Softbank Vision Fund

Auto Added by WPeMatico

Auto Added by WPeMatico

Trendyol, an e-commerce platform based in Turkey, has raised $1.5 billion in a massive funding round that values the company at $16.5 billion. General Atlantic, SoftBank Vision Fund 2, Princeville Capital and sovereign wealth funds, ADQ (UAE) and Qatar Investment Authority co-led the round.

The deal marks SoftBank’s first in the country.

The new financing also makes Trendyol Turkey’s first decacorn, and among the highest-valued private tech companies in Europe. It comes just months after strategic — and majority — backer Alibaba invested $350 million in the company at a $9.4 billion valuation.

Founded in 2010, Trendyol ranks as Turkey’s largest e-commerce company, serving more than 30 million shoppers and delivering more than 1 million packages per day. It claims to have evolved from marketplace to “superapp” by combining its marketplace platform (which is powered by Trendyol Express, its own last-mile delivery solution) with instant grocery and food delivery through its own courier network (Trendyol Go), its digital wallet (Trendyol Pay), consumer-to-consumer channel (Dolap) and other services.

Image Credits: Founder Demet Mutlu / Trendyol

Trendyol founder Demet Suzan Mutlu said the new capital will go toward expansion within Turkey and globally. Specifically, the company plans to continue investing in nationwide infrastructure, technology and logistics and toward accelerating digitalization of Turkish SMEs. She said the company was founded to create positive impact and that it intends to continue on that mission.

Evren Ucok, Trendyol’s chairman, added that part of the company’s goal is to create new export channels for Turkish merchants and manufacturers.

Melis Kahya Akar, managing director and head of consumer for EMEA at General Atlantic, said that Trendyol’s marketplace model — ranging from grocery delivery to mobile wallets — “brings convenience and ease to consumers” in Turkey and internationally.

“Turkey is one of the fastest growing economies in the world and benefits from attractive demographics, with a young population that is very active online,” wrote General Atlantic’s Kahya Akar via e-mail. “We expect its already sizable e-commerce market –$17 billion in 2020 – to continue to grow meaningfully on the back of growing online penetration. We think Trendyol is ideally positioned to meet the needs of consumers in Turkey and around the world as the company expands.”

A 2020 report by JPMorgan found that e-commerce represented only 5.3% of the overall Turkish retail market at the time but that Turkish e-commerce had notched impressive leaps in revenues in recent years: 2018 alone saw the market jump by 42%, followed by 31% in 2019. As of 2020, 67% of the Turkish population were making purchases online.

Powered by WPeMatico

Less than six months after raising $55 million in a Series C round of funding, SMB 401(k) provider Human Interest today announced it has raised $200 million in a round that propels it to unicorn status.

The Rise Fund, TPG’s global impact investing platform, led the round and was joined by SoftBank Vision Fund 2. The financing included participation from new investor Crosslink Capital and existing backers NewView Capital, Glynn Capital, U.S. Venture Partners, Wing Venture Capital, Uncork Capital, Slow Capital, Susa Ventures and others.

Over the past year, the San Francisco-based company has raised $305 million. With the latest financing, it has now raised a total of $336.7 million since its 2015 inception.

The company admittedly has an IPO in its sights, as evidenced by the appointment of former Yodlee CFO Mike Armsby to the role of CFO at Human Interest. It’s targeting a traditional IPO sometime in 2023, with execs saying the target is to have “$200 million+ in run-rate revenue before going public.” Currently, it’s at “tens of millions of run-rate revenue” now, and adding millions of new revenue each month.

Human Interest’s digital retirement benefits platform allows users “to launch a retirement plan in minutes and put it on autopilot,” according to the company. It also touts that it has eliminated all 401(k) transaction fees.

Demand for 401(k)s by SMBs appears to be at an all-time high, with Human Interest reporting that its sales tripled over the last year. The company has also more than doubled its headcount over the last 12 months to 350 employees.

The startup said it is seeing strong adoption in verticals that have not previously had retirement benefits, including construction, retail, manufacturing, restaurants, nonprofits and hospitality. For example, over the past three quarters, Human Interest has seen 4.5x customer growth in the restaurant sector. Since the start of the pandemic, Human Interest has experienced 2x higher enrollment growth among hourly workers than salaried workers, and hourly worker assets have tripled.

“Promoting financial health is a core investment pillar for The Rise Fund. Human Interest delivers one of the most compelling solutions to the persistent problem that roughly half of Americans will not have enough savings when they reach retirement age,” said Maya Chorengel, co-managing partner at The Rise Fund, in a written statement. “Despite recent legislation, primarily at the state level, legacy programs have not, to date, produced the same participant outcomes as Human Interest.”

The company said it will be using its new capital to expand its network of integrations and partnerships with financial advisers, benefits brokers and payroll companies. It also expects to, naturally, do some hiring –– another 200 employees by year’s end, primarily in its product, engineering and revenue teams.

The 401(k) for SMB space is heating up as of late. In June, competitor Guideline also raised $200 million in a round led by General Atlantic.

Additional details around the IPO and revenue were added post-publication.

Powered by WPeMatico

Paytm, India’s most valuable startup, confirmed to its shareholders and employees on Monday that it plans to file for an IPO.

In a letter to shareholders and employees, Paytm said that it plans to raise money by issuing fresh equity in the IPO, and also sell existing shareholders’ shares at the event. The startup has offered its employees the option to sell their stakes in the firm.

This is the first time the Noida-headquartered firm, which is valued at $16 billion and has raised over $3 billion to date, has commented on its plans about the IPO. The startup said in the letter that it has received an in-principle approval from the board of directors to pursue the public market.

Paytm, which is backed by Alibaba and SoftBank, hasn’t shared when it plans to file for the IPO, but has sought shareholders’ response to their intention to sell stakes by the end of the month.

Two sources familiar with the matter told TechCrunch that Paytm plans to raise about $3 billion and is targeting a valuation of up to $30 billion in the IPO. Paytm declined to comment.

Paytm’s letter — obtained by TechCrunch — to shareholders on Monday.

This isn’t the first time Paytm has planned to explore the public route. Exactly 10 years ago, long before Paytm established itself as the largest mobile wallet firm and expanded to several financial and commerce services, the startup had filed with the regulator with intentions to become public. The startup at the time cancelled the IPO plan and instead raised money from VCs to explore new avenues for growth.

A lot is riding on a successful IPO of Paytm — which reported a consolidated loss of $233.6 million for the financial year that ended in March this year, down from $404 million a year ago. (The startup’s revenue fell 10% during this period to $437.6 million.) India’s stock markets are yet to be fully tested for tech startups’ stocks in the country — though retail investors have shown good signs in recent years.

The startup, which competes with Google Pay and Flipkart-backed PhonePe, has realigned its payments strategy in recent years to assume a leadership position in the merchant payments market.

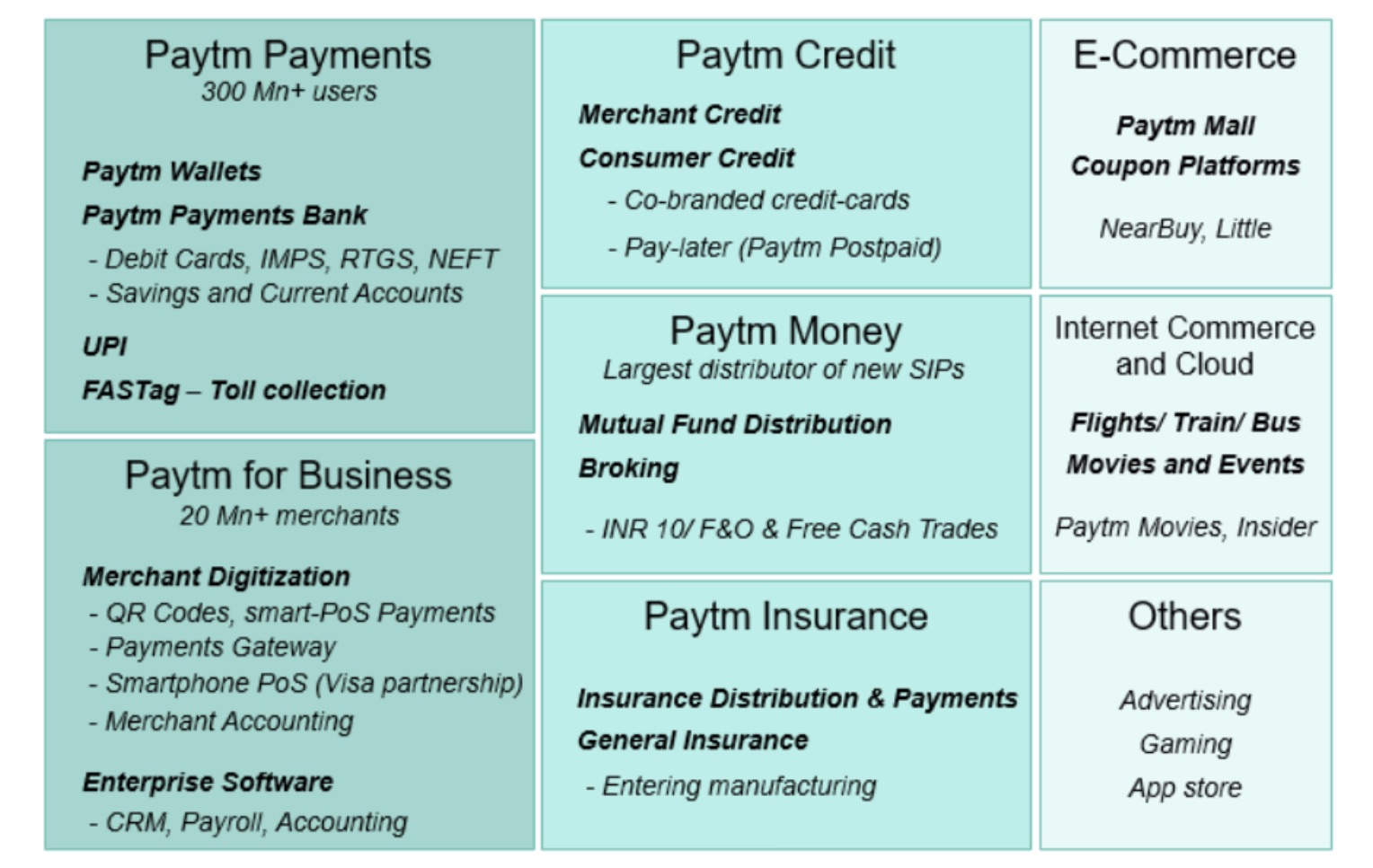

In a report to its clients late last month, analysts at Bernstein said the startup’s credit tech vertical is likely to lead the next wave of its revenue growth.

An overview of Paytm’s financial services ecosystem (Bernstein)

“With the advent of UPI, there has been a rising narrative that questioned Paytm’s market leadership,” the analysts wrote, referring to the exponential growth of payments stack developed by retail banks in India that has been adopted by several firms, including Google and PhonePe (as well as Paytm), and which has somewhat lowered the appeal of mobile wallets in India.

“However, under the hood, Paytm leads on merchant payments and has built an ecosystem of synergistic fintech verticals around its ‘super-app.’ The ecosystem spans payments (wallet/UPI), full-suite merchant acquiring, credit tech, digital bank, wealth, and insurance tech. We believe the super-app battle in India is not a ‘winner takes all’ but a game of execution, business building, and creating a superior customer experience with ecosystem integration,” Bernstein analysts added.

Paytm is the latest Indian giant startup that has expressed an interest in becoming public in recent months. Earlier this year, food delivery startup Zomato said it plans to raise $1.1 billion through an initial public offering. TechCrunch reported last month that Flipkart was in talks to raise over $1 billion in what is expected to be its financial fundraise ahead of an IPO.

Powered by WPeMatico

Creditas, the Brazilian lending business, has raised $255 million in new financing as financial services startups across Latin America continue to attract massive amounts of cash.

The company’s credit portfolio has crossed 1 billion reals ($196.66 million) and the new round will value the company at $1.75 billion thanks to $570 million raised in outside financing over five rounds.

Creditas is the latest company to benefit from a boom in financial services startup investing across the region. As the year dawned, venture investments into fintech startups in Latin America had grown from $50 million in 2014 to top $2.1 billion in 2020 across 139 deals, according to a report from CB Insights.

Investors in the round include new investors like LGT Lightstone, Tarsadia Capital, Wellington Management, e.ventures and an affiliate of Advent International, Sunley House Capital. Previous investors including SoftBank Vision Fund 1, SoftBank Latin America DFund, VEF, Kaszek and Amadeus Capital Partners also returned to put more money into the company.

“Creditas is still in the early innings of penetrating the huge untapped secured lending market in Brazil and Mexico” says Paulo Passoni, managing partner of SoftBank Latam fund, in a statement.

The company’s growth is a testament both to the need for new lending products across Latin America and the perspicacity of investors like Kaszek Ventures, whose portfolio has included several massive wins from bets on startups tackling financial services in Latin America.

“The journey since our investment in the Series A has been absolutely extraordinary. The team has executed on its vision, and Creditas has evolved into an asset-light ecosystem that resolves key financial needs of its customers throughout their lifetimes,” says Nicolas Szekasy, managing partner of Kaszek Ventures, in a statement.

Another big winner is Redpoint’s e.ventures fund, which has focused on investments in Latin America for the last several years.

“By empowering Brazilians to take control of their lending needs at reasonable rates, Creditas creates a beloved consumer product that will drive significant value for customers and investors. Having been involved since the seed stage through Redpoint e.ventures, we’re thrilled to support the company with our Global Growth Fund as well, as they change the Brazilian fintech landscape,” said Mathias Schilling, co-founder and managing partner of e.ventures.

Creditas has plans to use the cash to expand its home and auto lending as well as a payday lending service based on customers’ salaries and a retail option to sell through buy now, pay later loans based on a customer’s salary.

The company is also looking to expand to other markets, with an eye toward establishing a foothold in the Mexican market.

Founded in 2012, when the founders worked out of a five-square-meter office on Berrini Avenue in São Paulo, the company now boasts a robust business with hundreds of employees and a business resting on a secured lending marketplace and independent home and auto lending operations.

The company also released quarterly results for the first time, showing losses narrowing from 74.9 million Brazilian reals to 40.5 million reals in the year ago quarter.

Powered by WPeMatico

The Chinese Uber for trucks Manbang announced Tuesday that it has raised $1.7 billion in its latest funding round, two years after it hauled in $1.9 billion from investors including SoftBank Group and Alphabet Inc.’s venture capital fund CapitalG.

The news came fresh off a Wall Street Journal report two weeks ago that Manbang was seeking $1 billion ahead of an initial public offering next year. The company declined to comment on the matter, though its CEO Zhang Hui said in May 2019 that the firm was “not in a rush” to go public.

Manbang said it achieved profitability this year. Its valuation was reportedly on course to reach $10 billion in 2018.

The company, which runs an app matching truck drivers and merchants transporting cargo and provides financial services to truckers, was formed from a merger between rivals Yunmanman and Huochebang in 2017. It was a time when China’s “sharing economy” craze began to see consolidation and shakeup.

The latest financing again attracted high-profile backers, including returning investors SoftBank Vision Fund and Sequoia Capital China, Permira and Fidelity, a consortium that co-led the round. Other participants were Hillhouse Capital, GGV Capital, Lightspeed China Partners, Tencent, Jack Ma’s YF Capital and more.

The company has other Alibaba ties. Its CEO Zhang, who founded Yunmanman, hailed from Alibaba’s famed B2B department where Manbang chairman Wang Gang also worked before he went on to fund ride-hailing giant Didi’s angel round.

Manbang claims its platform has more than 10 million verified drivers and 5 million cargo owners. The latest funding will allow it to further invest in research and development, upgrade its matching system and expand its service capacity to functions like door-to-door transportation.

Sequoia is quite bullish about truck-hailing as it made its sixth investment in Manbang. For Permira, a European private equity fund, the Manbang investment marked the China debut of its Growth Opportunities Fund.

Powered by WPeMatico

The only thing more rare than a unicorn is an exited unicorn.

At TechCrunch, we cover a lot of startup financings, but we rarely get the opportunity to cover exits. This week was an exception though, as it was exitpalooza as Affirm, Roblox, Airbnb and Wish all filed to go public. With DoorDash’s IPO filing last week, this is upwards of $100 billion in potential float heading to the public markets as we make our way to the end of a tumultuous 2020.

All those exits raise a simple question — who made the money? Which VCs got in early on some of the biggest startups of the decade? Who is going to be buying a new yacht for the family for the holidays (or, like, a fancy yurt for when Burning Man restarts)? The good news is that the wealth is being spread around at least a couple of VC firms, although there are definitely a handful of partners who are looking at a very, very nice check in the mail compared to others.

So let’s dive in.

I’ve covered DoorDash’s and Airbnb’s investor returns in-depth, so if you want to know more about those individual returns, feel free to check out those analyses. But let’s take a more panoramic perspective of the returns of these five companies as a whole.

First, let’s take a look at the founders. These are among the very best startups ever built, and therefore, unsurprisingly, the founders all did pretty well for themselves. But there are pretty wide variations that are interesting to note.

First, Airbnb — by far — has the best return profile for its founders. Brian Chesky, Nathan Blecharczyk and Joe Gebbia together own nearly 42% of their company at IPO, and that’s after raising billions in venture capital. The reason for their success is simple: Airbnb may have had some tough early innings when it was just getting started, but once it did, its valuation just skyrocketed. That helped to limit dilution in its earlier growth rounds, and ultimately protected their ownership in the company.

David Baszucki of Roblox and Peter Szulczewski of Wish both did well: they own 12% and about 19% of their companies, respectively. Szulczewski’s co-founder Sheng “Danny” Zhang, who is Wish’s CTO, owns 4.9%. Eric Cassel, the co-founder of Roblox, did not disclose ownership in the company’s S-1 filing, indicating that he doesn’t own greater than 5% (the SEC’s reporting threshold).

DoorDash’s founders own a bit less of their company, mostly owing to the money-gobbling nature of that business and the sheer number of co-founders of the company. CEO Tony Xu owns 5.2% while his two co-founders Andy Fang and Stanley Tang each have 4.7%. A fourth co-founder, Evan Moore, didn’t disclose his share totals in the company’s filing.

Finally, we have Affirm . Affirm didn’t provide total share counts for the company, so it’s hard right now to get a full ownership picture. It’s also particularly hard because Max Levchin, who founded Affirm, was a well-known, multi-time entrepreneur who had a unique shareholder structure from the beginning (many of the venture firms on the cap table actually have equal proportions of common and preferred shares). Levchin has more shares all together than any of his individual VC investors — 27.5 million shares, compared to the second largest investor, Jasmine Ventures (a unit of Singapore’s GIC) at 22 million shares.

Powered by WPeMatico

Plenty Unlimited has raised $140 million in new funding to build more vertical farms around the U.S.

The new funding, which brings the company’s total cash haul to an abundant $500 million, was led by existing investor SoftBank Vision Fund and included the berry farming giant Driscoll’s. It’s a move that will give Driscoll’s exposure to Plenty’s technology for growing and harvesting fruits and vegetables indoors.

The funding comes as Plenty has inked agreements with both its new berry-interested investor and the Albertsons grocery chain. The company also announced plans to build a new farm in Compton, California.

The financing provides plenty of cash for a company that’s seeing a cornucopia of competition in the tech-enabled cultivated crop market raising a plethora of private and public capital.

In the past month, AppHarvest has agreed to be taken public by a special purpose acquisition company in a deal that would value that greenhouse tomato-grower at a little under $1 billion. And another leafy green grower, Revol Greens, has raised $68 million for its own greenhouse-based bid to be part of the new green revolution.

Meanwhile, Plenty’s more direct competitor, Bowery Farming, is expanding its retail footprint to 650 stores, even as Plenty touts its deal with Albertsons to provide greens to 431 stores in California.

Discoll’s seemed convinced by Plenty’s technology, although the terms of the agreement with the company weren’t disclosed.

“We looked at other vertical farms, and Plenty’s technology was one of the most compelling systems we’d seen for growing berries,” said J. Miles Reiter, Driscoll’s chairman and CEO, in a statement. “We got to know Plenty while working on a joint development agreement to grow strawberries. We were so impressed with their technology, we decided to invest.”

Powered by WPeMatico

As part of Disrupt 2020 we wanted to look at the contrasting positions of both early and later-stage investing in Europe. Who better to unpack this subject than two highly experienced operators in these fields?

After a career at Spotify and then as a VC at Atomico, Sophia Bendz has rapidly gained a reputation in Europe as a keen early-stage investor. She recently left Atomico to pursue her early and seed-stage passion with Cherry Ventures. Bendz is a prolific angel investor, with a total of more than 44 deals in the last nine years. Her angel investments include AidenAI, Tictail, Joints Academy, Omnius, LifeX, Eastnine, Manual, Headvig, Simple Feast and Sana Labs. She is known for being a champion of the femtech space, and her angel investments in that space include Clue, Grace Health, Daye, O School and Boost Thyroid.

Carolina Brochado, the former Atomico partner and most recently a partner at SoftBank Vision Fund’s London office, recently joined EQT Ventures to help launch EQT’s Growth fund, which is positioned between ventures and private equity. Brochado led investments in a number of promising companies at Atomico, including logistics company OnTruck, health tech company Hinge Health and restaurant supply chain app Rekki.

After establishing that these two knew each other while at Atomico, I asked Bendz why she headed back into the seed-stage arena.

“I’m a trained marketeer and storyteller by heart… What makes me excited is new markets opportunities, people, culture, teams. So with that, in combination with my angel investing, I think I’m better suited to be in the earlier stages of investing. When I was investing before joining Atomico, I said to myself, I want to learn from the best, I want to see how it’s done, how you structure the process and how you think about the bigger investments.”

Brochado says the European “cat is out of the bag,” as it were:

When I first moved to Europe in 2012 and first joined Atomico, after having been at a very small startup, there was still a massive gap in funding and Europe versus the U.S. I think you know the European secret is no longer a secret, and you have incredible funds being started at that early-stage seed and Series A, and because I was here in 2012, I’ve seen the amazing pipeline of growth companies that are coming up the curve, how the momentum of those companies is accelerating and how the market cap of those businesses are growing. And so I just became super excited about helping those businesses scale… I just now felt like bridging that gap in between was really exciting.

One of the perennial topics that come up time and time again is whether or not founders should go with VC partners who have previously been operators, versus those with a finance background.

“Looking back, my years at Spotify, we had great investors, but there were not many of them that had the experience of scaling a big company,” Bendz said. “So, I’m happy to give [a startup] more than just the check in a way that I would have wished I had a sounding board when I was 25 and tackling that challenge at Spotify.”

Brochado concurred: “Having operators in the room is just is an incredible gift I think to a fund and at certain levels, having people that understand you know different forms of financing and different structures can also be incredibly helpful to founders who may not necessarily have that background. So I think that the funds that do it best have that diversity.”

Bendz is passionate about investing in female founders and femtech: “It’s such a massive business opportunity that is completely untapped. We’ve seen it many times when you have a female investment partner [that] the pipeline opens up and you get more deal flow from female founders…. So I think we have a lot of work to do. I think it’s definitely improved a lot in the last couple of years but not enough… That is one of the drivers for why I put my money where my mouth is and invest in lifting the founders, but also because there are incredibly interesting business opportunities… There are so many opportunities and products or services that we will see being developed. When we have a more equal society, and more women, both building their own companies, coding and also investing… I can’t wait to see what that world will look like.”

Brochado’s view is that “even beyond founders… the best managers today are putting a lot of focus on this and I think what’s exciting is, I think we’re past the point where you have to explain to people why diversity matters.”

Is there a post-Series A chasm?

Bendz thinks: “We have more big funds in Europe [now]. We have a really solid ground here in Europe of A, B and C investors.”

Brochado said: “It’s definitely getting better. You don’t hear as many founders say that to do my Series B or my Series C I have to move to the Valley as you used to. But there’s a lot of room still for growth investors in Europe. I think Series B is the hardest round actually because, at seed or Series A, you can raise on very early traction or the quality of the management team. At Series B the price goes up but the risk doesn’t necessarily go down as much. And so I think that’s where you really need investors who are sector or thematic focused, who can come with conviction and also some knowledge around the company to really propel that company forward.”

Did they both see European entrepreneurs still making silly mistakes, or has the ecosystem mastered?

Brochado thinks 10 years ago it was hard for European founders as a lot of the talent to scale companies was still in the U.S. “What you’ve seen is a lot of big companies grow up in Europe, a lot of people come back from the U.S., and so I think that pool of talent now is larger, which is very helpful. I don’t think it’s yet at the scale of where the U.S. is. But it gives us, you know as investors, a great window of opportunity to help get some of that talent for our portfolio companies.”

The impact of COVID-19

Bendz thinks we will “see a much slower spring, but… I think it has been overall a good exercise for some companies, and I have not seen a slower deal flow. I’ve actually done more angel deals this spring than I normally do… Some businesses have definitely accelerated their whole business concept because of COVID. Investments are being made even though we haven’t met the founders. We’re able to do everything remotely so I think the system is kind of adjusting.”

Brochado’s view is that at the growth stage “there’s been a flight to quality. So actually, the really great companies or the companies that are seeing great tailwinds or companies that will still be category-leading once [have] seen a lot of interest. It’s been a very busy summer, which usually it isn’t, particularly at the growth stage… I think a lot of money is still in the system, and has flown into technology. And so if you look at how tech in the public markets has performed it’s performed extremely well. And that includes European public companies and within tech.”

Watch the full panel below.

Powered by WPeMatico

SoftBank Group confirmed today it is considering selling its T-Mobile U.S. shares.

Bloomberg reported last month that SoftBank was nearing an agreement to sell about $20 billion of its T-Mobile U.S. shares to investors, including Deutsche Telekom, T-Mobile’s controlling shareholder, in an effort to offset major losses from its investment business, including the Vision Fund.

In today’s notice, SoftBank Group, which owns about 25% of T-Mobile U.S. shares, said it is exploring transactions that could include private placements or public offerings and transactions with T-Mobile or its shareholders, including Deutsche Telekom AG, or third parties.

The potential sale would be part of SoftBank Group’s program, announced in March, to sell or monetize up to $41 billion in assets to reduce debt and increase its cash reserves. The company said, however, that it cannot assure any of the transactions involving T-Mobile shares will be completed.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re digging into SoftBank’s latest earnings slides. Not only do they contain a wealth of updates and other useful information, but some of them are gosh-darn-freaking hilarious. We all deserve a bit of levity after the last few months.

The visual elements we quote below come from SoftBank’s reporting of its own results from its fiscal year ending March 31, 2020. Much of the deck is made up of financial reporting tables and other bits of stuff you don’t want to read. We’ve cut all that out and left the fun parts.

Before we dive in, please note that we are largely giggling at some slide design choices and only somewhat at the results themselves. We are certainly not making fun of people who’ve been impacted by layoffs and other such things that these slides’ results encompass.

But we are going to have some fun with how SoftBank describes how it views the world, because how can we not? Let’s begin.

TechCrunch has a number of folks parsing SoftBank’s deck this morning, looking to do serious work. That’s not our goal. Sure, this post will tell you things like the fact that there are 88 companies in the Vision Fund portfolio, and that when it comes to unrealized gains and losses, the portfolio has seen $13.4 billion in gains and $14.2 billion in losses. $4.9 billion of gains have been realized, mind you, while just $200 million of losses have had the same honor.

And this post will tell you that the “net blended [internal rate of return] for SoftBank Vision Fund investors is -1%.”

Hell, you probably also want to know that Uber was detailed as Vision Fund’s worst-performing public company, generating a $1.46 billion loss for the group. In contrast, Guardant Health is good for a $1.67 billion gain, while 2019 IPO Slack has been good for $605 million in profits. Those were the two best companies in the Vision Fund’s public portfolio.

But what you really want is the good stuff. So, shared by slide number, here you go:

Powered by WPeMatico