sao paulo

Auto Added by WPeMatico

Auto Added by WPeMatico

Fintech and proptech are two sectors that are seeing exploding growth in Latin America, as financial services and real estate are two categories in particular dire need of innovation in a region.

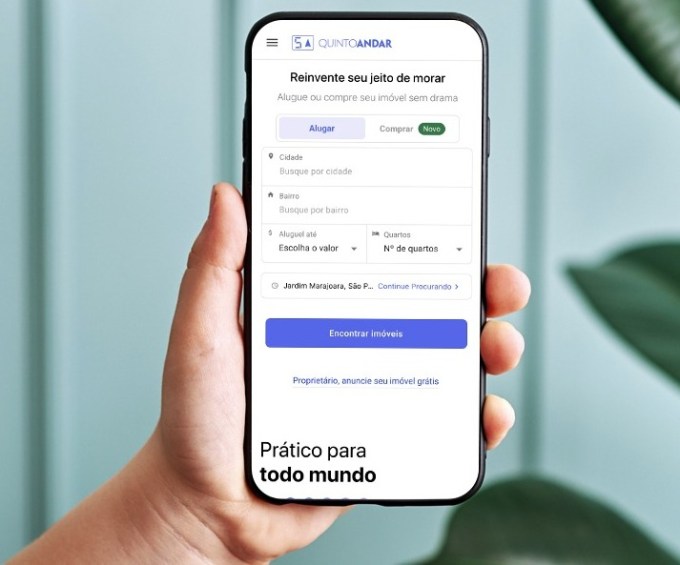

Brazil’s QuintoAndar, which has developed a real estate marketplace focused on rentals and sales, has seen impressive growth in recent years. Today, the São Paulo-based proptech has announced it has closed on $300 million in a Series E round of funding that values it at an impressive $4 billion.

The round is notable for a few reasons. For one, the valuation — high by any standards but especially for a LatAm company — represents an increase of four times from when QuintoAndar raised a $250 million Series D in September 2019.

It’s also noteworthy who is backing the company. Silicon Valley-based Ribbit Capital led its Series E financing, which also included participation from SoftBank’s LatAm-focused Innovation Fund, LTS, Maverik, Alta Park, an undisclosed U.S.-based asset manager fund with over $2 trillion in AUM, Kaszek Ventures, Dragoneer and Accel partner Kevin Efrusy.

Having backed the likes of Coinbase, Robinhood and CreditKarma, Ribbit Capital has historically focused on early-stage investments in the fintech space. Its bet on QuintoAndar represents clear faith in what the company is building, as well as its confidence in the startup’s plans to branch out from its current model into a one-stop real estate shop that also offers mortgage, title, insurance and escrow services.

The latest round brings QuintoAndar’s total raised since its 2013 inception to $635 million.

Ribbit Capital Partner Nick Huber said QuintoAndar has over the years built “a unique and trusted brand in Brazil” for those looking for a place to call home.

“Whether you are looking to buy or to rent, QuintoAndar can support customers through the entire transaction process: from browsing verified inventory to signing the final contracts,” Huber told TechCrunch. “The ability to serve customers’ needs through each phase of life and to do so from start to finish is a unique capability, both in Brazil and around the world.”

QuintoAndar describes itself as an “end-to-end solution for long-term rentals” that, among other things, connects potential tenants to landlords and vice versa. Last year, it expanded also into connecting a home buyers to sellers.

Image Credits: QuintoAndar

TechCrunch spoke with co-founder and CEO Gabriel Braga and he shared details around the growth that has attracted such a bevy of high-profile investors.

Like most other businesses around the world, QuintoAndar braced itself for the worst when the COVID-19 pandemic hit last year — especially considering one core piece of its business is to guarantee rents to the landlords on its platform.

“In the beginning, we were afraid of the implications of the crisis but we were able to honor our commitments,” Braga said. “In retrospect, the pandemic was a big test for our business model and it has validated the strength and defensibility of our business on the credit side and reinforced our value proposition to tenants and landlords. So after the initial scary moments, we actually felt even more confident in the business that we are building.”

QuintoAndar describes itself as “a distant market leader” with more than 100,000 rentals under management and about 10,000 new rentals per month. Its rental platform is live in 40 cities across Brazil, while its home-buying marketplace is live in four. Part of its plans with the new capital is to expand into new markets within Brazil, as well as in Latin America as a whole.

The startup claims that, in less than a year, QuintoAndar managed to aggregate the largest inventory among digital transactional platforms. It now offers more than 60,000 properties for sale across Sao Paulo, Rio de Janeiro, Belho Horizonte and Porto Alegre. To give greater context around the company’s growth of that side of its platform: In its first year of operation, QuintoAndar closed more than 1,000 transactions. It has now surpassed the mark of 8,000 transactions in annualized terms, growing between 50% and 100% quarter over quarter.

As for the rentals side of its business, Braga said QuintoAndar has more than 100,000 rentals under management and is closing about 10,000 new rentals per month. The company is not profitable as it’s focused on growth, although it’s unit economics are particularly favorable in certain markets such as Sao Paulo, which is financing some of its growth in other cities, according to Braga.

Now, the 2,000-person company is looking to begin its global expansion with plans to enter the Mexican market later this year. With that, Braga said QuintoAndar is looking to hire “top-tier” talent from all over.

“We want to invest a lot in our product and tech core,” he said. “So we’re trying to bring in more senior people from abroad, on a global basis.”

CEO Braga and CTO André Penha came up with the idea for QuintoAndar after receiving their MBAs at Stanford University. As many startups do, the company was founded out of Braga’s personal “nightmare” of an experience — in this case, of trying to rent an apartment in Sao Paulo.

The search process, he recalls, was difficult as there was not enough information available online and renters were forced to provide a guarantor, or co-signer, from the same city or pay rent insurance, which Braga described as “very expensive.”

“Overall, I felt it was a very inefficient and fragmented process with no transparency or tech,” Braga told me at the time of the company’s last raise. “There was all this friction and high cost involved, just real tangible problems to solve.”

The concept for QuintoAndar (which can be translated literally to “Fifth Floor” in Portuguese) was born.

“Little by little, we created a platform that consolidated supply and inventory in a uniform way,” Braga said.

The company took the search phase online for the first time, according to Braga. It also eliminated the need for tenants to provide a guarantor, thereby saving them money. On the other side, QuintoAndar also works to help protect the landlord with the guarantee that they will get their rent “on time every month,” Braga said.

It’s been interesting watching the company evolve and grow over time, just as it’s been fascinating seeing the region’s startup scene mature and shine in recent years.

Powered by WPeMatico

It looks like everyone and their mother is trying to reinvent the Brazilian banking system. Earlier this year we wrote about Nubank’s $400 million Series G, last month there was the PicPay IPO filing and today, alt.bank, a Brazilian neobank, announced a $5.5 million Series A led by Union Square Ventures (USV).

It’s no secret that the Brazilian banking system has been poised for disruption, considering the sector’s little attention to customer service and exorbitant fee structure that’s left most Brazilians unbanked, and alt.bank is just the latest company trying to take home a piece of the pie.

Following Nubank’s strategy of launching a bank with colors that are very un-bank-like, signaling that they do things differently, alt.bank similarly launched its first financial product in 2019 — a fluorescent-yellow debit card which the locals have endearingly dubbed, “o amarelinho,” meaning, “the little yellow card.”

The company, founded by serial entrepreneur Brad Liebmann, follows the founder’s $480 million exit of Simply Business, which was acquired by U.S. insurance giant Travelers in 2017.

Unlike many fintechs, alt.bank has a strong social mission and pays commissions for referrals that last for the customer’s lifetime.

“Most fintechs just help wealthy people get wealthier, so I thought let’s do something with a social mission,” Liebmann told TechCrunch in an interview.

To drive home the mission, and really target the unbanked, Liebman and his team of 80 employees have designed an app that can be used by the illiterate. Instead of words, users can follow color-coded prompts to complete a transaction. The company also plans to launch credit products soon.

According to the company, close to a million people have downloaded the android app since launch, but Liebman declined to disclose how many active users the company actually has.

Today, the company’s core offerings include the debit card, a prepaid credit card, Pix (similar to Zelle), a savings account and even telemedicine visits via a partnership with Dr. Consulta, a network of healthcare clinics throughout the country. The prepaid credit card is key because online stores in Brazil don’t accept debit card purchases.

In addition to the perk of ongoing commissions, alt.bank has also partnered with three major drugstores, allowing their users to get 5-30% off any item at the stores, including medication.

While the company is based in São Paulo and São Carlos, Liebmann and his family are currently based in London due to regulations around the pandemic.

The investment in alt.bank marks USV’s first investment in South America, solidifying a trend by other major U.S. investors such as Sequoia who only in the last several years have started looking to LatAm for deals.

“The bar was high for our first investment in South America,” said Union Square Ventures partner John Buttrick. “The combination of the alt.bank business model and world-class management team enticed us to expand our geographic focus to help build the leading digital bank targeting the 100 million Brazilians who are currently being neglected by traditional lenders,” he added in a statement.

Powered by WPeMatico

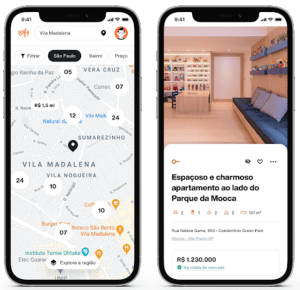

Nearly exactly one month ago, digital real estate platform Loft announced it had closed on $425 million in Series D funding led by New York-based D1 Capital Partners. The round included participation from a mix of new and existing investors such as DST, Tiger Global, Andreessen Horowitz, Fifth Wall and QED, among many others.

At the time, Loft was valued at $2.2 billion, a huge jump from its being just near unicorn territory in January 2020. The round marked one of the largest ever for a Brazilian startup.

Now, today, São Paulo-based Loft has announced an extension to that round with the closing of $100 million in additional funding that values the company at $2.9 billion. This means that the 3-year-old startup has increased its valuation by $700 million in a matter of weeks.

Baillie Gifford led the Series D-2 round, which also included participation from Tarsadia, Flight Deck, Caffeinated and others. Individuals also put money in the extension, including the founders of Better (Zach Frenkel), GoPuff, Instacart, Kavak and Sweetgreen.

Loft has seen great success in its efforts to serve as a “one-stop shop” for Brazilians to help them manage the home buying and selling process.

Image Credits: Loft

In 2020, Loft saw the number of listings on its site increase “10 to 15 times,” according to co-founder and co-CEO Mate Pencz. Today, the company actively maintains more than 13,000 property listings in approximately 130 regions across São Paulo and Rio de Janeiro, partnering with more than 30,000 brokers. Not only are more people open to transacting digitally, more people are looking to buy versus rent in the country.

“We did more than 6x YoY growth with many thousands of transactions over the course of 2020,” Pencz told TechCrunch at the time of the company’s last raise. “We’re now growing into the many tens of thousands, and soon hundreds of thousands, of active listings.”

The decision to raise more capital so soon was due to a variety of factors. For one, Loft has received “overwhelming investor interest” even after “a very, very oversubscribed main round,” Pencz said.

“We have seen a continued acceleration in our market share growth, especially in São Paulo and Rio de Janeiro, the two markets we currently operate in,” he added. “We saw an opportunity to grow even faster with additional capital.”

Pencz also pointed out that Baillie Gifford has relatively large minimum check size requirements, which led to the extension being conducted at a higher price and increased the total round size “by quite a bit to be able to accommodate them.”

While the company was less forthcoming about its financials as of late, it told me last year that it had notched “over $150 million in annualized revenues in its first full year of operation” via more than 1,000 transactions.

The company’s revenues and GMV (gross merchandise value) “increased significantly” in 2020, according to Pencz, who declined to provide more specifics. He did say those figures are “multiples higher from where they were,” and that Loft has “a very clear horizon to profitability.”

Pencz and Florian Hagenbuch founded Loft in early 2018 and today serve as its co-CEOs. The aim of the platform, in the company’s words, is “bringing Latin American real estate into the e-commerce age by developing online alternatives to analogue legacy processes and leveraging data to create transparency in highly opaque markets.” The U.S. real estate tech company with the closest model to Loft’s is probably Zillow, according to Pencz.

In the United States, prospective buyers and sellers have the benefit of MLSs, which in the words of the National Association of Realtors, are private databases that are created, maintained and paid for by real estate professionals to help their clients buy and sell property. Loft itself spent years and many dollars in creating its own such databases for the Brazilian market. Besides helping people buy and sell homes, it offers services around insurance, renovations and rentals.

In 2020, Loft also entered the mortgage business by acquiring one of the largest mortgage brokerage businesses in Brazil. The startup now ranks among the top-three mortgage originators in the country, according to Pencz. When it comes to helping people apply for mortgages, he likened Loft to U.S.-based Better.com.

This latest financing brings Loft’s total funding raised to an impressive $800 million. Other backers include Brazil’s Canary and a group of high-profile angel investors such as Max Levchin of Affirm and PayPal, Palantir co-founder Joe Lonsdale, Instagram co-founder Mike Krieger and David Vélez, CEO and founder of Brazilian fintech Nubank. In addition, Loft has also raised more than $100 million in debt financing through a series of publicly listed real estate funds.

Loft plans to use its new capital in part to expand across Brazil and eventually in Latin America and beyond. The company is also planning to explore more M&A opportunities.

This article was updated post-publication to reflect accurate investor information.

Powered by WPeMatico

FinanZero, a Brazilian online credit marketplace, announced today that it has closed a $7 million round of funding — its fourth since it launched in 2016. It has raised a total of $22.85 million to date.

The real-time online loan broker allows people to apply for a personal loan, a car equity loan or a home equity loan for free and receive an answer in minutes. A key to FinanZero’s success is that it doesn’t offer the loans itself, but has instead partnered with about 51 banks and fintechs who back the loans.

FinanZero is based in Brazil’s financial capital, São Paulo, and has 52 employees.

“From day one we said, ‘We only work with a success fee,’ so we only get paid when the customer signs the loan contract,” said Olle Widen, the company’s co-founder and CEO.

Instead of charging the customer, FinanZero gets a commission from one of its partners, and with a growing volume of credit applications — an average of 750,000 applications per month — the company has seen 61% revenue growth from 2019-2020.

Olle Widen, co-founder and CEO of FinanZero. Image Credits: FinanZero

The Brazilian finance and banking market has been ripe for disruption, as it has traditionally favored the rich.

Those with low incomes — the vast majority of Brazilian citizens — are then left with few options when it comes to financing, and which in turn forces them into compounding debt from which they’ll likely never escape. Traditionally, young Brazilians have lived with their families until they got married, and while there is a cultural aspect to it, the bottom line is that mortgages were infinitely hard to get approved.

With products like FinanZero and Nubank — Latin America’s largest digital bank — Brazilians are starting to see more economic mobility and independence from the legacy institutions that dictated their lives for so long.

Widen, who is Swedish, moved to Brazil about 10 years ago for personal reasons, and while there, was pitched the idea of FinanZero by Webrock Ventures, an investment company focused on bringing Nordic innovation to Brazil.

At the time, Swedish startup Lendo — a precursor to FinanZero — was making waves in Sweden, and the team felt that a similar model would succeed in Brazil, a country known for its bureaucracy and red tape, and thus primed for a streamlined and hassle-free approach to loans.

The original idea was to just copy Lendo, Widen said, but as others have discovered, along the way the team needed to “tropicalize” the product and the experience, meaning they had to build a custom solution for the Brazilian market and its people.

“The founder of Lendo was a childhood friend of mine,” said Widen, of his close ties to the Swedish fintech.

To apply for a loan on FinanZero you don’t need to provide your credit score. Instead, all you need is a utility bill (proof of address), proof of income and your government ID. The process is so simple, Widen said, that 92% of loan applications are initiated from a smartphone.

“Our business model is very based on the bank’s risk appetite and we saw 60% growth from 2019-2020. We are close to 3 million visits per month, about 1.5 are unique and in March of 2021, we had 800,000 people fill out the entire loan form. We have about a 10% approval rating across all products,” Widen said.

The round was led by the Swedish investors VEF, Dunross & Co, and Atlant Fonder, which are all previous investors in the company. The funding will go toward marketing — most of which will be on T.V. — product development, and talent acquisition.

Powered by WPeMatico

The Brazilian-based pan-Latin American food delivery startup iFood has announced a series of initiatives designed to reduce the company’s environmental impact as consumers push companies to focus more on sustainability.

The program has two main components — one focused on plastic pollution and waste and another aiming to become carbon neutral in its operations by 2025.

Perhaps the most ambitious, and surely the most capital intensive of the company’s waste reduction initiatives is the development of a semi-automated recycling facility in São Paulo.

“We want to transform the entire supply chain for plastic-free packaging in Brazil. By controlling the national supply chain, from production to marketing and logistics, we can offer more competitive pricing for packaging to industries that already exist but do not have a scale of production and demand today,” said Gustavo Vitti, the chief people and sustainability officer at iFood.

The company has also created an in-app option that allows customers to decline plastic cutlery when they’re getting their food delivered.

“These initiatives will contribute to reducing the consumption of plastic items, which are often sent without being requested and end up going unused into the garbage bin,” said Vitti. “In the first tests that we did, 90% of consumers used the resource, which resulted in the reduction of tens of thousands of plastic cutlery and shows our consumers’ desire to receive less waste in their homes.”

On the emissions front, the company will work with Moss.Earth, a technology company in the carbon market, which developed the GHG inventory to offset its emissions by buying credits tied to environmental preservation and reforestation projects.

But the company is also working with Tembici, a provider of electric bikes in Brazil, to move its delivery fleet off of internal combustion powered mopeds or scooters.

“We know that compensation alone is not enough. It is necessary to think of innovative ways to reduce CO2 emissions. In October last year, we launched the iFood Pedal program, in partnership with Tembici, a project developed exclusively for couriers that offers affordable plans for renting electric bikes,” said Vitti. “Currently, more than 2,000 couriers are registered and are sharing 1,000 electric bikes in São Paulo and Rio de Janeiro in addition to the educational aspect of program that we have contemplated. With good adherence indicators, our plan is to gradually expand the project, taking it to other cities and, thus, increase our percentage of clean deliveries.”

The Brazilian electric motorcycle company Voltz Motors is also working with iFood, which ordered 30 electric motorcycles for use by some of its delivery partners. The company hopes to roll out more than 10,000 motorcycles over the next 12 months.

Coupled with internal-facing initiatives to improve water reuse, deploy renewable energy and develop a green roof at its Osasco headquarters, iFood is hoping to hit sustainability goals that can improve the environment across Brazil and beyond.

“We know that we have a long way to go, but we trust that together with important partners and this set of initiatives, in addition to others that are under development, it will be possible to reduce plastic generation and CO2 emissions impact on the environment. Our relevance and presence in the lives of Brazilian families further reinforces the importance of these environmental commitments for the planet,” said Vitti.

Powered by WPeMatico

Creditas, the Brazilian lending business, has raised $255 million in new financing as financial services startups across Latin America continue to attract massive amounts of cash.

The company’s credit portfolio has crossed 1 billion reals ($196.66 million) and the new round will value the company at $1.75 billion thanks to $570 million raised in outside financing over five rounds.

Creditas is the latest company to benefit from a boom in financial services startup investing across the region. As the year dawned, venture investments into fintech startups in Latin America had grown from $50 million in 2014 to top $2.1 billion in 2020 across 139 deals, according to a report from CB Insights.

Investors in the round include new investors like LGT Lightstone, Tarsadia Capital, Wellington Management, e.ventures and an affiliate of Advent International, Sunley House Capital. Previous investors including SoftBank Vision Fund 1, SoftBank Latin America DFund, VEF, Kaszek and Amadeus Capital Partners also returned to put more money into the company.

“Creditas is still in the early innings of penetrating the huge untapped secured lending market in Brazil and Mexico” says Paulo Passoni, managing partner of SoftBank Latam fund, in a statement.

The company’s growth is a testament both to the need for new lending products across Latin America and the perspicacity of investors like Kaszek Ventures, whose portfolio has included several massive wins from bets on startups tackling financial services in Latin America.

“The journey since our investment in the Series A has been absolutely extraordinary. The team has executed on its vision, and Creditas has evolved into an asset-light ecosystem that resolves key financial needs of its customers throughout their lifetimes,” says Nicolas Szekasy, managing partner of Kaszek Ventures, in a statement.

Another big winner is Redpoint’s e.ventures fund, which has focused on investments in Latin America for the last several years.

“By empowering Brazilians to take control of their lending needs at reasonable rates, Creditas creates a beloved consumer product that will drive significant value for customers and investors. Having been involved since the seed stage through Redpoint e.ventures, we’re thrilled to support the company with our Global Growth Fund as well, as they change the Brazilian fintech landscape,” said Mathias Schilling, co-founder and managing partner of e.ventures.

Creditas has plans to use the cash to expand its home and auto lending as well as a payday lending service based on customers’ salaries and a retail option to sell through buy now, pay later loans based on a customer’s salary.

The company is also looking to expand to other markets, with an eye toward establishing a foothold in the Mexican market.

Founded in 2012, when the founders worked out of a five-square-meter office on Berrini Avenue in São Paulo, the company now boasts a robust business with hundreds of employees and a business resting on a secured lending marketplace and independent home and auto lending operations.

The company also released quarterly results for the first time, showing losses narrowing from 74.9 million Brazilian reals to 40.5 million reals in the year ago quarter.

Powered by WPeMatico

Over the last five years, Brazil has witnessed a startup boom.

The main startups hubs in the country have traditionally been São Paulo and Belo Horizonte, but now a new wave of cities are building their own thriving local startup ecosystems, including Recife with Porto Digital hub and Florianópolis with Acate. More recently, a “Black Silicon Valley” is beginning to take shape in Salvador da Bahia.

While finance and media are typically concentrated in São Paulo and Rio de Janeiro, Salvador, a city of three million in the state of Bahia, is considered one of Brazil’s cultural capitals.

With an 84% Afro-Brazilian population, there are deep, rich and visible roots of Africa in the city’s history, music, cuisine and culture. The state of Bahia is almost the size of France and has 15 million people. Bahia’s creative legacy is quite clear, given that almost all the big Brazilian cultural patrimonies have their roots here, from samba and capoeira to various regional delicacies.

Many people are unaware that Brazil has the largest Black population in any country outside of Africa. Like counterparts in the U.S. and across the Americas, Afro-Brazilians have long struggled for socio-economic equity. As with counterparts in the United States, Brazil’s Black founders have less access to capital.

According to research by professor Marcelo Paixão for the Inter-American Development Bank, Afro-Brazilians are three times more likely to have their credit denied than their white counterparts. Afro-Brazilians also have over twice the poverty rates of white Brazilians and only a handful of Afro-Brazilians have held legislative positions, despite comprising more than 50% of the population. Not to mention, they make up less than 5% of the top level of the top 500 companies. Compared with countries like the United States or the United Kingdom, the racial funding gap is even more stark as more than 50% of Brazil’s population is classified as Afro-Brazilian.

Salvador (Bahia’s capital) is the natural birthplace of Brazil’s Black Silicon Valley, which largely centers around a local ecosystem hub, Vale do Dendê.

Vale do Dendê coordinates with local startups, investors and government agencies to support entrepreneurship and innovation and runs startup acceleration programs specifically focusing on supporting Afro-Brazilian founders. The Vale do Dendê Accelerator organization has already been in the spotlight at international and national publications because of its innovative work in bringing startup and tech education from mainstream to traditionally underserved communities.

In almost three years, the accelerator has supported 90 companies directly that cut across various industries, with high representation from the creative and social impact sectors. Almost all of the companies have achieved double-digit growth and various companies have gone on to raise further funding or corporate backing. One of the first portfolio companies, TrazFavela, a delivery app that focuses on linking customers and goods from traditionally marginalized communities, was supported by the accelerator in 2019. Despite the lockdown, the business grew 230% between the period of March and May after incubation and recently signed an agreement for further support and investment from Google Brasil.

There is a clear recognition of the business case for Afro-Brazilian businesses. Another company supported in the beginning with mentoring by Vale do Dendê is Diaspora Black (which focuses on Black culture in the tourism sectors). It attracted backing from Facebook Brasil and grew 770% in 2020.

The same is true for AfroSaúde, a health tech company focused on low-income communities with a new service to prevent COVID-19 in favelas (urban slums, which incidentally have high Black representation). The app now has more than 1,000 Black health professionals on its platform, creating jobs while addressing a health crisis that had been tremendously racialized.

Despite Brazil’s challenging economic situation, large national and global companies and investors are taking notice of this startup boom. Major IT company Qintess has come on board as a major sponsor to help Salvador become the leading Black tech hub in Latin America.

The company announced an investment of around 10 million reais (nearly $2 million USD) over the next five years in Black startups, including a collaboration with Vale do Dendê to train around 2,000 people in tech and accelerate more than 500 startups led by Black founders. Also, in September, Google launched a 5 million reais (around $1 million USD) Black Founders Fund with the support of Vale do Dendê to boost the Afro-Brazilian startup ecosystem.

There is no doubt that the new wave of innovation will come from the emerging markets, and the African Diaspora can play an important role. With the world’s largest African diaspora population in the hemisphere, Brazil can be a major leader on this. Vale do Dendê is keen to build partnerships to make Brazil and Latin America a more representative startup and creative economy ecosystem.

Powered by WPeMatico

In May 2020, Intel announced its purchase of Moovit, a mobility as a service (MaaS) solutions company known for an app that stitched together GPS, traffic, weather, crime and other factors to help mass transit riders reduce their travel times, along with time and worry.

According to a release, Intel believes combining Moovit’s data repository with the autonomous vehicle solution stack for its Mobileye subsidiary will strengthen advanced driver-assistance systems (ADAS) and help create a combined $230 billion total addressable market for data, MaaS and ADAS .

Before he was a member of Niantic’s executive team, private investor Omar Téllez was president of Moovit for the six years leading up to its acquisition. In this guest post for Extra Crunch, he offers a look inside Moovit’s early growth strategy, its efforts to achieve product-market fit and explains how rapid growth in Latin America sparked the company’s rapid ascent.

In late 2011, Uri Levine, a good friend from Silicon Valley and founder of Waze, asked me to visit Israel to meet Nir Erez and Roy Bick, two entrepreneurs who had launched an application they had called “the Waze of public transportation.”

By then, Waze was already in conversations to be sold (Google would finally buy it for $1.1 billion) and Uri was thinking about his next step. He was on the board of directors of Moovit (then called Tranzmate) and thought they could use a lot of help to grow and expand internationally, following Waze’s path.

At the time, I was part of Synchronoss Technologies’ management team. After Goldman Sachs and Deutsche Bank took us public in 2006, AT&T and Apple presented us with an idea that would change the world. It was so innovative and secret that we had to sign NDAs and personal noncompete agreements to work with them. Apple was preparing to launch the first iPhone and needed a system where users could activate devices from the comfort of their homes. As such, Synchronoss’ stock became very attractive to the capital markets and ours became the best public offering of 2006.

After six years with Synchronoss while also making some forays into the field of entrepreneurship, I was ready for another challenge. With that spirit in mind, I got on the plane for Israel.

I will always remember the landing at Ben Gurion airport. After 12 hours traveling from JFK, I was called to the front of the immigration line:

“Hey! The guy in the Moovit T-shirt, please come forward!”

For a second, I thought I was in trouble, but then the immigration officer said, “Welcome to Israel! We are proud of our startups and we want the world to know that we are a high-tech powerhouse,” before he returned my passport and said goodbye.

I was completely amazed by his attitude and wondered if I really knew what I was getting into.

At first glance, the numbers seemed very attractive. In 2012, there were roughly seven billion people in the world and only a billion vehicles. Thus, many more people used mass public transport than private and users had to face not only the uncertainty of when a transport would arrive, but also what might happen to them while waiting (e.g., personal safety issues, weather, etc.). Adding more uncertainty: Many people did not know the fastest way to get from point A to point B. As designed, mass public transport was a real nightmare for users.

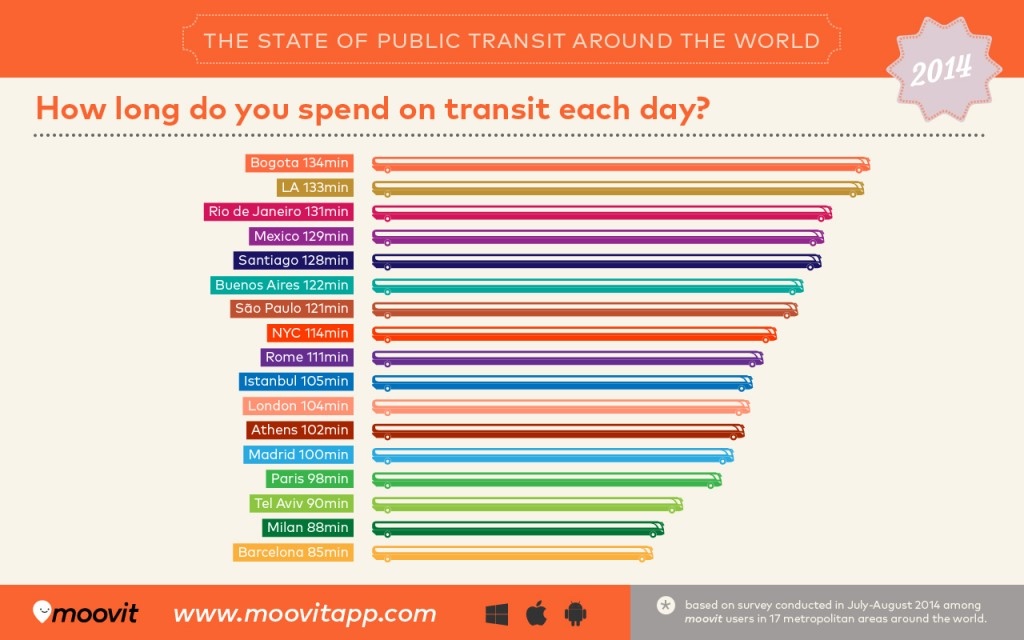

Uri advised us to “fall in love with the problem and not with the solution,” which is what we tried to do at Moovit. Although Waze had spawned a new transportation paradigm and helped reduce traffic in big cities, mass transit was a much bigger monster that consumed an average of two hours of each day for some people, which adds up to 37 days of each year*!

What would you do if someone told you that in addition to your vacation days, an app could help you find 18 extra days off work next year by cutting your transportation time in half?

* Assumes 261 working days a year, 14 productive hours per day.

Image Credits: Moovit (opens in a new window)

Powered by WPeMatico

In 2017, when a destructive earthquake struck Puebla, Mexico, sending shock waves to Mexico City and destroying buildings in the nation’s megalopolis and its surrounding suburbs, both public and private emergency services sprung into action.

For multinational corporations operating in the city it was a test of their internal support services, which were established to meet the “duty of care” requirements that multinationals have to their foreign employees. That’s a minimum threshold which companies must meet to ensure the safety of their employees.

After the Mexico City earthquake, at least one Fortune 500 insurance company found its services lacking. It took two weeks for the company to contact all of its employees and account for everyone.

So the company turned to a new Washington-based startup called Base Operations to see if they could do a better job.

Founded by a former security and risk management consultant, Cory Siskind, Base Operations uses a suite of hosted software services and mobile applications to provide security updates to corporate customers and their employees.

The insurance company tested Base Operations’ check-in feature to see how it would perform in a simulated natural disaster and Siskind said that Base Operations had identified the location of 80% of the company’s workforce in less than two days. More than half of the company’s employees checked in within the first 24 hours.

Base Operations offers a dashboard for corporate customers to monitor their employees’ locations and for staff traveling abroad, the company has an app that provides geo-tagged alerts on potential risks based on an individual’s location.

“This is a compliance situation for companies… They have to do it,” says Siskind. “We work with a company’s chief security officers and travel security. If you send people off into an emerging market with a risk PDF… It’s not dynamic information and it just sits in a report and nobody reads it.”

Companies with a sales or marketing team traveling around need to have some sort of tool to meet their compliance regulations and duty of care standards, says Siskind.

“We have a whole set of features that nudge towards safer behaviors so that you don’t end up getting mugged and so that you don’t end up in a situation that would be damaging to you,” she says.

Siskind recently raised $1 million for Base Operations from investors including Glasswing Ventures, Spiro Ventures, the Latin American early-stage investment firm Magma Partners and Good Growth Capital. Base Operations graduated from Techstars Impact Accelerator in 2018.

The money from the company’s most recent round will be used to expand the company’s sales and marketing efforts and continue its research and development.

So far, the company has three customers, including the undisclosed insurance provider, the energy company Enel and another, yet unnamed, corporation.

Base Operations provides its services in 15 cities, including: Mexico City, São Paulo, Rio de Janeiro, Buenos Aires, Santiago, San Juan (Puerto Rico) and San Jose (Costa Rica).

Powered by WPeMatico

Rappi represents a new era for Latin American technology startups.

Based in Bogotá, Colombia, the on-demand delivery startup has taken the region by storm, attracting a record amount of venture capital funding in mere months. Today marks the beginning of a new round of explosive growth as SoftBank, the Japanese telecom giant and prolific Silicon Valley tech investor, has confirmed a $1 billion investment in the business.

The king-sized financing comes two months after SoftBank announced its Innovation Fund, a new pool of capital committed to spending billions on the growing tech ecosystem in Central and South America.

VC funding in Latin America catapulted to new heights in 2018. Startups located across Argentina, Brazil, Chile, Colombia and more have secured nearly $2.5 billion since the beginning of 2018, according to PitchBook, up from less than $1 billion invested in 2017.

SoftBank plans to transfer the Rappi investment to the Innovation Fund “upon the fund’s establishment,” according to a press release. For now, the SoftBank Group and affiliated Vision Fund will each invest $500 million in the company. Jeffrey Housenbold, a managing director at SoftBank responsible for investments in Brandless, Opendoor and DoorDash, will join Rappi’s board of directors.

“SoftBank’s vision of accelerating the technology revolution deeply resonated with our mission of improving how people live through digital payments and a super-app for everything consumers need,” Rappi co-founder Sebastian Mejia said in a statement. “We will continue to focus on building innovations for couriers, restaurants, retailers and start-ups that translate into new sources of growth.”

Mejia, Simón Borrero and Felipe Villamarin launched Rappi in 2015, graduating from the Y Combinator startup accelerator the following year. It didn’t take long for the business to capture the attention of American VCs, including the likes of Andreessen Horowitz, DST Global and Sequoia Capital .

The latest round, the largest ever for a Latin American tech startup, brings Rappi’s total raised to date to a whopping $1.2 billion. The company was valued at more than $1 billion last year with a $200 million financing.

Rappi is among few venture-backed “unicorns” based in Latin America. São Paulo-based Nubank, a fast-growing fintech startup, garnered a $4 billion valuation last year with a $180 million investment.

Rappi didn’t immediately respond to a request for comment.

Powered by WPeMatico