Personnel

Auto Added by WPeMatico

Auto Added by WPeMatico

Earlier this year, Instacart‘s chief financial officer Sagar Sanghvi departed from the on-demand grocery delivery company after nearly six years. And now he’s returning to his investing roots. Specifically, Sanghvi has joined Accel as a partner focused on global growth-stage consumer and enterprise investments.

Prior to becoming CFO of Instacart, Sanghvi served as the company’s vice president of finance and strategy. Interestingly, when he became CFO of Instacart in 2019, he was succeeding Ravi Gupta, who left the company to join Sequoia Capital as a partner on its growth team.

Sanghvi and Gupta worked together as investors at KKR (after Sanghvi had worked as an analyst for Goldman Sachs), so it is notable they are following similar career paths of first working in finance and then becoming operators before transitioning into VC roles. Both joined Instacart in 2015. And Gupta is the one who introduced Sanghvi to Accel’s Miles Clements years ago.

When Sanghvi joined Instacart, it had approximately 300 employees. By the time he’d left earlier this year, it had more than 1,500.

“I’ve been through quite the roller coaster of ups and downs along the way. It was the classic Silicon Valley journey. During my time there, a few crazy things happened,” he told TechCrunch. “ Amazon bought Whole Foods. We experienced the COVID pandemic and lockdowns, which led to an amazing wave of demand. It was an interesting time to be navigating the company.”

And while Sanghvi says he would definitely rather see a business be smaller “than have COVID happen to the world,” it was a time where he learned a lot in helping grow the company.

One of the things Sanghvi worked on during his time at Instacart was a $200 million venture round in October 2020 that valued the company at $17.7 billion. (Since then it raised another $265 million at a $39 billion valuation.) In fact, during his tenure, the company raised more than $2 billion.

But now, Sanghvi will be the one investing in other companies’ rounds — out of Accel’s Palo Alto office.

While his Instacart experience is clearly relevant to the consumer space, Sanghvi said he’ll be working with not just consumer-focused startups, but also a lot of enterprise solutions.

“One of the things that drew me to Miles and the team was the experience and success Accel as a firm has had investing in all different types of companies within the technology sector and so I’m hoping to diversify my experience,” he told TechCrunch.

Clements praised what he described as Sanghvi’s “humility and versatility.”

“He’s done everything from raising $2 billion of capital to being in the minutiae of evaluating back office automation software. He has led a company that is on its way to being an iconic consumer brand, but he’s also been a media investor at KKR,” Clements said. “He guided Instacart through some massive recent fundraises but only because he has also helped navigate through some previous existential challenges. So he brings a lot of natural empathy to founders and entrepreneurs.”

For his part, Sanghvi is eager to start investing as part of the Accel team.

When deciding to move to the venture world, he said, he was looking for a “very well-known brand” that invested across at all stages. He found that in Accel, he said.

“One of the things that was important to me was to find the type of people who really care about the success of companies, and in every person I met at Accel, I could see they took that responsibility very seriously,” Sanghvi told TechCrunch.

He officially started in his new role last week, so he’s actively scoping out investments as I type.

Powered by WPeMatico

LinkedIn normalized the idea of making people’s resume’s visible to anyone who wanted to look at them, and today a startup that’s hoping to do the same for companies and how they are organized and run is announcing some funding. The Org, which wants to build a global, publicly viewable database of company organizational charts — and then utilize that database as a platform to power a host of other services — has raised $20 million, money that it will be using to hire more people, add on more org charts and launch new features, with a recruitment toolkit being first on the list.

The Series B is led by Tiger Global, with previous backers Sequoia, Founders Fund and Balderton Capital also participating alongside new investors Thursday Ventures, Lars Fjeldsoe-Nielsen (a former Balderton partner), Neeraj Arora (formative early WhatsApp exec), investor Gavin Baker, and more. From what we understand, the investment values The Org at $100 million.

Founders Fund led the company’s last round, a Series A in February 2020, and the whole world of work has really changed a lot in the interim because of COVID-19: companies have become more distributed (a result of offices shutting down); the make-up of businesses has changed because of new demands; and many of us have had our sense of connection to our jobs tested in ways that we never thought it would.

All of that has had a massive impact on The Org, and has played into its theory of why org charts are useful, and most useful as a tool for transparency.

“In many ways the pandemic has forced us to reevaluate the norms of how work happens. One of the misconceptions was the idea that you are only working when you are at the office, 9-5. But the future of work is a hybrid set up but you get a lot of issues that arise out of that, communication being one of them. Now it’s much more important to create alignment, a sense of connection, and really feeling a sense of belonging in your company,” Christian Wylonis, the CEO who co-founded the company with Andreas Jarbøl, said in an interview (the two are pictured below). “We think that a lot of these issues are rooted around transparency and that is what The Org is about. Who is doing what, and why?”

Image Credits: The Org

He said that when the coronavirus suddenly ramped up into a global issue — and it really was sudden; our conversation in February 2020 had nothing whatsoever to do with it, yet it was only weeks later that everything shut down — it wasn’t obvious that The Org would have a place in the so-called “new normal.”

“We were as nervous as anyone else, but the idea of what work would look like and how we enable people around that has gotten a lot higher on the agenda,” he said. “The appetite for new tools has improved dramatically, and we can see that in our traffic.”

The Org has indeed seen some very impressive growth. The company now hosts some 130,000 public org charts, sees 30,000 daily visitors and has more than 120,000 registered users. And more casual usage has boomed, too. Wylonis notes that The Org now has close to 1 million visitors each month versus just 100,000 in February 2020, when it only had 16,000 org charts on its platform.

Monetization is coming slowly for the startup. Building, editing and officially “claiming” a profile on the platform are all still free, but in the meantime The Org is working on its platform play and using the database that it is building to power other services. Job hunting is the first area that it will tackle.

Posting jobs will be free, and it’s integrating with Greenhouse to feed information into its system, but recruiters and HR pros are given an option to manage the sourcing and screening process through The Org, a kind of executive recruitment tool, which will come at a charge. Down the line there are plans for more communications and HR tools, Wylonis said. Some of this will be built by way of integrations and APIs with other services, and some tools — such as communications features — will be built in-house, from the ground up.

When I covered the company’s last round, I’d noted that there were some obvious hurdles for The Org, as well as potentially others like Charthop or Visier building business models on providing more transparency and information around hiring and how companies are run.

Sometimes the companies in question don’t actually want to have more transparency. And any database that is based around self-reporting runs the risk of being only as good as the data that is put into it — meaning it may be incomplete, or simply wrong, or just presented to the contributors’ best advantage, not that of the company itself. (This is one of the issues with LinkedIn, too: Even with people’s resumes being public, it’s still very easy to lie about what you actually do, or have done.)

So far, the theory is that some of this will be resolved by way of who The Org is targeting and how it is growing. Today the company’s “sweet spot” is early-stage startups with about 50-200 employees, and generally org charts are created for these businesses in part by The Org itself, and then largely by way of wiki-style user-edited content (anyone with a company email can get involved).

The plan is both to continue working with those smaller startups as they scale up, but also target bigger and bigger businesses. These, however, can be trickier to snag — not least because they will stretch into the realm of public companies, but also because their charts will be more complicated to map and manage consistently. For that reason, The Org is also adding in more features around how companies can “claim” their profiles, including managing permissions for who can edit profiles.

This might mean more managed public profiles, but the idea is that it will be a start, and once more companies post more information, we will see more transparency overall, not unlike how LinkedIn evolved, Wylonis said.

The LinkedIn analogy is interesting for another reason. It seems a no-brainer that LinkedIn, which is at its heart a massive database of information about the world of professional work, and the people and companies involved in it, would have wanted to build its own version of org charts at some point. And yet it hasn’t.

Some of this might be down to how LinkedIn has fundamentally built and organised its own database and knowledge graph, but Wylonis believes it might also be a conceptual difference.

“We think that this might be the fundamental difference between us and them,” Wylonis said of LinkedIn. “They are a database of resumes. ‘I can say whatever I want.’ But for us, the atomic unit is the organization itself. That is an important distinction because it’s a one to many relationship. It can’t be only me editing my profile. And allows us to build structures.”

He added that this was one of the reasons that Keith Rabois — who was an early exec at LinkedIn — became an early investor in The Org: “LinkedIn has been looking at this forever, but they haven’t been able to build it, and so that is how we caught his attention.”

Powered by WPeMatico

The wider world of employment has seen a huge shift in the wake of the COVID-19 pandemic. Looking for a job, finding someone to fill a role or simply developing professionally are just not the same as they used to be for many of us. So it’s no surprise to see companies that have built business models catering to these areas changing, too: today, LinkedIn, Microsoft’s social networking platform for the working world, announced a wave of news aimed at moving ahead with the times.

It’s launching a new Learning Hub aimed at organizations to provide professional development and other training to employees. And it’s making 40 courses free of charge to LinkedIn members specifically to address some of the changes afoot, such as how to adapt to hybrid working, how to be a better manager in the new normal, and how to return to the office, and run facilities when they are spread beyond a building to also include people’s private homes. Lastly, it’s also starting to tweak details that people can use to list and search for job openings to account for these kinds of working conditions, and more.

The Learning Hub was first previewed back in April of this year and has been running in a limited beta. Today, as part of a bigger event hosted by Microsoft CEO Satya Nadella and LinkedIn CEO Ryan Roslansky where they are discussing new trends in the world of work, the Hub is being rolled out more widely.

For some context, LinkedIn has been long on education for years, with acquisitions like the remote learning platform Lynda back in 2015 bolstering its own education strategy and position as a go-to platform for professional development; partnerships to bring in significant amounts of third-party content (for example, when it added some 13,000 courses via third parties in 2018); and efforts to tie together the concept of skills development with professional profiles, running research and building interactive tools for its users.

The free courses that are being launched today (and will remain free until October 9) are a timely set of videos to help companies as some of them start to make (or think about) the transitions from remote to in-office environments, but the bigger product launch, The Learning Hub, is not exactly an altruistic endeavor in that longer journey. It is being sold as a premium service for businesses — existing LinkedIn Learning Pro users will be able to use it for free until July 2022, potentially longer, it said. In addition to being a salient business, it is also connected to the company’s bigger efforts to bring in more business-focused services, and more engagement from HR departments, to bolster one of its other main revenue drivers: recruitment.

As a learning experience platform (often described as LXPs), LinkedIn’s relaunch of its own learning hub will bring it into closer competition with the likes of 360Learning, Coursera for Business, Workday, Cornerstone, and the many other platforms used by organizations to manage their own in-house and third-party professional training content. In addition to this, LinkedIn says it will be using its own data on employment trends, plus AI, to personalize content for organizations and users. The fact, however, that it’s also a platform where those HR teams can also list jobs and source candidates makes it a significantly stickier experience, and one that might feel more cohesive at a time when so much else might be more fragmented.

The new fields that LinkedIn is bringing into its recruitment service are also notable in that regard. It will now let recruiters indicate whether a job is remote, hybrid or onsite; and soon those looking for jobs will also be able to indicate which of these it’s looking for in a new role. Companies will also be able to start indicating more details on their own company status as it relates to things like vaccination requirements, and to let the world (employees, partners, customers, interested others) know whether your physical offices are open for business or not.

These new fields may sound a little trivial, or at least very specifically related to concerns and circumstances that we live with today, but I think they are more notable than this. They speak to what LinkedIn sees (and what many of us feel) are strong priorities in how we view jobs today. That opens the door to how and if LinkedIn might consider other kinds of details in company and personal profiles, as well as details that could be used in recruitment. This is something the company has also been working on for a little while already: in June it started to give users the option of adding pronouns to their profiles. All of this is pretty important, considering that there are a lot of smaller companies and calls for someone to knock LinkedIn off its pedestal. As LinkedIn dabbles with new formats and sunsets others, it’s all signals that it’s attempting to be more adaptable to counteract that.

Powered by WPeMatico

Factorial, a startup out of Barcelona that has built a platform that lets SMBs run human resources functions with the same kind of tools that typically are used by much bigger companies, is today announcing some funding to bulk up its own position: the company has raised $80 million, funding that it will be using to expand its operations geographically — specifically deeper into Latin American markets — and to continue to augment its product with more features.

CEO Jordi Romero, who co-founded the startup with Pau Ramon and Bernat Farrero — said in an interview that Factorial has seen a huge boom of growth in the last 18 months and counts more than anything 75,000 customers across 65 countries, with the average size of each customer in the range of 100 employees, although they can be significantly (single-digit) smaller or potentially up to 1,000 (the “M” of SMB, or SME as it’s often called in Europe).

“We have a generous definition of SME,” Romero said of how the company first started with a target of 10-15 employees but is now working in the size bracket that it is. “But that is the limit. This is the segment that needs the most help. We see other competitors of ours are trying to move into SME and they are screwing up their product by making it too complex. SMEs want solutions that have as much data as possible in one single place. That is unique to the SME.” Customers can include smaller franchises of much larger organizations, too: KFC, Booking.com, and Whisbi are among those that fall into this category for Factorial.

Factorial offers a one-stop shop to manage hiring, onboarding, payroll management, time off, performance management, internal communications and more. Other services such as the actual process of payroll or sourcing candidates, it partners and integrates closely with more localized third parties.

The Series B is being led by Tiger Global, and past investors CRV, Creandum, Point Nine and K Fund also participating, at a valuation we understand from sources close to the deal to be around $530 million post-money. Factorial has raised $100 million to date, including a $16 million Series A round in early 2020, just ahead of the Covid-19 pandemic really taking hold of the world.

That timing turned out to be significant: Factorial, as you might expect of an HR startup, was shaped by Covid-19 in a pretty powerful way.

The pandemic, as we have seen, massively changed how — and where — many of us work. In the world of desk jobs, offices largely disappeared overnight, with people shifting to working at home in compliance with shelter-in-place orders to curb the spread of the virus, and then in many cases staying there even after those were lifted as companies grappled both with balancing the best (and least infectious) way forward and their own employees’ demands for safety and productivity. Front-line workers, meanwhile, faced a completely new set of challenges in doing their jobs, whether it was to minimize exposure to the coronavirus, or dealing with giant volumes of demand for their services. Across both, organizations were facing economics-based contractions, furloughs, and in other cases, hiring pushes, despite being office-less to carry all that out.

All of this had an impact on HR. People who needed to manage others, and those working for organizations, suddenly needed — and were willing to pay for — new kinds of tools to carry out their roles.

But it wasn’t always like this. In the early days, Romero said the company had to quickly adjust to what the market was doing.

“We target HR leaders and they are currently very distracted with furloughs and layoffs right now, so we turned around and focused on how we could provide the best value to them,” Romero said to me during the Series A back in early 2020. Then, Factorial made its product free to use and found new interest from businesses that had never used cloud-based services before but needed to get something quickly up and running to use while working from home (and that cloud migration turned out to be a much bigger trend played out across a number of sectors). Those turning to Factorial had previously kept all their records in local files or at best a “Dropbox folder, but nothing else,” Romero said.

It also provided tools specifically to address the most pressing needs HR people had at the time, such as guidance on how to implement furloughs and layoffs, best practices for communication policies and more. “We had to get creative,” Romero said.

But it wasn’t all simple. “We did suffer at the beginning,” Romero now says. “People were doing furloughs and [frankly] less attention was being paid to software purchasing. People were just surviving. Then gradually, people realized they needed to improve their systems in the cloud, to manage remote people better, and so on.” So after a couple of very slow months, things started to take off, he said.

Factorial’s rise is part of a much, longer-term bigger trend in which the enterprise technology world has at long last started to turn its attention to how to take the tools that originally were built for larger organizations, and right size them for smaller customers.

The metrics are completely different: large enterprises are harder to win as customers, but represent a giant payoff when they do sign up; smaller enterprises represent genuine scale since there are so many of them globally — 400 million, accounting for 95% of all firms worldwide. But so are the product demands, as Romero pointed out previously: SMBs also want powerful tools, but they need to work in a more efficient, and out-of-the-box way.

Factorial is not the only HR startup that has been honing in on this, of course. Among the wider field are PeopleHR, Workday, Infor, ADP, Zenefits, Gusto, IBM, Oracle, SAP and Rippling; and a very close competitor out of Europe, Germany’s Personio, raised $125 million on a $1.7 billion valuation earlier this year, speaking not just to the opportunity but the success it is seeing in it.

But the major fragmentation in the market, the fact that there are so many potential customers, and Factorial’s own rapid traction are three reasons why investors approached the startup, which was not proactively seeking funding when it decided to go ahead with this Series B.

“The HR software market opportunity is very large in Europe, and Factorial is incredibly well positioned to capitalize on it,” said John Curtius, Partner at Tiger Global, in a statement. “Our diligence found a product that delighted customers and a world-class team well-positioned to achieve Factorial’s potential.”

“It is now clear that labor markets around the world have shifted over the past 18 months,” added Reid Christian, general partner at CRV, which led its previous round, which had been CRV’s first investment in Spain. “This has strained employers who need to manage their HR processes and properly serve their employees. Factorial was always architected to support employers across geographies with their HR and payroll needs, and this has only accelerated the demand for their platform. We are excited to continue to support the company through this funding round and the next phase of growth for the business.”

Notably, Romero told me that the fundraising process really evolved between the two rounds, with the first needing him flying around the world to meet people, and the second happening over video links, while he was recovering himself from Covid-19. Given that it was not too long ago that the most ambitious startups in Europe were encouraged to relocate to the U.S. if they wanted to succeed, it seems that it’s not just the world of HR that is rapidly shifting in line with new global conditions.

Powered by WPeMatico

You’ve heard the phrase “leading by example,” but what about “leading with values”?

I’ve always led by example by using my values as my guide. Still, it wasn’t until I founded my first company that I fully understood the importance of embedding those values into the company, too.

Integrity, individuals, impact and innovation are the “4 I values” that drive my decisions and the actions of those at my company each day. These are not just words on a wall at our HQ or on a mousepad for our remote crew, but values that everyone in the company lives and breathes. Over the last two years, these four values became even more important and continued to guide me, my family and the leaders at our company.

As organizations map out their “return to the workplace” (NOT “return to work,” because we never stopped working) plans, we should not simply go back to how things were before. Instead, let’s all take a moment to redesign something that sets everyone up for success, with values as the compass. I think you’ll find this approach helps people not only survive, but thrive in the workplace.

Leading with values is, in my experience, the best leadership position to take, and there are three ways to accomplish this goal.

The tone of the company’s culture comes from the top. The culture you envision for your company will only come about if your employees believe in the practices that you are asking them to implement.

At some point in your career — probably right out of school, a few years in or somewhere in the middle — you experienced a company where treating lower-level employees with less respect is just “a part of the job.” Companies with this type of “paying your dues” mentality tend to work these lower-level employees like grunts until they burn out and leave.

Or they eventually crawl their way up into management-level positions, and the cycle perpetuates itself as they deride the newer crop of employees, eroding any semblance of a healthy culture.

This is not the way.

As a leader, if you want your work environment to indicate inclusivity, support, collaboration and have the essence of a team mentality, you must set the precedent right away. This means stripping away the hierarchy that accompanies work titles and making it clear that your company values contribution based on merit, regardless of position. You are one team, united in your purpose to deliver on your mission, based on your values. This level setting ensures that everyone has skin in the game, and no one has the leeway to treat people poorly.

Early on in my career, I began sharing an office when I could. Those office spaces were purposely not what anyone would consider cool or nice “digs” — not the furniture and certainly not the view. Even as CEO now, I’ve had someone on the team describe my current office as a closet. But it gets the job done.

Simple signals like this send a powerful message, and the signal must remain consistent. Don’t take a limo; rent a cheap car. Don’t fly first class; fly coach. These may seem like minor details, but one of the biggest pitfalls any CEO can encounter is falling victim to an ivory tower mindset — when you become so out of touch with the people you manage, your employees start to notice.

Make a cognizant effort to know your people. Implement a “management by walking around” strategy. Don’t sit in your office all day; get out on the floor among your people. Drop by their desks and ask them how their day is going. Eat lunch in the break room. Put in the effort to attend new hire onboarding.

Not physically back in the office? Drop into Slack channels and Zoom meetings. I once “Zoom bombed” a baby shower for one of our crew members just to hear all the well wishes, and it made my day and theirs. Overall, just be present and humanize your workspace. It pays off in spades.

The tone of the company’s culture comes from the top. The culture you envision for your company will only come about if your employees believe in the practices that you are asking them to implement. More importantly, you will not grow a solid culture if you don’t give these initiatives and practices 100% of your own effort.

For example, one new initiative we rolled out last year is a campaign we call “Free2Focus.” Twice a week, the SailPoint crew is asked to avoid booking meetings for a couple of hours during Free2Focus time. Not only does this address Zoom fatigue, it also gives our crew the chance to catch their breath whichever way suits them best — whether that’s taking a walk, helping with their children’s schooling or just turning off the camera for a bit.

If I want my team to show themselves some grace during the week, I’ve found that I need to apply the same practice. This means not setting up meetings during Free2Focus, not sending emails all hours of the day and night and not judging people for taking breaks when they need them. I trust my team to get the job done largely on their own time and own their own terms. I promise, your employees’ performance will be better because of it.

Being a CEO is more than building on a vision, a product or an idea. It’s about leading your people with values to accomplish mutual goals in a way that doesn’t zap them of their morale or dignity. It’s easy to get caught up in all the things that come with a job, but if you don’t put in the effort to immerse yourself and your values into the entire company, you’ll end up too big for your own good — and certainly too big for your company’s good.

It won’t happen overnight, but remember, the smallest things are often the ones that have the biggest impact. If you’re the leader, lead by example. It’s the only way to build teams that stand the test of time.

Powered by WPeMatico

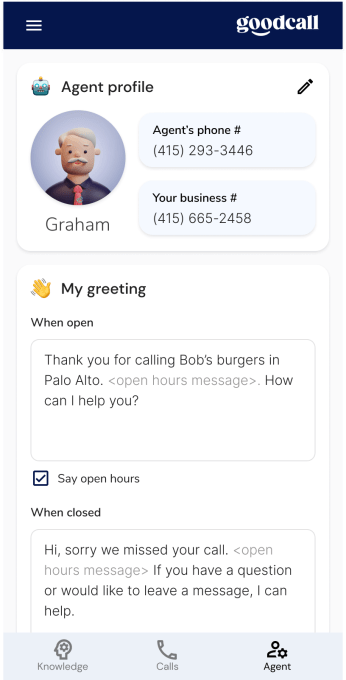

Even without staffing shortages, local merchants have difficulty answering calls while all hands are busy, and Goodcall wants to alleviate some of that burden from America’s 30 million small businesses.

Goodcall’s free cloud-based conversational platform leverages artificial intelligence to manage incoming phone calls and boost customer service for businesses of all sizes. Former Google executive Bob Summers left Google back in January, where he was working on Area 120 — an internal incubator program for experimental projects — to start Goodcall after recognizing the call problem, noting that in fact 60% of the calls that come into merchants go unanswered.

“It’s frustrating for you and for the person calling,” Summers told TechCrunch. “Every missed call is a lost opportunity.”

Goodcall announced its launch Wednesday with $4 million in seed funding led by strategic investors Neo, Foothill Ventures, Merus Capital, Xoogler Ventures, Verissimo Ventures and VSC Ventures, as well as angel investors including Harry Hurst, founder and co-CEO of Pipe.com, and Zillow co-founder Spencer Rascoff.

Goodcall mobile agent. Image Credits: Goodcall

Restaurants, shops and merchants can set up on Goodcall in a matter of minutes and even establish a local phone number to free up an owner’s mobile number from becoming the business’ main line. The service is initially deployed in English and the company has plans to operate in Spanish, French and Hindi by 2022.

Merchants can choose from six different assistant voices and monitor the call logs and what the calls were about. Goodcall can also capture consumer sentiment, Summers said.

The company offers three options, including its freemium service for solopreneurs and business owners, which includes up to 500 minutes per month of Goodcall services for a single phone line. Up to five additional locations and five staff members costs $19 per month for the Pro level, or the Premium level provides unlimited locations and staff for $49 per month.

During the company’s beta period, Goodcall was processing several thousands of calls per month. The new funding will be used to continue to offer the free service, hire engineers and continue product development.

In addition to the funding round, Goodcall is unveiling a partnership with Yelp to tap into its database of local businesses so that those owners and managers can easily deploy Goodcall. Yelp data shows that more than 500,000 businesses opened during the pandemic. The company pulls in from Yelp a merchant’s open hours, location, if they offer Wi-Fi and even their COVID policy.

“We are partnering with Yelp, which has the best data on small businesses, and other large distribution channels to get our product to market,” Summers said. “We are bringing technology into an industry that hasn’t innovated since the 1980s and democratizing conversational AI for small businesses that are the main driver of job creation, and we want to help them grow.”

Powered by WPeMatico

If you haven’t noticed yet, the hiring market is a hot one — and getting more complicated as enterprise talent acquisition leaders face technology gaps while assessing candidates. This leads to difficulty in determining compensation.

Enter Compa. The offer management platform provides “deal desk” software for recruiters to more easily manage their compensation strategies to create and communicate offers that are easy to understand and are unbiased.

Charlie Franklin, co-founder and CEO of Compa, told TechCrunch it was frustrating to lose a candidate at the compensation stage, so the company created its software to reduce the challenge of relying on crowdsourcing data or surveys to compare pay.

“Recruiters often lack the data and tools to figure out how much to pay people and communicate that effectively,” Franklin told TechCrunch. “We see talent acquisitions teams like a sales team. If you think of it from that perspective, they need to close a candidate, but to ask the recruiter to operate off of a spreadsheet slows that process down.”

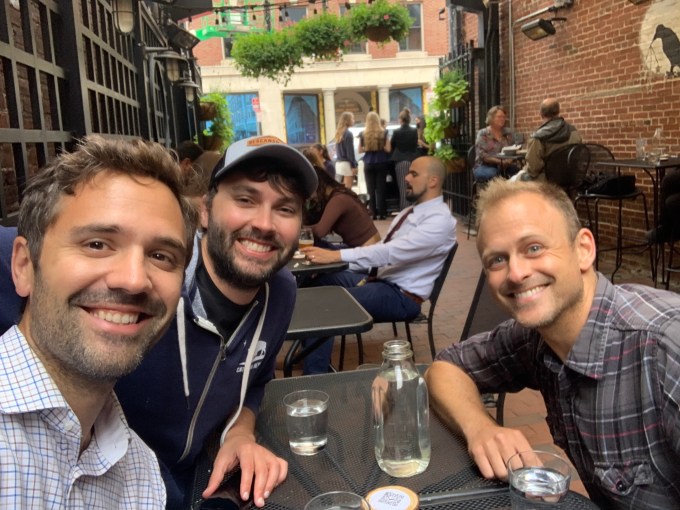

Compa co-founders, from left, Charlie Franklin, Joe Malandruccolo and Taylor Cone. Image Credits: Compa

With Compa, recruiters can input pay expectations and compare recent offers and collaborate with other team members and hiring managers to reach pay consensus quicker. The software automates all of the market intelligence in real time and provides insights about compensation across similar industries and organizations.

The company, based in both California and Massachusetts, emerged from stealth Thursday with $3.9 million in seed funding led by Base10 Partners. Participation in the round also came from Crosscut Ventures and Acadian Ventures, as well as a group of strategic angel investors including 2.12 Angels, Oyster HR CEO Tony Jamous and Scout RFP co-founders Stan Garber and Alex Yakubovich.

Jamison Hill, partner at Base10 Partners, said via email his firm was doing research in the ESG “megatrend,” particularly looking for startups focused on compensation management, when it came across Compa.

He was attracted to the founders’ “clarity and conviction” on the company’s vision, their understanding of the pay gap in the market, how Compa’s solution would “create a new wave of smarter, more-data driven recruiting teams” and how it was enabling employers to use compensation and a positive offer management approach to differentiate itself from competitors.

“They deeply understand the nuances that come with enterprise-level HR teams and bring that expertise to every aspect of Compa’s product offering, which is why we believe Compa can emerge as a leader in this trend and chose to partner with this very special team,” Hill added.

Franklin, who previously led human resources M&A at Workday, founded Compa last year with Joe Malandruccolo, who was on the engineering side at Facebook and Oculus, and Taylor Cone, who has done innovation consulting for organizations like Stanford University.

The company was bootstrapped prior to going after the seed round and will use the capital to expand the team and create additional products that fit into its mission of “making compensation fair and competitive for everyone,” Franklin said.

Going forward, he adds that job offers and compensation need to catch up to how quickly the world is changing. As more people work remotely and companies want to attract a diverse workforce, compensation will be an important factor.

“This is a long-term trend we are seeing in HR — compensation becoming more transparent — not just a spreadsheet shared internally, but a transition from secretive to open and accountable, Franklin said. “Technology is catching up to that, and we have the ability to produce outcomes that drive differences in pay.”

Powered by WPeMatico

Nearly three in 10 employees (29%) would quit their job if they were told they were no longer allowed to work remotely, according to a recent survey. In addition, a recent Harvard Business Study found that “companies that let their workers decide where and when to do their jobs — whether in another city or in the middle of the night — increase employee productivity, reduce turnover and lower organizational costs.”

Over the past 18 months, while instituting a remote work model, our turnover rate at Insightly was the lowest in company history and an internal survey found happiness levels to be twice as high from the previous year. This in the midst of a major pandemic, social movement, forest fires and a disruptive election — all happening at the same time.

As long as your employees are available when your customers are in need and goals are consistently met, 9 to 5 no longer needs to be a thing.

On a larger, global scale, employers from companies around the world are coming to the same realization: You don’t need an office to be productive and employees are happier working from home.

The next logical step is, at the same time, a majorly disruptive one and a 180-degree shift toward how companies have operated for over 100 years — the transition from in-person headquarters to a remote, work-from-anywhere model. In line with this shift, we’ve foregone our 40,000-square-foot Soma office space and employees are able to work from anywhere in the United States while keeping the same salary.

There will no doubt be challenges, and there already have been. But with these challenges also arises immense opportunity. Here are a few battle-tested tips on how to maintain productivity while delivering flexibility with this new work model:

Let employees choose where they live. Allowing this option will better their lives and make for happy, engaged employees. Overhead costs, especially in large cities such as San Francisco, are the largest operating expense for most companies. Take this large sum of money and invest in employee happiness. You don’t need thousands of square feet in office space to be successful.

That massive overhead cost you just got rid of? Use this toward more meaningful employee experiences that will enhance their lives.

Powered by WPeMatico

Everyone at an organization should own growth, right? Turns out when everyone owns something, no one does. As a result, growth teams can cause an enormous amount of friction in an organization when introduced.

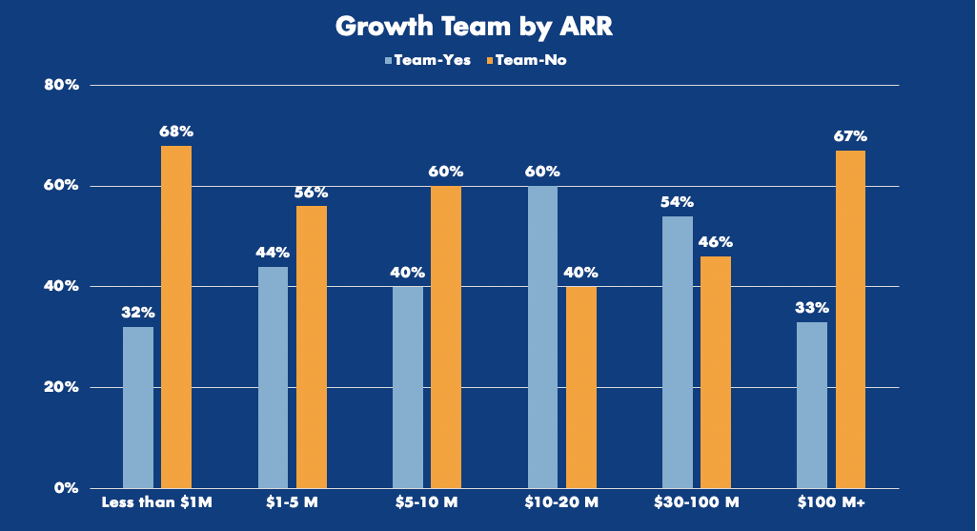

Growth teams are twice as likely to appear among businesses growing their ARR by 100% or more annually. What’s more, they also seem to be more common after product-market fit has been achieved — usually after a company has reached about $5 million to $10 million in revenue.

Image Credits: OpenView Partners

I’m not here to sell you on why you need a growth team, but I will point out that product-led businesses with a growth team see dramatic results — double the median free-to-paid conversion rate.

Image Credits: OpenView Partners

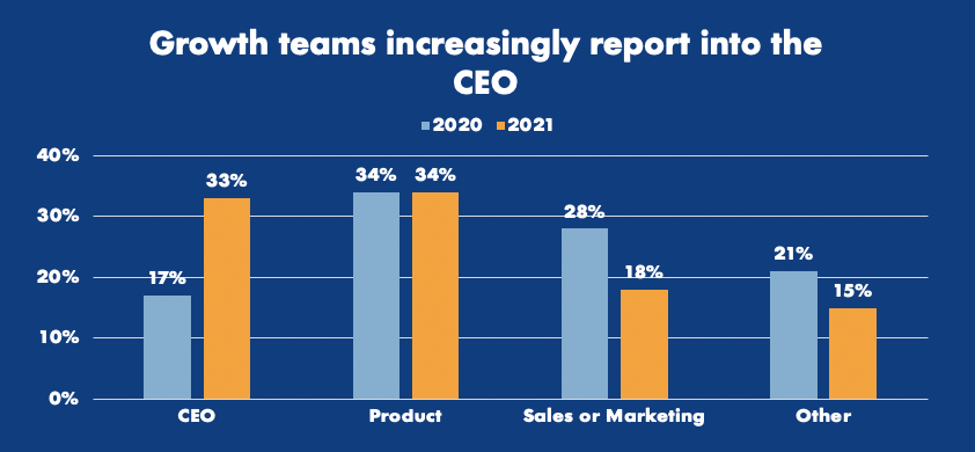

According to responses from product benchmarks surveys, growth teams have transitioned dramatically from reporting to marketing and sales to reporting directly to the CEO.

Some of the early writing on growth teams says that they can be structured individually as their own standalone team or as a SWAT model, where experts from various other departments in the organization converge on a regular cadence to solve for growth.

Image Credits: OpenView Partners

My experience, and the data I’ve collected from business-user focused software companies, has led me to the conclusion that growth teams in business software should not be structured as “SWAT” teams, with cross-functional leadership coming together to think critically about growth problems facing the business. I find that if problems don’t have a real owner, they’re not going to get solved. Growth issues are no different and are often deprioritized unless it’s someone’s job to think about them.

Becoming product-led isn’t something that happens overnight, and hiring someone will not be a silver bullet for your software.

I put early growth hires into a few simple buckets. You’ve got:

Product-minded growth experts: These folks are all about optimizing the user experience, reducing friction and expanding usage. They’re usually pretty analytical and might have product, data or MarketingOps backgrounds.

Powered by WPeMatico

Every week over the past three and a half years, an average of three CEOs have exited tech companies in the U.S. That tally is higher — in good times and bad — than in any of the other 26 for-profit sectors tracked by executive search firm Challenger, Gray & Christmas. You’d think tech companies should be the paradigm of how to prep for leadership transitions, since they operate in such a constant state of flux.

They’re far from it.

A change of command is one of the most delicate moments in the life cycle of any organization. If mishandled, the transition from one CEO to the next can result in a loss of market valuation, momentum and focus, as well as key personnel, customers and partners. It may even become that turning point when an organization begins to slide toward irrelevance.

With so much at stake, 84% of tech execs agree that succession planning is more important than ever because of today’s fast-changing business environment, according to our new survey of corporate America’s leaders. Seven out of 10 survey respondents agreed that tech companies face more scrutiny than other multinationals during a transition.

84% of tech execs agree that succession planning is more important than ever because of today’s fast-changing business environment.

Yet we found that tech execs appear just as unprepared for C-suite transitions as their peers in other sectors. Three out of five respondents said their companies don’t have a documented plan to handle a leadership change, even though, by that same ratio, they acknowledge that a documented plan is the biggest determinant in seamless transitions.

The findings may not be troubling if these respondents were millennial startup founders, years from leaving their companies. The executives we polled, however, hail from 160 companies that have been in business for a minimum of 15 years — 35 are tech companies, the largest industry cohort in the survey.

The smallest companies have at least 1,500 employees and $500 million in annual revenue, while the largest have head counts of over 500,000 and revenue upward of $100 billion. They have been around long enough to understand — and put into place — risk management and crisis planning, including what happens should their leaders fall victim to the proverbial milk truck.

Tech execs should be more rigorous about succession planning for one important reason: institutional memory. Tech firms generally are younger than other companies of a similar size, which partly explains why the median age of S&P 500 companies plunged to 33 years in 2018 from 85 years in 2000, according to McKinsey & Co.

These enterprises clearly have accomplished a lot in their short lives, but in their haste, most have not captured their history, unlike their longer-lived peers in other sectors. Less than half of these tech firms, in fact, have formally recorded their leader’s story for posterity. That puts them at a disadvantage when, inevitably, they will be required to onboard newcomers to their C-suites.

It’s best to record this history well before the intense swirl of a leadership transition begins. Crucially, it will help the incoming and future generations of leadership understand critical aspects of its track record, the lessons learned, culture and identity. It also explains why the organization has evolved as it has, what binds people together and what may trigger resistance based on previous experience. It’s as much about moving forward as looking back.

Most execs in our poll get it, with 85% saying a company’s history can be a playbook for new executives to learn and prepare for upcoming challenges and opportunities. “History is the mother of innovation for any type of company,” one respondent said. “History,” writes another, “includes the roadmap to failures as well as successes.”

But this documented history cannot be a hagiography of the departing CEO. Too often, outgoing execs spend their last years in office constructing their own trophy cases. Even as they conceded their own flat-footedness on transition planning, the majority of execs said they have already taken steps to create and reinforce their personal legacies — two-thirds said they have already completed their own formal legacy planning, many with the blessing of their boards.

It’s ironic, then, that three out of five also said that the legacy of a CEO or founder often overshadows the skill set and experience a successor brings. Two-thirds of tech execs believed that the longer a leader has been in office, the more it complicates a transition.

Tech leaders can do this right and have done so. Asked which five big-name CEO transitions was most successful, respondents’ No. 1 was Apple’s handoff from Steve Jobs to Tim Cook (38%), followed by Microsoft’s page-turn from Steve Ballmer to Satya Nadella (28%). The others, at General Electric, General Motors and Goldman Sachs, each netted no more than 13% of votes.

Apple’s apparent predominance in this survey might contradict the advice to play down the aggrandizement of an exiting CEO and highlight the compilation and transfer of an organization’s history to the next chief executive. Jobs, after all, painstakingly managed his legacy until the end. But even as he continued to take center-stage, he also made sure to pass along Apple’s institutional knowledge and ethos to Cook over the 13 years they shared space on Apple’s executive floor.

Sooner or later, everyone in the C-suite today — including startup founders — will depart. For the sake of everyone they’ll leave behind, they should begin prepping for that day now.

Powered by WPeMatico