pitchbook

Auto Added by WPeMatico

Auto Added by WPeMatico

Inflation may or may not prove transitory when it comes to consumer prices, but startup valuations are definitely rising — and noticeably so — in recent quarters.

That’s the obvious takeaway from a recent PitchBook report digging into valuation data from a host of startup funding events in the United States. While the data covers the U.S. startup market, the general trends included are likely global, given that the same venture rush that has pushed record capital into startups in the U.S. is also occurring in markets like India, Latin America, Europe and Africa.

The rapidly appreciating startup price chart is interesting, and we’ll unpack it. But the data also implies a high bar for future IPOs to not only preserve startup equity valuations at their point of exit, but exceed their private-market prices. A changing regulatory environment regarding antitrust could limit large future deals, leaving a host of startups with rich price tags and only one real path to liquidity.

Investors appear to be implicitly betting that the future IPO market will accelerate for a multiyear period at attractive prices.

That situation should be familiar: It’s the unicorn traffic jam that we’ve covered for years, in which the global startup markets create far more startups worth $1 billion and up than the public markets have historically accepted across the transom.

Let’s talk about some big numbers.

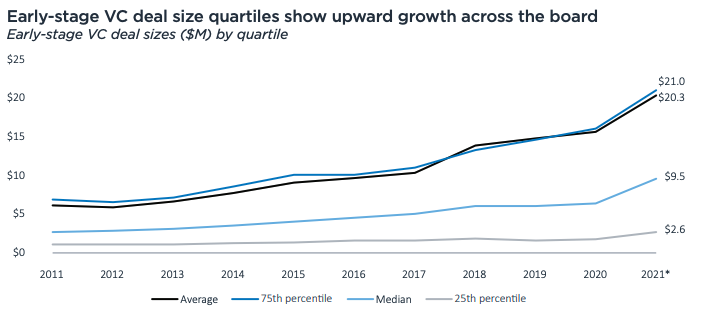

To summarize what PitchBook published: Round sizes are going up as valuations go up, and with the latter rising faster than the former, we’re not seeing investors get more ownership despite them having to spend more for deal access.

In the early-stage market, deal sizes are rising as follows:

Image Credits: PitchBook

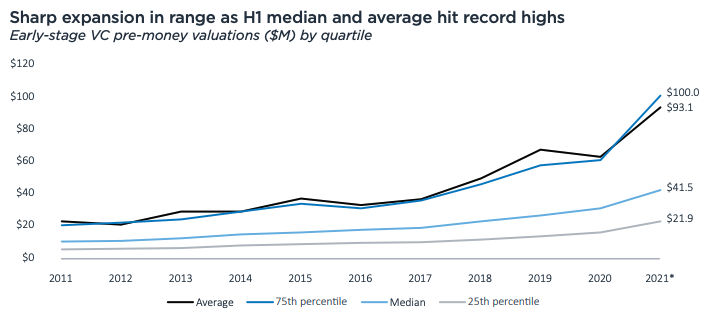

Prices are going up as well, as the following chart shows:

Image Credits: PitchBook

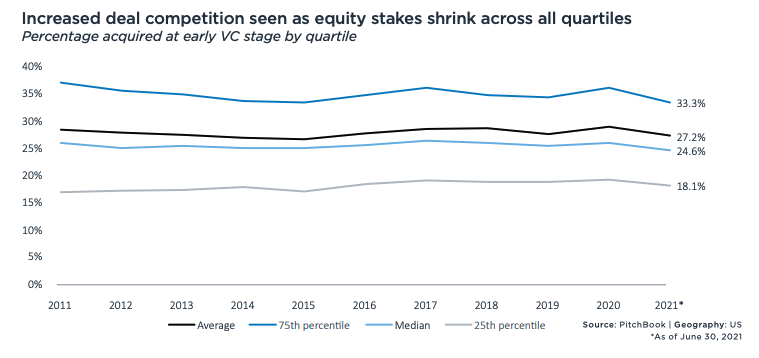

Which leads to the following decline in equity take rates:

Image Credits: PitchBook

Those charts belie somewhat how quickly venture capital is changing. For example, in 2020, the median early-stage value created between rounds was $16 million (or a 54% relative velocity, if you prefer). In 2021 thus far, it’s $39.4 million (120% relative velocity). And that 2020 figure was a prior record. It just got smashed.

The PitchBook dataset has other superlatives worth noting. Enterprise-focused seed pre-money valuations hit an average of $11 million in the first half of 2021, an all-time high. Early-stage valuations for enterprise-focused startups also hit fresh records — $92.7 million on average, $43 million median — this year after rising consistently since 2011.

And late-stage valuations for enterprise tech startups have gone vertical (chart on the right):

Powered by WPeMatico

A stunning first quarter in venture capital funding was not restricted to the United States; Europe also had one hell of a start to the year.

According to data from Dealroom and Crunchbase News, an investor, and an analyst from PitchBook, European startups put together an impressive fundraising haul. The venture capital world kicked off its 2021 European investing cycle with enough activity to set the continent on the path that would crush yearly records.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Inside the data, there’s lots to unpack, including which sectors of European startups stood out in terms of capital raised, rising seed and late-stage deals, and dollar volume. We’ll also need to discuss exits — the Deliveroo IPO and its various woes was not the only transaction from the period worth understanding.

As with our prior looks at AI startup fundraising and the United States’ own blistering start to the year, we’ll lean on multiple sources to ensure that we have a wide lens. And we’ll keep in mind that all venture capital data lags reality somewhat, as many deals from a particular period are not disclosed or discovered until long after they actually occurred.

As with our prior looks at AI startup fundraising and the United States’ own blistering start to the year, we’ll lean on multiple sources to ensure that we have a wide lens. And we’ll keep in mind that all venture capital data lags reality somewhat, as many deals from a particular period are not disclosed or discovered until long after they actually occurred.

In this case, it makes the numbers all the more impressive. Let’s get into the data.

Dealroom was first out of the gate, reporting that European startups had a record quarter in Q1 2021 back when April just got started. Its preliminary results for the first quarter indicated that startups on the continent raised €16.6 billion, or $19.9 billion at today’s exchange rates.

That total was not only a record, but what Dealroom described as double the results of Q1 2020. While we’ve become slightly inured in recent months to the venture capital market’s rapid pace and capital-rich environment, it’s worth considering for a moment, as the first quarter of last year ended, how few of us would have guessed that just a year later — as COVID-19 still harms public health and disrupts life and business — we’d see numbers like this.

The Dealroom data, however, was not all records. Round volume by the group’s estimates was down from the year-ago period, if slightly better than the last few quarters. The general move toward the later-stage and larger-round venture capital market is alive and well in Europe.

Powered by WPeMatico

It’s no surprise that the venture capital market was incredibly active in the United States during the first quarter of 2021, but precisely how strong has only recently become clear. This morning, we’re digging into the data.

According to a report from PitchBook, venture capitalists unleashed a wave of capital in the first three months of the year. So much, in fact, that funding in the United States nearly doubled compared to the same quarter of 2020.

We’ll dig into specific numbers and trends regarding aggregate venture capital results in a moment, but what stood out the most while digesting the Q1 dataset was how strong VC results appeared across different states; a solo late-stage boom the quarter was not.

Seed deal volume appeared strong and early-stage venture capital activity could reach new highs in 2021, but late-stage venture capital activity in the United States is already setting records in both deal count and invested dollars.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

We’ll parse the headline numbers and then dive into seed and super late-stage data with the help of Sarah Kunst of Cleo Capital, Jenny Lefcourt of Freestyle Capital, Iris Choi of Floodgate and Laela Sturdy of CapitalG.

With their help, we’ll contextualize the numbers and weave anecdotal observations into what the charts and graphs tell us. Especially in the case of seed data, which is famously laggy, added context is crucial. Let’s go!

According to PitchBook’s report, some 3,987 venture capital rounds were closed in the United States during Q1 2021. Those deals were worth $69 billion, a figure up nearly 93% from 2020’s first-quarter results.

In broad strokes, the United States had a crushing venture capital start to the new year, pandemic be damned. That is especially true when we consider 2020’s full-year figures. Last year, venture capitalists deployed some $166 billion into U.S.-based startups across 12,546 rounds. In contrast, if the first quarter’s pace was maintained during the rest of 2021, the United States would see around 16,000 rounds worth around $280 billion.

Of course, we cannot see the future, so those projections are merely shared to underscore how active the first quarter proved to be; we’ll have to wait for at least another quarter’s data to confidently predict full-year records for 2021.

Powering the rapid start to the venture capital year was a holistic boom: Seed deal volume is forecasted to have set a multiyear high, perhaps matching the historically strong Q2 2018 period. Early-stage venture capital during Q1 2021 was also robust, with $14.5 billion deployed across 1,170 rounds. Both numbers set a pace for fresh records in 2021.

Then there was late-stage dealmaking, which soared in the first quarter. In 2020, late-stage venture capital deals were worth $111.4 billion raised from 3,504 rounds. In the first quarter of 2021, some $51.9 billion was invested into late-stage startups across 1,291 deals.

Valuations and round sizes continued to rise across the board. If there was a better time to raise a big whack of venture capital as a U.S.-based startup, we cannot recall it. And the data seems to scream that the good times are now as good, or gooder, than ever.

Powered by WPeMatico

Microsoft’s huge purchase of health tech AI company Nuance led the technology news cycle this week. The $19.7 billion transaction is Microsoft’s second-largest to date, only beaten by its purchase of LinkedIn some years ago.

For the AI space, the sale is a coup. Nuance was already a public company, but to see Microsoft offer a firm premium over its public-market value demonstrates the value that AI technology can have to wealthy companies. For startups working in the AI space, the Nuance deal is good news; the value of AI revenue was repriced by the acquisition’s announcement — and for the better.

In light of the megadeal, The Exchange dug into the AI venture capital market. What’s happening on the startup side of the coin in the artificial intelligence and machine learning (AI/ML) space?

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

To get a handle on the situation, we’ve compiled Q1 2021 and historical venture capital investment data via PitchBook, spoken to an active venture capitalist with a focus on AI-powered startups, and heard from a couple of startups recently featured on CB Insights’ list of leading AI upstarts for their take on the recent news.

The picture that emerges is one of strong investor interest and the expectation of even more in the wake of the Microsoft-Nuance tie-up. For AI startups, it’s a great time to be in the market.

The picture that emerges is one of strong investor interest and the expectation of even more in the wake of the Microsoft-Nuance tie-up. For AI startups, it’s a great time to be in the market.

This morning, we’ll start with a look into recent venture capital activity in the AI/ML market and its historical context. Then we’ll talk to Zetta Ventures’ Jocelyn Goldfein and a few companies in the AI space. Let’s go!

According to historical data compiled by PitchBook, venture capital investment into U.S.-based, AI-focused startups is enjoying a strong start to the year. Per the group’s provided dataset, from the start of 2021 through April 12, or the first 101 days of the year, 442 deals in the space were worth $11.65 billion.

In 2020, the same query for U.S.-based startups working in the AI and ML space — the line between ML and AI is blurrier than ever — turned up 1,601 rounds worth $27.49 billion.

Powered by WPeMatico

The fourth quarter of 2020 was as busy as you imagined, with super-late-stage startups reaching new valuation thresholds at a record pace, and total venture capital funding in the United States recording its second-best result of all time.

That’s according to data released recently by CB Insights, which complements our look back at 2020’s venture capital year in America from yesterday.

At the time, we noted that American startups raised an average of $428 million each day last year, a sum that helps illustrate how rapid the private markets moved during the odd period.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But a peek at aggregate results for the world’s largest VC market provides only part of the picture. We need to narrow our lens and peer more deeply into standout categories to understand how the U.S. venture capital market managed to post its biggest year ever in terms of dollars invested, despite seeing deal volume slip for a second consecutive year.

This morning, we’re scraping data together to better understand.

This morning, we’re scraping data together to better understand.

First, we want to see how unicorns performed in Q4 2020. This column noted in late December that it felt like unicorn creation was rapid in the quarter; how did that hold up?

Then we’ll dig into PitchBook data concerning the fintech sector, a huge recipient of venture capital time, attention and money.

Fintech’s 2020 is a good perspective to view both the year and its wild final quarter. So this morning, as America itself resets, let’s take a moment to understand last year just a little bit better as we get into this new one.

One of the most curious things about the unicorn era is the rising bet it represents. I’ve written about this before so I will be brief: Nearly every quarter, the number of unicorns — private companies worth $1 billion or more — goes up.

The private market is able to create more unicorns than it has been historically able to exit them.

Some of these companies exit, sometimes in group fashion. But, quarter after quarter, the number of unexited unicorns rises. This means that the bet on expected future liquidity from venture capitalists and other private investors keeps ratcheting higher.

Powered by WPeMatico

On the heels of news that DoorDash is targeting an initial IPO valuation up to $27 billion, C3.ai also dropped a new S-1 filing detailing a first-draft guess of what the richly valued company might be worth after its debut.

C3.ai posted an initial IPO price range of $31 to $34 per share, with the company anticipating a sale of 15.5 million shares at that price. The enterprise-focused artificial intelligence company is also selling $100 million of stock at its IPO price to Spring Creek Capital, and another $50 million to Microsoft at the same terms. And there are 2.325 million shares reserved for its underwriters as well.

The total tally of shares that C3.ai will have outstanding after its IPO bloc is sold, Spring Creek and Microsoft buy in, and its underwriters take up their option, is 99,216,958. At the extremes of its initial IPO price range, the company would be worth between $3.08 billion and $3.37 billion using that share count.

Those numbers decline by around $70 and $80 million, respectively, if the underwriters do not purchase their option.

So is the IPO a win for the company at those prices? And is it a win for all C3.ai investors? Amazingly enough, it feels like the answers are yes and no. Let’s explore why.

If we just look at C3.ai’s revenue history in chunks, you can argue a growth story for the company; that it grew from $73.8 million in the the two quarters of 2019 ending July 31, to $81.8 million in revenue during the same portion of 2020. That’s growth of just under 11% on a year-over-year basis. Not great, but positive.

Powered by WPeMatico

The venture capital industry’s comeback from fear in Q1 and parts of Q2 to Q3 greed is worth understanding. To get our hands around what happened to private capital in 2020, we’ve taken looks into both the United States’ VC scene and the global picture this week.

Catching you up, there was lots of private money available for startups in the third quarter, with the money tilting toward later-stage rounds.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Late-stage rounds are bigger than early-stage rounds, so they take up more dollars individually. But Q3 2020 was a standout period for how high late-stage money stacked up compared to cash available to younger startups.

For example, according to CB Insights data, 54% of all venture capital money invested in the United States in the third quarter was part of rounds that were $100 million or more. That worked out to 88 rounds — a historical record — worth $19.8 billion.

The other 1,373 venture capital deals in the United States during Q3 had to split the remaining 46% of the money.

While the broader domestic and global venture capital scenes showed signs of life — dollars invested in Europe and Asia rose, American seed deal volume perked back up, that sort of thing — it’s the late-stage data that I can’t shake.

While the broader domestic and global venture capital scenes showed signs of life — dollars invested in Europe and Asia rose, American seed deal volume perked back up, that sort of thing — it’s the late-stage data that I can’t shake.

To my non-American friends, the data we have available is focused on the United States, so we’ll have to examine the late-stage dollar boom through a domestic lens. The general points should apply broadly, and we’ll always do our best to keep our perspective broad.

Powered by WPeMatico

The U.S. economy may be in a precarious state right now, with a presidential election looming on the horizon and the country still in the grips of the coronavirus pandemic. But partly thanks to lower interest rates, the housing market continues to rise, and today a startup that has built technology to help it run more efficiently is announcing a major growth round of funding.

Snapdocs, which is used by some 130,000 real estate professionals to digitally manage the mortgage process and other paperwork and stages related to buying a home, has raised $60 million in new equity funding on the heels of a few bullish months of business.

In August 2020 — a peak in home sales in the U.S., reaching their highest level in 14 years — the startup saw 170,000 home sales, totaling some $50 million in transactions, closed on its platform. This accounted for almost 15% of all deals done that month in the U.S. Snapdocs is now on track to close 1.5 million deals this year, double its 2019 volume.

On top of this, the startup’s platform is being used by more than 70% of settlement agents nationally, with customers including Bell Bank, LeaderOne Financial Corporation, Googain and Georgia United Credit Union among its customers.

The Series C is being led by YC Continuity (Snapdocs was part of Y Combinator’s Winter 2014 cohort), with existing investors Sequoia Capital, F-Prime Capital and Founders Fund, and new backers Lachy Groom (formerly of Stripe and now a prolific investor) and DocuSign, a strategic backer, also participating.

“Like us they are on a mission to defragment an ecosystem,” King said, referring to it as a “perfect complement” to Snapdocs’ own efforts.

Snapdocs is not talking about its valuation. Aaron King, the founder and CEO, said in an interview that he believes disclosing it is nothing more than “grandstanding” — which is interesting considering that the industry he focuses on, real estate, is all about public disclosures of valuation — but he noted that most of the $103 million that the startup has raised to date is still in the bank, which says something about the company’s overall financial health.

And for some further context, according to PitchBook data estimates, Snapdocs was valued at $200 million in its last round, in October 2019.

Snapdocs’ central premise is that buying a house requires not just a lot of paperwork but also a lot of different parties to be on the same page, so to speak, to set the wheels in motion and get a deal done. There is not just the mortgage (with its multiple parties) to settle; you also have real estate brokers and agents, the home sellers, inspectors and appraisers, the insurance company, the title company and more — some 15 parties in all.

The complexity of all of them working together in a quick and efficient way often means the process of buying and selling a house can be long and costly. And that’s before the pandemic — with the problems associated with social distancing and remote working — hit us.

Snapdocs’ solution has been to build one platform in the cloud that helps to manage the documents needed by all of these different parties, providing access to data and the ability to flag or approve things remotely, to speed the process along. It also has built a number of features, using AI technology and analytics, to also help identify what might be potential issues early on and get them fixed.

King is not your typical tech startup entrepreneur. He began working in mortgages as a notary when he was still in high school — he’s effectively been in the industry for 23 years, he said — and his earliest startup efforts were focused on one aspect of the complexities that he knew first-hand: he saw an opportunity to lean on technology to get notarized signatures sorted out in a legal, orderly and quicker way.

He then got deeper into identifying the possibilities of how tech could be used to improve the larger process, and that is how Snapdocs came into existence.

Given how big the real estate market is — it’s the largest asset class in the world, by many estimates — and how many other industries tech has “disrupted” over the years, it’s interesting that there have been so few attempting to solve it. One of the reasons, it seems, is that there hasn’t been enough of a crossover between tech experts and mortgage experts, and Snapdocs is a testament to the virtues of building a startup specifically around a hard problem that you happen to know really well.

“Most people have identified this as a tech problem, and a lot of the tech — such as e-signatures — has existed for 20 years, but the fragmentation of real estate is the issue,” he said. “We’re talking about a mass constellation of companies and workflow. But we’re obsessed about the workflow of all of these constituents.”

That’s a position that has helped Snapdocs build its standing with the industry, as well as with investors.

“I’ve known the Snapdocs team for many years and have always been amazed by their focus and execution toward bringing each stakeholder in the mortgage process online,” said Anu Hariharan, partner at YC Continuity, in a statement. “In 2013, Snapdocs began as a notary marketplace before expanding horizontally to service title companies and, more recently, lenders. By connecting the numerous parties involved in a mortgage on a single platform, Snapdocs is quickly becoming the “operating system” for mortgage closings. Mortgages, much like commerce, will shift online, bringing improved efficiency and a far better customer experience to the outdated home-closing process.” Hariharan has real estate experience herself and is joining the board with this round.

There have been a number of companies taking new, tech-based approaches to the market to find new and faster ways of doing things, and to open up new kinds of value in the market.

Opendoor, for example, has rethought the whole process of selling and buying houses, taking on a role as a middleman in the process both to take on a lot of the harder work of fixing up a home, and handling all of the difficult stages in the sales process: it’s a role that has recently seen the company catapult to a valuation of $4.8 billion by way of a SPAC-based public listing. An interesting idea, King said, but still only accounting for a small sliver of house sales.

Others, like Orchard, Reonomy and Zumper, have all also raised large rounds on the back of a lot of promise of the market continuing to grow and the opportunity to take part in that process through new approaches. It’s a sign that “safe as houses” still has a place in the market, even with all the other unknowns in play.

“Over the next five years the real estate industry will be completely digitized, so a lot of companies are trying to figure out what their place are, and how to provide value,” King said.

Powered by WPeMatico

So much for progress.

New data out this week from PitchBook indicates that the number of rounds raised by female-founded and co-founded companies fell year-over-year, with dollars invested in those rounds collapsing to 2017-era levels.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

It’s a disappointing quarter that comes after a few years in which female founders saw an increase in the amount of capital they were able to raise. In 2016, PitchBook data shows quarterly results for female founders totaling around 100 to 125 rounds, and between $300 and $400 million in value. By 2019, those figures rose to 150 to 200 rounds per quarter, worth between $700 million and $950 million.

To see Q3 2020 manage just 136 rounds worth just $434 million is a sharp disappointment.

To see Q3 2020 manage just 136 rounds worth just $434 million is a sharp disappointment.

The depressing results come not during a time of sharply lower aggregate venture capital results, notably. Recent data concerning Q3 2020 compiled by PwC indicates that the quarter was relatively rich. Certainly, overall deal volume in the United States is down slightly compared to year-ago periods, but female founders fared worse.

In short, a fear that well-known seed investor Charles Hudson discussed with TechCrunch during an Extra Crunch Live session back in April has come true. Let’s talk about it.

Cards on the table, I think it’s better when venture capital is more diversely distributed. Why? Because when there’s more general access to funds, we’ll see a more varied set of products built to attack a more diverse set of issues and problems. Even more, venture capital can be a pathway to financial success for founders and employees, so investing it in all sorts of folks instead of one particular demographic set can spread the wealth around more equitably.

Powered by WPeMatico

We can’t help but wonder what the future of work will look like in the wake of this pandemic. That’s the timely topic of today’s interactive webinar, COVID-19’s Impact on the Startup World.

The second of three in our free series of interactive webinars — exclusively for founders exhibiting in Digital Startup Alley at Disrupt 2020 — gets underway today, August 19 at 1 p.m. PDT/4 p.m. EDT. Exhibitors, be sure to register to attend.

Still on the fence about exhibiting at Disrupt? Hop off and get to it — buy a Disrupt Digital Startup Alley Package, tune in to the remaining webinars and then get ready to reap the benefits that come with introducing your startup to a global Disrupt audience. More on those in a minute.

You’ll hear from Nicola Corzine, executive director of the Nasdaq Entrepreneurship Center and Cameron Stanfill, a VC Analyst at PitchBook. Jon Shieber, a TechCrunch editor who covers venture capital and private equity investments will moderate the discussion. No one can predict the future, but these three bring years of experience to the table, and they’ll offer a data-informed perspective, tips and advice on how startups can adapt and what they need to think about both during and after COVID-19. It’s interactive, folks — got questions? Get answers.

Exhibiting in Digital Startup Alley is opportunity on steroids. Network with thousands of Disrupt attendees from around the globe. Expose your tech and talent to influencers of every stripe across the startup ecosystem — investors, R&D teams, advisors, potential customers. Make and nurture connections that can result in exciting partnerships.

CrunchMatch, our AI-powered networking platform bridges the physical distance of a virtual conference. It helps you quickly find and connect with the people who can help take your business to the next level. The platform’s up and running right now. Once you register for Disrupt, you can reach out to attendees and start expanding your network immediately.

Ready to exhibit? Great — be sure to mark your calendar for the final exclusive webinar. Tune in on August 26 for Fundraising and Hiring Best Practices with panelists Sarah Kunst of Cleo Capital and Brett Berson of First Round Capital.

We can’t predict the future, but there’s one thing we do know. It’s going to take every opportunity and every advantage to survive and thrive in these tumultuous times.

Buy a Disrupt Digital Startup Alley Package and tune in. It’s worth it.

Is your company interested in sponsoring or exhibiting at Disrupt 2020? Contact our sponsorship sales team by filling out this form.

Powered by WPeMatico