seed stage

Auto Added by WPeMatico

Auto Added by WPeMatico

I’ve fundraised a lot. Tactically, fundraising is a skill like any other. You get better the more you do it. But practicing gets you nowhere if you don’t have a strong foundation in understanding a fundraising round’s core components.

As a founder, you will understand less than investors when it comes to fundraising. For investors, negotiating with founders is their full-time job. For founders, fundraising is just a small part of building a business. Understanding the basics of venture financing can help founders raise on better terms.

We’ll cover:

As a founder, you will understand less than investors when it comes to fundraising.

Venture financing takes place in rounds. The first stage is the pre-seed or seed round, then a Series A, then a Series B, then a Series C and so on. You can continue to raise funding until the company is profitable, gets acquired or goes public.

We will focus here on seed-stage funding — your very first funding round.

Post-money SAFEs are the most common way to raise funding. These documents are used by Y Combinator, angel investors and most early-stage funds. You should raise on post-money SAFEs using standard documents created by YC. Standard documents have consistent terms that have been drafted to be fair to both investors and founders.

By using the standard post-money SAFE, your negotiation can focus on the two terms that matter:

Powered by WPeMatico

Extra Crunch Live is all about helping founders build better venture-backed businesses. Naturally, we do this by having candid conversations with founders and their investors.

On an upcoming episode of Extra Crunch Live, we’ll sit down with MaC Venture Capital founding managing partner Marlon Nichols and Wonderschool co-founder and CEO Chris Bennett. REGISTER HERE FOR FREE!

Not only will we discuss how they came together for Wonderschool’s seed round in 2017, but how that translated into what has become a total of $24 million in funding from VCs like a16z and First Round Capital.

We’ll also host the Extra Crunch Live Pitch-off, where folks in the audience can pitch their startup to Nichols and Bennett to get their live feedback.

Nichols is a former Kauffman Fellow and Investment Director at Intel Capital. His portfolio includes Gimlet Media, MongoDB, Thrive Market, PlayVS, Fair, LISNR, Mayvenn, Blavity and Wonderschool. Nichols knows more than most of us will ever learn about seed-stage fundraising, and even gave a chat at TechCrunch Early Stage in April that outlines four strategies for securing seed funding.

We’ll get even deeper on that subject with Nichols, and hear the perspective from the other side of the table with Bennett.

Wonderschool is a network of early childhood programs that combine the quality of top-notch early education with an in-home setting.

Bennett can talk extensively on edtech as a sector, and we’ll pick both his and Nichols’ mind on that fast-growing space.

Don’t forget that this episode will feature an Extra Crunch Live Pitch-off, so founders in the audience should be ready to “raise their hand” and get in the mix.

The episode goes down on Wednesday, June 16 at 3 p.m. ET/noon PT. Extra Crunch Live is accessible to anyone who wants to attend, but on-demand access to the content, including the entire library of ECL episodes, is reserved exclusively for Extra Crunch members. Join now to check out what Aileen Lee, Roelof Botha, Mark Cuban and more had to say on earlier episodes of ECL.

Powered by WPeMatico

In April 2020, when the entire world was laser-focused on the coronavirus pandemic, we realized that startupland was in unprecedented territory. How should startups navigate fundraising, operations, and better understand the market?

In a matter of a couple weeks, we spun up a little series called Extra Crunch Live, giving Extra Crunch members the chance to hear from and connect with leaders across the industry. We brought on some of the biggest names in tech and VC, including the likes of Roelof Botha, Kirsten Green, Zach Perret, Charles Hudson, Aileen Lee, Mark Cuban, Howard Lerman, Niko Bonatsos and Alexa Von Tobel — and the list could go on and on and on.

Somehow, we did 44 episodes of the show in 2020, the year of our Lord.

By any measure, it’s been a huge success. But we’re not ones to rest on our laurels here at TechCrunch. Which is why I’m thrilled to announce Extra Crunch Live 2.0.

In 2021, we’ll be tweaking the format of ECL to provide even more interactivity between founders and audience members and the speakers we host on the show. You’re going to love it.

What’s New:

We’re super excited about our ECL plans for 2021 and we hope you are, too. More on upcoming speakers soon.

Remember, Extra Crunch Live events are for EC members only, so if you haven’t joined Extra Crunch, get over here!

Powered by WPeMatico

Pear, a Palo Alto-based seed-stage fund that has made its name through early bets on Guardant Health, DoorDash, Memebox and Gusto, hosted its sixth annual demo day this week in what proved to be a scorchingly hot afternoon in Woodside, Calif. — not that invitees were put off by the heat.

Hundreds of investors showed up at a sprawling public estate and surrounding gardens to see the dozen teams that Pear spent the summer working with, each of them less than nine months old, according to Pear, and many incorporated only in recent months. (Each has also only received less than $200,000 so far from Pear, and no other institutional investment.)

While some are sure to evolve into other ideas or dissolve into other endeavors, the whole of the group gave those gathered food for thought and a first look at some very solid talent.

Following are the companies that presented:

1) Windborne: Founded by three Stanford grads and another from Harvard, this startup aims to improve the accuracy of weather data where it’s currently limited, like over oceans, by using weather balloons that could allow the team to do things like tell shipping companies which route to take to minimize fuel burn. CEO Paige Brown also says their system can fly 60 times longer than existing solutions and for the same price. The more specific claim: that in a single $350 flight, a Windborne balloon can fly for more than five days and travel a quarter of the way around the world, collecting direct measurements in places no one else can.

The team apparently bonded as engineers in the Stanford Student Space Initiative and they’ve all worked at SpaceX.

2) Guild: This one was started by two Stanford grads and helps companies make branded credit cards. Why would they bother? Because, the startup claims, branded credit cards are a lot more lucrative — increasing spending by 20%, cutting churn by roughly half and generating $50 per year of profit per customer. Co-founder Michael Spelfogel says he knows of which he speaks, having tried, unsuccessfully, to launch a branded credit card while at Lyft.

He also says the idea is to partner with sports teams first.

3) Polimorphic: Started by two computer scientists out of MIT, this startup is building a “civic media platform” meant to help politicians communicate with constituents. The platform basically invites visitors to express their views directly to their political and government leaders, while it also gives campaigns, civic groups and governments a way to engage with those individuals (though the latter has to pay to do this). It’s a meaningful market, they argue, saying that campaign spending has been growing by 50% in between major election cycles, with $9 billion spent in 2016 alone.

Of course, because this was a demo day, the founders also talked about their traction, saying they already have three letters of intent, and volunteering that they’re in early talks with three presidential campaigns.

4) Gradio: Launched by graduates of Stanford, Georgia Institute of Technology, NYU and MIT, Gradio says it speeds up the process of collecting and labeling data for use with AI and machine learning. The “Gradio data engine” corrects mislabeled data, identifies and removes “low value” data and highlights the highest-value data. It’s a smart pitch, considering that acquiring and labeling data right now requires tons of human labor and often requires pricey domain expertise and that, even so, something like one if five data points is mislabeled at a typical AI company.

As for who will use the technology, the founders say they’re targeting companies in the natural language processing space first.

5) Sympto Health: Launched by two founders from UC San Diego (one who graduated, one who dropped out to build Sympto), this startup is trying to tackle a universal problem, which is that patients very often forget clinical instructions, and when that happens, they sometimes wind up being readmitted to the hospital.

Sympto ties into a care facility’s existing systems/workflows and sends “patient engagement” messages — things like surgery checklists, pre-appointment questionnaires, etc. — to minimize missed information and unnecessary readmissions. It says its patient-as-an-engagement service has already landed the company two enterprise contracts worth $300,000, too.

6) Smarty: This startup was founded by a single person with multiple degrees (HBS, MIT) who previously worked as a software engineer at Yammer.

What she has built: an automation tool that’s focused on business tasks like scheduling meetings, making introductions and finding flights for out of town meetings. The tool is being made available first to users of G Suite and Office 365 (which have 200 million paying users, combined); they’ll be asked to pay Smarty $20 a month for its workflow automation tool. Eventually, though, it aims to be its own client.

7) Impct: Started by two MBAs from National Chengchi University and another from Stanford, Impct is making what it called snacks for good. It’s not that they’re more healthful than other options; instead, the idea is for companies to buy these white-label snacks for their offices, then re-invest a percentage of their sales into social responsibility programs chosen by employees. The thinking is that employees want their kombucha; why not spend on snack bars and drinks that give back?

8) Learn to Win: Started by two Stanford MBAs who say traditional learning management systems fall short of the needs of high-performance teams, Learn to Win is a “micro learning” training program that’s right now being used by 100 sports organizations; it also has a signed contract with the Air Combat Command to train fighter pilots.

What the program ostensibly offers: content that’s presented in a visual and easy-to-use content authoring engine, the ability to deploy mobile active learning content to users, and and the ability to quickly evaluate results and iterate.

Next on the startup’s to-do list: enticing other entities with training challenges, including in the commercial airline industry, at oil and gas companies and within police and fire departments.

9) Fanimal: Founders with degrees from Stanford, Columbia University and UC Berkeley (and who’ve worked at Boston Consulting Group, Gunderson Dettmer and Hackbright Academy) decided to come together to tackle two annoying problems associated with buying tickets for live events: high fees, and that feeling when you buy tickets for a group of people . . . then need to chase them down for reimbusement.

With Fanimal, everyone in a social group pays individually and receives their own tickets, and there are no hidden fees. Instead, Fanimal makes money by adding a “small markup” to tickets. Since launching a few weeks ago, they’ve sold more than $31,000 in tickets.

10) Xilis: A Stanford PhD and a PhD from UNC Chapel Hill (both now Duke University professors focused on oncology and precision health) came together for this company out of their acute awareness that when someone is diagnosed with cancer, finding the right treatment frequently takes months and often comes with countless side effects. To speed along the process, their company, Xilis, uses “micro-organoids” to make thousands of 3D replicas of a patient’s tumor in about six days, which the company says can be used for testing for drug compatibility faster.

They say it works, too. At least, the co-founders, Xiling Shen and David Hsu, claim they’ve tested the technology with 12 patients, with a 100% success rate in predicting how a tumor will respond to medication.

11) Equipped: Founded by two Stanford grads who’ve worked variously for the NBA, Tesla and Amazon, Equipped has an interesting proposal. What if instead of lugging an oversized umbrella to the beach or bringing a soccer ball to the park, you could get these things where they make sense, in on-demand equipment lockers at the beach, or outside a park, where you could rent what you need, then return it?

Nike seems to like the idea. CEO Dan Mandelman says the sports retail giant is paying them $200,000 for six lockers in LA, with the cities of Burlingame, San Ramon and Redwood City currently implementing pilot programs.

12) Maker: Two Stanford MBAs with marketing and management consultant experience have created a marketplace for small-batch wines.

Maker finds small/independent wineries, cans their product under the Maker label, then delivers to the end customer.

By the way, you can get a flavor for Pear’s demo day here if you’re curious.

Powered by WPeMatico

Round sizes are up. Valuations are up. There are more investors than ever hunting unicorns around the globe. But for all the talk about the abundance of venture funding, there is a lot less being said about what it all means for entrepreneurs raising their early funding rounds.

Take for instance Seed-stage dilution. Since 2014, enterprise-focused tech companies have given up significantly more ownership during Seed rounds. What gives?

Scale is an investor in early-in-revenue enterprise technology companies, so we wanted to better understand how this trend in Seed-stage dilution impacts companies raising Series A and Series B rounds.

Using our Scale Studio dataset of performance metrics on nearly 800 cloud and SaaS companies as well as Pitchbook fundraising records covering B2B software startups, we started connecting the dots between trends in valuations, round sizes, and winner-take-all markets.

Bottom line for founders: Don’t let all the capital in venture mislead you. There’s an important connection between higher Seed-stage dilution and increased investor expectations during Series A and Series B rounds.

These days, successful startups are growing up faster than ever.

Powered by WPeMatico

We’ve decided to step back from the breaking news for a minute to conduct a review of seed and early-stage funding trends over the last decade for U.S.-based companies.

I’m fairly certain we can all agree that the environment for startups has changed dramatically in the past 10 years, specifically in two major ways:

What we’ve also seen are recent concerns raised about the decline in seed stage funding by Mark Suster, a partner at UpFront Ventures, as there has not been commensurate growth in early stage funding (Series A and B), to meet this growth in seed-financed companies. This is often expressed as the Series A crunch.

So with venture funding at an all-time high, along with increased growth in supergiant rounds, now seems like an appropriate time to conduct this kind of review.

First, let’s set the stage for our analysis and explain where our data comes from with a few quick facts:

Now, let’s take a look at the trends.

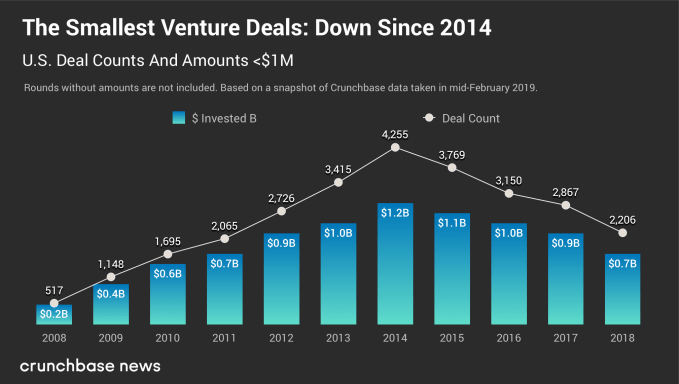

Since 2014 we have seen mostly double-digit declines in less than $1 million rounds each year – a strong pivot from 2008-2014 when we saw double-digit growth.

In 2018 seed funding counts and amounts below $1 million were down from 2015 at 41 and 35 percent respectively. Given that data at this stage can be added long after the round took place, we assess there could be a 20 percentage-point relative increase in 2018 compared to 2017.

If we factor this in, 2018 seed funding counts and amounts below $1 million are down from 2015 at 30 and 23 percent respectively. In other words, seed below $1 million are closer to 2012 and 2017 levels.

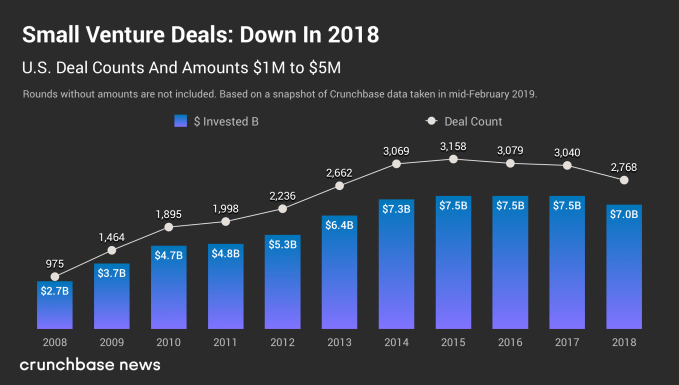

Round from $1 million to $5 million also experienced growth from 2008 through 2015, more than threefold for counts and close to threefold for amounts. Upward growth stalled from 2015. However, we do not see a substantial downward trend in the last three years. Dollars invested are stable at $7.5 billion from 2015 through 2017. Counts and amounts are down in 2018 from the 2015 height by 12 percent for deal count and 6 percent for amounts.

At Crunchbase we are always cautious about reporting downward trends for the most recent year or quarter, as data does flow in after the close of the most recent time period. If the trend is over a greater time period, that is a stronger signal for change in the market. Based on data continuing to be added after the end of a year for the previous year, we assess around 10 percentage point increase relative to 2017. This would make 2018 roughly equivalent to 2017 on rounds and slightly up on amounts.

Why is seed flattening? Seed investors report putting more dollars into fewer deals. Or as they raise more substantial subsequent funds, they are putting more dollars into the same number of transactions. Seed funds need to get enough equity for a meaningful stake, should a startup survive to raise subsequent rounds. Seed funds are investing in fewer startups for more equity.

UpFront Ventures’ Suster (referenced earlier) also talks about larger venture firms becoming less active in seed, as investing at the seed stage can limit their ability down the road to invest in competitive startups who emerge as growing contenders in a specific sector. The growth of more substantial funds in venture allows firms to see deals mature before investing, perhaps paying more to get the equity they want, and allowing startups not growing as quickly to fail or get acquired.

As Fred Wilson from Union Square Ventures notes, “In the first five years of this decade, we saw the seed portion of the market explode. In the last five years of this decade we saw the growth portion of the market explode. But over those last ten years, the middle part, the traditional venture capital market, has not changed much.”

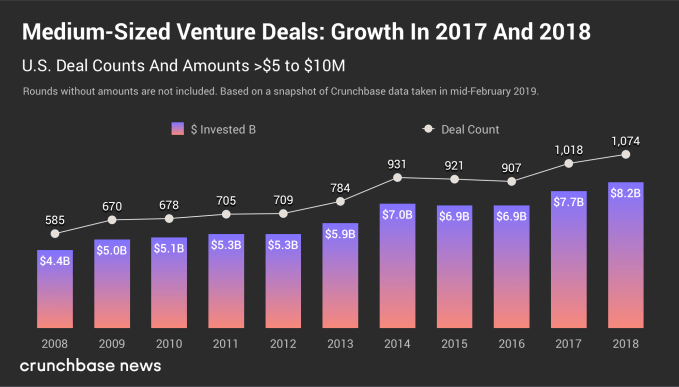

For the middle, Series A and B rounds (which used to be the first institutional money in), the market for $5 million to $10 million rounds has almost doubled, but it has taken from 2008 to 2018. In that same period, growth has been slower than round below $5 million. Growth has continued past 2015. Since 2015, rounds are down slightly for one year, and then continue to grow in 2017 and 2018. Counts are up from 2015 by 17 percent and dollars by 18 percent.

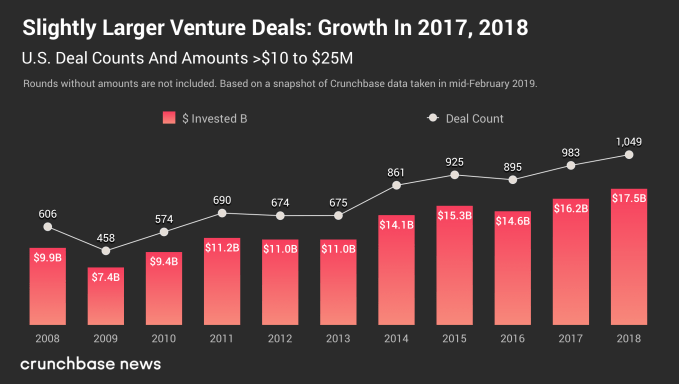

Rounds of $10 million to $25 million have grown over 11 years by 73 percentage points for counts, and 78 percentage points for amounts. This is a slower pace than $5 million to $10 million rounds, but continuing to edge up year over year.

Seed is its own class that is here to stay. Indeed pre-seed, seed and seed extension all seem to have specific dynamics. Of the 600-plus active seed funds who have raised a fund below $100 million, close to half have raised more than one fund. In the last three years in the U.S. we have not seen a slowing of seed funds raised for $100 million and below.

When we take into account the data lag, dollars for below $5 million is projected to be $8.5 billion, close to the height in 2015 of $8.6 billion. Deal counts are down from the height by a fifth, which does mean less seed-funded startups in the U.S. Provided that capital allocation is greater than $5 million continues to grow, less seed funded startups will die before raising a Series A. More companies have a chance to succeed, which is good for seed funds, and ultimately for the whole ecosystem.

Powered by WPeMatico