Sequoia Capital India

Auto Added by WPeMatico

Auto Added by WPeMatico

In “Macbeth,” Shakespeare described sleep as the “chief nourisher in life’s feast.” But like his titular character, many adults aren’t sleeping well. Revery wants to help with an app that combines cognitive behavioral therapy (CBT) for insomnia with mobile gaming concepts.

Founded in March 2021, Revery is currently in beta stealth mode and plans to launch its app in the United States later this year. The company announced today it has raised $2 million, led by Sequoia Capital India’s Surge program. Participants included GGV Capital, Pascal Capital, zVentures (Razer’s corporate venture arm) and angel investors like MyFitnessPal co-founder Albert Lee; gaming entrepreneur Juha Paananen; CRED founder Kunal Shah; Mobile Premier League founder Sai Srinivas; Carolin Krenzer; and Josh Lee.

Lee, a mutual friend, first introduced Revery’s founders, Tammie Siew and Khoa Tran, to one another. Before launching the startup, Siew worked at Sequoia Capital India, Boston Consulting Group and CRED, while Tran was a former product manager at Google.

Revery plans to focus on other mental health issues in the future, but it’s starting with sleep because “it has such a strong correlation with mental health and we’re leveraging protocols, cognitive behavioral therapy for insomnia, that’s robust and have been tried and tested for 30 years,” Siew told TechCrunch. “That is the first indication, but the goal is to build multiple games for other wellness indications as well.”

A study by research firm Infinium found that about 30% to 45% of adults in the world experience insomnia, a problem exacerbated by the COVID-19 pandemic. Chronic lack of sleep is linked to a host of health issues, including high blood pressure, strokes, depression and lowered immunity.

For Revery’s team, which also includes former Zynga and King lead game designer Kriti Sawa and software engineer Stephanie Wong, their focus on sleep is personal.

Revery’s team on a Zoom call

“Everyone on our team has a deeply personal connection to the mission, because everyone on our team has experienced, or had a family member or friends go through challenges in mental health,” said Siew. “They’ve seen how late intervention creates consequences that could have been avoided if they had gotten help earlier.”

When Tran was 15, he was diagnosed with hypertension and several other health conditions that needed medication. It wasn’t until he was 26 that Tran found out that sleep apnea was at the root of his medical issues. After getting surgery, Tran’s blood pressure became normal and many of his other conditions also improved.

“When I finally got treatment for my sleep disorder, only then did I realize the impact of sleep on mental health,” Tran said. “For me, I was really lucky that a doctor caught my sleep disorder and super lucky to have the time and resources to get treatment. For many people, it’s incredibly inaccessible.”

Revery’s medical advisory team includes the doctor who performed Tran’s surgery, Stanford Sleep Surgery Fellowship director Dr. Stanley Liu; Stanford professor and behavioral sleep medicine expert Dr. Fiona Barwick; and Dr. Ryan Kelly, a clinical psychologist who researches how video games can be used in therapy.

When people think of sleeping apps, ones that focus on meditation (Calm and Headspace, for example) or soothing noises usually come to mind. The Revery team isn’t sharing a lot of details about its app before launch, but says it draws from casual mobile games, which are designed to get people to return for short play sessions over a long period of time. The goal is to use gamification to make CBT practices interactive and fun, so it becomes part of users’ daily routines.

“That’s the same kind of gameplay that Zynga and King have used, which is why Kriti’s experience is super helpful,” said Siew. Casual games revolve around rewarding people for small actions, and for the Revery app, that means positive reinforcement for habits that contribute to better sleep. For example, it will reward people for putting down their phones.

“I think a lot of people have the misconception that solving sleep is only at the time you fall asleep. They don’t realize that sleep is impacted by what you do throughout the day,” Siew said. “A big part is also what are your thoughts, behavior and the other things that you do, so in order to effectively and sustainably improve sleep, we also have to change your thoughts and behaviors outside of the time you’re trying to fall asleep.”

In a statement, GGV Capital managing director Jenny Lee said, “We are excited about the growing mental wellness market, and believe that Revery’s unique mobile game-based approach has the opportunity to create immense impact. We are happy to back such a mission-driven team in this space.”

Powered by WPeMatico

Outbound sales managers typically rely on high volumes of inquiries to find customers, but this means that their revenue is often in proportion to the size of their team. Outplay helps them scale more easily with tools that automate campaigns, identifies the likeliest prospects and uses data to decide the right time to send pitches. The company announced today it has raised $7.3 million in seed funding from Sequoia Capital India.

The new capital will be used for tech development and hiring, and brings Outplay’s total raised so far to $9.3 million. Its previous funding was a $2 million raise from Sequoia Capital India’s Surge announced in March after Outplay took part in the program’s fourth cohort.

Since its seed round, Outplay says it has grown its revenue four times and now has customers in more than 50 countries, serving primarily B2B software companies.

Outplay was founded in 2019 by brothers Ram and Lax Papineni. The two previously launched AppVirality, a referral marketing tool for app developers.

Outplay was designed for sales team who contact prospects through multiple channels, like phone calls, emails, SMS, LinkedIn and Twitter. It integrates the channels into one interface, so salespeople don’t have to switch between apps. Outplay also automates sequences, or marketing campaigns that include an initial pitch sent through various channels and automatic follow-up messages if a reply isn’t received within a preset time.

The platform is meant to replace the process of cold-calling potential customers, which is time-consuming and difficult to scale, and enable salespeople to focus on the best prospects, helping them decide which channel to use and when to contact them.

Since its seed funding, Outplay has launched several new tools and features, including a Chrome extension that lets salespeople add prospects from LinkedIn and Gmail, send emails, make calls and perform other tasks without having to visit Outplay’s dashboard. It also added integrations with sales tools like Gong, Dynamics CRM and Zapier (Outplay was already integrated with customer relationship management platforms Pipedrive, Salesforce and HubSpot).

One major new feature is Magic Outbound Chat, a web chat box that is launched when a prospective customer clicks on an email link. Salespeople are notified and provided with context about the prospect. Laxman told TechCrunch that most chat boxes are designed for inbound sales teams, and Magic Outbound Chat has helped some of its teams grow their sales pipeline by 300%.

Laxman said that the onboarding process for Outplay takes just a few days and sales managers are provided with a playbook of successful sequences to help them get started.

Outplay’s competitors include unicorns Outbound and SalesLoft. Laxman said that in the mid-2000s, inbound sales processes and tech began rapidly evolving as SaaS adoption increased, but outbound sales teams still relied on the same high-volume tactics they had been using for years.

“The previous outbound sales tech disruption happened in 2011 when Outreach and Salesloft were founded. We really respect what they have done to the industry, but the approach is not scalable and the revenue eventually becomes a function of the size of the outbound sales team,” he said, adding that Outplay is changing the process by using data-driven signals to help sales representatives engage with the likeliest prospects at the right time in the right channel.

For example, Outplay’s Dynamic Sequencing automatically moves prospects from one sequence to another that has a higher chance of success. In one scenario, Outplay can be configured to move a prospective who opens a sales representative’s email more than four times to another sequence that focuses on people who appear interested in a product. Laxman said some of its customers have seen open rates as high as 80% in the second sequence with Dynamic Sequencing.

In a statement, Sequoia India principal Harshjit Sethi said, “Outbound sales needs are evolving rapidly and reps now need personalized, automated and contextual tools to drive sales which Outplay is successfully enabling. Sales reps spend an average of four hours per day on Outplay, demonstrating the effectiveness of the product which has category-leading customer reviews.”

Powered by WPeMatico

How big is the market in India for a neobank aimed at teenagers? Scores of high-profile investors are backing a startup to find out.

Bangalore-based FamPay said on Wednesday it has raised $38 million in its Series A round led by Elevation Capital. General Catalyst, Rocketship VC, Greenoaks Capital and existing investors Sequoia Capital India, Y Combinator, Global Founders Capital and Venture Highway also participated in the new round, which brings FamPay’s to-date raise to $42.7 million.

TechCrunch reported early this month that FamPay was in talks with Elevation Capital to raise a new round.

Founded by Sambhav Jain and Kush Taneja (pictured above) — both of whom graduated from Indian Institute of Technology, Roorkee in 2019 — FamPay enables teenagers to make online and offline payments.

The thesis behind the startup, said Jain in an interview with TechCrunch, is to provide financial literacy to teenagers, who additionally have limited options to open a bank account in India at a young age. Through gamification, the startup said it’s making lessons about money fun for youngsters.

Unlike in the U.S., where it’s common for teenagers to get jobs at restaurants and other places and understand how to handle money at a young age, a similar tradition doesn’t exist in India.

After gathering the consent from parents, FamPay provides teenagers with an app to make online purchases, as well as plastic cards — the only numberless card of its kind in the country — for offline transactions. Parents credit money to their children’s FamPay accounts and get to keep track of high-ticket spendings.

In other markets, including the U.S., a number of startups including Greenlight, Step and Till Financial are chasing to serve the teenagers, but in India, there currently is no startup looking to solve the financial access problem for teenagers, said Mridul Arora, a partner at Elevation Capital, in an interview with TechCrunch.

It could prove to be a good issue to solve — India has the largest adolescent population in the world.

“If you’re able to serve them at a young age, over a course of time, you stand to become their go-to product for a lot of things,” Arora said. “FamPay is serving a population that is very attractive and at the same time underserved.”

The current offerings of FamPay are just the beginning, said Jain. Eventually the startup wishes to provide a range of services and serve as a neobank for youngsters to retain them with the platform forever, he said, though he didn’t wish to share currently what those services might be.

Image Credits: FamPay

Teens represent the “most tech-savvy generation, as they haven’t seen a world without the internet,” he said. “They adapt to technology faster than any other target audience and their first exposure with the internet comes from the likes of Instagram and Netflix. This leads to higher expectations from the products that they prefer to use. We are unique in approaching banking from a whole new lens with our recipe of community and gamification to match the Gen Z vibe.”

“I don’t look at FamPay just as a payments service. If the team is able to execute this, FamPay can become a very powerful gateway product to teenagers in India and their financial life. It can become a neobank, and it also has the opportunity to do something around social, community and commerce,” said Arora.

During their college life, Jain and Taneja collaborated and built an app and worked at a number of startups, including social network ShareChat, logistics firm Rivigo and video streaming service Hotstar. Jain said their work with startups in the early days paved the idea to explore a future in this ecosystem.

Prior to arriving at FamPay, Jain said the duo had thought about several more ideas for a startup. The early days of FamPay were uniquely challenging to the founders, who had to convince their parents about their decision to do a startup rather than joining firms or startups as had most of their peers from college. Until being selected by Y Combinator, Jain said he didn’t even fully understand a cap table and dilutions.

He credited entrepreneurs such as Kunal Shah (founder of CRED) and Amrish Rau (CEO of Pine Labs) for being generous with their time and guidance. They also wrote some of the earliest checks to the startup.

The startup, which has amassed over 2 million registered users, plans to deploy the fresh capital to expand its user base and product offerings, and hire engineers. It is also looking for people to join its leadership team, said Jain.

Powered by WPeMatico

Four months after leading a $30 million growth round in Bibit, Sequoia Capital India has doubled down on its investment in the Indonesian robo-advisor app. Bibit announced today that the firm led a new $65 million growth round that also included participation from Prosus Ventures, Tencent, Harvard Management Company and returning investors AC Ventures and East Ventures.

This brings Bibit’s total funding to $110 million, including a Series A announced in May 2019. Its latest round will be used on developing and launching new products, hiring and increasing Bibit’s financial education services.

Bibit was launched in 2019 by Stockbit, a stock investing platform and community, and is part of a crop of Indonesian investment apps focused on new investors. Others include SoftBank Ventures-backed Ajaib, Bareksa, Pluang and FUNDtastic. Bibit runs robo-advisor services for mutual funds, investing users’ money based on their risk profiles, and claims that 90% of its users are millennials and first-time investors.

According to Indonesia’s Financial Services Authority (Otoritas Jasa Keuangan), the number of retail investors grew 56% year-over-year in 2020. For mutual funds in particular, Bibit said investors grew 78% year-over-year to 3.2 million, based on data from the Indonesia Stock Exchange and Central Securities Custodian.

Despite the economic impact of COVID-19, interest in stock investing grew as people took advantage of market dips (the Jakarta Composite Index fell in the first quarter of 2020, but is now recovering steadily). Apps like Bibit and its competitors want to make capital investing more accessible with lower fees and minimum investment amounts than traditional brokerages like Mandiri Sekuritas, which also saw an increase in new retail investors and average transaction value last year.

But the percentage of retail investors in Indonesia is still very low, especially compared to markets like Singapore or Malaysia, presenting growth opportunities for investment services.

Apps like Bibit focus on content that helps make capital investing less intimidating to first-time investors. For example, Ajaib also presents its financial educational features as a selling point.

In a press statement, Sequoia Capital India vice president Rohit Agarwal said, “Indonesian mutual fund customers have grown almost 10x in the past five years. Savings via mutual funds is the first step towards investing and Bibit has helped millions of consumers start their investing journey in a responsible manner. Sequoia Capital India is excited to double down on the partnership as the company brings the same customer focus to stock investing with Stockbit.”

Powered by WPeMatico

A startup by an Apple alum that has become home to millions of low-skilled workers in India said on Tuesday it has raised an additional $12.5 million, just five months after securing $8 million from high-profile investors.

One-year-old Apna said Sequoia Capital India and Greenoaks Capital led the $12.5 million Series B investment in the startup. Existing investors Lightspeed India and Rocketship VC also participated in the round. The startup, whose name is Hindi for “ours,” has now raised more than $20 million.

More than 6 million low-skilled workers such as drivers, delivery personnel, electricians and beauticians have joined Apna to find jobs and upskill themselves. But there’s more to this.

An analysis of the platform showed how workers are helping one another solve problems — such as a beautician advising another beautician to perform hair dressing in a particular way that tends to make customers happier and tip more, and someone sharing how they negotiated a hike in their salary from their employer.

“The sole idea of this is to create a network for these workers,” Nirmit Parikh, Apna founder and chief executive told TechCrunch in an interview. “Network gap has been a very crucial challenge. Solving it enables people to unlock more and more opportunities,” he said. Harshjit Sethi, principal at Sequoia India, said Apna was making inroads with “building a professional social network for India.”

The startup has become an attraction for several big firms, including Amazon, Flipkart, Unacademy, Byju’s, Swiggy, BigBasket, Dunzo, BlueStar and Grofers, which have joined as recruiters to hire workers. Apna offers a straightforward onboarding process — thanks to support for multiple local languages — and allows users to create a virtual business card, which is then shown to the potential recruiters. Parikh said Apna’s AI understands the cultural nuances, helping recruiters find the best candidates for their needs.

The past six months have been all about growth at Apna, said Parikh. The app, available on Android, had 1.2 million users in August last year, for instance. During this period, there have been 60 million interactions between recruiters and potential applicants, he said. The platform, which has amassed more than 80,000 employers, has a retention rate of over 95%, said Parikh.

“Apna has taken a jobs-centric approach to upskilling that we are very excited about. Lack of accountability has been the core issue with current skill / vocational learning alternatives for grey and blue-collar workers. Apna has turned the problem on its head by creating net-positive job outcomes for anyone who chooses to upskill on the platform,” said Vaibhav Agrawal, partner at Lightspeed India, in a statement.

Image Credits: Nirmit Parikh

Parikh got the idea of building Apna after he kept hearing about the difficulty his family and friends faced in India in hiring people. This was puzzling to Parikh, as he wondered how could there be a shortage of workers in India when there are hundreds of millions of people actively looking for such jobs. The problem, Parikh realized, was that there wasn’t a scalable networking infrastructure in place to connect workers with employers.

Before creating the startup, Parikh met workers and went undercover as an electrician and floor manager to understand the problems workers were facing. That journey has not ended. The startup talks to over 15,000 users each day to understand what else Apna could do for them.

“One of the things we heard was that users were facing difficulties with interviews. So we started groups to practice them with interviews. We also started upskilling users, which has made us an edtech player. We plan to ramp up this effort in the coming months,” said Parikh, who also started an AI firm more than a decade ago to solve challenges with electricity flux and then another startup to solve for information overload. (The first startup is now being run by family and friends, and the second firm was sold to Intel, Parikh said.)

Parikh said the startup is overwhelmed each day with the response it is getting from its customers and the industry. Each day, he said, people share how they were able to land jobs, or increase their earnings. In recent months, several high-profile executives from companies such as Uber and BCG have joined Apna to scale the startup’s vision, he said, adding that the problem Apna is solving in India exists everywhere and the startup’s hope is to eventually serve people across the globe.

The app currently has no ads, and Parikh said he intends to not change that. “Once you get in the ad business, you start doing things you probably shouldn’t be doing,” he said. The startup instead plans to monetize its platform by charging recruiters, and offering upskill courses. But Parikh maintained that Apna will always offer its courses to users for free. The premium version will target those who need extensive assistance, he said. The startup also plans to expand its team.

As is the case elsewhere, millions of people lost their livelihood in India in the past year as coronavirus shut many businesses and workers migrated to their homes. There are over 250 million blue and grey-collar workers in India, and providing them meaningful employment opportunities is one of the biggest challenges in our country, said Sethi.

Powered by WPeMatico

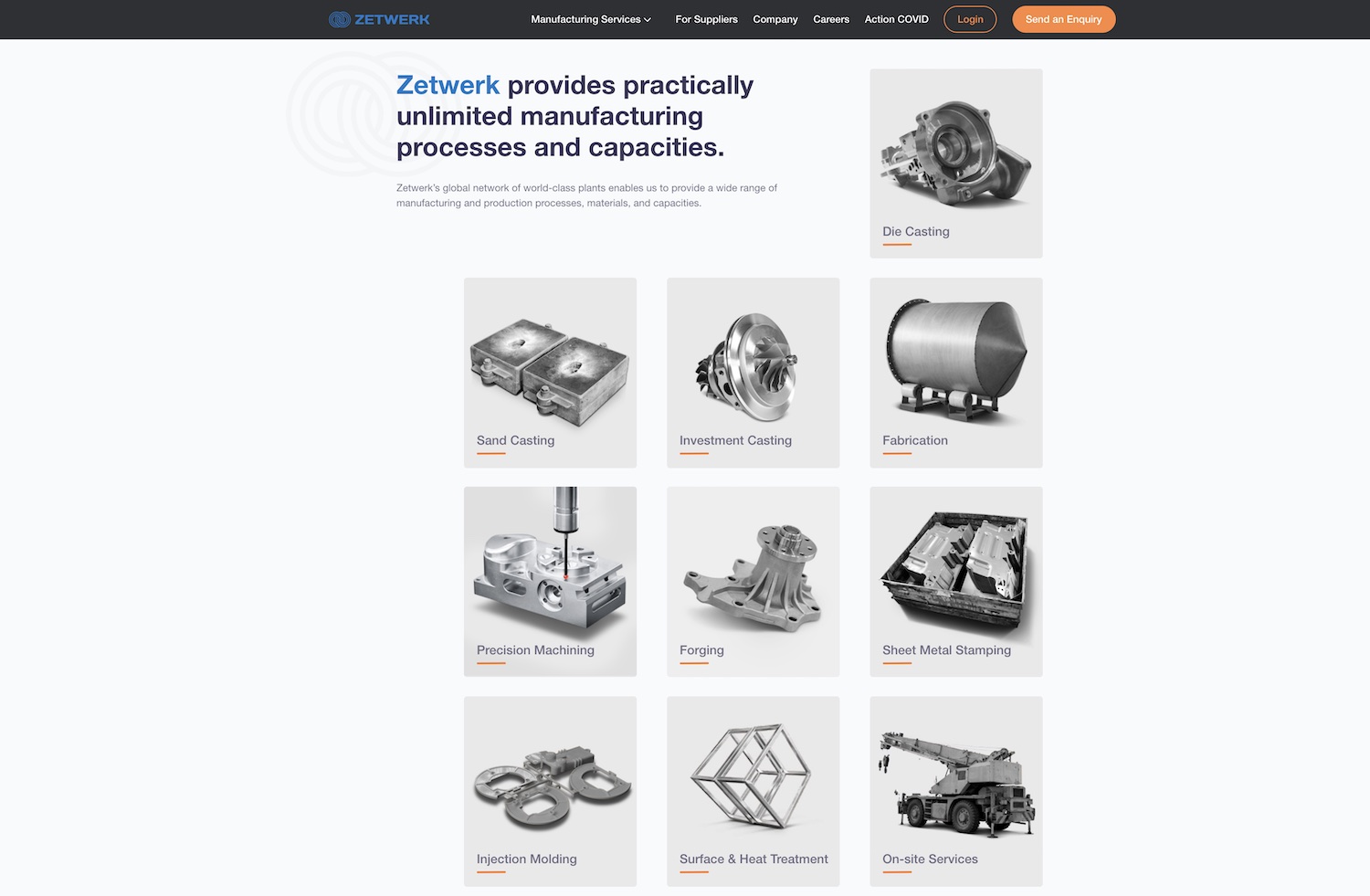

When you want to buy a refrigerator or a television, you can walk to the nearby electronics store or visit an e-commerce website like Amazon. But where do you go when you’re looking for parts of a crane, a door or chassis of different machines?

For several businesses globally, the answer to that question is increasingly Zetwerk, a Bangalore-based startup.

The three-year-old startup runs a business-to-business marketplace for manufacturing items that connects OEMs (original equipment manufacturers) and EPC (engineering procurement construction) customers with manufacturing small-businesses and enterprises.

All the products it sells today are custom-made. “Nobody has a stock of such inventories. You get the order, you find manufacturers and workshops that make them,” explained Amrit Acharya, co-founder and chief executive of Zetwerk, in an interview with TechCrunch.

Its customers — there are over 250 of them, up from 100 a year ago — operate across two-dozen industries (including process plants, oil & gas, steel, aerospace, medical devices, apparel and luxury goods) in the infrastructure space, and approach Zetwerk with digital designs they wish to be translated into physical products.

Customers aren’t alone in seeing value in Zetwerk. On Wednesday, the Indian startup said it has raised $120 million in a Series D financing round led by existing investors Greenoaks Capital and Lightspeed Venture Partners. Existing investors Sequoia Capital and Kae Capital also participated in the Series D round.

The new round, which brings Zetwerk’s to-date raise to $193 million, gives the firm a post-money valuation of somewhere between $600 million to $700 million, a person familiar with the matter told TechCrunch. (A quick side note: Zetwerk announced a $21 million Series C round last year, but ended up raising $31 million in that round.)

Zetwerk was co-founded by Acharya, Srinath Ramakkrushnan, Rahul Sharma and Vishal Chaudhary. Long before Acharya and Ramakkrushnan joined forces to tackle this space, they had been contemplating this idea.

Both of them studied at IIT Madras, went to the same exchange program in Singapore, and were colleagues at Kolkata-headquartered conglomerate ITC. While working there, they realized that part of a product manager’s job at the firm was dealing with gazillions of suppliers and the manufacturing items they offered.

The process was archaic: There were no databases, and people couldn’t track shipments.

The early version of Zetwerk, which was a database of suppliers, was a direct response to this. But after listening to requests from customers, the startup saw a bigger opportunity and transformed itself into a full-fledged marketplace with integrations with third-party vendors. Once a firm has placed an order, Zetwerk allows them to keep tabs on the progress of manufacturing and then the shipping. There are also quality checks in place.

Zetwerk website

Zetwerk operates in such a unique space today — Shailesh Lakhani, managing director at Sequoia India, says the startup has defined a new category of marketplace — that by and large it’s not competing with any other firm in India — or South Asia. (The startup competes with domain project consultants in the offline world.)

The opportunity in India itself is gigantic. According to industry reports, manufacturing today accounts for 14% of India’s GDP. Vaibhav Agarwal, a partner at Lightspeed, estimates that the market is as large as $40 billion to $60 billion in India and global trade-tailwinds that creates opportunity to serve international demand.

As more and more companies expand or shift their manufacturing to India — in part due to import duties imposed by India and geo-political tension with China, the global hub for manufacturing — this opportunity has only grown bigger in recent years.

“India has a lot of depth in manufacturing, but much of it has not been tapped well,” said Acharya.

Zetwerk — which grew 3X last year and reported revenue of $43.9 million in the financial year that ended in March, a 20X growth from the year prior — plans to deploy the new capital to expand to more areas of categories, and broaden its technology stack. Consumer goods (which covers items such as mixer grinders and TVs) is an area Zetwerk expanded to last year, and said it accounts for 15% of the revenue it generated in the last six months.

Currently 25 of its customers are in the U.S., Canada, Europe and other international markets. Acharya said the startup plans to open offices overseas this year as it scouts for more international customers.

“We are excited to partner with Zetwerk on the next leg of their journey, as they expand their value proposition globally. Zetwerk’s operating system for manufacturing has digitized multiple supply chains end-to-end, ensuring on-time delivery and high quality standards. This has led to rapid growth in India and internationally, with the potential to quickly become one of the most important manufacturing platforms globally,” said Neil Shah, partner at Greenoaks Capital, in a statement.

Powered by WPeMatico

Bangalore-headquartered Razorpay, one of a handful of Indian fintech startups that has demonstrated accelerated growth in recent years, has joined the coveted unicorn club after raising $100 million in a new financing round, the payments processing startup said on Monday.

The new financing round, a Series D, was co-led by Singapore’s sovereign wealth fund GIC and Sequoia India, the six-year-old Indian startup said. The new round valued the startup at “a little more than $1 billion,” co-founder and chief executive Harshil Mathur told TechCrunch in an interview.

Existing investors Ribbit Capital, Tiger Global, Y Combinator and Matrix Partners also participated in the round, which brings Razorpay’s total to-date raise to $206.5 million.

Razorpay accepts, processes and disburses money online for small businesses and enterprises. In recent years, the startup has expanded its offerings to provide loans to businesses and also launched a neo-banking platform to issue corporate credit cards, among other products.

Mathur and Shashank Kumar (pictured above), who met each other at IIT Roorkee, started Razorpay in 2014. They began to explore opportunities around a payments processing business after realizing just how difficult it was for small businesses such as young startups to accept money online less than a decade ago. There were very few payment processing firms in India then, and startups needed to produce a long list of documents.

The early team of about 11 people at Razorpay shared a single apartment as the co-founders rushed to meet with over 100 bankers to convince banks to work with them. The conversations were slow and remained in a deadlock for so long that the co-founders felt helpless explaining the same challenge to investors numerous times, they recalled in an interview last year.

To say things have changed for Razorpay would be an understatement. It’s become the largest payments provider for business in India, said Mathur. Razorpay, which competes with Prosus Ventures’ PayU, accepts a wide-range of payment options, including credit cards, debit cards, mobile wallets and UPI.

“Razorpay has established itself as a clear leader, with its strong focus on customer experience and product innovation,” said Choo Yong Cheen, chief investment officer for Private Equity at GIC, in a statement. “GIC has a long track record of partnering with leading fintech companies globally and is delighted to partner with Razorpay in its journey to transform payments and banking.”

India’s Razorpay launches corporate credit cards, current accounts support in major neo banking push

Some of Razorpay’s clients include budget lodging decacorn Oyo, fintech firm Cred, social giant Facebook, e-commerce Flipkart, top food delivery startups Zomato and Swiggy, online learning platform Byju’s, supply chain platform Zilingo, travel ticketing firms Yatra and Goibibo, and telecom giant Airtel .

The startup expects to process about $25 billion in transactions — up five times from last year — for nearly 10 million of its customers this year, said Mathur.

He attributed some of the growth to the coronavirus pandemic, which he said has accelerated the digital adoption among many businesses.

On the neo-banking and capital side, Mathur said, Razorpay expects RazorpayX and Razorpay Capital to account for about 35% of the startup’s revenue by the end of March next year.

Mathur said the startup’s payment processing service continues to be its fastest-growing business and does not need much capital to grow, so the startup will be deploying the fresh funds to expand its neo-banking offerings to include vendor payment, and expense and tax management and other features.

The startup, which aims to work with more than 50 million businesses by 2025, may also acquire a few firms as it explores opportunities around inorganic expansion in the neo-banking category, said Mathur.

“We will continue to make an impactful contribution to the growth of the industry, aid adoption in the under-served markets and drive new practices and a new thinking for the industry to follow. And this investment fits perfectly with our growth strategy,” he said.

While the coronavirus pandemic has slowed down deal-makings in India, about half a dozen startups in the country, including online learning platform Unacademy, and Pine Labs, have secured the unicorn status.

Powered by WPeMatico

Even as more than 150 million people are using digital payment apps each month in India, only about 20 million of them invest in mutual funds and stocks. A startup that is attempting to change that by courting millennials has just received a big backing.

Bangalore-headquartered Groww said on Thursday it had raised $30 million in its Series C financing round. YC Continuity, the growth-stage investment fund of Y Combinator, led the round, while existing investors Sequoia India, Ribbit Capital and Propel Ventures participated in it. The new round brings three-year-old startup Groww’s total raise-to-date to $59 million.

Groww allows users to invest in mutual funds, including systematic investment planning (SIP) and equity-linked savings. The app maintains a very simplified user interface to make it easier for its largely millennial customer base to comprehend the investment world. It offers every fund that is currently available in India.

In recent months, the startup has expanded its offerings to allow users to buy stocks of Indian firms and digital gold, said Lalit Keshre, co-founder and chief executive of Groww, in an interview with TechCrunch. Keshre and other three co-founders of Groww worked at Flipkart before launching their own startup.

Groww has amassed over 8 million registered users for its mutual fund offering, and over 200,000 users have bought stocks from the platform, said Keshre. The new fund will allow Groww to further expand its reach in the country and also introduce new products, he said.

One of those products is the ability to allow users to buy stocks of U.S.-listed firms and derivatives, he said. The startup is already testing this with select users, he said.

“We believe Groww is building the largest retail brokerage in India. At YC, we have known the founders since the company was just an idea and they are some of the best product people you will meet anywhere in the world. We are grateful to be partners with Groww as they build one of the largest retail financial platforms in the world,” said Anu Hariharan, partner at YC Continuity, in a statement.

More than 60% of Groww users come from smaller cities and towns of India and 60% of these have never made such investments before, said Keshre. The startup is conducting workshops in several small cities to educate people about the investment world. And that’s where the growth opportunities lie.

“India is seeing increased participation of retail investors in financial markets — with 2 million new stock market investors added in the last quarter alone,” said Ashish Agrawal, principal at Sequoia Capital India, in a statement.

Scores of startups such as Zerodha, INDWealth and Cube Wealth have emerged and expanded in India in recent years to offer wealth management platforms to the country’s growing internet population. Many established financial firms such as Paytm have also expanded their offerings to include investments in mutual funds. Amazon, which has aggressively expanded its financial services catalog in India in recent months, also sells digital gold in the country.

Powered by WPeMatico

DeHaat, an online platform that offers full-stack agricultural services to farmers, has raised $12 million as it looks to scale its network across India.

The Series A financial round for the eight-year-old Patna and Gurgaon-based startup was led by Sequoia Capital India. Dutch entrepreneurial development bank FMO, and existing investors Omnivore and AgFunder, also participated in the round. The startup, which began to seek funding from external investors last year, has raised $16 million to date and $3 million in venture debt.

DeHaat (which means village in Hindi) eases the burden on farmers by bringing together brands, institutional financers and buyers on one platform, explained Shashank Kumar, co-founder and chief executive of the startup, in an interview with TechCrunch.

The platform helps farmers secure thousands of agri-input products, including seeds and fertilizers, and receive tailored advisory on the crop they should sow in a season. “We have built a comprehensive database of crop tests to offer advice to farmers,” he said.

DeHaat, which employs 242 people, also helps them connect with 200 institutional partners to provide farmers with working capital, and when the season is over, helps them sell their yields to bulk buyers such as Reliance Fresh, food delivery startup Zomato and business-to-business e-commerce giant Udaan.

DeHaat today operates in 20 regional hubs in the eastern part of India — states such as Bihar, Uttar Pradesh, and Jharkhand — and serves more than 210,000 farmers, said Kumar.

Shashank Kumar, Amrendra Singh, Adarsh Srivastav and Shyam Sundar Singh co-founded DeHaat in 2012

The startup has developed a network of hundreds of micro-entrepreneurs in rural areas that distribute agri-input goods to farmers from their regional hubs and then bring back the output to the same hub.

“We have an app in local languages and a helpline desk that farmers, many of whom don’t own a smartphone, use to reach out to us and explain their pain points and needs,” he said.

DeHaat does not charge any fee for its advisory, but takes a cut whenever farmers use its platform to buy agri-inputs or sell their crop yields.

The startup will use the fresh capital to extend its network to 2,000 rural retail centres, on-board more micro-entrepreneurs for last-mile delivery and reach 1 million farmers by June of next year, said Kumar. DeHaat is also working on automating its supply chain and developing more sophisticated data analytics, he said.

At stake is India’s agriculture market that is worth $350 billion and serves nearly 100 million small and independent farmers, said Abhishek Mohan, VP at Sequoia Capital India, the VC fund that writes more checks than anyone else in the country.

“This industry is on the brink of a massive transformation thanks to ease of regulation, farmers getting organized and increasing penetration of smartphones. DeHaat is leveraging these trends to build the next-gen product in agricultural supply chain,” said Mohan in a statement.

“The tipping point that led to Sequoia India’s decision to partner with them was the field visit, where the farmers expressed how proud they were to be associated with a platform they felt truly worked in their favour. This impact and deep brand loyalty stems from the leadership team’s razor-sharp focus, deep empathy and fine execution,” he added.

Powered by WPeMatico

Two co-founders of Google Pay in India are building a neo-banking platform in the country — and they have already secured backing from three top VC funds.

Sujith Narayanan, a veteran payments executive who co-founded Google Pay in India (formerly known as Google Tez), said on Monday that his startup, epiFi, has raised $13.2 million in its Seed financial round led by Sequoia India and Ribbit Capital. The round valued epiFi at about $50 million.

David Velez, the founder of Brazil-based neo-banking giant Nubank, Kunal Shah, who is building his second payments startup CRED in India, and VC fund Hillhouse Capital also participated in the round.

The eight-month-old startup is working on a neo-banking platform that will focus on serving millennials in India, said Narayanan, in an interview with TechCrunch.

“When we were building Google Tez, we realized that a consumer’s financial journey extends beyond digital payments. They want insurance, lending, investment opportunities and multiple products,” he explained.

The idea, in part, is to also help users better understand how they are spending money, and guide them to make better investments and increase their savings, he said.

At this moment, it is unclear what the convergence of all of these features would look like. But Narayanan said epiFi will release an app in a few months.

Working with Narayanan on epiFi is Sumit Gwalani, who serves as the startup’s co-founder and chief product and technology officer. Gwalani previously worked as a director of product management at Google India and helped conceptualize Google Tez. In a joint interview, Gwalani said the startup currently has about two-dozen employees, some of whom have joined from Netflix, Flipkart, and PayPal.

Shailesh Lakhani, Managing Director of Sequoia Capital India, said some of the fundamental consumer banking products such as savings accounts haven’t seen true innovation in many years. “Their vision to reimagine consumer banking, by providing a modern banking product with epiFi, has the potential to bring a step function change in experience for digitally savvy consumers,” he said.

Cash dominates transactions in India today. But New Delhi’s move to invalidate most paper bills in circulation in late 2016 pushed tens of millions of Indians to explore payments app for the first time.

In recent years, scores of startups and Silicon Valley firms have stepped to help Indians pay digitally and secure a range of financial services. And all signs suggest that a significant number of people are now comfortable with mobile payments: More than 100 million users together made over 1 billion digital payments transaction in October last year — a milestone the nation has sustained in the months since.

A handful of startups are also attempting to address some of the challenges that small and medium sized businesses face. Bangalore-based Open, NiYo, and RazorPay provide a range of features such as corporate credit cards, a single dashboard to manage transactions and the ability to automate recurring payouts that traditional banks don’t currently offer. These platforms are also known as neo-bank or challenger banks or alternative banks. Interestingly, most neo-banking platforms in South Asia today serve startups and businesses — not individuals.

Powered by WPeMatico