalist interests will close it off. Let’s all hope that Iraq believes in freedom of expression and not Chinese-style surveillance. Worth a skim. (45 page report, but with prodigious tables)

Powered by WPeMatico

This week, I’ve tried to do something new at TechCrunch with this experimental column — getting obsessed about a topic broadly in tech and writing a continuous stream of thoughts and analysis about it.

With my research consultant and contributor Arman Tabatabai, we’ve covered two topics: Form Ds, the filing that startups usually submit to the SEC after a venture round closes (although increasingly do not), and SoftBank, which faces all kinds of strategic pressure due to its debt binging. If you missed the other episodes, here are links to the editions from Monday, Tuesday, Wednesday and Thursday.

We are experimenting with new content forms at TechCrunch. This is a rough draft of something new — provide your feedback directly to the authors: Danny at danny@techcrunch.com or Arman at Arman.Tabatabai@techcrunch.com if you like or hate something here.

Today, one final round of thoughts on SoftBank and Rakuten (heavily written by Arman) and a lengthy list of articles for your weekend reading.

BEHROUZ MEHRI/AFP/Getty Images

Understanding SoftBank’s competitive strategy requires a bit of a deep dive into Japanese e-commence giant Rakuten.

Rakuten has been struggling to compete with Amazon and others like SoftBank’s Yahoo! Japan. So at the end of 2017, Rakuten announced it would be entering the telco space, hoping that operating its own network could generate user growth through better incentives around mobile shopping, streaming and payments.

Today, Japan’s telco space is a relatively cozy oligopoly dominated by NTT DoCoMo, au-KDDI and SoftBank. A major reason why Rakuten feels it can succeed where others have failed to break in is because it has the government on its side.

Rakuten’s plan to offer prices at least 30 percent lower than incumbent rates has led to favorable treatment from Prime Minister Shinzo Abe’s government, which has been looking for ways to stimulate market competition to force lower the country’s high phone prices.

Though a new entrant hasn’t been approved to enter the telco market since eAccess in 2007, Rakuten has already gotten the thumbs-up to start operations in 2019. The government also instituted regulations that would make the new kid in town more competitive, such as banning telcos from limiting device portability.

Rakuten’s partnerships with key utilities and infrastructure players will also allow it to build out its network quickly, including one with Japan’s second largest mobile service provider, KDDI.

Just last week, Rakuten and KDDI announced an agreement where Rakuten will help KDDI utilize its payment and logistics infrastructure as KDDI turns its head toward e-commerce and payments, while KDDI will give Rakuten access to its network and nationwide roaming services, allowing Rakuten to provide nationwide service as its builds out its own infrastructure.

The agreement with KDDI is especially scary for SoftBank, the country’s third biggest telco and one of Rakuten’s e-commerce competitors, and whose customers seem most vulnerable to churn. The partnership also makes it seem even more likely that SoftBank’s competitors are looking to push it out of the market or turn into a dud its upcoming mobile segments IPO.

While Rakuten’s head-first dive into the market won’t ease investors into an IPO, it’s important we note that Rakuten is targeting a much smaller market share than the incumbents, targeting 10 million subscribers by 2028, a number lower than the company’s original 15 million subs goal and significantly lower than the 76 million, 52 million and 40 million subscribers NTT, KDDI and SoftBank (respectively) hold currently. And even with its agreements, Rakuten faces a serious and expensive uphill battle in building out its network infrastructure quickly enough to compete.

Ultimately, Rakuten’s telco initiative is a splash, but one that seems like it will merely make its competitors wet and not drown them. For SoftBank, it is an annoying distraction on its telco IPO roadshow, but a distraction that is easily explained to potential investors.

Rajeev Misra. Photo by Drew Angerer/Getty Images

Changing gears from Rakuten, emails from readers this week asked us to look deeper into SoftBank’s performance over the last two decades. As we did so, it became clear that SoftBank has had a long history of price competitions and new entrants across its businesses, and it has proven its ability to operate and consistently grow earnings.

Since 2000, SoftBank has grown earnings at a ~30 percent CAGR and experienced revenue growth in all but one year. When eAccess did enter the telco market and picked up four million subscribers, SoftBank bought it and integrated it into its own system.

As we discussed earlier this week, despite having always held on to a clunky amount of debt, SoftBank has managed to deliver consistent growth by making sure its revenue and operating growth outpaced the upticks in its debt and interest expense.

A great example of this came after SoftBank’s acquisition of Vodafone in 2006, when it saw a huge spike in its interest expense, but also in its operating income.

Over the following five years, SoftBank managed to reduce its interest expense at an annual rate of 12 percent while growing its operating income at 16 percent. And regardless of its debt balances, SoftBank has always seemingly been able to secure funding one way or another, as shown by its ability to raise $90+ billion for the Vision Fund in less than a year from when plans for the fund were first reported.

The Vision Fund itself started as a way for SoftBank to continue to invest while its balance sheet was tight due to nearly back-to-back massive acquisitions of Sprint and Arm. Just look at how Rajeev Misra, who oversees the Vision Fund, discussed its creation in an interview with The Economic Times:

We had just bought ARM in June for $32 billion and Masa felt we are on the cusp of a technology revolution over the next 5-10 years with machine learning, AI, robotics and the impact of that in disrupting every industry – from healthcare to financial services to manufacturing.

We felt the world was going through a new industrial revolution. We were constrained financially given that we just did a $32-billion acquisition.

SoftBank, historically over the last 20 years, has invested from its own balance sheet. So, we had two options.

Either monetise some of the gains we made in Alibaba which we decided has a lot more upside… Alibaba has more than doubled in the last 12 months. So we decided to keep it which turned out to be good decision. The second option was to go out and raise money and co-invest with others. We prepared a presentation, went out, and by god’s grace we raised the fund.

Even before the Vision Fund, SoftBank has always had a strategy to make big bets in industries of the future. And while many have failed, the several that have paid off, like its $20 million investment in Alibaba, had massive cash outs that have driven consistent earnings growth for decades. SoftBank seems to be banking its future on the same strategy and, frankly, it’s unclear how much they even care about how competitive their telco is, as shown by this exchange in the same interview with Misra:

Question: What about sectors like telecom?

Misra: Let the dust settle.

Our obsession with SoftBank this week is probably going to subside, and we are in the market for our next deep dive topic in tech and finance. Have ideas? Drop us a line at danny@techcrunch.com and arman.tabatabai@techcrunch.com

Photo by Darren Johnson / EyeEm via Getty Images

The CIA’s communications suffered a catastrophic compromise. It started in Iran. This is a great follow-up from Yahoo News’ Zach Dorfman and Jenna McLaughlin on one of the most important espionage stories this past decade. The CIA, using an internet-based communications system to connect with spies and sources in the field, failed to keep the security of the system intact, leading to the dismantling of its Iranian, Chinese and potentially other espionage rings. This article advances the story as we know it from the New York Times’ original piece, and Foreign Policy’s excellent follow up also written by Zach Dorfman. Definitely worth a read from a security/technical audience. (3,200 words)

The $6 Trillion Barrier Holding Electric Cars Back. Don’t read — the answer is infrastructure. (1,000 words, but should be one)

The Rodney Brooks Rules for Predicting a Technology’s Commercial Success. A a good reminder that some technologies are much closer to reality than others, and that the key difference between them is our collective experience handling the technology. Rodney Brooks is the right person to cover this subject, although one can’t help but feel that every example is Musk-inspired. (2,800 words)

Uber’s economics team is its secret weapon by Alison Griswold & Soon there may be more economists at tech companies than in policy schools by Roberta Holland, both in Quartz . Griswold does a great job giving an overview of how Uber is using economists not just to improve its product for end users, but also to shape the discussion of public policy around the company. Clearly, Uber is not alone; as Holland notes in her piece, academic economists are very popular in Silicon Valley right now, with salaries that can match the top machine learning experts. (2,750 words and 1,200 words, respectively)

The future’s so bright, I gotta wear blinders. A short piece by Nicholas Carr fighting back against the notion that computing is still “at the beginning.” Many of our devices and pieces of software are already decades old — if they haven’t had an effect on human behavior or productivity, when are they going to? A useful antidote to some ideas we hear from the Valley every single day. (900 words)

The future of photography is code. Yes, yes, I am very late to this — blame Pocket disease. TechCrunch’s own Devin Coldewey writes a candid essay on the transition from improving photography through hardware like lenses to improving photos through computation. The future is looking very bright for beautiful photos, indeed. (2,400 words)

Freedom on the Net 2018 | Freedom House. And if you are looking for some depressing news, Freedom House’s report (which I am also a bit late to) is dreary. China is now increasingly the source of authoritarian internet control technology, and countries across the world are backtracking on internet freedom (including the U.S.). Sobering, but with so much riding on the openness of the internet, we all need to pay attention and build the kind of future for this technology that we want. (32 page PDF with exec summary)

What we are reading (or at least, trying to read)

Powered by WPeMatico