seedinvest

Auto Added by WPeMatico

Auto Added by WPeMatico

In the wake of Coinbase’s direct listing earlier this year, other crypto companies may be looking to go public sooner than later. That appears to be the case with Circle, a Boston-based technology company that provides API-delivered financial services and a stablecoin.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Circle will not direct list or pursue a traditional IPO. Instead, the company is combining with Concord Acquisition Corp., a SPAC, or blank-check company. The transaction values the crypto shop at an enterprise value of $4.5 billion and an equity value of around $5.4 billion.

The offering marks an interesting moment for the crypto market. Unlike Coinbase, which operates a trading platform and generates fees in a manner that is widely understood by public-market investors, Circle’s offerings are a bit more exotic.

The offering marks an interesting moment for the crypto market. Unlike Coinbase, which operates a trading platform and generates fees in a manner that is widely understood by public-market investors, Circle’s offerings are a bit more exotic.

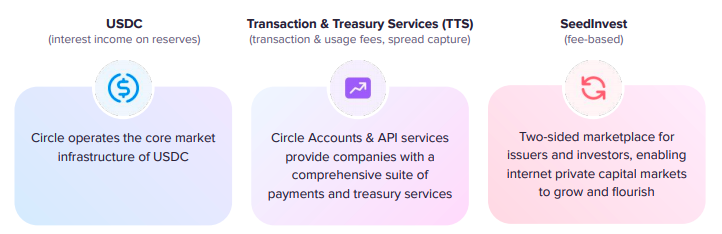

Circle’s SPAC presentation details a company whose core business deals with a stablecoin — a crypto asset pegged to an external currency, in this case, the U.S. dollar — and a set of APIs that provide crypto-powered financial services to other companies. It also owns SeedInvest, an equity crowdfunding platform, though Circle appears to generate the bulk of its anticipated revenues from its other businesses.

For more on the deal itself, TechCrunch’s Romain Dillet has a piece focused on the transaction. Here, we’ll dig into the company’s investor presentation, talk about its business model, and riff on its historical and anticipated results and valuation multiples.

In short, we get to have a little fun. Let’s begin.

As noted above, Circle has three main business operations. Here’s how it describes them in its deck:

Image Credits: Circle investor presentation

Let’s consider each one, starting with USDC.

Stablecoins have become popular in recent quarters. Because they are pegged to an external currency, they operate as an interesting form of cash inside the crypto world. If you want to have on-chain buying power, but don’t want to have all your value stored in more volatile, and tax-inducing, cryptos that you might have to sell to buy anything else, stablecoins can operate as a more stable sort of liquid currency. They can combine the stability of the U.S. dollar, say, and the crypto world’s interesting financial web.

Powered by WPeMatico

The flow of venture capital in 2020 has been surprisingly strong given the year’s general uncertainty, but while investors have showered plenty of dough on growth-stage companies, seed-stage startups are down 32% last quarter compared to the year before.

There have been plenty of recent conversations about alternative funding routes for founders, and one of those oft-overlooked paths has been equity crowdfunding. While crowdfunding platforms like Kickstarter push consumers to back unrealized projects in exchange for products or other services, equity crowdfunding allows consumers to actually invest cash and receive a piece of the company. It’s not a conventional path, but it can be a viable option for companies that have a close relationship with an engaged customer base.

The Security and Exchange Commission’s Regulation Crowdfunding guidelines were adopted under Title III of the JOBS Act back in 2016, but because many entrepreneurs were unfamiliar with how to participate, many of the startups that have taken advantage of it haven’t been the highest quality. The tide could be turning: This week, the SEC updated some of its guidance on crowdfunding, eliminating some ambiguities and increasing the amount of capital companies can raise from both accredited and nonaccredited investors. Additionally, companies can now raise $5 million per year using equity crowdfunding, compared to the previous limit of $1.07 million.

But life has gotten easier in other ways as well for founders pursuing this fundraising type and the platforms that seek to simplify it.

Wefunder is one of a handful of equity crowdfunding platforms that have popped up in the last few years. Before a company can raise on its platform, Wefunder vets them before allowing them to tap into their network of amateur investors who can invest as little as $100 with the median investment sitting at $250. Last month, 40 companies launched on Wefunder and collectively raised $12 million, according to Wefunder CEO Nicholas Tommarello.

Powered by WPeMatico

We profiled HyperSciences in February, when the team had just successfully completed a launch milestone for a small business grant with NASA. The last time we checked in, the hypersonic drilling company had raised about $5 million as part of an untraditional Reg A offering. By the end of March, HyperSciences rounded out its first major round with $9.6 million from 3,552 individual investors on SeedInvest in the equity crowdfunding platform’s second largest raise to date.

The heart of HyperSciences’ work is its hypersonic propulsion system that can fire a projectile at five times the speed of sound. At its most simplistic, HyperSciences’ hypersonic engine can fire upward to power suborbital space launches (HyperDrone) and point downward to penetrate deep pockets of geothermal energy, for example (HyperDrill).

Rather than going the normal venture capital route, HyperSciences decided to raise from regular people who believed in its vision. The way the company sees it, traditional VC would have likely forced HyperSciences to narrow its mission.

“Reg A lets everyone who cares about our planned hypersonic future vote with their checkbook,” HyperSciences founder and CEO Mark Russell told TechCrunch. “I think that’s important.” Russell comes from a family-run mining business and is no stranger to the challenges of a public company.

“I’ve learned a lot from running ops in the back offices,” Russell said. “Based on our public company experiences, we do like that the SEC Reg A process has a clear path to taking your company to the public markets as the next step in the process.”

With infusions of $125,000 from NASA’s Small Business Innovation Research grant and $1 million from Shell’s Global’s GameChanger program, HyperSciences is happy to bounce between research grants with a boost from the Reg A’s special form of “mini-IPO” in order to maintain its autonomy for the time being.

Russell explained that the Reg A’s intensive SEC process requires a fair level of maturity from a company — and enough capital to jump through all the hoops. “You’re not typically a seller of t-shirts in Reg A crowd financing,” Russell said.

HyperSciences’ next milestone will come in May when the company will demo its drilling tech in a field test for Shell. The company plans to leverage its new funding for additional future field testing, pushing its existing business plan forward and moving toward sustainability.

“Our investors are more like smart ‘crowd VCs.’ They’re generally are pretty savvy and see that we went through a stringent process to get here,” Russell said. “We’ve provided them with enough information to make a great decision.”

Powered by WPeMatico

The dream of a startup founder can often be summarized by the following well-intentioned, and mostly delusional, quote: “We’ll raise a few rounds and in a few years we’ll IPO on Nasdaq.”

But a more likely scenario looks something like this:

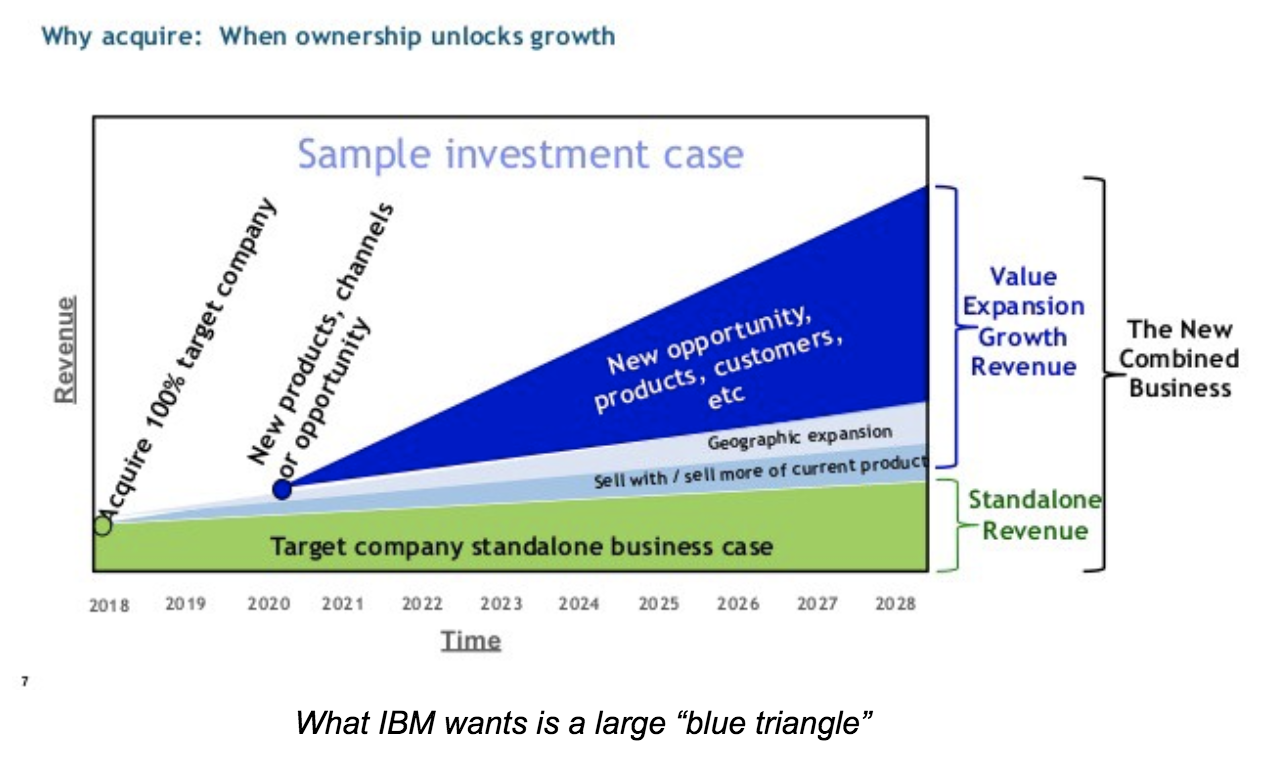

You invest a few years of hard work to build something of value. One day you receive an acquisition offer out of the blue. You’re elated. And you’re not prepared. You drop everything to focus on this opportunity. Exclusive due diligence starts. Your company is a mess (IP, contracts, burn). Days become weeks; weeks become months. You’ve neglected business and fundraising. You’re running out of money. M&A is now your one and only option. The buyer says they found a bunch of cockroaches in the walls and drops the price. Now what?

Sound unlikely?

This is still a favorable situation: You had an offer! Think about how much time you invested in your various funding rounds. The hundreds of names and Google spreadsheet or Streak-powered quasi-CRM process.

Have you spent even a fraction of that on understanding exit paths? If you’d rather not live the situation described above, read along.

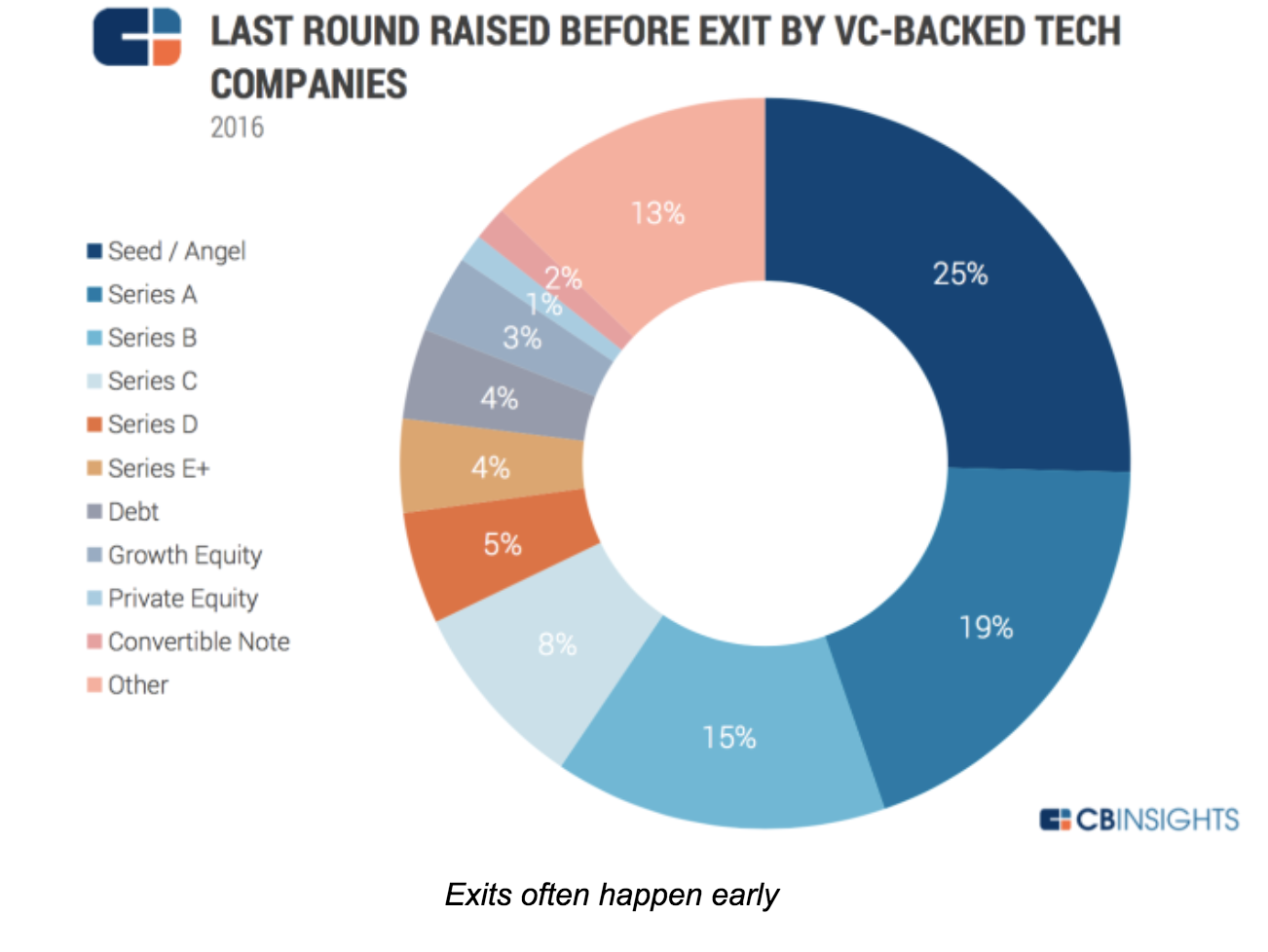

Investors live by exits, but many founders keep dreaming of unicornization and avoid the “E-word” until it’s too late. Yet, in 2016, 97 percent of exits were M&As. And most happened before Series B.

Exits matter because that’s when you, your team and your investors get paid. Oddly enough, and to use a chess metaphor, we hear a lot about the “opening game” (lean startup) and the “mid-game” (growth), but very little about this “end game.”

As a result, founders miss opportunities or leave money on the table. This is a shame. Our fund has more than 700 companies in portfolio. We want the best possible exit for each of them. And fortune favors the prepared! Now, how to get 700 exits (and counting)?

To explore the topic, we organized a series of Master Classes tapping corporate buyers, bankers, investors, lawyers and startup CEOs with M&A or IPO experience in San Francisco. It was a group that included the founders of Guitar Hero — bought by Activision; JUMP Bikes — a SOSV portfolio company bought by Uber, Ubiquisys — bought by Cisco and Withings — bought by Nokia. Each one for hundreds of millions.

Their observations can be summarized below.

“Founders must be aware of what contributes to an exit. This means understanding partnerships and how they are formed in the business space the entrepreneur is working in,” said one Master Class participant.

As founders, you build your product, your company and… optionality. You need to understand the options open to your company, and take steps to enable them.

The most likely one is an acquisition, but there are others like IPO (including small cap), RTO, SBO, LBO, Equity Crowdfunding and even ICO.

“Exit is not a goal per se, but as a CEO it is something you should think about as early in your cycle as possible, while being business-focused,” said the London-based investor Frederic Rombaut, of Seraphim Capital.

Indeed, most participants said that exits should always be on the chief executive’s agenda, no matter how early in the process. “Exits should be on the CEO agenda. Not front and center, but on the agenda. M&A is a by-product of a great business and targeted BD. IPOs are always an option once you’ve built significant cashflow forecasting.”

It’s important to ask questions like: How many “strategic engagements” with potential buyers have you had this month? Is your message and value clear in their eyes? Have you considered an acquisition track in parallel to a fundraise?

It doesn’t stop there:

One thing is sure: The time to exit is not when you’re running out of money.

Unicorn or not, the most likely exit is an acquisition.

As George Patterson, managing director at HSBC in New York said, “Good tech companies are bought, not sold. The question is thus: how to get bought?”

Patterson says it’s important to understand how mergers and acquisitions actually work; how to prepare a startup for an exit; and how to develop a “feel” for the market you’re exiting through and into.

Hearing from corp dev veterans from Cisco, Logitech, Dassault and IBM, a few key ideas emerged:

Motivations vary

It could be from least to most expensive, or as a mix, as listed by Mark Suster, managing partner at Upfront Ventures:

How corporates find you

Corporates find deals via the development of partnerships, investment (CVC), their business units, corp dev research, media and investor connections.

Asked about the best approach, Todd Neville, manager of Corporate Business Development and Strategy at IBM (who gave the most detailed description of the corp dev process), said, “Do something cool to one of the IBM customers. If they rave about even a POC, we’re interested.”

In other words, business development is corporate development.

Get the house in order

Buyers typically want to know three things:

For IP, they will check your contracts (staff and contractors), and run some automated code analysis for proprietary code and open source use. They will evaluate potential IP infringement. No point buying you if you end up costing more in lawsuits!

For your team skills: Sitting down with your engineers will tell them plenty enough without understanding the details of this or that algorithm. The last thing a corporate wants is to be accused of stealing!

Lawyers engaged early can help. The later the clean-up, the more costly and painful.

Develop a feel for your “market”

Develop relationships and create champions within corporates. It will help promote your deal when the time comes, and will let you keep your finger on the pulse of corporate strategy to time your moves.

Do you read the earning calls of Cisco or IBM (or others relevant to you)? This is where strategies are presented. Are your keywords coming up there or in their press releases?

Chris Gilbert, former CEO of Ubiquisys (sold to Cisco for more than $300 million) was very deliberate in planning his exit.

“Selling starts on day one and is a leadership-only function — work out who will be your buyer. Only the CEO can do this. Constantly articulate why a company should buy you,” Gilbert said. Bring clear messages into the acquiring company so it can be presented upwards: give them the presentation you would like them to show their boss! When the time is right, force decisions through competition. If you know they have to buy you, your starting position is strong.”

The dark art of price discovery

There are dozens of formulas (from DCF to comparables) to evaluate a deal — which also means none is “correct.” What matters is: How much would you sell for, and how much is the buyer ready to pay?

Gilbert, at Ubiquisys, described how close interactions with his banker helped drive the price up among the bidders assembled.

Just like buyers, we meet bankers and lawyers too rarely at startup events, but there is much to learn with them. They make deals happen, avoid value erosion and optimize price. They often also make introductions before you engage them, to build goodwill and earn your business.

And if you worry about fees, the right banker handsomely pays for itself by finding more bidders and playing “bad cop” for you, avoiding direct confrontation with your future employer. Do you want a slice of the watermelon or the whole grape?

When asked about what happens after an M&A or IPO, buyers said they generally hoped the founders would stay with them for many years. Often using re-vesting, earn-outs or shares of the acquiring company to incentivize them. Neville, from IBM, mentioned a security company they acquired whose founder is now the head of one of the largest IBM divisions.

In the case of IPOs, supposedly the ultimate “exit,” any block of shares sold by founders would face extreme scrutiny and might cause a price drop.

So who’s exiting during those deals? Investors (and not always).

Eventually, if the average age of a startup at exit is 8-10 years, the active duty period of founders (if not replaced in the meantime) extends even more. Better love the problem you’re solving, and your customers!

Thanks to speakers, participants and supporters of this Master Class series:

London: Frederic Rombaut (Seraphim Capital), Joe Tabberer (FirstBank), Chris Gilbert (Ubiquisys), Jonathan Keeling (Crowdcube), Fred Destin, Tony Fish (AMF Ventures, James Clark (London Stock Exchange), Denise Law (SGCIB).

Paris: Frederic Rombaut (Seraphim Capital), Manuel Gruson (Dassault Systemes), Pierre-Henri Chappaz (Rothschild Global Advisory), Christine Lambert-Goue (All Invest), Olivier Younes (EXPEN), Eric Carreel (Withings), Fabien Bardinet (Balyo), Xavier Lazarus (Elaia Partners), Pierre-Eric Leibovici(Daphni). Jean de La Rochebrochard (Kima Ventures), Jeremy Sartre (SmartAngels), Gwen Regina Tan (Entrepreneur First).

San Francisco: Natasha Ligai (Logitech), Matt Cutler (Cisco),Will Hawthorne, (CODE Advisors), Ryan Rzepecki (JUMP Bikes), Charles Huang (Guitar Hero), Jeff Thomas (Nasdaq), Shahin Farshchi (Lux Capital), Ammar Hanafi (Moment Ventures), Adam J. Epstein (Third Creek Advisors), Nathan Harding (EKSO Bionics), Kate Whitcomb, Anthony Marino and Ethan Haigh (SOSV).

New York: Todd Neville (IBM), George Patterson (HSBC), Ryan Rzepecki (JUMP Bikes), Aaron Kellner (SeedInvest), Jeremy Levine (Bessemer Venture Partners), Taylor Greene (Collaborative Fund), Adam Rothenberg (BoxGroup), Eli Curi (Fenwick & West), Ian Engstrand and Salil Gandhi (Goodwin), Warren Spar(Sparring Partners Capital), Duncan Turner, Vivian Law and Sheng Ge (SOSV).

Powered by WPeMatico

Music startup 8tracks has always had a strong sense of community. But the startup is taking this one step further by raising $30 million from its own community. Instead of asking money from venture capitalists, the company has started an equity crowdfunding campaign on SeedInvest and it’s been working well.

Music startup 8tracks has always had a strong sense of community. But the startup is taking this one step further by raising $30 million from its own community. Instead of asking money from venture capitalists, the company has started an equity crowdfunding campaign on SeedInvest and it’s been working well.

Around 30,000 community members have committed to invest $1,000 each to get a… Read More

Powered by WPeMatico