raleigh

Auto Added by WPeMatico

Auto Added by WPeMatico

As the oldest of 12 children, Bunim Laskin spent much of his teen years looking for ways to help keep his siblings entertained. Noticing that a neighbor’s pool was often empty, Laskin reached out to ask if his family could use her pool. To make it worth her while, he suggested that they could help cover her expenses for maintaining the pool.

Soon after, five other families had made the same arrangement with her and the pool owner had six families covering 25% of her expenses. This meant that the neighbor was actually making money off her pool. The arrangement sparked a business idea in Laskin’s mind. At the age of 20, he founded Swimply, a marketplace for homeowners to rent out their underutilized pools to local swimmers, with Asher Weinberger.

The Cedarhurst, New York-based company launched a beta in 2018, starting with four pools in the New Jersey area.

“We used Google Earth to find houses, and then knocked on 80 doors with a pool,” CEO Laskin recalls. “We got to 100 pools organically. Word of mouth really helped us grow.” The site was pretty bare bones, he admits, with potential customers only able to view photos of the pools and connect with the pool owner by phone.

That year, Swimply did around 400 reservations and raised $1.2 million from friends and family.

In 2019, Swimply launched what he describes as a “proper” website and app with an automated platform. It grew “four to five times” that year, again mostly organically. In an episode that aired in March 2020, the company appeared on Shark Tank but went home without a deal.

Then the COVID-19 pandemic hit. Swimply, Laskin said, pivoted right into the pandemic.

“We were the perfect solution for people when the world was falling on its head,” he said. The company restructured its offering to ensure that pool owners did not have to interact with guests. “It was the perfect, contact-free, self-serve experience to hang out and be with people you quarantined with.”

The CDC then came out to say that it was safe to swim because chlorine could help kill the virus, and that proved to be a big boon to its business.

“On one end, it was a way for people to have a normal day and on the other, it helped give owners a way to earn an income, at a time when many people were being affected financially,” Laskin told TechCrunch.

Business took off in 2020 with revenue growing 4,000% and now Swimply is announcing a $10 million Series A round. Norwest Venture Partners led the financing, which also included participation from Trust Ventures and a number of angel investors such as Poshmark founder and CEO Manish Chandra; Rob Chesnut, former general counsel and chief ethics officer at Airbnb; Ancestry.com CEO Deborah Liu and Michael Curtis.

Swimply is now operating in a total of 125 U.S. markets, two markets in Canada and five markets in Australia. It plans to use its new capital in part to expand into new markets and toward product development.

Image Credits: Swimply

The way it works is pretty straightforward. Swimply simply connects homeowners that have underutilized backyard spaces and pools with those seeking a way to gather, cool off or exercise, for example. People or families can rent pools by the hour, ranging in price from $15 to $60 per hour (at an average of $45/hour) depending on the amenities. New markets that Swimply has recently expanded to include Portland, Oregon; Raleigh, North Carolina and the California cities of Oakland, San Luis Obispo and Los Gatos.

“The shifting mindset from younger generations about ownership is a huge contributor to increased growth of the Swimply marketplace,” said co-founder Weinberger, who serves as Swimply’s COO. “Swimming is the third most popular activity for adults and number one for children, and yet no other company has tackled the aquatic space to make swimming more affordable and accessible…until now.”

While the company declined to provide hard revenue figures, Laskin said Swimply was seeing “seven digits a month in revenue” and 15,000 to 20,000 reservations a month. Families represent the most popular reservation.

“People can book and pay through our platform, and only 20% of hosts ever meet their guests,” Laskin said. “We’re enabling a new kind of consumer behavior with what we’re doing.”

The company is planning to use its new capital to also rebuild much of its tech infrastructure and boost its customer support team to be more “readily available.”

It is also now offering a complimentary up to $1 million worth of insurance per booking for liability as well as $10,000 for property damage.

Swimply has a little over 20 employees, up 10 times from two people in December of 2020. It plans to double that number over the next few months.

The company’s model has proven quite lucrative for some owners, according to Laskin.

“Last year, there were some owners who earned $10,000 a month. One owner in Denver earned $50,000 last year and he had signed up toward the end of the summer. He should make over $100,000 this year,” Lasken projects.

Its only criteria is that owners offer a clean pool. Eighty-five percent of hosts offer restrooms as well. If they don’t, they are limited to one-hour reservations with a max of five guests. Swimply has also partnered with local pool companies, and if they pay one of its owners a visit and certify that pool, that owner gets a badge on the site “so guests get an additional level of security,” Laskin said.

Ed Yip of Norwest Venture Partners admits that when he first heard of the concept of Swimply, he “didn’t know what to make of it.”

But the more he heard about it, the more excited he got.

“This is the Holy Grail for a consumer investor. We’re not changing consumer behavior, but rather [we] productize the experience and make it safer and easier on both sides,” Yip told TechCrunch.

What also gets the investor excited is the potential for Swimply beyond just swimming pools in the future.

“We’re seeing a ton of demand from hosts wanting to list hot tubs and tennis courts, for example,” Yip said. “So this can turn into a marketplace for shared outdoor resources and that’s a huge market opportunity that adds value on both sides.”

Indeed, the concept of monetizing underutilized space is a growing concept. Earlier this year, we reported on Neighbor, which operates a self-storage marketplace, raising $53 million in a Series B round of funding. Neighbor’s unique model aims to repurpose under-utilized or vacant space — whether it be a person’s basement or the empty floor of an office building — and turn it into storage.

Powered by WPeMatico

First some notes on SoftBank’s rumored expansion into China and its weird fund math, then Foxconn and then quick notes on tech depression, Huawei and more.

TechCrunch is experimenting with new content forms. This is a rough draft of something new — provide your feedback directly to the author (Danny at danny@techcrunch.com) if you like or hate something here.

Kane Wu at Reuters reported overnight that SoftBank is looking to open an office and hire an investment team in China, which Wu says will be based in Shanghai. That’s following the fund’s recent global expansion with new targeted offices in Saudi Arabia and India.

When I saw this, I sort of did a double-take: SoftBank doesn’t have a presence in China? The fund has reportedly been seeking investments in some of China’s leading unicorn stars, including controversial face recognition startup SenseTime, and leading edtech startup Zuoyebang (作业帮, which literally translates as “school assignment help”). (Hat-tips to Selina Wang at Bloomberg, who seems to just be sitting in Vision Fund partner meetings). And of course, it dumped a pretty penny into WeWork China, where it was part of a $500 million syndicate, and is a huge investor in Didi.

It’s sort of obvious that SoftBank would expand to China. What will be interesting though is to see how the fund structures itself long-term. As far as I know, the Vision Fund is a singular “fund” that invests worldwide (send me an email if I am wrong on this count). China has a thicket of regulations on funds and companies, which is one of several reasons we see specifically China-focused vehicles (such as Lightspeed and Lightspeed China or Sequoia and Sequoia China). If the Vision Fund continues to be a unified fund, that would be a notable strategy shift that might be cloned by other trans-Pacific funds.

Rajeev Misra, board director of SoftBank Group and CEO of SoftBank Investment Advisors. Photo by Drew Angerer/Getty Images.

When it first closed the Vision Fund, SoftBank explained they had raised just over $93 billion in committed capital or, more precisely, around $93.15-$93.2 billion, according to the initial investor presentations and its annual Form D filings. In those docs, SoftBank said that the fund was financed with $28 billion from SoftBank and $65 billion from third-party investors.

On top of the $93 billion raised for the Vision Fund, SoftBank detailed that it had committed $4.5 billion of its own capital to a separate “Delta Fund,” which was used to alleviate conflicts around SoftBank’s Didi investment. Thus, SoftBank’s total VC funding aggregates to around $97.7 billion.

To add a complication, SoftBank later shifted $1.6 billion of the Vision Fund’s previously disclosed $65 billion in third-party capital over to the Delta Fund. In current disclosures, SoftBank shows $91.7 billion of committed capital for the Vision Fund ($28.1 billion from SoftBank and $63.6 billion from third-party investors). For the Delta Fund, SoftBank shows $6 billion in committed capital ($4.5 billion SoftBank contribution and $1.6 billion from third-party investors).

Here is where it gets even more complicated. In its latest filings, SoftBank also notes that it completed the interim closing of an additional $5 billion for the Vision Fund in mid-October, “intended for the installment of an incentive scheme for operations of SoftBank Vision Fund.” That additional cash would bring Vision Fund’s total committed capital to $96.7 billion, and $102.7 billion together with the Delta Fund.

While it wouldn’t be included in the committed equity capital total, SoftBank is also rumored to be raising a $4 billion credit facility to help finance additional acquisitions.

So, it’s probably best to say that the Vision Fund — as constituted right now — is $97 billion or $96.7 billion with precision, assuming this $5 billion reaches a final close.

We have, of course, covered SoftBank quite obsessively, particularly its debt situation (Part 1, Part 2, Part 3, Part 4 and Part 5). What we haven’t covered more recently are the latest developments in SoftBank’s IPO, which is slated for December 19th and expected to bring in a haul of $21 billion. More to come on that front in the coming days.

U.S. President Donald Trump and Foxconn Chairman Terry Gou. BRENDAN SMIALOWSKI/AFP/Getty Images

The South China Morning Post reported yesterday that Foxconn is investigating expanding its factories to Vietnam in order to avoid tariffs. Makes sense, and I have some calls this week and next trying to suss out how much hardware supply chains have really changed in response to the trade conflict.

That decision though isn’t just about the trade conflict, but also about the quickly increasing wages of Chinese laborers, as well as political interference from Beijing. The Trump administration’s trade policies are just the excuse Foxconn needs to (at least partially) extricate itself from China, while saving face in the process.

What’s interesting is that Foxconn is also dealing with a massive brush fire in Wisconsin, where it received one of the largest economic development incentives ever offered by an American government, a whopping $3 billion package that was expected to drive manufacturing employment in the state.

Overnight, Republicans in the state legislature passed a bill that would place large restrictions on incoming Democratic governor Tony Evers. Jessie Opoien for the (Madison) Cap Times:

Under the bill, legislators would have increased influence over the Wisconsin Economic Development Corporation, and the WEDC board, not the governor, would appoint the job creation agency’s CEO. However, the governor’s power to appoint a CEO would be restored in September 2019.

That is the agency that provided the Foxconn funding, which has become a political football in Wisconsin politics. Republicans are trying to protect one of the major economic legacies of outgoing governor Scott Walker, as well as what they believe is the future direction of manufacturing work in the state. Democrats smell a boondoggle in the making.

If that wasn’t all, rumored skimpy sales for iPhones is putting enormous pressure on Foxconn’s bottom line. Debby Wu at Bloomberg reported two weeks ago that:

The contract manufacturer aims to cut 20 billion yuan ($2.9 billion) from expenses in 2019 as it faces “a very difficult and competitive year,” according to an internal document obtained by Bloomberg. The company’s spending in the past 12 months is about NT$206 billion ($6.7 billion).

Foxconn is a very dynamic organization that has weathered repeated crises over the years. It is pretty much unique in what it does today: very few other companies can scale up and down hundreds of thousands of workers to meet iPhone and other device demands with such alacrity.

But, the fundamentals of the mobile device market have apparently changed dramatically this year, and Foxconn is likely to be the company most harmed as the assembler of those devices. That could destroy not just the Chinese dream of leading in manufacturing, but also the Vietnam and Wisconsin dreams as well.

Also: If you haven’t read it, this poetry by a Foxconn worker who committed suicide really resonated with me. Foxconn’s suicide problem is well-documented, but we often don’t hear from the individuals themselves.

Blind, the anonymous enterprise chatting app that has taken the tech world by storm, published survey results asking tech employees “I believe I am depressed.” Roughly 40 percent of employees responded yes. Interestingly, there wasn’t too much variation between companies. Amazon had the highest rate at 43 percent and Apple had the lowest rate at 30 percent. It’s an informal survey, probably without high scientific validation, but it is a reminder for all of us in the community that mental health and burnout is very real in the startup and tech ecosystems and we should be vigilant in helping each other when times are rough.

This is one of those stories that we are just going to keep hearing about. After bans in Australia and New Zealand, British Telecom has announced they will not just ban Huawei’s 5G equipment, but also its 3G and 4G equipment. Britain, like Aus/NZ, Canada and the U.S., is part of the Five Eyes intelligence network, and national security officials have been leading the crusade against Huawei infrastructure. What’s interesting is not just the rapidity of the bans, but also that the bans haven’t (from what I have seen) migrated outside the Five Eyes community yet.

Raleigh skyline. Photo by James Willamor used under Creative Commons via Flickr.

Pendo is a digital product management platform that has had quite a bit of success with customers and has raised more than $100 million in VC funding, most recently a Series D from Sapphire. The company announced that they have received a grant from home state North Carolina’s economic development department to grow in the Raleigh region. Pendo is committing $34.5 million to its headquarters (with the potential of creating 590 jobs), while the state will offer around $8.8 million in potential reimbursements over the next 12 years.

Given what I wrote yesterday about Wes McKinney leaving NYC and heading to Nashville and the work Chattanooga is doing to aid startups, it’s great to see other hotspots like Raleigh, NC invest to build out their ecosystems in a compelling way.

Todd Olson, CEO of Pendo, explained to me by email that, “Office rents in our downtown are a fraction of the cost of operating in other cities, and the cost of living is appealing to our employees. They can afford to buy a house here. In some markets around the country, that is becoming more difficult. It’s also just a nice place to live and work.”

Creative work is increasingly going to have to find a lower-cost home.

I am still obsessing about next-gen semiconductors. If you have thoughts there, give me a ring: danny@techcrunch.com.

The LP Anti-Portfolio – Great short read. Lindel Eakman, former managing director at UTIMCO, the University of Texas/Texas A&M endowment, gives a list of funds that he passed on that he now regrets. Unfortunately, this is pretty rare coming from an LP, albeit a former one. It would be great to get more public discussion on which funds were missed and why by LP investors.

Hopefully more reading time tomorrow.

What I’m reading (or at least, trying to read)

Powered by WPeMatico

In the days leading up to TechCrunch Disrupt SF 2018, The Economist published the cover story, ‘Why Startups Are Leaving Silicon Valley.’

The author outlined reasons why the Valley has “peaked.” Venture capital investors are deploying capital outside the Bay Area more than ever before. High-profile entrepreneurs and investors, Peter Thiel, for example, have left. Rising rents are making it impossible for new blood to make a living, let alone build businesses. And according to a recent survey, 46 percent of Bay Area residents want to get the hell out, an increase from 34 percent two years ago.

Needless to say, the future of Silicon Valley was top of mind on stage at Disrupt.

“It’s hard to make a difference in San Francisco as a single entrepreneur,” said J.D. Vance, the author of ‘Hillbilly Elegy’ and a managing partner at Revolution’s Rise of the Rest Fund, which backs seed-stage companies based outside Silicon Valley. “It’s not as a hard to make a difference as a successful entrepreneur in Columbus, Ohio.”

In conversation with Vance, Revolution CEO Steve Case said he’s noticed a “mega-trend” emerging. Founders from cities like Pittsburgh, Detroit or Portland are opting to stay in their hometowns instead of moving to U.S. innovation hubs like San Francisco.

“The sense that you have to be here or you can’t play is going to start diminishing.”

“We are seeing the beginnings of a slowing of what has been a brain drain the last 20 years,” Case said. “It’s not just watching where the capital flows, it’s watching where the talent flows. And the sense that you have to be here or you can’t play is going to start diminishing.”

J.D. Vance says that most entrepreneurs don’t need to move to Silicon Valley.

Here’s why. #TCDisrupt pic.twitter.com/0mFPeTuHLe

— TechCrunch (@TechCrunch) September 6, 2018

Farewell, San Francisco

“It’s too expensive to live here,” said Aileen Lee, the founder of seed-stage VC firm Cowboy Ventures, amid a conversation with leading venture capitalists Spark Capital general partner Megan Quinn and Benchmark general partner Sarah Tavel .

“I know that there are a lot of people in the Bay Area that are trying to work on that problem and I hope that they are successful,” Lee added. “It’s an amazing place to live and we’ve made it really challenging for people to live here and not worry about making ends meet.”

One of Cowboy’s portfolio companies opted to relocate from Silicon Valley to Colorado when it came time to scale their business. That kind of move would’ve historically been seen as a failure. Today, it may be a sign of strong business acumen.

Quinn said that of all 28 of Spark’s growth-stage portfolio companies, Raleigh, North Carolina-based Pendo has the easiest time recruiting folks locally and from the Bay Area.

She advises her Bay Area-based late-stage companies to open a second office outside of the Valley where lower-cost talent is available.

“We often say go to [flySFO.com], draw a three-hour circle around San Francisco where they have direct flights, find a city that has a university and open up a second office as quickly as possible,” Quinn said.

Still, all three firms invest in a lot of companies based in San Francisco. Of Benchmark’s 10 most recent investments, for example, eight were based in SF, according to Crunchbase.

“I used to believe really strongly if you wanted to build a multi-billion dollar company you had to be based here,” Tavel said. “I’ve stopped giving that soap speech.”

Aileen Lee (Cowboy Ventures), Megan Quinn (Spark Capital), and Sarah Tavel (Benchmark Capital) on whether or not Silicon Valley is on the wane for investors #TCDisrupt pic.twitter.com/SOpn7p0eNQ

— TechCrunch (@TechCrunch) September 5, 2018

Underestimated talent

A lot of Bay Area VCs have been blind to the droves of tech talent located outside the region. Believe it or not, there are great engineers in America’s small- and medium-sized markets too.

At Disrupt, Backstage Capital founder Arlan Hamilton announced the firm would launch an accelerator to further amplify companies led by underestimated founders. The program will have cohorts based in four cities; San Francisco was noticeably absent from that list.

Instead, the firm, which invests in underrepresented founders and recently raised a $36 million fund, will work with companies in Philadelphia, Los Angeles, London and one more city, which will be determined by a public vote. Aniyia Williams, the founder of Tinsel and Black & Brown Founders, will spearhead the Philadelphia effort.

“For us, it’s about closing that wealth gap to address inequity in tech,” Williams said. “There needs to be more active participation from everyone.”

Hamilton added that for her, the tech talent in LA and London is undeniable.

“There is a lot of money and a lot of investors … it reminds me of three years ago in Silicon Valley,” Hamilton said.

Silicon Valley vs. China

Silicon Valley’s demise may not be just as a result of increased costs of living or investors overlooking talent in other geographies. It may be because of heightened competition abroad.

Doug Leone, an early- and growth-stage investor at Sequoia Capital, said at Disrupt that he’s noticed a very different work ethic in China.

Chinese entrepreneurs, he explained, are more ruthless than their American counterparts and they’re putting in a whole lot more hours.

Doug Leone of Sequoia Capital says founders in the US and China both want to change the world, but Chinese founders are a little more desperate (and you see it in the crazy work ethic they have).#TCDisrupt pic.twitter.com/dPxsRTbJoq

— TechCrunch (@TechCrunch) September 6, 2018

“I’ve had dinner in China until after 10 p.m. and people go to work after 10 p.m.,” Leone recalled.

“We don’t see that in the U.S. I’m not saying the U.S. founders oughta do that but those are the differences. They are similar in character. They are similar in dreams. They are similar in how they want to change the world. They are ultra-driven … The Chinese founders have a half other gear because I think they are a little more desperate.”

Much of this, however, has been said before and still, somehow, Silicon Valley remained the place to be for investors and startup entrepreneurs.

The reality is, those engaged in tech culture are always anxiously awaiting for the bubble to pop, the market to crash and for “peak Valley” to finally arrive.

Maybe, just maybe, Silicon Valley is forever.

Here’s more of our coverage of Disrupt 2018.

Powered by WPeMatico

America’s mayors have spent the past nine months tripping over each other to curry favor with Amazon.com in its high-profile search for a second headquarters.

More quietly, however, a similar story has been playing out in startup-land. Many of the most valuable venture-backed companies are venturing outside their high-cost headquarters and setting up secondary hubs in smaller cities.

Where are they going? Nashville is pretty popular. So is Phoenix. Portland and Raleigh also are seeing some jobs. A number of companies also have a high number of remote offerings, seeking candidates with coveted skills who don’t want to relocate.

Those are some of the findings from a Crunchbase News analysis of the geographic hiring practices of U.S. unicorns. Since most of these companies are based in high-cost locations, like the San Francisco Bay Area, Boston and New York, we were looking to see if there is a pattern of setting up offices in smaller, cheaper cities. (For more on survey technique, see Methodology section below.)

Here is a look at some of the hotspots.

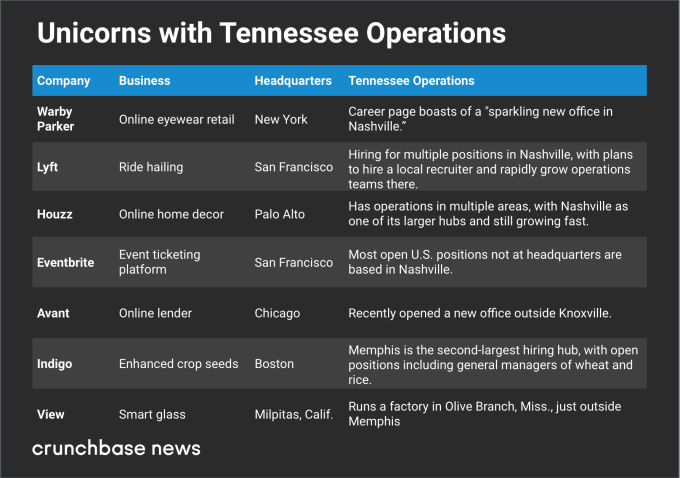

One surprise finding was the prominence of Nashville among secondary locations for startup offices.

We found at least four unicorns scaling up Nashville offices, plus another three with growing operations in or around other Tennessee cities. Here are some of the Tennessee-loving startups:

When we referred to Nashville’s popularity with unicorns as surprising, that was largely because the city isn’t known as a major hub for tech startups or venture funding. That said, it has a lot of attributes that make for a practical and desirable location for a secondary office.

Nashville’s attractions include high quality of life ratings, a growing population and economy, mild climate and lots of live music. Home prices and overall cost of living are also still far below Silicon Valley and New York, even though the Nashville real estate market has been on a tear for the past several years. An added perk for workers: Tennessee has no income tax on wages.

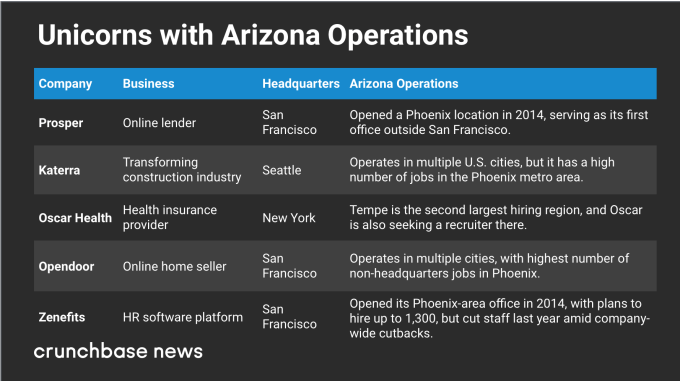

Phoenix is another popular pick for startup offices, particularly West Coast companies seeking a lower-cost hub for customer service and other operations that require a large staff.

In the chart below, we look at five unicorns with significant staffing in the desert city:

Affordability, ease of expansion and a large employable population look like big factors in Phoenix’s appeal. Homes and overall cost of living are a lot cheaper than the big coastal cities. And there’s plenty of room to sprawl.

One article about a new office opening also cited low job turnover rates as an attractive Phoenix-area attribute, which is an interesting notion. Startup hubs like San Francisco and New York see a lot of job-hopping, particularly for people with in-demand skill sets. Scaling companies may be looking for people who measure their job tenure in years rather than months.

Nashville and Phoenix aren’t the only hotspots for unicorns setting up secondary offices. Many other cities are also seeing some scaling startup activity.

Let’s start with North Carolina. The Research Triangle region is known for having a lot of STEM grads, so it makes sense that deep tech companies headquartered elsewhere might still want a local base. One such company is cybersecurity unicorn Tanium, which has a lot of technical job openings in the area. Another is Docker, developer of software containerization technology, which has open positions in Raleigh.

The Orlando metro area stood out mostly due to Robinhood, the zero-fee stock and crypto trading platform that recently hit the $5 billion valuation mark. The Silicon Valley-based company has a significant number of open positions in Lake Mary, an Orlando suburb, including HR and compliance jobs.

Portland, meanwhile, just drew another crypto-loving unicorn, digital currency transaction platform Coinbase. The San Francisco-based company recently opened an office in the Oregon city and is currently in hiring mode.

But you don’t have to be anywhere in particular to score jobs at many fast-growing startups. A lot of unicorns have a high number of remote positions, including specialized technical roles that may be hard to fill locally.

GitHub, which makes tools developers can use to collaborate remotely on projects, does a particularly good job of practicing what it codes. A notable number of engineering jobs open at the San Francisco-based company are available to remote workers, and other departments also have some openings for telecommuters.

Others with a smattering of remote openings include Silicon Valley-based cybersecurity provider CrowdStrike, enterprise software developer Apttus and also Docker.

Of course, not every unicorn is opening large secondary offices. Many prefer to keep staff closer to home base, seeking to lure employees with chic workplaces and lavish perks. Other companies find that when they do expand, it makes strategic sense to go to another high-cost location.

Still, the secondary hub phenomenon may offer a partial antidote to complaints that a few regions are hogging too much of the venture capital pie. While unicorns still overwhelmingly headquarter in a handful of cities, at least they’re spreading their wings and providing more jobs in other places, too.

For this analysis, we were looking at U.S. unicorns with secondary offices in other North American cities. We began with a list of 125 U.S.-based companies and looked at open positions advertised on their websites, focusing on job location.

We excluded job offerings related to representing a local market. For instance, a San Francisco company seeking a sales rep in Chicago to sell to Chicago customers doesn’t count. Instead, we looked for openings for team members handling core operations, including engineering, finances and company-wide customer support. We also excluded secondary offices outside of North America.

Additionally, we were looking principally for companies expanding into lower-cost areas. In many cases, we did see companies strategically adding staff in other high-cost locations, such as New York and Silicon Valley.

A final note pertains to Austin, Texas. We did see several unicorns based elsewhere with job openings in Austin. However, we did not include the city in the sections above because Austin, although a lower-cost location than Silicon Valley, may also be characterized as a large, mature technology and startup hub in its own right.

Powered by WPeMatico

The American South may not be the first region that comes to mind when you hear the phrase “hotbed of tech entrepreneurship,” but, slightly misguided perceptions aside, it’s home to a diverse and growing collection of startups.

Here, we’re going to take a deep dive into the startup funding data for the region.

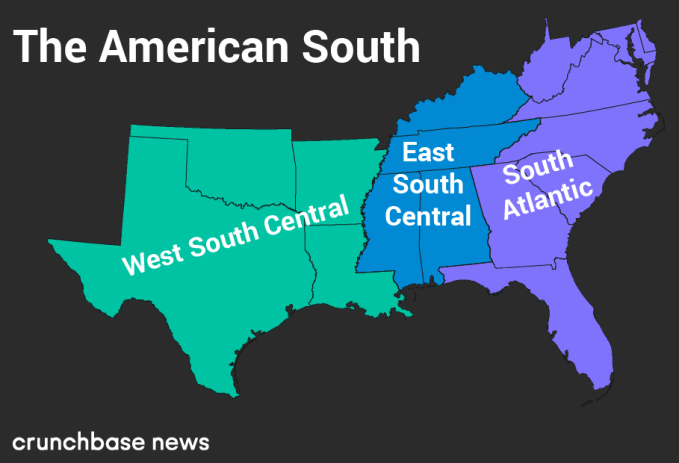

Just like it’s a common pastime for many city dwellers to argue about the precise boundaries of neighborhoods, there’s often some disagreement about the exact contours of the U.S.’s various regions. To quash rabble-rousing from the get-go, we’re using the U.S. Census Bureau’s definition of “the South” on its official map of the United States. Below, we display a map of the states we’re going to look at today.

Much like barbecue, the South is not a monolithic concept. So to incorporate some regional flavor into the following analysis, we’re also going to use the same regional divisions that the U.S. Census Bureau uses.

By doing this, we’ll be able to get a better idea of the relative contribution states from each sub-region make to startup activity in the South overall.

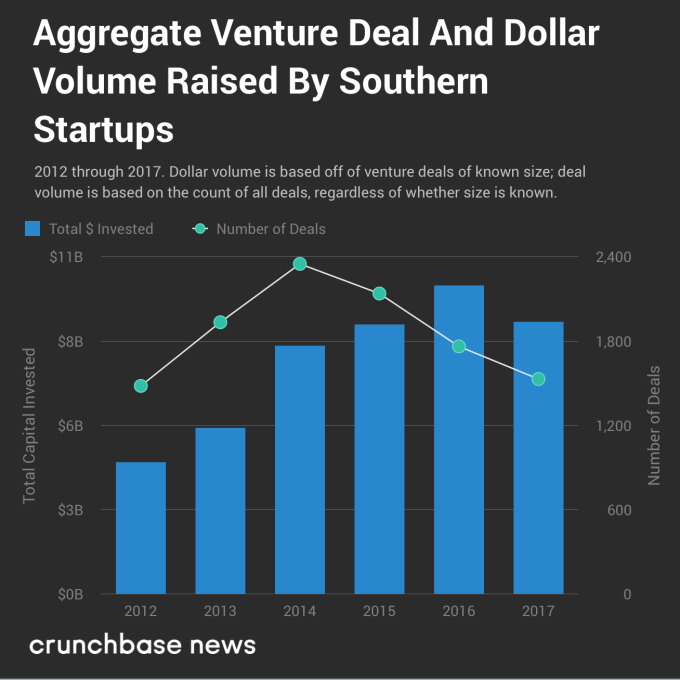

As is the case with most of the country, the South appears to be experiencing a shift in startup funding as we move toward the latter half of a bull run in entrepreneurial activity. The chart below shows a divergence in overall deal and dollar volume over time.

Much like in the rest of the U.S., reported deal and dollar volume are heading in different directions. Part of this may be due to reporting delays — it can sometimes take a few years for seed and early-stage rounds to get added to databases like Crunchbase’s . Nonetheless, there is a slow and generally upward creep in round sizes at most stages of funding. And that’s not just a Southern thing; it’s a country-wide trend.

Let’s disaggregate these figures a bit. We’ll start with deal counts and move on to dollar volume from there.

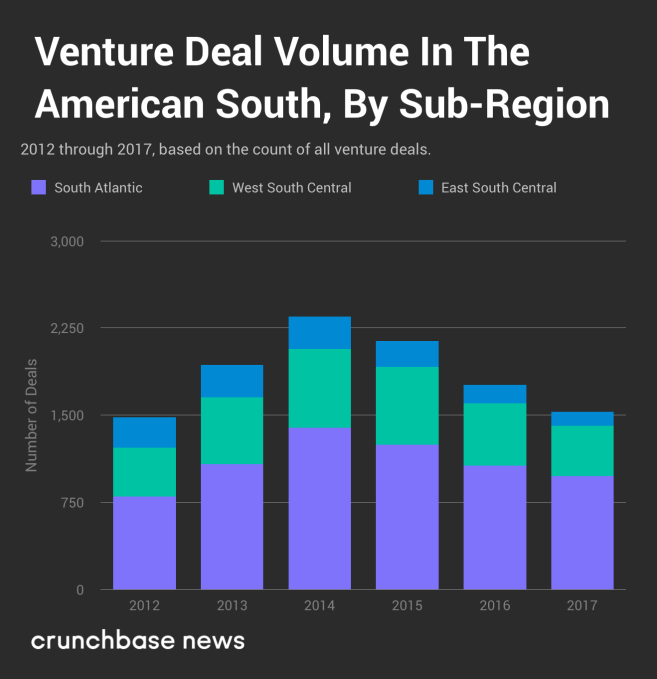

In the chart below, you’ll see venture deal volume broken out by sub-region.

Over the past several years, reported venture deal volume has been on the downswing. From a local maximum in 2014 through the end of 2017, it’s down almost 35 percent overall. But that’s not the whole picture. The relative share of deal volume has changed, as well.

Although it’s not immediately clear just by looking at the chart above, startups in the South Atlantic sub-region have accounted for an increasingly large share of the funding rounds. For example, in 2012, South Atlantic startups attracted 54 percent of the deal volume. In 2017, that grows to 64 percent. Startups in the West South Central sub-region have pretty consistently pulled in between 28 and 30 percent of the deals, so where’s the loss coming from? Startups headquartered in Kentucky, Tennessee, Mississippi and Alabama pulled in just 8 percent of deals in 2017, compared to 18 percent in 2012.

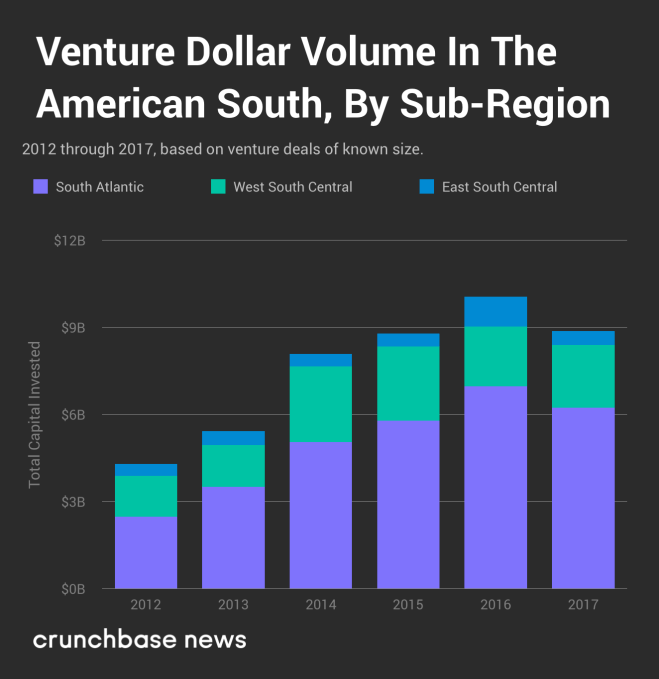

It’s a similar story with dollar volume.

In general, dollar volume follows the same pattern, albeit with a bit more variability. Regardless, startups in the South Atlantic sub-region are hoovering up an ever-larger share of venture dollars, and there’s little to indicate that trend will reverse itself any time soon.

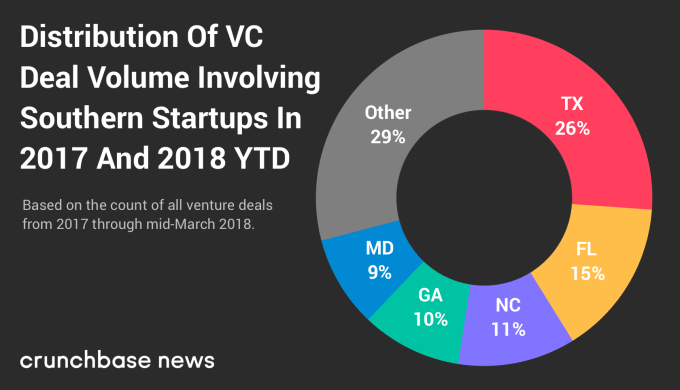

Let’s see which states accounted for most of the deal volume. The chart below shows the geographic distribution of deal-making activity by startups in each Southern state from the beginning of 2017 through time of writing. It should come as no surprise that much of the activity is concentrated in states with higher populations.

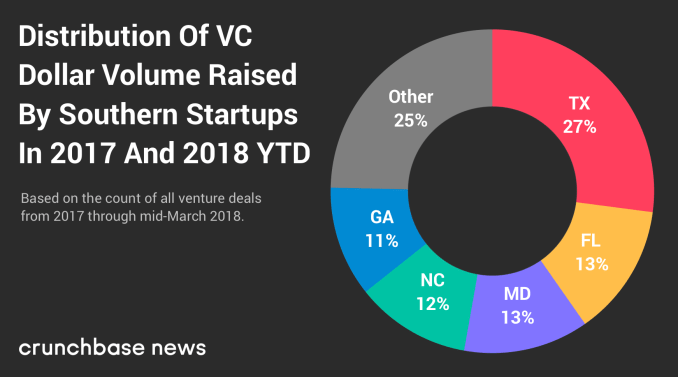

And here’s the distribution of dollar volume among southern states.

Despite some variation in which states are at the top of the ranks, the share of deal and dollar volume raised by startups in the top three states is remarkably similar, coming in at between 52 and 53 percent for both metrics.

We started by looking at the South as a whole and then drilled into its sub regions and states. But there’s one layer deeper we can go here, and that’s to rank the top startup cities in the South.

In the interest of keeping our rankings fresh and timely, we’re covering activity from the past 15 months or so, from the start of 2017 through mid-March 2018. But before highlighting some of the more notable hubs, let’s take a look at the numbers.

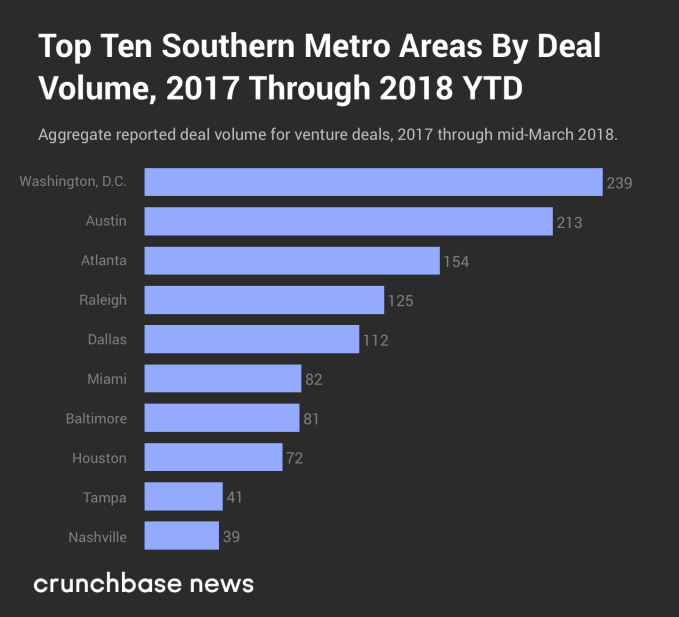

In the chart below, you’ll find the top 10 metropolitan areas where Southern startups closed the most funding rounds.

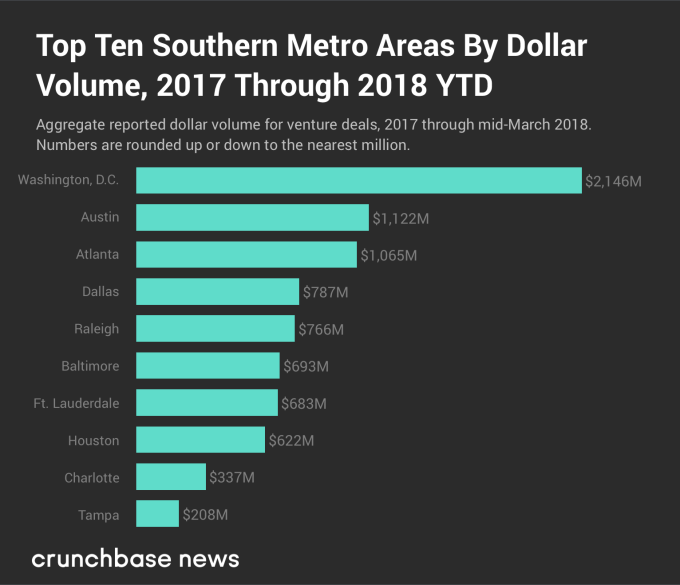

The chart below shows reported dollar volume over the same period of time.

Much like we saw at the state level, the top five startup cities — ranked by both deal and dollar volume — are the same, although there’s some variation between where each one ranks. In order, the D.C., Austin and Atlanta metro areas rank in the top three for each metric, while Dallas and Raleigh, NC switch off between fourth and fifth place.

To be frank, Washington, D.C.’s top-shelf ranking was a bit of a surprise. It may be the fact that Austin, TX plays host to South By Southwest, a somewhat more relaxed culture and/or a preponderance of excellent breakfast taco and barbecue joints, but to many — ourselves included — the city feels like it would have a more active startup scene than the nation’s capital. But that’s not exactly the case. The D.C. metro area had more venture deal and dollar volume than Austin for seven out of the last 10 years, and startups based in the nation’s capital have raised more than twice as much money so far in 2018.

D.C.-area startups have recently raised some notable rounds. Just a couple of weeks prior to the time of writing, Viela Bio raised $250 million in a Series A round (in late February 2018) to continue funding research and testing of its treatments for severe inflammation and autoimmune diseases. And on the later-stage end of things, education technology company Everfi raised $190 million in a Series D round that had participation from Amazon founder and CEO Jeff Bezos, former Alphabet executive Eric Schmidt and Medium CEO Ev Williams. Other D.C. companies, including Mapbox, Upside.com, Afiniti and ThreatQuotient, have all raised late-stage rounds within the past 15 months.

Startup ecosystems in Southern cities may pale in comparison to places like New York and San Francisco, but it wouldn’t be wise to discount the region entirely. A large number of interesting companies call the lower half of the Lower 48 home, and as the cost of living continues to rise on the east and west coasts, don’t be surprised if many current and would-be founders opt to stay down home in the South.

Powered by WPeMatico