savings

Auto Added by WPeMatico

Auto Added by WPeMatico

The stakes keep getting higher for American discount brokerage Robinhood, which today disclosed that it has added hundreds of millions of dollars to its previously disclosed funding round.

Including the $280 million that the company had already announced, Robinhood said that it was “pleased to share” that it “raised an additional $320 million in subsequent closings.” Its now $600 million funding round brings its post-money valuation to $8.6 billion. Fortune first reported the news.

(A detail, but the new capital is part of the same round as it was raised at the same price. TechCrunch reported when the company’s $280 million round was announced, the fintech company was worth $8.3 billion. Another $300 million in capital at a flat share price means that the company’s valuation should have risen by only the dollar amount added. As it did.)

Robinhood has had a good business year, even if some of its practices have come under fire. The company pledged to tighten up parts of its platform relating to more exotic trading after the suicide of one of its users, for example; a topic that TechCrunch discussed at length last week.

What is inescapable is that Robinhood is having one hell of a year. When it might go public isn’t clear, especially as the private company is having no problem raising capital without an IPO. But as its value continues to rise, it becomes an increasingly remote acquisition target.

Powered by WPeMatico

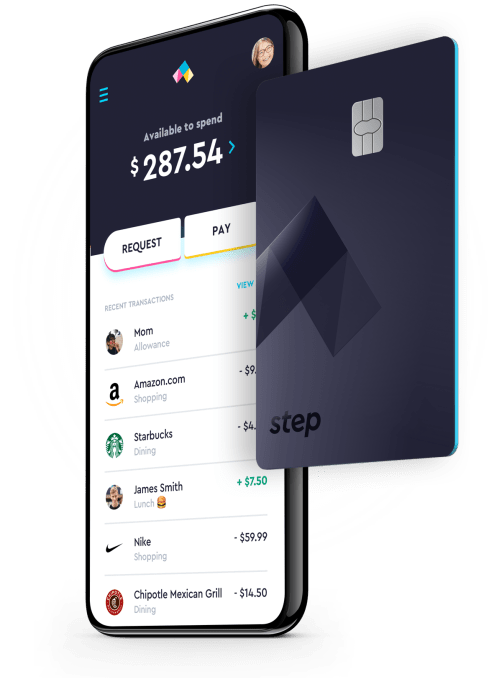

A new mobile banking startup called Step wants to help bring teenagers and other young adults into the cashless era. Today, cash is used less often, as more consumers shop online and send money to one another through payment apps like Venmo. But teenagers in particular are still heavily burdened with cash — even though they, too, want to spend their money on things that require a payment card, like Amazon.com purchases or mobile gaming, for example.

That’s where Step comes in.

The company aims to address the needs of what it believes is an underserved market in mobile banking — the 75 million children and young adults under the age of 21 in the U.S., who are still being forced to use cash.

This market isn’t the “unbanked,” it’s the “pre-banked,” explains Step CEO CJ MacDonald, whose previous startup, mobile gift card platform Gyft, sold to First Data several years ago.

Above: Step CEO, CJ MacDonald

“We’re building an all-in-one banking solution that primarily focuses on teens and parents,” he says. “We want it to be a teen’s first bank account. We want to be a teen’s first spending card. And we want to teach financial literacy and responsibility firsthand.”

MacDonald, along with CTO Alexey Kalinichenko, previously of Square and financial services startup Token, founded Step in May 2018. The 10-person team also includes several prior Gyft employees.

Last summer, Step closed on $3.8 million in seed funding from Sesame Ventures, Crosslink Capital and Collaborative Fund. Crosslink general partner Eric Chin sits on the board.

While there are a number of mobile banking apps out there today — like Chime, Monzo, Simple, Revolut and others — Step will specifically target teens, 13 and up, and other young adults with its marketing. Teens under 18 still need parents’ approval to sign up, of course. But the goal is to encourage the teens to bring the idea to their parents — not the other way around.

Step’s focus on this younger demographic puts it in a different space, where there are fewer competitors. Its more direct rivals are not the bigger mobile banks, but rather startups like teen debit card and bank app Current, or the parent-managed debit card for kids from Greenlight.

Step’s focus on this younger demographic puts it in a different space, where there are fewer competitors. Its more direct rivals are not the bigger mobile banks, but rather startups like teen debit card and bank app Current, or the parent-managed debit card for kids from Greenlight.

The mobile banking service Step provides will also aim to be more comprehensive than just a debit card. It will offer a combination of checking, savings and a Visa card that works as both credit and debit.

The card includes Visa’s Zero Liability Protection on all purchases from unauthorized use, and allows parents to set spending limits.

Parents will also be able to connect their own bank accounts to Step to instantly transfer in funds, which can then be distributed to kids’ accounts for things like allowances and chores, or other everyday spending needs. Step’s bank account itself is backed by Evolve Bank, so it’s FDIC-insured up to $250,000.

Unlike Current, which charges a subscription to use its service, Step aims to be a fee-free bank for consumers. Users don’t have to pay for their account, and there are no fees for things like overdrafts. Instead, Step’s plan is to generate revenue through traditional means — like interchange fees and by way of lending practices, once it has established a deposit base.

The company pays a 2.5 percent interest rate on deposits, offers a round-up savings feature and a range of budgeting tools and supports free instant transfers between Step accounts. It also provides access to a network of 35,000 ATMs with no fees.

The company pays a 2.5 percent interest rate on deposits, offers a round-up savings feature and a range of budgeting tools and supports free instant transfers between Step accounts. It also provides access to a network of 35,000 ATMs with no fees.

Beyond simply facilitating mobile banking, Step’s bigger goal is to teach teens to become financially responsible.

“Schools do not teach kids about money. A lot of families don’t talk about money. And it’s a crucial life skill that’s not really addressed properly when people are growing up,” says MacDonald, who says he was lacking in life skills in this area, even as a young college grad.

“There were ‘Money 101’ skills that I had not learned — that no one had talked to me about. Things like building credit, how many credit cards you should have, debt to income ratio,” he continues. “A lot of people get released into the real world without experience [in those areas],” he says.

Long-term, after solving the needs associated with everyday banking transactions, Step wants to layer on other products and services — like tools that allow a family to save together for college, for example.

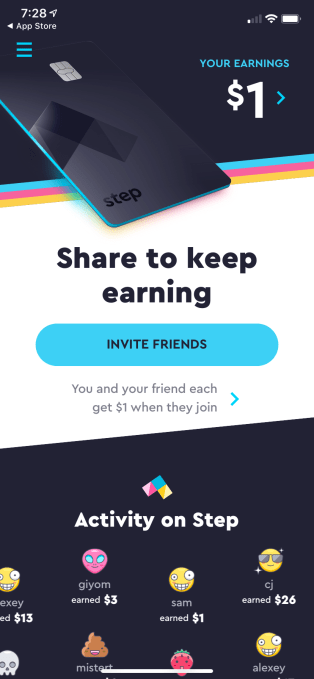

The company is launching the banking service under an invite-only system to scale up.

Today, it’s opening a waitlist and referral program. When you invite a friend, you each receive one dollar. Access will then be rolled out on a first-come, first-serve basis this spring. Users can join Step through the website, iOS or Android application.

Powered by WPeMatico

Yahoo Finance today launched a new app called Tanda that allows small groups of either five or nine people to save money together for short-term goals. The app uses the concept of a “money pool” – that is, everyone participating in one Tanda’s collaborative savings circles will pay a fixed amount to the group’s savings pot every month. And every month, one member… Read More

Yahoo Finance today launched a new app called Tanda that allows small groups of either five or nine people to save money together for short-term goals. The app uses the concept of a “money pool” – that is, everyone participating in one Tanda’s collaborative savings circles will pay a fixed amount to the group’s savings pot every month. And every month, one member… Read More

Powered by WPeMatico

Target’s mobile app strategy will undergo a significant change, starting this summer. The retailer announced this week it will soon combine the functionality of its Cartwheel savings app with its main shopping app, in preparation for an eventual Cartwheel shutdown. The Target app will also receive a notable upgrade this year, adding support for an indoor map that shows your location in… Read More

Target’s mobile app strategy will undergo a significant change, starting this summer. The retailer announced this week it will soon combine the functionality of its Cartwheel savings app with its main shopping app, in preparation for an eventual Cartwheel shutdown. The Target app will also receive a notable upgrade this year, adding support for an indoor map that shows your location in… Read More

Powered by WPeMatico

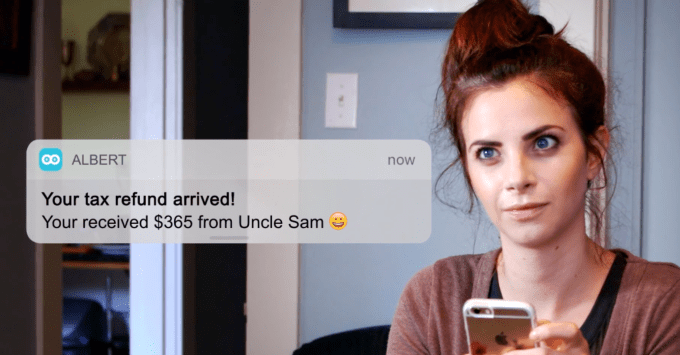

Everyone knows the basics of how to improve their financial health: put money into savings, track your spending, reduce your debt, look for ways to save on your monthly bills, and make smart investments. Where people struggle is translating that knowledge into specific actions you can take today. That’s where an application called Albert steps into help. The startup, which has now closed… Read More

Everyone knows the basics of how to improve their financial health: put money into savings, track your spending, reduce your debt, look for ways to save on your monthly bills, and make smart investments. Where people struggle is translating that knowledge into specific actions you can take today. That’s where an application called Albert steps into help. The startup, which has now closed… Read More

Powered by WPeMatico

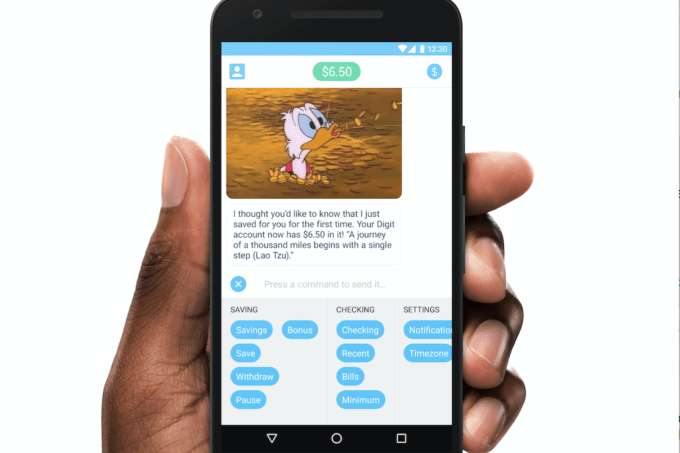

Whether you’re working out of a dorm room or running a billion-dollar company, a little pivot can go a long way. At their worst, pivots can derail a company’s success, but at their best, they demonstrate a company is still attuned to its user base — no matter how big it gets. Digit, a fintech service that helps people save, launched a year and a half ago with the… Read More

Whether you’re working out of a dorm room or running a billion-dollar company, a little pivot can go a long way. At their worst, pivots can derail a company’s success, but at their best, they demonstrate a company is still attuned to its user base — no matter how big it gets. Digit, a fintech service that helps people save, launched a year and a half ago with the… Read More

Powered by WPeMatico

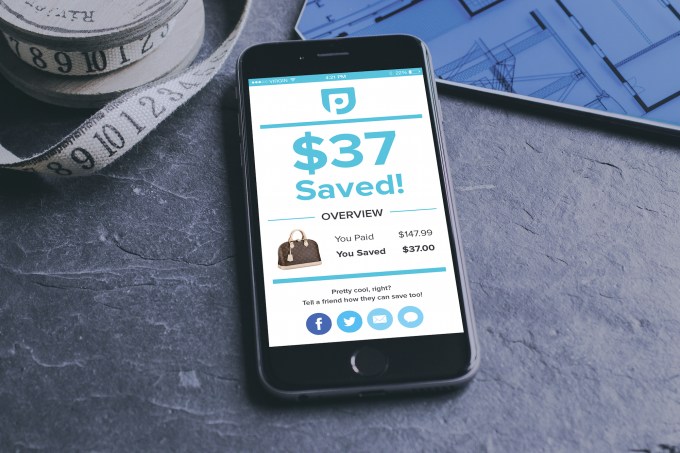

A service that helps online shoppers save when prices drop, Paribus, has raised $2.1 million in seed funding to continue to grow its business following the startup’s participation in the Y Combinator summer program and the Startup Battlefield at TechCrunch Disrupt NY 2015, where it first debuted. The company’s idea is to take a process that consumers were used to managing… Read More

A service that helps online shoppers save when prices drop, Paribus, has raised $2.1 million in seed funding to continue to grow its business following the startup’s participation in the Y Combinator summer program and the Startup Battlefield at TechCrunch Disrupt NY 2015, where it first debuted. The company’s idea is to take a process that consumers were used to managing… Read More

Powered by WPeMatico

Mobile shopping app Ibotta, which got its start as an alternative means of saving money while grocery shopping without having to clip coupons, has now closed on $40 million in Series C funding to continue to scale its business. A testament to building something practical and useful for the everyday consumer, Ibotta has seen over 10 million downloads to date and a user base that has saved a… Read More

Mobile shopping app Ibotta, which got its start as an alternative means of saving money while grocery shopping without having to clip coupons, has now closed on $40 million in Series C funding to continue to scale its business. A testament to building something practical and useful for the everyday consumer, Ibotta has seen over 10 million downloads to date and a user base that has saved a… Read More

Powered by WPeMatico

In my house, I have a small stockpile of shampoo and other health and beauty products that I’ve acquired for almost nothing, thanks to coupon stacking techniques that let you go into stores and walk out with vastly discounted products. I’m disappointed if I don’t save at least 50% of my grocery bill using coupons, if not more. But working the system to your advantage in this… Read More

In my house, I have a small stockpile of shampoo and other health and beauty products that I’ve acquired for almost nothing, thanks to coupon stacking techniques that let you go into stores and walk out with vastly discounted products. I’m disappointed if I don’t save at least 50% of my grocery bill using coupons, if not more. But working the system to your advantage in this… Read More

Powered by WPeMatico

The creators of coupon-code finder Honey, which helps online shoppers save at checkout, have now launched a new app called Milk (mmm…milk and honey…) that lets you save at the grocery store. The app is now one of many aimed at helping consumers save on consumer packaged good purchases, even if they don’t have time for clipping coupons from a newspaper. Today, there a lot of… Read More

The creators of coupon-code finder Honey, which helps online shoppers save at checkout, have now launched a new app called Milk (mmm…milk and honey…) that lets you save at the grocery store. The app is now one of many aimed at helping consumers save on consumer packaged good purchases, even if they don’t have time for clipping coupons from a newspaper. Today, there a lot of… Read More

Powered by WPeMatico