renaissance capital

Auto Added by WPeMatico

Auto Added by WPeMatico

Spotify did it. Slack did it. Many other late-stage private technology companies are reported to be seriously considering it. Should yours?

If you are a board member of a late-stage, venture-backed company or part of its management team, you likely have heard of the term “direct listing.” Or you may have attended one or all of the slew of recent conferences being hosted by big-name investment banks and others, including tech investor guru Bill Gurley, who recently debated the pros and cons of choosing a direct listing over a traditional IPO.

Before you decide what’s right for your company, here are a few things you need to know about direct listings.

For people not familiar with the term, a direct listing is an alternative way for a private company to “go public,” but without selling its shares directly to the public and without the traditional underwriting assistance of investment bankers.

In a traditional IPO, a company raises money and creates a public market for its shares by selling newly created stock to investors. In some instances, a select number of pre-IPO investors, usually very large stockholders or management, may also sell a portion of their holdings in the IPO. In an IPO, the company engages investment bankers to help promote, price and sell the stock to investors. The investment bankers are paid a commission for their work that is based on the size of the IPO—usually seven percent for a traditional technology company IPO.

In a direct listing, a company does not sell stock directly to investors and does not receive any new capital. Instead, it facilitates the re-sale of shares held by company insiders such as employees, executives and pre-IPO investors. Investors in a direct listing buy shares directly from these company insiders.

Does this mean that a company doing a direct listing doesn’t need investment banks? Not quite. Companies still engage investment banks to assist with a direct listing and those banks still get paid quite well (to the tune of $35 million in Spotify and $22 million in Slack).

However, the investment banks play a very different role in a direct listing. Unlike a traditional IPO, in a direct listing, investment banks are prohibited under current law from organizing or attending investor meetings and they do not sell stock to investors. Instead, they act purely in an advisory capacity helping a company to position its story to investors, draft its IPO disclosures, educate a company’s insiders on process and strategize on investor outreach and liquidity.

The concept of a direct listing is actually not a new one. Companies in a variety of industries have used similar structures for years. However, the structure has only recently received a lot of investor and media attention because high-profile technology companies have started to use it to go public. But why have technology companies only recently started to consider direct listings?

The rise of massive pre-IPO fundraising rounds

With an abundance of investor capital, especially from institutional investors that historically hadn’t invested in private technology companies, massive pre-IPO fundraising rounds have become the norm. Slack raised over $400 million in August 2018—just over a year prior to its direct listing. Because of this widespread availability of capital, some technology companies are now able to raise sufficient capital before their actual IPO to either become profitable or put them on a path to profitability.

Criticism of current IPO process

There has been increasing negative sentiment, especially amongst well-known venture capitalists, about certain aspects of the traditional IPO process—namely IPO lock-up agreements and the pricing and allocation process.

IPO lock-up agreements. In a traditional IPO, investment bankers require pre-IPO investors, employees and the company to sign a “lock-up agreement” restricting them from selling or distributing shares for a specified period of time following the IPO—usually 180 days. The bankers put these agreements in place in order to stabilize the stock immediately after the IPO. While the merits of a lock-up agreement can certainly be debated, by the time VCs (and other insiders) are allowed to sell following an IPO, oftentimes the stock price has fallen significantly from its highs (sometimes to below the IPO price) or the post lock-up flood of selling can have an immediate negative impact on the trading price.

In a direct listing, there is no lock-up agreement, which allows for equal access to the offering to all of the company’s pre-IPO investors, including rank-and-file employees and smaller pre-IPO stockholders.

IPO pricing and allocation: In a traditional IPO, shares are often allocated directly by a company (with the assistance of its underwriters) to a small number of large, institutional investors. Traditional IPOs are often underpriced by design to provide large institutional investors the benefit of an immediate 10-15% “pop” in the stock price. Over the last few years, some of these “pops” have become more pronounced. For example, Beyond Meat’s stock soared from $25 to $73 on its first day of trading, a 163% gain. This has fueled a concern, particularly shared amongst the VC community, that investment banks improperly price and allocate shares in an IPO in order to benefit these institutional investors, which are also clients of the same investment banks that are underwriting the IPO. While the merits of this concern can also be debated, in instances where there is a large price discrepancy between the trading price of the stock following the IPO and the price of the IPO, there is often a sense that companies have left money on the table and that pre-IPO investors have suffered unnecessary dilution. If the IPO had been priced “correctly,” the company would have had to sell fewer shares to raise the same amount of proceeds.

Because a company is not selling stock in a direct listing, the trading price after listing is purely market driven and is not “set” by the company and its investment bankers. Moreover, since no new shares are issued in a direct listing, insiders do not suffer any dilution.

The Spotify effect

Before Spotify’s direct listing, technology companies hadn’t used the direct listing structure to go public. Spotify was, in many ways, the perfect test case for a direct listing. It was well known, didn’t need any additional capital and was cash flow positive. In addition, prior to its direct listing, Spotify had entered into a debt instrument that penalized the company so long as it remained private. As a result, it just needed to go public. After clearing some regulatory hurdles, Spotify successfully executed its direct listing in April 2018. After Spotify’s direct listing, Slack (relatively) quickly followed suit. Slack’s direct listing was notable because it represented the first traditional Silicon Valley-based VC-backed company to use the structure. It was also an enterprise software company, albeit one with a consumer cult following.

While a direct listing offers many benefits, the structure does not make sense for every company. Below is a list of key benefits and drawbacks:

Powered by WPeMatico

For people who make investment decisions based on revenues and projected earnings, biotech IPOs are kind of a non-starter. Not only are new market entrants universally unprofitable, most have zero revenue. Going public is mostly a means to raise money for clinical trials, with red ink expected for years to come.

That pattern may be one reason the venture capital press, Crunchbase News included, tends to devote a disproportionately small portion of coverage to biotech IPOs. It’s more exciting to watch a big-name internet company pop in first-day trading or poke fun at an underperforming dud.

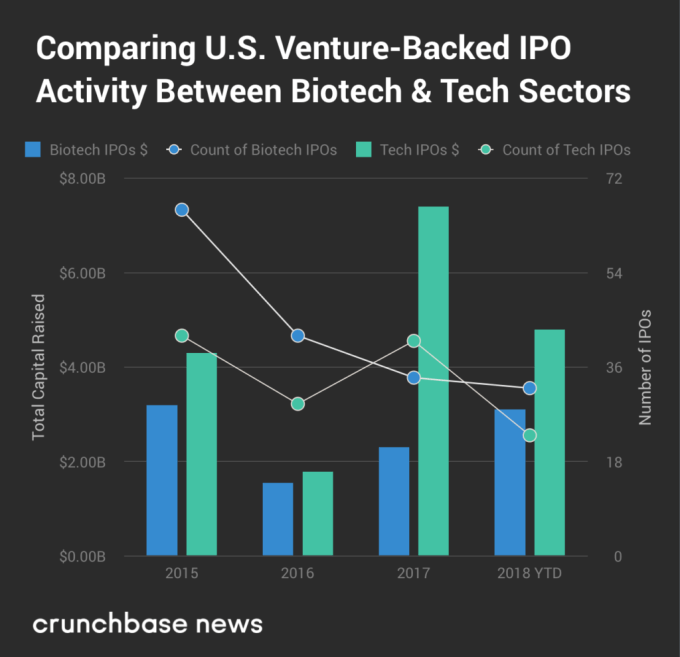

But with our fixation on all things tech, we’re missing out on the big picture. There are actually a lot more biotech and healthcare startup IPOs than tech offerings. In the second quarter of this year, for instance, at least 16 U.S. venture-backed biotech and healthcare companies went public, compared to just 11 tech startups. In three of the past four years, bio offerings outnumbered tech IPOs, according to Crunchbase data.

In the following analysis, we attempt to get up to speed on the pace of biotech offerings, assess where we are in the cycle and spotlight some of the rising stars.

As mentioned above, U.S. bio IPOs outnumber tech offerings in most years. However, the bio cohort raises less total capital, partly because the largest technology IPOs tend to be much bigger than the largest bio IPOs. In the chart below, we compare the two sectors over the past four years.

Globally, the numbers are much higher. Using Crunchbase data, we’ve put together a chart looking at global VC-backed biotech and healthcare IPOs over the past four years. While we’re just over halfway through 2018, biotech and health IPOs have already raised more money than in any of the prior three full calendar years.

It’s pretty clear we’re in an upcycle for all things startup-related. VCs are flush with cash, late-stage rounds are ballooning in size and IPO and M&A action is picking up, too.

So what does that mean for bio IPOs? Is the uptick in the pace and size of offerings mostly a result of bullish market conditions? Or is the current slate of pre-IPO candidates more compelling than in the past?

We turned to Bob Nelsen, co-founder of ARCH Venture Partners, one of the top-performing biotech investors, for his take, which is that it’s a “fundamentals driven, cycle amplified” IPO boomlet.

More companies are launching well-received IPOs because the pace of startup innovation is faster than in the past. Nelson calls it “the result of the previous 30 years of investment and innovation in biotech that has finally led to essentially data-driven innovation.” That’s leading to more curative treatments, disease-modifying therapies and preventative technologies.

Yet we’re also in a bullish segment of the market cycle for biotech. That’s prompting companies that might have stayed private under other conditions to give going public a shot. It’s also providing bigger outcomes for emerging companies that were already on the IPO track.

The latest example of a big outcome IPO is Rubius Therapeutics, which develops drugs based on genetically engineered red blood cells. This week, the five-year-old company raised $241 million at an initial valuation of over $2 billion, making it the largest bio offering of 2018. The Cambridge, Mass. company, which previously raised nearly a quarter-billion-dollars in venture funding, is still in the pre-clinical trial phase.

This year has delivered several other good-sized offerings as well, including drug developers Eidos Therapeutics and Homology Medicines, recently valued around $800 million each, along with Tricida, valued around $1.2 billion. (See the full list of 2018 global bio and health offerings here.)

As for aftermarket performance, that’s been up and down, but includes some big ups. Last year, biotech led the pack for best-performing IPOs on U.S. exchanges. The sector accounted for four of the six top spots, according to Renaissance Capital, led by drug developers AnaptysBio, Argenx and UroGen, along with Calyxt, an agbio startup.

While things are already up, bio VCs, generally an optimistic bunch, see several reasons why bio IPOs could go higher.

Nelson points to what he sees as the lagging pace of in-house innovation at big pharma and biotech players. Increasingly, they need to acquire startups and recently public companies to stay competitive and build out new product pipelines.

There is also tons of fresh capital earmarked for healthcare startups. In the U.S. in 2017, healthcare-focused venture capitalists raised $9.1 billion. That figure was up 26 percent from 2016, per Silicon Valley Bank.

More dollars also are flowing from venture firms that invest in a mix of tech and life sciences through a single fund. That list includes well-established VCs with dry powder to invest, including Polaris Partners, Founders Fund, Kleiner Perkins and Sequoia Capital.

Still, Nelson observes, deep into an IPO bull market, the average quality of offerings does tend to decline. That said, he’s been through similar inflection points in previous cycles and “for the same point in the cycle, the quality is markedly higher.”

Powered by WPeMatico