Policy

Auto Added by WPeMatico

Auto Added by WPeMatico

Birthday cakes, gift cards, free lunches, snacks, movie tickets, and other perks are generously bestowed on employees to celebrate life’s happy moments. This is an improvement from the industrial approach to management, but can we go deeper for our work-family members?

Life’s darker moments hold the greatest opportunity to exemplify a genuine and caring 21st-century workplace culture. One which fosters empathy and camaraderie. Employee turnover is highest when employees take leave, claim FMLA, or use PTO. According to Global Studies, 79% of employees report their reason for quitting was simply due to feeling unnoticed (lack of appreciation).

Appreciation for your employees is best demonstrated as an act of kindness in moments that really matter, like the loss of a family member. Acknowledging that someone great is gone, instead of ignoring the uncomfortable aspects of grief, is a valuable way to embed empathy into your workplace culture.

Recently, while working with a mid-sized (500+ employees) tech company, I asked what they were doing to support employees during the negative life moments. The HR Director replied, “um, nothing really”.

Once realizing how crappy that sounded, another executive countered her by saying he sent an employee a t-shirt and card after a miscarriage. I later learned that the employee he was referring to had been with the company for over 5 years, so it’s safe to assume that she had a couple of company swag t-shirts in her collection prior to getting one as a get well gift.

Even in the largest and most notable companies, where a variety of employee amenities and benefits are offered, the concept and practice of empathy is often neglected. Perhaps you haven’t come across such extreme examples of indifference in your workplace, but you may have participated in signing a generic condolences card or chipping in for some flowers.

Powered by WPeMatico

Facebook provided TechCrunch with new information on how its cryptocurrency will stay legal amidst allegations from President Trump that Libra could facilitate “unlawful behavior.” Facebook and Libra Association executives tell me they expect Libra will incur sales tax and capital gains taxes. They confirmed that Facebook is also in talks with local convenience stores and money exchanges to ensure anti-laundering checks are applied when people cash-in or cash-out Libra for traditional currency, and to let you use a QR code to buy or sell Libra in person.

A Facebook spokesperson said the company wouldn’t respond directly to Trump’s tweets, but noted that the Libra association won’t interact with consumers or operate as a bank, and that Libra is meant to be a complement to the existing financial system.

Trump had tweeted that “Unregulated Crypto Assets can facilitate unlawful behavior, including drug trade and other illegal activity. Similarly, Facebook Libra’s ‘virtual currency’ will have little standing or dependability. If Facebook and other companies want to become a bank, they must seek a new Banking Charter and become subject to all Banking Regulations, just like other Banks, both National and International.”

For a primer on how Libra works, watch our explainer video below or read our deep dive into everything you need to know:

In a wide-reaching series of interviews this week, the Libra Association’s head of policy Dante Disparte, Facebook’s head economist for blockchain Christian Catalini and Facebook’s blockchain project subsidiary Calibra’s VP of product Kevin Weil answered questions about regulation of Libra. Here’s what we’ve learned (their answers were trimmed for clarity but not edited):

Calibra’s Kevin Weil: We believe that creating a financial ecosystem that has significantly broader access where all it takes is a phone and lower transaction fees across the board is good for people. And we want to bring it to as many people around the world as we can. But as a custodial wallet we are regulated and will be compliant and we will only operate in markets where we’re allowed.

We want that to be as many markets as possible. That’s why we announced well in advance of actually launching a product — because we’ve been engaging with regulators. We’re continuing to engage with regulators and we can help them understand the effort that we’re taking to make sure that people are safe and also the value that accrues to the people in their countries when there’s broader access to financial services with lower transaction fees across the board.

TechCrunch: But what if you’re banned in the U.S.?

Weil: I’m hesitant to give a blanket answer. But in general, we believe that Libra is positive for people and we want to launch as broadly as possible. The world where the U.S. does that I think would probably cause other regulatory regimes to also be concerned about it. I think that’s very much a bridge that we’ll cross when we get there. But so far we’re having frank, open and honest discussions with regulators. Obviously, that continues next week with David’s testimony. And I hope it doesn’t come to that, because I think that Libra can do a lot of good for a lot of people.

TechCrunch’s Analysis: The U.S. House subcommittee has already submitted a letter to Facebook requesting that it cease development of Libra and Calibra until regulators can better examine it and take action. It sounds like Facebook believes a U.S. ban on Libra/Calibra would cause a domino effect in other top markets, and therefore make it tough to rationalize still launching. That puts even more pressure on the outcome of July 16th and 17th’s congressional hearings on Libra with the head of Facebook’s head of Calibra, David Marcus.

We already know that Facebook’s own Libra wallet called Calibra will be baked into Messenger and WhatsApp plus have its own standalone app. There, those with connected bank accounts and government ID that go through a Know Your Customer (KYC) anti-fraud/laundering check will be able to buy and sell Libra. But a big goal of Libra is to bring the unbanked into the modern financial system. How does that work?

Weil: Because Libra is an open ecosystem, any money exchange business or entrepreneur can begin supporting cash-in/cash-out without needing any permission from anyone associated with the Libra Association or member of the Libra Association. They can just do it. Today in a lot of emerging markets [there’s a service for matching you with someone to exchange cryptocurrency for cash or vice-versa called] LocalBitcoins.com and I think you’ll see that with Libra too.

Second, we can augment that by by working with local exchanges, convenience stores and other cash-in/cash-out providers to make it easy from within Calibra. You could imagine an experience in the Calibra app or within Messenger or WhatsApp, where if you want to cash in or cash out, you’ll pop up a map that highlights physical locations around that allow you to do it. You select one that’s nearby, you select an amount, and you get a QR code that you can take to them and complete the transaction.

I’d imagine that most of these businesses that we work with will support Libra more broadly, so even if we get these deals started it will benefit the whole ecosystem and every Libra wallet, not just Calibra.

TechCrunch: Have you struck relationships with any convenience store operators or money exchangers like Western Union or MoneyGram, or Walgreens, CVS or 7-Eleven? Are you in talks with them yet?

Weil: I probably shouldn’t comment on any specific deals but we’re in conversation with a lot of the folks you might think, because ultimately being able to move between Libra and your local currency is critical to driving adoption and utility in the early days . . . If you’re banked there are easier ways to do that. If you’re not banked and you’re in cash — those are the people we really want to serve with Libra — we’re working very hard to make that process easy for people.

TechCrunch’s analysis: This approach will let Calibra largely avoid the complicated and potentially error-prone process of KYCing people in person or handing out cash by offloading the responsibility and liability to other parties.

Weil: There are very important populations that don’t have an ID. People in a refugee camp may not, as an example, and we want Libra to serve them. So this is one example of many of why it’s important that Calibra isn’t the only option for people who want to participate in the Libra ecosystem . . . Others of these will be run by local providers and they have programs to meet customers face-to-face and other ways to serve people and even KYC them that we may not . . . We’re not going be the only wallet, we don’t want to be the only wallet.

This is one of the reasons NGOs have been members of the Libra association from the start, because we want to encourage the monetization of identity processes both through working with governments issuing credentials for more people and also making use of new types of information for identity and authentication. We hope this process will hep the last mile problem.

In the case of a non-custodial wallet, the user isn’t trusting anyone. The way the regulations have worked and this is evolving as we speak. The on-ramps and off-ramps to the crypto world are regulated and they have direct customer relationships and it’s their responsibility to KYC people. In our case we’ll be a custodial wallet and we’ll KYC people. There are a number of wallets in the Bitcoin or Ethereum ecosystem — non-custodial wallets that don’t have a direct relationships with the users. . . They have to get that Bitcoin somehow. Usually they’re going through an exchange where usually as part of the process they’re KYC’d.

In a lot of emerging markets you have LocalBitcoins.com where you can find a representative or agent who will meet you in person and exchange cash for bitcoin in whatever market you have to be in. And I believe that they just started making sure that they KYC everyone, but they’re doing it in person. And they have more flexibility in how they do it than you might otherwise. I think there are lots of ways that this will happen and the fact that Libra is an open ecosystem will enable people to be entrepreneurial about it.

There are lots an lots of people who are underserved by today’s financial ecosystem who have government ID. So even with requiring everyone go through a KYC process, we’ll be able to serve many, many people who are not well-served by today’s financial ecosystem. We want to find ways to support people who can’t KYC and the important part is that Calibra will fully interoperate with any other wallet, including ones that people in local markets are using because it’s a better fit for their needs.

TechCrunch: Through that interoperability, if someone with a non-custodial wallet receives Libra and then sends it a Calibra wallet user, does that mean you Libra coming into Calibra from users who weren’t KYC’d and could be laundering money?

Weil: So it’s part of the regulatory situation that’s evolving as we speak. There’s something called the Travel Rule . . . If there’s a transfer above a certain value you have to make sure that you understand both who the sender is, which you do if they’re using a custodial wallet, and who the receiver is. These are evolving regulations, but it’s something that obviously we’re going to make sure that we implement as regulations solidify.

TechCrunch’s Analysis: Calibra appears to be inviting regulation that it can strictly abide by rather than trying to guess at what the best approach is. But given it’s unclear when concrete rules will be established for transfers between non-custodial wallets and custodial wallets, or for in-person cashing, Facebook and Calibra may need to establish their own strong protocols. Otherwise they could be guilty of permitting the “unlawful behavior” Trump describes.

Dante Disparte of Libra: Taxing of digital assets is something that’s being designed at the local level and at the jurisdiction level. Our view of the world is that like with any form of money or any form of payment or banking, the onus in terms of compliance with tax is with the individual user and consumer, and the same would hold true broadly here.

We expect that the many, many wallets and financial services providers building solutions on the Libra blockchain would begin to provide tools that make it much easier than it is today [to calculate and file taxes] for digital assets and cryptocurrencies more generally . . . There’s plenty of time between now and Libra hitting the market to begin defining this more strictly at the jurisdictional level among providers.

TechCrunch’s Analysis: Again, here Facebook, Calibra and the Libra Association are hoping to avoid shouldering all the responsibility for taxes. Their position is that just as you have to take the initiative of paying your taxes whether or not you use a Visa card or your bank’s checks to transact, it’s on you to pay your Libra taxes.

TechCrunch: Do you think in the United States that it’s reasonable for the government to ask that Libra transactions be taxed?

Disparte: Tax treatments of digital assets broadly hasn’t been entirely clarified in most places around the world. And we hope that this is something that this project and the ecosystem around it helps to clarify.

Tax authorities will see a benefit from Libra at the consumption level and at the household level, while some cryptocurrencies have avoided taxes until the point they tried to cash out. But the nature of it and the lack of speculation and its design we think should give it a light tax treatment the way you would find with traditional currencies.

Christian Catalini of Facebook: Cryptocurrencies are taxed right now every time you have a sale on the differences in gains and losses. Because Libra is designed to be a medium of exchange, those gains and losses are likely to be very tiny relative to your local currency . . . Sales tax would likely be implemented the exact same way on Libra as it is today when you pay with a credit card.

At launch giving current regulations, the Calibra wallet will have to track every purchase and sale of Libra for a U.S. user and those differences will have to be reported on tax day. You can think of the losses, albeit they may be very small gains and losses relative to USD, as similar to the what people do today when they have a Coinbase account with Bitcoin.

The sales tax I think could be implemented in the exact same way as it today with any other sort of digital payment, it would be no different. If you’re buying goods or services with Libra you’ll be paying sales tax the same way as if you used a different form of payment. Like today when you see a percentage, that is the sales tax on your total.

Disparte: Maybe the best way to frame how taxes work all over the world is that it’s not up to Libra, Calibra, Facebook or any company to make that determination. It’s up to regulators and authorities.

TechCrunch: Does Calibra already have plans in place for how to handle sales tax?

Weil: That’s also a pretty rapidly evolving part of the regulatory ecosystem right now. It’s really an ongoing discussion. We will do whatever the regulation says we need to do.

TechCrunch’s Analysis: Here we have the firmest answers of our interviews. Facebook, Calibra and the Libra Association believe the proper approach to taxes is that Libra transactions carry a country’s traditional sales tax, and that Libra you hold in your wallet will have to pay taxes based on the Libra stablecoin’s value (that’s pegged to a basket of international currencies) relative to the U.S. dollar.

If the Libra Association recommends all wallets and transactions follow these rules and Calibra builds in protocols to handle these taxes simply, at least the government can’t argue Libra is a method of dodging taxes and everyone paying their fair share.

Powered by WPeMatico

The immigration process in the U.S. has become a high-stakes undertaking for employers, workers, and entrepreneurs. Predictability has eroded. Processing times have soared. And any mistake or misstep now has dire consequences.

Over the past three years, immigration policies and procedures have been in a state of flux and the process has become more unforgiving for even the smallest mistakes. Putting your best foot forward is crucial. Employers and individuals need to formulate a long-term strategy and backup options to stay protected.

The increase in Requests for Evidence and the backlog for many visa and green card categories has meant longer waiting times. What’s more, the Trump administration’s recent decision to close all USCIS’s international offices—and shift that workload back to the U.S.—is expected to compound the backlogs and delays.

We are seeing these issues affect startups every day. My law firm works with hundreds of startups every year to help them and their employers figure out their immigration paperwork. The overall piece of advice we give is to decide on a specific goal based on a deep understanding of the company and the individual and by examining the options strategically.

Then, you can figure out the right approach for a visa, green card, or citizenship application. Regardless of my personal interest in the matter, now more than ever, I recommend consulting with an experienced immigration attorney who can handle the process with integrity, creativity, compassion, and rigor.

The new normal for immigration means increased employee recruiting and retention costs for employers. However, hiring immigrants remains possible.

Powered by WPeMatico

Deciding what to patent can be a confusing process but by creating a formal process it is something that every startup can manage.

Intellectual property (IP) is one of the most valuable assets of a startup and patents are often chief among IP in terms of value. Patents allow the startup to prevent competitors from using their technology, which is a powerful feature that can grant unique advantages in the marketplace.

From a business perspective, patents can help with driving investment and acquisitions, provide protection during partnerships and business deals, and help defend itself against patent lawsuits by others.

However, startups also often have a hard time determining when and what to patent. Innovative startups are inventing new things on a regular basis, and there is a danger of slipping into a haphazard approach of patenting whatever happens to be available rather than systematically analyzing the business needs of the company and protecting the IP that moves the needle the most.

Moreover, startups must balance the need to protect IP with other areas of the business: Patents are complex documents that require an investment of time and resources to obtain. They often require specialized legal counsel to write and a lengthy examination process at the U.S. Patent & Trademark Office (USPTO).

This article is a how-to guide for startups to make the decision on when and what to patent with a mature approach to IP strategy.

In order to make a decision about what to patent, a startup must first know what IP it has. For very small teams, it may be possible for everyone to have a shared idea of the IP. However, once teams grow beyond a few people, it is no longer possible to have complete visibility into what everyone on the team is doing and potentially inventing. Therefore, a regular IP harvesting process must be put in place to ensure proper reporting of IP to the executive level.

Most startups are best served with a simple IP harvesting process involving just three steps: (1) disclosure (2) invention review and (3) patent filing. In the disclosure stage, employees who are in IP creation roles must be trained to disclose ideas that are potentially protectable IP.

Powered by WPeMatico

It’s not every day the three biggest competitors in a space join forces to denounced political action. Of course, this isn’t the first time the Trump administration has had this impact on a category.

Microsoft, Nintendo and Sony (collectively known as gaming’s “big three) penned a joint letter noting the harm the industry stands to face in the age of Trump administration tariffs on China. Addressed to Office of the United States Trade Representative General Counsel Joseph Barloon, the note asks for a modification the existing tariff list.

“While we appreciate the Administration’s efforts to protect U.S. intellectual property and preserve U.S. high-tech leadership,” the letter reads, diplomatically, “the disproportionate harm caused by these tariffs to U.S. consumers and businesses will undermine—not advance—these goals.”

The three companies highlight a broad range of cascading impacts the laws could ultimately have the vast industry, including,

The impacts of tariffs have already begun to take their toll on various technology sectors, with several leaders — including, notably, Apple’s Tim Cook — personally petitioning Trump for exceptions.

Powered by WPeMatico

“I just want to be proud of the company that I work for,” Maren Costa told me recently.

Costa is a Principal UX Design Lead at Amazon, for which she has worked since 2002. I was referred to her because of her leadership in the Amazon Employees for Climate Justice group I covered earlier this week for my series on the ethics of technology.

Like many of her peers at Amazon, Costa has been experiencing a tension between work she loves and a company culture and community she in many ways admires deeply, and what she sees as the company’s dangerous failings, or “blind spots,” regarding critical ethical issues such as climate change and AI.

Indeed, her concerns are increasingly typical of employees not only at Amazon, but throughout big tech and beyond, which seems worth noting particularly because hers is not the typical image many call to mind when thinking of giant tech companies.

A Gen-X poet and former Women’s Studies major, Costa drops casual references to neoliberal capitalism running amok into discussions of multiple topics. She has a self-deprecating sense of humor and worries about the impact of her work on women, people of color, and the Earth.

If such sentiments strike you as too idealistic to take seriously, it seems Glass Lewis and ISS, two of the world’s largest and most influential firms advising investors in such companies, would disagree. Both firms recently advised Amazon shareholders to vote in support of a resolution put forward by Amazon Employees for Climate Justice and its supporters, calling on Amazon to dramatically change its approach to climate issues.

Glass Lewis’s statement urged Amazon to “provide reassurance” about its climate policies to employees like Ms. Costa, as “the Company’s apparent inaction on issues of climate change can present human capital risks, which have the potential to lead to the Company having problems attracting and retaining talented employees.” And in its similar report, ISS highlighted research reporting that 64 percent of millennials would be reluctant to work for a company “whose corporate social responsibility record does not align with their values.”

Amazon’s top leadership and shareholders ultimately voted down the measure, but the work of the Climate Justice Employees group continues unabated. And if you read the interview below, you might well join me in believing we’ll see many similar groups crop up at peer companies in the coming years, on a variety of issues. All of those groups will require many leaders — perhaps including you. After all, as Costa said, “leadership comes from everywhere.”

Maren Costa: (Apologizes for coughing as interview was about to start)

Greg Epstein: … Well, you could say the Earth is choking too.

Costa: Segue.

Epstein: Exactly. Thank you so much for taking the time, Maren. You are something of an insider at your company.

Costa: Yeah, I took two years off, so I’ve actually worked here for 15 years but started 17 years ago. I actually came back to Amazon, which is surprising to me.

Epstein: You’ve really seen the company evolve.

Costa: Yes.

Epstein: And, in fact, you’ve helped it to evolve — I wouldn’t call myself a big Amazon customer, but based on your online portfolio, you’ve even worked on projects I personally have used. Though find it hard to believe anyone can find jeans that actually fit them on Amazon, I must say.

Costa: [My work is actually] on every page. You can’t use Amazon without using the global navigation, and that was my main project for years, in addition to a lot of the apparel and sort of the softer side of Amazon. Because when I started, it was very super male-dominated.

I mean, still is, but much more so. Jeff literally thought by putting a search box that you could type in Boolean queries was a great homepage, you know? He didn’t have any need for sort of pictures and colors.

(Photo: Lisa Werner/Moment Mobile/Getty Images)

Epstein: My previous interview [for this TechCrunch series on tech ethics] was with Jessica Powell, who used to be PR director of Google and has written a satirical novel about Google . One of the huge themes in her work is the culture at these companies that are heavily male-dominated and engineer-dominated, where maybe there are blind spots or things that the-

Costa: Totally.

Epstein: … kinds of people who’ve been good at founding these companies don’t tend to see. It sounds like that’s something you’ve been aware of and you’ve worked on over the years.

Costa: Absolutely, yes. It was actually a great opportunity, because it made my job pretty easy.

Powered by WPeMatico

Welcome to this week’s transcribed edition of This is Your Life in Silicon Valley. We’re running an experiment for Extra Crunch members that puts This is Your Life in Silicon Valley in words – so you can read from wherever you are.

This is your Life in Silicon Valley was originally started by Sunil Rajaraman and Jascha Kaykas-Wolff in 2018. Rajaraman is a serial entrepreneur and writer (Co-Founded Scripted.com, and is currently an EIR at Foundation Capital), Kaykas-Wolff is the current CMO at Mozilla and ran marketing at BitTorrent. Rajaraman and Kaykas-Wolff started the podcast after a series of blog posts that Sunil wrote for The Bold Italic went viral.

The goal of the podcast is to cover issues at the intersection of technology and culture – sharing a different perspective of life in the Bay Area. Their guests include entrepreneurs like Sam Lessin, journalists like Kara Swisher and Mike Isaac, politicians like Mayor Libby Schaaf and local business owners like David White of Flour + Water.

This week’s edition of This is Your Life in Silicon Valley features Lisa Fetterman – the Founder/CEO of Nomiku (a Y Combinator alum). Lisa talks extensively about why Silicon Valley does not care about female founders, and proposes a solution to the problem.

If you are interested in diving deep into the diversity problem in technology, this episode is for you.

For access to the full transcription, become a member of Extra Crunch. Learn more and try it for free.

Rajaraman: Welcome to season three of This is Your Life in Silicon Valley. A podcast about the Bay Area, technology and culture. I’m your host Sunil Rajaraman and I’m joined by my co-host Jascha Kaykas-Wolff.

Kaykas-Wolff: So, now I got a straw poll for you. Are you ready?

Rajaraman: I’m ready.

Powered by WPeMatico

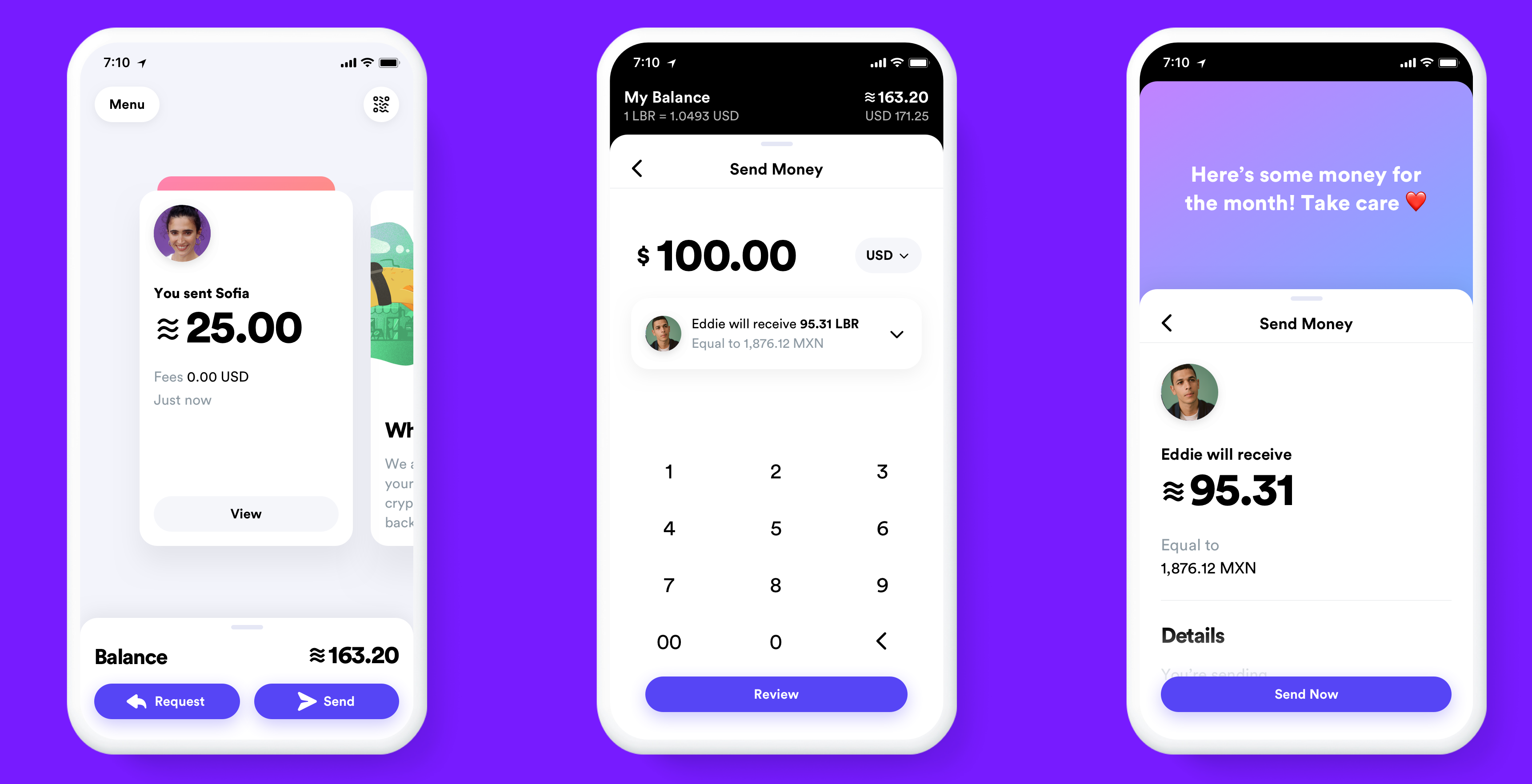

They’re not called Zuckerbucks, but Facebook just reinvented digital money. Facebook’s Libra cryptocurrency that will launch early next year is more like PayPal than Bitcoin — it’s designed to be easy enough for everyone to use. But it’s still complicated to understand, so I’m going to break it down for you nice and simple.

Watch our handy video above or read the transcript below.

Libra is like cash that lives inside your phone. How do you buy Facebook’s cryptocurrency? Starting in 2020, you’ll be able to purchase Libra through Libra wallet apps on your phone or from some local grocery and convenience stores. You cash in your local currency like dollars and get nearly the same number of Libra coins, which are represented by this wavy three-line emoji instead of the $ symbol. But first you’ll have to verify your identity with a photo.

![]()

You’ll then be able to spend your Libra while online shopping, or potentially pay for things like Ubers or your subscription for Spotify, since those companies have partnered with Facebook to make Libra popular. Since it’s almost free to digitally move Libra from one account to the other, you won’t have to pay high credit card processing fees that can add almost 4% to your total. And some Libra wallet apps and shops will give bonus discounts or free coins for signing up and paying with Libra.

You’ll also be able to send and request money from friends like you would with Venmo or PayPal. It’s as easy to send Libra as it is a message. In fact, Facebook is building its own Libra wallet app called Calibra that will live inside of WhatsApp, Facebook Messenger and its own standalone app.

You won’t have to attach your real name and identity to any of your payments, but they will be public. Facebook knows it’s a little bit creepy and you probably don’t want it spying on what you buy. So Facebook set up a new company also called Calibra that will keep all your financial data separate from your Facebook profile. That means it can’t use your transaction data to target you with ads, re-order your News Feed or sell your info to marketers.

Eventually, Facebook hopes you’ll use Libra to pay your bills, scan your wallet’s QR code to purchase coffee or tap your phone to buy your public transit ticket. At any time, you can cash out of Libra and get your local currency back in your bank account, or handed to you at a local grocery store.

But how does the Libra cryptocurrency technically work…without a bunch of blockchain buzzwords? Libra is coded to have a stable price, be secure and be controlled not just by Facebook.

Instead, Libra is run by the 28-member Libra Association that it hopes will grow to 100 members by the time it launches in the first half of 2020. Financial companies like Visa and Mastercard, merchants and apps like eBay and Lyft, venture capital funds like Andreessen Horowitz and Union Square Ventures and nonprofits like Kiva are all members. They each paid at least $10 million to get one vote on the Libra council that controls what happens to the currency. They’ll be responsible for checking to make sure Libra transactions are real and creating the Libra Reserve.

Each time you cash in a dollar, that money goes into a big bank account called the Libra Reserve that creates and sends you roughly one Libra token. The Libra Reserve is made up of a collection of the most stable international currencies, like the U.S. dollar, British pound, the euro and the Japanese yen. The idea is that even if one of those currencies goes up or down in price, the value of the Libra will stay stable. That way, shops will accept the Libra as payment without worrying the value of the coin will drop tomorrow. Big swings in price are why older cryptocurrencies like Bitcoin or Ethereal haven’t grown popular as payment methods. Libra can also handle 1,000 transactions per second, while Bitcoin can only handle 7.

So how do Facebook and the other Libra Association members earn money? Off of interest on all the assets held in the Libra Reserve. After the Libra Association pays for its operations and investments in technology, members earns a cut of the remaining interest in proportion to how much they invested when they joined. If Libra gets popular, tons of people cash in and the reserve grows huge, the interest could add up to serious revenue for Facebook.

But there’s also a subtle second way Facebook could get rich from Libra. If the currency makes it easier for small businesses to accept payments online, they’ll sell more stuff. They’ll then have extra money to spend on Facebook ads, which will make it extra quick to buy things with Libra. Ninety million small businesses already have Facebook Pages, but Facebook only has 7 million advertisers. If it can turn more of those local merchants into ad buyers, Facebook’s revenues could skyrocket.

The big risk of Libra is that anyone will be able to develop apps for it. That could lead to another Cambridge Analytica situation. But instead of some shady app maker snatching your personal info, they could steal your digital currency. Facebook and the Libra Association say they won’t vet Libra developers, which leaves the door wide open to abuse. And if people get scammed, they’ll blame Facebook.

But if Facebook succeeds, the real win could be for the 1.7 billion people left in poverty with no bank account around the world. They’re exploited by international money sending services like Western Union or Monogram that charge steep 7% fees that take $50 billion away from families per year. And if they’re mugged, they could lose all their money since they have nothing stored online. All they’ll need is a photo ID and Libra could give them an alternative to a bank account that’s tougher to steal and could make it easy to pay for what they need.

There are plenty of reasons to worry that Libra could give Facebook and other tech giants more power or lead to people getting scammed. But it could also give disadvantaged people everywhere a way to join the modern economy. And at least it’s not called FaceCoin.

And if you want to know how Libra could spawn Facebook’s next scandal, read this:

Video by Gregory Manalo, b-roll via Libra Association

Powered by WPeMatico

Everyone’s worried about Mark Zuckerberg controlling the next currency, but I’m more concerned about a crypto Cambridge Analytica.

Today Facebook announced Libra, its forthcoming stablecoin designed to let you shop and send money overseas with almost zero transaction fees. Immediately, critics started harping about the dangers of centralizing control of tomorrow’s money in the hands of a company with a poor track record of privacy and security.

Facebook anticipated this, though, and created a subsidiary called Calibra to run its crypto dealings and keep all transaction data separate from your social data. Facebook shares control of Libra with 27 other Libra Association founding members, and as many as 100 total when the token launches in the first half of 2020. Each member gets just one vote on the Libra council, so Facebook can’t hijack the token’s governance even though it invented it.

With privacy fears and centralized control issues at least somewhat addressed, there’s always the issue of security. Facebook naturally has a huge target on its back for hackers. Not just because Libra could hold so much value to steal, but because plenty of trolls would get off on screwing up Facebook’s currency. That’s why Facebook open-sourced the Libra Blockchain and is offering a prototype in a pre-launch testnet. This developer beta plus a bug bounty program run in partnership with HackerOne is meant to surface all the flaws and vulnerabilities before Libra goes live with real money connected.

Yet that leaves one giant vector for abuse of Libra: the developer platform.

“Essential to the spirit of Libra . . . the Libra Blockchain will be open to everyone: any consumer, developer, or business can use the Libra network, build products on top of it, and add value through their services. Open access ensures low barriers to entry and innovation and encourages healthy competition that benefits consumers,” Facebook explained in its white paper and Libra launch documents. It’s even building a whole coding language called Move for making Libra apps.

Apparently Facebook has already forgotten how allowing anyone to build on the Facebook app platform and its low barriers to “innovation” are exactly what opened the door for Cambridge Analytica to hijack 87 million people’s personal data and use it for political ad targeting.

But in this case, it won’t be users’ interests and birthdays that get grabbed. It could be hundreds or thousands of dollars’ worth of Libra currency that’s stolen. A shady developer could build a wallet that just cleans out a user’s account or funnels their coins to the wrong recipient, mines their purchase history for marketing data or uses them to launder money. Digital risks become a lot less abstract when real-world assets are at stake.

In the wake of the Cambridge Analytica scandal, Facebook raced to lock down its app platform, restrict APIs, more heavily vet new developers and audit ones that look shady. So you’d imagine the Libra Association would be planning to thoroughly scrutinize any developer trying to build a Libra wallet, exchange or other related app, right? “There are no plans for the Libra Association to take a role in actively vetting [developers],” Calibra’s head of product Kevin Weil surprisingly told me. “The minute that you start limiting it is the minute you start walking back to the system you have today with a closed ecosystem and a smaller number of competitors, and you start to see fees rise.”

That translates to “the minute we start responsibly verifying Libra app developers, things start to get expensive, complicated or agitating to cryptocurrency purists. That might hurt growth and adoption.” You know what will hurt growth of Libra a lot worse? A sob story about some migrant family or a small business getting all their Libra stolen. And that blame is going to land squarely on Facebook, not some amorphous Libra Association.

Image via Getty Images / alashi

Inevitably, some unsavvy users won’t understand the difference between Facebook’s own wallet app Calibra and any other app built for the currency. “Libra is Facebook’s cryptocurrency. They wouldn’t let me get robbed,” some will surely say. And on Calibra they’d be right. It’s a custodial wallet that will refund you if your Libra are stolen and it offers 24/7 customer support via chat to help you regain access to your account.

Yet the Libra Blockchain itself is irreversible. Outside of custodial wallets like Calibra, there’s no getting your stolen or mis-sent money back. There’s likely no customer support. And there are plenty of crooked crypto developers happy to prey on the inexperienced. Indeed, $1.7 billion in cryptocurrency was stolen last year alone, according to CypherTrace via CNBC. “As with anything, there’s fraud and there are scams in the existing financial ecosystem today . . . that’s going to be true of Libra too. There’s nothing special or magical that prevents that,” says Weil, who concluded “I think those pros massively outweigh the cons.”

Until now, the blockchain world was mostly inhabited by technologists, except for when skyrocketing values convinced average citizens to invest in Bitcoin just before prices crashed. Now Facebook wants to bring its family of apps’ 2.7 billion users into the world of cryptocurrency. That’s deeply worrisome.

Facebook founder and CEO Mark Zuckerberg arrives to testify during a Senate Commerce, Science and Transportation Committee and Senate Judiciary Committee joint hearing about Facebook on Capitol Hill in Washington, DC, April 10, 2018. (Photo: SAUL LOEB/AFP/Getty Images)

Regulators are already bristling, but perhaps for the wrong reasons. Democrat Senator Sherrod Brown tweeted that “We cannot allow Facebook to run a risky new cryptocurrency out of a Swiss bank account without oversight.” And French Finance Minister Bruno Le Maire told Europe 1 radio that Libra can’t be allowed to “become a sovereign currency.”

Most harshly, Rep. Maxine Waters issued a statement saying, “Given the company’s troubled past, I am requesting that Facebook agree to a moratorium on any movement forward on developing a cryptocurrency until Congress and regulators have the opportunity to examine these issues and take action.”

Yet Facebook has just one vote in controlling the currency, and the Libra Association preempted these criticisms, writing, “We welcome public inquiry and accountability. We are committed to a dialogue with regulators and policymakers. We share policymakers’ interest in the ongoing stability of national currencies.”

That’s why as lawmakers confer about how to regulate Libra, I hope they remember what triggered the last round of Facebook execs having to appear before Congress and Parliament. A totally open, unvetted Libra developer platform in the name of “innovation” over safety is a ticking time bomb. Governments should insist the Libra Association thoroughly audit developers and maintain the power to ban bad actors. In this strange new crypto world, the public can’t be expected to perfectly protect itself from Cambridge Analytica 2.$.

Get up to speed on Facebook’s Libra with this handy guide:

Powered by WPeMatico

When a company hires talent away from a competitor, onboarding the new employee can pose significant legal risks for both the company and the new employee. A fundamental aspect of Silicon Valley is that employees are generally free to move between competitors.

This unrestricted movement of talent facilitates the robust competition that helps drive the Silicon Valley economy. While this is no doubt positive, unfettered employment mobility also creates unique challenges when it comes to protecting a company’s trade secrets, which are the lifeblood of many Silicon Valley companies.

Because of California’s policies regarding free employment mobility, unlike in most other states, California companies cannot protect their trade secrets with non-compete contracts. So, they instead rely heavily on trade secret laws for protection.

And, of course, when trade secret theft occurs, it is often when an employee transitions from one company to another. Thus, when a key employee gives notice that he or she is leaving for a competitor, it sets off alarm bells for the soon-to-be former company.

Unfortunately, because of the hypersensitivity to protecting trade secrets, many departing employees who have no interest in actually taking their former company’s trade secrets get accused of theft. This allegation can trigger a long, stressful, expensive legal process for both the employee and the new company, and sometimes cost the employee his or her reputation and new job.

This article explains how this situation arises and provides some practical considerations for how the employee transitioning jobs, and the onboarding company, can avoid an unnecessary legal fight.

Powered by WPeMatico