small business

Auto Added by WPeMatico

Auto Added by WPeMatico

Both as a term and as a financial product, “buy now, pay later” has become mainstream in the past few years. BNPL has evolved to assume various forms today, from small-ticket offerings by fintechs on consumer checkout platforms and marketplaces, to closed-loop products offered on marketplaces such as Amazon Pay Later (which they are now extending for outside use as well). You can also see some variants offered by companies that want to expand the scope of consumption and consumer credit.

Globally, BNPL has seen the most growth in the consumer segment and has driven retail consumption and lending over the past few years. Consumer BNPL offerings are a good alternative to credit cards, especially for people who do not have a credit history and can’t get credit from banks. That said, a specific vertical of BNPL products is gaining traction — one targeted toward small and medium enterprises (SMEs). This new vertical is known as “SME BNPL.”

BNPL can be particularly useful when flow-based underwriting or transaction-based underwriting is used to offer credit to small businesses.

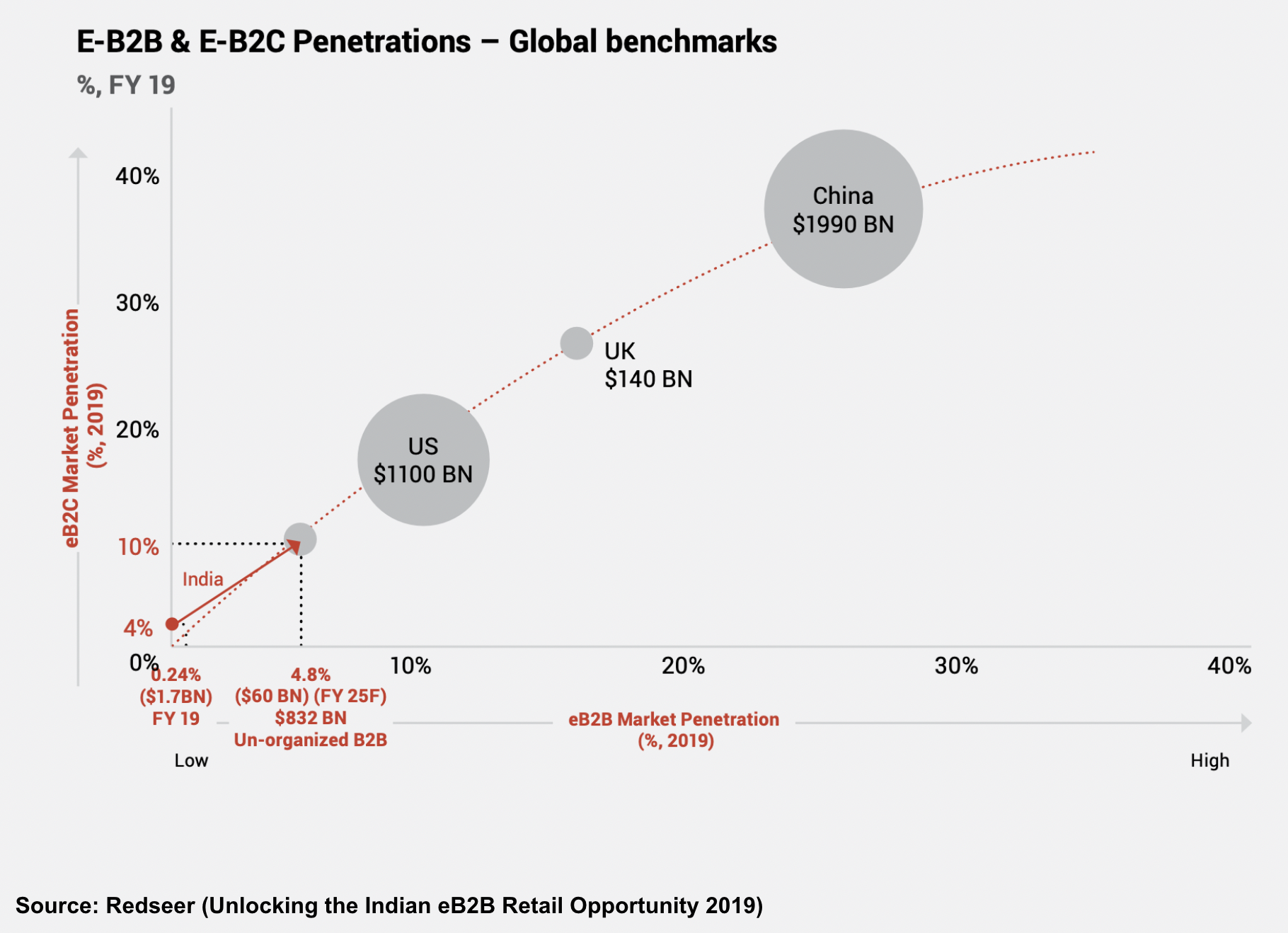

E-commerce has seen tremendous growth in India over the past decade. Skyrocketing smartphone and internet penetration led to rapid growth in e-commerce across large cities and smaller towns alike. Consumer credit has also taken off in parallel as credit cards and digital lending spurred credit-based consumption across offline and online stores.

However, the large B2B supply chain enabling the burgeoning retail market was plagued by bottlenecks and inefficiencies because it involved a plethora of intermediaries and streamlining became a big problem. A number of tech players responded by organizing the previously disorganized B2B commerce market at various touch points, inserting convenience, pricing and easier product access through tech-enabled logistics and a modern supply chain.

Image Credits: Redseer

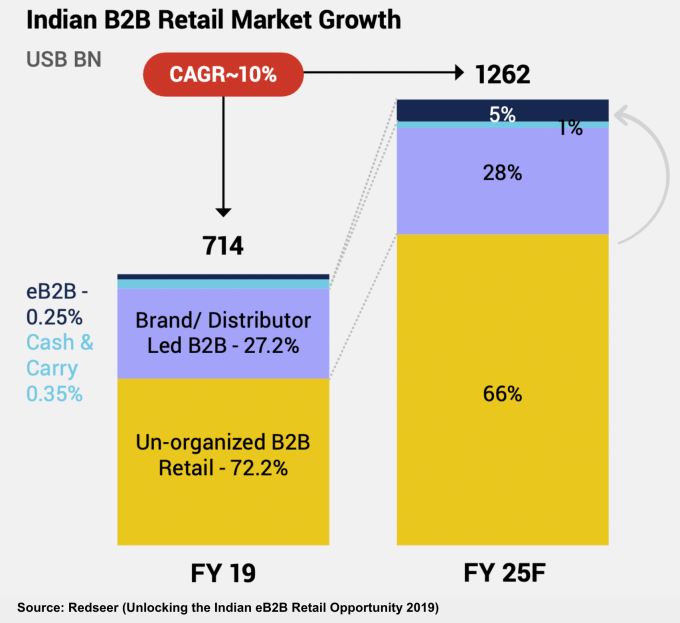

India’s B2B e-commerce space has developed rapidly since 2020. Small businesses have moved from using paper to smartphone apps for running a significant part of their day-to-day business, leading to widespread disruption in how businesses transact today. The COVID-19 pandemic also forced small businesses, which were earlier using physical means to procure goods and services, to try new and online models to conduct their affairs.

Image Credits: Redseer

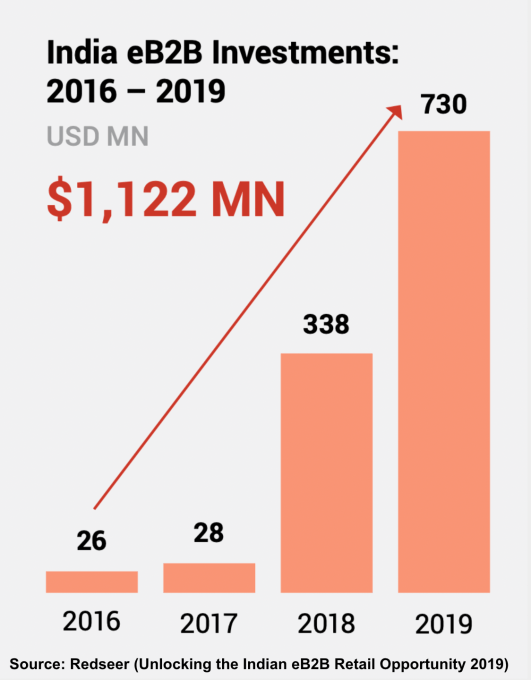

Moreover, the Indian government’s widespread promotion of an instant payments system in the form of the Unified Payments Interface (UPI) has changed how people send money to each other or pay merchants for their goods and services. The next step for solving the digital B2B puzzle is to embed credit inside every transaction and invoice.

Image Credits: Redseer

If we compare online B2B transactions to the offline world, there is only one missing link: The terms offered to small businesses by their supplier/distributor or vendor. Businesses, unlike consumers, must buy goods and services to eventually trade them, or add value and sell to consumers or others down the value chain. This process is not immediate and has a certain time cycle attached.

The longer sales cycle means many small businesses require credit payment terms when buying inventory. As B2B commerce scales and grows through digital means, a BNPL product that caters to the needs of SMEs can support their growth and alleviate the burden on their cash flows.

An SME BNPL product is a purchase financing product for small businesses transacting with suppliers, distributors, aggregator platforms or B2B marketplaces.

Powered by WPeMatico

Trust wants to give smaller businesses the same advantages that large enterprises have when marketing on digital and social media platforms. It came out of beta with $9 million in seed funding from Lerer Hippeau, Lightspeed Venture Partners, Upfront Ventures and Upper90.

The Los Angeles-based company was started in 2019 by a group of five Snap alums working in various roles within Snap’s revenue product strategy business. They were building tools for businesses to fund success with digital marketing, but kept hearing from customers about the advantage big advertisers had over smaller ones — the ability to receive good payment terms, credit lines, as well as data and advice.

Aiming to flip the script on that, the group created Trust, which is a card and business community to help digital businesses navigate the ever-changing pricing models to market online, receive the same incentives larger advertisers get and make the best decision of where their marketing dollars will reach the furthest.

Trust dashboard

Trust does this in a few ways: Its card, built in partnership with Stripe, enables businesses to increase their buying power by up to 20 times and have 45 days to make payments on their marketing investments, CEO James Borow told TechCrunch. Then as part of its community, companies share knowledge of marketing buys and data insights typically reserved for larger advertisers. Users even receive news via their dashboard around their specific marketing strategy, he added.

“The ad platforms are walled gardens, and most people don’t know what is going on inside, so our customers work together to see what is going on,” Borow said.

The growth of e-commerce is pushing more digital marketing investments, providing opportunity for Trust to be a huge business, Borow said. E-commerce sales in the U.S. grew by 39% in the first quarter, while digital advertising spend is forecasted to increase 25% this year to $191 billion. Meanwhile, Google, Facebook, Snapchat and Twitter all recently reported rapid growth in their year-over-year advertising revenues, Borow said.

The new funding will go toward increasing the company’s headcount.

“We have active customers on the platform, so we wanted to ramp up hiring as soon as we went into general release,” he added. “We are leaving beta with 25 businesses and a few hundred on our waitlist.”

That list will soon grow. In addition to the funding round, Trust announced a strategic partnership with social shopping e-commerce platform Verishop. The company’s 3,500 merchants will receive priority access to the Trust card and community, Borow said.

Andrea Hippeau, partner at Lerer Hippeau, said she knew Borow from being an investor in his previous advertising company Shift, which was acquired by Brand Networks in 2015.

When Borow contacted Lerer about Trust, Hippeau said this was the kind of offering that would be applicable to the firm’s portfolio, which has many direct-to-consumer brands, and knew marketing was a huge pain point for them.

“Digital marketing is important to all brands, but it is also a black box that you put marketing dollars into, but don’t know what you get,” she said. “We hear this across our portfolio — they spend a lot of money on ad platforms, yet are treated like mom-and-pop companies in terms of credit. When in reality Casper is outspending other companies by five times. Trust understands how important marketing dollars are and gives them terms that are financially better.”

Powered by WPeMatico

Small and medium enterprises have become a big opportunity in the world of B2B technology in the last several years, and today a startup that’s building tools aimed at helping them manage their teams of workers is announcing some funding that underscores the state of that market.

Homebase, which provides a platform that helps SMBs manage various services related to their hourly workforces, has closed $71 million in funding, a Series C that values the company between $500 million and $600 million, according to sources close to the startup.

The round has a number of big names in it that are as much a sign of how large VCs are valuing the SMB market right now as it is of the strategic interest of the individuals who are participating. GGV Capital is leading the round, with past backers Bain Capital Ventures, Baseline Ventures, Bedrock, Cowboy Ventures and Khosla Ventures also participating. Individuals include Focus Brands President Kat Cole; Jocelyn Mangan, a board member at Papa John’s and Chownow and former COO of Snag; former CFO of payroll and benefits company Gusto, Mike Dinsdale; Guild Education founder Rachel Carlson; star athletes Jrue and Lauren Holiday; and alright alright alright actor and famous everyman and future political candidate Matthew McConaughey.

Homebase has raised $108 million to date.

The funding is coming on the heels of strong growth for Homebase (which is not to be confused with the U.K./Irish home improvement chain of the same name, nor the YC-backed Vietnamese proptech startup).

The company now has some 100,000 small businesses, with 1 million employees in total, on its platform. Businesses use Homebase to manage all manner of activities related to workers that are paid hourly, including (most recently) payroll, as well as shift scheduling, timeclocks and timesheets, hiring and onboarding, communication and HR compliance.

John Waldmann, Homebase’s founder and CEO, said the funding will go toward both continuing to bring on more customers as well as expanding the list of services offered to them, which could include more features geared to frontline and service workers, as well as features for small businesses who might also have some “desk” workers who might still work hourly.

The common thread, Waldmann said, is not the exact nature of those jobs, but the fact that all of them, partly because of that hourly aspect, have been largely underserved by tech up to now.

“From the beginning, our mission was to help local businesses and their teams,” he said. Part of his inspiration came from people he knew: a childhood friend who owned an independent, expanding restaurant chain, and was going through the challenges of managing his teams there, carrying out most of his work on paper; and his sister, who worked in hospitality, which didn’t look all that different from his restaurant friend’s challenges. She had to call in to see when she was working, writing her hours in a notebook to make sure she got paid accurately.

“There are a lot of tech companies focused on making work easier for folks that sit at computers or desks, but are building tools for these others,” Waldmann said. “In the world of work, the experience just looks different with technology.”

Homebase currently is focused on the North American market — there are some 5 million small businesses in the U.S. alone, and so there is a lot of opportunity there. The huge pressure that many have experienced in the last 16 months of COVID-19 living, leading some to shut down altogether, has also focused them on how to manage and carry out work much more efficiently and in a more organized way, ensuring you know where your staff is and that your staff knows what it should be doing at all times.

What will be interesting is to see what kinds of services Homebase adds to its platform over time: In a way, it’s a sign of how hourly wage workers are becoming a more sophisticated and salient aspect of the workforce, with their own unique demands. Payroll, which is now live in 27 states, also comes with pay advances, opening the door to other kinds of financial services for Homebase, for example.

“Small businesses are the lifeblood of the American economy, with more than 60% of Americans employed by one of our 30 million small businesses. In a post-pandemic world, technology has never been more important to businesses of all sizes, including SMBs,” Jeff Richards, managing partner at GGV Capital and new Homebase board member, said in a statement. “The team at Homebase has worked tirelessly for years to bring technology to SMBs in a way that helps drive increased profitability, better hiring and growth. We’re thrilled to see Homebase playing such an important role in America’s small business recovery and thrilled to be part of the mission going forward.”

It’s interesting to see McConaughey involved in this round, given that he’s most recently made a turn toward politics, with plans to run for governor of Texas in 2022.

“Hardworking people who work in and run restaurants and local businesses are important to all of us,” he said in a statement. “They play an important role in giving our cities a sense of livelihood, identity and community. This is why I’ve invested in Homebase. Homebase brings small business operations into the modern age and helps folks across the country not only continue to work harder, but work smarter.”

Powered by WPeMatico

HoneyBook, which has built out a client experience and financial management platform for service-based small businesses and freelancers, announced today that it has raised $155 million in a Series D round led by Durable Capital Partners LP.

Tiger Global Management, Battery Ventures, Zeev Ventures, 01 Advisors as well as existing backers Norwest Venture Partners and Citi Ventures also participated in the financing, which brings the San Francisco-based company’s valuation to over $1 billion. With the latest round, HoneyBook has now raised $248 million since its 2013 inception. The Series D is a big jump from the $28 million that HoneyBook raised in March 2019.

When the COVID-19 pandemic hit last year, HoneyBook’s leadership team was concerned about the potential impact on their business and braced themselves for a drop in revenue.

Rather than lay off people, they instead asked everyone to take a pay cut, and that included the executive team, who cut theirs “by double” the rest of the staff.

“I remember it was terrifying. We knew that our customers’ businesses were going to be impacted dramatically, and would impact ours at the same time dramatically,” recalls CEO Oz Alon. “We had to make some hard decisions.”

But the resilience of HoneyBook’s customer base surprised even the company, who ended up reinstating those salaries just a few months later. And, as corporate layoffs driven by the COVID-19 pandemic led to more people deciding to start their own businesses, HoneyBook saw a big surge in demand.

“Our members who saw a hit in demand went out and found demand in another thing,” Oz said. As a result, HoneyBook ended up doubling its number of members on its SaaS platform and tripling its annual recurring revenue (ARR) over the past 12 months. Members booked more than $1 billion in business on the platform in the past nine months alone.

HoneyBook combines on its platform tools like billing, contracts and client communication, with the goal of helping business owners stay organized. Since its inception, service providers across the U.S. and Canada such as graphic designers, event planners, digital marketers and photographers have booked more than $3 billion in business on its platform. And as the pandemic had more people shift to doing more things online, HoneyBook prepared to help its members adapt by being armed with digital tools.

Image Credits: HoneyBook

“Clients now expect streamlined communication, seamless payments, and the same level of exceptional service online that they were used to receiving from business owners in person,” Alon said.

Oz co-founded HoneyBook with wife Naama and longtime friend Dror Shimoni. Oz and Naama were both small business owners themselves at one time, so they had firsthand insight on the pain points of running a service-based business.

HoneyBook’s software not only helps SMBs do more business, but helps them “convert potentials to actual clients,” Oz said.

“We help them communicate with potential clients so they can win their business, and then help them manage the relationship so they can keep them,” Naama said.

The company plans to use its new capital toward continued product development and to “dramatically” boost its 103-person headcount across its New York and Tel Aviv offices.

“We’re seeing so much demand for additional services and products, so we definitely want to invest and create better ways for our members to present themselves online,” Alon told TechCrunch. “We’re also seeing demand for financial products and the ability to access capital faster. So that’s just a few of the things we plan to invest in.”

The company also wants to make its platform “more customizable” for different categories and verticals.

Chelsea Stoner, general partner at Battery Ventures, said her firm recognized that the expansive market of productivity tools to serve small businesses and entrepreneurs was “a market of discrete and separate productivity tools.”

HoneyBook, she said, is a true platform for SMBs, “providing a huge array of functionality in one cohesive UX.”

“It unites and connects every task for the solopreneurs, from creating and distributing marketing collateral, to organizing and executing proposals, to sending invoices and collecting payments,” Stoner said. “The company is constantly innovating and iterating in response to its members; we also see a lot of opportunity with payments going forward…And, due to COVID-19 and other factors, the company is sitting on pent-up demand that will accelerate growth even more.”

Powered by WPeMatico

Index Ventures, a London- and San Francisco-headquartered venture capital firm that primarily invests in Europe and the U.S., recently announced its latest partner. Carlos Gonzalez-Cadenas, currently COO of London-based fintech GoCardless and previously the chief product officer of Skyscanner, will join Index in January.

Gonzalez-Cadenas is a seasoned entrepreneur and operator, but has also become a prolific angel investor in the U.K. and Europe over the last three years, making more than 50 angel investments in total. Well-regarded by founders and co-investors, his transition to a full-time role in venture capital feels like quite a natural one.

Earlier this week, TechCrunch caught up with Gonzalez-Cadenas over Zoom to learn more about his new role at Index and how he intends to source deals and support founders. Index’s latest hire also shared his insights on Europe’s venture market, describing this era as the “best moment in entrepreneurship in Europe.”

TechCrunch: Let me start by asking, why do you want to become a VC? You’re obviously a well-established entrepreneur and operator, are you sure venture capital is the career for you?

Carlos Gonzalez-Cadenas: I’ve been an angel investor for the last three years and this is something that has basically grown for me quite organically. I started doing just a handful and seeing if this is something I like and over time it has grown quite a lot and so has the number of entrepreneurs I’m partnered with. And this is something I’ve been increasingly more excited to do. So it has grown organically and something that emotionally has been getting closer and closer as time has passed.

And the things I like more specifically are: One, I’m quite a curious person, and for me, investing gives you the possibility of learning a lot about different sectors, about different entrepreneurs, different ways of building businesses, and that is something that I enjoy a lot.

The second bit is that I care a lot about helping entrepreneurs, especially the next generation of entrepreneurs, build great businesses in Europe. I’ve been very lucky, in the past, to learn from great people, like Gareth [Williams, Skyscanner co-founder] and Hiroki [Takeuchi. CEO at GoCardless], in my journey. I feel a duty of helping the next generation of entrepreneurs and sharing all the things that I’ve learnt. I care a lot about setting up founders as much as possible for success and sharing all those experiences I’ve learned [from].

These are the key two motivations that have led me to decide that it would be a great time now to move to the investing side.

How have you managed your deal flow while having a full-time job and where is that deal flow coming from?

It is typically coming in three buckets. A part of it is coming from my entrepreneur and operator network. So there are entrepreneurs and operators I know that are referring other entrepreneurs to me. Another bucket is other investors that I typically co-invest with. Another bucket is venture capitalists. I basically tend to invest quite a lot with VCs and in some cases they are referring deals to me.

In terms of managing it alongside GoCardless, it takes quite a lot of effort. It requires a lot of dedication and time invested during evenings and weekends.

The good thing is that my network typically tends to send me quite highly curated deals so essentially the deal flow I have luckily tends to be quite high quality, which makes things a bit more manageable. But don’t get me wrong, it still takes quite a lot of effort even if the deal flow is relatively high quality.

Presumably you haven’t been able to be all that hands-on as an angel investor, so how are you going to make that transition and what is it that you think you bring with the operational side to venture?

The way I think about this is, the entrepreneurs I typically invest in and their companies tend to be quite capable in their day-to-day perspective. Where they tend to find more value in interactions with me is what I call the “moments of truth.” Those key decisions, those key points in the journey where essentially it can influence the trajectory of the business in a fundamental way. It could be things like, I am fundraising and I don’t know how to position the business. Or I’m thinking about my strategy for the next 18 months and I will basically welcome an experienced person giving me a qualified opinion.

Or I have a big people problem and I don’t know how to solve that problem and I need that third person who has been in my shoes before. Or it could be that I’m thinking about how to organize my team as I move from startup to scale-up and I need help from someone who has scaled teams before. Or could be that I’m hiring three executives and I don’t know what a great CMO looks like. It’s those high-impact, high-leverage questions that the entrepreneurs tend to find helpful engaging with me, as opposed to very detailed day-to-day things that most of the entrepreneurs I work with tend to be quite capable of doing. And so far that model is working. The other thing is that the model is quite scalable because you are engaging 2-3 times per year but those times are high quality and highly impactful for the entrepreneur.

I typically also tend to have pretty regular and frequent communication with entrepreneurs on Slack. It’s more like quick questions that can be solved, and I tend to get quite a lot of that. So I think it’s that bimodel approach of high-frequency questions that we can solve by asynchronous means or high-impact moments a few times per year where, essentially, we need to sit down and we need to think together deeply about the problem.

And I tend to do nothing in the middle, where essentially, it’s stuff that is not so impactful but takes a huge amount of time for everyone, that doesn’t tend to be the most effective way of helping entrepreneurs. Obviously, I’m guided by what entrepreneurs want from perspective, so I’m always training the models in response to what they need.

Powered by WPeMatico

Marco Financial, a new Miami-based startup, is looking to take a piece of the roughly $350 billion trade finance market for Latin American exporters with its novel factoring services business.

Small and medium-sized businesses in Latin America can have trouble getting the financing they need to launch export operations to the U.S. and Marco said it aims to bridge that gap with new risk modeling and management tools that can make better decisions on who should receive loans.

“For smaller businesses in Latin America, accessing trade finance to export their goods is a major concern and a top reason why many don’t succeed,” said Javier Urrutia, director of Foreign Investments at PROCOLOMBIA, an organization that promotes foreign investment and non-traditional exports in Colombia, in a statement from the company. “In Colombia alone, a 1% increase in exporter productivity in our textile industry would result in 500,000 new jobs for the country.”

The company is backed by a small seed round from Struck Capital and Antler and over $20 million in a credit facility underwritten by Arcadia Funds.

“As a former owner of a small business in Latin America, I saw firsthand how difficult it is for SMEs in this region to access trade financing that will let them export their goods while retaining enough capital to keep their business running,” said Peter D. Spradling, COO and co-founder of Marco, in a statement. “Access to trade finance is one of the greatest hurdles in business operations and the traditional system dominated by banks is simply not working anymore, disproportionately hurting SMEs and further restricting economic mobility and job creation in emerging markets. Equity funding and a material credit facility let us serve this underserved market in Latin America and help build a healthier, more equitable trade ecosystem reflective of an increasingly borderless global economy.”

Spradling met his co-founder Jacob Shoihet through the Antler accelerator, a Singapore and New York-based early-stage investment and advisory services program that connects entrepreneurs and tech operators to launch new businesses.

Shoihet, a classically trained musician who fell in with the startup scene in New York through work at Yelp, was eager to launch his own company and connected with Spradling over shared interests in intermittent fasting and sports.

Small and medium businesses have a hard time receiving loans from traditional lenders thanks to tighter regulations and capital controls dating back to the 2008 financial crisis, according to Marco’s founders. And the long periods that companies have to wait between when goods are shipped and orders are payed can put undue pressure on business operations. Factoring solves the gap by lending to merchants based on their receivables.

Marco said that it can reduce the length of the loan origination process from over two months to one week and provide funding to approved exporters within 24 hours.

The company is initially focused on Mexico, Uruguay, Chile, Colombia and Peru, and chose those markets because of Spradling’s previous experience as an importer and exporter across the region.

“We look for companies that not only target massive, sleepy industries but also for ones that are led by management teams with fresh perspectives and asymmetric information that position them to upend incumbents,” said Yida Gao, partner at Struck Capital, in a statement. “In short order, Marco has assembled a world-class team to tackle the multi trillion-dollar trade finance market in a post-Covid time when SMEs around the world need, more than ever, reliable capital to fund operations and growth. We are excited to be part of Marco’s journey to support the suppliers that are the backbone of global trade.”

Powered by WPeMatico

Building a business is hard; about 50% of businesses fail in the first five years. The early years of an entrepreneur’s journey can be difficult and lonely. When starting my digital services firm Fearless, I convinced my wife to rent out our home and move in with my mother so we could have an extra income while I built Fearless in my mother’s basement.

That was 10 years ago — Fearless now has over 115 employees.

That story of struggling to build a tech company and working out of a basement or garage until you “make it” is pretty common, but the barriers facing Black entrepreneurs make it harder to find success and support.

Research by the University of California, Santa Cruz states that minority-owned startups have access to less capital than their white counterparts. The right investors can offer more than just funding to early-stage companies; the connections those in the venture capitalist world have can bring an entrepreneur the new business, mentorship and employees needed to grow.

Venture capital firms like Harlem Capital and Black Angel Tech Fund are focused on changing the faces of entrepreneurship by diversifying their portfolio, but traditional venture capitalist funding is not the only way to grow your business.

There are other avenues and opportunities to get the support, financial and otherwise, to help build a successful company:

Equity crowdfunding: Similar to crowdfunding campaigns like GoFundMe or Kickstarter, equity crowdfunding allows nontraditional investors to support businesses and receive equity. Enabled through Title III of the 2012 JOBS Act’s Regulation CF, equity crowdfunding allows all companies to sell securities, whether in the form of equity in the company, debt, revenue shares, convertible notes and more. Equity crowdfunding platforms include WeFunder and LocalStake.

Mentor programs: Fearless was lucky enough to be accepted into the DoD Mentor-Protégé program early in our growth. As the oldest continuously operating federal mentor-protégé program in existence, the DoD program helped us establish and expand our footprint in the federal government contracting space. NewMe and Black Girl Ventures are two programs that specialize in mentorship for early-stage companies.

Become 8(a) certified: The federal government has a goal of awarding at least 5% of all federal contracting dollars to small, disadvantaged businesses each year. These businesses fall under the 8(a) classification. To qualify for the program, you must be a small business with 51% of ownership and control from U.S. citizens who are economically and socially disadvantaged and the owner’s adjusted gross income for three years is $250,000 or less.

The full definition of what counts as being economically and socially disadvantaged can be found in Title 13 Part 124 of the Code of Federal Regulations. Fearless has been classified as an 8(a) company for several years and we have been able to secure several contracts through the certification.

Tap into Small Business Administration resources: More than a million users visit SBA.gov to utilize tools like the SBA Business Guide and Lender Match site. By using the SBA website and reaching out to your local SBA office, you can make full use of the programs available and connect with business owners who can offer advice and mentorship.

Identify supportive bankers: Your business is your top priority and the people you engage with should view your company as a priority too. You need someone vested in your success who will advocate for you when you need them. If you meet with a banker and get a sense that you would be an account number instead of a person, then find another one. If you don’t have your banker’s personal cell phone number, and they aren’t willing to visit you at your business, then take a pass and find a true partner who supports you.

I am putting the call out to business owners and entrepreneurs who are further along in their journey to mentor and invest in Black-owned businesses. Think back on the support you received, and be that model for someone else. Or be the mentor that you wished you had when you were starting out. Take time to invest in other Black-owned tech companies or fund the programs that do. Share your knowledge and experience with Black tech leaders.

If there isn’t a resource hub for Black entrepreneurs in your city, create one. Fearless is a small company and we have still managed to help 13 new companies get off the ground through our accelerator program, Hutch.

Hutch is an intensive 12-month program that gives entrepreneurs a blueprint for building successful digital service firms, by empowering them with the tools, mentorship and peer support they need to have a lasting impact. We think of this program kind of like a home base for our entrepreneurs, providing them with a foundation of support so they can grow without getting lost amongst bigger companies in the industry.

Help create the spaces in your community that will foster innovation and business growth.

Powered by WPeMatico

Akron, Ohio, the hometown of LeBron James; the seat of the U.S. tire industry; the 127 largest city in the U.S.; and the home of America’s first toy company, is now the latest site of a global experiment in whether cities can use behavioral economics to help foster good citizenship.

Thanks to the work of the city’s deputy mayor for integrated development, James Hardy, Akron is the first city to roll out services from an Israeli-based company called Colu. A startup backed by just over $20 million in financing from American and Israeli investors, the company has developed an app-based rewards service that cities can roll out to provide perks to users.

In Akron’s case, the initiative rewards points for shopping at local businesses that can be redeemed for discounts at those stores. The initial effort, which includes a platform for businesses to market directly to the app’s users, focuses on businesses owned by women and minorities (a response to the movement for racial justice that has sprung up in the wake of the murder of George Floyd in Minneapolis).

Akron is the first city of what Colu founder Amos Meiri expects to be a nationwide rollout throughout the U.S. The company already has managed to ink another agreement with the city of Chula Vista, Calif.

Colu, which has raised its capital from investors associated with blockchain technologies like Barry Silbert’s Digital Currency Group; the Boston-based venture capital firm, Spark Capital; New York’s Box Group and the Israeli corporate conglomerate, IDB Group, has deep ties to the cryptocurrency world of alternative financial instruments through Meiri.

One of the original architects of the Color coin blockchain experiment, Meiri’s work with Colu is in some ways an extension of that effort to create new kinds of economies powered by alternative financial mechanisms.

Meiri said cities typically pay for Colu out of their marketing budgets as a new way to communicate and attempt to influence civic behavior.

For Akron’s government officials, the company’s services are a way to boost locally owned businesses that have been hit hard by the state’s attempts to contain the COVID-19 outbreak.

“Our locally owned small businesses are facing enormous challenges and we need out-of-the-box ideas that safely connect them to consumers and turn local spending into a source of pride for residents,” said Akron Mayor Dan Horrigan, in a statement. “Our partnership with Colu will enable the city to reward customers for shopping local, improving revenues for our small businesses while helping folks stretch their dollars.”

Earlier work with the municipal government in Tel Aviv promoted sustainable business practice and encouraged businesses to do more to manage their waste and carbon footprint by introducing a “green label.” Businesses that followed the city’s guidelines were given the label and shoppers were encouraged to frequent those merchants.

Colu envisions itself as more than just a marketing and rewards platform for businesses. The company hopes it can draw users into a kind of social networking platform for civic engagement where users can share their own stories about city-life and their interactions with local business owners and the community.

In some ways, it’s a kinder, gentler version of China’s social credit scoring system, which is also designed to influence civic behavior. In this formulation, there’s a rewards system, but no mechanisms to punish citizens for bad behavior.

“Akron has a long history of innovation within our economy — this initiative draws on that legacy,” said Deputy Mayor Hardy, in a statement. “By putting the future of Akron’s locally owned small businesses in the palm of our citizens’ hands, we hope to make it easy for consumers to keep their money local and continue to strengthen our incredible community.”

Powered by WPeMatico

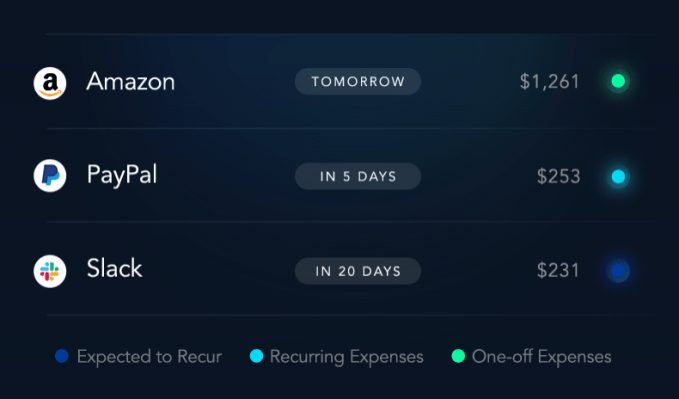

Digits, a fintech startup hailing from the same team that built and sold Crashlytics to Twitter, is officially launching today after two years of development. It’s also announcing a $22 million Series B round of funding led by GV, as it makes its public debut.

While the company had been fairly quiet about product details while in stealth mode, it’s today unveiling its first product: a visual, machine learning-powered expense monitoring dashboard aimed at startups and small businesses.

The dashboard, called Digits for Expenses, helps business owners track how their company is spending money, by showing things like spend by category, by identifying vendors and recurring expenses and by offering real-time alerts, among other features.

Instead of requiring business owners to make a switch from their existing financial solutions, Digits connects with the accounting software, banks, payroll providers, financial packages, sources of revenue and credit cards the business already uses — like Xero, QuickBooks, NetSuite, Citi, Bank of America or Chase, for example.

Instead of requiring business owners to make a switch from their existing financial solutions, Digits connects with the accounting software, banks, payroll providers, financial packages, sources of revenue and credit cards the business already uses — like Xero, QuickBooks, NetSuite, Citi, Bank of America or Chase, for example.

At launch, the list includes more than 9,000 banks, with support for Xero and NetSuite coming soon.

After setup, Digits will then automatically analyze the company’s spend and visualize it, in real time.

While visualizations of data may be reminiscent of personal finance startup Mint, Digits’ web-based solution is more technical in nature and offers an expanded analysis of the data on hand. Plus, as a business solution, it has to offer features like security, permissioning and collaborative workflows, which results in a more sophisticated product.

Digits also uses machine learning technology to predictively categorize transactions as they happen and the software can alert users to anomalies — like suspicious activity or unexpectedly large transactions — in real time. Business owners can use the dashboard to find out things like how quickly expenses are growing, what the cash flow looks like, where costs can be trimmed, what services are being paid for on a recurring basis and more, and can search for transactions.

Digits also uses machine learning technology to predictively categorize transactions as they happen and the software can alert users to anomalies — like suspicious activity or unexpectedly large transactions — in real time. Business owners can use the dashboard to find out things like how quickly expenses are growing, what the cash flow looks like, where costs can be trimmed, what services are being paid for on a recurring basis and more, and can search for transactions.

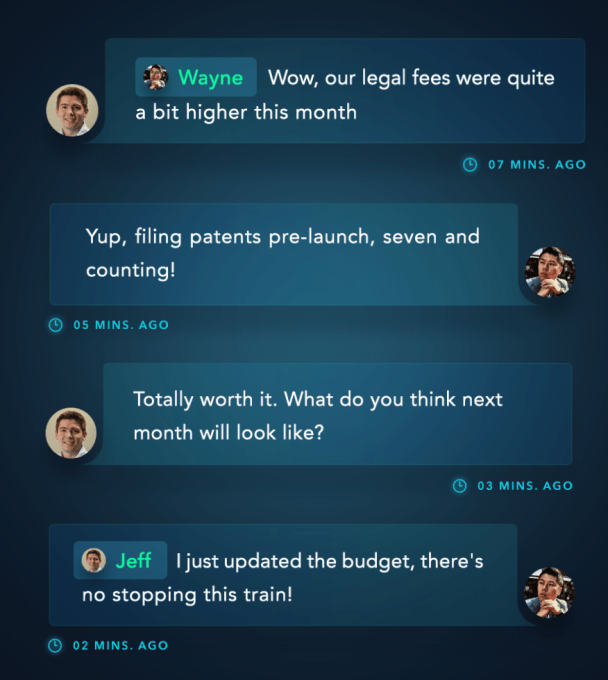

The software also supports the ability to comment on transactions, loop in a colleague to ask for clarification about a charge and upload missing receipts. Everything uses HTTPS along with TLS and certificates so data is encrypted between Digit’s services and at rest.

The original idea for Digits came from a problem that co-founders Wayne Chang and Jeff Seibert faced themselves when building Crashlytics. As they explained previously, their focus as entrepreneurs was on solving technical challenges, not on the operational side of running a business.

Many entrepreneurs also find themselves in this same space. They’re trying to solve a problem or crack a tough engineering puzzle, but instead have to redirect their time and resources to spreadsheets, financial reports, transaction records and other paperwork required to actually run the business.

“Startups and small businesses today simply don’t have the resources to manage their finances internally. Most of them still settle for spreadsheets, and the lucky ones work on an hourly basis with external accountants,” explains Seibert. “As a result, their accounting itself is seen as a cost-center, and they pay for little beyond the basic monthly financial statements — Profit & Loss, Balance Sheet, etc. By the time those statements are delivered — weeks after the end of each month — they’re already out of date,” he said.

That means things businesses need — like updates, one-off reports and new budgets — can require additional costs and longer wait times, so they get skipped.

The COVID-19 pandemic has put even more pressure on small businesses, many of which are now struggling to even survive. As a result, Digits has decided to launch the product for free to those who sign up — not a free trial, but actually free. It plans to later charge for additional products and paid upgrades to support its own business.

Digits is able to make this offer because of its now-expanded venture funding.

Already, the company had raised $10.5 million in Series A funding in a round led by Benchmark. That round had included a sizable 72 angel investors as well, including founders and CEOs from companies like Box, GitHub, Tinder, Twitch, StitchFix, SoFi and several others — entrepreneurs with an understanding of the problems Digits is aiming to solve.

Today, Digits is announcing an additional $22 million led by Jessica Verrilli at GV, who also now joins Digits’ board alongside Benchmark’s Peter Fenton. (Benchmark also participated in the new round).

“Jeff and Wayne are masterful at creating intuitive, high-utility products from complicated data,” said Verrilli about the GV investment. “I saw this up close with Crashlytics and Twitter, and I’m thrilled to partner with them on Digits as they reimagine financial software for startups,” she added.

The startup, now a team of 18 and hiring, was already offering its software solution to a group of customers ahead of today’s public launch, who effectively operated as beta testers allowing Digits to refine its product. Digits isn’t able to share its customer names, for the most part. However, it noted that Coda was one of early adopters and provided valuable feedback.

It also has over 10,000 companies who joined its waitlist over the past two years who are now being let in.

At the time of its Series A, Digits saw more than $1.5 billion in transaction value flowing across its production systems. That number has since grown to $8 billion.

The software is free starting today for U.S.-based small businesses. The company plans to add support for international markets later this year.

Powered by WPeMatico

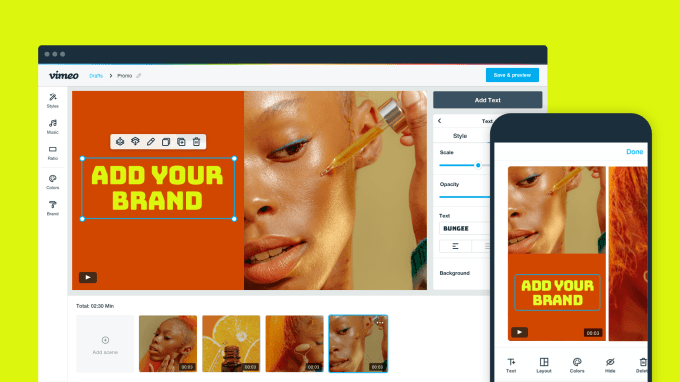

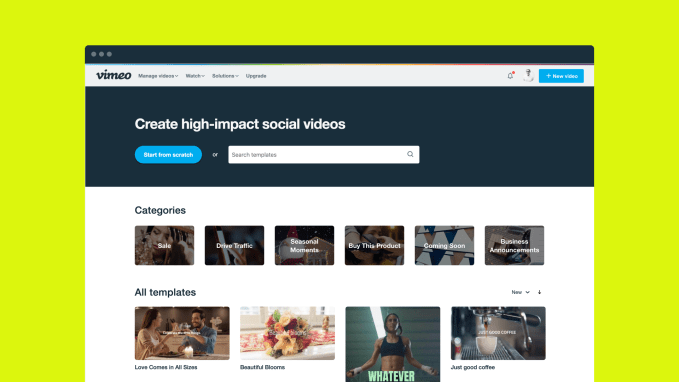

Vimeo signaled last year its plans to move further into the social video creation and editing space with its acquisition of short-form video editor Magisto. Today, the company is unveiling the results of its work in the months following the deal’s close with the debut of Vimeo Create. The new app includes a set of video creation tools aimed at small businesses and marketers looking to tell their stories using social video, but who lack the resources, time or budget to invest in video production at the scale they need to compete.

With Vimeo Create, available on both the desktop and as an app, businesses choose from pre-made, professionally designed video templates that can be customized to meet their needs. More advanced users could opt to start a new video from scratch, as an alternative.

The app includes a library of stock content to add to videos, including millions of HD video clips, photos and commercially licensed music tracks available for no extra fee, Vimeo says. Businesses also can customize their videos by selecting the colors, fonts, layouts, logos, text captions and calls-to-action they want to use.

The app then leverages AI-powered technology to turn the clips, photos, music and text into a high-quality social video in minutes.

Vimeo Create also simplifies the process of designing videos for different social platforms, where aspect ratios (e.g. square, vertical, horizontal) and format requirements vary. After the video is finalized, users are able to publish across the web — including to Facebook, YouTube, Instagram, Twitter and LinkedIn — as a part of the Vimeo Create workflow.

The move into social video creation is part of Vimeo’s larger strategy of becoming a one-stop shop for companies and individuals who publish videos online. The company has long since abandoned its plans to be a YouTube competitor, instead seeing the potential in the other side of the video market. Today, Vimeo makes money by offering tools and services to video creators both large and small. It has launched tools for uploading and live streaming across social sites and updated its mobile app to include more features previously available only to desktop users, among other things.

Vimeo’s decision to prioritize social video resulted from its own research. The company found that only 22% of small business owners felt they were using enough video. The businesses complained that issues around time, cost and complexity were keeping them from going further. Nearly all (96%) of small business owners said they would create more video if all those friction points were removed.

The service was built using parts of Magisto’s backend and its AI, but the overall app, feature set, content, user interface and integration into Vimeo’s tools were built from the ground up, the company says.

The company hopes Vimeo Create will help it to grow its subscription revenue, as the service is offered as a part of Vimeo’s Pro, Business and Premium membership plans, instead of as a standalone paid or freemium app.

“Video is the most impactful medium we have today for human expression at scale, and businesses

need an online video strategy to reach their customers. But the research is clear: small business owners

and entrepreneurs don’t have the tools, time or budgets to make videos at the volume and quality

needed to compete,” said Vimeo CEO Anjali Sud, in a statement about the launch. “Vimeo Create levels the playing field. It’s a radically simple tool that shortens the distance from idea to execution, so more businesses can have a successful video strategy.”

Vimeo isn’t alone in addressing the social video needs of small businesses. Last fall, Facetune maker Lightricks launched a full suite of apps for small businesses to use for their social media marketing campaigns. There also are dozens of tools for video editing on the market, including those from incumbents, like Adobe and Apple, as well as from others like Magisto, Canva, PicsArt and many more that offer features craved by small business owners like templates, easy editing tools, access to stock content and support for one-click multi-platform publishing, among other things.

Vimeo first launched Vimeo Create into beta back in January, but today it’s available to all across web, iOS and Android.

Powered by WPeMatico