Revolut

Auto Added by WPeMatico

Auto Added by WPeMatico

Consumer fintech startups were massively successful in 2019, attracting millions of new users and disrupting traditional retail banks and financial services with mobile-first, consumer-oriented products. Despite the economic downturn in public markets and the massive wave of cuts at public and private companies in recent weeks, fintech startups have been raising a ton of money.

It feels like they’re all building a war chest to survive the economic winter as traditional banks continue to iterate so they can catch up and offer more user-friendly services. This is not the time to raise fees, slow down on product development or plans to acquire new users.

Back in January, I looked at challenger banks and their growth trajectories, but since then, they have managed to attract even more customers. According to the most recent figures:

And that’s without mentioning Starling Bank, Atom Bank, Bunq, Bnext, Paysend, etc. At some point, there will be as many challenger banks as non-challenger banks — perhaps we shouldn’t call them challenger banks anymore.

Beyond these startups, trading app Robinhood recently reached 13 million users, international payments startup TransferWise has 7 million customers and cryptocurrency exchange Coinbase has 30 million users.

Powered by WPeMatico

European fintech startup Revolut is launching its app and service in the U.S. Starting today, anybody can sign up and get a Revolut debit card. In the U.S., Revolut has partnered with Metropolitan Commercial Bank for the banking infrastructure — deposits are FDIC insured up to $250,000.

In just a few years, Revolut has managed to attract over 10 million customers by building a financial hub that lets you spend, send, receive and manage money from a single app. The company recently raised a $500 million funding round, valuing the company at $5.5 billion.

But the U.S. has been watching from the sidelines. Tens of thousands of customers have signed up to the waiting list and they’ll now be able to access all of Revolut’s core features.

Like competing challenger banks, such as Chime and N26, Revolut lets you open an account from your phone. After downloading the app, you enter personal details and send a few official documents to comply with know-your-customer regulation.

After that, you get U.S. account details and you can instantly top up your account with a bank transfer or a card transfer. A few days later, you also receive a physical debit card. You can also generate a virtual debit card from the app.

Revolut lets you control your debit card from the app directly. You can receive notifications every time you make a transaction. You can freeze and unfreeze your card, set some limits and restrict some feature, such as online payments or ATM withdrawals.

One of Revolut’s key features is that you can convert from one currency to another based on interbank rate with a low fee — sometimes without any markup for popular currencies and small transactions (more details on foreign exchange fees here). You can hold foreign currencies in your Revolut account or send money to another Revolut user or a bank account in another country.

In the U.S., Revolut offers the ability to receive your salary two days in advance if you share your Revolut banking details with your employer.

Revolut offers a ton of additional features in Europe, but the company is starting with this basic feature set in the U.S. You can expect more features in the future, such as the ability to purchase cryptocurrencies and invest on the stock market.

In Europe, Revolut also offers insurance products through premium monthly subscriptions, mobile phone insurance, savings accounts, credit, rewards and more. Many of those features require partnerships with third-party companies. But it gives you an idea of Revolut’s roadmap in the U.S.

Powered by WPeMatico

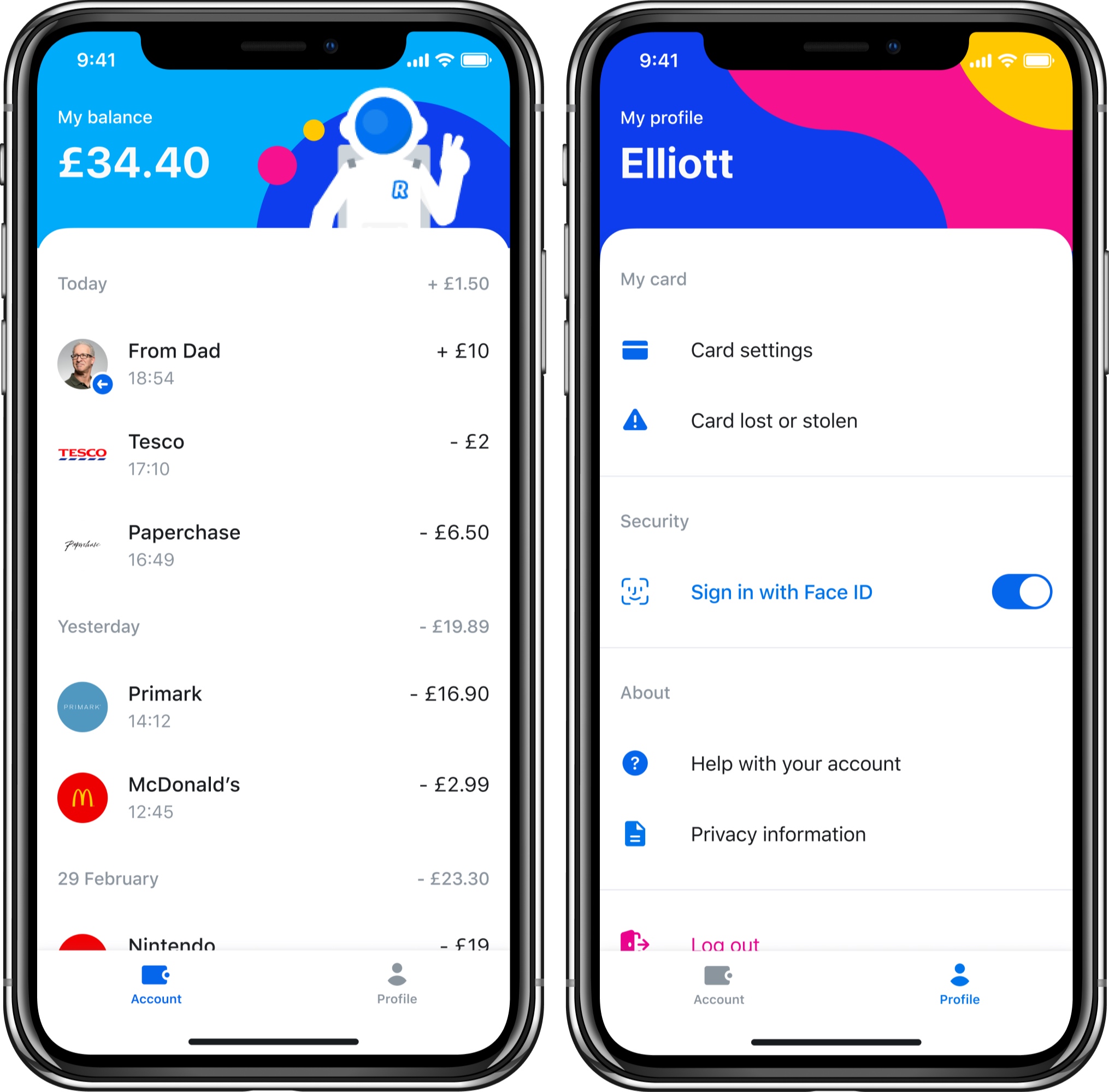

Revolut is introducing a new product specifically targeted toward kids aged 7-17 years old — Revolut Junior. Revolut Junior is a new app and service that integrates directly with the main Revolut app on the parent’s side.

Parents or legal gardians who are also Revolut users can create a Revolut Junior account for their kid. After that, your kid can download the Revolut Junior app and get a Revolut Junior card.

The new app offers a limited set of features with an interface divided in two tabs — Account and Profile. Kids can see a list of transactions in real time in the Account tab. They can configure card settings in the Profile tab. And that’s about it.

On the other end, parents can control their kids’ spending from Revolut. They can transfer money to a Revolut Junior account instantly. Parents can also access balances and transactions as well as disable some card features, such as online payments. They can also choose to receive notifications when a child is using their card.

The reason why Revolut Junior can attract a ton of users is that Revolut itself already has over 10 million users. It’s going to be easier to convince existing Revolut customers to use Revolut Junior over a custom-made challenger bank for teens, such as Kard or Step. Arguably, the biggest competitor of challenger banks for teens is still cash.

As kids grow up, chances are they’ll switch to a full-fledged Revolut account if they’ve been using Revolut Junior for years. Revolut Junior represents a great acquisition funnel as well.

Revolut Junior is only available to Premium and Metal customers in the U.K. for now. The company will eventually roll it out to more users and more countries.

Revolut plans to add more features to Revolut Junior in the future. For instance, parents will be able to set a regular allowance and financial goals. Kids will get savings options, spending reports, spending limits and more.

Powered by WPeMatico

Fintech startup Revolut has introduced a new trading feature for premium users. Starting today, Premium and Metal users can access gold exposure from the app.

Revolut works with a gold services partner (London Bullion Market Association) so that money you spend on gold exposure is backed by real gold held by this partner. In other words, you’re not going to receive gold coins in the mail. You can just invest money based on the price of gold.

The startup has been building a financial hub and already lets you purchase cryptocurrencies and buy public shares. Gold is part of a new feature called Commodities.

There are multiple ways to invest in gold. You can purchase gold exposure directly at market price, set a limit price to auto-exchange gold when it reaches a certain price or get cashback in gold for Metal customers.

At any time, you can convert your gold investment back into fiat currencies or cryptocurrencies. If you spend money with your Revolut card and you only have gold, Revolut will use your gold exposure automatically. You can also transfer gold exposure to another Revolut user.

According to the company’s website, Revolut charges a 0.25% markup when you trade gold during the week and a 1% markup from Saturday at midnight to Monday at midnight U.K. time.

It’s worth noting that gold isn’t protected through the Financial Services Compensation Scheme in the U.K. “However, in the unlikely event of Revolut’s insolvency, all Precious Metals holdings will be sold and proceeds will be credited to your e-money account,” Revolut says. You’ll have to trust their word.

Powered by WPeMatico

Fintech startup Revolut is raising a large Series D round of funding. TCV is leading the $500 million round, valuing the company at $5.5 billion. Over the past few years, Revolut has raised $836 million in total.

Some existing investors are also participating in today’s funding round, but Revolut isn’t sharing names. Previous investors include DST Global, Index Ventures, Balderton Capital and many others.

If you’re not familiar with Revolut, the company is building a financial service to replace traditional bank accounts. You can open an account from an app in just a few minutes. You can then receive, send and spend money from the app or using a debit card.

On top of that, Revolut has added a ton of features that it has built in-house or through partnerships. You can insure your phone, get a travel medical insurance package, buy cryptocurrencies, buy shares, donate to charities, save money and more.

Revolut currently has more than 10 million customers, mostly in Europe and the U.K. The company doesn’t share specific numbers when it comes to transaction volume and monthly active customers, but here are some percentage-based metrics:

With the new influx of cash, the company says that it’ll focus on improving its product for existing users as well as revenue. It’s all about making Revolut more useful and stickier going forward.

In particular, you can expect new lending services for both retail customers as well as companies using Revolut for Business. While Revolut provides a ton of services in the U.K., customers in other markets don’t have the same feature set. For instance, Revolut recently launched savings vaults in the U.K. — customers in other markets will be able to open savings sub-accounts in the future, as well.

Other than that, Revolut wants to double down on the core features. The company will improve its two subscription tiers (Premium and Metal) and improve banking operations across Europe — you can expect full bank accounts in Europe in the future.

There are currently 2,000 people working for Revolut. “We’re on a mission to build a global financial platform — a single app where our customers can manage all of their daily finances, and this investment demonstrates investor confidence in our business model. Going forward, our focus is on rolling-out banking operations in Europe, increasing the number of people who use Revolut as their daily account, and striving towards profitability,” Revolut co-founder and CEO Nik Storonsky said in the release.

Revolut is currently live in the U.K., Europe, Singapore and Australia (in beta). While the company has announced plans to expand to a handful of countries, the main focus is on launching in the U.S. and Japan in the coming months.

Powered by WPeMatico

Allowance is going digital. Venmo has been spotted prototyping a new feature that would allow adult users to create for their teenage children a debit card connected to their account. That could potentially let parents set spending notifications and limits while giving kids more flexibility in urgent situations than a few dollars stuffed in a pocket.

Delving into children’s banking could establish a new reason for adults to sign up for Venmo, get them saving more in Venmo debit accounts where the company can earn interest on the cash and drive purchase frequency that racks up interchange fees for Venmo’s owner PayPal .

But Venmo is arriving late to the teen debit card market. Startups like Greenlight and Step let parents manage teen spending on dedicated debit cards. More companies like Kard and neo banking giant Revolut have announced plans to launch their own versions. And Venmo’s prototype uses very similar terminology to that of Current, a frontrunner in the children’s banking space with over 500,000 accounts that raised a $20 million Series B late last year.

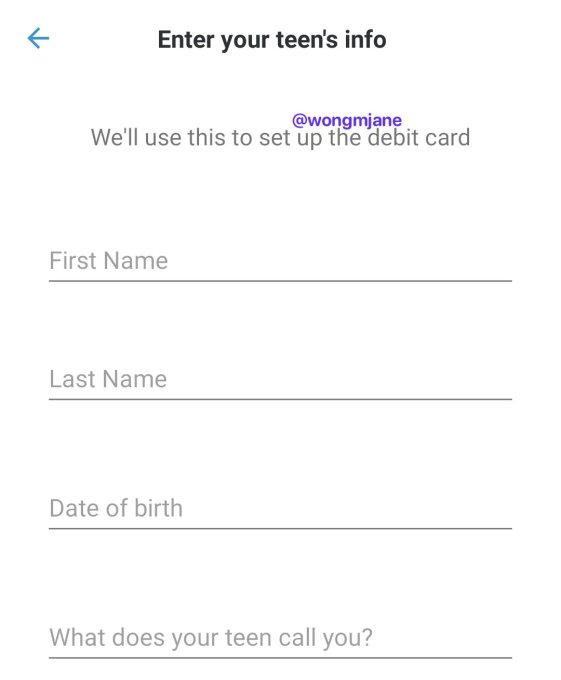

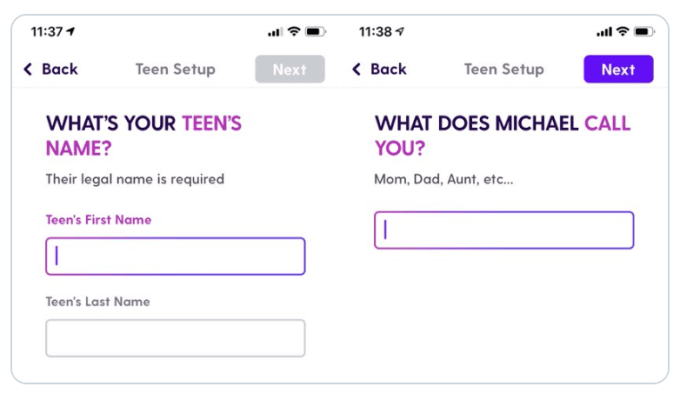

The first signs of Venmo’s debit card were spotted by reverse engineering specialist Jane Manchun Wong, who has provided slews of accurate tips to TechCrunch in the past. Hidden in Venmo’s Android app is code revealing a “delegate card” feature, designed to let users create a debit card that’s connected to their account but has limited privileges.

A screenshot generated from hidden code in Venmo’s app, via Jane Manchun Wong

A set-up screen Wong was able to generate from the code shows the option to “Enter your teen’s info,” because “We’ll use this to set up the debit card.” It asks parents to enter their child’s name, birth date and “What does your teen call you?” That’s almost identical to the “What does [your child’s name] call you?” set-up screen for Current’s teen debit card.

When TechCrunch asked about the teen debit feature and when it might launch, a Venmo spokesperson gave a cagey response that implies it’s indeed internally testing the option, writing “Venmo is constantly working to identify ways to refine and enhance the user experience. We frequently test product offerings to understand the value it could have for our users, and I don’t have anything further to share right now.”

Typically, the tech company product development flow sees them come up with ideas, mock them up, prototype them in their real apps as internal-only features, test them externally with small percentages of real users, then launch them officially if feedback and data is positive throughout. It’s unclear when Venmo might launch teen debit cards, though the product could always be scrapped. It’d need to move fast to beat Revolut and Kard to market.

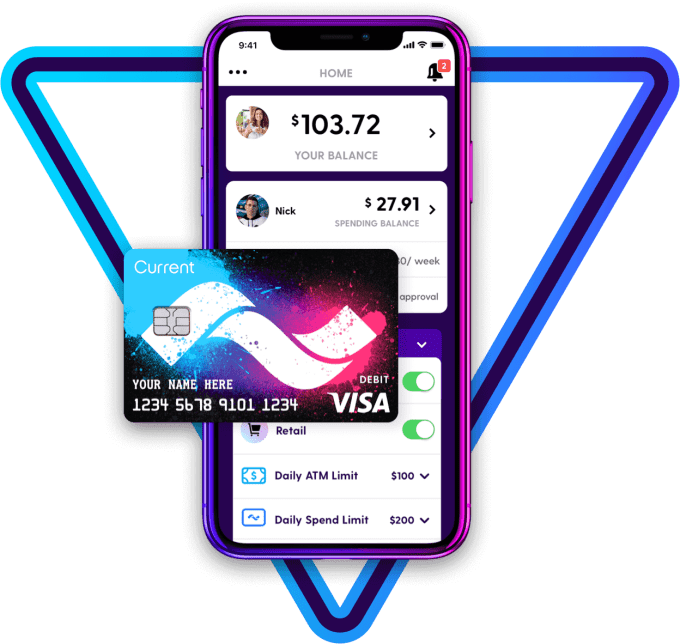

Current’s teen debit card

The launch would build upon the June 2018 launch of Venmo’s branded Mastercard debit card that’s monetized through interchange fees and interest on savings. It offers payment receipts with options to split charges with friends within Venmo, free withdrawls at MoneyPass ATMs, rewards and in-app features for reseting your PIN or disabling a stolen card. Venmo also plans to launch a credit card issued by Synchrony this year.

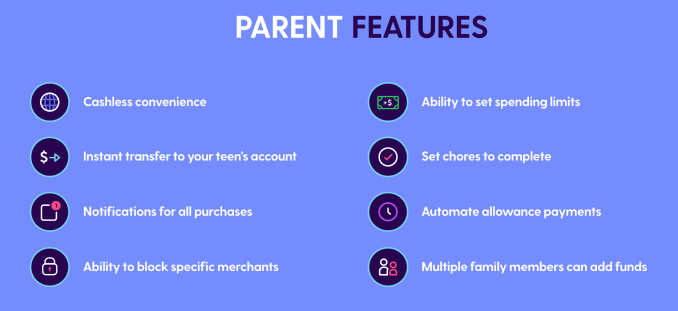

Venmo might look to equip its teen debit card with popular features from competitors, like automatic weekly allowance deposits, notifications of all purchases or the ability to block spending at certain merchants. It’s unclear if it will charge a fee like the $36 per year subscription for Current.

Current offers these features for parents who set up a teen debit card

Tech startups are increasingly pushing to offer a broad range of financial services where margins are high. It’s an easy way to earn cheap money at a time when unit economics are coming under scrutiny in the wake of the WeWork implosion. Investors are pinning their hopes on efficient financial services too, pouring $34 billion into fintech startups during 2019.

Venmo’s already become a popular way for younger people to split the bill for Uber rides or dinner. Bringing social banking to a teen demographic probably should have been its plan all along.

Powered by WPeMatico

Fintech startup Revolut lets you earn interest on your savings thanks to a new feature called savings vaults. That feature is currently only available to users living in the U.K. and paying taxes in the U.K.

The company has partnered with Flagstone for that feature. For now, the feature is limited to Revolut customers with a Metal subscription (£12.99 per month or £116 per year). But Revolut says that it will be available to Revolut Premium and Standard customers in the near future.

Savings vaults work pretty much like normal vaults. You can create sub-accounts in the Revolut app to put some money aside. And Revolut offers you multiple ways to save. You can round up all your card transactions to the nearest pound and save spare change in a vault.

You also can set up weekly or monthly transactions from your main account to a vault. And, of course, you can transfer money manually whenever you want.

Metal customers in the U.K. can now turn normal vaults into savings vaults. The only difference is that you’re going to earn interest — Revolut pays that interest daily. You can take money from your savings vault whenever you want.

Revolut promises 1.35% AER interest rate up to a certain limit. If you put a huge sum of money in your savings vault, you’ll get a lower interest rate above the limit. Your money is protected by the FSCS up to a value of £85,000 for eligible customers.

Powered by WPeMatico

Two years ago, we created the Matrix FinTech Index to highlight what we saw as the beginnings of a 10+ year mega innovation wave in financial services.

The trillion-dollar financial services industry was going to be turned on its head over the next decade, and we were just getting started. At the time, the top 10 publicly traded U.S. fintech companies had just surpassed the $100 billion mark in terms of total market capitalization, 12 unicorns had emerged in the category, and the U.S. VC industry had just poured in $6.7B — a record at the time.

As we predicted last year, the innovation cycle continues, and we are transitioning into its mid-phase. So what happened in U.S. fintech in 2019? In short, monster growth.

On the public side, fintechs delivered resoundingly. PayPal alone gained $26B in market capitalization. On a return basis, the public Matrix FinTech Index continued to crush every major equity index as well as the financial services incumbents. Nicely matching our forecasts, our Index delivered 213% returns over the last three years. The Index outperformed the financial services incumbents by 151 percentage points and the S&P 500 by 170 percentage points.

Powered by WPeMatico

Over the past year, startup banks have proven that they have a shot at disrupting retail banking. These challengers have amassed a war chest of funding, announced some ambitious international expansion plans and attracted millions of customers.

And yet, building a bank has proven to be even harder than building a startup in general. Retail banks aren’t willing to sit back and watch startups eat their lunch. Here’s a look back at the biggest moves of the year from challenger banks, some trends you should keep an eye on and the upcoming challenges for those startups.

Due to the regulatory framework and the size of the market, it is much easier to launch a challenger bank in Europe compared to anywhere else in the world. That’s why challenger banks have been thriving in Europe.

When a company gets a full banking license from the central bank of a EU country, the startup can passport its license across all EU countries and operate across the continent.

N26 raised a ton of money in 2019: last January, the Berlin-based startup announced a $300 million funding round, raising another $170 million in July. The company is now valued at $3.5 billion.

With more than 3.5 million customers in Europe, N26 announced some ambitious expansion plans. N26 is now live in the U.S. and is already planning a launch in Brazil.

Revolut has also been aggressively expanding in order to beat its competitors to new markets. In addition to its home market in the U.K., Revolut is available across Europe. In 2019, the company expanded to Singapore and Australia and currently has at least 8 million users.

While Revolut announced that it should launch in the U.S. and Canada by the end of last year, the clock ran out on that prediction. The startup has been very transparent about its expansion plans, even though it sometimes means that you have to wait months or even years before a full rollout.

For instance, Revolut announced in September 2018 that it would launch in New Zealand, Hong Kong and Japan “in the coming months.” It later became “early 2019,” then “2019.” India, Brazil, South Africa, Mexico and the UAE have also all been mentioned at some point. In other words: launching a banking product in a new country is hard.

The U.S. is a tedious market as you have to get a license in all 50 states to operate across the country

Monzo has been doing well at home in the U.K. It has attracted 3 million customers and raised £113 million (~$144m) in funding last year from Y Combinator’s Continuity fund. It is expanding to the U.S., but the rollout has been slow.

Nubank is another well-funded challenger bank. Backed by Tencent, the startup has raised a $400 million Series F round from TCV. According to the WSJ, the startup has a valuation above $10 billion.

Originally from Brazil, Nubank expanded to Mexico and has plans to expand to Argentina.

Chime is increasingly looking like the bigger player in the U.S., recently raising a $500 million funding round and reached a valuation of $5.8 billion. It only operates in the U.S.

Starling Bank and Atom Bank only operate in the U.K. Bunq is based in Amsterdam with a product tailor-made for the Netherlands, but it accepts customers across Europe.

This isn’t meant to be an exhaustive list as it’s becoming increasingly hard to cover all challenger banks.

There are a few basic features that separate challenger banks from legacy retail banks. Signing up is extremely simple and only requires a mobile app. The mobile app itself is usually much more polished than traditional banking apps.

Users receive a Mastercard or Visa debit card that communicates with the company’s server for each transaction. This way, users can receive instant notifications, block and unblock their cards and turn off some features, such as foreign payments, ATM withdrawals and online transactions.

Challenger banks usually customers promise no markup fees on transactions in foreign currencies, but there are sometimes some limits on this feature.

So how do these companies make money? When you pay with your card, banks generate a tiny, tiny interchange fee of money on each transaction. It’s really small, but it could become serious revenue at scale with tens of millions or hundreds of millions of users.

Challenger banks also offer other financial services like insurance products, foreign exchange or consumer credit. Some challenger banks develop those features in house, but many of those features are actually managed by external fintech partners. Challenger banks generate a commission on those products.

But the most promising product is premium subscriptions. While challenger banks started with free accounts and low, transparent fees, they have been selling premium subscriptions for a fixed monthly fee.

Challenger banks have become a software-as-a-service industry with a freemium component

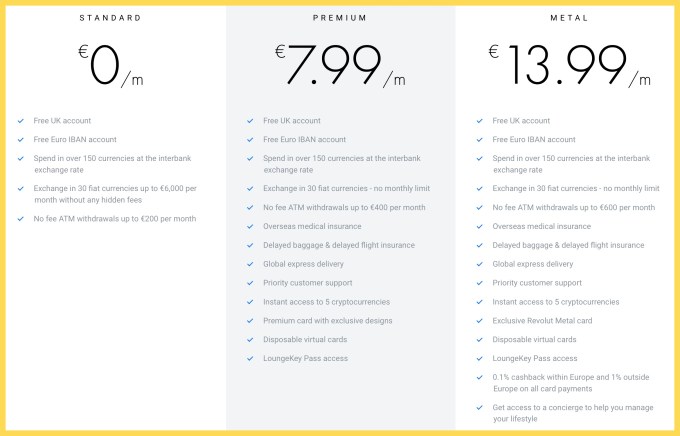

For example, Revolut offers premium accounts for €7.99 per month with higher limits, some insurance benefits that you’d expect from a premium card and access to advanced features, such as cryptocurrencies and disposable virtual cards. There’s a super premium product for €13.99 called Metal with a metal card design, cashback on card payments and access to a concierge feature.

This seems a bit counterintuitive, but premium subscriptions have been performing well, according to discussions with people working in the industry. You pay a lot in subscription fees in order to avoid small transactional fees. (And you also get a cool card.)

Challenger banks have become a software-as-a-service industry with a freemium component. It leads to a premium positioning and high expectations from customers.

Revolut’s fees top out at €13.99/month.

Powered by WPeMatico

Fintech startup Revolut is adding a key feature for users who want to replace their traditional bank account altogether. You can now pay with GBP direct debits. Revolut already added EUR direct debits last year.

While most people use cards to pay for goods and services in the U.K., some businesses require you to pay with direct debit. It can be a utility bill, a gym membership or a phone contract for instance.

Compared to card transactions, direct debits pull money directly from your account and transfer it to the recipient’s account. It doesn’t go through Mastercard or Visa. Some businesses love direct debits because it’s usually cheaper than card processing fees. Direct debits also don’t have an expiry date, unlike cards.

Customers from the European Economic Area can now share their GBP account details for direct debits in the U.K. Direct debits are protected against some fraud and payment errors by the U.K. Direct Debit Guarantee.

Revolut has partnered with Modulr for this feature as it uses Modulr’s API. Business customers will also be able to take advantage of direct debits. You can now pay suppliers with your account details, which could be convenient for large sums of money for instance.

Powered by WPeMatico