sensor tower

Auto Added by WPeMatico

Auto Added by WPeMatico

The underpinnings of how app store analytics platforms operate were exposed this week by BuzzFeed, which uncovered the network of mobile apps used by popular analytics firm Sensor Tower to amass app data. The company had operated at least 20 apps, including VPNs and ad blockers, whose main purpose was to collect app usage data from end users in order to make estimations about app trends and revenues. Unfortunately, these sorts of data collection apps are not new — nor unique to Sensor Tower’s operation.

Sensor Tower was found to operate apps such as Luna VPN, for example, as well as Free and Unlimited VPN, Mobile Data and Adblock Focus, among others. After BuzzFeed reached out, Apple removed Adblock Focus and Google removed Mobile Data. Others are still being investigated, the report said.

Apps’ collection of usage data has been an ongoing issue across the app stores.

Facebook and Google have both operated such apps, not always transparently, and Sensor Tower’s key rival App Annie continues to do the same today.

For Facebook, its 2013 acquisition of VPN app maker Onavo for years served as a competitive advantage. The traffic through the app gave Facebook insight into which other social applications were growing in popularity — so Facebook could either clone their features or acquire them outright. When Apple finally booted Onavo from the App Store half a decade later, Facebook simply brought back the same code in a new wrapper — then called the Facebook Research app. This time, it was a bit more transparent about its data collection, as the Research app was actually paying for the data.

But Apple kicked out that app, too. So Facebook last year launched Study and Viewpoints to further its market research and data collection efforts. These apps are still live today.

Google was also caught doing something similar by way of its Screenwise Meter app, which invited users 18 and up (or 13 if part of a family group) to download the app and participate in the panel. The app’s users allowed Google to collect their app and web usage in exchange for gift cards. But like Facebook, Google’s app used Apple’s Enterprise Certificate program to work — a violation of Apple policy that saw the app removed, again following media coverage. Screenwise Meter returned to the App Store last year and continues to track app usage, among other things, with panelists’ consent.

App Annie

App Annie, a firm that directly competes with Sensor Tower, has acquired mobile data companies and now operates its own set of apps to track app usage under those brands.

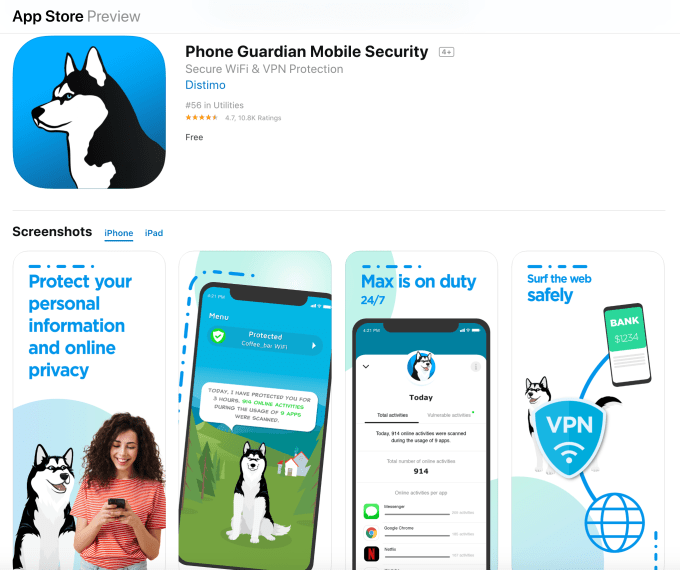

In 2014, App Annie bought Distimo, and as of 2016 has run Phone Guardian, a “secure Wi-Fi and VPN” app, under the Distimo brand.

The app discloses its relationship with App Annie in its App Store description, but remains vague about its true purpose:

“Trusted by more than 1 million users, App Annie is the leading global provider of mobile performance estimates. In short, we help app developers build better apps. We build our mobile performance estimates by learning how people use their devices. We do this with the help of this app.”

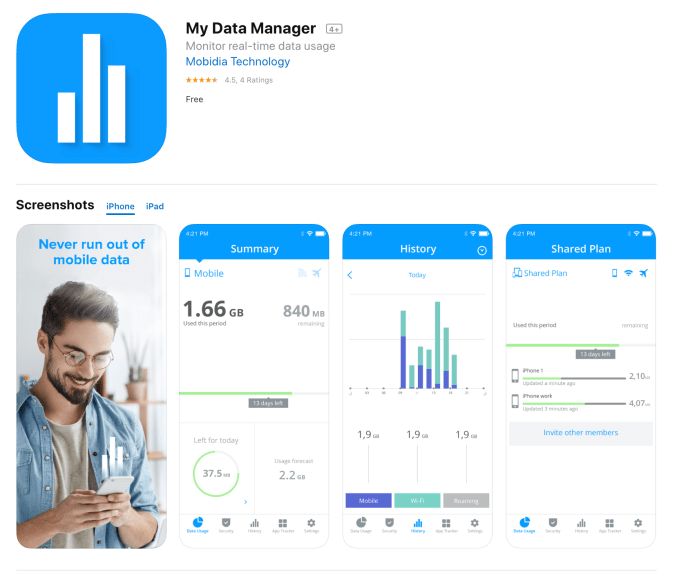

In 2015, App Annie acquired Mobidia. Since 2017, it has operated real-time data usage monitor My Data Manager under that brand, as well. The App Store description only offers the same vague disclosure, which means users aren’t likely aware of what they’re agreeing to.

Disclosure?

The problem with apps like App Annie’s and Sensor Tower’s is that they’re marketed as offering a particular function, when their real purpose for existing is entirely another.

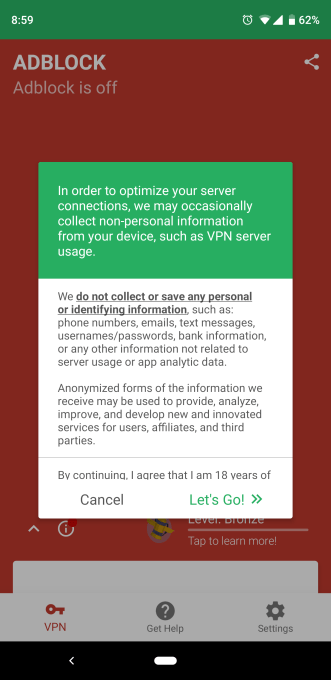

The app companies’ defense is that they do disclose and require consent during onboarding. For example, Sensor Tower apps explicitly tell users what is collected and what is not:

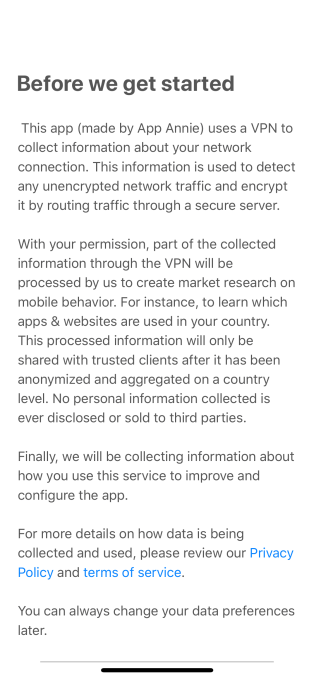

App Annie’s app offers a similar disclosure, and takes the extra step of identifying the parent company by name:

App Annie also says its apps can continue to be used even if data sharing is turned off.

Despite these opt-ins, end users may still not understand that their VPN app is actually tied to a much larger data collection operation, however anonymized that data may be. After all, App Annie and Sensor Tower aren’t household names (unless you’re an app publisher or marketer.)

Apple and Google’s responsibility

Apple and Google, let’s be fair, are also culpable here.

Of course, Google is more pro-data collection because of the nature of its own business as an advertising-powered company. (It even tracks users in the real world via the Google Maps app.)

Apple, meanwhile, markets itself as a privacy-focused company, so is deserving of increased scrutiny.

It seems unfathomable that, following the Onavo scandal, Apple wouldn’t have taken a closer look into the VPN app category to ensure its apps were compliant with its rules and transparent about the nature of their businesses. In particular, it seems Apple would have paid close attention to apps operated by companies in the app store intelligence business, like App Annie and its subsidiaries.

Apple is surely aware of how these companies acquire data — it’s common industry knowledge. Plus, App Annie’s acquisitions were publicly disclosed.

oh wait! pic.twitter.com/ktVc6E9t1f

— Will Strafach (@chronic) March 10, 2020

But Apple is conflicted. It wants to protect app usage and user data (and be known for protecting such data) by not providing any broader app store metrics of its own. However, it also knows that app publishers need such data to operate competitively on the App Store. So instead of being proactive about sweeping the App Store for data collection utilities, it remains reactive by pulling select apps when the media puts them on blast, as BuzzFeed’s report has since done. That allows Apple to maintain a veil of innocence.

But pulling user data directly covertly is only one way to operate. As Facebook and Google have since realized, it’s easier to run these sorts of operations on the App Store if the apps just say, basically, “this is a data collection app,” and/or offer payment for participation — as do many marketing research panels. This is a more transparent relationship from a consumer’s perspective too, as they know they’re agreeing to sell their data.

Meanwhile, Sensor Tower and App Annie competitor Apptopia says it tested then scrapped its own ad blocker app around six years ago, but claims it never collected data with it. It now favors getting its data directly from its app developer customers.

“We can confidently state that 100% of the proprietary data we collect is from shared App Analytics Accounts where app developers proactively and explicitly share their data with us, and give us the right to use it for modeling,” stated Apptopia co-founder and COO, Jonathan Kay. “We do not collect any data from mobile panels, third-party apps or even at the user/device level.”

This system (which is used by the others as well) isn’t necessarily a solution for end users concerned about data collection, as it further obscures the collection and sharing process. Generally, consumers don’t know which app developers are sharing this data, what data is being shared, or how it’s being utilized. App data of this nature isn’t on the user level (meaning it’s not personal data), but it’s still about reporting back to the developer things like installs, daily and monthly users, and revenue, among other things. (Fortunately, Apple allows users to disable the sharing of some diagnostic and usage data from within iOS Settings.)

Data collection done by app analytics firms is only one of many, many ways that apps leak data, however.

In fact, many apps collect personal data — including data that’s far more sensitive than anonymized app usage trends — by way of their included SDKs (software development kits). These tools allow apps to share data with numerous technology companies, including ad networks, data brokers and aggregators, both large and small. It’s not illegal, and mainstream users probably don’t know about this either.

Instead, user awareness seems to crop up through conspiracy theories, like “Facebook is listening through the microphone,” without realizing that Facebook collects so much data it doesn’t really need to do so. (Well, except when it does).

In the wake of BuzzFeed’s reporting, Sensor Tower says it’s “taking immediate steps to make Sensor Tower’s connection to our apps perfectly clear, and adding even more visibility around the data their users share with us.”

Google isn’t providing an official comment. Apple didn’t respond to requests for comment.

Sensor Tower’s full statement is below:

Our business model is predicated on high-level, macro app trends. As such, we do not collect or store any personally identifiable information (PII) about users on our servers or elsewhere. In fact, based on the way our apps are designed, such data is separated before we could possibly view or interact with it, and all we see are ad creatives being served to users. What we do store is extremely high level, aggregated advertising data that may demonstrate trends that we share with customers.

Our privacy policy follows best practices and makes our data use clear. We want to reiterate that our apps do not collect any PII, and therefore it cannot be shared with any other entity, Sensor Tower or otherwise. We’ve made this very clear in our privacy policy, which users actively opt into during the apps’ onboarding processes after being shown an unambiguous disclaimer detailing what data is shared with us. As a routine matter, and as our business evolves, we’ll always take a privacy-centric approach to new features to help ensure that any PII remains uncollected and is fully safeguarded.

Based on the feedback we’ve received, we’re taking immediate steps to make Sensor Tower’s connection to our apps perfectly clear, and adding even more visibility around the data their users share with us.

App Annie shared the below statement, referencing the root certificate installations mentioned in the BuzzFeed article. (On iOS devices, VPN certificates don’t get full root access, however):

App Annie does not use root certificates at any point in its data collection process.

App Annie discloses that when users opt into data collection (and data sharing is not mandatory to use our apps), data will be shared with App Annie for the purposes of creating market research. We only collect data after users expressly consent to this collection within our apps. We are very transparent, both on the app stores and in the apps themselves and clearly connect App Annie to our mobile apps.

Powered by WPeMatico

There are billions of gamers on the planet, and even as gaming consoles and devices grow more powerful, there’s a good deal of investor attention being paid to so-called “hyper-casual” games that likely could have shipped on decades-old hardware.

Simplicity has never been something to take for granted in game design, but as design tools have gotten easier to use, a larger group of game creators has entered the fray. Many popular games have introduced “creator modes” to whet user appetites, but this has emerged alongside the introduction of dedicated tool that enable amateur developers to become miniature studios.

This past week, I chatted with David Lau-Kee, general partner at London Venture Partners, about opportunities in the game development industry for less-experienced game creators to build titles that find an audience. His firm closed an $80 million fund last September to invest in early-stage gaming startups.

“[Hyper-casual] is a very elegant trend in the demographics of getting games into the hands of people who weren’t traditional gamers who want very low on-boarding so they can get straight into the game,” Lau-Kee says. “The challenge with that for us is that, you know, as a developer in hyper-casual games, you can have a great business, but it might not be a VC-investable opportunity.”

Powered by WPeMatico

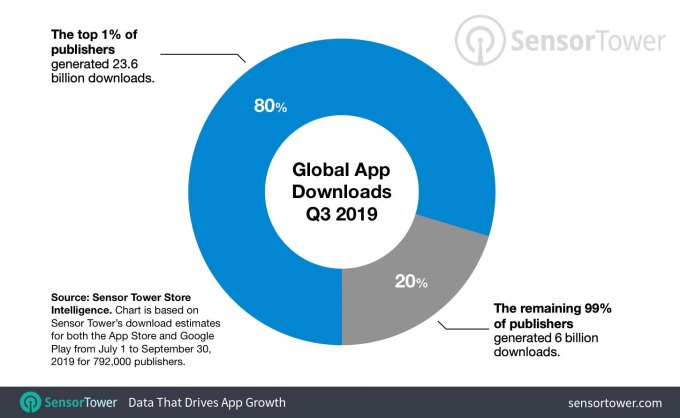

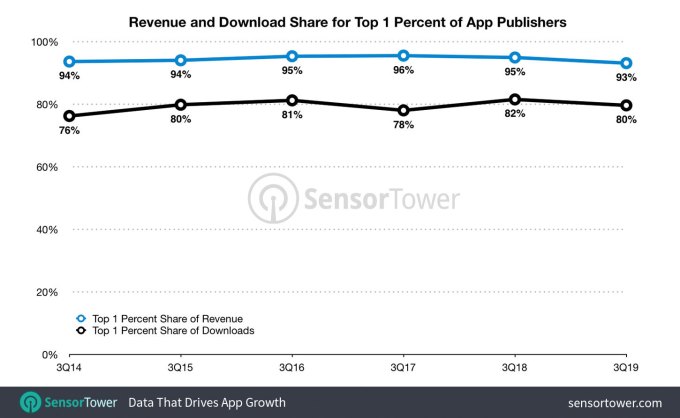

The current app store ecosystem doesn’t favor the indie developer. According to new data from Sensor Tower, the top 1% of publishers globally accounted for a whopping 80% of the total 29.6 billion app downloads in the third quarter of 2019. That means just 20%, or 6 billion, downloads are left for the rest of the publishers.

This bottom 99%, which equates to roughly 784,080 publishers, averaged approximately 7,650 downloads each during the quarter. To put that in context, that’s less than one-thousandth of a percent of the downloads Facebook generated in the quarter (682 million).

The data should not be all that surprising, given that larger, social platforms like Facebook and YouTube already serve audiences of over a billion. But it is concerning how uneven the market for new apps remains, especially considering that the number of available apps continues to expand, which makes the competition even more difficult.

The report notes there were more than 3.4 million apps available across the App Store and Google Play in 2018, up 65% from the 2.2 million apps available in 2014. But the number of apps that were able to achieve at least 1,000 installs has been declining over that same period — from 30% to 26%.

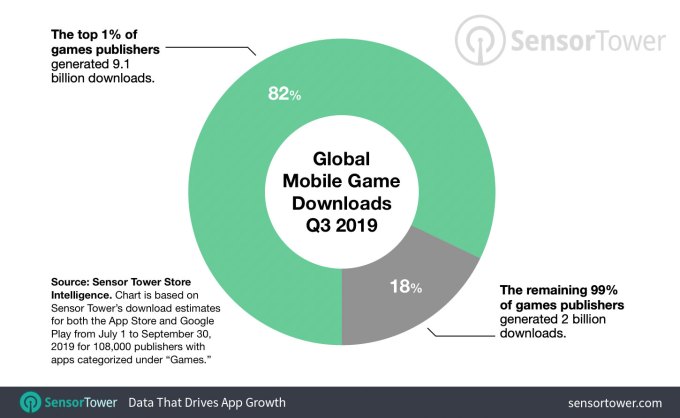

Focusing only on games, the top 1% of publishers — or 1,080 out of a total 108,000 publishers — saw 9.1 billion downloads out of the total 11.1 billion, or 82%. This averages out to more than 8.4 million installs each. The remaining 18% of downloads, or 2 billion, were shared among the remaining 106,920 publishers. That averages out to around 18,000 downloads each.

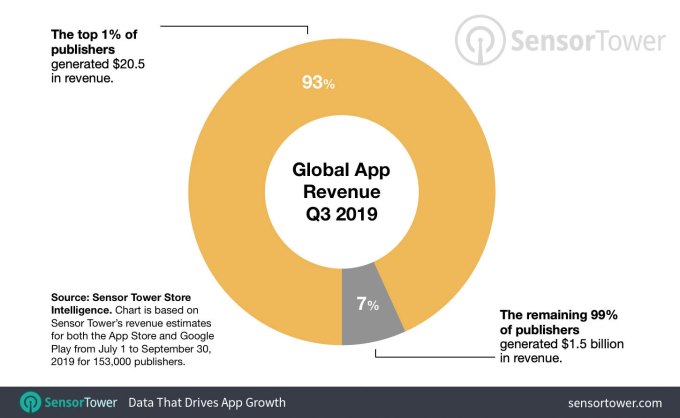

When apps were analyzed by revenue, the gap was wider. Just 1,526 publishers generated $20.5 billion out of the total $22 billion in revenue in the quarter. Meanwhile, the remaining $1.5 billion was split among 151,056 publishers, averaging out around $9,990 each.

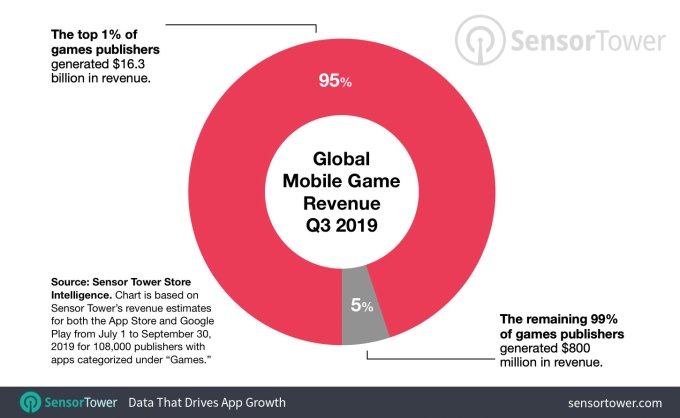

In terms of games revenue alone, the 445 publishers that make up the top 1% generated $15.5 billion in revenue, or 95% of all revenue, with the remaining $800 million split between the 44,029 publishers in the bottom 99%. This averages out to around $18,100 each.

None of these are new trends, Sensor Tower also notes. There hasn’t been much fluctuation in the top 1% share of installs or revenue for years. That means the majority of publishers will compete for a minority of new users and installs.

Image credits: Sensor Tower

Powered by WPeMatico

Global app revenue continues to climb, thanks to the growth in mobile gaming and the subscription economy. In the third quarter of 2019, consumer revenue grew 22.9% year-over-year from $17.9 billion to reach an estimated $21.9 billion across both the App Store and Google Play worldwide, according to new data from Sensor Tower.

Notably, the App Store continues to account for the large majority of this revenue, the report found, making up 65% of total spending compared with just 35% on Google Play.

App Store users spent $14.2 billion, up 22.3% from the $11.6 billion they spent in Q3 2018. Google Play generated $7.7 billion in revenue, up 24% from the $6.2 billion spent in the year-ago quarter.

Sensor Tower’s revenue estimates are a bit lower than those provided by App Annie’s recent report, which said the quarter saw $23 billion in consumer spending, not ~$22 billion.

App Annie also estimated nearly 31 billion downloads in Q3, while Sensor Tower claimed 29.6 billion.

In both cases, Google Play is still said to be the main source for downloads, with nearly three times more first-time installs than the App Store. In Q3, the total number of downloads was up 9.7% year-over-year to 29.6 billion, said Sensor Tower, with Google Play accounting for 21.6 billion of those.

Despite the overall growth, one big app market — China — saw a slight decline, Sensor Tower found. Its installs dropped 6% year-over-year to 2.2 billion in the quarter. But its revenue grew by 26.9% to $4.1 billion, up from $3.2 billion the year prior. This could be attributed to the nine-month game license freeze in China which, though now lifted, had slowed momentum.

Sensor Tower’s charts don’t include third-party app stores, so it’s not a full picture of the Chinese app market, it’s worth noting.

The top money-making (non-game) app in the quarter was again Tinder, which generated $233 million in consumer spending, up 7% over the prior quarter. Netflix was No. 2 and YouTube clocked in at No. 3, at $164 million in Q3.

App Annie has a slightly different ranking. It has Tinder and Netflix leading the top-grossing charts, but puts IQIYI ahead of YouTube. This could be because App Annie has a bigger window into the Chinese app market.

In terms of downloads, TikTok is continuing to disrupt Facebook-owned apps’ dominance over the top of the charts. In Sensor Tower’s rankings, WhatsApp was No. 1 and Messenger was No. 3, but Facebook and Instagram dropped to No. 4 and No. 5, respectively. And TikTok reached No. 2.

This isn’t the first time TikTok has passed Facebook, Sensor Tower said — it did so back in Q4 2018 and in Q1 2019, before dropping to No. 4 again last quarter. But with 177 million downloads in Q3, it’s inching its way up to the top.

App Annie, on the other hand, sees TikTok having just a bit more of climb, sticking it at No. 3 in the quarter, behind Messenger and Facebook. It also called out some Q3 break-out hits, like the return of FaceApp’s popularity (No. 9 in downloads) and the growing subscription revenue of Google One (No. 7 in non-game revenue). Sensor Tower put FaceApp at No. 6 instead, but agreed on Google One.

Mobile gaming continues to generate most of the cash, and did so again in Q3 with $16.3 billion in mobile game gross revenue — or 74% of the total in-app spending, the new report said. The App Store accounted for $9.8 billion of that figure, with Google Play users spending $6.5 billion.

Game downloads across both Google Play and the App Store increased by 17.6% in Q3 from 9.5 billion last year to 11.1 billion.

The top three games in the quarter by downloads were Fun Race 3D (123 million downloads), PUBG Mobile (94 million) and newcomer Mario Kart Tour, which hit 86 million downloads despite only launching in late September.

PUBG Mobile was the top-grossing game with $496 million in revenue, up 652% over last year. The No. 2 title, Tencent’s Honor of Kings, and No. 3 Aniplex’s Fate/Grand Order generated $377 million and $354 million, respectively.

Image credits: Sensor Tower

Correction: App Annie estimated nearly 31 billion downloads in Q3, not 23 billion as first written. We corrected this. Apologies for the error.

Powered by WPeMatico

With the App Store’s big makeover in fall 2017, Apple attempted to shift consumers’ attention away from the Top Charts and more toward editorial content. But app developers still want to make it to the No. 1 position. According to new research from app store intelligence firm Sensor Tower, it’s become easier for non-game apps over the past few years to achieve the top ranking.

Specifically, the firm found that the median number of daily downloads required for non-game applications on the U.S. iPhone App Store to reach No. 1 decreased around 34%, from 136,000 to 90,000 in 2018, then increased a little more than 4% to 94,000 this year.

At the same time, the number of non-game installs on the U.S. App Store had increased by 33% between Q1 2016 and Q1 2019.

These findings, Sensor Tower suggests, indicate that the U.S. market for the top social and messaging apps has become saturated, with downloads for top apps like Facebook and Messenger decreasing over time. In addition, no other apps have found the same level of success that Snapchat and Bitmoji did back in 2016 and 2017, the report adds.

For example, Messenger saw 5 million U.S. App Store installs in November 2016 while Bitmoji and Snapchat passed 5 million installs in August 2016 and March 2017, respectively. And no other non-game app has topped 3.5 million installs in a single month since March 2017.

Meanwhile, the decline in downloads needed to reach the No. 1 spot on Google Play was even more significant.

The median daily downloads for the top non-game app decreased by 65%, from 209,000 in 2016 to 74,000 so far in 2019.

Similarly, the store saw a decrease in installs among top apps, including Messenger, Facebook, Snapchat, Pandora and Instagram. Messenger, for example, saw its yearly installs fall by 68% from nearly 80 million in 2016 to 26 million in 2018.

Games

With mobile games, however, it’s a different story across both app stores.

On the Apple App Store, it has taken 174,000 downloads for a game to reach the top of the rankings on any given day in 2019 — 85% more the 94,000 installs required for non-game app to reach the top of the charts.

This figure also represents an increase of 47% compared to the 118,000 median daily downloads required to top the charts back in 2016, Sensor Tower said.

In part, this trend is due to the rise of hyper-casual gaming. So far in 2019, 28 games have reached the No. 1 position on the U.S. App Store, with hyper-casual games making up all but four of those. And of those four, only Harry Potter: Wizards Unite spent more than one day at the top of the charts. Meanwhile, hyper-casual games like aquapark.io and Colorbump 3D have spent 25 and 30 days at No. 1, respectively.

On Google Play, the median daily installs to reach the No. 1 position increased from 70,000 in 2017 to 116,000 so far in 2019, or 66% growth. Overall game downloads, however, decreased 16% from 646 million in Q1 2017 to 544 million in Q1 2019.

Similarly, 21 out of the 23 games that reached the top spot this year have been hyper-casual titles, like Words Story or Traffic Run.

Breaking the top 10

While topping the charts has gotten easier for non-game apps over the years, breaking into the top 10 has gotten more difficult. Median U.S. daily installs for the No. 10 free non-game app increased 11%, from 44,000 in 2016 to 49,000 in 2019.

On Google Play, median daily installs for non-game apps fell nearly 50%, from 55,000 median daily installs in 2016 to 31,000 in 2019.

For games, the No. 10 game’s spot on the App Store increased from 25,000 median daily installs in 2016 to 43,000 so far in 2019, and Google Play saw 26% growth, from 27,000 to 34,000 during the same period.

Categories making the Top 10

In terms of breaking into the top 10 by category, Photo & Video apps on the App Store present the most challenge. The category where YouTube, Instagram, TikTok and Snapchat reside saw a median daily amount of more than 16,000 downloads for the No. 10 app.

This was followed by Shopping (15,300 daily downloads for the No. 10 app), Social Networking (14,500), Entertainment (12,600) and Productivity (12,400).

On Google Play, Entertainment apps — like Hulu, Netflix and Bitmoji — need around 17,100 U.S. installs in a day to reach the top 10. This is followed by Shopping (10,800), Social (9,100), Music (8,200) and Finance (8,000).

Beyond the U.S.

Outside the U.S., a non-game app needs approximately 91,000 downloads to reach the top 10 on the App Store in China — higher than the 49,000 installs needed in the U.S. For games, the U.S. is the most difficult to crack the top 10, with a median of 43,000 daily downloads for the No. 10 game.

On Google Play, India required the most downloads to reach the top 10, with apps needing 256,000 downloads in a day and games needing 117,000 downloads.

Of course, the App Store’s ranking algorithms — nor Google Play’s algorithms — don’t rely on downloads alone to determine an app’s ranking. Apple takes into consideration downloads and velocity, among other undocumented factors. Google Play does something similar.

But these days, developers are more concerned with showing up highly ranked in app store searches than they are on top charts, where they’ll need to consider numerous other factors beyond downloads — like keywords, description, user engagement and even app quality, among other things.

Powered by WPeMatico

App store spending is continuing to grow, although not as quickly as in years past. According to a new report from Sensor Tower, the iOS App Store and Google Play combined brought in $39.7 billion in worldwide app revenue in the first half of 2019 — that’s up 15.4% over the $34.4 billion seen during the first half of last year. However, at that time, the $34.4 billion was a 27.8% increase from 2017’s numbers, then a combined $26.9 billion across both stores.

Apple’s App Store continues to massively outpace Google Play on consumer spending, the report also found.

In the first half of 2019, global consumers spent $25.5 billion on the iOS App Store, up 13.2% year-over-year from the $22.6 billion spent in the first half of 2018. Last year, the growth in consumer spending was 26.8%, for comparison’s sake.

Still, Apple’s estimated $25.5 billion in the first half of 2019 is 80% higher than Google Play’s estimated gross revenue of $14.2 billion — the latter a 19.6% increase from the first half of 2018.

The major factor in the slowing growth is iOS in China, which contributed to the slowdown in total growth. However, Sensor Tower expects to see China returning to positive growth over the next 12 months, we’re told.

To a smaller extent, the downturn could be attributed to changes with one of the top-earning apps across both app stores: Netflix.

Last year, Netflix dropped in-app subscription sign-ups for Android users. Then, at the end of December 2018, it did so for iOS users, too. That doesn’t immediately drop its revenue to zero, of course — it will continue to generate revenue from existing subscribers. But the number will decline, especially as Netflix expands globally without an in-app purchase option, and as lapsed subscribers return to renew online with Netflix directly.

In the first half of 2019, Netflix was the second highest earning non-game app with consumer spending of $339 million, Sensor Tower estimates, down from $459 million in the first half of 2018. (We should point out the firm bases its estimates on a 70/30 split between Netflix and Apple’s App Store that drops to 85/15 after the first year. To account for the mix of old and new subscribers, Sensor Tower factors in a 25% cut. But Daring Fireball’s John Gruber claims Netflix had a special relationship with Apple where it had an 85/15 cut from year one.)

In any event, Netflix’s contribution to the app stores’ revenue is on the decline.

In the first half of last year, Netflix had been the No. 1 non-game app for revenue. This year, that spot went to Tinder, which pulled in an estimated $497 million across the iOS App Store and Google Play, combined. That’s up 32% over the first half of 2018.

But Tinder’s dominance could be a trend that doesn’t last.

According to recent data from eMarketer, dating app audiences have been growing slower than expected, causing the analyst firm to revise its user estimates downward. It now expects that 25.1 million U.S. adults will use a dating app monthly this year, down from its previous forecast of 25.4 million. It also expects that only 21% of U.S. single adults will use a dating app at all in 2019, and that will only grow to 23% by 2023.

That means Tinder’s time at the top could be overrun by newcomers in later months, especially as new streaming services get off the ground (assuming they offer in-app subscriptions); if TikTok starts taking monetization seriously; or if any other large apps from China find global audiences outside of China’s third-party app stores.

For example, Tencent Video grossed $278 million globally in the first half of 2019, outside of the third-party Chinese Android app stores. That made it the third-largest non-game app by revenue. And Chinese video platform iQIYI and YouTube were the No. 4 and No. 5 top-grossing apps, respectively.

Meanwhile, iOS app installs actually declined in the first half of the year, following the first quarter that saw a decline in downloads, Q1 2019, attributed to the downturn in China.

The App Store in the first half of 2019 accounted for 14.8 billion of the total 56.7 billion app installs.

Google Play installs in the first half of the year grew 16.4% to 41.9 billion, or about 2.8 times greater than the iOS volume.

The most downloaded apps in the first half of 2019 were the same as before: WhatsApp, Messenger and Facebook led the top charts. But TikTok inched ahead of Instagram for the No. 4 spot, and it saw its installs grow around 28% to nearly 344 million worldwide.

In terms of mobile gaming specifically, spending was up 11.3% year-over-year in the first half of 2019, reaching $29.6 billion across the iOS App Store and Google Play. Thanks to the fallout of the game licensing freeze in China, App Store revenue growth for games was at $17.6 billion, or 7.8% year-over-year growth. Google Play game spending grew by 16.8% to $12 billion.

The top-grossing games, in order, were Tencent’s Honor of Kings, Fate/Grand Order, Monster Strike, Candy Crush Saga and PUBG Mobile.

Meanwhile, the most downloaded games were Color Bump 3D, Garena Free Fire and PUBG Mobile.

Image credits: Sensor Tower

Powered by WPeMatico

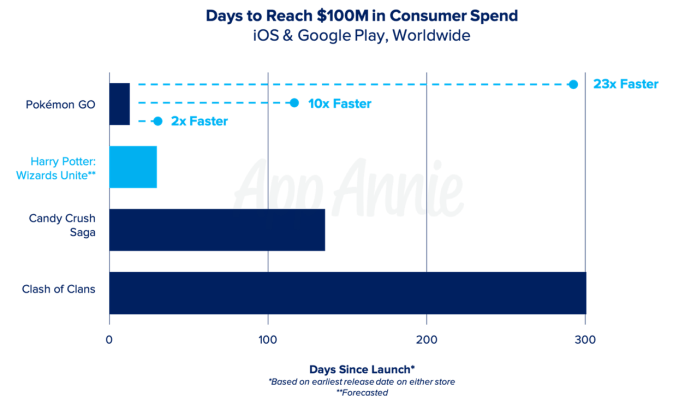

Harry Potter: Wizards Unite, the highly anticipated new mobile game from Pokémon GO makers Niantic and Warner Brothers’ games division, is off to a good start, but it’s not breaking Pokémon GO records. According to preliminary estimates from Sensor Tower, the new game has been installed some 400,000 times in its first 24 hours in its launch markets of the U.S. and U.K. — where the game arrived ahead of schedule on Thursday. Gross player spending in these markets hit around $300,000 across both iOS and Android during this time.

This is not the full picture, however.

The game was also available in Australia and New Zealand during a pre-launch beta trial of sorts, and is only now rolling out to worldwide users on a country-by-country basis. During its beta test period, Sensor Tower estimates the game grossed around $80,000.

But in the same number of days, Pokémon GO grossed $1.6 million in those two markets.

Following its U.S. launch, it took Harry Potter: Wizards Unite around 15 hours to reach the No.1 position on the iOS App Store. This ascension is also going a bit slower than Pokémon GO did when it arrived. That game was an immediate hit, debuting at No. 1 on its launch day of July 6, 2016. It was then installed 7.5 million times in the U.S. during its first 24 hours. And it didn’t reach the U.K. until seven days later.

In its first 24 hours, Pokémon GO became the No. 1 app by revenue in the U.S., as well. The new Harry Potter title is ranked No. 102 overall for iPhone revenue and No. 62 among top grossing games, Sensor Tower says. It’s also No. 48 for U.K. revenue. (It’s not yet ranked on Google Play.)

App Annie hasn’t yet put out numbers related to Harry Potter: Wizards Unite’s revenue, but the company tells us it hit No. 1 in the U.S. for downloads as of 12 AM on June 21, 2019. And for consumer spending, App Annie says the game broke into the top 100 grossing games by hitting No. 63 as of 7:00 AM June 21 on iPhone in the U.S.

The new game’s lesser demand compared with Pokémon GO could be attributed to a number of factors. Pokémon GO was hugely anticipated, had a massive fan base ready to download and was one of the first compelling use cases of AR in gaming.

Harry Potter’s fan base is active as well, but they’ve also had other games to play before now.

For example, Jam City has a Harry Potter: Hogwarts Mystery game that’s been getting a huge boost since yesterday’s news of the new Niantic title. That points to a case of mistaken identity or perhaps clever App Store SEO… or both.

It’s also worth noting the App Store itself has changed in the years since Pokémon GO’s launch.

In September 2017, Apple introduced its brand-new App Store that took the emphasis off its Top Charts as a means of discovery, and instead features apps in editorial “stories” on its Today tab. Within the dedicated apps and games section, the revamped App Store points users to editorial collections, with Top Charts only found upon scrolling down the page quite a bit.

We’ve heard from some developers that these changes reduced their downloads, as getting into the Top Charts doesn’t drive numbers like it used to. They said getting into the Today tab’s feature editorial doesn’t send as many installs, either. But this is all anecdotal — and of course, Apple doesn’t talk about numbers like this. Further investigation is needed.

In any event, the two app store intelligence firms — App Annie and Sensor Tower — both predict big numbers for the new Harry Potter title over time.

Sensor Tower estimates the game will pull in $400 million to $500 million in revenue in its first year. However, the firm notes that Harry Potter isn’t as popular in Asia — a market that delivers Pokémon GO over 40% of its revenue.

App Annie, meanwhile, predicts the game will hit $100 million in consumer spend in its first 30 days. (Pokémon GO hit this milestone in two weeks.)

“Pokémon GO shattered mobile gaming records, clearing $100 million in its first two weeks and becoming the fastest game to reach $1 billion in consumer spend,” noted App Annie. “While we don’t expect it to surpass Pokémon GO’s launch, Harry Potter: Wizards Unite is set to clear $100 million in its first 30 days — which is no small feat.”

Powered by WPeMatico

Every company’s online acquisition strategy is out in the open. If you know where to look.

This post shows you exactly where to look, and how to reverse engineer their growth tactics.

Why is this important? Competitive analysis de-risks your own growth experiments: You find the best growth ideas to adopt and the worst ones to avoid.

First, a warning: Your goal is not to repurpose another company’s hard work. That makes you a thief. Your goal is to identify other companies who face the same growth challenges as you, then to study their approaches for solutions to draw from.

As I walk through uncovering a competitor’s tactics, keep in mind which competitors are worth looking at: For instance, you should rarely over-analyze early-stage companies. They’re unlikely to be methodical at growth.

Meaning, if you blindly copy their site and their ads, it’s possible you’ll be copying tactics that are not actually responsible for their growth. Their success may instead be from network effects or other hidden factors.

Instead, it’s safest to get inspiration from companies who’ve sustained high growth rates for a long time, and who face the same growth challenges as you. They’re likely to have sophisticated growth operations worth studying deeply. Examples include:

If these aren’t your direct competitors, don’t worry. You don’t need to audit a direct competitor’s tactics to get incredibly valuable insights.

You’ll gain useful insights from auditing the user acquisition funnel of any company who has a similar audience and business model.

Examples of audiences:

Audiences matter because their behaviors and needs differ wildly. Each requires its own growth strategy. You want to audit a company whose audiences is similar to yours.

You also want to ensure the company shares your business model. Examples include:

Each model may necessitate different ads, landing pages, automated emails, and sales collateral.

Never implement another company’s tactics blindly.

There’s an effective process for growth analysis, and it looks like this:

Here’s a brief example before we dive into tactics.

Let’s pretend we’re a SaaS company offering consumer banking tools, and that we’re struggling to get users to onboard our app. Our hypothesis is that visitors are bouncing because they don’t trust us with their sensitive information.

Our first step is to define both our audience and our business model:

Our next step is to look for companies who share those two aspects. (We can find them on Crunchbase.)

Once we have a few in hand, we look for how they handle customers’ sensitive information throughout their funnel. Specifically, we audit their:

It’s time to learn how we audit all that. I’ll share how our marketer training program teaches marketers to do this on the job.

Powered by WPeMatico

In a move clearly driven by economic interests and an urgency to meet stringent regulations, the world’s largest games publisher Tencent pulled its mobile version of PlayerUnknown’s Battlegrounds on Wednesday and launched a new title called Game for Peace (the literal translation of its Chinese name 和平精英 is ‘peace elites’) on the same day.

As of this writing, Game for Peace is the most downloaded free game and top-grossing game in Apple’s China App Store, according to data from Sensor Tower data. That’s early evidence that the new title is on course to stimulate Tencent’s softening gaming revenues following a prolonged licensing freeze in China. Indeed, analysts at China Renaissance estimated that Game for Peace could generate up to $1.48 billion in annual revenue for Tencent.

Tencent licensed PUBG from South Korea’s Krafton, previously known as Bluehole, in 2017 and subsequently released a test version of the game for China’s mobile users.

Game for Peace is available only to users above the age of 16, a decision that came amid society’s growing concerns over video games’ impact on children’s mental and physical health. Tencent has recently pledged to do more ‘good’ with its technology, and the new game release appears to be a practice of that.

Tencent told Reuters the two titles are from “very different genres.” Well, many signs attest to the fact that Game for Peace is intended as a substitute for PUBG Mobile, which never received the green light from Beijing to monetize because it’s deemed too gory. Game for Peace received the license to sell in-game items on April 9.

For one, PUBG users were directed to download Game for Peace in a notice announcing its closure. People’s gaming history and achievement were transferred to the new game, and players and industry analysts have pointed out the striking resemblance between the two.

“It’s basically the same game with some tweaks,” said a Guangzhou-based PUBG player who has been playing the title since its launching, adding that the adjustment to tone down violence “doesn’t really harm the gamer experience.”

“Just ignore those details,” suggested the user.

For instance, characters who are shot don’t bleed in Game for Peace. A muzzle flash replaces gore as bloody scenes no longer pass the muster. And when people are dying, they kneel, surrender their loot box, and wave goodbye. Very civil. Very friendly.

“It’s what we call changing skin [for a game],” a Shenzhen-based mobile game studio founder said to TechCrunch. “The gameplay stays largely intact.”

Other PUBG users are less sanguine about the transition. “I don’t think this is the correct decision from the regulators. Getting oversensitive in the approval process will prevent Chinese games from growing big and strong,” wrote one contributor with more than 135 thousand followers on Zhihu, the Chinese equivalent of Quora.

But such compromise is increasingly inevitable as Chinese authorities reinforce rules around what people can consume online, not just in games but also through news readers, video platforms, and even music streaming services. Content creators must be able to decipher regulators’ directives, some of which are straightforward as “the name of the game should not contain words other than simplified Chinese.” Others requirements are more obscure, like “no violation of core socialist’s values,” a set of 12 moral principles — including prosperity, democracy, civility, and harmony — that are propagated by the Chinese Communist Party in recent years.

Powered by WPeMatico

China’s new rules on video games, introduced last month, are having an effect on the country’s gamers. Today, Tencent replaced hugely popular battle royale shooter game PUBG with a more government-friendly alternative that seems primed to pull in significant revenue.

The company introduced “Game for Peace” in a Weibo post at the same time as PUBG — which stands for Player Unknown Battlegrounds — was delisted from China. The title had been in wide testing but without revenue, and now it seems Tencent gave up on securing a license to monetize the title.

In its place, Game for Peace is very much the type of game that will pass the demands of China’s game censorship body. Last month, the country’s State Administration of Press and Publication released a series of demands for new titles, including bans on corpses and blood, references of imperial history and gambling. The new Tencent title bears a striking resemblance to PUBG, but there are no dead bodies, while it plays up to a nationalist theme with a focus on China’s air force — or, per the Weibo message, “the blue sky warriors that guard our country’s airspace” — and their battle against terrorists.

Game for Peace was developed by Krafton, the Korea-based publisher formerly known as BlueHole which made PUBG. Beyond visual similarities, Reuters reported that the games are twinned since some player found that their progress and achievements on PUBG had transferred over to the new game.

Tencent representatives declined to comment on the new game or the end of PUBG’s “beta testing” period in China when contacted by TechCrunch. But a company rep apparently told Reuters that “they are very different genres of games.”

Tencent’s new “Game for Peace” title is almost exactly the same as its popular PUBG game, which it is replacing [Image via Weibo]

Fortnite may have grabbed the attention for its explosive growth — we previously reported that the game helped publisher Epic Games bank a profit of $3 billion last year — but PUBG has more quietly become a fixture among mobile gamers, particularly in Asia.

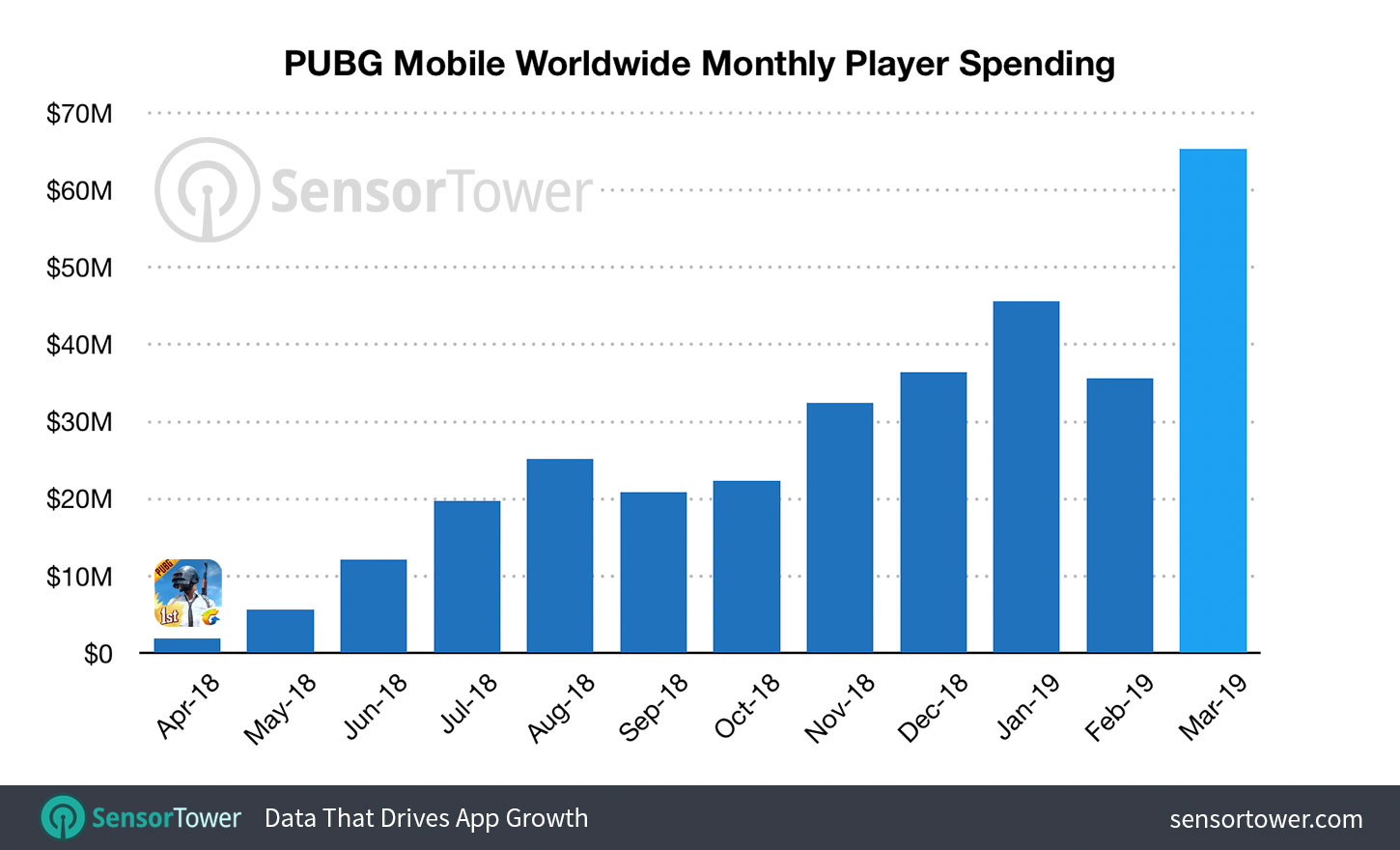

At the end of last year, Krafton told The Verge that it was past 200 million registered gamers, with 30 million players each day. According to app analytics company Sensor Tower, PUBG grossed more than $65 million from mobile players in March thanks to 83 percent growth, which saw it even beat Fortnite. There is also a desktop version.

PUBG made more money than Fortnite on mobile in March 2019, according to data from Sensor Tower

That is really the point of Tencent’s switcheroo: to make money.

The company suffered at the hands of China’s gaming license freeze last year, and a regulatory-compliant title like Game for Peace has a good shot at getting the green light for monetization — through the sale of virtual items and seasonal memberships.

Indeed, analysts at China Renaissance believe the new title could rake in as much as $1.5 billion in annual revenue, according to the Reuters report. That’s a lot to get excited about and resuscitating gaming will be an important part of Tencent’s strategy this year — which has already seen it restructure its business to focus emerging units like cloud computing, and pledge to use its technology to “do good.”

Powered by WPeMatico