qr code

Auto Added by WPeMatico

Auto Added by WPeMatico

Amazon revolutionized one-click shopping, and it has a nearly $2 trillion market cap to show for the effort.

Now, a 10-person startup founded by JD Maresco, who previously cofounded the public safety app Citizen, says it plans to make it a lot easier for retailers who sell directly to their customers to make re-ordering their products just as fast and simple through its QR codes. Indeed, Maresco’s new startup, Batch, is already working with numerous products and brands that use Shopify, promising their customers “one-tap checkout” when it’s time to reorder an item as long as the retailer has slapped one of Batch’s codes on their items or incorporated the codes directly into their packaging.

For the moment, New York-based Batch is wholly reliant on Apple’s App Clip technology, which produces a lightweight version of an app to save people from having to download and install it before using it. (Users can instead load just a small part of an app on demand, and when they’re done, the App Clip disappears.)

But Maresco — whose company just raised $5 million in seed funding co-led by Coatue and Alexis Ohanian’s Seven Seven Six, with participation from Weekend Fund, Shrug Capital, and the Chainsmokers, among others — says Batch will eventually work on both iOS and Android phones. We talked with him yesterday to learn more about its ambitions to make the physical world “instantly shoppable.” Our chat has been edited lightly for length and clarity.

TC: Citizen and Batch are very different companies. Is there a unifying thread?

JM: I’ve spent a good portion of my career, trying to change the way people think about and interact with their physical environment. With Citizen, we were questioning why everyone doesn’t have immediate access to information about what the police are doing in our neighborhoods. With Batch, we’re asking a simpler question but something that matters to me as a consumer: Why isn’t it easier for me to get more of a product I love and use?

With subscriptions in general, I’ve found myself constantly frustrated because every few weeks I’m emailing to either pause a subscription, or restart it. I wanted an easier way to use my phone to reorder in 10 seconds on the spot. Our phones are capable of much more than we put them to use for and, so we set out to tackle that problem.

TC: Right now, Batch integrates with Shopify alone, correct?

JM: We have a Shopify plugin that brands can connect into the Batch platform, and then we integrate the experience, all the way from the physical world wherever this QR code lives, through the purchase experience on the mobile side of things into their fulfillment on the back end. But we’re also expanding to other e-commerce platforms.

TC: And Batch takes a per-transaction fee from every item that’s purchased using your codes?

JM: We’re developing our pricing model over time, but currently we’re taking a service percentage-based fee.

TC: How are you getting brands to partner with you?

JM: Brands are starting to wake up to this idea that they can actually create a new retail channel off their physical packaging, where a customer can effectively shop throughout their home or their place of work or anywhere where they interact with these products the moment they run out of an item. So we’ve been able to spend time with dozens of brands now, and work with them to actually reengineer their packaging and say, ‘Let’s put QR codes front and center and figure out how to make this a really important customer touchpoint.’

TC: How many brands are using the codes currently?

JM: We’re launching dozens of brands this summer. We’ve had overwhelming demand, to be honest, and we haven’t really even fully launched yet.

TC: These are physical codes that you’re sending off to your retail partners — stickers, magnets. Are you also creating digital QR codes?

JM: We have customers that are integrating QR codes into out-of-home advertisements, into direct mail, into T shirts, into promotional vans, so we’re not just limited to packaging. There’s a wide range of places that you can integrate QR codes for your customers.

TC: It’s interesting that Coatue led your round. We’ve seen the firm delve more into early-stage deals but a seed round seems anomalous. How did you connect with the firm?

JM: We met during the seed process. They reached out to me and I developed a relationship with Andy Chen and Matt Mazzeo and it was a great opportunity to to work with their platform — the way they support the go-to-market motion around B2B companies; they have a great data platform. Alexis [Ohanian’s] experience in the consumer space was really appealing, too.

TC: Your company makes sense, but I wonder what’s special about these codes. What’s to prevent countless other startups from doing what you’re doing?

JM: QR codes are all over the place. The product we’re building makes it really easy for brands to create high converting shopping experiences and a native mobile interface. It’s a combination of our Shopify integration and our native product design experience and the relationships we have with these brands and how we help them with their packaging that’s not something you can spin up overnight.

TC: I have to ask about Citizen, which was in the headlines recently for all the wrong reasons. Is there anything you want to say about the company or the app or some of that recent coverage?

JM: I’m not going to comment on the recent press, but I continue to be proud of what the company is continuing to do to help communities stay safe and understand what police and first responders are doing in their neighborhoods.

Powered by WPeMatico

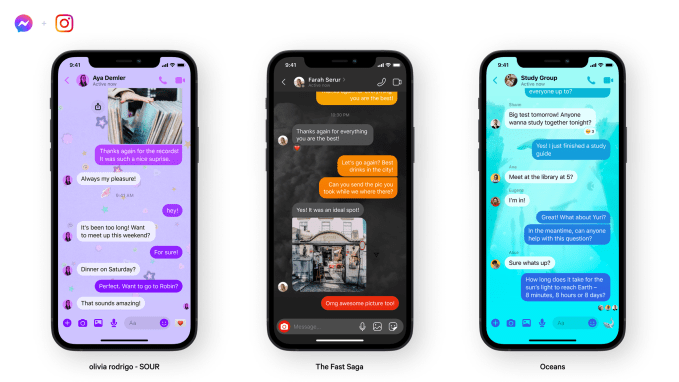

This spring, Facebook confirmed it was testing Venmo-like QR codes for person-to-person payments inside its app in the U.S. Today, the company announced those codes are now launching publicly to all U.S. users, allowing anyone to send or request money through Facebook Pay — even if they’re not Facebook friends.

The QR codes work similarly to those found in other payment apps, like Venmo.

The feature can be found under the “Facebook Pay” section in Messenger’s settings, accessed by tapping on your profile icon at the top left of the screen. Here, you’ll be presented with your personalized QR code which looks much like a regular QR code except that it features your profile icon in the middle.

Underneath, you’ll be shown your personal Facebook Pay UR which is in the format of “https://m.me/pay/UserName.” This can also be copied and sent to other users when you’re requesting a payment.

Facebook notes that the codes will work between any U.S. Messenger users, and won’t require a separate payment app or any sort of contact entry or upload process to get started.

Users who want to be able to send and receive money in Messenger have to be at least 18 years old, and will have to have a Visa or Mastercard debit card, a PayPal account or one of the supported prepaid cards or government-issued cards, in order to use the payments feature. They’ll also need to set their preferred currency to U.S. dollars in the app.

After setup is complete, you can choose which payment method you want as your default and optionally protect payments behind a PIN code of your choosing.

The QR code is also available from the Facebook Pay section of the main Facebook app, in a carousel at the top of the screen.

Facebook Pay first launched in November 2019, as a way to establish a payment system that extends across the company’s apps for not just person-to-person payments, but also other features, like donations, Stars and e-commerce, among other things. Though the QR codes take cues from Venmo and others, the service as it stands today is not necessarily a rival to payment apps because Facebook partners with PayPal as one of the supported payment methods.

However, although the payments experience is separate from Facebook’s cryptocurrency wallet, Novi, that’s something that could perhaps change in the future.

Image Credits: Facebook

The feature was introduced alongside a few other Messenger updates, including a new Quick Reply bar that makes it easier to respond to a photo or video without having to return to the main chat thread. Facebook also added new chat themes including one for Olivia Rodrigo fans, another for World Oceans Day, and one that promotes the new F9 movie.

Powered by WPeMatico

E-commerce is taking off faster than ever. In the last couple of weeks, my Twitter timeline has been filled with operators gushing about how the weekends seem like Black Friday, even for non-essential commodities. Change is already here.

As we help thousands of businesses to move online, our platform is now handling Black Friday level traffic every day!

It won’t be long before traffic has doubled or more.

Our merchants aren’t stopping, neither are we. We need

to scale our platform.https://t.co/e2JeyjcEeC pic.twitter.com/6lqSrNUCte

— Jean-Michel Lemieux (@jmwind) April 16, 2020

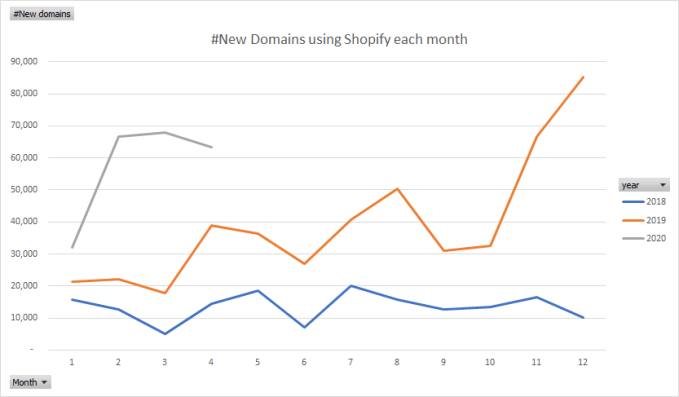

Looking at the above graph in this Tweet from Shopify CTO Jean-Michel Lemieux — and the passing, contextless mention of “Offline2Online” — we got curious.

Beyond just the anecdotal evidence, we looked for signs that tell us e-commerce is being adopted at a faster pace. One way to ascertain that is to look at the historical data of how Shopify has been onboarding merchants for the last two years on a monthly basis, and compare that with what happened this year in Q1.

All of these data points come from PipeCandy’s own data platform that tracks close to 750K+ Shopify merchants with historical data for each:

New domains using Shopify each month

While 2020 started on a faster clip than 2018 and 2019, February and March have seen nothing short of jaw-dropping growth in merchant numbers for Shopify. In those two months alone, Shopify seems to have onboarded more merchants than in the whole of 2018.

The softening you see in April is a result of the lag in the way our systems validate and confirm the data and not a slowdown in Shopify per se. The e-commerce embrace is real.

Powered by WPeMatico

While Amazon has been methodical (read: a little slow) in launching local versions of its site for various global markets, it has now embarked on a secondary track to snag more business outside the 14 countries where it has built out full operations.

Amazon has partnered with Western Union to set up a service called PayCode, which lets people shop and pay for Amazon items using local currencies that would not have been accepted on the site before, starting with services in 10 countries: Chile, Columbia, Hong Kong, Indonesia, Kenya, Malaysia, Peru, Philippines, Taiwan and Thailand.

Specifically, shoppers in these markets will now be able to go into Western Union outposts and pay for their Amazon purchases in cash, which also means that payment cards or other virtual payment methods will also not be required to buy from Amazon — one of the barriers to expanding the service up to now into more emerging economies, where card and bank account penetration is much lower than in developed markets like the U.S. and Europe.

“Amazon is committed to enabling customers anywhere in the world to shop on Amazon.com, and a big part of that is to allow customers to pay for their cross-border online purchases in a way that is most convenient for them,” said Ben Volk, director, Payment Acceptance and Experience at Amazon, in a statement. “Amazon PayCode leverages the reach of Western Union to make cross-border online shopping a reliable and convenient experience for customers who do not have access to international credit cards, or prefer to pay in cash.”

In terms of what they will be able to buy, people can shop across the breadth of the Amazon marketplace, but Amazon notes that they will only be able to use PayCode if it’s offered as an option at checkout (which will only happen in the markets where PayCode is supported); if the item that is chosen is “export eligible,” and if the item’s value “exceeds the maximum value allowed for use on this payment type” — although Amazon doesn’t appear to specify what that maximum value is. Once you complete the purchase online (or possibly more likely, on mobile), you get a “PayCode” QR code that you will have 48 hours to take to a Western Union to pay for the goods; otherwise your order gets cancelled.

The deal between Amazon and Western Union was initially announced last October, with very little detail and fanfare. The PayCode name then appeared to leak out a month later around what appeared to be a test in India (where it has not launched… yet). Today was the first time that the companies unveiled the first launch countries.

PayCode is a significant advance for Amazon as it seeks to step up to the next level of being a global e-commerce powerhouse to compete against the likes of Alibaba.

The latter company has made a lot of inroads to work in a wider array of markets beyond its home base of China, specifically tapping into a long tail of supply from its home market and demand for those goods abroad. Alibaba is also taking care of business when it comes to making more seamless transactions related to those trades. Just today, its financial services affiliate Ant Financial announced that it would acquire U.K.’s WorldFirst, which provides foreign money transfer for businesses and individuals, for a price that we heard from sources was in the region of $700 million.

Amazon currently operates 15 Amazon websites globally: in the U.S., U.K., Australia, Brazil, Canada, China, France, Germany, India, Italy, Japan, Mexico, Netherlands, Spain and Turkey. (It appears also to have a Prime-only site in Singapore.) Up to now, these would have been the only countries where Amazon would offer goods in local currencies.

Adding a new tranche of countries using PayCode will potentially massively expand how many people can shop on Amazon without Amazon going through the steps of setting up full-fledged operations in those countries to serve those consumers and sellers. (Or, this being Amazon, this would be a key way for the company to start testing the waters to figure out which market might do best with a full-fledged store.) Over time, you might imagine that Amazon might extend PayCode to markets where it has sites, too, to give shoppers more flexibility in how they pay for goods for themselves or that they are buying for others.

It’s a big market opportunity. Amazon cites estimates from Forrester Research that say cross-border shopping will represent 20 percent of e-commerce by 2022, accounting for $630 billion.

For Western Union, this is a potentially big partnership, too.

Today, PayCode allows people to use Western Union to act as a physical pay station for their Amazon goods, giving Western Union a small cut on those transactions. But you might imagine how this could evolve over time, where remittances sent from family members abroad via Western Union — a very common use of remittance networks — might immediately get redeemed to cover purchases on Amazon.

Similarly, Western Union is working closer with MPesa, the African mobile wallet service that lets people essentially use their phone top-up account as a payment account, and you could imagine how this too could get incorporated into the PayCode experience to facilitate buying and paying on devices, without having to go into Western Union shops and use actual cash.

“We’re helping to unlock access to Amazon.com for customers who need and want items that can only be found online in many parts of the world,” said Khalid Fellahi, SVP and General Manager of Western Union Digital, in a statement. “This is a great example of two global brands innovating and collaborating to bring customers more convenience and choice. In a world where cross-border buyers and sellers are often located on different continents and in completely different financial ecosystems, our platform is ideally suited to solving the complexity of collecting local currency and converting it into whatever currency merchants need on the other end.”

Powered by WPeMatico

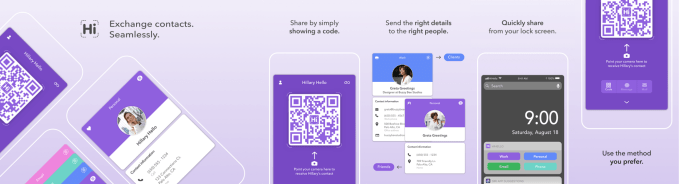

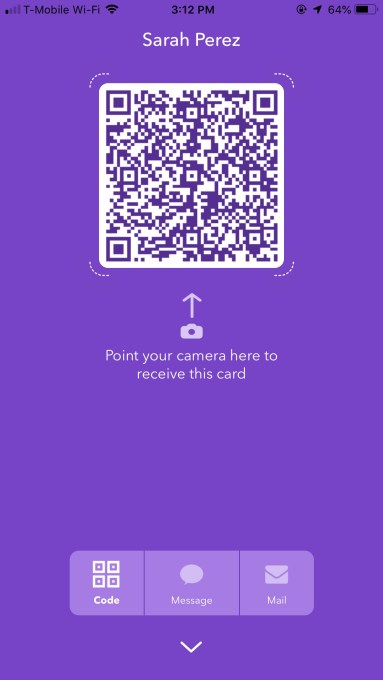

A new app called HiHello is taking aim at business cards. While plenty of apps in the past have tried to kill the business card, they never achieved critical mass. Mainly, this is because most required that both parties — the business card holder and recipient — have their app installed. HiHello is different. Instead of forcing everyone to download its app, it simply generates a QR code that can be scanned by anyone with a modern smartphone.

HiHello specifically takes advantage of the fact that today’s smartphones now have QR code readers built in — users no longer need to download a separate QR code scanner app to exchange information over this format.

On iPhone, you can use the native iOS Camera app to scan QR codes. And on Android, Google Lens (a part of Google Assistant) offers similar functionality. (Although this should really be in its camera, too, ahem.)

What this means is that when a HiHello user wants to share their contact information with another person, all they need to do is have the recipient scan the QR code the HiHello app generates. The recipient doesn’t have to download or install anything, and is able to quickly save the contact information right into their phone’s address book.

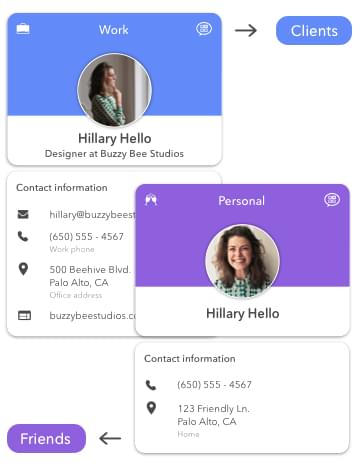

HiHello also allows you to create different types of cards with different information on them.

For example, you could have one card for your business, one for your side hustle and one for personal connections. This way, you can keep some of your information private, as needed.

You could create a card without your cell number for those contacts you didn’t want to be able to reach you by phone; or you could create a card with your virtual number (e.g. a Skype line or Burner) for dating prospects. You could create a card with your home address, cell and personal email for your family and friends. Or you could make one with your office address, work email, fax and office line for business contacts. And so on.

The idea for the app comes from K9 Ventures founder Manu Kumar, who along with co-founder and Caltech and Columbia alum Hari Ravi, and a small team of fewer than half a dozen, has been working on the app following the release of iOS 11, which introduced the QR code reader functionality in the native camera app.

The idea for the app comes from K9 Ventures founder Manu Kumar, who along with co-founder and Caltech and Columbia alum Hari Ravi, and a small team of fewer than half a dozen, has been working on the app following the release of iOS 11, which introduced the QR code reader functionality in the native camera app.

Kumar, in particular, has been trying to solve the problem of business cards for years. In 2009, he co-founded CardMunch to turn business cards into digital contacts. The company was sold to LinkedIn a few years later, but LinkedIn abandoned it and shut it down.

“LinkedIn…failed to recognize the potential for what this could do for them, and in a typical big company fashion proceeded to ruin and eventually kill the product,” Kumar wrote in a blog post about HiHello’s launch. “Yes, I’m still peeved,” he added. (So are we.)

Kumar also noted that another problem with business cards is that people have to carry around different ones to represent their different roles or jobs.

“The information you choose to share with someone is often dependent on the context in which you are meeting that person,” he said.

To address this issue, HiHello allows users to create multiple cards with different information on them, which can be shared via the QR code scan in person, or sent out via text message or email — without exposing the email or phone number tied to your phone.

HiHello has also made it easy to find the right card quickly through its iOS and Android widgets that let you choose which card you want to share with just a tap.

The app is straightforward to set up and use. You’re first walked through a form where you enter your basic contact information to get started, and can then proceed to customize the different card types like “work” and “personal,” for example. You also can just choose to share your phone or email. (See above photo).

When someone scans the QR code, it launches a website hosted on hihello.com where there’s a link to save the information directly to their phone’s contacts. This link can be sent in other ways right from the QR code screen as well, thanks to buttons at the bottom for “Message” and “Mail.”

The new app is the first step in a bigger vision the company has for contact and relationship management, Kumar notes.

Palo Alto-based HiHello, a team of five, is backed by Kumar’s K9 Ventures. The app is a free download on iOS and Android.

Powered by WPeMatico