Shippo

Auto Added by WPeMatico

Auto Added by WPeMatico

What happens to technology companies with slowing growth and a rising focus on profitability before they reach behemoth scale? How much does the market value hypergrowth?

Just because a technology startup has a hot start, that doesn’t mean it will grow quickly forever. Most will wind up somewhere in the middle — or worse. Put simply, there is a larger number of tech companies that do fine or a little bit worse after they reach scale.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

But what every investor hopes for is the hot company that can keep growth alive even after reaching material scale, running through walls, competitors, economic headwinds and anything else that comes its way. Those companies don’t end up worth a few hundred million, or a billion, but can end up valued in the dozens of billions or more.

In reverse, tech companies — even those with strong gross margins — with slipping growth can see their multiples compress rapidly. Then, the vultures circle.

In reverse, tech companies — even those with strong gross margins — with slipping growth can see their multiples compress rapidly. Then, the vultures circle.

Which explains some of the news we’ve seen recently in the market. As Dropbox comes under fresh pressure from external parties, joining its erstwhile rival Box in the public-market growth penalty box, we’re seeing companies like Braze, Gong, Shippo and others rip ahead with rapid-fire funding rounds or public brags about their growth.

While the differential between the two groups is clear, it’s still worth exploring in more detail. Let’s talk about the growth dividend. Or, if you’d prefer, the existential cost of growth deceleration.

The news this week that Dropbox has attracted an activist shareholder should not have been a surprise. Its former rival Box is in the midst of a long-running struggle with an activist investor of its own. (More here.)

Powered by WPeMatico

This morning Shippo, a software company that provides shipping-related services to e-commerce companies, announced a new $45 million investment. The new capital values the startup at $495 million. TechCrunch is calling the new funding a Series D as it is a priced round that followed its Series C; the company did not award the round a moniker.

Shippo’s 2020 Series C, a $30 million transaction that was announced last April, valued the company at around $220 million. D1 Capital led both Shippo’s Series C and D rounds, implying that it was content to pay around twice as much for the company’s equity in 2021 than it was in 2020. (Recall that investors doubling-down on previous bets as lead investor in successive rounds is no longer considered to be a negative signal concerning startup quality, but a positive indicator.)

Why raise more money so soon after its last round? According to Shippo CEO and founder Laura Behrens Wu, her company made material progress on customer acquisition and partnerships last year. That led to a decision around the time of Shippo’s Q4 board meeting with her investors that it was a good time to put more capital into the company.

In a sense the timing is reasonable. As Shippo scales its customer base, it can negotiate better shipping deals with various providers, which, in turn, help it continue to attract new customers. Behrens Wu noted in an interview with TechCrunch that when her company was helping its early customers ship just a few packages, shipping companies it supports on its platform didn’t want to meet with the startup. Now armed with more volume, Shippo can recycle customer demand into partner leverage, improving its total customer offering.

Behrens Wu said that Shippo had secured such a partnership with UPS before it raised its new round.

Turning to growth, Shippo doubled its platform spend, or “GPV” last year. GPV is the company’s acronym for gross postage volume. It roughly tracks with revenue, TechCrunch confirmed. So Shippo likely doubled its top-line last year. That’s good. Shippo wants to do that again this year, Behrens Wu told TechCrunch. The startup will also double its headcount this year, adding around 150 people.

Now flush with more capital, what’s next for Shippo? Per its CEO, the startup wants to invest more in platforms (where Shippo is baked into a marketplace, for example), international expansion (Shippo only does a “little bit” of international shipping, per Behrens Wu), and double-down on what it considers its core customer base.

TechCrunch was curious about how broad Shippo might take its product from its original home in shipping labels. The startup said that there’s lots of room in the journey of a package, from pre-purchase on, where her company might expand into. However, Behrens Wu cautioned that such a broadening of product work is not an immediate focus at her company.

Let’s see how long the current e-commerce boom lasts and how far this new capital can take Shippo. If it doubles in size again this year we’ll have to start its IPO countdown sometime in mid-2022.

Powered by WPeMatico

Since moving to the United States, I’ve come to appreciate and admire the United States Postal Service as a symbol of American ingenuity and resilience.

Like electricity, telephones and the freeway system, it’s part of our greater story and what binds the United States together. But it’s also something that’s easy to take for granted. USPS delivers 181.9 million pieces of First Class mail each day without charging an arm and a leg to do so. If you have an address, you are being served by the USPS — and no one’s asking you for cash up front.

As CEO of Shippo, an e-commerce technology platform that helps businesses optimize their shipping, I have a unique vantage point into the USPS and its impact on e-commerce. The USPS has been a key partner since the early days of Shippo in making shipping more accessible for growing businesses. As a result of our work with the USPS, along with several other emerging technologies (like site builders, e-commerce platforms and payment processing), e-commerce is more accessible than ever for small businesses.

And while my opinion on the importance of the USPS is not based on my company’s business relationship with the Postal Service, I want to be upfront about the fact that Shippo generates part of its revenue from the purchase of shipping labels through our platform from the USPS along with several other carriers. If the USPS were to stop operations, it would have an impact on Shippo’s revenue. That said, the negative impact would be far greater for many thousands of small businesses.

I know this because at Shippo, we see firsthand how over 35,000 online businesses operate and how they reach their customers. We see and support everything from what options merchants show their customers at checkout through how they handle returns — and everything in between. And while each and every business is unique with different products, customers operations and strategies, they all need to ship.

In the United States, the majority of this shipping is facilitated by the USPS, especially for small and medium businesses. For context, the USPS handles almost half of the world’s total mail and delivers more than the top private carriers do in aggregate, annually, in just 16 days. And, it does all of this without tax dollars, while offering healthcare and pension benefits to its employees.

As has been the case for many organizations, COVID-19 has significantly impacted the USPS. While e-commerce package shipments continue to rise (+30% since early March based on Shippo data), it has not been enough to overcome the drastic drop in letter mail. With this, I’ve heard opinions of supposed “inefficiency,” calls for privatization, pushes for significant pricing and structural changes, and even indifference to the possibility of the USPS shutting down.

Amid this crisis, we all need the USPS and its vital services now more than ever. In a world with a diminished or dismantled USPS, it won’t be Amazon, other major enterprises, or even Shippo that suffer. If we let the USPS die, we’ll be killing small businesses along with it.

Quite often, opinions on the efficiency (or lack thereof) of the USPS are very narrow in scope. Yes, the USPS could pivot to improve its balance sheet and turn operating losses into profits by axing cumbersome routes, increasing prices and being more selective in who they serve.

However, this omits the bigger picture and the true value of the USPS. What some have dubbed inefficient operations are actually key catalysts to small business growth in the United States. The USPS gives businesses across the country, regardless of size, location or financial resources, the ability to reach their customers.

We shouldn’t evaluate the USPS strictly on balance sheet efficiency, or even as a “public good” in the abstract. We should look at how many thousands of small businesses have been able to get started thanks to the USPS, how hundreds of billions of dollars of commerce is made possible by the USPS annually and how many millions of customers, who otherwise may not have access to goods, have been served by the USPS.

In the U.S., e-commerce accounts for over half a trillion dollars in sales annually, and is growing at double-digit rates each year. When I hear people talk about the growth of e-commerce, Amazon is often the first thing that comes up. What doesn’t shine through as often is the massive growth of small business — which is essential to the health of commerce in general (no one needs a monopoly!). In fact, the SMB segment has been growing steadily alongside Amazon. And with the challenges that traditional businesses face with COVID-19, more small businesses than ever are moving online.

USPS Priority Mail gets packages almost anywhere in the U.S. in two to three days (average transit time is 2.5 days based on Shippo data) and starts at around $7 per shipment, with full service: tracking, insurance, free pickups and even free packaging that they will bring to you.

In a time when we as consumers have become accustomed to free and fast shipping on all of our online purchases, the USPS is essential for small businesses to keep up. As consumers we rarely see behind the curtain, so to speak, when we interact with e-commerce businesses. We don’t see the small business owner fulfilling orders out of their home or out of a small storefront, we just see an e-commerce website. Without the USPS’ support, it would be even harder, in some cases near impossible, for small business owners to live up to these sky-high expectations. For context, 89% of U.S.-based SMBs (under $10,000 in monthly volume) on the Shippo platform rely on the USPS.

I’ve seen a lot of talk about the USPS’s partnership with Amazon, how it is to blame for the current situation, and how under a private model, things would improve. While we have our own strong opinions on Amazon and its impact on the e-commerce market, Amazon is not the driver of USPS’s challenges. In fact, Amazon is a major contributor in the continued growth of the USPS’s most profitable revenue stream: package delivery.

While I don’t know the exact economics of the deal between the USPS and Amazon, significant discounting for volume and efficiency is common in e-commerce shipping. Part of Amazon’s pricing is a result of it actually being cheaper and easier for the USPS to fulfill Amazon orders, compared to the average shipper. For this process, Amazon delivers shipments to USPS distribution centers in bulk, which significantly cuts costs and logistical challenges for the USPS.

Without the USPS, Amazon would be able to negotiate similar processes and efficiencies with private carriers — small businesses would not. Given the drastic differences in daily operations and infrastructure between the USPS and private carriers, small businesses would see shipping costs increase significantly, in some cases by more than double. On top of this, small businesses would see a new operational burden when it comes to getting their packages into the carriers’ systems in the absence of daily routes by the USPS.

Overall, I would expect to see the level of entrepreneurship in e-commerce slow in the United States without the USPS or with a private version of the USPS that operates with a profit-first mindset. The barriers to entry would be higher, with greater costs and larger infrastructure investments required up-front for new businesses. For Shippo, I’d expect to see a much greater diversity of carriers used by our customers. Our technology that allows businesses to optimize across several carriers would become even more critical for businesses. Though, even with optimization, small businesses would still be the group that suffers the most.

Today, most SMB e-commerce brands, based on Shippo data, spend between 10-15% of their revenue on shipping, which is already a large expense. This could rise well north of 20%, especially when you take into account surcharges and pick-up fees, creating an additional burden for businesses in an already challenging space.

I urge our lawmakers and leaders to see the full picture: that the USPS is a critical service that enables small businesses to survive and thrive in tough times, and gives citizens access to essential services, no matter where they reside.

This also means providing government support — both financially and in spirit — as we all navigate the COVID-19 crisis. This will allow the USPS to continue to serve both small businesses and citizens while protecting and keeping their employees safe — which includes ensuring that they are equipped to handle their front-line duties with proper safety and protective gear.

In the end, if we continue to view the USPS as simply a balance sheet and optimize for profitability in a vacuum, we ultimately stand to lose far more than we gain.

Powered by WPeMatico

Early this afternoon Shippo, a shipping software and services company, announced that it has closed a $30 million Series C. The funding round roughly doubles the capital that the firm has raised to-date, from a little over $29 million to just under $60 million.

The round, however, wasn’t put together recently. As is often the case with funding events, Shippo raised its capital a while back and is only announcing it now. According to its CEO, Laura Behrens Wu, her startup started raising its Series C in late Q4 2019, with the capital hitting its accounts the day after Christmas. So, Shippo started 2020 well capitalized, and should have a comfortable capital base heading into this year’s economic uncertainty.

The funding round was led by a new investor, D1 Capital Partners, and participated in by a number of prior investors including Uncork Capital (which led a 2014 Seed investment into the company), Union Square Ventures (which led the company’s Series A in 2016) and Bessemer (which led its 2017 Series B).

Shippo sits between retailers and consumers, helping sellers ship goods to buyers quickly and, it promises, inexpensively. The startup works with nearly five dozen shipping partners around the world, and plugs into the merchant worlds of Amazon, Shopify, Wix and others.

Like a number of successful startups, Shippo is trying to take something that is complex, and make it simple while generating revenue along the way. There are a number of loose examples we can lean on. For example, Plaid took all the complexity of talking to different financial institutions and shoved it into an accessible API. Twilio did something similar for telephony. Stripe made payments simple for others to integrate. You get the idea. Shippo wants to the same for shipping.

So far its model has good momentum. Heading into its funding round the firm had doubled (“100% growth,” Behrens Wu) in the preceding year, the sort of expansion that investors covet. It’s never bad to raise on the back of aggressive growth, as Shippo’s Series C shows; the company’s new valuation is “slightly higher” than TechCrunch’s estimate of $150 million, according to its CEO.

And even more, Shippo’s hybrid software and sales model (it charges for access to its shipping software and generates revenue from select shipping spend) creates attractive economics. Shippo’s gross margins are right around 80%, according to the startup, putting the company in the middle-upper tier of SaaS firms. Its growth isn’t based on the upselling shipping by a few points at volume; Shippo does have venture-ready economics.

It might seem odd to stress that point, but after WeWork’s implosion, it’s worth checking to make sure that startups raising as if they have strong revenue quality actually do.

Shippo has big aspirations, as you’d expect. “When you think about shipping software,” Behrens Wu told TechCrunch during an interview, “most people, even in tech, can’t name a single shipping software company, but everyone can name one or two payment companies. Everyone knows PayPal, Stripe, maybe Adyen or Braintree.” She wants to make Shippo as well known for shipping as Stripe is for payments.

There was secular movement towards her vision even before the pandemic. Today, online shopping — the grist for Shippo’s mill — is even more important. And it’s likely to become even more so over time, if growth shown by Amazon and Shopify in recent quarters is any indication of what’s to come, which means that the market for Shippo’s services will grow in time, and it’s always easier to grow in an expanding market than to claw for share in a stagnant pool.

Finally, in addition to its new capital and raised valuation, Shippo also announced that it has hired Catherine Stewart, former chief business officer at WordPress juggernaut Automattic, to be its COO. If Shippo is hiring a COO now, then we expect to see a CFO added around the time of its Series D. And then we get to start annoying the company about its IPO timeline.

Shippo is one of the lucky startups that raised right before the world changed. Now it’s up to the startup to conserve cash while continuing to grow while the global economy struggles. Let’s see how it performs.

Powered by WPeMatico

Depending on which study you believe, the wearable and digital health market could be worth anywhere from $30 billion to nearly $90 billion in the next six years.

If the numbers around the size of the market are a moving target, just think about how to gauge the validity and efficacy of the products that are behind all of those billions of dollars in spending.

Andy Coravos, the co-founder of Elektra Labs, certainly has.

Coravos, whose parents were a dentist and a nurse practitioner, has been thinking about healthcare for a long time. After a stint in private equity and consulting, she took a coding bootcamp and returned to the world she was raised in by taking an internship with the digital therapeutics company Akili Interactive.

Coravos always thought she wanted to be in healthcare, but there was one thing holding her back, she says. “I’m really bad with blood.”

That’s why digital therapeutics made sense. The stint at Akili led to a position at the U.S. Food and Drug Administration as an entrepreneur in residence, which led to the creation of Elektra Labs roughly two years ago.

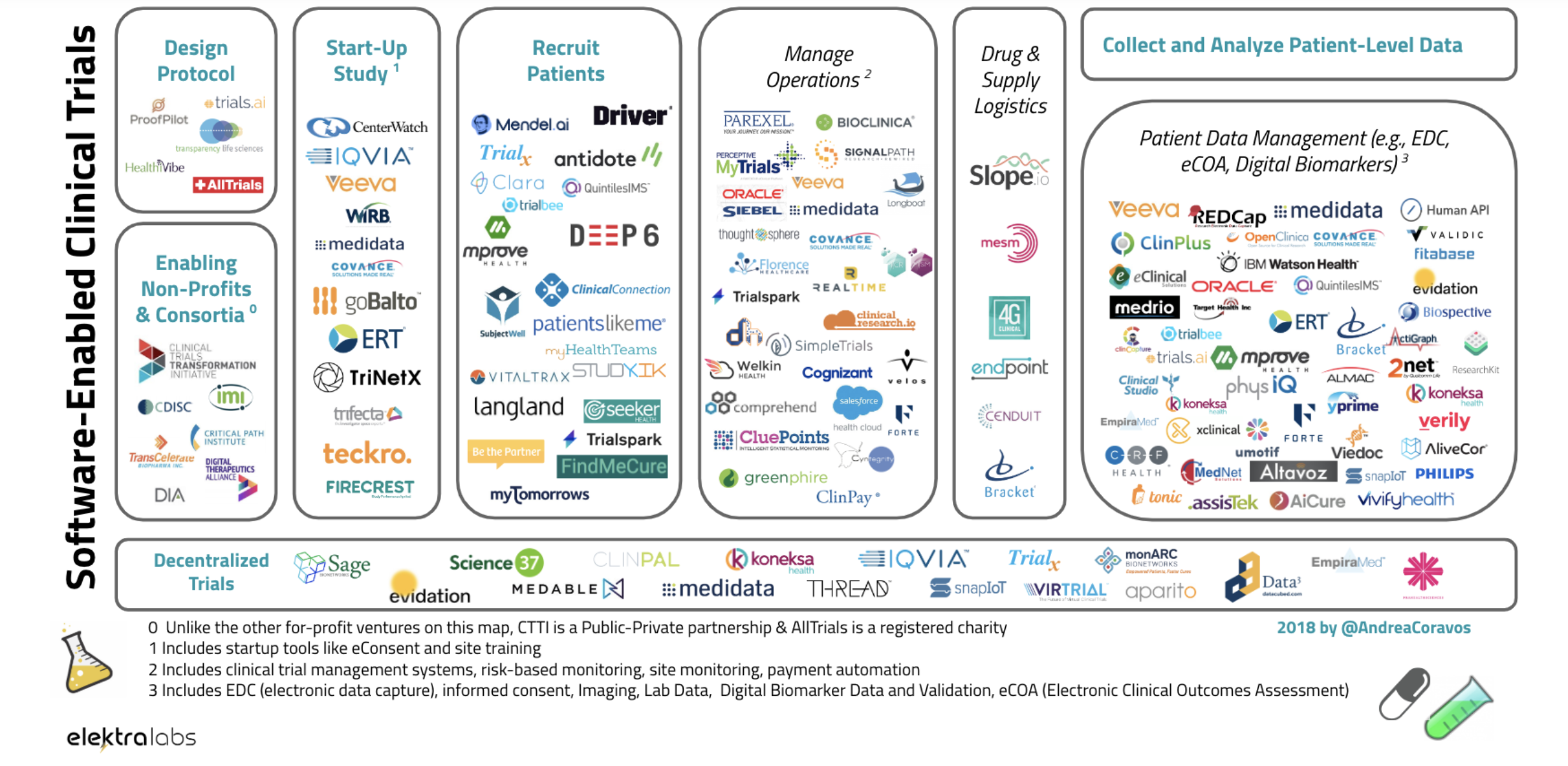

Now the company is launching Atlas, which aims to catalog the biometric monitoring technologies that are flooding the consumer health market.

These monitoring technologies, and the applications layered on top of them, have profound implications for consumer health, but there’s been no single place to gauge how effective they are, or whether the suggestions they’re making about how their tools can be used are even valid. Atlas and Elektra are out to change that.

The FDA has been accelerating its clearances for software-driven products like the atrial fibrillation detection algorithm on the Apple Watch and the ActiGraph activity monitors. And big pharma companies like Roche, Pfizer and Novartis have been investing in these technologies to collect digital biomarker data and improve clinical trials.

Connected technologies could provide better care, but the technologies aren’t without risks. Specifically, the accuracy of data and the potential for bias inherent in algorithms that were created using flawed data sets mean there’s a lot of oversight that still needs to be done, and consumers and pharmaceutical companies need to have a source of easily accessible data about the industry.

”The increase in FDA clearances for digital health products coupled with heavy investment in technology has led to accelerated adoption of connected tools in both clinical trials and routine care. However, this adoption has not come without controversy,” said Coravos in a statement. “During my time as an Entrepreneur in Residence in the FDA’s Digital Health Unit, it became clear to me that like pharmacies which review, prepare, and dispense drug components, our healthcare system needs infrastructure to review, prepare, and dispense connected technologies components.”

The analogy to a pharmacy isn’t an exact fit, because Elektra Labs currently doesn’t prepare or dispense any of the treatments that it reviews. But Atlas is clearly the first pillar that the digital therapeutics industry needs as it looks to supplant pharmaceuticals as treatments for some of the largest and most expensive chronic conditions (like diabetes).

Courtesy of Andrea Coravos/Elektra Labs

Coravos and here team interviewed more than 300 professionals as they built the Atlas toolkit for pharmaceutical companies and other healthcare stakeholders seeking a one-stop shop for all their digital healthcare data needs. Like a drug label, or nutrition label, Atlas publishes labels that highlight issues around the usability, validation, utility, security and data governance of a product.

In an article in Quartz earlier this year, Coravos made her pitch for Elektra Labs and the types of things it would monitor for the nascent digital therapeutics industry. It includes the ability to handle adverse events involving digital therapies by providing a single source where problems could be reported; a basic description for consumers of how the products work; an assessment of who should actually receive digital therapies, based on the assessment of how well certain digital products perform with certain users; a description of a digital therapy’s provenance and how it was developed; a database of the potential risks associated with the product; and a record of the product’s security and privacy features.

As the projections on market size show, the problem isn’t going to get any smaller. As Google’s recent acquisition bid for Fitbit and the company’s reported partnership with Ascension on “Project Nightingale” to collect and digitize more patient data shows, the intersection of technology and healthcare is a huge opportunity for technology companies.

“Google is investing more. Apple is investing more… More and more of these devices are getting FDA cleared and they’re becoming not just wellness tools but healthcare tools,” says Coravos of the explosion of digital devices pitching potential health and wellness benefits.

Elektra Labs is already working with undisclosed pharmaceutical companies to map out the digital therapeutic environment and identify companies that might be appropriate partners for clinical trials or acquisition targets in the digital market.

“The FDA is thinking about these digital technologies, but there were a lot of gaps,” says Coravos. And those gaps are what Elektra Labs is designed to fill.

At its core, the company is developing a catalog of the digital biomarkers that modern sensing technologies can track and how effective different products are at providing those measurements. The company is also on the lookout for peer-reviewed published research or any clinical trial data about how effective various digital products are.

Backing Coravos and her vision for the digital pharmacy of the future are venture capital investors, including Maverick Ventures, Arkitekt Ventures, Boost VC, Founder Collective, Lux Capital, SV Angel and Village Global.

Alongside several angel investors, including the founders and chief executives from companies including: PillPack, Flatiron Health, National Vision, Shippo, Revel and Verge Genomics, the venture investors pitched in for a total of $2.9 million in seed funding for Coravos’ latest venture.

“Timing seems right for what Elektra is building,” wrote Brandon Reeves, an investor at Lux Capital, which was one of the first institutional investors in the company. “We have seen the zeitgeist around privacy data in applications on mobile phones and now starting to have the convo in the public domain about our most sensitive data (health).”

If the validation of efficacy is one key tenet of the Atlas platform, then security is the other big emphasis of the company’s digital therapeutic assessment. Indeed, Coravos believes that the two go hand-in-hand. As privacy issues proliferate across the internet, Coravos believes that the same troubles are exponentially compounded by internet-connected devices that are monitoring the most sensitive information that a person has — their own health records.

In an article for Wired, Koravos wrote:

Our healthcare system has strong protections for patients’ biospecimens, like blood or genomic data, but what about our digital specimens? Due to an increase in biometric surveillance from digital tools—which can recognize our face, gait, speech, and behavioral patterns—data rights and governance become critical. Terms of service that gain user consent one time, upon sign-up, are no longer sufficient. We need better social contracts that have informed consent baked into the products themselves and can be adjusted as user preferences change over time.

We need to ensure that the industry has strong ethical underpinning as it brings these monitoring and surveillance tools into the mainstream. Inspired by the Hippocratic Oath—a symbolic promise to provide care in the best interest of patients—a number of security researchers have drafted a new version for Connected Medical Devices.

With more effective regulations, increased commercial activity, and strong governance, software-driven medical products are poised to change healthcare delivery. At this rate, apps and algorithms have the opportunity to augment doctors and complement—or even replace—drugs sooner than we think.

Powered by WPeMatico

Spearhead, an investment fund launched by AngelList’s Naval Ravikant and Accomplice’s Jeff Fagnan, plans to raise roughly $100 million for its third fund to provide founders $1 million each to invest in technology startups of their choosing.

The firm, created in 2017, initially provided founders $200,000 in investment capital sourced from Spearhead I, a $25 million vehicle, followed by Spearhead II, a $35 million vehicle. The group now plans roughly $100 million to give its founders 5x more capital to play with.

Each founder is allotted 15% carry in his or her fund, while Spearhead holds on to 5%. This time around, says Spearhead’s Jeff Fagnan, standout “leads,” or those tapped to deploy capital from the fund, will also have the opportunity to receive another $10 million to invest at the end of the two-year program during a culminating demo day-like event.

Spearhead is designed to train founders, who tend to be well-connected to the tech ecosystem and knowledgeable about startups, to be effective angel investors. Previous Spearhead leads include Shippo co-founder and chief executive officer Laura Behrens Wu, Scale AI founder and CEO Alex Wang and Rippling co-founder and chief technology officer Prasanna Sankar. To date, 35 founders have completed the program.

Applications to join Spearhead’s third cohort will become available this week. Those who participate will be encouraged to write checks at the pre-seed stage.

“There’s starting to be gap opening up again at the pre-seed,” Fagnan tells TechCrunch. “Founders are the right way to fill that gap. Founders backing their most talented friends … founders backing founders is the right way for this to go. We need to redefine who thinks of themselves as an angel investor.”

To be eligible to become a Spearhead lead, you must live in San Francisco, Los Angeles, Boston or New York City and run, or very recently have run, a startup. The firm plans to accept around 15 applicants.

“We are trying to build an active community within the leads and we’ve found smaller equals better; fewer people coming together and taking deeper accountability,” Fagnan said.

Spearhead leads can invest their capital in any tech startups, so long as there’s no existing equity relationship. Existing Spearhead investments include ZeroDown, Altitude Networks, Scythe, Airgarage, Cloosiv, Height, O.School, PopSQL, Superplastic and Sword Health.

Powered by WPeMatico