Portland

Auto Added by WPeMatico

Auto Added by WPeMatico

In the days leading up to TechCrunch Disrupt SF 2018, The Economist published the cover story, ‘Why Startups Are Leaving Silicon Valley.’

The author outlined reasons why the Valley has “peaked.” Venture capital investors are deploying capital outside the Bay Area more than ever before. High-profile entrepreneurs and investors, Peter Thiel, for example, have left. Rising rents are making it impossible for new blood to make a living, let alone build businesses. And according to a recent survey, 46 percent of Bay Area residents want to get the hell out, an increase from 34 percent two years ago.

Needless to say, the future of Silicon Valley was top of mind on stage at Disrupt.

“It’s hard to make a difference in San Francisco as a single entrepreneur,” said J.D. Vance, the author of ‘Hillbilly Elegy’ and a managing partner at Revolution’s Rise of the Rest Fund, which backs seed-stage companies based outside Silicon Valley. “It’s not as a hard to make a difference as a successful entrepreneur in Columbus, Ohio.”

In conversation with Vance, Revolution CEO Steve Case said he’s noticed a “mega-trend” emerging. Founders from cities like Pittsburgh, Detroit or Portland are opting to stay in their hometowns instead of moving to U.S. innovation hubs like San Francisco.

“The sense that you have to be here or you can’t play is going to start diminishing.”

“We are seeing the beginnings of a slowing of what has been a brain drain the last 20 years,” Case said. “It’s not just watching where the capital flows, it’s watching where the talent flows. And the sense that you have to be here or you can’t play is going to start diminishing.”

J.D. Vance says that most entrepreneurs don’t need to move to Silicon Valley.

Here’s why. #TCDisrupt pic.twitter.com/0mFPeTuHLe

— TechCrunch (@TechCrunch) September 6, 2018

Farewell, San Francisco

“It’s too expensive to live here,” said Aileen Lee, the founder of seed-stage VC firm Cowboy Ventures, amid a conversation with leading venture capitalists Spark Capital general partner Megan Quinn and Benchmark general partner Sarah Tavel .

“I know that there are a lot of people in the Bay Area that are trying to work on that problem and I hope that they are successful,” Lee added. “It’s an amazing place to live and we’ve made it really challenging for people to live here and not worry about making ends meet.”

One of Cowboy’s portfolio companies opted to relocate from Silicon Valley to Colorado when it came time to scale their business. That kind of move would’ve historically been seen as a failure. Today, it may be a sign of strong business acumen.

Quinn said that of all 28 of Spark’s growth-stage portfolio companies, Raleigh, North Carolina-based Pendo has the easiest time recruiting folks locally and from the Bay Area.

She advises her Bay Area-based late-stage companies to open a second office outside of the Valley where lower-cost talent is available.

“We often say go to [flySFO.com], draw a three-hour circle around San Francisco where they have direct flights, find a city that has a university and open up a second office as quickly as possible,” Quinn said.

Still, all three firms invest in a lot of companies based in San Francisco. Of Benchmark’s 10 most recent investments, for example, eight were based in SF, according to Crunchbase.

“I used to believe really strongly if you wanted to build a multi-billion dollar company you had to be based here,” Tavel said. “I’ve stopped giving that soap speech.”

Aileen Lee (Cowboy Ventures), Megan Quinn (Spark Capital), and Sarah Tavel (Benchmark Capital) on whether or not Silicon Valley is on the wane for investors #TCDisrupt pic.twitter.com/SOpn7p0eNQ

— TechCrunch (@TechCrunch) September 5, 2018

Underestimated talent

A lot of Bay Area VCs have been blind to the droves of tech talent located outside the region. Believe it or not, there are great engineers in America’s small- and medium-sized markets too.

At Disrupt, Backstage Capital founder Arlan Hamilton announced the firm would launch an accelerator to further amplify companies led by underestimated founders. The program will have cohorts based in four cities; San Francisco was noticeably absent from that list.

Instead, the firm, which invests in underrepresented founders and recently raised a $36 million fund, will work with companies in Philadelphia, Los Angeles, London and one more city, which will be determined by a public vote. Aniyia Williams, the founder of Tinsel and Black & Brown Founders, will spearhead the Philadelphia effort.

“For us, it’s about closing that wealth gap to address inequity in tech,” Williams said. “There needs to be more active participation from everyone.”

Hamilton added that for her, the tech talent in LA and London is undeniable.

“There is a lot of money and a lot of investors … it reminds me of three years ago in Silicon Valley,” Hamilton said.

Silicon Valley vs. China

Silicon Valley’s demise may not be just as a result of increased costs of living or investors overlooking talent in other geographies. It may be because of heightened competition abroad.

Doug Leone, an early- and growth-stage investor at Sequoia Capital, said at Disrupt that he’s noticed a very different work ethic in China.

Chinese entrepreneurs, he explained, are more ruthless than their American counterparts and they’re putting in a whole lot more hours.

Doug Leone of Sequoia Capital says founders in the US and China both want to change the world, but Chinese founders are a little more desperate (and you see it in the crazy work ethic they have).#TCDisrupt pic.twitter.com/dPxsRTbJoq

— TechCrunch (@TechCrunch) September 6, 2018

“I’ve had dinner in China until after 10 p.m. and people go to work after 10 p.m.,” Leone recalled.

“We don’t see that in the U.S. I’m not saying the U.S. founders oughta do that but those are the differences. They are similar in character. They are similar in dreams. They are similar in how they want to change the world. They are ultra-driven … The Chinese founders have a half other gear because I think they are a little more desperate.”

Much of this, however, has been said before and still, somehow, Silicon Valley remained the place to be for investors and startup entrepreneurs.

The reality is, those engaged in tech culture are always anxiously awaiting for the bubble to pop, the market to crash and for “peak Valley” to finally arrive.

Maybe, just maybe, Silicon Valley is forever.

Here’s more of our coverage of Disrupt 2018.

Powered by WPeMatico

America’s mayors have spent the past nine months tripping over each other to curry favor with Amazon.com in its high-profile search for a second headquarters.

More quietly, however, a similar story has been playing out in startup-land. Many of the most valuable venture-backed companies are venturing outside their high-cost headquarters and setting up secondary hubs in smaller cities.

Where are they going? Nashville is pretty popular. So is Phoenix. Portland and Raleigh also are seeing some jobs. A number of companies also have a high number of remote offerings, seeking candidates with coveted skills who don’t want to relocate.

Those are some of the findings from a Crunchbase News analysis of the geographic hiring practices of U.S. unicorns. Since most of these companies are based in high-cost locations, like the San Francisco Bay Area, Boston and New York, we were looking to see if there is a pattern of setting up offices in smaller, cheaper cities. (For more on survey technique, see Methodology section below.)

Here is a look at some of the hotspots.

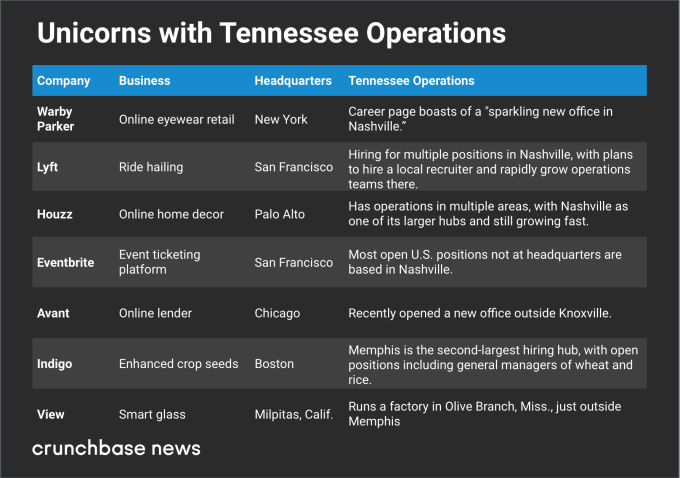

One surprise finding was the prominence of Nashville among secondary locations for startup offices.

We found at least four unicorns scaling up Nashville offices, plus another three with growing operations in or around other Tennessee cities. Here are some of the Tennessee-loving startups:

When we referred to Nashville’s popularity with unicorns as surprising, that was largely because the city isn’t known as a major hub for tech startups or venture funding. That said, it has a lot of attributes that make for a practical and desirable location for a secondary office.

Nashville’s attractions include high quality of life ratings, a growing population and economy, mild climate and lots of live music. Home prices and overall cost of living are also still far below Silicon Valley and New York, even though the Nashville real estate market has been on a tear for the past several years. An added perk for workers: Tennessee has no income tax on wages.

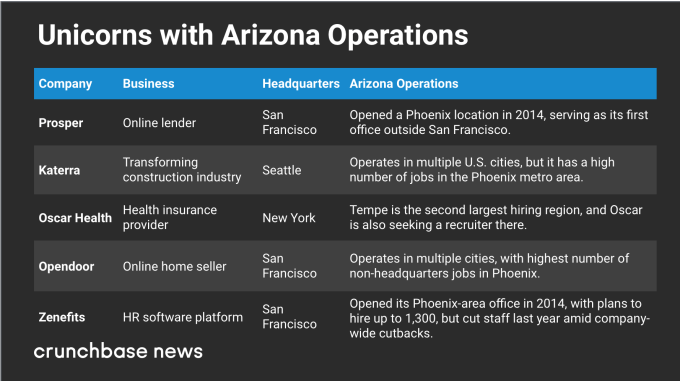

Phoenix is another popular pick for startup offices, particularly West Coast companies seeking a lower-cost hub for customer service and other operations that require a large staff.

In the chart below, we look at five unicorns with significant staffing in the desert city:

Affordability, ease of expansion and a large employable population look like big factors in Phoenix’s appeal. Homes and overall cost of living are a lot cheaper than the big coastal cities. And there’s plenty of room to sprawl.

One article about a new office opening also cited low job turnover rates as an attractive Phoenix-area attribute, which is an interesting notion. Startup hubs like San Francisco and New York see a lot of job-hopping, particularly for people with in-demand skill sets. Scaling companies may be looking for people who measure their job tenure in years rather than months.

Nashville and Phoenix aren’t the only hotspots for unicorns setting up secondary offices. Many other cities are also seeing some scaling startup activity.

Let’s start with North Carolina. The Research Triangle region is known for having a lot of STEM grads, so it makes sense that deep tech companies headquartered elsewhere might still want a local base. One such company is cybersecurity unicorn Tanium, which has a lot of technical job openings in the area. Another is Docker, developer of software containerization technology, which has open positions in Raleigh.

The Orlando metro area stood out mostly due to Robinhood, the zero-fee stock and crypto trading platform that recently hit the $5 billion valuation mark. The Silicon Valley-based company has a significant number of open positions in Lake Mary, an Orlando suburb, including HR and compliance jobs.

Portland, meanwhile, just drew another crypto-loving unicorn, digital currency transaction platform Coinbase. The San Francisco-based company recently opened an office in the Oregon city and is currently in hiring mode.

But you don’t have to be anywhere in particular to score jobs at many fast-growing startups. A lot of unicorns have a high number of remote positions, including specialized technical roles that may be hard to fill locally.

GitHub, which makes tools developers can use to collaborate remotely on projects, does a particularly good job of practicing what it codes. A notable number of engineering jobs open at the San Francisco-based company are available to remote workers, and other departments also have some openings for telecommuters.

Others with a smattering of remote openings include Silicon Valley-based cybersecurity provider CrowdStrike, enterprise software developer Apttus and also Docker.

Of course, not every unicorn is opening large secondary offices. Many prefer to keep staff closer to home base, seeking to lure employees with chic workplaces and lavish perks. Other companies find that when they do expand, it makes strategic sense to go to another high-cost location.

Still, the secondary hub phenomenon may offer a partial antidote to complaints that a few regions are hogging too much of the venture capital pie. While unicorns still overwhelmingly headquarter in a handful of cities, at least they’re spreading their wings and providing more jobs in other places, too.

For this analysis, we were looking at U.S. unicorns with secondary offices in other North American cities. We began with a list of 125 U.S.-based companies and looked at open positions advertised on their websites, focusing on job location.

We excluded job offerings related to representing a local market. For instance, a San Francisco company seeking a sales rep in Chicago to sell to Chicago customers doesn’t count. Instead, we looked for openings for team members handling core operations, including engineering, finances and company-wide customer support. We also excluded secondary offices outside of North America.

Additionally, we were looking principally for companies expanding into lower-cost areas. In many cases, we did see companies strategically adding staff in other high-cost locations, such as New York and Silicon Valley.

A final note pertains to Austin, Texas. We did see several unicorns based elsewhere with job openings in Austin. However, we did not include the city in the sections above because Austin, although a lower-cost location than Silicon Valley, may also be characterized as a large, mature technology and startup hub in its own right.

Powered by WPeMatico

It seems like startup news is full of overnight success stories and sudden failures, like the scooter rental company that went from zero to a $300 million valuation in months or the blood-testing unicorn that went from billions to nearly naught.

But what about those other companies that mature more gradually? Is there such a thing as slow and successful in startup-land?

To contemplate that question, Crunchbase News set out to assemble a data set of top late-blooming startups. We looked at companies that were founded in or before 2010 that raised large amounts of capital after 2015, and we also looked at companies founded a least five years ago that raised large early-stage funds in the last year. (For more details on the rules we used to select the companies, check “Data Methods” at the end of the post.)

The exercise was a counterpoint to a data set we did a couple of weeks ago, looking at characteristics of the fastest growing startups by capital raised. For that list, we found plenty of similarities between members, including a preponderance of companies in a few hot sectors, many famous founders and a lot of cancer drug developers.

For the late bloomers, however, patterns were harder to pinpoint. The breakdown wasn’t too different from venture-backed companies overall. Slower-growing companies could come from major venture hubs as well as cities with smaller startup ecosystems. They could be in biotech, medical devices, mobile gaming or even meditation.

What we did find, however, was an interesting and inspiring collection of stories for those of us who’ve been toiling away at something for a long time, with hopes still of striking it big.

Even youthful startups have been known to make a major pivot or two. So it’s not surprising to see a lot of pivots among late bloomers that have had more time to tinker with their business models.

One that fits this mold is Headspace, provider of a popular meditation app. The company, founded in 2010 by a British-born Buddhist monk with a degree in circus arts, started as a meditation-focused events startup. But it turned out people wanted to build on their learning on their own time, so Headspace put together some online lessons. Today, Santa Monica-based Headspace has millions of users and has raised $75 million in venture funding.

For late bloomers, the pivot can mean going from a model with limited scalability to one that can attract a much wider audience. That’s the case with Headspace, which would have been limited in its events business to those who could physically show up. Its online model, with instant, global reach, turns the business into something venture investors can line up behind.

They say if you wait long enough, everything comes back in style. That mantra usually works as an excuse for hoarding ’80s clothes in the attic. But it also can apply to entrepreneurial companies, which may have launched years before their industry evolved into something venture investors were competing to back.

Take Vacasa, the vacation rental management provider. The company has been around since 2009, but it began raising VC just a couple of years ago amid a broad expansion of its staff and property portfolio. The Portland-based company has raised more than $140 million to date, all of it after 2016, and most in a $103 million October round led by technology growth investor Riverwood Capital.

CloudCraze, which was acquired by Salesforce earlier this week, also took a long time to take venture funding. The Chicago-based provider of business-to-business e-commerce software launched in 2009, but closed its first VC round in 2015, according to Crunchbase records. Prior to the acquisition, the company raised about $30 million, with most of that coming in just a year ago.

Meanwhile, some late bloomers have always been fashionable, just not necessarily as VC-funded companies. Untuckit, a clothing retailer that specializes in button-down shirts that look good untucked, had been building up its business since 2011, but closed its first venture round, a Series A led by VC firm Kleiner Perkins, last June.

So yes, there is still capital available for those who wait. However, the truth of the matter is most companies that raise substantial sums of venture capital secure their initial seed rounds within a couple years of founding. Companies that chug along for five-plus years without a round and then scale up are comparatively rare.

That said, our data set, which looks at venture and seed funding, does not come close to capturing the full ecosystem of slow-growing startups. For one, many successful bootstrapped companies could raise venture funding but choose not to. And those who do eventually decide to take investment may look at other sources, like private equity, bank financing or even an IPO.

Additionally, the landscape is full of slow-growing startups that do make it, just not in a venture home run exit kind of way. Many stay local, thriving in the places they know best.

On the flip side, companies that wait a long time to take VC funding have also produced some really big exits.

Take Atlassian, the provider of workplace collaboration tools. Founded in 2002, the Australian company waited eight years to take its first VC financing, despite plentiful offers. It went public two years ago, and currently has a market valuation of nearly $14 billion.

The moral: Those who take it slow can still finish ahead.

Data methods

We primarily looked at companies founded in 2010 or earlier in the U.S. and Canada that raised a seed, Series A or Series B round sometime after the beginning of last year, and included some that first raised rounds in 2015 or later and went on to substantial fundraises. We also looked at companies founded in 2012 or earlier that raised a seed or Series A round after the beginning of last year and have raised $30 million or more to date. The list was culled further from there.

Powered by WPeMatico

The Rose City isn’t happy with Uber… again. After the company failed to turn over details on its deeply sketchy “Greyball” software by Portland’s deadline, the city may seek to compel Uber to hand it over with a subpoena. Those intentions, reported by the Oregonian, were articulated by Portland Commissioner Dan Saltzman, who oversees the city’s Bureau… Read More

The Rose City isn’t happy with Uber… again. After the company failed to turn over details on its deeply sketchy “Greyball” software by Portland’s deadline, the city may seek to compel Uber to hand it over with a subpoena. Those intentions, reported by the Oregonian, were articulated by Portland Commissioner Dan Saltzman, who oversees the city’s Bureau… Read More

Powered by WPeMatico

Portland, Ore.-based DevOps company Puppet Labs today announced that it has secured a $22 million credit facility from Silicon Valley Bank.

Portland, Ore.-based DevOps company Puppet Labs today announced that it has secured a $22 million credit facility from Silicon Valley Bank.

In addition, the company today appointed former Genentech CFO Lou Lavigne to its board, where he will be the chairman of its audit committee — a critical role Puppet had to fill as it prepares for a future IPO. Read More

Powered by WPeMatico

Portland, Oregon, has started a pilot program to bring car sharing and alternative fuels to low-income neighborhoods where residents might not consider either type of transportation accessible.

Portland, Oregon, has started a pilot program to bring car sharing and alternative fuels to low-income neighborhoods where residents might not consider either type of transportation accessible.