Pets.com

Auto Added by WPeMatico

Auto Added by WPeMatico

Hey everyone. Thank you for welcoming me into your inboxes yet again.

I’m in Berlin. where TechCrunch just pulled off another great Disrupt event — we’ve got a lot of great Europe-focused startup content on the site, so get to scrolling if your interest is piqued.

If you’re reading this on the TechCrunch site, you can get this in your inbox here, and follow my tweets here.

Just as Pets.com symbolized the ridiculousness that came to frame the tech industry preceding the Dot-com bubble burst at the start of the century, dog-walking startup Wag might symbolize that SoftBank’s earthquaking investment overexposure may extend far beyond a one-time WeWork mistake.

This week, The WSJ reported that SoftBank had tossed in the towel on Wag, selling off its massive “nearly 50% stake” in the startup. The report states that SoftBank sold its stake back to the startup at a valuation far below its previous $650 million value. SoftBank is walking away from its two board seats in the process.

Wag will be laying off “a significant amount of the remainder of its workforce,” according to the report.

High-ambition startups stumble all the time, but SoftBank’s money bag-swinging swagger has left a handful of startups with dollar signs in their eyes and the desire to grow at a pace that they never dreamed of. When LA-based Wag closed its $300 million raise from SoftBank at the beginning of 2018, plenty of people wondered why on earth a dog-walking startup needed that kind of money.

Shift forward to the end of 2019, and startups that have relied on connecting contractor labor with phone-wielding consumers haven’t proven to be as capable in shifting into profitability, with Wag seeming to be yet another example.

Needless to say, Pets.com and Wag really don’t hold much comparison when it comes to the broader impact. Pets.com was well-known largely because of its hilarious marketing overextension; Wag’s stumblings are far more impactful, especially as they relate to the reputation of its Japanese benefactor, which has significantly reshaped the venture capital market in Silicon Valley and around the world.

On to the rest of the week’s news.

Here are a few big news items from big companies, with green links to all the sweet, sweet added context:

How did the top tech companies screw up this week? This clearly needs its own section, in order of badness:

Image: Bryce Durbin/TechCrunch

Our premium subscription business had another great week of content. Our good friend Alex Wilhelm (who hired me as an intern four years ago!) is back at TechCrunch and has fired up a new series on Extra Crunch. Here’s his first post on the new hot club to join:

The $100M ARR Club

…Firms with valuations that their revenues can’t back are in similar straits. In the post-WeWork era, some unicorns are starting to look a bit long in the tooth. I suspect that the companies in most danger are those with slim revenues (compared to their valuations), poor revenue quality (compared to software startups) or both.

That said, there is a club of private companies that are really something, namely private ones that have managed to reach the $100 million annual recurring revenue (ARR) threshold. It’s not a large group, as startups that tend to cross the $100 million ARR mark are well on the path to going public…

Sign up for more newsletters, including my colleague Darrell Etherington’s new space-focused newsletter Max Q, here.

Powered by WPeMatico

The RealReal, an online retailer for authenticated luxury consignment, has authorized the sale of up to $70 million in new shares, per a Delaware stock authorization filing discovered by the Prime Unicorn Index. If the company raises the entire amount, it would reach a valuation of $1.06 billion, cementing its status as the newest e-commerce unicorn.

The filing doesn’t guarantee The RealReal will sell the full amount of authorized shares. The company declined to comment on its fundraising plans.

The RealReal is led by founder and chief executive officer Julie Wainwright (pictured), the former CEO of Pets.com, a company now synonymous with the dot-com bust. It has raised quite a bit of capital to date — a total of $288 million from venture capital and private equity backers, including Great Hill Partners, Sandbridge Capital, PWP Growth Equity, Industry Ventures, Greycroft Partners and Canaan Partners. Most recently, The RealReal closed a Series G financing of $115 million in July 2018 that valued the business at $745 million, per PitchBook.

The RealReal has recently expanded its brick-and-mortar footprint and added additional e-commerce fulfillment centers as demand increased for its supply of second-hand luxury items. Founded in 2011, the company operates eight luxury consignment offices, where customers can receive free valuations of their luxury items. The RealReal is headquartered in San Francisco.

In a conversation with TechCrunch in 2017, Wainwright confirmed the company’s intent to go public at some point. With this upcoming round, The RealReal would be well placed for a 2020 initial public offering.

“That’s the goal,” Wainwright said during the interview. “We really aren’t in the mood to sell the business, we’re in the mood to go public at some point in the future.”

The RealReal competes with fellow second-hand e-tailers ThredUp and Poshmark . The latter is gearing up for a fall IPO, according to The Wall Street Journal. The online marketplace has tapped Morgan Stanley and Goldman Sachs to lead its offering after closing in on $150 million in revenue in 2018. ThredUp, another major player in the fashion retail market, hasn’t raised capital since 2015, but did begin opening physical stores in 2017 as part of its greater effort to compete with fellow venture-backed second-hand e-tailers.

The RealReal would also be the latest in a series of high-profile female-founded companies to gain unicorn status. Glossier tripled its valuation to $1.2 billion with a $100 million round earlier this year, followed by Rent the Runway, which attracted a $125 million investment at a $1 billion valuation, to name a few.

Powered by WPeMatico

things")

Startup life is full of quick, lateral thinking. “Move fast and break things” is the mantra. However, with the rise of token sales – essentially vehicles for untested startups to raise millions in a few minutes – lots of stuff gets broken and little gets fixed.

Take BCT – the Blockchain Terminal – for example. This frothy project led by Bob Bonomo, a former hedge fund guy turned Blockchain guru, features some interesting breakages.

Yesterday at about 3pm Eastern Time the company’s FAQ – which has since been updated but is still hidden here – read something like this:

While this sort of techno greeking is fine if you’re sending mock-ups back and forth, the token sale had been running since April 1st, a fact that was baffling to me and another reporter. Was this an April Fool’s joke? No, because when I visited the sale’s Telegram room I found a group of happy buyers asking questions about their future tokens.

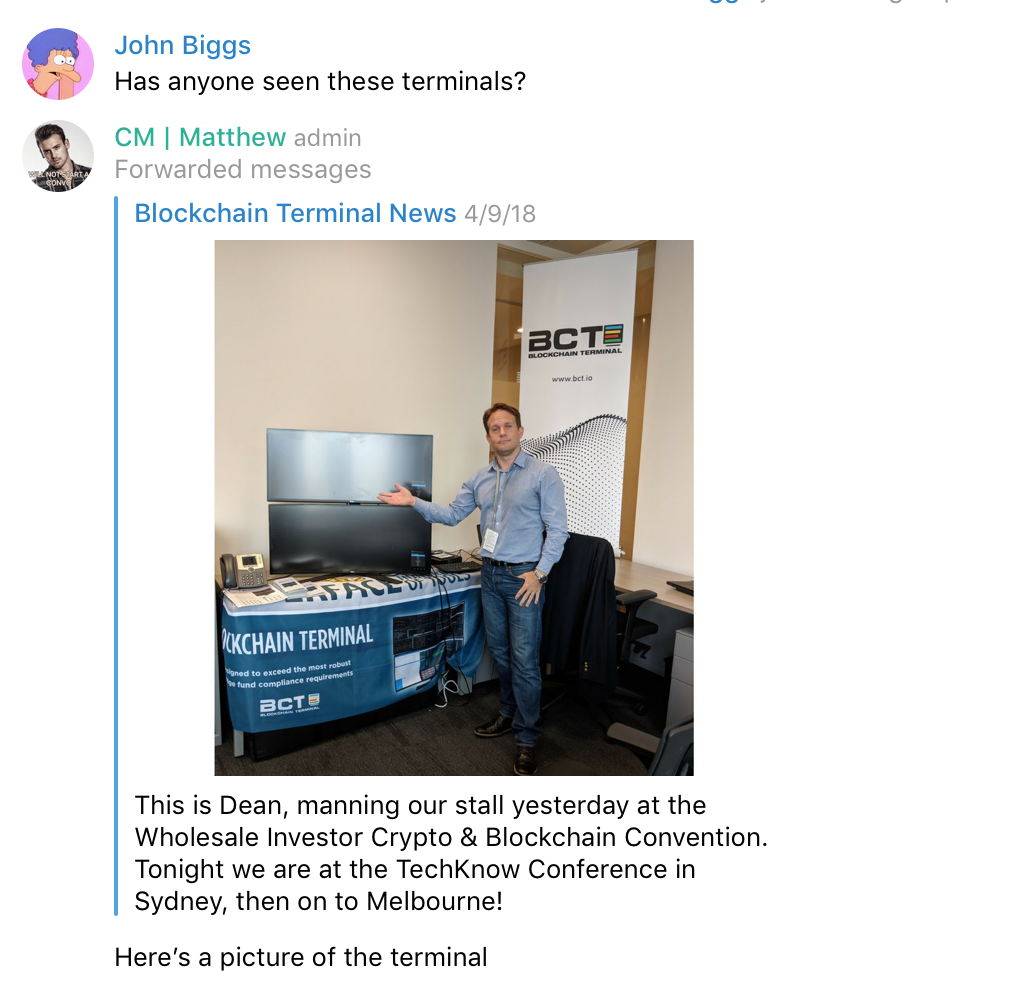

Ever the reporter, I asked if anyone had seen the terminals and a community manager sent me this:

Interesting… blank screens at a demo event. The other CM, quicker on the draw, sent this:

Fair enough. In fact, crypto needs a product like this to legitimize it with Wall Street. But clearly they were moving so fast that the wheels were falling off.

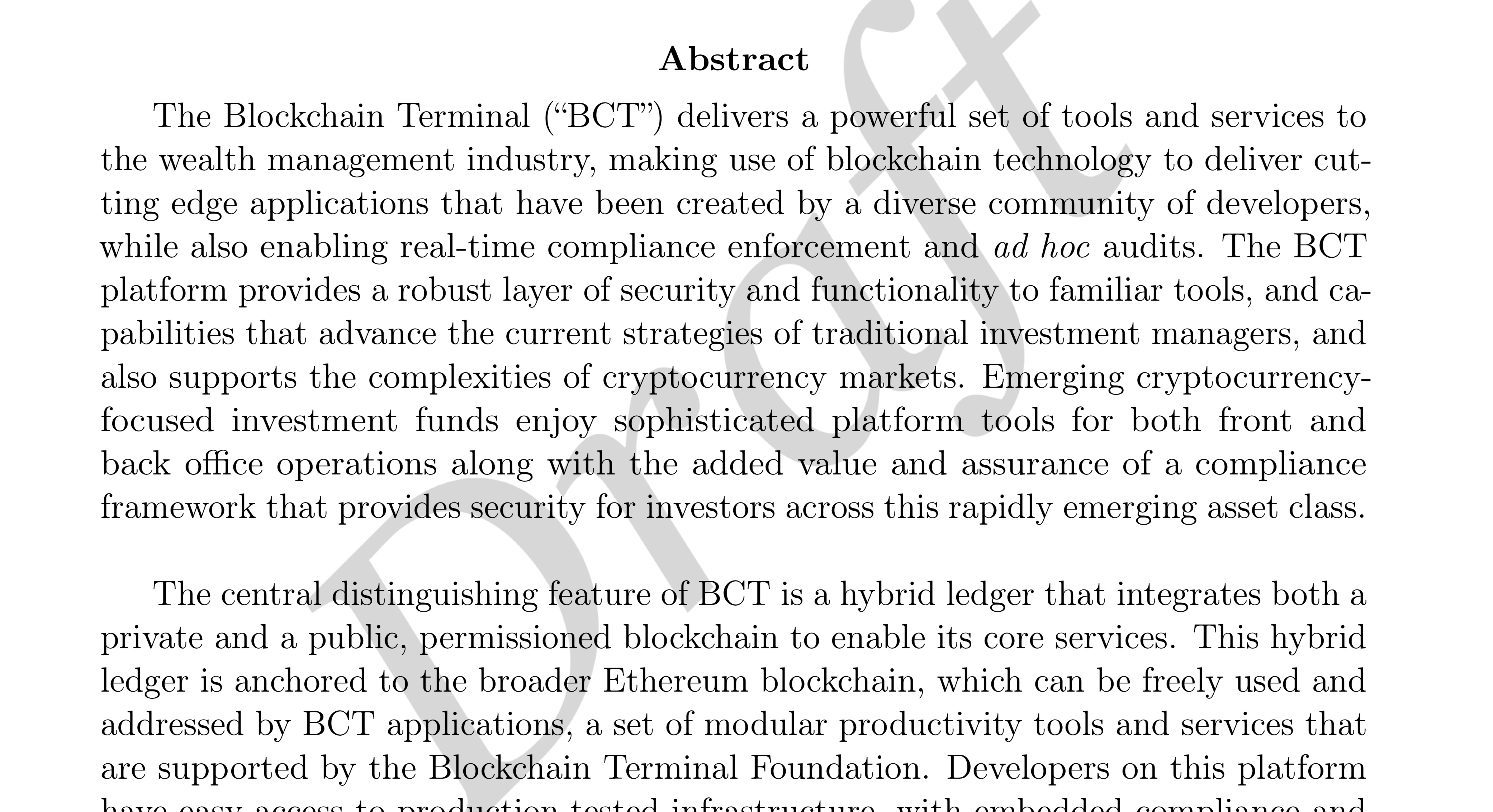

Finally I did the obvious thing: visit the white paper. There we find that the Terminal is being built in conjunction with FactSet, a venerable research company that has seen all the vicissitudes of financial data. In fact, the paper is a tour-de-force on par with the best of the white papers I’ve seen. But we also discover that the white paper is a draft.

In short, BCT wouldn’t pass the average human investor sniff test but is definitely well on the way to completing its token sale. This is a problem.

BCT is not alone. I’ve spoken to development houses working with founders who barely understand cryptocurrency let alone understand their own token sales. I’ve seen founders’ eyes light up like the Big Bad Wolf eyeing Porky Pig when they talk about all the capital they will unlock. And I spoke to a founder on stage who said he would be very careful with the $80 million they raised for a company designed to raise money for ICOs. Greed is clouding this market in ways that are at once dangerous and comical.

There is precedent for this. In the early days of the Internet and even the frothiest dot-com days you could see the avarice in the eyes of Pets.com and Cisco executives who knew that big money was just around the corner. And we can’t begrudge these founders their excitement. What founder wouldn’t want the sweet feeling of being fully funded for, we presume, the next decade?

I’ve been following token sales with great interest over the past few months for a few reasons. First, I understand the hype cycle. I’ve seen tactics used by token sellers used before by hardware sellers, most notably with flops like the Phantom gaming console and the Notion Ink Adam, and there is a stink that permeates projects that are, at best, half-baked.

I want token sales to thrive as a method to raise capital. I want small startups to be able to turn on a spigot previously available to the well-connected and well-heeled. But the exact opposite seems true. Bankers are moving into a technology space that they little understand while carpetbaggers – lawyers, PR folks, advisors – are working hard to extract cash out of these windfalls. In the end the token sale industry should formalize itself and become as boring as the VC industry. I just hope it survives long enough to get there.

Powered by WPeMatico