Safaricom

Auto Added by WPeMatico

Auto Added by WPeMatico

The economic effects of COVID-19 could delay Africa’s next big IPO — that of Nigerian fintech unicorn Interswitch.

If so, it wouldn’t be the first time the Lagos-based payments company’s plans for going public were postponed; the tech world has been anticipating Interswitch’s stock market debut since 2016.

For the continent’s innovation ecosystem, there’s a lot riding on the digital finance company’s IPO. After e-commerce venture Jumia, it would become only the second listing of a VC-backed African tech company on a major exchange. And Interswitch’s stock market debut — when it occurs — could bring more investor attention and less controversy to the region’s startup scene.

TechCrunch reached out to Interswitch on the window for listing, but the company declined to comment. The tech firm’s path from startup to IPO aspirant traces back to the vision of founder Mitchell Elegbe, a Nigerian electrical engineering graduate whose entire career has pretty much been Interswitch.

Africa’s tech scene is still fairly young, but it does have a timeline with several definitive points. An early one would be the success of mobile money in East Africa, with the launch of Safaricom’s M-Pesa in 2007. Another is the notable wave of VC-backed startups and founders that launched around 2010.

Interswitch CEO Mitchell Elegbe (Photo Credits: Interswitch)

With Interswtich, Elegbe pre-dated both by a number of years, founding his fintech company back in 2002 to connect Nigeria’s largely disconnected banking system. The firm became a pioneer of the infrastructure to digitize Nigeria’s economy.

Interswitch created the first electronic switch whereby Nigerian financial institutions could communicate and thereby operate ATMs and point of sales operations. The company now provides much of the rails for Nigeria’s online banking system.

Powered by WPeMatico

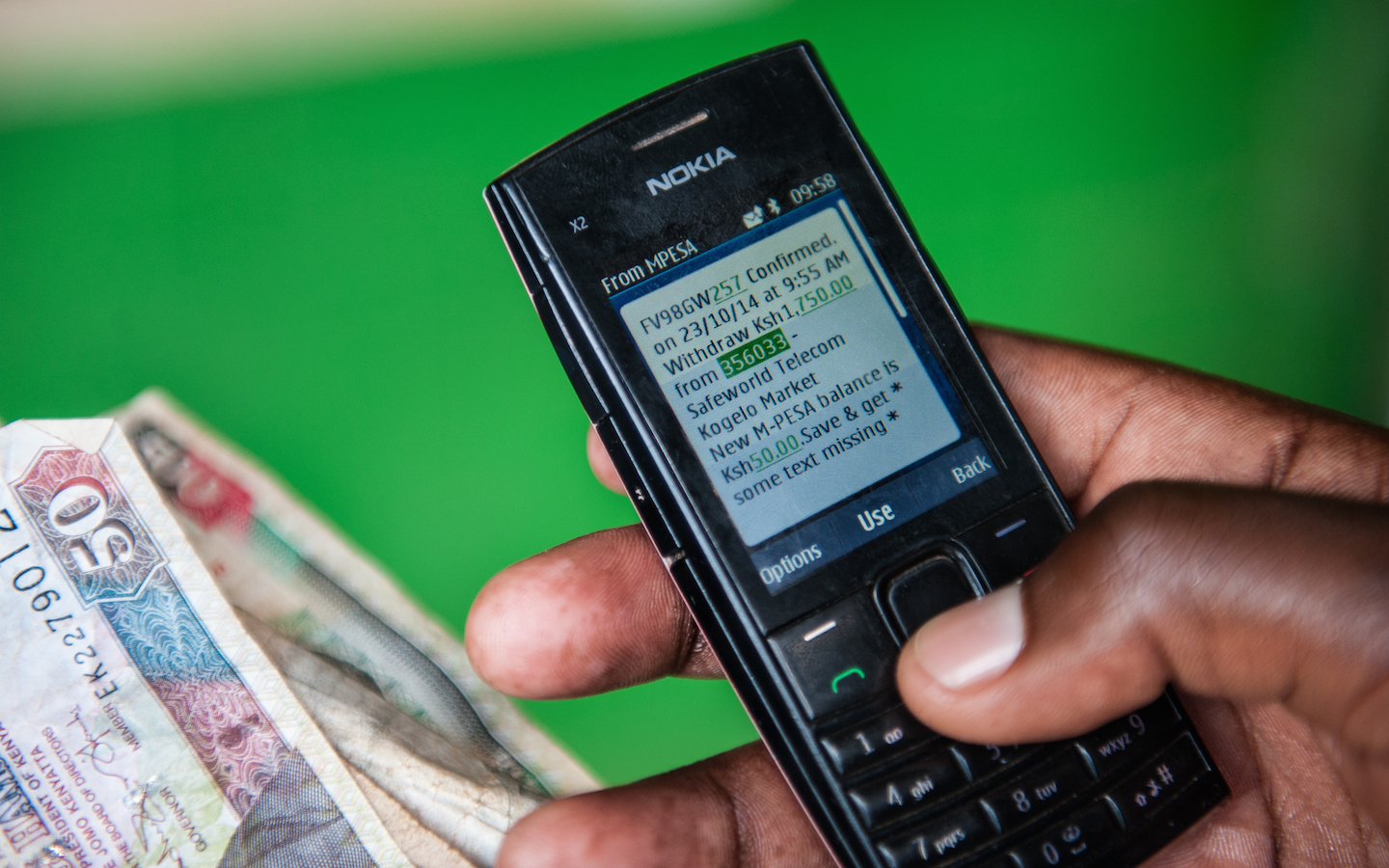

Kenya’s largest teleco, Safaricom, will implement a fee-waiver on East Africa’s leading mobile-money product, M-Pesa, to reduce the physical exchange of currency in response to the COVID-19 outbreak.

The company announced that all person-to-person (P2P) transactions under 1,000 Kenyan Schillings (≈ $10) would be free starting Tuesday for the next 90 days.

The move came after Safaricom met with the country’s Central Bank and per a directive from Kenya’s President Uhuru Kenyatta “to explore ways of deepening mobile-money usage to reduce risk of spreading the virus through physical handling of cash,” according to a release provided to TechCrunch from Safaricom.

To encourage the use of digital payments over cash, the East African telecom will also allow SMEs to increase their daily M-Pesa transaction limits from 70,000 Kenyan Schillings to 150,000 (≈ $700 to $1,500).

The measures represent the ability of the Kenyan government to use digital finance as a lever to influence social distancing and P2P transactions in an infectious health crisis.

M-Pesa has 20.5 million customers across a network of 176,000 agents and generates around one-fourth ($531 million) of Safaricom’s ≈ $2.2 billion annual revenues (2018). The company has held nearly 75% of the mobile-money market share in Kenya for nearly a decade and the country has the highest mobile-money usage rates in Africa.

In some respects, having all that output on one platform represents systemic risks to Kenya’s economy. But in the case of a global health pandemic spread by human contact, the dominance of mobile money in the country provides a policy tool to encourage digital versus physical contact on a wide scale through financial transactions.

Kenya has only three cases of COVID-19 (aka the coronavirus), according to Worldometer, but the country is taking cautionary measures. President Uhuru cancelled two foreign meetings due to the virus, the University of Nairobi shut down classes and a number of companies in the country are encouraging workers to telecommute, according to local sources and press reporting.

Powered by WPeMatico

In African fintech, the fourth quarter of 2019 brought big money to new entrants.

Chinese investors put $220 million into OPay and PalmPay — two fledgling startups with plans to scale in Nigeria and the broader continent. Several sources told me the big bucks had created anxiety for more than few payments ventures in Nigeria with similar strategies and smaller coffers. They may not need to fret just yet, however: lessons from Africa’s most successful mobile-money case study, M-Pesa, suggest that VC alone won’t buy scale in digital finance.

Over the last decade, Africa has been in the midst of a startup boom accompanied by big growth in VC and improvements in internet and mobile penetration.

Some definitive country centers for company formation, tech hubs and investment have emerged; Nigeria, South Africa and Kenya lead the continent in numbers for all those categories. Additional strong and emerging points for innovation and startups across Africa’s 54 countries and 1.2 billion people include Ghana, Tanzania, Ethiopia, and Senegal.

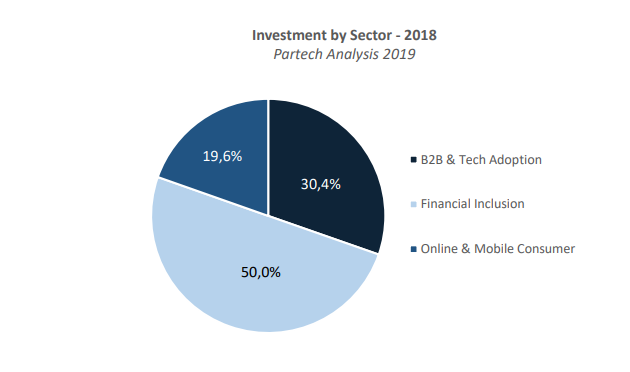

The continent surpassed $1 billion in VC to startups in 2018 and per research done by Partech and WeeTracker, fintech is the focus of the bulk of capital and deal-flow.

By several estimates, Africa is home to the largest share of the world’s unbanked and underbanked population.

This runs parallel to the region’s off-the-grid SME’s and economic activity — on display and in commercial motion through the street traders, roadside kiosks and open-air markets common from Nairobi to Lagos.

IMF estimates have pegged Africa’s informal economy as one of the largest in the world. Thousands of fintech startups have descended onto this large pool of unbanked and underbranked citizens and SMEs looking to grow digital finance products and market share.

In this race, the West African nation of Nigeria — home to Africa’s largest economy and population — is becoming an epicenter for VC. Many fintech-related companies are adopting a strategy of scaling there first before expanding outward.

That includes new entrants OPay and PalmPay, which raised so much capital in fourth quarter 2019. It’s notable that both were founded in 2019 and largely incubated by Chinese actors.

PalmPay, a consumer-oriented payments product, went live in November with a $40 million seed-round (one of the largest in Africa in 2019) led by Africa’s biggest mobile-phones seller — China’s Transsion. The startup was upfront about its ambitions, stating its goals to become “Africa’s largest financial services platform,” in a company statement.

![]() To that end, PalmPay conveniently entered a strategic partnership with its lead investor. The startup’s payment app will come pre-installed on Transsion’s mobile device brands, such as Tecno, in Africa — for an estimated reach of 20 million phones in 2020.

To that end, PalmPay conveniently entered a strategic partnership with its lead investor. The startup’s payment app will come pre-installed on Transsion’s mobile device brands, such as Tecno, in Africa — for an estimated reach of 20 million phones in 2020.

PalmPay also launched in Ghana in November and its U.K. and Africa-based CEO, Greg Reeve, confirmed plans to expand to additional African countries in 2020.

If PalmPay’s $40 million seed round got founders’ attention, OPay’s $120 million Series B created shock-waves, coming just months after the mobile-based fintech venture raised $50 million — making OPay’s $170 million capital haul equivalent to roughly a fifth of all VC raised in Africa in 2018.

Founded by Chinese owned consumer internet company Opera — and backed by 9 Chinese investors — OPay is the payment utility for a suite of Opera -developed internet based commercial products in Nigeria that include ride-hail apps ORide and OCar and food delivery service OFood.

With its latest Series A, OPay announced it would expand in Kenya, South Africa, and Ghana.

In Nigeria, OPay’s $170 million Series A and B announced in the span of months dwarfs just about anything raised by new and existing fintech players, with the exception of Interswitch.

The homegrown payments processing company — which pioneered much of Nigeria’s digital finance infrastructure — reached unicorn status in November when Visa took a reported $200 million minority stake in the venture.

A sampling of more common funding amounts for payments ventures in Nigeria includes established fintech company Paga’s $10 million Series B. Recent market entrant Chipper Cash’s May 2019 seed-round was $2.4 million.

There is a large disparity between fintech startups in Nigeria with capital raises in ones and tens of millions vs. OPay and PalmPay’s $40 and $120 million rounds. Conventional wisdom could be that the big-capital, big spending firms have an unmistakable advantage in scaling digital payments in Nigeria and other markets.

A look at Kenya’s M-Pesa may prove otherwise.

Powered by WPeMatico

When it comes to VC, vehicles, and startups, Africa’s ride-hail markets are becoming a multi-wheeled and global affair.

The big players such as Uber and Bolt are competing in Kampala and Nairobi—where in addition to car-service—they offer rickshaw taxis. On-demand motorcycle startups are multiplying and piloting EVs with funds from international partners. And many ride-hail companies in Africa are adapting unique product solutions to local transit needs.

In this analysis, I take a look at the leading startups in the mobility space and how the future of transportation on the continent will increasingly come from new entrants.

Africa’s in the midst of digital innovation boom, the components of which are intersecting rapidly across its 54 countries and 1.2 billion people.

Smartphone penetration is improving and in 2017, the continent saw the largest global increase in internet users—20 percent.

By Partech data, the continent surpassed the $1 billion VC mark in 2018. And greater connectivity and venture funding are fueling thousands of startups in every imaginable sector, including digital-transit.

While reliable markets stats for the size and potential of Africa’s ride-hail markets are sparse, there are some indicators of the sector’s potential.

Car ownership and cars per capita in Africa is among the lowest in the world. Parallel to that, any eyes and ears survey of the continent’s big cities reveals that shared transport by buses, cars, or motorcycles is big business that’s already ingrained in consumer culture. Millions of people daily pay fares to pack onto East and West Africa’s Mutatu and Danfo minibuses and Okada and Boda Boda motorbike taxis.

As Africa continues to urbanize, converts to smartphones, and discretionary consumer spending continues to rise—it all adds up to suggest strong potential for conversion to on-demand mobility services.

Unsurprisingly, the most active markets for ride-hail startups and investment in Africa align with the continent’s top spots for VC and tech activity: primarily Nigeria, Kenya, and South Africa.

Powered by WPeMatico

To become a global fintech player, locate your company in San Francisco and Africa.

That’s the approach of payments company Flutterwave, digital lending startup Mines, and mobile-money venture Chipper Cash—Africa-founded ventures that maintain headquarters in San Francisco and operations in Africa to tap the best of both worlds in VC, developers, clients, and the frontier of digital finance.

This arrangement wasn’t exactly coordinated across the ventures, but TechCrunch coverage picked up the trend and some common motives among these rising fintech firms.

Founded in 2016 by Nigerians Iyinoluwa Aboyeji and Olugbenga Agboola, Flutterwave has positioned itself as a global B2B payments solutions platform for companies in Africa to pay other companies on the continent and abroad.

Clients can tap its APIs and work with Flutterwave developers to customize payments applications. Existing customers include Uber, Booking.com and African e-commerce unicorn Jumia.com.

The Y-Combinator backed company is headquartered in San Francisco, runs its operations center in Nigeria, and plans to add offices in South Africa and Cameroon.

Flutterwave opened an office in Uganda in June and raised a $10 million Series A round in October. The company also plugged into ledger activity in 2018, becoming a payment processing partner to the Ripple and Stellar blockchain networks.

Powered by WPeMatico

The San Francisco-based startup Branch International, which makes small personal loans in emerging markets, has raised $170 million and announced a partnership with Visa to offer virtual, pre-paid debit cards to Branch client networks in Africa, South-Asia and Latin America.

Branch — which has 150 employees in San Francisco, Lagos, Nairobi, Mexico City and Mumbai — makes loans starting at $2 to individuals in emerging and frontier markets. The company also uses an algorithmic model to determine credit worthiness, build credit profiles and offer liquidity via mobile phones.

“We’ll use [the money] to deepen existing business in Africa. Later this year we’ll announce high-yield savings accounts…in Africa,” says Branch co-founder and chief executive Matt Flannery.

The $170 million round from Foundation Capital and its new debit card partner, Visa, will support Branch’s international expansion, which could include Brazil and Indonesia, according to Flannery. Branch launched in Mexico and India within the last year. In Africa, it offers its services in Kenya, Nigeria and Tanzania.

A potential Branch customer

The Branch-Visa partnership will allow individuals to obtain virtual Visa accounts with which to create accounts on Branch’s app. This gives Branch larger reach in countries such as Nigeria — Africa’s most populous country with 190 million people — where cards have factored more prominently than mobile money in connecting unbanked and underbanked populations to finance.

Founded in 2015, Branch started operating in Kenya, where mobile money payment products such as Safaricom’s M-Pesa (which does not require a card or bank account to use) have scaled significantly. M-Pesa now has 25 million users, according to sector stats released by the Communications Authority of Kenya. Branch has more than 3 million customers and has processed 13 million loans and disbursed more than $350 million, according to company stats.

Branch has one of the most downloaded fintech apps in Africa, per Google Play app numbers combined for Nigeria and Kenya, according to Flannery.

Already profitable, Branch International expects to reach $100 million in revenues this year, with roughly 70 percent of that generated in Africa, according to Flannery.

In addition to Visa and Foundation Capital, the $170 Series C round included participation from Branch’s existing investors Andreessen Horowitz, Trinity Ventures, Formation 8, the IFC, CreditEase and Victory Park, while adding new investors Greenspring, Foxhaven and B Capital.

Branch last raised $70 million in 2018. The company’s overall VC haul and $100 million revenue peg register as pretty big numbers for a startup focused primarily on Africa. Pan-African e-commerce startup Jumia, which also announced its NYSE IPO last month, generated $140 million in revenue (without profitability) in 2018.

Startups building financial technologies for Africa’s 1.2 billion population have gained the attention of investors. As a sector, fintech (or financial inclusion) attracted 50 percent of the estimated $1.1 billion funding to African startups in 2018, according to Partech.

Startups building financial technologies for Africa’s 1.2 billion population have gained the attention of investors. As a sector, fintech (or financial inclusion) attracted 50 percent of the estimated $1.1 billion funding to African startups in 2018, according to Partech.

Branch’s recent round and plans to add countries internationally also tracks a trend of fintech-related products growing in Africa, then expanding outward. This includes M-Pesa, which generated big numbers in Kenya before operating in 10 countries around the world. Nigerian payments startup Paga announced its pending expansion in Asia and Mexico late last year. And payment services such as Kenya’s SimbaPay have also connected to global networks like China’s WeChat.

Powered by WPeMatico

African tech in 2017 was about the normalization of market events mostly absent even a decade ago. There were acquisitions, multiple investment rounds, lots of expansion, big strategic partnerships and some surprise failures. Africa is fast becoming home to a dynamic tech sector. Here’s a snapshot of the news that shaped that transition over the last year. Read More

African tech in 2017 was about the normalization of market events mostly absent even a decade ago. There were acquisitions, multiple investment rounds, lots of expansion, big strategic partnerships and some surprise failures. Africa is fast becoming home to a dynamic tech sector. Here’s a snapshot of the news that shaped that transition over the last year. Read More

Powered by WPeMatico

Logistics transportation company Lori Systems won best of show at TechCrunch’s Startup Battlefield Africa after gaining majority votes of the event’s 15 judges. The Kenyan-based venture pitched its platform to optimize all points of the cargo delivery supply chain. Lori wasn’t the only winner at Startup Battlefield Africa. Read More

Logistics transportation company Lori Systems won best of show at TechCrunch’s Startup Battlefield Africa after gaining majority votes of the event’s 15 judges. The Kenyan-based venture pitched its platform to optimize all points of the cargo delivery supply chain. Lori wasn’t the only winner at Startup Battlefield Africa. Read More

Powered by WPeMatico

Kenya’s leading mobile provider, Safaricom, is teaming up with data collection startup mSurvey to launch Consumer Wallet ― an online platform using mobile and SMS to map Africa’s cash-based economy.

Kenya’s leading mobile provider, Safaricom, is teaming up with data collection startup mSurvey to launch Consumer Wallet ― an online platform using mobile and SMS to map Africa’s cash-based economy.