San Francisco

Auto Added by WPeMatico

Auto Added by WPeMatico

Tunisian human rights activist Amira Yahyaoui couldn’t go to college.

Not because she couldn’t afford it; where she comes from, college is virtually free. She lost the opportunity to pursue higher education, to finish high school, even, when she was exiled from Tunisia at age 17, under the repressive regime of the country’s former President, Zine El Abidine Ben Ali.

As part of the Tunisian human rights diaspora, she was inspired to build Al Bawsala, a globally renowned NGO that fights for government accountability, transparency and access to information. Now, Yahyaoui has traveled thousands of miles to San Francisco to fight another battle near and dear to her heart: civic education, or in Silicon Valley terms, edtech.

“I always knew that I wouldn’t allow myself to do anything else before solving the problem in my country and today, Tunisia is the only Arab democracy in the world,” Yahyaoui told TechCrunch.

With that in mind, her focus has shifted to Mos, a tech-enabled platform for students to apply for financial aid. With backing from Uber co-founder Garrett Camp, his startup studio Expa, Kleiner Perkins chairman John Doerr, Base Ventures, Sweet Capital and others, Mos has closed a $4 million seed round and plans to take its recently-launched product to the next level.

The startup seeks to decrease American student debt, which totaled nearly $1.6 trillion in 2018, and digitize the antiquated government systems that deter students from applying for financial aid. For a one-time fee of $149 and about 20 minutes of their time, Mos helps students of all backgrounds maximize their aid awards.

“Our mission is to bridge the gap between citizens and government in a way that works with technology today,” Yahyaoui said.

Yahyaoui is applying what she’s learned building a government-fighting NGO to the startup world, and with the support of top-tier investors, she’s well on her way to proving an “uneducated” immigrant woman of color can write a Silicon Valley success story for the masses.

Mos founder and chief executive officer Amira Yahyaoui.

After being forced out of her home country, Yahyaoui fled to France, where she lived as an illegal immigrant and continued to fight against Tunisia’s authoritarian leadership through her blog and an anti-censorship campaign she started online.

When social media sparked anti-government protests across the Middle East, Yahyaoui, still unable to reenter Tunisia, became a face of what was later called the Arab Spring. Her digital prowess, activist reputation and persistent efforts to highlight the Tunisian administration’s human rights abuses quickly made her a face of the movement.

On January 14, 2011, when the protests succeeded in making Tunisia a pioneer of Arab democracy and ended Ben Ali’s reign, Yahyaoi got her passport back and went home, immediately.

Back in Tunisia with newfound freedom, she had an agenda: To hold the governing agency charged with writing a new Tunisian constitution accountable.

Yahyaoui built Al Bawsala, translated as The Compass, an NGO focused on transparency and government accountability. Al Bawsala became one of the largest NGOs in the Middle East, a bona fide success that attracted numerous awards and cemented Yahyaoui’s status as a fearless advocate for human rights, a freedom fighter and one of the most influential Arab women in the world.

“I had to work probably 10 times harder to get to be the self-educated me I am today,” she said. “I saw way too many people getting their education refused and therefore their future ruined.”

Her global standing earned her a seat on the board of the United Nation’s High Commissioner For Refugees Advisory Group on Gender, Forced Displacement, and Protection, as well as the title of Young Global Leader at the World Economic Forum and co-chair of the Davos Conference in 2016, a title she shard with Microsoft’s Satya Nadella and GM’s Mary Barra .

Three years later, with a resume enviable to any dignitary, Yahyaoui is leveraging her unique experience to lure in venture capitalists and use their cash for good.

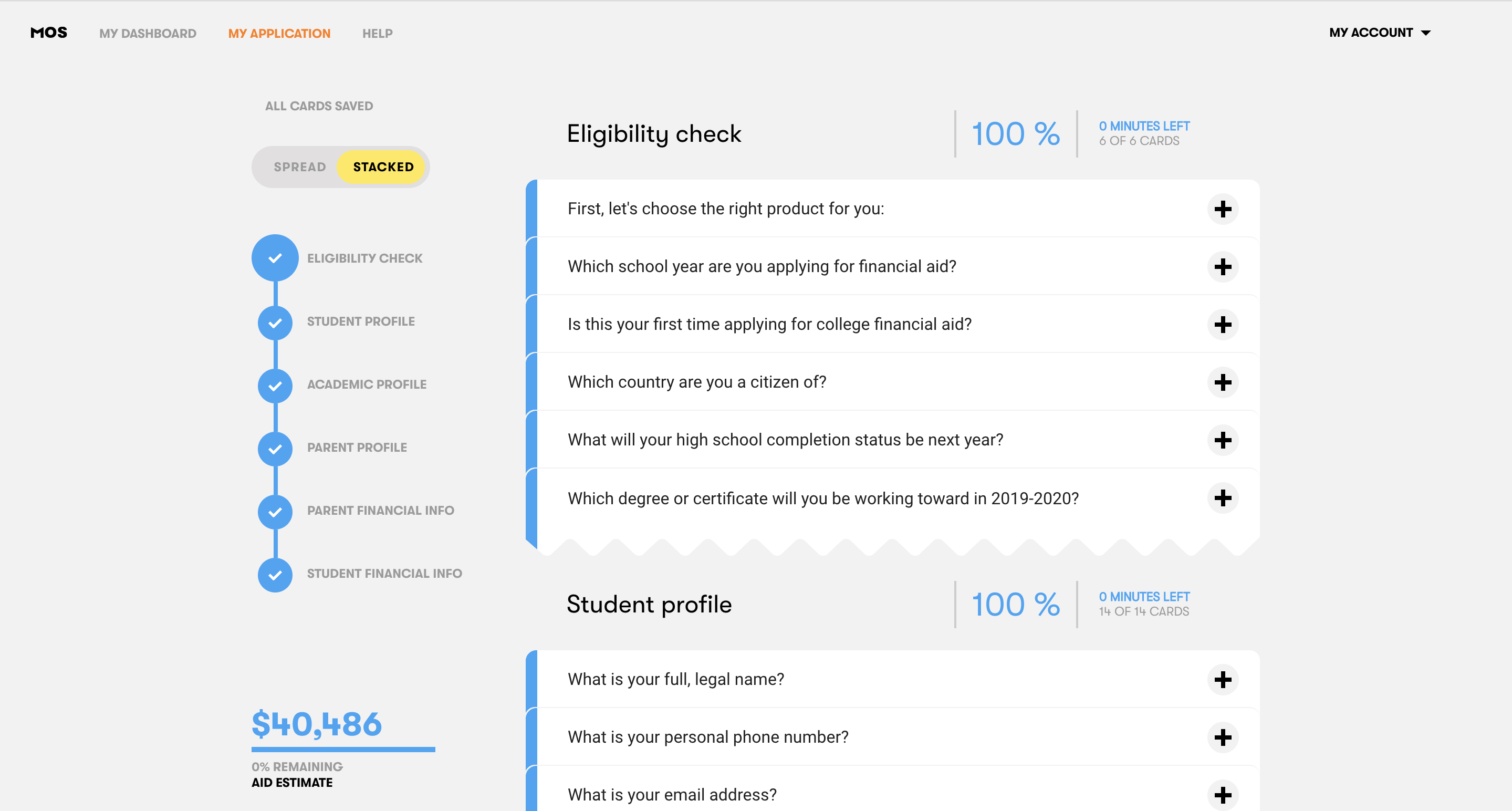

The Mos dashboard.

Mos is like if Turbo Tax married Typeform and had a baby, Yahyaoui explained. Not dissimilar to Common App, Mos lets students apply to more than 500 federal and state-based aid programs in minutes using a survey that matches them to every grant and scholarship program they qualify for, while simultaneously completing the FAFSA and state aid applications. To ensure every family is getting the most financial support possible, a Mos financial aid advisor reviews each case and negotiates with colleges for higher awards.

“Today, the biggest problem is people think they are not eligible for financial aid just because of how the thing is designed,” Yahyaoui said. “You’re supposed to just go ahead and fill a form that has 200 questions and then send it like a bottle in the sea and wait for months.”

Mos will complete a full-scale launch this summer and eventually tackle other nation’s college financial aid systems thanks to the new infusion of capital and the high-profile relationships Yahyaoui has forged in just one year living in the Bay Area.

Ultimately, it was Yahyaoui’s activism that granted her a ticket into the opaque world of Silicon Valley VC. As it turns out, angel investor Khaled Helioui, a fellow Tunisian immigrant in tech, was familiar with Yahyaoui’s work and when he heard she had relocated to the Bay Area to launch a technology startup, he wanted to know exactly what she was building. Today, he’s a Mos investor and board member and it was his introductions that helped Yahyaoui quickly and skillfully close her seed round.

An early angel investor in Uber, Helioui connected Yahyaoui with his friend Garrett Camp, the very wealthy co-founder and chairman of the ride-hailing giant, who was sold on Mos’s mission right off the bat.

“I think because Garrett is an immigrant, he knows what it is to suffer with bureaucracy,” Yahyaoui said. “He was a huge believer. He actually made it so easy for me because he said, okay, here’s an office, just stay and work.”

She was then introduced to John Doerr, the chairman of the esteemed VC firm Kleiner Perkins, known for his successful bets on companies like Google and Amazon. With Camp and Doerr on board, Mos didn’t struggle to raise additional capital; in fact, Yahyaoui was in an unusual position of being able to reject investors whose values and vision for Mos clearly didn’t align with hers.

Yahyaoui, center, with the Mos team in San Francisco.

Yahyaoui isn’t in the startup business to get rich off students trying to navigate their way through the absorbently expensive process of applying to and attending college. She’s part of a growing class of founders out to prove that you can pair profits with good morals and lead venture-backed values-based businesses.

“I know if I created the same thing as an NGO, I could have already raised $100 million, but I like the accountability of business,” she said. “We can create businesses that are good for people.”

Yahyaoui’s story, from being exiled from her home country at a young age to fighting an authoritarian regime is not one that’s ever been told before in Silicon Valley.

In addition to being a trailblazing human rights advocate, she’s a woman, an immigrant, “uneducated” by Silicon Valley standards and a first-time tech founder that was able to walk into a meeting with John Doerr and walk out with a term sheet.

If she’s successful in building a global edtech business, she’ll be emblematic of the meritocratic culture The Valley has falsely claimed to uphold. Even if she’s not successful, she’ll have torn down barriers for other underrepresented founders and written a success story fitting for this new era of accountability in tech.

Powered by WPeMatico

The San Francisco-based startup Branch International, which makes small personal loans in emerging markets, has raised $170 million and announced a partnership with Visa to offer virtual, pre-paid debit cards to Branch client networks in Africa, South-Asia and Latin America.

Branch — which has 150 employees in San Francisco, Lagos, Nairobi, Mexico City and Mumbai — makes loans starting at $2 to individuals in emerging and frontier markets. The company also uses an algorithmic model to determine credit worthiness, build credit profiles and offer liquidity via mobile phones.

“We’ll use [the money] to deepen existing business in Africa. Later this year we’ll announce high-yield savings accounts…in Africa,” says Branch co-founder and chief executive Matt Flannery.

The $170 million round from Foundation Capital and its new debit card partner, Visa, will support Branch’s international expansion, which could include Brazil and Indonesia, according to Flannery. Branch launched in Mexico and India within the last year. In Africa, it offers its services in Kenya, Nigeria and Tanzania.

A potential Branch customer

The Branch-Visa partnership will allow individuals to obtain virtual Visa accounts with which to create accounts on Branch’s app. This gives Branch larger reach in countries such as Nigeria — Africa’s most populous country with 190 million people — where cards have factored more prominently than mobile money in connecting unbanked and underbanked populations to finance.

Founded in 2015, Branch started operating in Kenya, where mobile money payment products such as Safaricom’s M-Pesa (which does not require a card or bank account to use) have scaled significantly. M-Pesa now has 25 million users, according to sector stats released by the Communications Authority of Kenya. Branch has more than 3 million customers and has processed 13 million loans and disbursed more than $350 million, according to company stats.

Branch has one of the most downloaded fintech apps in Africa, per Google Play app numbers combined for Nigeria and Kenya, according to Flannery.

Already profitable, Branch International expects to reach $100 million in revenues this year, with roughly 70 percent of that generated in Africa, according to Flannery.

In addition to Visa and Foundation Capital, the $170 Series C round included participation from Branch’s existing investors Andreessen Horowitz, Trinity Ventures, Formation 8, the IFC, CreditEase and Victory Park, while adding new investors Greenspring, Foxhaven and B Capital.

Branch last raised $70 million in 2018. The company’s overall VC haul and $100 million revenue peg register as pretty big numbers for a startup focused primarily on Africa. Pan-African e-commerce startup Jumia, which also announced its NYSE IPO last month, generated $140 million in revenue (without profitability) in 2018.

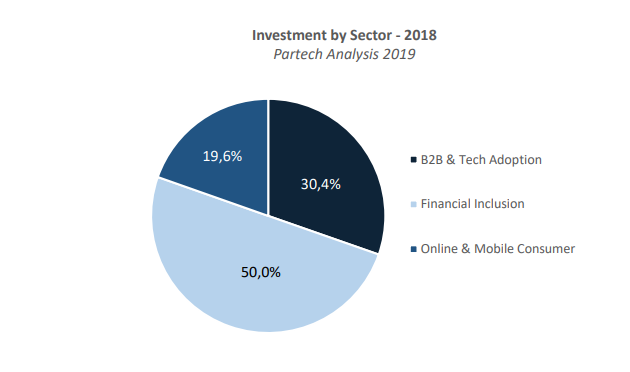

Startups building financial technologies for Africa’s 1.2 billion population have gained the attention of investors. As a sector, fintech (or financial inclusion) attracted 50 percent of the estimated $1.1 billion funding to African startups in 2018, according to Partech.

Startups building financial technologies for Africa’s 1.2 billion population have gained the attention of investors. As a sector, fintech (or financial inclusion) attracted 50 percent of the estimated $1.1 billion funding to African startups in 2018, according to Partech.

Branch’s recent round and plans to add countries internationally also tracks a trend of fintech-related products growing in Africa, then expanding outward. This includes M-Pesa, which generated big numbers in Kenya before operating in 10 countries around the world. Nigerian payments startup Paga announced its pending expansion in Asia and Mexico late last year. And payment services such as Kenya’s SimbaPay have also connected to global networks like China’s WeChat.

Powered by WPeMatico

There are a lot of people who never thought they’d see the day venture capitalists would funnel millions into femtech businesses, direct-to-consumer tampon retailers no less. But that’s our new reality and Cora is proof.

San Francisco-based Cora, which develops and sells organic tampons, pads and other personal care products, has just closed a $7.5 million Series A led by Harbinger Ventures. Cora is one of many femtech startups to raise funding this week alone, in what is turning out to be a red-hot year for VC investment in the space.

Femtech, defined as any software, diagnostics, products and services that leverage technology to improve women’s health, has attracted at least $241 million in VC funding so far this year, according to PitchBook. That puts the sector on pace to secure nearly $1 billion in investment by year-end, greatly surpassing last year’s record of $650 million. For more historical context, startups in the space brought in only $62 million in 2012, $225 million in 2014 and $231 million in 2016.

“Investors have realized there is a huge pent-up demand in the market for healthier products for women,” Cora co-founder Molly Hayward tells TechCrunch. “The way in which the VC world is structured, there just has not been a lot of representation. It’s really difficult to understand the value of a product you aren’t ever going to use or to understand a problem you aren’t ever going to have, particularly around period care. This isn’t something we were talking about as a society five years ago.”

The four-year-old startup operates a little differently than your run-of-the-mill D2C company. Like TOMS, the popular footwear brand, Cora donates a month’s supply of products for every month’s supply sold. To date, Cora has donated 5 million pads to girls in India and Kenya and 100,000 products to women in the U.S.

“To me, [Cora] was this incredible, holistic opportunity to change the way that women experience their period,” Hayward said.

Investors must be excited about Cora’s growth. Though she didn’t disclose specific numbers, Hayward says the brand has expanded 400 percent year-over-year, a metric they are expecting to sustain with this new bout of funding. Cora’s products are sold on a subscription basis, with prices ranging from $8 per month for six tampons to $16 per month for 24. For those unfamiliar with the costs of such products, $8 for six tampons comes at quite the premium. A box of 50 Playtex tampons, for example, retails for around $9.

Investors must be excited about Cora’s growth. Though she didn’t disclose specific numbers, Hayward says the brand has expanded 400 percent year-over-year, a metric they are expecting to sustain with this new bout of funding. Cora’s products are sold on a subscription basis, with prices ranging from $8 per month for six tampons to $16 per month for 24. For those unfamiliar with the costs of such products, $8 for six tampons comes at quite the premium. A box of 50 Playtex tampons, for example, retails for around $9.

In Cora’s case, customers are shelling out extra cash for millennial-inspired branding, a soothing unboxing experience and a general ease of access to its products, as well as Cora’s organic, hypoallergenic and compostable materials, which aren’t characteristic of many similar products on the market.

Cora plans to use the capital to put more of its items in Target stores, where it already sells its tampons and pads, and expand its portfolio of products. As part of the funding, Cora has added two more women to its board of directors: Lisa Bougie, the former GM of Stitch Fix, and Andrea Freedman, the former chief financial officer of Method. Its board is now 80 percent female.

Powered by WPeMatico

Amid calls for a dozen different global cities to replace Silicon Valley — Austin, Beijing, London, New York — nobody has yet nominated “nowhere.” But it’s now a possibility.

There are two trends to unpack here. The first is startups that are fully, or almost fully, remote, with employees distributed around the world. There’s a growing list of significant companies in this category: Automattic, Buffer, GitLab, Invision, Toptal and Zapier all have from 100 to nearly 1,000 remote employees.

The second trend is nomadic founders with no fixed location. For a generation of founders, moving to Silicon Valley was de rigueur. Later, the emergence of accelerators and investors worldwide allowed a wider range of potential home bases. But now there’s a third wave: a culture of traveling with its own, growing support networks and best practices.

You don’t have to look far to find startup gurus and VCs who strongly advise against being remote, much less a nomad. The basic reasoning is simple: Not having a location doesn’t add anything, so why do it? Startups are fragile, so it’s best to avoid any work practice that could disrupt delicate growth cycles.

Powered by WPeMatico

Two years ago, former Amazon product manager Xiao Wang stood on the stage at TechCrunch Disrupt San Francisco and made the case for a platform meant to help couples apply for marriage green cards, a complex process made worse by bureaucracy and red tape.

Called Boundless, the startup had spun out of Seattle startup studio Pioneer Square Labs and raised a $3.5 million seed round. Now, Foundry Group’s Brad Feld has led a $7.8 million Series A in the startup, with participation from existing investors Trilogy Equity Partners, PSL, Two Sigma Ventures and Founders’ Co-Op.

“Families have really only had two choices, they could spend weeks or months trying to figure this out on their own, or they can spend thousands and thousands of dollars on an immigration attorney,” Wang, Boundless co-founder and chief executive officer, told TechCrunch. “What we are trying to do is basically give everyone access to the information, the tools and the support that was previously only available to those that could afford high-priced attorneys.”

Boundless charges $750 for its online green card application support services, which includes ensuring families correctly complete applications and have access to an immigration lawyer to review those applications. The fee comes at a major discount to the costs of an immigration lawyer and streamlines a process that can be delayed months when errors are made. The startup also offers a recently launched $395 naturalization product meant to assist eligible green card holders with their U.S. citizenship applications.

Wang founded Boundless in 2017 after helping build Amazon Go, the e-commerce giant’s line of cashierless convenience stores. Wang is an immigrant, having relocated to the U.S. from China when he was a child.

“We spent almost five months of rent money on an immigration attorney because the stakes were so high and we only had one shot,” Wang said. “We wanted to make sure we were doing it right. This is a story that is echoed by millions of families every year; this is such an important part of them starting a new life in a new country.”

Wang, after three years at Amazon, realized he could use his technology background and data prowess to build an information platform supportive of these millions of families.

“This is exactly what tech and data is meant to do,” he said. “I believe there is a moral obligation for tech to be used in meaningfully improving people’s lives.”

Boundless plans to use this investment to expand its team and product offerings, as well as build out its content library, which Wang said is rapidly becoming the go-to place for immigrants navigating the legal labyrinth that is the U.S. green card and citizenship process. Its resources page, which includes straightforward guides, a number of forms and more, counts 300,000 unique visitors per month.

“We hold their hand through the entire process,” Wang said. “We want to be the single source of information and tools for all family-based immigration.”

Wang and his team also hope to shine a brighter light on immigration policy. In late 2018, as part of its effort to be louder advocates for immigrants, Boundless, alongside Warby Parker, Foursquare, Foundation Capital and more, published an open letter to the U.S. Department of Homeland Security opposing its proposed “public charge” immigration regulation, which would allow for non-citizens who are in the country legally to be denied a visa or a green card if they have a medical condition, financial liabilities and other disqualifiers.

“The stakes for making sure your application is correct have never been higher; the government has far more leeway to be able to deny applications,” Wang said. “While we can’t speed up the government processing times, we can make meaningful improvements to helping families gather all the materials they need to send in the right information.”

Powered by WPeMatico

Ouster has raised $60 million as the San Francisco-based lidar startup opens a new facility that will have the capacity to assemble and ship several thousand sensors a month by the end of 2019.

The new factory, which will have a grand opening ceremony March 28, currently produces hundreds of sensors per month. Ouster says at full capacity, the factory will produce $25 million to $50 million in inventory per month.

Lidar measures distance using laser light to generate highly accurate 3D maps of the world around the car. It’s considered by most in the self-driving car industry a key piece of technology required to safely deploy robotaxis and other autonomous vehicles (although not everyone agrees). However, the sensors are also useful in other industries — and this is where Ouster’s business model is targeted.

Ouster has cast a wider net for customers than some of its rivals. Unlike others vying solely for automotive customers working on the development of autonomous vehicles, Ouster is selling sensors to other industries. Ouster is selling its light detection and ranging radar sensors to robotics, drones, mapping, defense, building security, mining and agriculture companies.

The strategy has appeared to pay off. Ouster says it has 400 customers from 15 industries.

The $60 million in additional funding follows a Series A raise of $27 million announced back in 2017 as Ouster came out of stealth mode. In the years since, the company led by Angus Pacala has grown to more than 100 employees and announced four lidar sensors, with resolutions from 16 to 128 channels, and two product lines, the OS-1 and OS-2. The startup expects to nearly double its headcount in the coming year to support further product line development.

The $60 million in equity and debt funding includes investments from Runway Growth Capital and Silicon Valley Bank, as well as additional funding from Series A participants Cox Enterprises, Constellation Tech Ventures, Fontinalis Partners, Carthona and others.

Ouster said the additional investment has helped to develop Ouster’s product lines, including the launch of the OS-1 128 lidar sensor, and fund the expansion of its production facilities.

The company also announced the appointment of Susan Heystee, senior VP for OEM business at Verizon Connect, to its board of directors.

Waymo, the self-driving car company under Google’s Alphabet, could be a new competitor to the company. Waymo announced this month it will start selling its custom lidar sensors to companies outside of self-driving cars. Waymo will initially target robotics, security and agricultural technology. The sales will help the company scale its autonomous technology faster, making each sensor more affordable through economies of scale, Simon Verghese, head of Waymo’s lidar team, wrote in a Medium post at the time.

Powered by WPeMatico

One year after a $38 million Series B valued on-demand aviation startup Blade at $140 million, the company has begun taxiing the Bay Area’s elite.

As part of a new pilot program, Blade has given 200 people in San Francisco and Silicon Valley exclusive access to its mobile app, allowing them to book helicopters, private jets and even seaplanes at a moments notice for $200 per seat, at least.

Blade, backed by Lerer Hippeau, Airbus, former Google CEO Eric Schmidt and others, currently flies passengers around the New York City area, where it’s headquartered, offering the region’s wealthy $800 flights to the Hamptons, among other flights at various price points. According to Business Insider, it has worked with Uber in the past to help deep-pocketed Coachella attendees fly to and from the Van Nuys Airport to Palm Springs, renting out six-seat helicopters for more than $4,000 a pop.

Its latest pilot seems to target business travelers, connecting riders to the San Francisco International Airport and Oakland International Airport to Palo Alto, San Jose, Monterey and Napa Valley. The goal is to shorten trips made excruciatingly long due to bad traffic in major cities like New York, Los Angeles and San Francisco. Recently, the startup partnered with American Airlines to better establish its network of helicopters, a big step for the company as it works to integrate with existing transportation infrastructure.

New work with @flybladenow pic.twitter.com/eONvKU3rhM

— Tyler Babin (@Tyler_Babin) March 11, 2019

Blade, led by founder and chief executive officer Rob Wiesenthal, a former Warner Music Group executive, has raised about $50 million in venture capital funding to date. To launch at scale and, ultimately, to compete with the likes of soon-to-be-public transportation behemoth Uber, it will have to land a lot more investment support.

Uber too has lofty plans to develop a consumer aerial ridesharing business, as do several other privately-funded startups. Called UberAIR, Uber will offer short-term shareable flights to commuters as soon as 2023. The company has raised billions of dollars to turn this sci-fi concept into reality.

Then there’s Kitty Hawk, a company launched by former Google vice president and Udacity co-founder Sebastian Thrun, which is developing an aircraft that can take off like a helicopter but fly like a plane for short-term urban transportation purposes. Others in the air taxi or vertical take-off and landing aircraft space, including Volocopter, Lilium and Joby Aviation, have raised tens of millions to eliminate traffic congestion or, rather, to chauffer the rich.

Blade’s next stop is India, the Financial Times reports, where it will conduct a pilot connecting travelers in downtown Mumbai and Pune. The company tells TechCrunch they are currently exploring one additional domestic pilot and one additional international pilot.

Powered by WPeMatico

As I’m sure everyone reading this knows, female-founded businesses receive just over 2 percent of venture capital on an annual basis. Most of those checks are written to early-stage startups. It’s extremely difficult for female founders to garner late-stage support, let alone cash $100 million checks.

Maybe that’s finally changing. This week, not one but two female-founded and led companies, Glossier and Rent The Runway, raised nine-figure rounds and cemented their status as unicorn companies. According to PitchBook data from 2018, there are only about 15 unicorn startups with female founders. Though I’m sure that number has increased in the last year, you get the point: There are hundreds of privately held billion-dollar companies and shockingly few of those have women founders (even fewer have female CEOs)…

Moving on…

I spent a good part of the week at San Francisco’s Pier 48 in a room full of vest-wearing investors. We listened to some 200 YC companies make their 120-second pitch and though it was a bit of a whirlwind, there were definitely some standouts. ICYMI: We wrote about each and every company that pitched on day 1 and day 2. If you’re looking for the inside scoop on the companies that forwent demo day and raised rounds, or were acquired, before hitting the stage, we’ve got that too.

Lyft: This week, Lyft set the terms for its highly-anticipated initial public offering, expected to be completed next week. The company will charge between $62 and $68 per share, raising more than $2 billion at a valuation of ~$23 billion. We previously reported its initial market cap would be around $18.5 billion, but that was before we knew that Lyft’s IPO was already oversubscribed. Here’s a little more background on the Lyft IPO for those interested.

Uber: The global ride-hailing business flew a little more under the radar this week than last week, but still managed to grab a few headlines. The company has decided to sell its stock on the New York Stock Exchange, which is the least surprising IPO development of 2019, considering its key U.S. competitor, Lyft, has been working with the Nasdaq on its IPO. Uber is expected to unveil its S-1 in April.

Ben Silbermann, co-founder and CEO of Pinterest, at TechCrunch Disrupt SF 2017.

Pinterest: Pinterest, the nearly decade-old visual search engine, unveiled its S-1 on Friday, one of the final steps ahead of its NYSE IPO, expected in April. The $12.3 billion company, which will trade under the ticker symbol “PINS,” posted revenue of $755.9 million in the year ending December 31, 2018, up from $472.8 million in 2017. It has roughly doubled its monthly active user count since early 2016, hitting 265 million last year. The company’s net loss, meanwhile, shrank to $62.9 million in 2018 from $130 million in 2017.

Zoom: Not necessarily the buzziest of companies, but its S-1 filing, published Friday, stands out for one important reason: Zoom is profitable! I know, what insanity! Anyway, the startup is going public on the Nasdaq as soon as next month after raising about $150 million in venture capital funding. The full deets are here.

General Catalyst, a well-known venture capital firm, is diving more seriously into the business of funding seed-stage business. The firm, which has investments in Warby Parker, Oscar and Stripe, announced earlier this week its plan to invest at least $25 million each year in nascent teams.

Earlier this week, Opendoor, the SoftBank -backed real estate startup, filed paperwork to raise even more money. According to TechCrunch’s Ingrid Lunden, the business is planning to raise up to $200 million at a valuation of roughly $3.7 billion. It’s possible this is a Series E extension; after all, the company raised its $400 million Series E only six months ago. Backers of OpenDoor include the usual suspects: Andreessen Horowitz, Coatue, General Atlantic, GV, Initialized Capital, Khosla Ventures, NEA and Norwest Venture Partners.

Startup capital

Backstage Capital founder and managing partner Arlan Hamilton, center.

Axios’ Dan Primack and Kia Kokalitcheva published a report this week revealing Backstage Capital hadn’t raised its debut fund in total. Backstage founder Arlan Hamilton was quick to point out that she had been honest about the challenges of fundraising during various speaking engagements, and even on the Gimlet “Startup” podcast, which featured her in its latest season. A Twitter debate ensued and later, Hamilton announced she was stepping down as CEO of Backstage Studio, the operations arm of the venture fund, to focus on raising capital and amplifying founders. TechCrunch’s Megan Rose Dickey has the full story.

This week, TechCrunch’s Connie Loizos revisited a long-held debate: Pro rata rights, or the right of an earlier investor in a company to maintain the percentage that he or she (or their venture firm) owns as that company matures and takes on more funding. Here’s why pro rata rights matter (at least, to VCs).

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about Glossier, Rent The Runway and YC Demo Days. Then, in a special Equity Shot, we unpack the numbers behind the Pinterest and Zoom IPO filings.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico

Hundreds gathered this week at San Francisco’s Pier 48 to see the more than 200 companies in Y Combinator’s Winter 2019 cohort present their two-minute pitches. The audience of venture capitalists, who collectively manage hundreds of billions of dollars, noted their favorites. The very best investors, however, had already had their pick of the litter.

What many don’t realize about the Demo Day tradition is that pitching isn’t a requirement; in fact, some YC graduates skip out on their stage opportunity altogether. Why? Because they’ve already raised capital or are in the final stages of closing a deal.

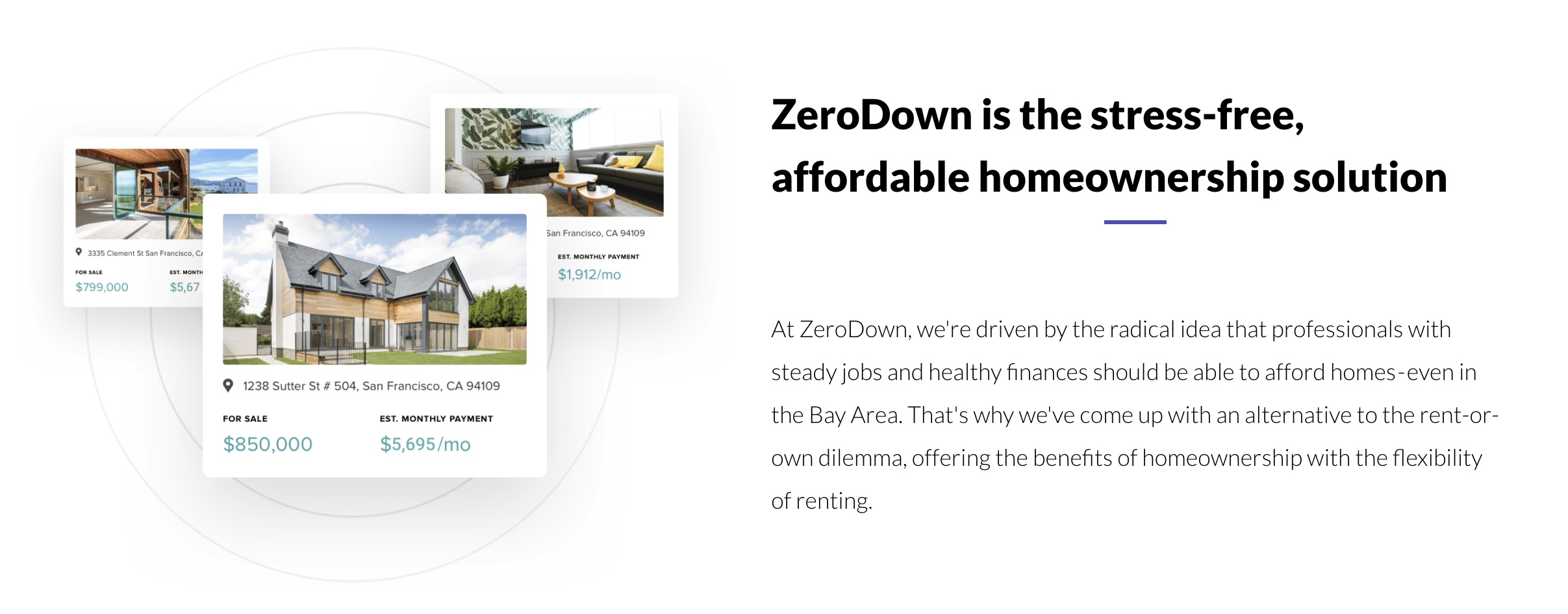

ZeroDown, Overview.AI and Catch are among the startups in YC’s W19 batch that forwent Demo Day this week, having already pocketed venture capital. ZeroDown, a financing solution for real estate purchases in the Bay Area, raised a round upwards of $10 million at a $75 million valuation, sources tell TechCrunch. ZeroDown hasn’t responded to requests for comment, nor has its rumored lead investor: Goodwater Capital.

Without requiring a down payment, ZeroDown purchases homes outright for customers and helps them work toward ownership with monthly payments determined by their income. The business was founded by Zenefits co-founder and former chief technology officer Laks Srini, former Zenefits chief operating officer Abhijeet Dwivedi and Hari Viswanathan, a former Zenefits staff engineer.

The founders’ experience building Zenefits, despite its shortcomings, helped ZeroDown garner significant buzz ahead of Demo Day. Sources tell TechCrunch the startup had actually raised a small seed round ahead of YC from former YC president Sam Altman, who recently stepped down from the role to focus on OpenAI, an AI research organization. Altman is said to have encouraged ZeroDown to complete the respected Silicon Valley accelerator program, which, if nothing else, grants its companies a priceless network with which no other incubator or accelerator can compete.

Overview .AI’s founders’ resumes are impressive, too. Russell Nibbelink and Christopher Van Dyke were previously engineers at Salesforce and Tesla, respectively. An industrial automation startup, Overview is developing a smart camera capable of learning a machine’s routine to detect deviations, crashes or anomalies. TechCrunch hasn’t been able to get in touch with Overview’s team or pinpoint the size of its seed round, though sources confirm it skipped Demo Day because of a deal.

Catch, for its part, closed a $5.1 million seed round co-led by Khosla Ventures, NYCA Partners and Steve Jang prior to Demo Day. Instead of pitching their health insurance platform at the big event, Catch published a blog post announcing its first feature, The Catch Health Explorer.

“This is only the first glimpse of what we’re building this year,” Catch wrote in the blog post. “In a few months, we’ll be bringing end-to-end health insurance enrollment for individual plans into Catch to provide the best health insurance enrollment experience in the country.”

TechCrunch has more details on the healthtech startup’s funding, which included participation from Kleiner Perkins, the Urban Innovation Fund and the Graduate Fund.

Four more startups, Truora, Middesk, Glide and FlockJay had deals in the final stages when they walked onto the Demo Day stage, deciding to make their pitches rather than skip the big finale. Sources tell TechCrunch that renowned venture capital firm Accel invested in both Truora and Middesk, among other YC W19 graduates. Truora offers fast, reliable and affordable background checks for the Latin America market, while Middesk does due diligence for businesses to help them conduct risk and compliance assessments on customers.

Finally, Glide, which allows users to quickly and easily create well-designed mobile apps from Google Sheets pages, landed support from First Round Capital, and FlockJay, the operator an online sales academy that teaches job seekers from underrepresented backgrounds the skills and training they need to pursue a career in tech sales, secured investment from Lightspeed Venture Partners, according to sources familiar with the deal.

Raising ahead of Demo Day isn’t a new phenomenon. Companies, thanks to the invaluable YC network, increase their chances at raising, as well as their valuation, the moment they enroll in the accelerator. They can begin chatting with VCs when they see fit, and they’re encouraged to mingle with YC alumni, a process that can result in pre-Demo Day acquisitions.

This year, Elph, a blockchain infrastructure startup, was bought by Brex, a buzzworthy fintech unicorn that itself graduated from YC only two years ago. The deal closed just one week before Demo Day. Brex’s head of engineering, Cosmin Nicolaescu, tells TechCrunch the Elph five-person team — including co-founders Ritik Malhotra and Tanooj Luthra, who previously founded the Box-acquired startup Steem — were being eyed by several larger companies as Brex negotiated the deal.

“For me, it was important to get them before batch day because that opens the floodgates,” Nicolaescu told TechCrunch. “The reason why I really liked them is they are very entrepreneurial, which aligns with what we want to do. Each of our products is really like its own business.”

Of course, Brex offers a credit card for startups and has no plans to dabble with blockchain or cryptocurrency. The Elph team, rather, will bring their infrastructure security know-how to Brex, helping the $1.1 billion company build its next product, a credit card for large enterprises. Brex declined to disclose the terms of its acquisition.

Y Combinator partners Michael Seibel and Dalton Caldwell, and moderator Josh Constine, speak onstage during TechCrunch Disrupt SF 2018. (Photo by Kimberly White/Getty Images)

Ultimately, it’s up to startups to determine the cost at which they’ll give up equity. YC companies raise capital under the SAFE model, or a simple agreement for future equity, a form of fundraising invented by YC. Basically, an investor makes a cash investment in a YC startup, then receives company stock at a later date, typically upon a Series A or post-seed deal. YC made the switch from investing in startups on a pre-money safe basis to a post-money safe in 2018 to make cap table math easier for founders.

Michael Seibel, the chief executive officer of YC, says the accelerator works with each startup to develop a personalized fundraising plan. The businesses that raise at valuations north of $10 million, he explained, do so because of high demand.

“Each company decides on the amount of money they want to raise, the valuation they want to raise at, and when they want to start fundraising,” Seibel told TechCrunch via email. “YC is only an advisor and does not dictate how our companies operate. The vast majority of companies complete fundraising in the 1 to 2 months after Demo Day. According to our data, there is little correlation between the companies who are most in demand on Demo Day and ones who go on to become extremely successful. Our advice to founders is not to over optimize the fundraising process.”

Though Seibel says the majority raise in the months following Demo Day, it seems the very best investors know to be proactive about reviewing and investing in the batch before the big event.

Khosla Ventures, like other top VC firms, meets with YC companies as early as possible, partner Kristina Simmons tells TechCrunch, even scheduling interviews with companies in the period between when a startup is accepted to YC to before they actually begin the program. Another Khosla partner, Evan Moore, echoed Seibel’s statement, claiming there isn’t a correlation between the future unicorns and those that raise capital ahead of Demo Day. Moore is a co-founder of DoorDash, a YC graduate now worth $7.1 billion. DoorDash closed its first round of capital in the weeks following Demo Day.

“I think a lot of the activity before demo day is driven by investor FOMO,” Moore wrote in an email to TechCrunch. “I’ve had investors ask me how to get into a company without even knowing what the company does! I mostly see this as a side effect of a good thing: YC has helped tip the scale toward founders by creating an environment where investors compete. This dynamic isn’t what many investors are used to, so every batch some complain about valuations and how easy the founders have it, but making it easier for ambitious entrepreneurs to get funding and pursue their vision is a good thing for the economy.”

This year, given the number of recent changes at YC — namely the size of its latest batch — there was added pressure on the accelerator to showcase its best group yet. And while some did tell TechCrunch they were especially impressed with the lineup, others indeed expressed frustration with valuations.

Many YC startups are fundraising at valuations at or higher than $10 million. For context, that’s actually perfectly in line with the median seed-stage valuation in 2018. According to PitchBook, U.S. startups raised seed rounds at a median post-valuation of $10 million last year; so far this year, companies are raising seed rounds at a slightly higher post-valuation of $11 million. With that said, many of the startups in YC’s cohorts are not as mature as the average seed-stage company. Per PitchBook, a company can be several years of age before it secures its seed round.

I did not talk to a single company in this batch raising under $10M post (admittedly I only was able to speak with a fraction of the 205).

— Peter Rojas (@peterrojas) March 20, 2019

Nonetheless, pricey deals can come as a disappointment to the seed investors who find themselves at YC every year but because their reputations aren’t as lofty as say, Accel, aren’t able to book pre-Demo Day meetings with YC’s top of class.

The question is who is Y Combinator serving? And the answer is founders, not investors. YC is under no obligation to serve up deals of a certain valuation nor is it responsible for which investors gain access to its best companies at what time. After all, startups are raking in larger and larger rounds, earlier in their lifespans; shouldn’t YC, a microcosm for the Silicon Valley startup ecosystem, advise their startups to charge the best investors the going rate?

Powered by WPeMatico

Deloitte’s Technology, Media and Telecommunications division published its 13th-annual Digital Media Trends survey, focused on identifying changes in the ways US consumers engage with various types of media.

Led by an independent research firm, the survey had roughly 2,000 consumer respondents across demographics – with the report categorizing respondents based on age (Gen-Z: ages 14-21, Millenials: 22-35, Gen-X: 36-52, Boomers: 53-71, and Matures: 72+).

While already accompanied by a succinct 13-page executive summary, the report can largely be summarized in just a couple of sentences: more people are using streaming or alternative media services than ever before, largely due to more user freedom and customization, though the growing quantity and fragmentation of platforms are becoming more frustrating for users to manage.

The survey results directionally echo already well-discussed dynamics, which we’ve previously dug into such as here, here and here. Instead, the most poignant aspects of the report were not the answers or conclusions themselves, but the immense level of support many of them received.

Powered by WPeMatico