Rocket Internet

Auto Added by WPeMatico

Auto Added by WPeMatico

During my five years with Global Founders Capital, Rocket Internet’s $1 billion VC arm, I saw more than a hundred of Rocket’s incubated companies attempt to internationalize. For background, Rocket Internet has helped launch some very successful businesses internationally, including HelloFresh ($12.9 billion market cap), Lazada ($1 billion exit to Alibaba), Jumia ($3.2 billion market cap), Zalando ($21.2 billion market cap) and many others. Rocket often followed the Blitzscaling model popularized by Reid Hoffman — earning them an appearance in his book of the same name.

After an initial success helping Groupon scale internationally via a merger with Rocket’s incubation firm CityDeal, Rocket’s team have aggressively scaled businesses from Algeria to Zimbabwe — sometimes in a matter of weeks. No surprise, Rocket also has a graveyard of failed companies that were victims of bad internationalization efforts.

Many companies make the costly mistake of launching abroad too soon.

My personal observations on Rocket’s successes and failures start with this crucial point: These learnings might not apply to your unique combination business model, market and timing. No matter how well you prepare and plan your internationalization, in the end you need to be agile, alert and smart as you dip your toes into your first foreign market.

Internationalization can be a big driver of growth and consequently enterprise value, which is why investors always push for it. But going abroad can also destroy value just as quickly. As a founder, it’s your job to manage financial and operational risks. Finding the right balance between keeping costs in check and not underinvesting can mean doing things more slowly than your board would like. For example, you might launch new markets sequentially instead of rolling 10 out at the same time.

Adopt a “hire slow, fire fast” mentality for your expansion strategy. Don’t be afraid to pull the plug if things don’t work out.

Our team at Heartcore Capital use the following framework and learnings to guide internationalization strategies for our portfolio companies. A successful internationalization strategy needs to answer and address the “Four Ws”: When, Where, Which and With whom to internationalize. (Regarding the fifth W from journalism, you should not need to ask the “Why” question if you want to build a large business!)

Many companies make the costly mistake of launching abroad too soon. They look at internationalization as a detached function, isolated from the rest of the business and then launch their second market prematurely. Follow this simple rule: Wait to internationalize until you hit product/market fit.

How do you know exactly when you’ve reached product/market fit? According to Marc Andreessen, “Product/market fit means being in a good market with a product that can satisfy that market.” He adds that experienced entrepreneurs can usually feel if they’ve reached this point.

Let’s take the man for his word and move on to the actual argument: Until you have product/market fit, you will not be able to distinguish between what you’ve learned from your business model and what you’ve learned from your in-country experience. Mistakes will compound. Complexities and costs will multiply. I contend that insufficient understanding of their business and operating model is the main reason why companies fail with their expansion strategies.

Founders should also consider the underlying costs of internationalizing before they decide to expand (more about this in the “What” section below). Some companies are global by default — think mobile gaming companies — or simply require language localization. Others need to build new warehouses, hire local teams or build entirely new products. The costs and respective risks of expanding prematurely depend heavily on the business model.

There are edge cases where companies need to move quickly to internationalize for strategic reasons — despite uncertainty about their market fit. For instance, companies like Groupon or those engaged in food delivery face winner-takes-most markets, where opportunities for product differentiation are limited. “Blitzscaling” makes sense in cases like these.

However, you should tread carefully if your only reason to start scaling abroad is a large fundraise or to match a competitor’s internationalization efforts. Scaling prematurely for the wrong reasons might just cost you your entire company.

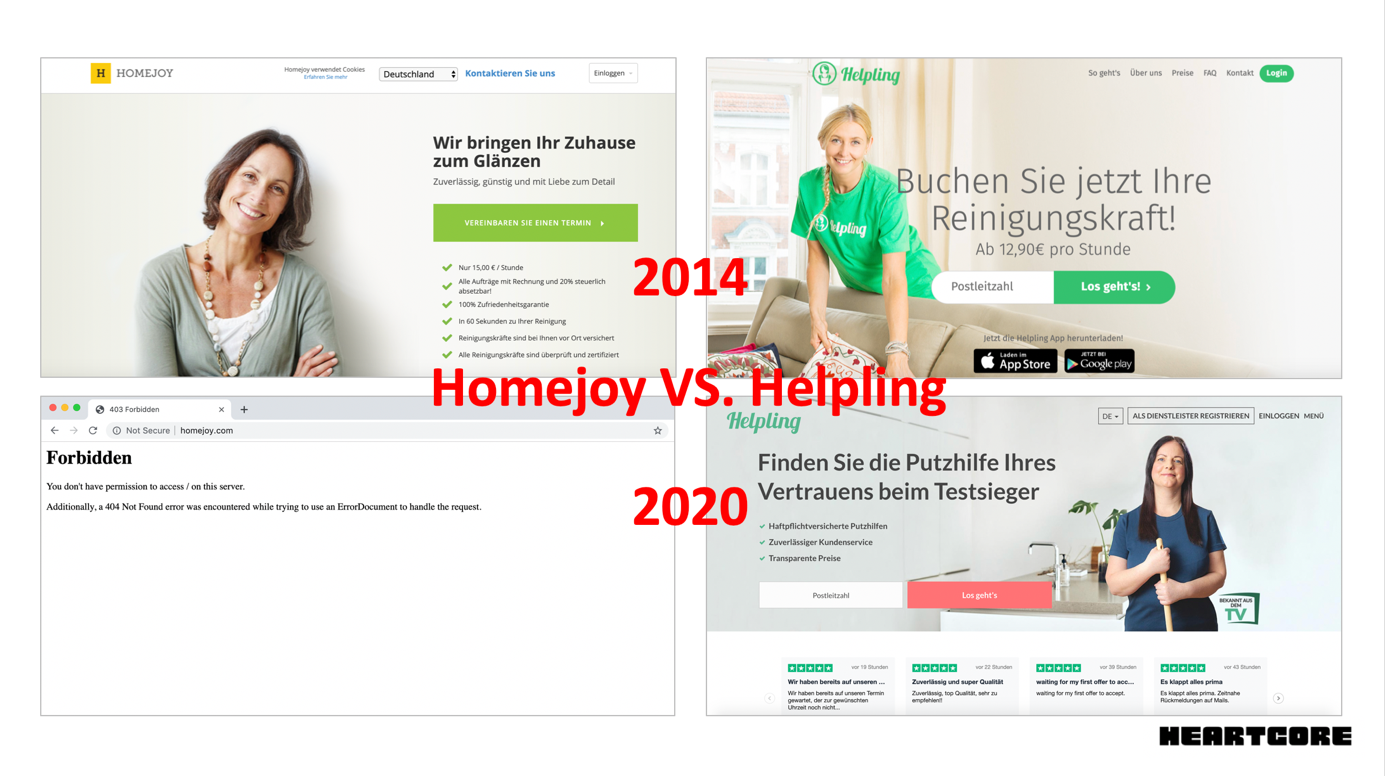

When Rocket Internet announced it would launch the Homejoy model into European markets with Helpling, the American “original” company launched quickly in Germany in an effort to squash their new competitor. In the early days of “on-demand everything,” a managed marketplace for cleaning services sounded like the next unicorn in the making.

In 2013, Homejoy had a fresh $24 million Series A from Google Ventures and First Round — considered a huge round at a time when Instacart had just raised an $8 million Series A and Snapchat had done a $13 million Series A round. It must have seemed like a good idea to squash the German competition early.

As it turned out, Homejoy’s product was not yet ready to scale internationally. Just 13 months after launching in Germany, Homejoy had to cease operations globally, while Rocket’s Helpling is still alive and kicking. Helpling focused carefully on product, automation and making their unit economics work. A rush to crush an international competitor caused the demise of a would-be unicorn.

Homejoy expanded internationally in 2014 in a rush to squash a new German competitor Helpling. Their websites in 2020 show starkly different outcomes. Image Credits: Homejoy/Helpling

When deciding which new international market to tackle, it is vital to do your homework. Analyze the competitive environment, partner availability, infrastructure, culture, regulation and synergies with your home market.

In the early days of e-commerce, it was rather easy to analyze if a market was an expansion target. In the absence of professional competition, Rocket chose new countries based solely on GDP and internet penetration.

Powered by WPeMatico

Increasingly, the streets of Karachi and Lahore are being flooded with men riding bikes and wearing green T-shirts, a writer friend recently told me. In a sense, these men represent the emergence of Pakistan’s tech startups.

India now has more than 25,000 startups and raised a record $14.5 billion last year, according to government figures. But not all Asian countries are as large as India or have such a thriving startup ecosystem. Long overdue, things are beginning to change in bordering Pakistan.

Bykea, a three-year-old ride-hailing and delivery service, today has more than 500,000 bikes registered on its platform. It operates in some of Pakistan’s most populated cities, such as Karachi, Lahore and Islamabad, Muneeb Maayr, Bykea founder and CEO, told TechCrunch.

Maayr is one of the most recognized startup founders in Pakistan, and previously worked for Rocket Internet, helping the giant run fashion e-commerce platform Daraz in the country. While leading Daraz, he expanded the platform to cater to categories beyond fashion; Daraz was later sold to Alibaba.

Powered by WPeMatico

Less than a decade ago IPOs, acquisitions and global expansion by African startups were more possibility than reality. March saw all three from the continent’s tech scene.

Pan-African e-commerce company Jumia filed for an IPO on the New York Stock Exchange, per SEC documents and confirmation from chief executive Sacha Poignonnec.

In an updated filing, (since the March 12 original) Jumia indicated it will offer 13,500,000 ADR shares, for an offering price of $13 to $16 per share to trade under the ticker symbol “JMIA.” The IPO could raise up to $216 million for Jumia.

Since our first story (and reflected in the latest SEC docs), Mastercard Europe agreed upfront to buy $50 million in Jumia ordinary shares.

With a smooth filing process, Jumia will become the first African startup to list on a major global exchange. The company is incorporated in Germany, but maintains its headquarters in Nigeria, and operates exclusively in Africa, with 4,000 employees on the continent.

The pending IPO creates another milestone for Jumia. The venture became the first African startup unicorn in 2016, achieving a $1 billion valuation after a funding round that included Goldman Sachs, AXA and MTN.

Founded in Lagos in 2012 with Rocket Internet backing, Jumia now operates multiple online verticals in 14 African countries. Goods and services lines include Jumia Food (an online takeout service), Jumia Flights (for travel bookings) and Jumia Deals (for classifieds). Jumia processed more than 13 million packages in 2018, according to company data. The company has started to generate annual revenues over $100 million, but like many burn-rate startups, has done so while racking up big losses.

There’ll be a lot more to cover, analyze and debate pre and post Jumia’s NYSE bell toll — which could happen in coming weeks or months. For example, can Jumia generate a profit; is it really an African startup; will Jumia become an acquisition target for a big outside name or an acquirer of smaller startups in African e-commerce? Stay tuned for continuing TechCrunch coverage.

On the acquisition front, Lagos-based online lending startup OneFi bought Nigerian payment solutions company Amplify for an undisclosed amount.

OneFi is taking over Amplify’s IP, team and client network of more than 1,000 merchants to which Amplify provides payment processing services, OneFi CEO Chijioke Dozie told TechCrunch.

The purchase of Amplify caps off a busy period for OneFi. Over the last seven months the Nigerian venture secured a $5 million lending facility from Lendable, announced a payment partnership with Visa and became one of the first (known) African startups to receive a global credit rating. OneFi is also dropping the name of its signature product, Paylater, and will simply go by OneFi (for now).

Collectively, these moves represent a pivot for OneFi away from operating primarily as a digital lender, toward becoming an online consumer finance platform.

“We’re not a bank but we’re offering more banking services…Customers are now coming to us not just for loans but for cheaper funds transfer, more convenient bill payment, and to know their credit scores,” said Dozie.

OneFi will add payment options for clients on social media apps, including WhatsApp, this quarter — something in which Amplify already holds a specialization and client base. Through its Visa partnership, OneFi will also offer clients virtual Visa wallets on mobile phones and start providing QR code payment options at supermarkets, on public transit and across other POS points in Nigeria.

On the back of the acquisition, OneFi is in the process of raising a round and will look to expand internationally, considering Senegal, Côte d’Ivoire, DRC, Ghana and Egypt and Europe for Diaspora markets.

On African startups expanding globally, FlexClub — a South African venture that matches investors and drivers to cars for ride-hailing services — announced it will expand in Mexico in a partnership with Uber after closing a $1.2 million seed round led by CRE Venture Capital.

The move comes as Africa’s tech-transit space continues to produce unique mobility solutions shaped around local needs.

FlexClub touts itself as a “gig economy investment platform” that is creating new asset classes in emerging markets, according to chief executive and co-founder Tinashe Ruzane.

That asset class, for now, is ride-hail vehicles. FlexClub allows investors to go on the site and purchase a car (ultimately managed and serviced by FlexClub). The startup then connects that car to an Uber driver who uses earnings to pay a weekly rental charge.

Those fees generate monthly fixed-rate interest income for the investor. The driver has the option of buying the car after 12 months, with a descending purchase price over time.

FlexClub’s platform manages the investment, rental income and disbursement of funds across all parties. The startup also handles insurance, maintenance and upkeep of the cars.

Ruzane envisions this as a model to finance multiple asset classes in emerging markets — where lending options are fewer for individuals who may not have credit histories.

“Our goal is to make this completely passive… where investors can invest in different kinds of assets on our platform, login to a dash, and see this is how my five cars in South Africa are doing, my vans in Mexico, my motorbikes in Indonesia — with a diversified portfolio around the world,” he explained.

FlexClub will begin work matching investors to cars and Uber drivers in Mexico in April. The startup sees opportunities to move into other mobility classes, such as Africa’s ride-hail motorcycle taxi and three-wheel tuk-tuk market, CEO Tinashe Ruzane told TechCrunch in this feature.

And finally, francophone Africa will see a boost in funds and support for startups. The Dakar Network Angels group launched last month, making its first investment to cleantech venture Coliba — an Ivorian startup that uses a mobile app to coordinate waste recycling

The deal is part of Dakar Network Angels’ mission of convening experts and capital to bridge the resource gap for startups in French-speaking Africa — or 24 of the continent’s 54 countries.

The organization — which goes by DNA for short — will offer seed fund investments of between $25,000 to $100,000 to early-stage ventures with high growth potential. These rounds will come with the entrepreneurial guidance of DNA’s angel network.

Launched in Senegal, the organization’s founder Marieme Diop — a VC investor at Orange Digital Ventures — named the goal of bridging VC disparities between francophone and non-francophone Africa as the primary driver for DNA. She pointed to funding data by Partech, indicating that 76 percent of investment to African startups goes to three English-speaking countries — Nigeria, Kenya and South Africa.

To gain consideration for DNA investment, startups must gain referral by a member. DNA will take a minority stake (less than 10 percent) in ventures that receive seed funds and provide program mentorship until exits, Diop told TechCrunch.

To become an angel, members must commit to investing a minimum of $10,000 a year (for those coming on as individuals), $20,000 (for corporates) and be on hand to support the portfolio startups, according to DNA’s Corporate Membership Charter.

More Africa Related Stories @TechCrunch

African Tech Around The Net

Powered by WPeMatico

Despite not being Brazilian and having their first exposure to the country only a few years ago, the two co-founders of Escale have managed to raise $22.6 million for their company, which provides customer acquisition services to companies in telecommunications and healthcare across Brazil.

Their secret? A knowledge of search engine optimization technologies honed through side businesses the two ran back in the United States.

The state of online marketing and digital sales was so woefully bad in Brazil that co-founders Matthew Kligerman and Ken Diamond had a green field in front of them on which to build Brazil’s first true online customer acquisition service, according to Diamond.

“We fell in love with Brazil for its warm culture and natural beauty, but as consumers, we had terrible experiences acquiring the most fundamental products and services for our new lives: internet, cell phone plans, health insurance and basic banking needs,” Kligerman said in a statement.

The company’s largest customer, according to Diamond, is NET, the Brazilian cable and telecom operator. NET was the first company to sign on for Escale’s customer acquisition services, but the company’s roster of clients now includes some of Brazil’s largest companies, including Bradesco, Sul America, Claro, GNDI and Amil.

It’s that marquee client list that attracted QED Investors and Invus Opportunities to co-lead the $22.6 million round that Escale just closed. The company’s previous investors, Kaszek Ventures, Rocket Internet’s GFC and Redpoint e.Ventures, also participated in the funding.

Latin America is in the throes of a startup renaissance at the moment, with Brazilian companies like Nubank and iFood and the Colombian company Rappi reaching billion-dollar valuations. Meanwhile investors are committing more capital to the region. SoftBank, for instance, is committing $5 billion to a new Latin American-focused fund.

With the new funding, Escale intends to move deeper into the development of customer acquisition platforms across verticals like consumer finance, insurance and education with comparison shopping sites and informational services (à la Credit Karma in the U.S.).

“With millions of web and cloud voice interactions every month, Escale can transform each of those interactions into data points, and continually improve its proprietary acquisition platform, ‘EscaleOS,’ to create highly-intelligent, customized marketing and sales funnels, helping consumers at the right moment connect with the products and services they need,” says Nicolas Berman, a partner at Kaszek Ventures. “The more consumer interactions they have, the faster Escale’s data flywheel spins.”

Powered by WPeMatico

Pan-African e-commerce company Jumia filed for an IPO on the New York Stock Exchange today, per SEC documents and confirmation from CEO Sacha Poignonnec to TechCrunch.

The valuation, share price and timeline for public stock sales will be determined over the coming weeks for the Nigeria-headquartered company.

With a smooth filing process, Jumia will become the first African tech startup to list on a major global exchange.

Poignonnec would not pinpoint a date for the actual IPO, but noted the minimum SEC timeline for beginning sales activities (such as road shows) is 15 days after submitting first documents. Lead adviser on the listing is Morgan Stanley .

There have been numerous press reports on an anticipated Jumia IPO, but none of them confirmed by Jumia execs or an actual SEC, S-1 filing until today.

Jumia’s move to go public comes as several notable consumer digital sales startups have faltered in Nigeria — Africa’s most populous nation, largest economy and unofficial bellwether for e-commerce startup development on the continent. Konga.com, an early Jumia competitor in the race to wire African online retail, was sold in a distressed acquisition in 2018.

With the imminent IPO capital, Jumia will double down on its current strategy and regional focus.

“You’ll see in the prospectus that last year Jumia had 4 million consumers in countries that cover the vast majority of Africa. We’re really focused on growing our existing business, leadership position, number of sellers and consumer adoption in those markets,” Poignonnec said.

The pending IPO creates another milestone for Jumia. The venture became the first African startup unicorn in 2016, achieving a $1 billion valuation after a $326 funding round that included Goldman Sachs, AXA and MTN.

Founded in Lagos in 2012 with Rocket Internet backing, Jumia now operates multiple online verticals in 14 African countries, spanning Ghana, Kenya, Ivory Coast, Morocco and Egypt. Goods and services lines include Jumia Food (an online takeout service), Jumia Flights (for travel bookings) and Jumia Deals (for classifieds). Jumia processed more than 13 million packages in 2018, according to company data.

Starting in Nigeria, the company created many of the components for its digital sales operations. This includes its JumiaPay payment platform and a delivery service of trucks and motorbikes that have become ubiquitous with the Lagos landscape.

Starting in Nigeria, the company created many of the components for its digital sales operations. This includes its JumiaPay payment platform and a delivery service of trucks and motorbikes that have become ubiquitous with the Lagos landscape.

Jumia has also opened itself up to traders and SMEs by allowing local merchants to harness Jumia to sell online. “There are over 81,000 active sellers on our platform. There’s a dedicated sellers page where they can sign-up and have access to our payment and delivery network, data, and analytic services,” Jumia Nigeria CEO Juliet Anammah told TechCrunch.

The most popular goods on Jumia’s shopping mall site include smartphones (priced in the $80 to $100 range), washing machines, fashion items, women’s hair care products and 32-inch TVs, according to Anammah.

E-commerce ventures, particularly in Nigeria, have captured the attention of VC investors looking to tap into Africa’s growing consumer markets. McKinsey & Company projects consumer spending on the continent to reach $2.1 trillion by 2025, with African e-commerce accounting for up to 10 percent of retail sales.

Jumia has not yet turned a profit, but a snapshot of the company’s performance from shareholder Rocket Internet’s latest annual report shows an improving revenue profile. The company generated €93.8 million in revenues in 2017, up 11 percent from 2016, though its losses widened (with a negative EBITDA of €120 million). Rocket Internet is set to release full 2018 results (with updated Jumia figures) April 4, 2019.

Jumia’s move to list on the NYSE comes during an up and down period for B2C digital commerce in Nigeria. The distressed acquisition of Konga.com, backed by roughly $100 million in VC, created losses for investors, such as South African media, internet and investment company Naspers .

In late 2018, Nigerian online sales platform DealDey shut down. And TechCrunch reported this week that consumer-focused venture Gloo.ng has dropped B2C e-commerce altogether to pivot to e-procurement. The CEO cited better unit economics from B2B sales.

In late 2018, Nigerian online sales platform DealDey shut down. And TechCrunch reported this week that consumer-focused venture Gloo.ng has dropped B2C e-commerce altogether to pivot to e-procurement. The CEO cited better unit economics from B2B sales.

As demonstrated in other global startup markets, consumer-focused online retail can be a game of capital attrition to outpace competitors and reach critical mass before turning a profit. With its unicorn status and pending windfall from an NYSE listing, Jumia could be better positioned than any venture to win on e-commerce at scale in Africa.

Powered by WPeMatico

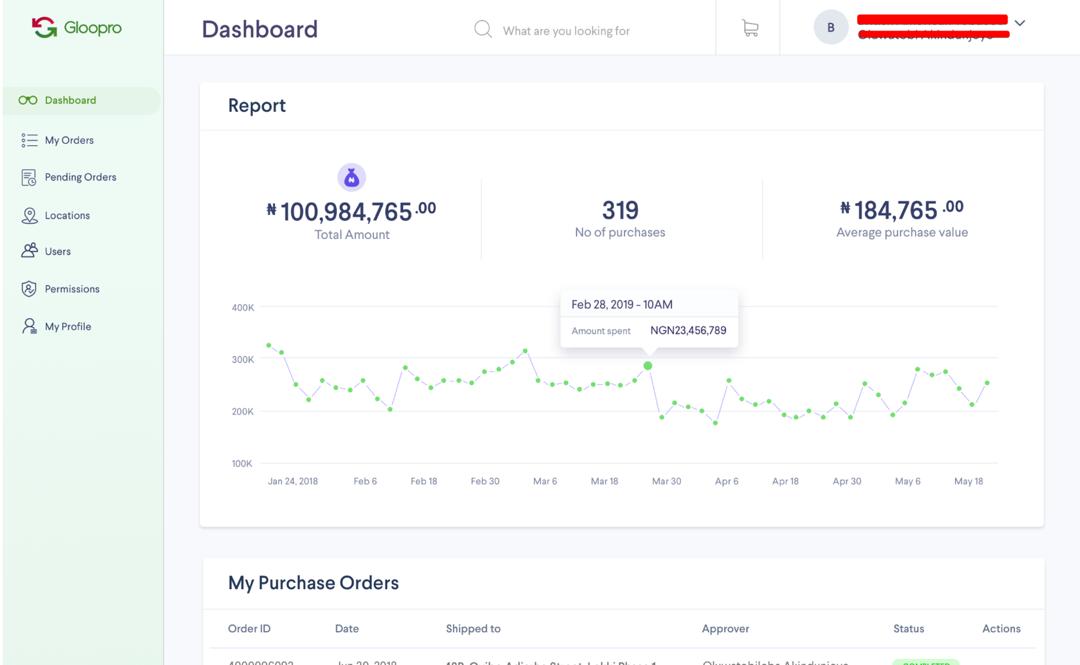

Nigerian startup Gloo.ng is dropping consumer online retail and pivoting to B2B e-procurement with Gloopro as its new name.

The Lagos-based venture has called it quits on e-commerce grocery services, shifting to a product that supplies large and medium corporates with everything from desks to toilet paper.

Gloopro’s new platform will generate revenues on a monthly fee structure and a percentage on goods delivered, according to Gloopro CEO D.O. Olusanya.

Gloopro, which raised around $1 million in seed capital as Gloo.ng, is also in the process of raising its Series A round. The startup looks to expand outside of Nigeria on that raise, “before the end of next year,” Olusanya told TechCrunch.

Gloopro’s move away from B2C comes as several notable consumer digital sales startups have failed to launch in Nigeria — Africa’s most populous nation with the continent’s highest number of online shoppers, per a recent UNCTAD report.

The country is home to the continent’s first e-commerce startup unicorn, Jumia, and serves as an unofficial bellwether for e-commerce startup activity in Africa.

Gloo.ng’s shift to B2B electronic commerce was prompted by Nigeria’s 2016 economic slump and a customer request, according Olusanya.

“When the recession hit it affected all consumer e-commerce negatively. We saw it was going to take a longer time to get to sustainability and profitability,” he told TechCrunch.

Then an existing client, Unilever, requested an e-procurement solution in 2017. “We observed that the unit economics of that business was far better than consumer e-commerce,” said Olusanya.

Gloopro dubs itself as a “secure cloud based enterprise e-procurement and commerce platform…[for]…corporate purchasing,” per a company description.

“The old brand Gloo.ng, is going to be rested and shut down completely. The corporate name will be PayMente Limited with the brand name Gloopro,” Olusanya said.

From the Gloopro interface customers can order, pay for and coordinate delivery of office supplies across multiple locations. The product also produces procurement analytics and allows companies to designate users and permissions.

Olusanya touts the product’s benefits at improving transparency and efficiency in the purchasing process.

“It makes procurement transparent and secure. A lot of companies in Nigeria still use paper invoices and there are some shenanigans,” he said.

Gloopro began offering the service in beta and building a customer base prior to winding down its Gloo.ng grocery service.

In addition to Unilever, Gloopro clients include Uber Nigeria, Cars45 and industrial equipment company LaFarge. Cars45 CEO Etop Ikpe and a spokesperson for Uber Nigeria confirmed their client status to TechCrunch.

Olusanya believes the company can compete with other global e-procurement providers, such as SAP Ariba and GT-Nexus, by “leveraging our sourcing and last-mile delivery experience in Nigeria” and expertise working around local requirements in Africa.

Gloopro expects to hit $4 million in revenue by the end of the year and the company could reach $100 million over the course of its international expansion into countries like South Africa, Kenya, Morocco, Egypt and the Ivory Coast, according to Olusanya. A seed investor briefed on Gloo.ng’s estimates confirmed the company’s revenue expectations with TechCrunch.

Gloo.ng’s pivot to Gloopro and e-procurement comes during an up and down period for B2C online retail in Nigeria, home of Africa’s largest economy.

Last year, e-commerce startup Konga.com, backed by roughly $100 million in VC, was sold in a distressed acquisition, at a loss to investors, including Naspers. In late 2018, Nigerian online sales platform DealDey shut down.

On the possible upside, several outlets reported this year that Jumia — Africa’s largest e-commerce site and first unicorn headquartered in Nigeria — is pursuing an IPO. But that information is unconfirmed based on a February 8, Bloomberg story without named sources. Jumia has declined to comment.

Powered by WPeMatico

Every year I teach an MBA course at Stanford about the exciting opportunities for tech investors and entrepreneurs in developing economies. When we designed the syllabus back in 2013, Rocket Internet was still firing on all cylinders on four continents. The unapologetic machine built to copy big American internet companies created billions of dollars for the Samwer brothers and its backers. During Rocket’s golden years, the best startups in the developing economies seemed to inevitably have an original reference in Silicon Valley.

Accordingly, we added a class about the opportunity of replicating business models to seize this information arbitrage. Call it the second-mover advantage.

Despite my conviction about the model, the copycat word — short for replicating startups and attached to these ventures — annoyed me from the start. More than a term to describe a straightforward recipe to launch, I see it as an unconscious way to belittle an entire group of hard-charging founders and investors.

Indeed, while in foreign eyes, we have been building a Mexican Kickstarter, a Middle Eastern Uber, an Indian Amazon or a Colombian Postmates, I argue visionary founders are taking a simple idea that already exists and creating new worlds.

On the internet, there are Einsteins and there are Bob the Builders. I’m Bob the Builder. Oliver Samwer, founder of Rocket Internet

While impact is the final goal, founders can approach the journey in different ways. The most common approach in the startup world is to use the business method, or more pompously, the design thinking methodology. “Fall in love with the problem, not the solution,” mentors keep telling a succession of startup clusters in acceleration programs. The best and “leanest” way to product market fit is by starting small then keep iterating the solution until you nail it.

A second way to start is favored by engineers and scientists: Take a new promising technology or a forgotten molecule, then find a big problem. Keep iterating until you find a problem worth solving, like a hammer looking for a nail.

A third way is starting like painters create, building skills by copying classics, or like a new chef cooks by starting with iconic recipes: replicate a proven idea and iterate until you find traction.

Until a few years ago it was ostensibly the only way to scale in developing economies. The model helped raise local capital from risk-averse investors who needed reassurance. The playbook to scale was unfolding a couple of years ahead and served as a guide to founders without previous startup experience and no local role models. The potential acquirer was identified and sometimes contacted in advance. Founders weren’t crazy and investors weren’t dumb.

Replicating a business model has served in emerging ecosystems as the gateway to entrepreneurship and venture investing.

Photo courtesy of Flickr/A_Marga

According to conventional wisdom, new ecosystems around the world grow through the following three stages, be them in developing economies or more developed countries. First, local and foreign entrepreneurs replicate successful models focused on local markets. Then as the ecosystem evolves, founders start applying existing technologies to solve local problems. Finally, as the tech space matures, new technologies begin to flourish.

In my opinion, those stages never happen sequentially as stated by ecosystem observers. Successful startups that started with a foreign inspiration can outgrow the master. If they are not bought into submission by the first mover, some of the most famous copycats reinvented the original and made it better: Mercado Libre is much more relevant in the e-commerce space than eBay . Flipkart is hardly an Amazon, not to mention WeChat. These companies are in turn some of the most prolific tech innovators on the globe. Truly ecosystems evolve organically in unique ways reflecting their history, geopolitical environment, economic structure and cultural features.

Two ways to defend the status quo: “It’s been done before” and “It’s never been done before.” –Thibault @Kpaxs

Recently, it’s hard to hear American observers use the word copycat to describe any American company. After all, Guilt replicated VentesPrivees and Lime, Chinese dockless bike sharing and many more examples. All American startups are treated as innovators while the rest as mere followers.

Recently, Chinese or Indian startups seem to be given the benefit of the doubt regarding their originality. Is it because these regions have become more innovative? Maybe. But it’s also because these ecosystems have gained the respect of Silicon Valley. Indeed, Chinese consumer tech surpassed decisively the U.S. as the most important country in terms of investments.

So here’s my humble suggestion to our wealthier and more accomplished colleagues: stop using the c-word with founders. It’s offensive. Most probably, these founders are facing more challenges to build their companies and lower odds for success that the first mover. If anything, they have more merit than the originals.

As for founders, when they call you a me-too, remember all teams started somewhere, somehow. In fact, most started like Bob the Builder before turning into Einsteins. The truth is, it doesn’t matter where you start. You can start by applying a new technology or protocol. You can start with a problem you feel passionate about. You can start by replicating a business model. It doesn’t really matter if you take a big swing at the future and trust you will figure out how to make it happen. It doesn’t matter what label they use while you change the world for the better.

Powered by WPeMatico

There has been no shortage of thoughtful articles exploring a bubble in technology. I would argue that the world has already been transformed, and there is no bubble in the purest sense. Instead of massive flameouts that leave everyone burned, I think we are going to see a wave of beneficial consolidation and rationalization in industries that appropriately have seen exceptional venture… Read More

There has been no shortage of thoughtful articles exploring a bubble in technology. I would argue that the world has already been transformed, and there is no bubble in the purest sense. Instead of massive flameouts that leave everyone burned, I think we are going to see a wave of beneficial consolidation and rationalization in industries that appropriately have seen exceptional venture… Read More

Powered by WPeMatico

Rocket Internet has its fingers in pretty much every part of the online food ordering and delivery pie. Heck, it even has a special division, the unimaginatively-named Global Online Takeaway Group, where its rolled up a number of those companies. But one slice it has yet to serve is corporate catering — until now, that is. Read More

Rocket Internet has its fingers in pretty much every part of the online food ordering and delivery pie. Heck, it even has a special division, the unimaginatively-named Global Online Takeaway Group, where its rolled up a number of those companies. But one slice it has yet to serve is corporate catering — until now, that is. Read More

Powered by WPeMatico

Rocket Internet has shuffled the online takeout pack of cards once again. This time the publicly-listed German ‘startup factory’ and investor is selling foodpanda to its much larger rival Delivery Hero, of which it also holds a significant stake.

Rocket Internet has shuffled the online takeout pack of cards once again. This time the publicly-listed German ‘startup factory’ and investor is selling foodpanda to its much larger rival Delivery Hero, of which it also holds a significant stake.