SMBs

Auto Added by WPeMatico

Auto Added by WPeMatico

When it comes to software to help IT manage workers’ devices wherever they happen to be, enterprises have long been spoiled for choice — a situation that has come in especially handy in the last 18 months, when many offices globally have gone remote and people have logged into their systems from home. But the same can’t really be said for small and medium enterprises: As with so many other aspects of tech, they’ve long been overlooked when it comes to building modern IT management solutions tailored to their size and needs.

But there are signs of that changing. Today, a startup called Atera that has been building remote, and low-cost, predictive IT management solutions specifically for organizations with less than 1,000 employees, is announcing a funding round of $77 million — a sign of the demand in the market, and Atera’s own success in addressing it. The investment values Atera at $500 million, the company confirmed.

The Tel Aviv-based startup has amassed some 7,000 customers to date, managing millions of endpoints — computers and other devices connected to them — across some 90 countries, providing real-time diagnostics across the data points generated by those devices to predict problems with hardware, software and network, or with security issues.

Atera’s aim is to use the funding both to continue building out that customer footprint, and to expand its product — specifically adding more functionality to the AI that it currently uses (and for which Atera has been granted patents) to run predictive analytics, one of the technologies that today are part and parcel of solutions targeting larger enterprises but typically are absent from much of the software out there aimed at SMBs.

“We are in essence democratizing capabilities that exist for enterprises but not for the other half of the economy, SMBs,” said Gil Pekelman, Atera’s CEO, in an interview.

The funding is being led by General Atlantic, and it is notable for being only the second time that Atera has ever raised money — the first was earlier this year, a $25 million round from K1 Investment Management, which is also in this latest round. Before this year, Atera, which was founded in 2016, turned profitable in 2017 and then intentionally went out of profit in 2019 as it used cash from its balance sheet to grow. Through all of that, it was bootstrapped. (And it still has cash from that initial round earlier this year.)

As Pekelman — who co-founded the company with Oshri Moyal (CTO) — describes it, Atera’s approach to remote monitoring and management, as the space is typically called, starts first with software clients installed at the endpoints that connect into a network, which give IT managers the ability to monitor a network, regardless of the actual physical range, as if it’s located in a single office. Around that architecture, Atera essentially monitors and collects “data points” covering activity from those devices — currently taking in some 40,000 data points per second.

To be clear, these data points are not related to what a person is working on, or any content at all, but how the devices behave, and the diagnostics that Atera amasses and focuses on cover three main areas: hardware performance, networking and software performance and security. Through this, Atera’s system can predict when something might be about to go wrong with a machine, or why a network connection might not be working as it should, or if there is some suspicious behavior that might need a security-oriented response. It supplements its work in the third area with integrations with third-party security software — Bitdefender and Acronis among them — and by issuing updated security patches for devices on the network.

The whole system is built to be run in a self-service way. You buy Atera’s products online, and there are no salespeople involved — in fact most of its marketing today is done through Facebook and Google, Pekelman said, which is one area where it will continue to invest. This is one reason why it’s not really targeting larger enterprises (the others are the level of customization that would be needed; as well as more sophisticated service level agreements). But it is also the reason why Atera is so cheap: it costs $89 per month per IT technician, regardless of the number of endpoints that are being managed.

“Our constituencies are up to 1,000 employees, which is a world that was in essence quite neglected up to now,” Pekelman said. “The market we are targeting and that we care about are these smaller guys and they just don’t have tools like these today.” Since its model is $89 dollars per month per technician using the software, it means that a company with 500 people with four technicians is paying $356 per month to manage their networks, peanuts in the greater scheme of IT services, and one reason why Atera has caught on as more and more employees have gone remote and are looking like they will stay that way.

The fact that this model is thriving is also one of the reason and investors are interested.

“Atera has developed a compelling all-in-one platform that provides immense value for its customer base, and we are thrilled to be supporting the company in this important moment of its growth trajectory,” said Alex Crisses, MD, global head of New Investment Sourcing and co-head of Emerging Growth at General Atlantic, in a statement. “We are excited to work with a category-defining Israeli company, extending General Atlantic’s presence in the country’s cutting-edge technology sector and marking our fifth investment in the region. We look forward to partnering with Gil, Oshri and the Atera team to help the company realize its vision.”

Powered by WPeMatico

Allan Jones dropped out of college and spent a decade learning how to run a startup. In 2016, that education resulted in the launch of Los Angeles-based Bambee, which helps small companies by acting as their HR department with the goal of keeping them in compliance with government rules and regulations.

But he found getting funded a challenge in spite of his background. He said that as a Black man, he had to move more carefully in the startup world.

“I think it came as part of the complexities of navigating a mostly white male ecosystem, a mostly straight cis white male ecosystem that either helps you create some skills that make you really effective at the job, or generates so much resentment that it becomes hard to be effective. […] I think that I was always one comment away from the opposite direction [I ended up going],” he explained.

Fortunately, that didn’t happen, and he kept on climbing and gaining skills and single-handedly founded his own company, one which has reached Series B and raised $33 million, a significant amount of money for any startup, but particularly for a startup run by a Black founder.

A study published by Crunchbase in February found that VC firms distributed $150 billion in venture funding in 2020. Of that, less than 1%, or around $1 billion, went to Black founders. That highlights just how difficult it has been for him to raise from such a limited pool of money in spite of having a great idea and the business skill and acumen to pull it off.

Jones got his start at the age of 20 at a startup called Helio, which targeted the youth market for multimedia services on mobile phones. It was eventually acquired by Virgin Mobile. He went on to run product at a couple of companies before landing as CMO at ZipRecruiter in 2013. He left that position after three years to launch Bambee in 2016.

In spite of all that experience, he felt that as a gay Black man in Silicon Valley that he was continually saddled with the label of “the kid with potential,” and not always taken as seriously as his straight white counterparts. “And I don’t think those intentions necessarily were bad, I think it was quite the opposite, which actually makes them almost worse because they were entrenched in a bias of how to characterize [my abilities].”

Jones launched Bambee, a startup that is going after SMBs with fewer than 500 employees, most of which are operating without an HR department, and could be out of compliance with federal mandates because they don’t have anyone in charge who is aware of the rules.

“Bambee aims to put an HR manager in every American small business. We’ve done so by building a model that allows you to hire one on our platform for $99 a month. So you pay us a flat fee and you get access to our platform and your own dedicated HR professional. […] She acts as your human resource manager and your human resource arm for your company. And our platform helps keep those companies compliant,” Jones explained.

Jones says that while he might not encounter direct bias as he builds his business, there is an unconscious bias that investing in Bambee could be riskier than investing in someone who fits the prototypical startup founder mold, and this is especially true in early-stage investing when investors are essentially betting on the entrepreneur.

“They take bets that they deem as a bit safer — entrepreneurs that look like a certain profile — white cis-gender males that come from Stanford and Harvard that match the profile of confidence and they have kind of built in an anti-bias determination around, so they automatically get the benefit of the doubt to those pedigrees, and those profiles,” Jones said.

He says that means that Black founders have to work that much harder to overcome those biases. Today Bambee has some decent metrics to show investors with revenue reaching tens of millions, growing 300% year over year with thousands of customers across all 50 states, according to Jones. With 100 employees, he plans to double that number by the end of this year.

Even with that, he says there are still barriers to entry he has to deal with. Even if it’s harder for investors to ignore the company’s numbers, he still sees a tendency to accentuate the negative.

“Building a great company with the deficit in belief in you that starts so early on in the venture process, the [obstacles] that you have to [overcome] to get here. It seems impossible with less than 1% of venture capital dollars going to Black founders, and it isn’t because Black founders don’t exist, it’s because the belief in us is not there at scale,” he said.

As Jones continues to build the company, he has learned to look for investors who believe in him and his vision for the company. If he senses that negativity from a potential investor, he moves on because he wants to work with people who want to help build the company and believe in it as much as he does. He says this won’t change when he goes to raise his C round, a stage few Black entrepreneurs reach.

“Is it going to be easier for me going forward? I don’t think so. I think the type of bias that I have to combat based on the class of entrepreneur I’m becoming, it starts to shift and change, and I’ve seen that in every round and I’m prepared for it in my Series C, as well.”

He says that the progress he’s made in the company and his belief in the business will help him find the right partners to continue on that journey, just as he has in previous rounds.

“We will navigate this […] and I think we’ll build a really great business, and ultimately the partners we discover along this journey will be the exact right ones who we were meant to.”

Powered by WPeMatico

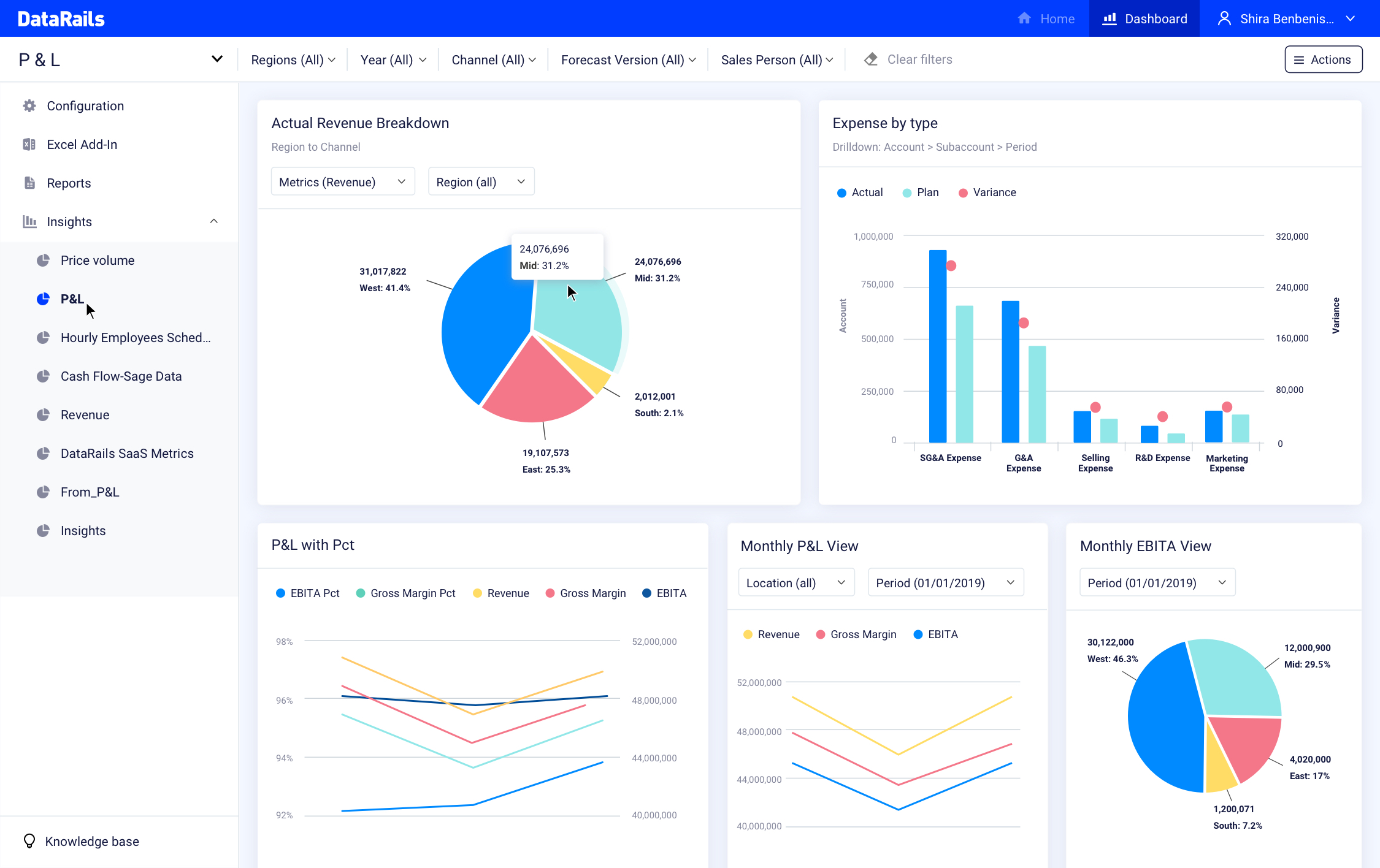

As enterprise startups continue to target interesting gaps in the market, we’re seeing increasingly sophisticated tools getting built for small and medium businesses — traditionally a tricky segment to sell to, too small for large enterprise tools, and too advanced in their needs for consumer products. In the latest development of that trend, an Israeli startup called DataRails has raised $25 million to continue building out a platform that lets SMBs use Excel to run financial planning and analytics like their larger counterparts.

The funding closes out the company’s Series A at $43.5 million, after the company initially raised $18.5 million in April (some at the time reported this as its Series A, but it seems the round had yet to be completed). The full round includes Zeev Ventures, Vertex Ventures Israel and Innovation Endeavors, with Vintage Investment Partners added in this most recent tranche. DataRails is not disclosing its valuation, except to note that it has doubled in the last four months, with hundreds of customers and on target to cross 1,000 this year, with a focus on the North American market. It has raised $55 million in total.

The challenge that DataRails has identified is that on one hand, SMBs have started to adopt a lot more apps, including software delivered as a service, to help them manage their businesses — a trend that has been accelerated in the last year with the pandemic and the knock-on effect that has had for remote working and bringing more virtual elements to replace face-to-face interactions. Those apps can include Salesforce, NetSuite, Sage, SAP, QuickBooks, Zuora, Xero, ADP and more.

But on the other hand, those in the business who manage finances and financial reporting are lacking the tools to look at the data from these different apps in a holistic way. While Excel is a default application for many of them, they are simply reading lots of individual spreadsheets rather than integrated data analytics based on the numbers.

DataRails has built a platform that can read the reported information, which typically already lives in Excel spreadsheets, and automatically translate it into a bigger picture view of the company.

For SMEs, Excel is such a central piece of software, yet such a pain point for its lack of extensibility and function, that this predicament was actually the germination of starting DataRails in the first place,

Didi Gurfinkel, the CEO who co-founded the company with Eyal Cohen (the CPO) said that DataRails initially set out to create a more general-purpose product that could help analyze and visualize anything from Excel.

Image: DataRails

“We started the company with a vision to save the world from Excel spreadsheets,” he said, by taking them and helping to connect the data contained within them to a structured database. “The core of our technology knows how to take unstructured data and map that to a central database.” Before 2020, DataRails (which was founded in 2015) applied this to a variety of areas with a focus on banks, insurance companies, compliance and data integrity.

Over time, it could see a very specific application emerging, specifically for SMEs: providing a platform for FP&A (financial planning and analytics), which didn’t really have a solution to address it at the time. “So we enabled that to beat the market.”

“They’re already investing so much time and money in their software, but they still don’t have analytics and insight,” said Gurfinkel.

That turned out to be fortunate timing, since “digital transformation” and getting more out of one’s data was really starting to get traction in the world of business, specifically in the world of SMEs, and CFOs and other people who oversaw finances were already looking for something like this.

The typical DataRails customer might be as small as a business of 50 people, or as big as 1,000 employees, a size of business that is too small for enterprise solutions, “which can cost tens of thousands of dollars to implement and use,” added Cohen, among other challenges. But as with so many of the apps that are being built today to address those using Excel, the idea with DataRails is low-code or even more specifically no-code, which means “no IT in the loop,” he said.

“That’s why we are so successful,” he said. “We are crossing the barrier and making our solution easy to use.”

The company doesn’t have a huge number of competitors today, either, although companies like Cube (which also recently raised some money) are among them. And others like Stripe, while currently not focusing on FP&A, have most definitely been expanding the tools that it is providing to businesses as part of their bigger play to manage payments and subsequently other processes related to financial activity, so perhaps it, or others like it, might at some point become competitors in this space as well.

In the meantime, Gurfinkel said that other areas that DataRails is likely to expand to cover alongside FP&A include HR, inventory and “planning for anything,” any process that you have running in Excel. Another interesting turn would be how and if DataRails decides to look beyond Excel at other spreadsheets, or bypass spreadsheets altogether.

The scope of the opportunity — in the U.S. alone there are more than 30 million small businesses — is what’s attracting the investment here.

“We’re thrilled to reinvest in DataRails and continue working with the team to help them navigate their recent explosive and rapid growth,” said Yanai Oron, general partner at Vertex Ventures, in a statement. “With innovative yet accessible technology and a tremendous untapped market opportunity, DataRails is primed to scale and become the leading FP&A solution for SMEs everywhere.”

“Businesses are constantly about to start, in the midst of, or have just finished a round of financial reporting — it’s a never-ending cycle,” added Oren Zeev, founding partner at Zeev Ventures. “But with DataRails, FP&A can be simple, streamlined, and effective, and that’s a vision we’ll back again and again.”

Powered by WPeMatico

Small businesses have traditionally been underserved when it comes to IT — they are too big and have too many requirements that can’t be met by consumer products, yet are much too small to afford, implement or thoroughly need apps and other IT build for larger enterprises. But when it comes to neobanks, it feels like there is no shortage of options for the SMB market, nor venture funding being invested to help them grow.

In the latest development, Novo, a neobank that has built a service targeting small businesses, has closed a round of $40.7 million, a Series A that it will be using to continue growing its business, and its platform.

The funding is being led by Valar Ventures with Crosslink Capital, Rainfall Ventures, Red Sea Ventures and BoxGroup all participating. The startup is not disclosing valuation, but Novo — originally founded in New York in 2018 but now based out of Miami — has racked up 100,000 SMB customers — which it defines as businesses that make between $25,000 and $100,000 in annualized revenues — and has seen $1 billion in lifetime transactions, with growth accelerating in the last couple of years.

There are a wide variety of options for small businesses these days when it comes to going for a banking solution. They include staying with traditional banks (which are starting to add an increasing number of services and perks to retain small business customers), as well as a variety of fintechs — other neobanks, like Novo — that are building banking and related financial tools to cater to startups and other small businesses.

Just doing a quick search, some of the others targeting the sector include Rho, NorthOne, Lili, Mercury, Brex, Hatch, Anna, Tide, Viva Wallet, Open and many more (and you could argue also players like Amazon, offering other money management and spending tools similar to what neobanks are providing). Some of these are not in the U.S., and some are geared more at startups, or freelancers, but taken together they speak to the opportunity and also the attention that it is getting from the tech industry right now.

As CEO and co-founder Michael Rangel — who hails from Miami — described it to me, one of the key differentiators with Novo is that it’s approaching SMB banking from the point of view of running a small business. By this, he means that typically SMBs are already using a lot of other finance software — on average seven apps per business — to manage their books, payments and other matters, and so Novo has made it easier by way of a “drag and drop” dashboard where an SMB can integrate and view activity across all of those apps in one place. There are “dozens” of integrations currently, he said, and more are being added.

This is the first step, he said. The plan is to build more technology so that the activity between different apps can also be monitored, and potentially automated

“We’re able to see this is your balance and what you should expect,” he said. “The next frontier is to marry the incoming with outgoing. We’re using the funding to build that, and it’s on the roadmap in the next six months.”

Novo has yet to bring cash advances or other lending products into its platform, although those too are on the roadmap, but it is also listening to its customers and watching what they want to do on the platform — another reason why it’s clever to make it easy to for those customers to integrate other services into Novo: not only does that solve a pain point for the customer, but it becomes a pretty clear indicator of what customers are doing, and how you could better cater to that.

Listening to the customers is in itself becoming a happy challenge, it seems. Novo launched quietly enough — between 2018 and the end of 2019, it had picked up only 5,000 accounts. But all that changed during 2020 and the COVID-19 pandemic, which Rangel describes as “just hockey stick growth. We grew like crazy.”

The reason, he said, is a classic example of why incumbent banks have to catch up with the times. Everyone was locked down at home, and suddenly a lot of people who were either furloughed or laid off were “spinning up businesses,” he said, and that led to many of them needing to open bank accounts. But those who tried to do this with high-street banks were met with a pretty significant barrier: you had to go into the bank in person to authenticate yourself, but either the banks were closed, or people didn’t want to travel to them. That paved the way for Novo (and others) to cater to them.

Its customer numbers shot up to 24,000 in the year.

Then other market forces have also helped it. You might recall that banking app Simple was shut down by BBVA ahead of its merger with PNC; but at the same time, it also shut down Azlo, it’s small business banking service. That led to a significant number of users migrating to other services, and Novo got a huge windfall out of that, too.

In the last six months, Novo grew four-fold, and Rangel attributed a lot of that to ex-Azloans looking for a new home.

The fact that there are so many SMB banking providers out there might mean competition, but it also means fragmentation, and so if a startup emerges that seems to be catching on, it’s going to catch something else, too: the eye of investors.

“The ability of the Novo team to grow the company rapidly during a year where businesses have faced unprecedented challenges is impressive,” said Andrew McCormack, founding partner at Valar Ventures, the firm co-founded by Peter Thiel, another big figure in fintech. “Novo tripled its small business customer base in the first half of 2021! Their custom infrastructure and banking platform put them in prime position to expand their services at an even faster pace as we come out of the health crisis. All of us at Valar Ventures are excited to join this team.”

Powered by WPeMatico

With more people than ever before going online to pay for things and pay each other, startups that are building the infrastructure that enables these actions continue to get a lot of attention.

In the latest development, Paysend, a fintech that has built a mobile-based payments platform — which currently offers international money transfers, global accounts, and business banking and e-commerce for SMBs — has picked up some money of its own. The London-based startup has closed a round of $125 million, a sizable Series B that the company’s CEO and founder Ronnie Millar said it will be using to continue expanding its business geographically, to hire more people, and to continue building more fintech products.

The funding is being led by One Peak, with Infravia Growth Capital, Hermes GPE, previous backer Plug and Play and others participating.

Millar said Paysend is not disclosing valuation today but described it as a “substantial kick-up” and “a great step forward in our position ahead toward unicorn status.”

From what I understand though, the company was valued at $160 million in its previous round, and its core metrics have gone up 4.5x. Doing some basic math, that gives the company a valuation of around $720 million, a figure that a source close to the company did not dispute when I brought it up.

Something that likely caught investors’ attention is that Paysend has grown to the size it is today — it currently has 3.7 million consumer customers using its transfer and global account services, and 17,000 small business customers, and is now available in 110 receiving countries — in less than four years and $50 million in funding.

There are a couple of notable things about Paysend and its position in the market today, the first being the competitive landscape.

On paper, Paysend appears to offer many of the same features as a number of other fintechs: money transfer, global payments, and banking and e-commerce services for smaller businesses are all well-trodden areas with companies like Wise (formerly “TransferWise”), PayPal, Revolut, and so many others also providing either all or a range of these services.

To me, the fact that any one company relatively off the tech radar can grow to the size that it has speaks about the opportunity in the market for more than just one or two, or maybe five, dominant players.

Considering just remittances alone, the WorldBank in April said that flows just to low- and middle-income countries stood at $540 million last year, and that was with a dip in volumes due to COVID-19. The cut that companies like Paysend make in providing services to send money is, of course, significantly smaller than that — business models include commission charges, flat fees or making money off exchange rates; Paysend charges £1 per transfer in the U.K. More than that, the overall volumes, and the opportunity to build more services for that audience, are why we’re likely to see a lot of companies with ambitions to serve that market.

Services for small businesses, and tapping into the opportunity to provide more e-commerce tools at a time when more business and sales are being conducted online, is similarly crowded but also massive.

Indeed, Paysend points out that there is still a lot of growing and evolution left to do. Citing McKinsey research, it notes that some 70% of international payments are currently still cash-to-cash, with fees averaging up to 5.2% per transaction, and timing taking up to an hour each for sender and recipient to complete transfers. (Paysend claims it can cut fees by up to 60%.)

This brings us to the second point about Paysend: How it’s built its services. The fintech world today leans heavily on APIs: Companies that are knitting together a lot of complexity and packaging it into APIs that are used by others who bypass needing to build those tools themselves, instead integrating them and adding better user experience and responsive personalization around them. Paysend is a little different from these, with a vertically integrated approach, having itself built everything that it uses from the ground up.

Millar — a Scottish repeat entrepreneur (his previous company Paywizard, which has rebranded to Singula, is a specialist in pay-TV subscriber management) — notes that Paysend has built both its processing and acquiring facilities. “Because we have built everything in-house it lets us see what the consumer needs and uses, and to deliver that at a lower cost basis,” he said. “It’s much more cost-efficient and we pass that savings on to the consumer. We designed our technology to be in complete control of it. It’s the most profitable approach, too, from a business point of view.”

That being said, he confirmed that Paysend itself is not yet profitable, but investors believe it’s making the right moves to get there. To be clear, Paysend actually does partner with other companies, including those providing APIs, to improve its services. In April, Plaid and Paysend announced they were working together to power open banking transfers, reducing the time to initiate and receive money.

“We are excited by Paysend’s enormous growth potential in a massive market, benefiting from a rapid acceleration in the adoption of digital payments,” said Humbert de Liedekerke, managing partner at One Peak Partners, in a statement. “In particular, we are seeing strong opportunities as Paysend moves beyond consumers to serve business customers and expands its international footprint to address a growing need for fast, easy and low-cost cross-border digital payments. Paysend has built an exceptional payment platform by maintaining an unwavering focus on its customers and constantly innovating. We are excited to back the entire Paysend team in their next phase of explosive growth.”

Powered by WPeMatico

After his last startup, Framed Data, was acquired by Square, Thomson Nguyen began exploring new ideas. While an entrepreneur-in-residence at Kleiner Perkins, Nguyen interviewed hundreds of small business owners and realized that many pay hundreds of dollars in fees to maintain a business checking account. “Most small businesses are low margin, high cash flow, so they don’t have $4,000 just laying around,” Nguyen told TechCrunch. “We found in our analysis that micro-SMBs actually end up paying on average $450 in overdraft fees a year.”

Nguyen’s new startup Hatch recently launched its first two products and announced today it has secured a total of $20 million in funding from investors like Kleiner Perkins, Foundation Capital, SVB and Plaid’s founders. The fintech’s Hatch Business Checking accounts cost $10 a month, don’t charge non-sufficient funds (NSF) or overdraft fees and include cashback offers. Eligible account holders can also enroll in Hatch Cover, which covers overdrafts up to $100, or apply for lines of credit.

Some of Hatch’s customers have hundreds of employees, but Nguyen said the startup primarily focuses on businesses with up to 20 people. Many are run by only one person, who might be setting up a business account for the first time.

Hatch draws on Nguyen’s professional and personal backgrounds. Framed Data, a predictive analytics company, was acquired by Square in 2016. He worked as Square Capital’s head of data science before becoming an entrepreneur-in-residence at Kleiner Perkins in 2018, focusing on fintech and machine learning problems. As a child of immigrants, Nguyen saw firsthand the challenges small businesses can face.

“During my time at Kleiner, the goal was to think about what other problems I wanted to solve. I definitely wanted to solve additional problems within small businesses. I think a lot of what I appreciate about Square’s mission of economic empowerment for small businesses also really resonated with my own family story,” he said. “My parents immigrated here from Vietnam after the war and were like so many immigrants to the States to start small businesses. Figuring out how to use whatever talents I had to try to make it easier to start small businesses was definitely something I wanted to pursue.”

Hatch’s leadership team, including alumni of fintech companies and major financial institutions like Square, Stripe, Morgan Stanley and JP Morgan, talked to small business owners, and found that recent immigrants or people without credit histories were paying the majority of bank fees. The startup raised a $5 million seed round from Kleiner Perkins, Abstract Ventures and former Square executive Gokul Rajaram in January 2019, then a $14 million Series A round from Foundation Capital, SVB and Plaid founders William Hockey and Zack Perret in February 2020.

Hatch Business Checking began rolling out in January and currently has 4,000 users. The company’s inception coincided with an especially brutal time for many small business owners, as they weathered the COVID-19 pandemic’s economic impact and navigated the process of getting government aid through the Coronavirus Aid, Relief and Economic Security (CARES) Act.

“Initially I was a little worried, but as I was talking to all of our small business customers and even as I was doing these interviews, I realized that amidst a global pandemic, it’s been humbling to see the grit and perseverance of small business owners trying to innovate and learn,” Nguyen said.

For example, some of Hatch’s users are restaurants that hadn’t done deliveries before, but quickly signed up for multiple on-demand platforms like Postmates or Uber Eats. Others include accountants and lawyers who figured out how to move their practices online.

Hatch serves businesses in a wide range of sectors, including first-time entrepreneurs.

“There’s been this interesting trend of sole proprietors and individual creators who maybe had a side hustle, and after they were laid off during COVID, they decided, okay, I’m going start a small business,” Nguyen said. “Through our research, that’s actually how a lot of small businesses think of themselves, not as Thomson Tacos LLC for example, but just as myself, as Thomson, a person who is running this business.”

The startup uses machine learning to automate Hatch Business Checking’s online sign-up process and its know your customer (KYC) and know your business (KYB) requirements. This includes confirming business incorporation paperwork, social security or employer ID numbers and regulatory compliance like Office of Foreign Asset Control (OFAC) checks. Hatch can approve applications in less than five minutes. Once that process is complete, customers get a Mastercard virtual number and can link external bank accounts. Hatch also uses machine learning for real-time fraud and risk monitoring.

Nguyen said Hatch launched its overdraft coverage program because “we found it is a really great way for folks to get themselves out of a bind, finish the point sale and then top up their account later.”

If a business with a Hatch Business Checking account needs more working capital, it can apply for a Hatch Business Line of Credit, or loans between $200 to $5,000 at an APR of 18% to 24%. Hatch does not do hard credit checks and sees the credit lines as an alternative to the payday lenders or check cashers that customers without a FICO score or subprime ratings often use.

To screen loan applicants, Hatch uses information from their Business Checking accounts, including activity from connected point-of-sale systems. This allows Hatch to see real-time data and forecast a business’ potential forward revenue. It also enables the company to approve credit lines in as little as two hours.

“A hard credit check is actually quite difficult for recent immigrants or Americans who had trouble in their recent history. If you declare bankruptcy, it takes seven years to get it struck off your credit history,” said Nguyen. “To us, I think the more important factors are whether you actually have a business and whether that business is growing. We have a couple of examples of folks who declared bankruptcy three or four years ago, but they have a business that is booming and growing, and we’re happy to underwrite or originate that line of credit for them.”

But he emphasizes that Hatch, a signatory of the Small Business Owner’s Bill of Rights, does not see lending as a permanent solution and will not encourage its users to take on unnecessary debt.

“I think the reason we feel so strongly about this is that we want to win when our customers win,” Nguyen said. “If all we did was lending, then you would almost have a misalignment of incentives where you want to encourage lending retention. Given our business bank accounts and our revenue model, which is $10 a month and debit interchange, we really win when the business continues to exist. So for us, it’s almost a matter of building that financial independence for our customers.”

Hatch currently covers overdrafts and credit lines with its own balance sheet. “Because we’re using machine learning data to understand our own risk position, the main focus right now is to understand how businesses grow and model those products accordingly,” said Nguyen.

In an emailed statement, Kleiner Perkins partner Ilya Fushman told TechCrunch, “Small businesses account for nearly half of all economic activity in the U.S., but are often hamstrung by the banking ecosystem today. Hatch is democratizing access to the financial resources that small businesses need to start out and grow. Thomson and team are already working with thousands of SMBs and are uniquely suited with the technology and industry expertise to help them grow with the financial resources they need to be successful.”

In his statement about Foundation Capital’s investment, partner Charles Moldow said, “Our view at Foundation Capital is that the next phase of financial innovation is confluence: a coming together of lending and mobile banking. Hatch is a breaker wave of this movement for small businesses. That Thomson and his team were able to so rapidly stand up the only full-solution, mobile-first bank offering for SMBs is a testament to what they can and will accomplish.”

Since Hatch’s Series A, it has grown its team from eight people to 48, hiring remotely during the pandemic. Its plan is to expand its Business Checking accounts and continue building products for the estimated 40 million small businesses in the United States.

“When I think of the future products we can provide, it really centers around how do we make sure that a small business succeeds in starting up correctly and efficiently, and scaling their business,” said Nguyen. “Sometimes that’s financial products like our business accounts. Potentially, it could be software products that help you actually start that business. So there’s a wealth of different ideas and directions in which we can take Hatch.”

Powered by WPeMatico

Cora, a São Paulo-based technology-enabled lender to small and-medium-sized businesses, has raised $26.7 million in a Series A round led by Silicon Valley VC firm Ribbit Capital.

Kaszek Ventures, QED Investors and Greenoaks Capital also participated in the financing, which brings the startup’s total raised to $36.7 million since its 2019 inception. Kaszek led Cora’s $10 million seed round (believed at that time to be one of the largest seed investments in LatAm) in December 2019, with Ribbit then following.

Last year, Cora got its license approved from the Central Bank of Brazil, making it a 403 bank. The fintech then launched its product in October 2020 and has since grown to have about 60,000 customers and 110 employees.

Cora offers a variety of solutions, ranging from a digital checking account, Visa debit card and management tools such as an invoice manager and cashflow dashboard. With the checking account, customers have the ability to send and receive money, as well as pay bills, digitally.

This isn’t the first venture for Cora co-founders Igor Senra and Leo Mendes. The pair had worked together before — founding their first online payments company, MOIP, in 2005. That company sold to Germany’s WireCard in 2016 (with a 3 million-strong customer base), and after three years the founders were able to strike out again.

Cora co-founders Leo Mendes and Igor Senra; Image courtesy of Cora

With Cora, the pair’s long-term goal is to “provide everything that a SMB will need in a bank.”

Looking ahead, the pair has the ambitious goal of being “the fastest growing neobank focused on SMBs in the world.” It plans to use the new capital to add new features and improve existing ones; on operations; and launching a portfolio of credit products.

In particular, Cora wants to go even deeper in certain segments, such as B2B professional services such as law and accounting firms, real estate brokerages and education.

Ribbit Capital partner Nikolay Kostov believes that Cora has embarked on “an ambitious mission” to change how small businesses in Brazil are able to access and experience banking.

“While the consumer banking experience has undergone a massive transformation thanks to new digital experiences over the last decade, this is, sadly, still not the case on the small business side,” he said.

For example, Kostov points out, opening a traditional small business bank account in Brazil takes weeks, “reels of paper, and often comes with low limits, poor service and antiquated digital interfaces.”

Meanwhile, the number of new small businesses in the country continues to grow.

“The combination of these factors makes Brazil an especially attractive market for Cora to launch in and disrupt,” Kostov told TechCrunch. “The Cora founding team is uniquely qualified and deeply attuned to the challenges of small businesses in the country, having spent their entire careers building digital products to serve their needs.”

Since Ribbit’s start in 2012, he added, LatAm has been a core focus geography for the firm “given the magnitude of challenges, and opportunities in the region to reinvent financial services and serve customers better.”

Ribbit has invested in 15 companies in the region and continues to look for more to back.

“We fully expect that several fintech companies born in the region will become global champions that serve to inspire other entrepreneurs across the globe,” Kostov said.

Powered by WPeMatico

There are 12 million small and medium businesses in the U.S., yet they have continued to be one of the most underserved segments of the B2B universe: That volume underscores a lot of fragmentation, and alongside other issues like budget constraints, there are a number of barriers to building for them at scale. Today, however, a startup helping SMBs get online is announcing some significant funding — a sign of how things are changing at a moment when many businesses have realised that being online is no longer an option, but a necessity.

GoSite, a San Diego-based startup that helps small and medium enterprises build websites, and, with a minimum amount of technical know-how, run other functions of their businesses online — like payments, online marketing, appointment booking and accounting — has picked up $40 million in funding.

GoSite offers a one-stop shop for users to build and manage everything online, with the ability to feed in up to 80 different third-party services within that. “We want to help our customers be found everywhere,” said Alex Goode, the founder and CEO of GoSite. “We integrate with Facebook and other consumer platforms like Siri, Apple Maps and search engines like Google, Yahoo and Bing and more.” It also builds certain features like payments from the ground up.

The Series B comes on the back of a strong year for the company. Driven by COVID-19 circumstances, businesses have increasingly turned to the internet to interact with customers, and GoSite — which has “thousands” of SMB customers — said it doubled its customer base in 2020.

This latest round is being led by Left Lane Capital out of New York, with Longley Capital, Cove Fund, Stage 2, Ankona Capital and Serra Ventures also participating. GoSite is clearly striking while the iron is hot: Longley, also based out of San Diego, led the company’s previous round, which was only in August of this year. It has now raised $60 million to date.

GoSite is, in a sense, a play for more inclusivity in tech: Its customers are not companies that it’s “winning” off other providers that provide website building and hosting and other services typically used by SMBs, such as Squarespace and Wix, or GoDaddy, or Shopify.

Rather, they are companies that may have never used any of these: local garages, local landscapers, local hair salons, local accountancy firms, local dentists and so on. Barring the accounting firm, these are not businesses that will ever go fully online, as a retailer might, not least because of the physical aspect of each of those professions. But they will need an online presence and the levers it gives them to communicate in order to survive, especially in times when their old models are being put under strain.

Goode started GoSite after graduating from college in Michigan with a degree in computer science, having previously grown up around and working in small businesses — his parents, grandparents and others in his Michigan town all ran their own stores. (He moved to San Diego “for the weather,” he joked.)

His belief is that while there are and always will be alternatives like Facebook or Yelp to plant a flag, there is nothing that can replace the value and longer-term security and control of building something of your own — a sentiment small business owners would surely grasp.

That is perhaps the most interesting aspect of GoSite as it exists today: It precisely doesn’t see any of what already exists out there as “the competition.” Instead, Goode sees his purpose as building a dashboard that will help business owners manage all that — with up to 80 different services currently available — and more, from a single place, and with minimum need for technical skills and time spent learning the ropes.

“There is definitely huge demand from small businesses for help and something like GoSite can do that,” Goode said. “The space is very fragmented and noisy and they don’t even know where to start.”

This, combined with GoSite’s growth and relevance to the current market, is partly what attracted investors.

“The opportunity we are betting on here is the all-in-one solution,” said Vinny Pujji, partner at Left Lane. “If you are a carpet cleaner or house painter, you don’t have the capacity to understand or work with five or six different pieces of software. We spoke with thousands of SMBs when looking at this, and this was the answer we heard.” He said the other important thing is that GoSite has a customer service team and for SMBs that use it, they like that when they call, “GoSite picks up the phone.”

Powered by WPeMatico

Facebook has been making a big play to be a go-to partner for small and medium businesses that use the internet to interface with the wider world, and its messaging platform WhatsApp, with some 50 million businesses and 175 million people messaging them (and more than 2 billion users overall) has been a central part of that pitch.

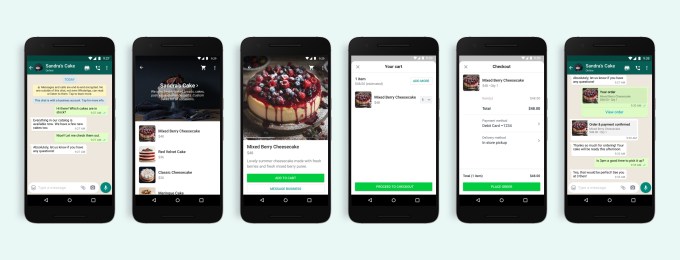

Now, the company is making three big additions to WhatsApp to fill out that proposition.

It’s launching a way to shop for and pay for goods and services in WhatsApp chats; it’s going head to head with the hosting providers of the world with a new product called Facebook Hosting Services to host businesses’ online assets and activity; and — in line with its expanding product range — Facebook said it will finally start to charge companies using WhatsApp for Business.

Facebook announced the news in a short blog post light on details. We have reached out to the company for more information on pricing, availability of the services and whether Facebook will provide hosting itself or work with third parties, and we will update this post as we learn more.

Update: Facebook responded and we are putting the replies below, in-line where it makes sense.

Here is what we know for now:

In-chat Shopping: Companies are already using WhatsApp to present product information and initiate discussions for transactions. One of the more recent developments in that area was the addition of QR codes and the ability to share catalog links in chats, added in July. At the same time, Facebook has been expanding the ways that businesses can display what they are selling on Facebook and Instagram, most recently with the launch in August of Facebook Shop, following a similar product roll out on Instagram before that.

Today’s move sounds like a new way for businesses in turn to use WhatsApp both to link through to those Facebook-native catalogs, as well as other products, and then purchase items, while still staying in the chat.

At the same time, Facebook will be making it possible for merchants to add “buy” buttons in other places that will take shoppers to WhatsApp chats to complete the purchase. “We also want to make it easier for businesses to integrate these features into their existing commerce and customer solutions,” it notes. “This will help many small businesses who have been most impacted in this time.”

Although Facebook is not calling this WhatsApp Pay, it seems that this is the next step ahead for the company’s ambitions to bring payments into the chat flow of its messaging app. That has been a long and winding road for the company, which finally launched WhatsApp Payments, using Facebook Pay, in Brazil, in June of this year only to have it shut down by regulators for failing to meet their requirements. (The plan has been to expand it to India, Indonesia and Mexico next.)

Facebook Hosting Services: These will be available in the coming months, but no specific date to share right now. “We’re sharing our plans now while we work with our partners to make these services available,” the company said in a statement to TechCrunch.

No! This is not about Facebook taking on AWS. Or… not yet at least? The idea here appears that it is specifically aimed at selling hosting services to the kind of SMBs who already use Facebook and WhatsApp messaging, who either already use hosting services for their online assets, whether that be their online stores or other things, or are finding themselves now needing to for the first time, now that business is all about being “online.”

“Today, all businesses using our API are using either an on-premise solution or leverage a solutions provider, both of which require costly servers to maintain,” Facebook said. “With this change, businesses will be able to choose to use Facebook’s own secure hosting infrastructure for free, which helps remove a costly item for every company that wants to use the WhatsApp Business API, including our business service providers, and will help them all save money.” It added that it will share more info about where data will be hosted closer to launch.

This is a very interesting move, since the SMB hosting market is pretty fragmented with a number of companies, including the likes of GoDaddy, Dream Host, HostGator, BlueHost and many others also offering these services. That fragmentation spells opportunity for a huge company like Facebook with a global profile, a burgeoning amount of connections through to other online services for these SMBs and a pretty extensive network of data centers around the world that it has built for itself and can now use to provide services to others — which is, indeed, a pretty strong parallel with how Amazon and AWS have done business.

Facebook already has an “app store” of sorts with partners it works with to provide marketing and related services to businesses using its platform. It looks like it plans to expand this, and will sell the hosting alongside all of that, with the kicker that hosting natively on Facebook will speed up how everything works.

“Providing this option will make it easier for small and medium size businesses to get started, sell products, keep their inventory up to date, and quickly respond to messages they receive – wherever their employees are,” it notes.

Charging tiers: As you would expect, to encourage more adoption, Facebook has not been charging for WhatsApp Business up to now, but it has charged for some WhatsApp business messages — for example when businesses send a boarding pass or e-commerce receipt to a customer over Facebook’s rails. (These prices vary and a list of them is published here.) Now, with more services coming into the mix, and businesses tying their fates more strongly to how well they are performing on Facebook’s platforms, it’s no surprise to see Facebook converting that into a pay to play scenario.

“What we’ve heard over the past couple years is how the conversational nature of business messaging is really valuable to people. So in the future we may look at ways to update how we charge businesses that better reflect how it’s used,” the company told us. Important to note that this will relate to how businesses send messages. “As always, it’s free for people to send a business a message,” Facebook added.

Frustratingly, there seems so far to be no detail on which services will be charged, nor how much, nor when, so this is more of a warning than a new requirement.

“We will charge business customers for some of the services we offer, which will help WhatsApp continue building a business of our own while we provide and expand free end-to-end encrypted text, video and voice calling for more than two billion people,” it notes.

For those who might find that annoying, on the plus side, for those who are concerned about an ever-encroaching data monster, it will, at the least, help WhatsApp and Facebook continue to stick to its age-old commitment to stay away from advertising as a business model.

The new services come at a time when Facebook is doubling down on providing services for businesses, spurred in no small part by the coronavirus pandemic, which has driven physical retailers and others to close their actual doors, shifting their focus to using the internet and mobile services to connect with and sell to customers.

Citing that very trend, last month the company’s COO Sheryl Sandberg announced the Facebook Business Suite, bringing together all of the tools it has been building for companies to better leverage Facebook, Instagram and WhatsApp profiles both to advertise themselves as well as communicate with and sell to customers. And the fact that Sandberg was leading the announcement says something about how Facebook is prioritizing this: it’s striking while the iron is hot with companies using its platform, but it sees/hopes that business services can a key way to diversify its business model while also helping buffer it — since many businesses building Pages may also advertise.

Facebook has also been building more functionality across Facebook and Instagram specifically aimed at helping power users and businesses leverage the two in a more efficient way. Adding in more tools to WhatsApp is the natural progression of all of this.

To be sure, as we pointed out earlier this year, even while there is a lot of very informal use of WhatsApp by businesses all around the world, WhatsApp Business remains a fairly small product, most popular in India and Brazil. Facebook launching more tools for how to use it will potentially drive more business not just in those markets but help the company convert more businesses to using it in other places, too.

Smaller businesses have been on Facebook’s radar for a while now. Even before the pandemic hit, in many cases retailers or restaurants do not have websites of their own, opting for a Facebook Page or Instagram Profile as their URL and primary online interface with the world; and even when they do have standalone sites, they are more likely to update people and spread the word about what they are doing on social media than via their own URLs.

Facebook’s also made a video to help demonstrate how it sees these WhatsApp Business in action, which you can here:

Powered by WPeMatico

Another tech unicorn is feeling the pinch of doing business during the coronavirus pandemic. Today, Kabbage, the SoftBank-backed lending startup that uses machine learning to evaluate loan applications for small and medium businesses, is furloughing a “significant number” of its U.S. team of 500 employees, according to a memo sent to staff and seen by TechCrunch, in the wake of drastically changed business conditions for the company. It is also completely closing down its office in Bangalore, India, and executive staff is taking a “considerable” pay cut.

The announcement is effective immediately and was made to staff earlier today by way of a video conference call, as the whole company is currently remote working in the current conditions.

Kabbage is not disclosing the full number of staff that are being affected by the news (if you know, you can contact us anonymously). It’s also not putting a time frame on how long the furlough will last, but it’s going to continue providing benefits to affected employees. The intention is to bring them back on when things shift again.

“We realize this is a shock to everyone. No business in the world could have prepared for what has transpired these past few weeks and everyone has been impacted,” co-founder and CEO Rob Frohwein wrote in the memo. “The economic fallout of this virus has rattled the small business community to which Kabbage is directly linked. It’s painful to say goodbye to our friends and colleagues in Bangalore and to furlough a number of U.S. team members. While the duration of the furlough remains uncertain, please bear in mind that the full intention of furloughing is temporary. We simply have no clear idea of how long quarantining or its reverberations in the economy will last.”

Kabbage’s predicament underscores the complicated and stressful calculus faced by tech companies built around providing services to SMBs, or fintech (or both, as in the case of Kabbage).

SMBs are struggling right now in the U.S.: many operate on very short terms when it comes to finances, and closing their businesses (or seeing a drastic reduction in custom) means they will not have the cash to last 10 days without revenue, “and we’re already well past that window,” Frohwein noted in his memo.

In Kabbage’s case, that means not only are SMBs not able to be evaluated and approved for normal loans at the moment, but SMBs that already have loans out are likely facing delinquencies.

The decision to furlough is hard but in relative terms it’s good news: it was made at the eleventh hour after a period when Kabbage was considering layoffs instead.

The company has raised hundreds of millions of dollars in equity and debt, and it was in a healthy state before the coronavirus outbreak. The memo notes that the “board and our top investors are aware of the challenges we are facing and have committed to helping us through this period,” although it doesn’t specify what that means in terms of financial support for the business, and whether that support would have been there for the business as-is.

The shift to furlough from layoffs came in the wake of an announcement yesterday by Steven Mnuchin, the U.S. Secretary of the Treasury, who clarified that “any FDIC bank, any credit union, any fintech lender will be authorized” to make loans to small businesses as a part of the U.S. government’s CARE Act, the giant stimulus package that included nearly $350 billion in loan guarantees for small businesses.

While that provides much-needed relief for these businesses, the implementation of it — the Small Business Administration has already received nearly 1 million claims for disaster-relief loans since the crisis started — has been and is going to be a challenge.

That effectively opens up an opportunity for Kabbage and companies like it to revive and reorient some of its business. (Its USP was always that the AI it uses, which draws on a number of different sources of online data for the business, means a more creative, faster and more accurate assessment of loan applications than what traditional banks typically provide.) Kabbage said it is in “deep discussions” with the Treasury Department, the White House and the Small Business Administration to help expedite applications for aid.

While loans still make up the majority of Kabbage’s business, the company has been making a move to diversify its services, and in recent times it has made acquisitions and launched new services around market intelligence insights and payments services. While there has certainly been a jump in e-commerce, overall the tightening economy will have a chilling effect on the wider market, and it will be worth seeing what happens with other tech companies that focus on loans, as well as adjacent financial services.

Powered by WPeMatico