pre-seed

Auto Added by WPeMatico

Auto Added by WPeMatico

As the United States entered its first wave of COVID-19 lockdowns, there were wide expectations in startup land that a reckoning had arrived. But the expected comeuppance of high-burn, high-growth startups fueled by cheap capital provided by venture capitalists raising ever-larger funds, failed to arrive.

Instead, the very opposite came to pass.

Layoffs happened swiftly and aggressively during the early months of the pandemic era. But by the middle of Q2, venture activity had warmed and third quarter dealmaking felt swift and competitive, with some investors describing it as the hottest summer in recent years.

Venture capital as an asset class has survived the pandemic’s stress test.

But somewhat lost amongst the splashy megarounds and high-interest IPOs that can dominate the news cycle were seed-stage startups. The raw little companies that represent the grist that will shape itself into the next set of giants.

TechCrunch explored what happened in seed investing to uncover what was missed amidst the storm and fury of late-stage startup activity. According to a TechCrunch analysis of PitchBook data and a survey of venture capitalists, a few trends became clear.

First, the pattern of rising seed-check sizes seen in prior years continued despite the tumultuous business climate. Second, more expensive and larger seed deals were not only caused by excessive capital present in the private markets. Instead, COVID-19 shook up which startups were considered attractive by private investors. And the changeup did not necessarily raise their number.

Let’s dig into the data and see what it can teach us about this wild year. Then we’ll hear from Eniac Ventures’ Nihal Mehta, Freestyle’s Jenny Lefcourt, Pear VC’s Mar Hershenson and Contrary Capital’s Eric Tarczynski about what they saw in 2020 while writing a chunk of the checks that our data encompasses.

If you didn’t think much about seed in 2020, you’re not alone. Late, huge rounds consumed most of the media’s oxygen, leaving smaller startups to compete for scraps of attention. There was so much late-stage activity — around 90 $100 million or larger rounds in Q3, for example — it was difficult for smaller investments to command attention.

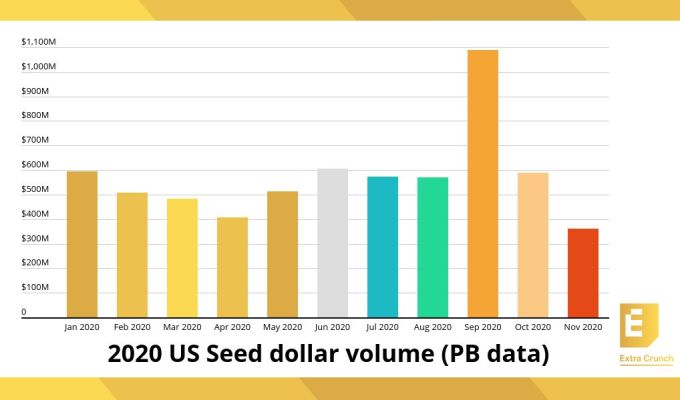

But despite living in the background, the dollars invested into seed-stage startups in the United States had an up-and-down year that was fascinating:

Image Credits: PitchBook

Seed dollar volume fell as Q1 progressed, reaching a 2020 nadir in April, the start of Q2. But as May arrived, the pace at which investors put money into seed-stage startups accelerated, recovering to January levels — which is to say, pre-pandemic — by June. The COVID dip, for seed, then, was a short-term affair.

Powered by WPeMatico

Internships are an opportunity for students to experiment with new career paths and land a full-time offer ahead of graduation. For companies, the weeks-long programs help recruit and train job-ready hires.

While the stakes are high, the coronavirus-spurred office closures and market volatility made a number of tech companies slim down or cancel their internship programs. Similar to remote schooling, the startups that kept their programs had a huge hurdle to face: How do you teach and train students across the world about your company?

That’s where Symba, a Techstars alum, comes in. The 12-person startup created a white-label software tool to help companies, including Robinhood and Genentech, create an online space to communicate and collaborate with their now-distributed interns.

“Every year, organizations are reinventing the wheel and starting their internship program from scratch,” Ahva Sadeghi, CEO of Symba, said. “It’s like, you’re spending so much money, this is a core part of your recruitment, but you’re not invested in an infrastructure to make sure it’s sustainable.”

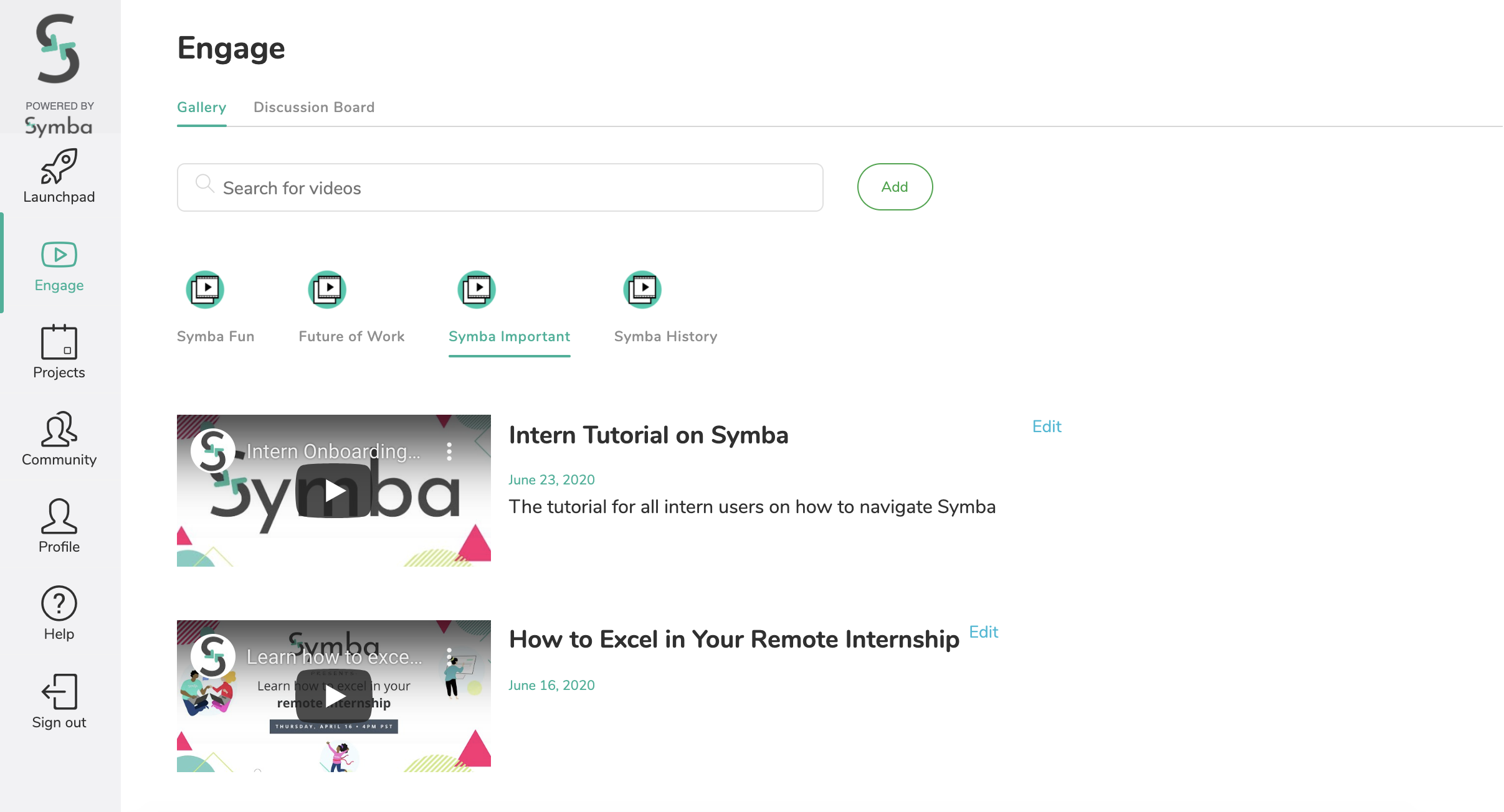

Symba sells a plug-and-play workspace for both interns and managers. Interns sign into Symba through a branded landing page and are brought into a workspace. They can then toggle between feedback, community, profiles and projects. There’s also an entire area for onboarding tutorials and company history.

Interns are brought to a workspace upon login. Image via Symba.

Sadeghi is joined by co-founder and CTO Nikita Gupta, who built the entire site from scratch.

Symba was built with a big focus on creating channels for feedback between interns and managers. There is a tab dedicated solely to feedback, where managers can consistently rank their direct reports on a five-star rating scale across various skills. Interns are also able to request feedback.

Each user is invited to create a profile so other interns can reach out and learn about their cohort. While Symba wants to be where interns live during their internship, there’s no direct messaging mechanisms within the web-based platform. Instead, Symba has embedded a Slack integration for users who want to talk directly.

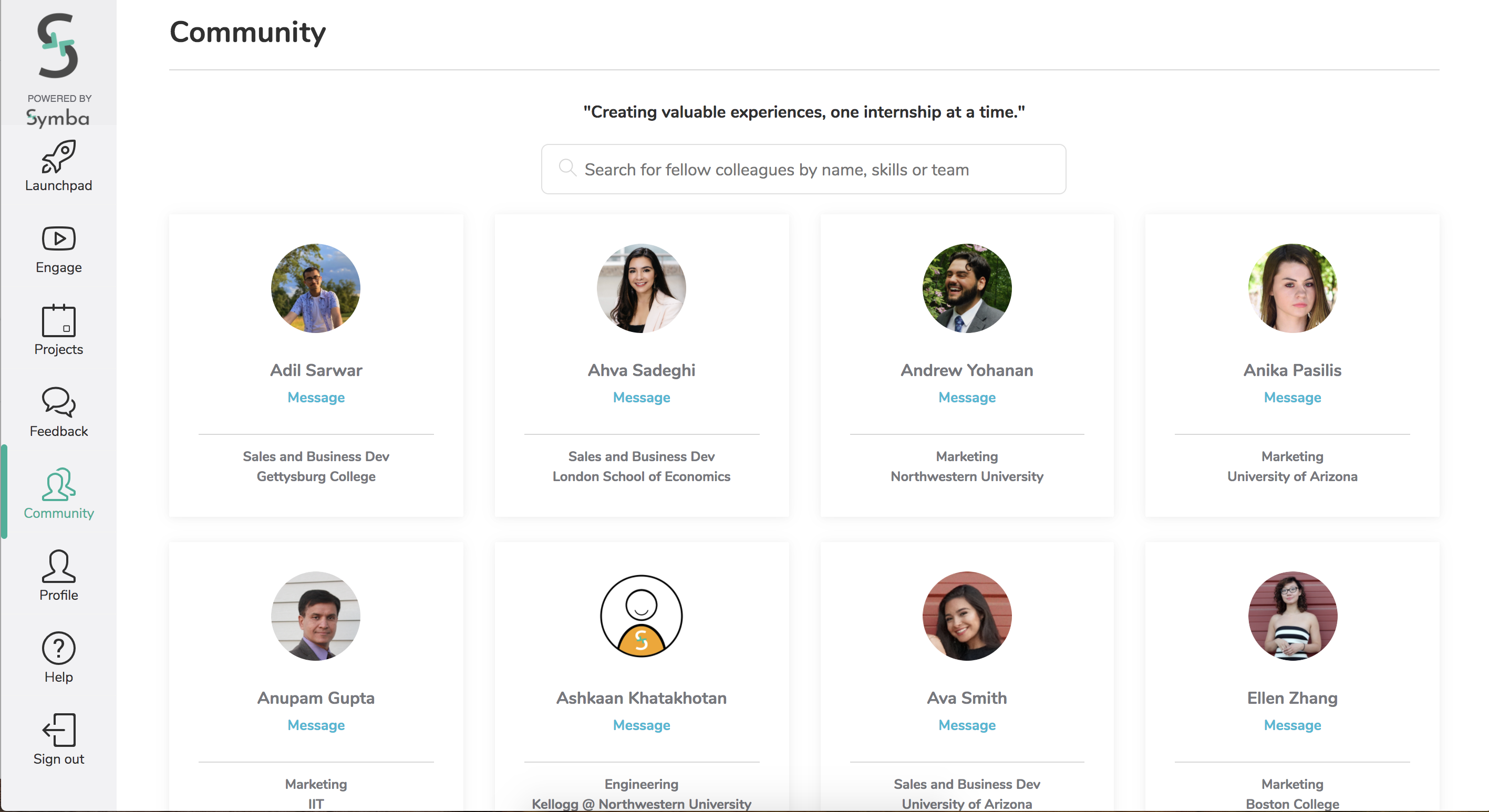

The community board allows interns to meet other interns and chat. Image via Symba.

Managers, on the other hand, are able to log in, assign tasks and check on progress for their direct reports. Feedback is also tracked during the entirety of the internship, to help see who has made progress and deserves a potential return offer.

Because interns come in for only eight to 12 weeks, she says the traditional internship onboarding process — which includes bringing them all onto a company’s full-time tech stack — could create chaos for the organization. Symba wants to be a low-lift alternative.

Sadeghi says that customers have been attracted to the alumni features in their platform, which allow managers to engage interns after the program is complete. The applicant-tracking system works to keep potential hires in the fold of the company.

So far, Symba is optimistic that the tool is working. Users log into the product an average of six to nine times per day, and there have been more than 15,000 intern-projects created on Symba.

The company declined to disclose revenue, citing the stage of its business, but said that it charges companies $30 to $50 per user per month for the product. The average size of a Symba cohort is 80, but they have had customers who bring more than 2,000 interns onto the product. It only works with companies who pay their interns.

A hurdle of Symba will be the seasonality of its revenue. Because most internships are in the summer, Symba will likely find most growth opportunities during that three-month period.

Symba’s early growth is directly related to the pandemic, as the fear of the virus closed offices, and, in turn, shuttered internship programs. Symba’s success will hinge on if the team can convince companies that an online workspace for interns is a necessary product even when offices reopen.

Beyond translating into a post-pandemic world, Symba wants to be a solution for clients such as bootcamps, accelerators or fellowships. If it’s able to land year-round clients, it will be able to balance the seasonality of its current revenue of summer internships.

The success so far is promising: Early momentum has helped Symba raise $750,000 from a number of investors, including 1517 Fund, January Ventures and Hustle Fund.

Powered by WPeMatico

Venture capital has a long way to go when it comes to investing in underrepresented founders in a meaningful way. But according to The Venture Collective’s Cat Hernandez, the issue is too complex to solve by just cutting checks and spending time with entrepreneurs.

“You have to be maniacally focused on solutions,” Hernandez said.

So, Hernandez has teamed up with a number of operators-turned-investors to tackle tech’s diversity problem from a creative angle.

The Venture Collective, based in London and New York, launches today to make access to capital more equal. Fair warning: its experimental structure is knotty, as TVC is part investment vehicle and part management company. But it’s a creative strategy in a deserving sector that tech struggles to make progress within.

The team is stacked with a variety of experience: Founding partner Nick Shekerdemian is a former YC startup founder who launched a diversity recruitment platform, and his co-founder, Gina Kirch, was one of his investors, as well as a former director at BlackRock. Other partners include former Primary Venture Partners investor Cat Hernandez and Elliot Richmond, who invests out of the United Kingdom and previously worked at Moelis & Company.

The team was finalized during COVID-19.

TVC’s funding model has two customer bases: startup founders and family offices.

For startups, the business will invest a $100,000 check into one company per month, with the flexibility to do more. TVC intends to reserve between $1 to $5 million for follow-on rounds.

For family offices, TVC charges an annual fee to serve as intel for what they think are lucrative pre-seed deals in the Valley. If a family office or someone within its network wants to invest, TVC will ultimately deploy an allocated amount of capital. It hopes that total capital commitments will increase over time.

While TVC says the structure model is in stealth, it is reasonable to compare the structures of these family office investments to the structures of special purpose vehicles. SPVs are investment vehicles that exist outside a fund’s capital allotment and are more spur of the moment, versus traditionally syndicated.

The biggest difference is that SPV structure is centered around deals, but TVC’s structure is centered around a capital allotment, deployed into multiple deals. They essentially act as middlemen between promising startups and family offices.

It’s good news for family offices, as they often take the role of institutional investors, which are decade-long relationships. The problem with lengthy bets is that what was hot in 2010 might not be hot in 2020. TVC’s model lets LPs deploy capital in their interest areas on a year by year basis. So an LP who is newly bullish on remote work (for some wild reason) could get their hands in early deals instead of waiting for the AR/VR fund they invested in years ago to make that move.

Putting all these pieces together, TVC gets more funds by:

Because of all of these mechanisms, TVC’s total “fund size” will change depending on the week. It’s a unique example of how first-time fund managers are tackling investing in a volatile landscape.

Today TVC launches with an undisclosed amount of equity-based financing. The company declined to share total assets under management.

So a big factor in TVC’s success is if it can convince both founders and family offices that its perspective is worth the set up. TVC’s flexibility can be a blessing, but it also can be risky and unreliable in case family offices pull out. Or if there is an extended recession, for example.

As a sweetener, the company says that it will donate two-thirds of partner time to helping portfolio companies.

But how does this fit into diversity? It all goes back to TVC’s goal to make access to capital more equal.

According to the team, pre-seed to Series A is where most companies fail, but the very funds that back pre-seed are also the most strapped for resources (small fund sizes, fixed management fees). Thus, firms have to selectively pick the companies they think are outliers and spend time with those companies on a more regular basis. This disproportionately impacts underrepresented founders, who might have a slower start due to lack of access to resources.

TVC thinks its strategy will help grow the number of startups that are venture-backable by heavily supporting them through this time, without competing and driving up valuations for only a few outliers.

The company defined underrepresented founders through diversity, geography, age and social background. When asked if they will publicly disclose diversity metrics, TVC said “it wants to be thoughtful about how we hold our investments accountable in the long-term and we are balancing that with a desire to not be prescriptive.”

“We believe that part of our job as early investors is to ensure that this intent is top of mind as the business scales. That can come in many forms — tracking/reporting on diversity metrics being one of them. At its core, this isn’t about window dressing,” the firm told TechCrunch. Generally, TVC is focused on helping more people get funding, and pointed toward financial optionality as the “flywheel we’re playing for.”

In terms of sourcing, TVC is partnering with tech-focused groups in New York and London and will identify talent at the university and college level. It also said it will build relationships with underrepresented operators “at the most prominent tech companies” and co-invest with diversity-focused founders.

TVC also launched a group called “The Collective” that includes diverse founders, operators and investors, who will help as a deal flow channel.

Powered by WPeMatico

As expectations from seed investors intensify, a new stage of investment has established itself earlier in the venture-backed company life cycle.

Known as “pre-seed” investing, one of the first legitimate outfits to double down on the stage has refueled, closing its second fund on $77 million.

Afore Capital’s sophomore fund is likely the largest pool of venture capital yet to focus exclusively on pre-seed companies, or pre-product businesses seeking their first bout of institutional capital. In many cases, a pre-seed startup may even be “pre-idea,” yet to fully incorporate. While some funds are happy to invest that early, Afore seeks slightly more mature companies.

Afore invests between $500,000 and $1 million in nascent startups. As it kicks off its second fund, founding partners Anamitra Banerji and Gaurav Jain tell TechCrunch they plan to lead all of their investments.

We have the opportunity to build a firm that defines a category. – Afore founding partner Anamitra Banerji

Standouts in Afore’s existing portfolio include the no-fee credit card company Petal — which has raised roughly $50 million to date — mobile executive coaching business BetterUp, childcare information platform Winnie and Modern Health, a B2B mental wellness platform.

Afore portfolio companies have raised more than $360 million in follow-on funding, with an aggregate market cap of $1.5 billion, Jain, the founding product manager at Android Nexus and former principal at Founder Collective, tells TechCrunch. “These are high-quality teams with high-quality projects and ideas.”

Jain and Banerji — a founding product manager at Twitter and former partner at Foundation Capital — began raising capital for Afore’s $47 million debut fund in 2016. Since then, the landscape for seed investing has shifted. Early-stage investors have begun funneling larger sums of capital to standout teams at the seed, while billion-dollar venture capital funds set aside capital for serial entrepreneurs working on their next big idea. As a result, deal sizes have swelled and deal count has shrunk simultaneously.

“Pre-seed has replaced seed in the venture ecosystem,” Banerji tells TechCrunch. “We saw this early as a result of both of us having been at funds. We knew that this was going to be a massive category just like seed was before it. Now we think it’s clearly here to stay and we have the opportunity to build a firm that defines a category.”

Since launching the firm, the pair explain they’ve noticed more and more founders explicitly stating that they are in the market for a pre-seed round, a statement you wouldn’t have heard as recently as two years ago.

This is a result of Afore’s efforts to legitimize the stage through investments and programming, including its annual Pre-Seed Summit. Though Afore is certainly not the only VC fund focused on the earliest stage of startup investing — other firms deploying capital at the stage include Hustle Fund, which closed an $11.8 million debut fund last year, plus the $20 million immigrant-focused pre-seed fund Unshackled Ventures and the predominant seed and pre-seed stage firm Precursor Ventures, which announced a $31 million second fund earlier this year.

In the past year alone, more than $200 million has been dedicated to the pre-seed stage, with at least nine new funds launching to nurture early-stage startups.

More and more firms are setting up shop at the pre-seed stage as competition at the seed stage reaches new heights. As we’ve previously reported, monster funds are becoming increasingly active at the seed stage, muscling seed funds out of top deals with less dilutive offers. While the pre-seed stage, for the most part, remains protected from competition at the later stage, these firms still have to compete.

“Nobody wants to lose sight of a deal, so they are willing to toss small amounts of capital very early behind interesting founders,” Jain said. “But frankly, we aren’t sure if it’s good for a company to raise that much capital that early in their life cycle.”

Working with a fund that isn’t passionate about what you are building or familiar with the plights of the stage of your business is terrible for founders, adds Jain. Pairing with a focused fund like Afore, on the other hand, allows for “incentive alignment.”

Afore invests across all industries, preferring to back startups in categories “before they are categories.”

“What we are looking for is deep authenticity and passion around the product they are building,” says Banerji. “Ideas on their own aren’t enough. Founder resumes on their own aren’t enough. While we do care about all of those aspects, we get crazy about their clarity of thought in the short term.”

“We don’t take the point of view of ‘here is some money, it’s OK to lose it,’ ” he adds. “For us to invest, the founder must be all in. And we generally don’t invest in celebrity founders; we are going after the underdog founder.”

Powered by WPeMatico

Bee Partners in San Francisco has raised a $30 million fund, its second, to lead investments in very early stage startups based in the U.S. Founded in 2009, the firm is best-known as the first investor in TubeMogul, now a publicly traded adtech company. Bee was also an early backer of the crowdfunding platform Indiegogo, drone tech startup Skycatch, the second-hand fashion marketplace Tradesy… Read More

Bee Partners in San Francisco has raised a $30 million fund, its second, to lead investments in very early stage startups based in the U.S. Founded in 2009, the firm is best-known as the first investor in TubeMogul, now a publicly traded adtech company. Bee was also an early backer of the crowdfunding platform Indiegogo, drone tech startup Skycatch, the second-hand fashion marketplace Tradesy… Read More

Powered by WPeMatico