Plaid

Auto Added by WPeMatico

Auto Added by WPeMatico

Sila announced Monday it raised $13 million in Series A funding for its banking and payment platform that gives software teams tools to build the next generation of financial products and services.

Revolution Ventures led the round and was joined by existing investors Madrona Venture Group, Oregon Venture Fund and Mucker Capital, as well as Wise co-founder Taavet Hinrikus. The funding brings the total investment to date for Portland, Oregon-based Sila to $20 million.

The company was founded in 2018 by Shamir Karkal, Angela Angelovska, Isaac Hines and Alex Lipton to simplify digital payments and storage in a regulatory compliant way and build on blockchain technology. CEO Karkal has a long history in the fintech space, co-founding Simple, an app unifying various accounts into one accessible bank card, in 2009. It was acquired by BBVA in 2014 for $117 million and shuttered earlier this year.

Karkal told TechCrunch that the idea for Sila was born out of frustration while starting another bank. He saw a need for financial application development, but was hindered by a banking system “still stuck in the 20th century.” He thought consumers expected a different level of service, which is why many flock to fintechs.

However, whenever a business tried to connect existing banking systems, fintechs and cryptocurrency innovators, as it built and scale, would always run into technology and compliance issues, Karkal said.

“The problem with working with banks, is that you have to figure out how to integrate with their mainframe,” he added. “In the process, you end up having to also be compliance experts just to be able to do it.”

Whereas it took Karkal three years to get bank processes set up for other companies, it took Sila 18 months. Its banking APIs enable developers to create their own digital wallets, replacing the need to integrate with legacy financial institutions. Sila also has partnerships with fintech platforms, including Plaid, Alloy, Lithic and Arcus to move money, and is backed by Evolve Bank and Trust.

Sila can now get customers up-and-running in six to eight weeks. And unlike competitors that focus almost exclusively on e-commerce, most of Sila’s customers are doing regulated payments within the fintech, insurtech, commercial real estate and cryptocurrency spaces that tend to be more complex from a compliance basis, Karkal said.

Since the company launched its platform, business was building steadily, and took off in the second half of 2020. The company raised a $7.7 million seed round earlier in the year. In the last 12 months, Sila grew its revenue 10 times and customers’ end users grew over 500% in the last seven months.

Sila will use the new funding to increase headcount, target additional partners and expand product features, including its Ethereum MainNet stablecoin issuance and interoperability between FedWire and the Nacha Automated Clearing House network.

“There is a massive wave of fintechs emerging in the U.S., and we have barely scratched the surface,” Karkal said. “Places like India, Africa and Latin America could accelerate at the same time because they are mainly starting from zero. We are here to ‘arm the rebels’ and help those innovators build applications to give all end users a much better financial experience.”

As part of the investment, Clara Sieg, partner at Revolution Ventures, is joining the company’s board. She told TechCrunch she met the company’s co-founders through the Portland ecosystem.

Revolution tends to look at fintech startups from a consumer angle. Recognizing that the problem with building infrastructure meant dealing with banks, the firm set out how to find a company building the pipes to solve it, she said.

In the landscape of fintech, she considers Dwolla to be a competitor to Sila. Last week, the company raised $21 million to continue developing its API that allows companies to build and facilitate fast payments, specifically with a focus on ACH. However, it comes down to actually signing up customers, and that competitive landscape is pretty thin, Sieg added.

“Sila is building an easy way for people to program money and taking a regulatory eye to things,” Sieg said. “When Shamir was building Simple, he could see how challenging it was for incumbents to provide the tools developers need to embed financial services, and this is why we have confidence in his ability to win.”

Powered by WPeMatico

Plaid, the fintech giant, has announced the inaugural cohort of startups in its new accelerator program, FinRise.

The equity-free and capital-free program has chosen five early-stage fintech startups out of 100 applications to join its cohort, working on issues central to the financial services industry such as simplifying payments and access to credit. The accelerator, announced two months ago, is explicitly focused on backing underrepresented founders in tech.

Last week, The Information reported that Plaid is nearing a new financing deal that would value the company at between $10 billion to $15 billion. Beyond a high valuation, Plaid sports a key characteristic that positions it well to help early-stage startups: it has gone through regulatory hurdles. Months ago, Plaid announced it would not merge with Visa in what would have been a $5.3 billion acquisition. This event, as well as advice on how private fintech startups can deal with policy issues, will be part of FinRise programming.

While participants don’t get funding, FinRise has collated a number of “capital access partners,” which basically means investors who are committed to meeting with these companies and potentially writing a check. This network includes Accion, Acrew, Amex Ventures, Flourish, Harlem Capital, Kapor, Matrix, Village Capital, Visible Hands and First Round.

Powered by WPeMatico

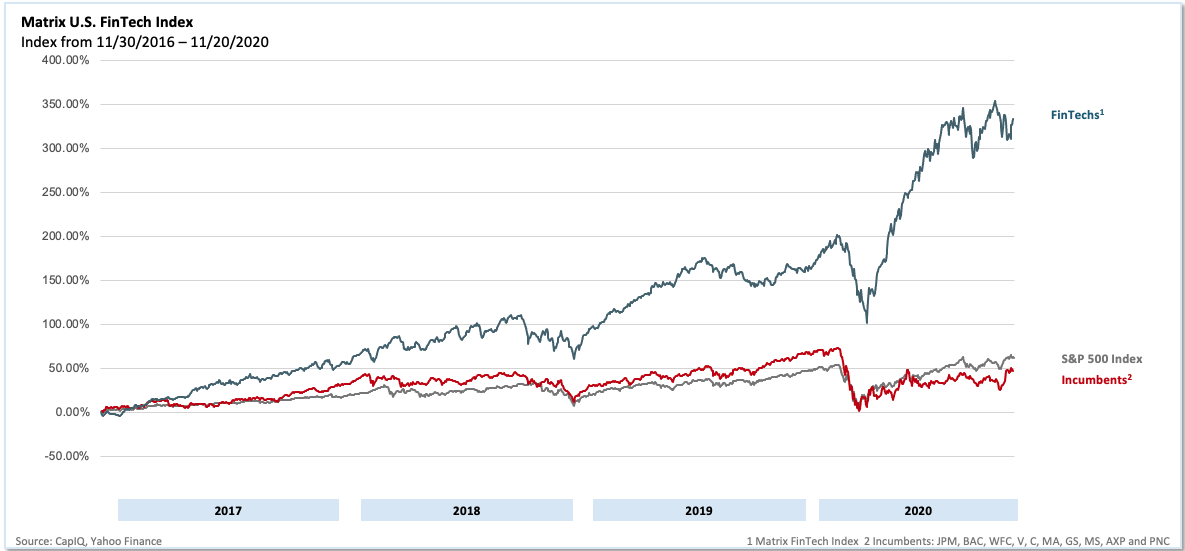

Three years ago, we released the first edition of the Matrix Fintech Index. We believed then, as we do now, that fintech represents one of the most exciting major innovation cycles of this decade. In 2020, all the long-term trends forcing change in this sector continued and even accelerated.

The broad movement away from credit toward debit, particularly among younger consumers, represents one such macro shift. However, the pandemic also created new, unforeseen drivers. Among them, millennials decamped from their rentals in crowded cities to accelerate their first home purchases to the benefit of proptech companies and challenger mortgage players alike.

E-commerce saw an enormous acceleration in growth rates, furthering adoption of online payments platforms. Lastly, low interest rates and looming inflation helped pave the way for the price of Bitcoin to charge toward $30,000. In short, multiple tailwinds combined to produce a blockbuster year for the category.

In this year’s refresh of the Matrix Fintech Index, we’ll divide our attention into three parts. First, a look at the public stocks’ performance. Second, liquidity. Third, we highlight one major trend in the sector: Buy Now Pay Later, or BNPL.

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index. While the underlying performance of these companies was strong, the pandemic further bolstered results as consumers avoided appearing in-person for both shopping and banking. Instead, they sought — and found — digital alternatives.

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index.

Our own representation of the public fintechs’ performance is the Matrix Fintech Index — a market cap-weighted index that tracks the progress of a portfolio of 25 leading public fintech companies. The Matrix fintech Index rose 97% in 2020, compared to a 14% rise in the S&P 500 and a 10% drop for the incumbent financial service companies over the same time period.

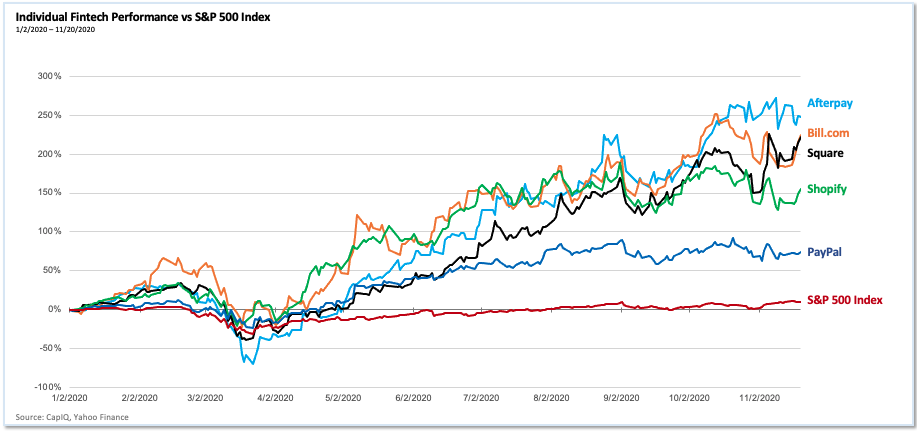

2020 performance of individual fintech companies vs. SPX Image Credits: CapiQ, Yahoo Finance

Matrix U.S. Fintech Index, 2016 -2020 Image Credits: CapiQ, Yahoo Finance

E-commerce undoubtedly stood out as a major driver. As a category, retail e-commerce grew 35% YoY as of Q3, propelling PayPal and Shopify to add over $160 billion of market capitalization over the year. For its part, PayPal in the third quarter signed up 15 million net new active accounts (its highest ever).

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

This week we — Natasha and Danny and Alex and Grace — had more than a little to noodle over, but not so much that we blocked out a second episode. We try to stick to our current format, but, may do more shows in the future. Have a thought about that? equitypod@techcrunch.com is your friend and we are listening.

Now! We took a broad approach this week, so there is a little of something for everything down below. Enjoy!

Like we said, it’s a lot, but all of it worth getting into before the weekend. Hugs from the team, we are back early Monday.

Equity drops every Monday at 7:00 a.m. PST and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Congratulations, you’re no longer selling your company for billions of dollars!

As strange as it sounds, that’s the leading perspective from venture capitalists concerning Plaid, now that its much-touted sale to Visa has fallen apart.

The $5.3 billion deal would have seen banking API startup Plaid join consumer payments and credit giant Visa. But the American government took a dim view of the deal, and according to Axios reporting, Plaid felt like it could be worth more money in time.

The TechCrunch team has collected views from venture capitalists, analysts and Anshu Sharma, CEO of another API-powered startup and a former VC to get a better view on the perspectives in the market concerning the blockbuster breakup.

From the venture capital side of things, most takes we received were bullish regarding Plaid’s chances now that it’s no longer being taken over by Visa. Amy Cheetham, for example, of Costanoa Ventures, said that the result is “good for the company, ultimately.” She added that Plaid may now see better “talent acquisition,” faster product decisions and a better eventual valuation.

“There is so much left for them to build in fintech infrastructure,” Cheetham said in an email, adding that she sees “Stripe-like scale potential” in Plaid. Stripe is reportedly raising capital at a valuation that could reach $100 billion.

Cheetham is not alone in her bullish perspective. Nico Berandi of Animo Ventures wrote to TechCrunch to say that he “still wishes” that his firm had been “around back then to have invested” in Plaid, adding a smiley face at the end of his missive.

Powered by WPeMatico

Visa and Plaid called off their agreement this afternoon, ending the consumer credit giant’s takeover of the data-focused fintech API startup.

The deal, valued at $5.3 billion at the time of its announcement, first broke cover on January 13, 2020, or nearly one year ago to the day. However, the Department of Justice filed suit to block the deal in November of 2020, arguing that the combination would “eliminate a nascent competitive threat that would likely result in substantial savings and more innovative online debit services for merchants and consumers.”

At the time Visa argued that the government’s point of view was “flawed.”

However, today the two companies confirmed the deal is officially off. In a release Visa wrote that it could have eventually executed the deal, but that “protracted and complex litigation” would take lots of time to sort out.

It all got too hard, in other words.

Plaid was a bit more upbeat in its own notes, writing that in the last year it has seen “an unprecedented uptick in demand for the services powered by Plaid.” Given the fintech boom that 2020 saw, as consumers flocked to free stock trading apps and neobanks, that Plaid saw growth last year is not surprising. After all, Plaid’s product sits between consumers and fintech companies, so if those parties were executing more transactions, the API startup likely saw more demand for its own offerings.

TechCrunch reached out to Plaid for comment on its plans as an independent company, also asking how quickly it grew during 2020. Update: Plaid responded to TechCrunch noting that it saw 60% customer growth in 2020, bringing it to more than 4,000 clients. If we presume even moderate net dollar retention amongst its customer base, Plaid could have grown by triple-digits last year, in percentage terms.

While the Visa-Plaid deal was merely a single transaction, its scuttling doesn’t bode well for other fintech startups and unicorns that might have eyed an exit to a wealthy incumbent. The Department of Justice, in other words, may have undercut the chances of M&A exits for a number of fintech-focused startups or at least created more skittishness around that possible exit path.

If so, expected exit valuations for fintech upstarts could fall. And that could ding both fintech-focused venture capital activity, and the price at which startups in the niche can raise funds. If the Visa-Plaid deal was a huge boon to fintech companies that used it as a signpost to help raise money at new, higher valuations, the inverse may also prove true.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast (now on Twitter!), where we unpack the numbers behind the headlines.

A few notes before we get into this. One, we have a bonus episode coming this Saturday focused on this week’s earnings reports. And, second, we did not record video this week. So, if you like watching the show on YouTube, this is not the week for that!

Right, here’s what Natasha, Danny and your humble servant got into this week:

We capped off with the latest from r2c, and then got the hell off the mics. Catch you all Saturday, and then back to regular programming on Monday morning.

Equity drops every Monday at 7:00 a.m. PDT and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

The fintech revolution is just getting started.

At least that’s the impression we got after a conversation with Plaid co-founder Zach Perret. He appeared on Extra Crunch Live last week to talk about his company’s announced exit to Visa and the larger fintech landscape.

Perret and Plaid announced a deal to sell the company to Visa earlier this year for $5.3 billion, a transaction that highlighted the company’s central position in the fintech world. Plaid provides APIs that link consumer bank accounts to apps and other financial services, making it the connective tissue of the fintech boom.

It’s probably no surprise, then, that Perret is bullish: “You’ve heard it a million times, but the quote of software eating the world [is true], and my corollary to that is [that] every company is a fintech company. And certainly every financial services company should be a fintech company.”

He said there’s lots of room left for fintech and finservices companies to create new products, which is not a bad view of the future if you want to be cheered up. Perret also noted that there are widespread opportunities for fintech companies to help underbanked people in the U.S. and abroad, which indicates a massive, untapped total addressable market.

To make sure you can take your own notes, we’ve included the full session below and excerpted a few passages from the transcript. (You can sign up for Extra Crunch here if you need access.)

First up, here’s the full call:

Powered by WPeMatico

The fintech wars continue to heat up with another major exit in the space.

Consumer financial services platform SoFi announced today that it is acquiring payments and bank account infrastructure company Galileo for $1.2 billion in total cash and stock. The acquisition is dependent on customary closing conditions.

Salt Lake City-based Galileo was founded in 2000 by Clay Wilkes and was bootstrapped to profitability over the intervening two decades. My colleague Jon Shieber wrote a profile of Galileo back in November after the company announced its second round of external funding, a $77 million Series A check from Accel, which was led by growth partner John Locke. The company had previously raised an $8 million Series A round from Mercato Partners in April 2014.

Galileo provides APIs that allow fintech companies like Monzo and Chime to easily create bank accounts and issue physical and virtual credit cards, among myriad other services. While simple in theory, banking regulations and financial rules place a huge regulatory burden on fintech companies, burdens that Galileo takes on as part of its platform.

The company has found particular success in the United Kingdom, where all five of the country’s largest fintechs are customers. Globally, it processed an annualized $45 billion in transaction volume last month, up from $26 billion in October 2019 — nearly doubling in just six months.

From a strategic perspective, SoFi’s objective is that Galileo will help power its expanding suite of finance products and offer it another revenue source outside of consumer services. While SoFi was founded a decade ago to offer ways to secure better financial terms for student loans, it now offers a bevy of consumer financial options, including loan, investment and insurance products as well as cash and wealth management tools. With Galileo, it now has a clear B2B revenue component as well.

SoFi, which is now led by ex-Twitter COO Anthony Noto, has also raised hundreds of millions of new capital from the likes of Qatar in recent years. The company was most recently valued at $4.3 billion.

Galileo will operate as an independent division of SoFi, and will be continuing its operations with founder Wilkes remaining as chief executive.

As fintech valuations have rapidly expanded in recent years, the companies that empower those fintechs have increasingly become strategic for investors. Earlier this year, Visa bought Plaid for $5.3 billion, in what was considered a key exit for a finance infrastructure company. That exit brought acute investor and strategic interest to the space, interest that almost certainly accrued to Galileo, as well, and helps explain the company’s relatively quick exit from its funding round last year.

As for Accel, the firm has long had a strategy of investing in mostly bootstrapped companies, sometimes a decade or more after their founding, with examples outside of Galileo including 1Password, Qualtrics, Atlassian, GoFundMe and Tenable. Accel also led this type of round into payments platform Braintree, where the firm met the startup’s GM Juan Benitez, who also joined Galileo’s board in November along with Accel’s Locke.

Accel’s valuation of the deal was not publicly disclosed in November, but a source with knowledge of the acquisition today characterizes the firm’s return as more than 4x. Given that Accel held the equity for roughly half a year, that’s quite the IRR multiple in an otherwise challenging global macro context. Given that the acquisition of Galileo was for cash and stock, Accel likely now holds a stake in SoFi, making at least part of the return unrealized.

Galileo was represented by Qatalyst in the transaction.

Updated April 7 to include the $8 million Series A funding round led by Mercato Partners and more context on IRR.

Powered by WPeMatico

These days, most of the games developed need to be social, multi-platform and extensible, but there are only a few developers with the expertise to bring those toolsets to the profusion of new games that crop up every year.

Well, now those development studios can turn to Pragma, which is building the back-end toolkit for gaming companies so their developers can focus on what they do best — making games.

It’s basically taking a page from the application development playbook where off-the-shelf toolkits can reduce by months the time it takes to get an app into the market, according to Pragma chief executive Eden Chen. In the game industry, a game can stay in beta for years as developers work out the kinks.

“In the game world, because of the necessity to build multiplayer, the length to launch a game has gotten way, way, way, way longer. Games are taking five to 10 years to launch out of beta,” Chen said.

Founded by Chen and former Riot Games engineering lead Chris Cobb, Pragma is offering a “backend as a service,” according to the company, selling a toolkit that includes accounts, player data, lobbies, matchmaking, social systems, telemetry and store fulfillment.

In a way it’s a complement to the front-end game engines from companies like Epic, the creator of Fortnite.

Indeed, Epic had announced plans to create a back-end system for game developers of its own, but Chen sees the benefits of having an independent operator doing the work — not a potential competitor.

Pragma’s investors agreed. The company raised $4.2 million in funding from a clutch of high-quality firms and individual investors, led by the Los Angeles-based Upfront Ventures with participation from Advancit Capital and angel investors Jarl Mohn, president emeritus at NPR and former Riot Games board member; Dan Dinh, founder of TSM; and William Hockey, founder of Plaid.

“In a world where gaming studios have long used third-party engines to power their front-end development, it makes no sense for the same studios to spend millions of dollars to build their own custom back-end,” said Kevin Zhang, partner at Upfront Ventures and board member at Pragma, in a statement. “This broken system has lasted for so long because creating a reusable, platform-agnostic backend is not just extremely complex but rarely prioritized compared to the game.”

The gaming industry is a $139 billion behemoth that in some ways lags behind its technologically-savvy peers in creating off-the-shelf tools to speed production. They’re combinations of social media platforms like Facebook and Snap, and big, high-budget movie productions, but lack any tools to simplify the process of development or ensure that persistence, scale and feature complexity don’t lead to downtimes. And downtimes could mean millions in expenses and lost revenues, Pragma said.

“Creating online multiplayer games is increasingly complex and expensive. Studios are hindered by the need to not just create compelling games, but also to build custom server technology to operate their game,” Chris Cobb, the company’s chief technology officer, said in a statement.

The company currently has one customer on its platform and will launch to an exclusive set of beta users in late 2020.

Powered by WPeMatico