real estate tech

Auto Added by WPeMatico

Auto Added by WPeMatico

Nearly exactly one month ago, digital real estate platform Loft announced it had closed on $425 million in Series D funding led by New York-based D1 Capital Partners. The round included participation from a mix of new and existing investors such as DST, Tiger Global, Andreessen Horowitz, Fifth Wall and QED, among many others.

At the time, Loft was valued at $2.2 billion, a huge jump from its being just near unicorn territory in January 2020. The round marked one of the largest ever for a Brazilian startup.

Now, today, São Paulo-based Loft has announced an extension to that round with the closing of $100 million in additional funding that values the company at $2.9 billion. This means that the 3-year-old startup has increased its valuation by $700 million in a matter of weeks.

Baillie Gifford led the Series D-2 round, which also included participation from Tarsadia, Flight Deck, Caffeinated and others. Individuals also put money in the extension, including the founders of Better (Zach Frenkel), GoPuff, Instacart, Kavak and Sweetgreen.

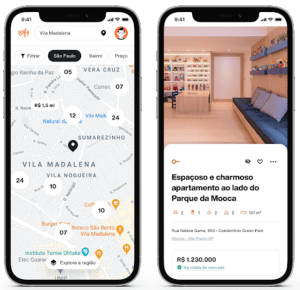

Loft has seen great success in its efforts to serve as a “one-stop shop” for Brazilians to help them manage the home buying and selling process.

Image Credits: Loft

In 2020, Loft saw the number of listings on its site increase “10 to 15 times,” according to co-founder and co-CEO Mate Pencz. Today, the company actively maintains more than 13,000 property listings in approximately 130 regions across São Paulo and Rio de Janeiro, partnering with more than 30,000 brokers. Not only are more people open to transacting digitally, more people are looking to buy versus rent in the country.

“We did more than 6x YoY growth with many thousands of transactions over the course of 2020,” Pencz told TechCrunch at the time of the company’s last raise. “We’re now growing into the many tens of thousands, and soon hundreds of thousands, of active listings.”

The decision to raise more capital so soon was due to a variety of factors. For one, Loft has received “overwhelming investor interest” even after “a very, very oversubscribed main round,” Pencz said.

“We have seen a continued acceleration in our market share growth, especially in São Paulo and Rio de Janeiro, the two markets we currently operate in,” he added. “We saw an opportunity to grow even faster with additional capital.”

Pencz also pointed out that Baillie Gifford has relatively large minimum check size requirements, which led to the extension being conducted at a higher price and increased the total round size “by quite a bit to be able to accommodate them.”

While the company was less forthcoming about its financials as of late, it told me last year that it had notched “over $150 million in annualized revenues in its first full year of operation” via more than 1,000 transactions.

The company’s revenues and GMV (gross merchandise value) “increased significantly” in 2020, according to Pencz, who declined to provide more specifics. He did say those figures are “multiples higher from where they were,” and that Loft has “a very clear horizon to profitability.”

Pencz and Florian Hagenbuch founded Loft in early 2018 and today serve as its co-CEOs. The aim of the platform, in the company’s words, is “bringing Latin American real estate into the e-commerce age by developing online alternatives to analogue legacy processes and leveraging data to create transparency in highly opaque markets.” The U.S. real estate tech company with the closest model to Loft’s is probably Zillow, according to Pencz.

In the United States, prospective buyers and sellers have the benefit of MLSs, which in the words of the National Association of Realtors, are private databases that are created, maintained and paid for by real estate professionals to help their clients buy and sell property. Loft itself spent years and many dollars in creating its own such databases for the Brazilian market. Besides helping people buy and sell homes, it offers services around insurance, renovations and rentals.

In 2020, Loft also entered the mortgage business by acquiring one of the largest mortgage brokerage businesses in Brazil. The startup now ranks among the top-three mortgage originators in the country, according to Pencz. When it comes to helping people apply for mortgages, he likened Loft to U.S.-based Better.com.

This latest financing brings Loft’s total funding raised to an impressive $800 million. Other backers include Brazil’s Canary and a group of high-profile angel investors such as Max Levchin of Affirm and PayPal, Palantir co-founder Joe Lonsdale, Instagram co-founder Mike Krieger and David Vélez, CEO and founder of Brazilian fintech Nubank. In addition, Loft has also raised more than $100 million in debt financing through a series of publicly listed real estate funds.

Loft plans to use its new capital in part to expand across Brazil and eventually in Latin America and beyond. The company is also planning to explore more M&A opportunities.

This article was updated post-publication to reflect accurate investor information.

Powered by WPeMatico

The venture capital industry is less transparent today than at any time in recent memory.

For all the talk about expanding access and improving its sordid record on diversity, in reality, it has never been harder for founders to figure out who can even write a check to their startups in the first place.

When I first returned to TechCrunch after my second stint in venture capital, my first piece was entitled “The loss of first check investors.” While working in the venture capital industry, it was maddening to see — particularly at the pre-seed and seed stages — how few investors were really willing to go out on a limb and invest in founders before another VC had committed a check.

It’s only gotten worse in the past two years since that article, and the complexity comes from a number of different places. As our investigation showed more than a year ago, fewer and fewer venture rounds are being announced through SEC Form D filings.

There are almost no publicly accountable datasets left indicating who is writing checks in the venture industry and which companies are receiving those checks. While stealthiness is valid in the early days of a startup, the excuse wears thin after years.

Powered by WPeMatico

Several months ago, we surveyed more than 20 leading real estate VCs to learn about what was exciting them most in the real estate tech sector and hear their opinions on proptech trends like co-working, flexible office space and remote office space.

Since we published our survey, COVID-19 has flipped the real estate sector on its head as more companies move toward mandatory remote work, retail businesses are forced to temporarily shut their doors and high-traffic properties thin out. Suddenly, the traditionally predictable world of real estate is more chaotic and unclear than ever.

What are the short and long-term impacts of pandemic-induced volatility? Does this open up opportunities for proptech startups or shutter them? What does this mean from an investing point of view? We asked several of the VCs that participated in our last survey to update us on how COVID-19 is impacting real estate startups, non-proptech companies in general and the broader real estate market overall:

Despite its banner year in 2019, proptech will not be immune to the pressures venture-backed companies face in a market pullback, and we are preparing ourselves and our portfolio companies for a bumpy year.

Powered by WPeMatico

Yesterday at TechCrunch’s Enterprise event in San Francisco, we sat down with three venture capitalists who spend a lot of their time thinking about enterprise startups. We wanted to ask what trends they are seeing, what concerns they might have about the state of the market and, of course, how startups might persuade them to write out a check.

We covered a lot of ground with the investors — Jason Green of Emergence Capital, Rebecca Lynn of Canvas Ventures and Maha Ibrahim of Canaan Partners — who told us, among other things, that startups shouldn’t expect a big M&A event right now, that there’s no first-mover advantage in the enterprise realm and why grit may be the quality that ends up keeping a startup afloat.

Jason Green: When we started Emergence 15 years ago, we saw maybe a few hundred startups a year, and we funded about five or six. Today, we see over 1,000 a year; we probably do deep diligence on 25.

Powered by WPeMatico

It feels like there’s a WeWork on every street nowadays. Take a walk through midtown Manhattan (please don’t actually) and it might even seem like there are more WeWorks than office buildings.

Consider this an ongoing discussion about Urban Tech, its intersection with regulation, issues of public service, and other complexities that people have full PHDs on. I’m just a bitter, born-and-bred New Yorker trying to figure out why I’ve been stuck in between subway stops for the last 15 minutes, so please reach out with your take on any of these thoughts: @Arman.Tabatabai@techcrunch.com.

Co-working has permeated cities around the world at an astronomical rate. The rise has been so remarkable that even the headline-dominating SoftBank seems willing to bet the success of its colossal Vision Fund on the shift continuing, having poured billions into WeWork – including a recent $4.4 billion top-up that saw the co-working king’s valuation spike to $45 billion.

And there are no signs of the trend slowing down. With growing frequency, new startups are popping up across cities looking to turn under-utilized brick-and-mortar or commercial space into low-cost co-working options.

It’s a strategy spreading through every type of business from retail – where companies like Workbar have helped retailers offer up portions of their stores – to more niche verticals like parking lots – where companies like Campsyte are transforming empty lots into spaces for outdoor co-working and corporate off-sites. Restaurants and bars might even prove most popular for co-working, with startups like Spacious and KettleSpace turning restaurants that are closed during the day into private co-working space during their off-hours.

Before you know it, a startup will be strapping an Aeron chair to the top of a telephone pole and calling it “WirelessWorking”.

But is there a limit to how far co-working can go? Are all of the storefronts, restaurants and open spaces that line city streets going to be filled with MacBooks, cappuccinos and Moleskine notebooks? That might be too tall a task, even for the movement taking over skyscrapers.

Photo: Vasyl Dolmatov / iStock via Getty Images

So why is everyone trying to turn your favorite neighborhood dinner spot into a part-time WeWork in the first place? Co-working offers a particularly compelling use case for under-utilized space.

First, co-working falls under the same general commercial zoning categories as most independent businesses and very little additional infrastructure – outside of a few extra power outlets and some decent WiFi – is required to turn a space into an effective replacement for the often crowded and distracting coffee shops used by price-sensitive, lean, remote, or nomadic workers that make up a growing portion of the workforce.

Thus, businesses can list their space at little-to-no cost, without having to deal with structural layout changes that are more likely to arise when dealing with pop-up solutions or event rentals.

On the supply side, these co-working networks don’t have to purchase leases or make capital improvements to convert each space, and so they’re able to offer more square footage per member at a much lower rate than traditional co-working spaces. Spacious, for example, charges a monthly membership fee of $99-$129 dollars for access to its network of vetted restaurants, which is cheap compared to a WeWork desk, which can cost anywhere from $300-$800 per month in New York City.

Customers realize more affordable co-working alternatives, while tight-margin businesses facing increasing rents for under-utilized property are able to pool resources into a network and access a completely new revenue stream at very little cost. The value proposition is proving to be seriously convincing in initial cities – Spacious told the New York Times, that so many restaurants were applying to join the network on their own volition that only five percent of total applicants were ultimately getting accepted.

Basically, the business model here checks a lot of the boxes for successful marketplaces: Acquisition and transaction friction is low for both customers and suppliers, with both seeing real value that didn’t exist previously. Unit economics seem strong, and vetting on both sides of the market creates trust and community. Finally, there’s an observable network effect whereby suppliers benefit from higher occupancy as more customers join the network, while customers benefit from added flexibility as more locations join the network.

Photo: Caiaimage / Robert Daly via Getty Images

So is this the way of the future? The strategy is really compelling, with a creative solution that offers tremendous value to businesses and workers in major cities. But concerns around the scalability of demand make it difficult to picture this phenomenon becoming ubiquitous across cities or something that reaches the scale of a WeWork or large conventional co-working player.

All these companies seem to be competing for a similar demographic, not only with one another, but also with coffee shops, free workspaces, and other flexible co-working options like Croissant, which provides members with access to unused desks and offices in traditional co-working spaces. Like Spacious and KettleSpace, the spaces on Croissant own the property leases and are already built for co-working, so Croissant can still offer comparatively attractive rates.

The offer seems most compelling for someone that is able to work without a stable location and without the amenities offered in traditional co-working or office spaces, and is also price sensitive enough where they would trade those benefits for a lower price. Yet at the same time, they can’t be too price sensitive, where they would prefer working out of free – or close to free – coffee shops instead of paying a monthly membership fee to avoid the frictions that can come with them.

And it seems unclear whether the problem or solution is as poignant outside of high-density cities – let alone outside of high-density areas of high-density cities.

Without density, is the competition for space or traffic in coffee shops and free workspaces still high enough where it’s worth paying a membership fee for? Would the desire for a private working environment, or for a working community, be enough to incentivize membership alone? And in less-dense and more-sprawl oriented cities, members could also face the risk of having to travel significant distances if space isn’t available in nearby locations.

While the emerging workforce is trending towards more remote, agile and nomadic workers that can do more with less, it’s less certain how many will actually fit the profile that opts out of both more costly but stable traditional workspaces, as well as potentially frustrating but free alternatives. And if the lack of density does prove to be an issue, how many of those workers will live in hyper-dense areas, especially if they are price-sensitive and can work and live anywhere?

To be clear, I’m not saying the companies won’t see significant growth – in fact, I think they will. But will the trend of monetizing unused space through co-working come to permeate cities everywhere and do so with meaningful occupancy? Maybe not. That said, there is still a sizable and growing demographic that need these solutions and the value proposition is significant in many major urban areas.

The companies are creating real value, creating more efficient use of wasted space, and fixing a supply-demand issue. And the cultural value of even modestly helping independent businesses keep the lights on seems to outweigh the cultural “damage” some may fear in turning them into part-time co-working spaces.

Powered by WPeMatico

SoftBank may soon own up to 50 percent of WeWork, a well-funded provider of co-working spaces headquartered in New York, according to a new report from The Wall Street Journal.

SoftBank is reportedly weighing an investment between $15 billion and $20 billion, which would come from its $92 billion Vision Fund, a super-sized venture fund led by Japanese entrepreneur and investor Masayoshi Son.

WeWork declined to comment.

SoftBank already owns some 20 percent of WeWork. The firm invested $4.4 billion in the company in August 2017, $1.4 billion of which was set aside to help WeWork expand in China, Japan and Southeast Asia.

This August, WeWork raised another $1 billion from SoftBank in convertible debt. At the same time, WeWork disclosed financials to a handful of media outlets, sharing that its revenue had doubled to $763.8 million in the first half of 2018 as losses increased to $723 million.

SoftBank, for its part, seems to have a hankering for real estate tech. Not only has it become a key stakeholder in WeWork, but it has deployed significant amounts of capital to Opendoor, Compass, Katerra and others.

Last month, the Vision Fund backed Opendoor, a platform for buying and selling homes, with $400 million. The same day, it led a $400 million round for Compass, valuing the real estate brokerage startup at $4.4 billion. As for Katerra, SoftBank poured $865 million into the construction tech business in January.

WeWork, founded in 2010 by Adam Neumann and Miguel McKelvey, has raised nearly $5 billion in a combination of debt and equity funding to date. It was valued at $20 billion in 2017, though reports earlier this summer estimated its valuation would fall somewhere between $35 billion and $40 billion with additional capital from SoftBank. A $40 billion valuation would make it the second most valuable VC-backed company in the U.S. behind only Uber.

WeWork has more than 268,000 members across 287 locations in 23 countries.

Powered by WPeMatico