revenue-based financing

Auto Added by WPeMatico

Auto Added by WPeMatico

Revenue-based investing (RBI), also known as revenue-based financing, or revenue-share investing,1 is a natural next step for the private equity and early-stage venture investment industry. However, due to RBI being a relatively new model, publicly available data is limited.

To address this foundational gap in market information, we have developed a proprietary data set of 32 RBI investment firms, 57 distinct funds and 134 companies that have secured revenue-based investing.

Bootstrapp developed this extensive analysis on revenue-based investing for the purpose of accelerating the shift toward greater transparency and standardization within the industry.

Upon thoroughly analyzing the data, we’ve been able to identify the total number of investment firms and amount of capital that comprise the RBI industry, the specific verticals and business models that are most actively leveraging RBI, and the typical profile of companies that access this form of capital.

These findings are summarized below; a full industry-spanning report that defines the overall revenue-based investing market as it stands today is available to download here.

As context, the financial structures used by VCs haven’t evolved much since they first emerged in 1957. Today, the model is almost precisely the same, with only incremental changes such as more efficient capital markets and industry standards for structuring deals, pricing companies and more.

More recently, we have seen numerous new investment models and financing instruments, including shared earnings agreements and point-of-sale capital. One of the most prominent and popular new models for investors is revenue-based investing (RBI).

However, because the model is new, there is a lack of publicly available data, industry standards have not yet been fully established, and similarly to the equity investment market, there is little transparency into the cost of capital that investees truly pay in exchange for taking on a revenue-based investment.

Thankfully, there have been some notable efforts to drive transparency in the RBI market. For example, Bigfoot Capital open-sourced its RBI model, outlining it in a blog post and sharing their RBI financial model and anonymized term sheet, but a thorough, quantitative, industry-wide analysis has not been conducted until now.

In order to raise RBI, the company must normally be generating revenue, but is not necessarily required to be profitable, although profitability, or at least a near-term path to profitability, is often an important criteria for many investors. “For startups with revenue, RBI may be a good option because, even though the startup may not be profitable, it can reduce dilution — especially for founders,” said Emily Campbell of The Campbell Firm PLLC, a law firm that represents serial entrepreneurs and venture-backed businesses.

“Taking in some smart equity or convertible debt and balancing that money with other financing can be a good strategy for a startup,” she said. Profitability decreases the risk of default and assures that the investee has the ability to service the debt.

In regards to the applications that are best suited to RBI, B2B software-as-a-service (SaaS) companies rise to the top of the list primarily because one is able to — in essence — securitize the revenue being generated by a company and then lend capital against that theoretical security. In addition to SaaS companies, RBI is being used quite frequently in the impact investing community as it solves the problem of a lack of normal M&A or IPO exit paths for impact-driven companies and are sometimes marketed as a nonextractive form of investment structure.

Beyond B2B SaaS and impact investing, many other verticals are adopting the model as well, including e-commerce/D2C, consumer software, food and beverage, and more. It ought to be noted, however, that regardless of the specific business model a company employs, the investee is typically required to have repeatable sales and a track record that demonstrates a strong revenue stream, and therefore a clear ability to return the capital to the investors.

We have identified 32 U.S.-based firms actively investing via a revenue-based investing instrument, with those firms managing 57 distinct funds representing an estimated $4.31 billion in capital. Through our analysis of those firms, funds and investees, we found that:

Firms were included in the data set (and by extension, determined to be actively making revenue-based investments) if they:

The specific number of firms we believe to be quite accurate, representing only active, U.S.-based revenue-based investing firms. The number of funds, however, may be underestimated. This is due to the fact that, although each firm is associated with at least one fund, we did not include additional funds beyond that unless they were confirmed through other sources, such as the firms’ public communications, their SEC Form D or other sources as outlined in the methodology section at the conclusion of the full report.

The total amount of RBI capital that has already been allocated to companies across all firms and all years is $2.1 billion. However, it should be noted that this includes the outliers in our dataset, namely Kapitus, Clearbanc, Braavo and United Capital Source. Once we remove those firms, the remaining 28 firms, representing 51 funds, have allocated $592.8 million.

This figure of $592.8 million is almost certainly an underestimate due to the fact that only 19 of 32 firms had a known “amount of allocated capital,” whereas the remaining 13 firms have unknown values (i.e., zeros) for the amount of capital they have allocated thus far. Therefore, if all 32 firms had a valid and confirmed amount of allocated capital, we can logically conclude that the number would rise dramatically from the current figure of $592.8 million.

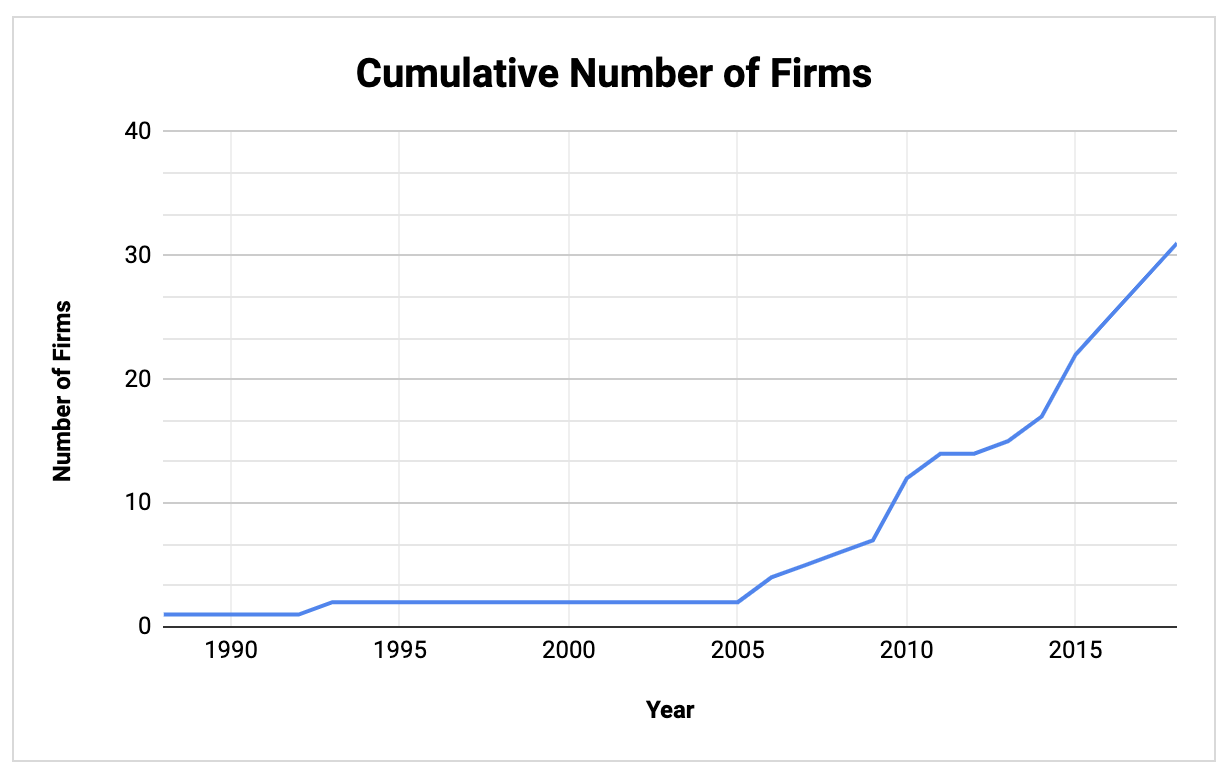

New RBI firms have been founded every year since 2013. In 2010, five firms were founded and in 2015 four additional firms were founded, then from 2014-2019, two or more firms were founded each year.

Image Credits: Bootstrapp (opens in a new window)

Clearly, there has been a major uptick in RBI firms being founded since 2005, with a relatively consistent number of new firms being founded over the 15 years since then. In the last 10 years alone, 25 RBI firms have been founded.

Powered by WPeMatico

Most founders who are raising capital look first to traditional equity VCs. But should they? Or should they look to one of the new wave of revenue-based investors?

Revenue-based investing (“RBI”) is a new form of VC financing, distinct from the preferred equity structure most VCs use. RBI normally requires founders to pay back their investors with a fixed percentage of revenue until they have finished providing the investor with a fixed return on capital, which they agree upon in advance.

This guest post was written by David Teten, Venture Partner, HOF Capital. You can follow him at teten.com and @dteten. This is the 5th part of our series on Revenue-based investing VC that touches on:

Powered by WPeMatico

This guest post was written by David Teten, Venture Partner, HOF Capital. You can follow him at teten.com and @dteten. This is part of an ongoing series on revenue-based investing VC that will hit on:

A new wave of revenue-based investors are emerging who are using creative investing structures with some of the upside of traditional VC, but some of the downside protection of debt.

I’ve been a traditional equity VC for 8 years, and I’m researching new business models in venture capital. As I’ve learned about this model, I’ve been impressed by how these venture capitalists are accomplishing a major social impact goal… without even trying to.

Many are reporting that they’re seeing a more diverse pool of applicants than traditional equity VCs — even though virtually none have a particular focus on women or underrepresented founders. In addition, their portfolios look far more diverse than VC industry norms.

For context, revenue-based investing (“RBI”) is a new form of VC financing, distinct from the preferred equity structure most VCs use. RBI normally requires founders to pay back their investors with a fixed percentage of revenue until they have finished providing the investor with a fixed return on capital, which they agree upon in advance. For more background, see “Revenue-based investing: A new option for founders who care about control“.

I contacted every RBI venture capital investor I could identify, and learned:

By contrast, according to PitchBook Data, since the beginning of 2016, companies with women founders have received only 4.4% of venture capital deals. Those companies have garnered only about 2% of all capital invested. This is despite the fact that the data says that in fact you’re better off investing in women.

Paul Graham href=”http://www.paulgraham.com/bias.html”> observes, “many suspect that venture capital firms are biased against female founders. This would be easy to detect: among their portfolio companies, do startups with female founders outperform those without?

A couple months ago, one VC firm (almost certainly unintentionally) published a study showing bias of this type. First Round Capital found that among its portfolio companies, startups with female founders outperformed those without by 63%.”

Image via Getty Images / runeer

Why are RBI investors investing disproportionately in women & underrepresented founders, and vice versa: why do these founders approach RBI investors?

I’d argue it’s not that RBI is so unbiased and attractive; it’s that traditional equity VC is biased structurally against some women and underrepresented founders.

The Boston Consulting Group and MassChallenge, a US-based global network of accelerators, partnered to study why “women-owned startups are a better bet”. Through their analysis and interviews, BCG identified three primary reasons why female founders are less likely to receive VC funds.

The study used multivariate regression analysis to control for education levels and pitch quality to conclude that gender was a statistically significant factor. I argue that these 3 reasons are much less applicable for RBI investors than for conventional VCs.

Traditional equity VCs are looking for high-risk, high-reward, “swing for the fences” models. The founders of such companies inherently are taking financial risk, reputational risk, and career risk.

Paul Graham, co-founder of Y Combinator, said, “few successful founders grew up desperately poor.” Ricky Yean, a serial founder, agrees: “building and sustaining a company that is “designed to grow fast” is especially hard if you grew up desperately poor”.

Most of the founders of the paradigmatic VC home runs were privileged: male, cisgender, well-educated, from affluent families, etc. Think Bill Gates and Mark Zuckerberg .

That privilege makes it easier for them to take very high risk. The average person, worried about students loans and long term employability, quite rationally is less likely to take the huge risk of founding a company. It’s far safer to just get a job.

Investors who back diverse teams can win much higher returns than the industry norm. Both RBI investors and the founders they back will hopefully benefit from this pattern.

Note that none of the lawyers quoted or I are rendering legal advice in this article, and you should not rely on our counsel herein for your own decisions. I am not a lawyer. Thanks to the experts quoted for their thoughtful feedback.

Powered by WPeMatico

You’re working on launching a new VC fund; congratulations! I’ve been a traditional equity VC for 8 years, and I’m now researching revenue-vased investing and other new approaches to VC. The question I’m asking myself: should a new VC fund use revenue-based investing, traditional equity VC, or possibly both (likely from two separate pools of capital)?

Revenue-based investing (“RBI”) is a new form of VC financing, distinct from the preferred equity structure most VCs use. RBI normally requires founders to pay back their investors with a fixed percentage of revenue until they have finished providing the investor with a fixed return on capital, which they agree upon in advance.

This guest post was written by David Teten, Venture Partner, HOF Capital. You can follow him at teten.com and @dteten. This is part of an ongoing series on Revenue-based investing VC that will hit on:

From the investors’ point of view, the advantages of the RBI models are manifold. In fact, the Kauffman Foundation has launched an initiative specifically to support VCs focused on this model. The major advantages to investors are:

Powered by WPeMatico

This guest post was written by David Teten, Venture Partner, HOF Capital. You can follow him at teten.com and @dteten. This is part of an ongoing series on Revenue-Based Investing VC that will hit on:

So you’re interested in raising capital from a Revenue-Based Investor VC. Which VCs are comfortable using this approach?

A new wave of Revenue-Based Investors (“RBI”) are emerging. This structure offers some of the benefits of traditional equity VC, without some of the negatives of equity VC.

I’ve been a traditional equity VC for 8 years, and I’m now researching new business models in venture capital.

(For more background, see the accompanying article “Revenue-based investing: A new option for founders who care about control” published on Extra Crunch.

RBI normally requires founders to pay back their investors with a fixed percentage of revenue until they have finished providing the investor with a fixed return on capital, which they agree upon in advance.

I’ve listed below all of the major RBI venture capitalists I’ve identified. In addition, I’ve noted a few multi-product lending firms, e.g., Kapitus and United Capital Source, which provide RBI as one of many structural options to companies seeking capital.

Alternative Capital: “You qualify if you have $5k+ MRR. We have a special program if you are pre-seed and need product development. Since 2017 we’ve managed $3 million in revenue-based financing, which helps cash-strapped technology companies grow. In 2019 we partnered with several revenue-based lending providers, effectively creating a marketplace.”

Bigfoot Capital: According to Brian Parks, “Bigfoot provides RBI, term loans, and lines of credit to SaaS businesses with $500k+ ARR. Our wheelhouse is bootstrapped (or lightly capitalized) SMB SaaS. We make fast, data-driven credit decisions for these types of businesses and show Founders how the math/ROI works. We’re currently evaluating about 20 companies a month and issuing term sheets to 25% of them; those that fit our investment criteria. We’re also regularly following-on for existing portfolio companies.”

Investment Criteria:

Benefits:

Corl: “No need to wait 3-9 months for approval. Find out in 10 minutes. Corl can fund up to 10x your monthly revenue to a maximum of $1,000,000. Payments are equal to 2-10% of your monthly revenue, and stop when the business buys out the contract at 1-2x the investment amount.”

According to Derek Manuge, Corl CEO, “Funds are closed significantly quicker than the industry average at under 24 hours. The majority of businesses that apply for funding with Corl are E-commerce, SaaS, and other digital businesses.”

Manuge continues, “Corl connects to a business’ bank accounts, accounting software, payment processors, and other digital services to collect 10,000+ historical data points that are analyzed in real-time. We collect more data on an individual business than, to our knowledge, any other RBI investor, through our application process, data partners, and various public sources online. We have reviewed the application process of other RBI lenders and have not found one that has more API connections that ours. We have developed a proprietary machine learning algorithm that assesses the risk and return profile of the business and determines whether to invest in the business. Funding decisions can take as little as 10 minutes depending on the amount of data provided by a business.”

In the past 12 months, 500+ companies have applied for funding with Corl. The following information is based on companies funded by us and/or our capital partners:

Decathlon Capital: According to John Borchers, Co-founder, Decathlon is the largest revenue-based financing investor in the US. His description: “We announced a new $500 million fund in Q1 of 2019, in our 10th year. Unlike many RBI investors, a full 50% of our investment activity is in non-tech businesses. Like other RBI firms, Decathlon does not require warrants, governance involvement, or the types of financial covenants that are often associated with other venture debt type solutions. Decathlon typically targets monthly payment percentages in the 1% to 4% range, with total targeted multiples of 1.5x to 3.0x.”

Earnest Capital: Earnest is not technically RBI. Tyler Tringas, General Partner, observes, “Almost all of these new [RBI] forms of financing really only work for more mature companies (say $25-50k MRR and up) and there are still very few new options at the stage where we are investing.” From their website: “We invest via a Shared Earnings Agreement, a new investment model developed transparently with the community, and designed to align us with founders who want to run a profitable business and never be forced to raise follow-on financing or sell their business.” Key elements:

Feenix Venture Partners: Feenix Venture Partners has a unique investment model that couples investment capital with payment processing services. Each of Feenix’s portfolio companies receives an investment in debt or equity and utilizes a subsidiary of Feenix as its credit card payment processor (“Feenix Payment Systems”). The combination of investment capital and credit card processing (CCP) fees creates a “win-win” partnership for investors and portfolio companies. The credit card processing data provides the investor with real-time sales transparency and the CCP fee margin provides the investor high current income, with equity-like upside and significant recovery for downside protection. Additionally, portfolio companies are able to access competitive and often non-dilutive financing by monetizing an unavoidable expense that is being paid to its current processors, thus yielding a mutual benefit for both parties.

Feenix focuses on companies in the consumer space across a number of industry verticals including: multi-unit Food & Beverage operators, hospitality, managed workspace (office or food halls), location-based entertainment venues, and various direct to consumer online companies. Their average check size is between $1-3 million, with multi-year term and competitive interest rates for debt. Additionally, Feenix typically needs fewer financial covenants and can provide quicker turnaround for due diligence with the benefit of transparency they receive by tracking credit card sales activity. 10% of Feenix’s portfolio companies have received VC equity prior to their financing.

Founders First Capital Partners: “Founders First Capital Partners, LLC is building a comprehensive ecosystem to empower underrepresented founders to become leading premium wage job creators within their communities. We provide revenue-based funding and business acceleration support to service-based small businesses located outside of major capital markets such as Silicon Valley and New York City.”

“We focus our support on businesses led by women, ethnic minorities, LGBTQ, and military veterans, especially teams and businesses located in low to moderate income areas. Our proprietary business accelerator programs, learning platform, and growth methodologies transition these underserved service-based businesses into companies with $5 million to $50 million in recurring revenue. They are tech-enabled companies that provide high-yield investments for fund limited partners (LPs) that perform like bonds but generate returns on par with equity investments. Founders First Capital Partners defines these high performing organizations as Zebra Companies .”

“Each year, Founders First Capital Partners works with hundreds of entrepreneurs. Three tracks of pre-funding accelerator programs determine the appropriate level of funding and advisory support needed for each founder to achieve their desired expansion: 1) Fastpath for larger companies with $2 million to $5 million in annual revenue, 2) Founders Growth Bootcamp program for companies with $250,000 to $2 million in annual revenue, and 3) Elevate My Business Challenge for companies with $50,000 to $250,000 in annual revenue.”

“Founders First Capital Partners (FFCP) runs a 5-step process:

According to Kim Folson, Co-Founder, “Founders First Capital Partner (F1stcp) has just secured a $100M credit facility commitment from a major institutional impact investor. This positions F1stcp to be the largest revenue-based investor platform addressing the funding gap for service-based, small businesses led by underserved and underrepresented founders.”

GSD Capital: “ GSD Capital partners with early-stage SaaS founders to fund growth initiatives. We work with founding teams in the Mountain West (Arizona, Colorado, Idaho, Montana, Nevada, New Mexico, Utah and Wyoming) who have demonstrated an ability to get sh*t done… We empower founders with a 30-day fundraising process instead of multiple months running a gauntlet. ”

“To best explain the process of RBF funding, let’s use an example. Pied Piper Inc needs funding to accelerate customer acquisition for its SaaS solution. GSD Capital loans $250,000 to Pied Piper taking no ownership or control of the business. The funding agreement outlines the details of how the loan will be repaid, and sets a “cap”, or a point at which the loan has been repaid. On a 3-year term, the cap amounts typically range from 0.4-0.6x the loan amount. Each month Pied Piper reviews its cash receipts and sends the agreed upon percentage to GSD. If the company experiences a rough patch, GSD shares in the downside. Monthly payments stop once the cap is reached and the loan is repaid. In a situation where Pied Piper’s revenue growth exceeds expectations, prepayment discounts are built into the structure, lowering the cost of capital.”

“Requirements for funding consideration:

Indie.VC: Part of the investment firm O’Reilly AlphaTech Ventures. See Indie VC’s Version 3.0 . “On the surface, our v3 terms are a fairly vanilla version of a convertible note with a few key variables to be negotiated between the investor and the founder: investment amount, equity option, and repurchase start date and percentage.”

Kapitus: Offers RBI among many other options. “Because this [RBI] is not a loan, there is no APR or compounded interest associated with this product. Instead, borrowers agree to pay a fixed percentage in addition to the amount provided.”

Lighter Capital: “Since 2012, we’ve provided over $100 million in growth capital to over 250 companies.” Revenue-based financing which “helps tech entrepreneurs get to the next level without giving up equity, board seats, or personal guarantees… At Lighter Capital, we don’t take equity or ask you to make personal guarantees. And we don’t take a seat on your board or make you write a big check if you’re having a down month.”

Novel Growth Partners: ” We invest using Revenue-Based Investing (RBI), also known as Royalty-Based Investing… We provide up to $1 million in growth capital, and the company pays that capital back as a small percentage (between 4% and 8%) of its monthly revenue up to a predetermined return cap of 1.5-2.2x over up to 5 years. We can usually provide capital in an amount up to 30% of your ARR. Our approach allows us to invest without taking equity, without taking board seats, and without requiring personal guarantees. We also provide tailored, tactical sales and marketing assistance to help the companies in our portfolio accelerate their growth.” Keith Harrington, Co-Founder & Managing Director at Novel Growth Partners, observes that he sees two categories of RBI:

He said, “We chose the structure we did because we think it’s easier to understand, for both LPs and entrepreneurs.”

Podfund: Focused on podcast creators. “We agree to provide funding and services to you in exchange for a percentage of total gross revenue (including ads/sponsorship, listener support, and ancillary revenue such as touring, merchandise, or licensing) per quarter. PodREV terms are 7-15% of revenue for 3-5 years, depending on current traction, revenue, and projected growth. At any time you may also opt to pay down the revenue share obligation in full, as follows:

RevUp: “Companies receive $100K-250K in non-dilutive cash… [paid back in a] 36-month return period with revenue royalty ranging from 4-8%, no equity .”

Riverside Acceleration Capital: Closed Fund I for $50m in 2016. Fund II has raised over $100m as of mid-2019.

” Investment size : $1 – 5+ million, significant capacity for additional investment.

Return method: Small percentage of monthly revenue. Keeps capital lightweight and aligned to companies’ growth.

Capped return: 1.5 – 2x the investment amount. Company maximizes equity upside from growth.

Investment structure: 5-year horizon. Long-term nature maximizes flexibility of capital.”

Jim Toth writes, “One thing that makes us different is that we live inside of an $8Bn private equity firm. This means that we have a tremendous amount of resources that we can leverage for our companies, and our companies see us as being quite strategic. We also have the ability to continue investing behind our companies across all stages of growth.”

ScaleWorks: “We developed Scaleworks venture finance loans to fill a need we saw for our own B2B SaaS companies. No personal guarantees, board seats, or equity sweeteners. No prepayment penalties. Monthly repayments as a percentage of revenue.”

United Capital Source: Provides a wide structure of loans, including but not limited to RBI. The firm has provided more than $875 million in small business loans in its history, and is currently extending about $10m/month in RBI loans. Jared Weitz, Founder & CEO, said, “[Our] typical RBF client is $120K-$20M in annual revenue, with 4-200 employees. We only look at financials for deals over a certain size.

For smaller deals, we’ll look at bank statements and get a pretty good picture of revenues, expenses and cash flow. After all, since this is a revenue-based business loan, we want to make sure revenues and cash flow are consistent enough for repayment without hurting the business’s daily operations. When we do look at financials to approve those larger deals we are generally seeing a 5 to 30% EBITDA margin on these businesses.” United Capital Source was selected in the 2015 & 2017 Inc. 5000 Fastest Growing Companies List.

Note that none of the lawyers quoted or I are rendering legal advice in this article, and you should not rely on our counsel herein for your own decisions. I am not a lawyer. Thanks to the experts quoted for their thoughtful feedback. Thanks to Jonathan Birnbaum for help in researching this topic.

Powered by WPeMatico

Does the traditional VC financing model make sense for all companies? Absolutely not. VC Josh Kopelman makes the analogy of jet fuel vs. motorcycle fuel. VCs sell jet fuel which works well for jets; motorcycles are more common but need a different type of fuel.

A new wave of Revenue-Based Investors are emerging who are using creative investing structures with some of the upside of traditional VC, but some of the downside protection of debt. I’ve been a traditional equity VC for 8 years, and I’m now researching new business models in venture capital.

I believe that Revenue-Based Investing (“RBI”) VCs are on the forefront of what will become a major segment of the venture ecosystem. Though RBI will displace some traditional equity VC, its much bigger impact will be to expand the pool of capital available for early-stage entrepreneurs.

This guest post was written by David Teten, Venture Partner, HOF Capital. You can follow him at teten.com and @dteten. This is part of an ongoing series on Revenue-Based Investing VC that will hit on:

RBI structures have been used for many years in natural resource exploration, entertainment, real estate, and pharmaceuticals. However, only recently have early-stage companies started to use this model at any scale.

According to Lighter Capital, “the RBI market has grown rapidly, contrasting sharply with a decrease in the number of early-stage angel and VC fundings”. Lighter Capital is a RBI VC which has provided over $100 million in growth capital to over 250 companies since 2012.

Lighter reports that from 2015 to 2018, the number of VC investments under $5m dropped 23% from 6,709 to 5,139. 2018 also had the fewest number of angel-led financing rounds since before 2010. However, many industry experts question the accuracy of early-stage market data, given many startups are no longer filing their Form Ds.

John Borchers, Co-founder and Managing Partner of Decathlon Capital, claims to be the largest revenue-based financing investor in the US. He said, “We estimate that annual RBI market activity has grown 10x in the last decade, from two dozen deals a year in 2010 to upwards of 200 new company fundings completed in 2018.”

Powered by WPeMatico

Revenue-based financing is on the rise, at least according to Lighter Capital, a firm that doles out entrepreneur-friendly debt capital.

What exactly is RBF you ask? It’s a relatively new form of funding for tech companies that are posting monthly recurring revenue. Here’s how Lighter Capital, which completed 500 RBF deals in 2018, explains it: “It’s an alternative funding model that mixes some aspects of debt and equity. Most RBF is technically structured as a loan. However, RBF investors’ returns are tied directly to the startup’s performance, which is more like equity.”

Source: Lighter Capital

What’s the appeal? As I said, RBFs are essentially dressed up debt rounds. Founders who opt for RBFs as opposed to venture capital deals hold on to all their equity and they don’t get stuck on the VC hamster wheel, the process in which you are forced to continually accept VC while losing more and more equity as a means of pleasing your investors.

RBFs, however, are better than traditional debt rounds because the investors are more incentivized to help the companies they invest in because they are receiving a certain portion of that business’s monthly revenues, typically 1% to 9%. Eventually, as is explained thoroughly in Lighter Capital’s newest RBF report, monthly payments come to an end, usually 1.3 to 2.5X the amount of the original financing, a multiple referred to as the “cap.” Three to five years down the line, any unpaid amount of said cap is due back to the investor. When all is said in done, ideally, the startup has grown with the support of the capital and hasn’t lost any equity.

At this point, they could opt to raise additional revenue-based capital, they could turn to venture capital or they could tap a tech bank to help them get to the next step. The idea is RBF is easier on the founder and it allows them optionality, something that is often lost when companies turn to VCs.

IPO corner, rapid-fire edition

Slack’s direct listing will be on June 20th. Get excited.

China’s Luckin Coffee raised $650 million in upsized U.S. IPO

Crowdstrike, a cybersecurity unicorn, dropped its S-1.

Freelance marketplace Fiverr has filed to go public on the NYSE.

Plus, I had a long and comprehensive conversation with Zoom CEO Eric Yuan this week about the company’s closely watched IPO. You can read the full transcript here.

Silicon Valley entrepreneur Hosain Rahman, the man behind Jawbone, has managed to raise $65.4 million for his new company, according to an SEC filing. The paperwork, coincidentally or otherwise, was processed while most of the world’s attention was focused on Uber’s IPO. Jawbone, if you remember, produced wireless speakers and Bluetooth earpieces, and went kaput in 2017 after burning up $1 billion in venture funding over the course of 10 years. Ouch.

On the heels of enterprise startup UiPath raising at a $7 billion valuation, the startup’s biggest investor is announcing a new fund to double down on making more investments in Europe. VC firm Accel has closed a $575 million fund — money that it plans to use to back startups in Europe and Israel, investing primarily at the Series A stage in a range of between $5 million and $15 million, reports TechCrunch’s Ingrid Lunden. Plus, take a closer look at Contrary Capital. Part accelerator, part VC fund, Contrary writes small checks to student entrepreneurs and recent college dropouts.

Our paying subscribers are in for a treat this week. Our in-house venture capital expert Danny Crichton wrote down some thoughts on Uber and Lyft’s investment bankers. Here’s a snippet: “Startup CEOs heading to the public markets have a love/hate relationship with their investment bankers. On one hand, they are helpful in introducing a company to a wide range of asset managers who will hopefully hold their company’s stock for the long term, reducing price volatility and by extension, employee churn. On the other hand, they are flagrantly expensive, costing millions of dollars in underwriting fees and related expenses…”

Read the full story here and sign up for Extra Crunch here.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about the notable venture rounds of the week, CrowdStrike’s IPO and more of this week’s headlines.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico