Polaris Partners

Auto Added by WPeMatico

Auto Added by WPeMatico

SpineZone is a startup that creates personalized exercise programs and treatment for neck and back pain. The company uses an online platform and in-person clinics to deliver a curriculum that, ideally, helps patients avoid the need for prescription drugs, injections and surgeries, and providers then avoid the cost of all of the above. Co-founded by brothers Kian Raiszadeh and Kamshad Raiszadeh, the company tells TechCrunch that it has raised $12 million in a Series A round led by Polaris Partners and Providence Ventures, with participation from Martin Ventures.

At its core, SpineZone is a virtual physical therapy platform augmented by in-person clinics. The latter bit is important because it takes a video repository, which has health outcomes baked into it, and helps get those same users some real-life support.

Patients can log onto the site, either through smartphone or laptop, and then answer a series of questions around pain and risk factors. Then, patients can go through a series of exercises. These exercises are created in tandem with professionals, and are based on peer-reviewed and evidence-based articles on musculoskeletal health.

Beyond this digital archive of videos, SpineZone offers an in-person clinic option to help patients practice these exercises. Off of this strategy, the startup claims that it has “1 million lives under management.”

SpineZone’s value proposition is that it helps payers and providers, whether that be employers, clinics or health plans such as Cigna or Aetna, avoid placing their patients in surgeries, which are expensive. By taking care of pain issues before they bubble up, SpineZone says that its current partners have been able to have a 50% reduction in surgery rate (it’s worth noting that COVID-19 could also play a role in this because it is high-risk to enter a medical facility).

Partners are happy because footing the bill of a non-operative procedure is remarkably cheaper than a non-operative procedure.

The cost saving that a medical center could endure can be in the millions. For example, the Sharp Community Medical Group saved $3.4 million in cost savings after working with SpineZone for two years.

SpineZone’s business model is a smidge more complicated than your classic SaaS fee. For example, it charges a clinic based on the number of members it serves per month, and also shares in the downside. For example, if SpineZone promises to get a clinic to $12 million in spend from $15 million, and the cost ends up being $17 million, the company will pay the clinic a portion of the difference. Alternatively, if SpineZone got the clinic to $10 million, even below estimates, it shares in the upside.

SpineZone joins a cohort of health tech startups that focus on musculoskeletal conditions. Venture-backed competitors include Peerwell, Force Therapeutics and Hinge Health, which was most recently valued at $3 billion, with plans to go public.

In order to win, many startups, SpineZone including, need value-based care to replace fee-for-service care. Value-based care is the idea that doctors are paid for outcomes instead of the number of times you enter a doctor’s office. The end goal is that this format creates monetary incentives around getting to an outcome faster: If a doctor is going to make $30,000 on fixing a knee, regardless of whether it takes two appointments or 20 appointments, they might as well do a more thorough job upon check-up instead of elongating the process. The flipside of this, of course, is that doctors might optimize for outcome volume and speed rather than the quality of the result itself.

While SpineZone’s early traction is promising, the healthcare ecosystem still has a ways to go before value-based models take precedence. Right now, Kian Raiszadeh estimates that 10 to 20% of revenue in a medical center comes from value-based care. SpineZone is projecting that it will get to 50% of revenue in the near future.

“And that’s the biggest evolution and tallest lift that we’re expecting,” he said.

Early Stage is the premiere ‘how-to’ event for startup entrepreneurs and investors. You’ll hear first-hand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company-building: Fundraising, recruiting, sales, legal, PR, marketing and brand building. Each session also has audience participation built-in – there’s ample time included in each for audience questions and discussion.

Powered by WPeMatico

Thirty Madison, the New York-based startup developing a range of direct to consumer treatments for hair loss, migraines and chronic indigestion, has raised $47 million in new financing.

After last week’s nearly $19 billion merger between Teladoc and Livongo, remote therapies and virtual care companies are all the rage among the healthcare industry, and Thirty Madison’s business is no exception.

An indicator of just how important these companies are to the future of the healthcare business can be seen in the presence of Johnson & Johnson Innovation – JJDC, Inc. (JJDC) in the latest round for Thirty Madison.

Existing investors Maveron and Northzone also returned to back the company in a deal led by Polaris Partners. Thirty Madison has raised a total of $70 million so far.

Founded just three years ago by Steven Gutentag and Demetri Karagas, Thirty Madison expanded from treating hair loss with its Keeps brand in 2018 to migraine treatments in early 2019 with Cove, and launched Evens (the company’s acid reflux treatment service) later that year.

Thirty Madison has just begun offering urgent care consultations for users on a pay-what-you-will model.

And the company’s founders differentiate Thirty Madison’s business from their better-funded competitors like Hims and Ro by emphasizing that their company provides continuing care after a diagnosis and offers a range of treatment options for the conditions that the company treats. That, coupled with the more narrow focus on a few specific conditions, distinguish Thirty Madison from its peers in the industry.

“Over 59% of Americans suffer from at least one chronic condition, but few resources exist to help them connect the dots of their care,” said Amy Schulman, a partner with Polaris Partners and new director on the Thirty Madison board.

Powered by WPeMatico

The microbiome testing service uBiome has placed its founders and co-chief executives, Jessica Richman and Zac Apte, on administrative leave following an FBI raid on the company’s offices last week.

The company’s board of directors have named John Rakow, currently the company’s general counsel, as its interim chairman and chief executive, the company said in a statement.

Directors of the company are also conducting an independent investigation into the company’s billing practices, which is being overseen by a special committee of the board.

It was only last week that the FBI went to the company’s headquarters to search for documents related to an ongoing investigation. What’s at issue is the way that the company was billing insurers for the microbiome tests it was performing on customers.

“As interim CEO of uBiome, I want all of our stakeholders to know that we intend to cooperate fully with government authorities and private payors to satisfactorily resolve the questions that have been raised, and we will take any corrective actions that are needed to ensure we can become a stronger company better able to serve patients and healthcare providers,” Rakow said in a statement.

”My confidence is based on the significant clinical evidence and medical literature that demonstrates the utility and value of uBiome’s products as important tools for patients, health care providers and our commercial partners.” added Mr. Rakow.

It’s been a rough few weeks for consumer companies working on developing microbiome testing services and treatments based on those diagnosis. In addition to the FBI raid, the Seattle-based company, Arivale, was forced to shut down its “consumer program” after raising more than $50 million from investors, including Maveron, Polaris Partners and ARCH Venture Partners.

UBiome is backed by investors including Andreessen Horowitz, OS Fund, 8VC, Y Combinator, DNA Capital, Crunchfund, StartX, Kapor Capital, Starlight Ventures and 500 Startups.

Powered by WPeMatico

Backed with nearly $87 million in venture capital funding from GV, Oak HC/FT and F-Prime Capital, Quartet Health was founded in 2014 by Arun Gupta, Steve Shulman and David Wennberg to improve access to behavioral healthcare. Its mission: “enable every person in our society to thrive by building a collaborative behavioral and physical health ecosystem.”

Recent shakeups within the New York-based company’s c-suite and a perusal of its Glassdoor profile suggest Quartet’s culture is not fully in line with its own philosophy.

In the last few weeks, chief product officer Rajesh Midha has left the company and president and chief operating officer David Liu is on his way out, TechCrunch has learned and confirmed with Quartet. Founding chief executive officer Arun Gupta, meanwhile, has stepped into the executive chairman role, relinquishing responsibility of the company’s day-to-day operations to former chief science officer David Wennberg, who’s taken over as CEO.

“I’m focusing on our external growth,” Gupta told TechCrunch on Friday. “David has really stepped up as CEO.”

Gupta and Wennberg said Liu’s role was no longer needed because Wennberg had assumed his responsibilities. Liu will formally exit the company at the end of the month. As for its product chief, the pair say Midha had “transitioned out” of the role and that an unnamed internal candidate was tapped to replace him.

When asked whether other employees had left in recent weeks, Wennberg provided the following indeterminate statement: “We are always having people coming in. I don’t think we’ve had any unusual turnover. We’re hiring and people’s roles change and that’s just part of growth.”

Quartet, which provides a platform that allows providers to collaborate on treatment plans, currently has 150 employees, according to its executives.

In a LinkedIn status update published this week — after TechCrunch’s initial inquiries — Gupta announced his transition to executive chairman:

“Still full-time, though focused largely on our opportunity to further evangelize our mission, [I will] drive the change we want to see in this world, and expand our reach … I have tremendous confidence in David’s ability to lead our many talented Quartetians to deliver this next phase.”

Several former employees seemed less than pleased with Gupta’s performance, writing in a number of Glassdoor reviews that he was “abominable,” “kind of a monster” and “by far the worst executive.”

When asked for comment on those reviews, Gupta and Wennberg shrugged it off: “Glassdoor is Glassdoor.” They agreed its important to pay attention to but impossible to vet.

Gupta began his career as a management consultant at McKinsey and served as a consultant to The World Bank before joining Palantir, Peter Thiel’s data-mining company, as an advisor in 2014. Wennberg, for his part, was the CEO of The High Value Healthcare Collaborative, a consortium of 15 healthcare delivery systems, before co-founding Quartet.

In January, Quartet raised a $40 million Series C to expand throughout the U.S. F-Prime Capital and Polaris Partners led the round, with participation from GV and Oak HC/FT. The financing valued the company at $300 million, according to PitchBook.

As part of the funding, Quartet announced it was adding three new directors to its board: F-Prime’s executive partner Carl Byers; Ken Goulet, an executive vice president at health insurance provider Anthem; and former Rackspace CEO and BuildGroup co-founder Lanham Napier. Other outside board members include Oak HC/FT’s managing partner Annie Lamont, GV partner Krishna Yeshwant, Polaris managing partner Brian Chee and former U.S. Congressman Patrick Kennedy.

Quartet previously raised a $40 million Series B in April 2016 led by GV. The investment marked the venture capital investment arm of Google’s first in a mental health startup. Before that, the startup brought in a $7 million Series A led by Oak HC/FT’s managing partner Annie Lamont.

For now, Quartet remains committed to growth.

“We learn from what we are doing and we continue to learn,” Wennberg said. “That is part of growth. It’s hard and you just keep working and growing because we have a huge mission.”

Powered by WPeMatico

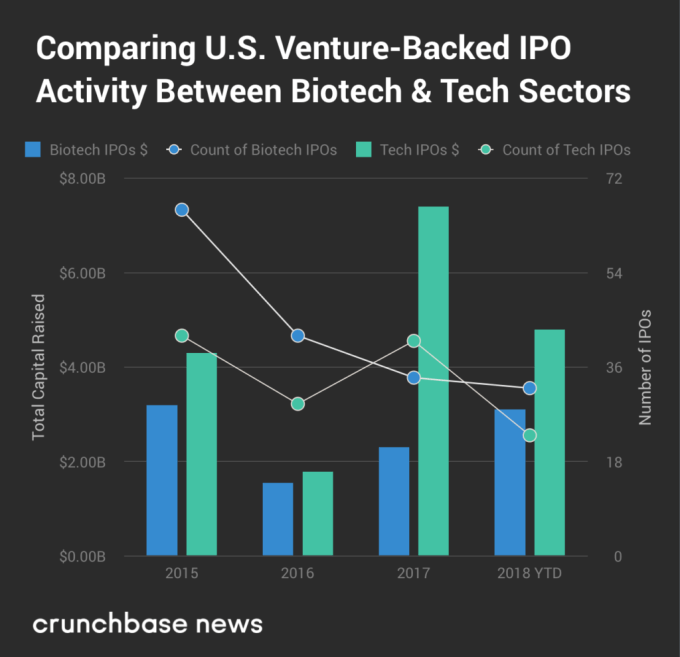

For people who make investment decisions based on revenues and projected earnings, biotech IPOs are kind of a non-starter. Not only are new market entrants universally unprofitable, most have zero revenue. Going public is mostly a means to raise money for clinical trials, with red ink expected for years to come.

That pattern may be one reason the venture capital press, Crunchbase News included, tends to devote a disproportionately small portion of coverage to biotech IPOs. It’s more exciting to watch a big-name internet company pop in first-day trading or poke fun at an underperforming dud.

But with our fixation on all things tech, we’re missing out on the big picture. There are actually a lot more biotech and healthcare startup IPOs than tech offerings. In the second quarter of this year, for instance, at least 16 U.S. venture-backed biotech and healthcare companies went public, compared to just 11 tech startups. In three of the past four years, bio offerings outnumbered tech IPOs, according to Crunchbase data.

In the following analysis, we attempt to get up to speed on the pace of biotech offerings, assess where we are in the cycle and spotlight some of the rising stars.

As mentioned above, U.S. bio IPOs outnumber tech offerings in most years. However, the bio cohort raises less total capital, partly because the largest technology IPOs tend to be much bigger than the largest bio IPOs. In the chart below, we compare the two sectors over the past four years.

Globally, the numbers are much higher. Using Crunchbase data, we’ve put together a chart looking at global VC-backed biotech and healthcare IPOs over the past four years. While we’re just over halfway through 2018, biotech and health IPOs have already raised more money than in any of the prior three full calendar years.

It’s pretty clear we’re in an upcycle for all things startup-related. VCs are flush with cash, late-stage rounds are ballooning in size and IPO and M&A action is picking up, too.

So what does that mean for bio IPOs? Is the uptick in the pace and size of offerings mostly a result of bullish market conditions? Or is the current slate of pre-IPO candidates more compelling than in the past?

We turned to Bob Nelsen, co-founder of ARCH Venture Partners, one of the top-performing biotech investors, for his take, which is that it’s a “fundamentals driven, cycle amplified” IPO boomlet.

More companies are launching well-received IPOs because the pace of startup innovation is faster than in the past. Nelson calls it “the result of the previous 30 years of investment and innovation in biotech that has finally led to essentially data-driven innovation.” That’s leading to more curative treatments, disease-modifying therapies and preventative technologies.

Yet we’re also in a bullish segment of the market cycle for biotech. That’s prompting companies that might have stayed private under other conditions to give going public a shot. It’s also providing bigger outcomes for emerging companies that were already on the IPO track.

The latest example of a big outcome IPO is Rubius Therapeutics, which develops drugs based on genetically engineered red blood cells. This week, the five-year-old company raised $241 million at an initial valuation of over $2 billion, making it the largest bio offering of 2018. The Cambridge, Mass. company, which previously raised nearly a quarter-billion-dollars in venture funding, is still in the pre-clinical trial phase.

This year has delivered several other good-sized offerings as well, including drug developers Eidos Therapeutics and Homology Medicines, recently valued around $800 million each, along with Tricida, valued around $1.2 billion. (See the full list of 2018 global bio and health offerings here.)

As for aftermarket performance, that’s been up and down, but includes some big ups. Last year, biotech led the pack for best-performing IPOs on U.S. exchanges. The sector accounted for four of the six top spots, according to Renaissance Capital, led by drug developers AnaptysBio, Argenx and UroGen, along with Calyxt, an agbio startup.

While things are already up, bio VCs, generally an optimistic bunch, see several reasons why bio IPOs could go higher.

Nelson points to what he sees as the lagging pace of in-house innovation at big pharma and biotech players. Increasingly, they need to acquire startups and recently public companies to stay competitive and build out new product pipelines.

There is also tons of fresh capital earmarked for healthcare startups. In the U.S. in 2017, healthcare-focused venture capitalists raised $9.1 billion. That figure was up 26 percent from 2016, per Silicon Valley Bank.

More dollars also are flowing from venture firms that invest in a mix of tech and life sciences through a single fund. That list includes well-established VCs with dry powder to invest, including Polaris Partners, Founders Fund, Kleiner Perkins and Sequoia Capital.

Still, Nelson observes, deep into an IPO bull market, the average quality of offerings does tend to decline. That said, he’s been through similar inflection points in previous cycles and “for the same point in the cycle, the quality is markedly higher.”

Powered by WPeMatico

Boston-based Drizly used to be known as the on-demand delivery app for alcohol. More recently, the company evolved into a marketplace that helps brick-and-mortar liquor stores to connect with and sell to customers nearby through web and mobile commerce. The Drizly app shows shoppers different prices on the beer, wine and liquor that they’re looking for at local shops, along with… Read More

Boston-based Drizly used to be known as the on-demand delivery app for alcohol. More recently, the company evolved into a marketplace that helps brick-and-mortar liquor stores to connect with and sell to customers nearby through web and mobile commerce. The Drizly app shows shoppers different prices on the beer, wine and liquor that they’re looking for at local shops, along with… Read More

Powered by WPeMatico